Finance for Managers Report: Financial Reporting and Budgeting

VerifiedAdded on 2020/10/04

|15

|4994

|265

Report

AI Summary

This report provides a comprehensive overview of finance for managers, encompassing critical aspects such as the importance and requirements of maintaining financial records, including their role in monitoring business progress, preparing financial statements, identifying income sources, and facilitating tax return preparation. It analyzes various financial information recording techniques, including manual and electronic methods, day books, and accounts. The report also explores legal and organizational financial reporting requirements, emphasizing their significance for tax compliance, stakeholder information, and internal decision-making. It evaluates the usefulness of financial statements for stakeholders, differentiating between financial and management accounting, and elucidates the budgetary control process, including its advantages and various types. The report's scope also touches upon the evaluation of costing methods for pricing and the application of investment appraisal techniques, making it a valuable resource for understanding financial management principles.

Finance for Managers

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

INTRODUCTION

Finance is the most important part of any business organisation as it is a core requirement

of business. It is important for managers to manage the finance available for business. Managing

finance is an essential aspect as managing finance includes recording, summarizing of business

transactions. This report contains the detailed information about the requirements of keeping

financial records it also analyses various techniques which are used while recording financial

information. This report also explains the usefulness of financial statements to various interested

parties, it explains the difference between financial and management accounting and it also

covers the process of budgetary control. This report also states the evaluation of the uses of

various methods of costing used for pricing purposes. This report also contains the calculation of

variance from budget and actual profit and the various investment appraisal methods.

TASK 1

1.1 Requirements and Purpose for financial records keeping

Financial Records: They are the formal documents which represents the transactions

related to business, individual or any other organisation (Baker and Wurgler, 2013). The records

which are maintained by most business organisation includes the statement of cash flow and

retained earning, revenue statement and tax returns. For a successful business it is essential for a

business to keep their financial records in an organised manner. Following are the various

purpose:

Monitor Business Progress: the main purpose of financial records keeping is to monitor

the progress of its business, it shows a growth of business. These records helps managers

to see that whether their business is growing or not, which items are selling aggressively

in the market. Good records supply a picture which clearly indicates the performance of

its business.

Prepare Financial Statements: keeping good financial records can help company to

prepare good and accurate financial statements which states the financial health of the

company. These financial positions includes the income statements and statements of

financial positions also known as balance sheet (Bull, 2013). It is essential for any

business to store their records of financial transactions which can help companies to

manage their bank or creditors.

1

Finance is the most important part of any business organisation as it is a core requirement

of business. It is important for managers to manage the finance available for business. Managing

finance is an essential aspect as managing finance includes recording, summarizing of business

transactions. This report contains the detailed information about the requirements of keeping

financial records it also analyses various techniques which are used while recording financial

information. This report also explains the usefulness of financial statements to various interested

parties, it explains the difference between financial and management accounting and it also

covers the process of budgetary control. This report also states the evaluation of the uses of

various methods of costing used for pricing purposes. This report also contains the calculation of

variance from budget and actual profit and the various investment appraisal methods.

TASK 1

1.1 Requirements and Purpose for financial records keeping

Financial Records: They are the formal documents which represents the transactions

related to business, individual or any other organisation (Baker and Wurgler, 2013). The records

which are maintained by most business organisation includes the statement of cash flow and

retained earning, revenue statement and tax returns. For a successful business it is essential for a

business to keep their financial records in an organised manner. Following are the various

purpose:

Monitor Business Progress: the main purpose of financial records keeping is to monitor

the progress of its business, it shows a growth of business. These records helps managers

to see that whether their business is growing or not, which items are selling aggressively

in the market. Good records supply a picture which clearly indicates the performance of

its business.

Prepare Financial Statements: keeping good financial records can help company to

prepare good and accurate financial statements which states the financial health of the

company. These financial positions includes the income statements and statements of

financial positions also known as balance sheet (Bull, 2013). It is essential for any

business to store their records of financial transactions which can help companies to

manage their bank or creditors.

1

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Identification of Source of Income: It is essential for business to store its financial

records as one business can generate its revenue from various different sources (Cheng,

Hong and Shue, 2016). These financial records can help companies to keep a track on its

various source through which it can generate the revenue. This information is also needed

to separate business transactions form non business transactions and also to determine the

taxable and non taxable income.

Keeping Track of Deductible Expenses: The second main purpose of storing the

records of financial transaction is to keep a track on it expenses for filling tax return to

claim the deduction. It is important for a business to record their expenses at time when it

occurs so that it dos not forget the expenses at the time while preparing tax return for its

business.

Preparation of Tax Return: Financial records are important for companies while

preparing their tax return. As these financial records shows the various sources which are

used by companies to generate its revenue and all the expenses which a company has

incurred in generating revenue.

Above mentioned are the purpose for which it is essential for companies to store its

financial records. As per the Maltese law and regulations following are the requirements for

keeping its financial records:

As per companies Act of Malta law under chapter 386 it is important for companies to

keep its record of accounting in respect to the following:

a) All sums of money which is expended or receive by the company and a matter in a

respect which companies expenditure and receipts takes place.

b) The liabilities and assets of the company

c) if a company deals in the dealing of goods:

.i Statements which states the stock held by a company at end of every accounting

period.

.ii All the statements which states the stock taking from any such statements of stock

which has to be prepared or has been prepared by the company.

1.2 Analysis of financial information recording techniques

In order to record the financial transaction there are various techniques available some of

the techniques of recording financial information are as follows:

2

records as one business can generate its revenue from various different sources (Cheng,

Hong and Shue, 2016). These financial records can help companies to keep a track on its

various source through which it can generate the revenue. This information is also needed

to separate business transactions form non business transactions and also to determine the

taxable and non taxable income.

Keeping Track of Deductible Expenses: The second main purpose of storing the

records of financial transaction is to keep a track on it expenses for filling tax return to

claim the deduction. It is important for a business to record their expenses at time when it

occurs so that it dos not forget the expenses at the time while preparing tax return for its

business.

Preparation of Tax Return: Financial records are important for companies while

preparing their tax return. As these financial records shows the various sources which are

used by companies to generate its revenue and all the expenses which a company has

incurred in generating revenue.

Above mentioned are the purpose for which it is essential for companies to store its

financial records. As per the Maltese law and regulations following are the requirements for

keeping its financial records:

As per companies Act of Malta law under chapter 386 it is important for companies to

keep its record of accounting in respect to the following:

a) All sums of money which is expended or receive by the company and a matter in a

respect which companies expenditure and receipts takes place.

b) The liabilities and assets of the company

c) if a company deals in the dealing of goods:

.i Statements which states the stock held by a company at end of every accounting

period.

.ii All the statements which states the stock taking from any such statements of stock

which has to be prepared or has been prepared by the company.

1.2 Analysis of financial information recording techniques

In order to record the financial transaction there are various techniques available some of

the techniques of recording financial information are as follows:

2

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Manual Recording: It is a techniques which is used by small business owners in which

financial transactions are recorded by using pen and paper. In this type of technique an

accountant records the daily transaction that what has been sold and for what price it is

sold. Now days this types are techniques are not commonly used (Coles, Lemmon and

Meschke, 2012).

Electronic Recording: Electronic recording is the most commonly used method of

recording financial information. In this type of recording techniques data are recorded by

using electronic means such as computer with the help of various software.

Day Books: In this type of financial information recording technique data are recorded in

a book which includes data, price, quantity and amount. This could be a book in which all

debit entries are recorded on side and credit entries are recorded on the other.

Accounts: in this type of technique for recording financial information an account is

prepared which is a record of financial transactions which includes loss, profit, revenue

and sales. Basically this type of accounting method is done for government, banks and

shareholders.

Petty Cash: Type of financial recording techniques is used in which a some amount of

cash is given on hand for just in case needed for petty things. It is very useful to make

change for various customers and patients.

1.3 Legal and Organisational financial reporting requirements

It is important for a business organisation to record its financial transactions. There are

various legal and organisational requirements which a company needs to follow in a financial

reporting (De Graaf and Stoelhorst, 2013). Following are the various requirements of legal and

organisational for reporting its financial transactions:

Taxes: The main legal requirement for financial reporting is to calculate the tax liability

which is payable by a company. As per the Companies Act of Maltese Law it is

mandatory for a company to keep a record of its financial statements in order to compute

the total tax payable by that organisation.

For other companies, Investors, shareholders etc.: It is important for a company to

keep a record of its financial transactions in order to create financial statements and help

investors to make appropriate decision in investing in the business. As per legal

requirements it is necessary for the businesses to prepare the financial statements for its

3

financial transactions are recorded by using pen and paper. In this type of technique an

accountant records the daily transaction that what has been sold and for what price it is

sold. Now days this types are techniques are not commonly used (Coles, Lemmon and

Meschke, 2012).

Electronic Recording: Electronic recording is the most commonly used method of

recording financial information. In this type of recording techniques data are recorded by

using electronic means such as computer with the help of various software.

Day Books: In this type of financial information recording technique data are recorded in

a book which includes data, price, quantity and amount. This could be a book in which all

debit entries are recorded on side and credit entries are recorded on the other.

Accounts: in this type of technique for recording financial information an account is

prepared which is a record of financial transactions which includes loss, profit, revenue

and sales. Basically this type of accounting method is done for government, banks and

shareholders.

Petty Cash: Type of financial recording techniques is used in which a some amount of

cash is given on hand for just in case needed for petty things. It is very useful to make

change for various customers and patients.

1.3 Legal and Organisational financial reporting requirements

It is important for a business organisation to record its financial transactions. There are

various legal and organisational requirements which a company needs to follow in a financial

reporting (De Graaf and Stoelhorst, 2013). Following are the various requirements of legal and

organisational for reporting its financial transactions:

Taxes: The main legal requirement for financial reporting is to calculate the tax liability

which is payable by a company. As per the Companies Act of Maltese Law it is

mandatory for a company to keep a record of its financial statements in order to compute

the total tax payable by that organisation.

For other companies, Investors, shareholders etc.: It is important for a company to

keep a record of its financial transactions in order to create financial statements and help

investors to make appropriate decision in investing in the business. As per legal

requirements it is necessary for the businesses to prepare the financial statements for its

3

stakeholders. Stakeholders includes government, employees, shareholders and all the

parties who have direct interest in the operations of a business (Dezső and Ross, 2012).

For Internal Decision Making: As per the organisational requirement of keeping

financial reports it is important for a business to maintain a record of its financial

transactions. These financial reports help managers to make effective decision and

identify the problems due to which a company could not perform well in the market. It

also help managers in decision making process as it provides the clear picture of

organisational efficiency to earn revenue.

1.4 Evaluation of the usefulness of financial statements to stakeholders

Financial statements refers to those reports and documents that are developed by the

management department for the company to present the financial information, performance and

position at a point in time. The firm presented this information in context of stakeholder of the

organisation (Christensen and et. al., 2015). Internal and external stakeholders are the two form

of them. Internal stakeholder refers to those who are belong within the organisation like director,

worker, boards of directors etc. Whereas external stakeholders indicates those who are not

directly a part of the organisation like, shareholders, customers, suppliers and others. All the

stakeholders are more conscious to get the information about their investment because financial

statements are beneficial for the business. In context of stakeholders, the usefulness of financial

statements are as following:

For directors and managers it is important so that they can know about new investment

and project appreciation decision.

It is useful for shareholders to make comparison in their investments and benefits with

other companies and industries.

For government, having proper information about financial statements is useful so that

they can gather and collect taxes on due dates from firms.

For having appropriate knowledge about the price information about the products or

goods and services that are producing by the organisation.

For employees, financial statements are useful because with the help of it they can secure

the fairness of the salaries and wages they get from the company according to their

income.

4

parties who have direct interest in the operations of a business (Dezső and Ross, 2012).

For Internal Decision Making: As per the organisational requirement of keeping

financial reports it is important for a business to maintain a record of its financial

transactions. These financial reports help managers to make effective decision and

identify the problems due to which a company could not perform well in the market. It

also help managers in decision making process as it provides the clear picture of

organisational efficiency to earn revenue.

1.4 Evaluation of the usefulness of financial statements to stakeholders

Financial statements refers to those reports and documents that are developed by the

management department for the company to present the financial information, performance and

position at a point in time. The firm presented this information in context of stakeholder of the

organisation (Christensen and et. al., 2015). Internal and external stakeholders are the two form

of them. Internal stakeholder refers to those who are belong within the organisation like director,

worker, boards of directors etc. Whereas external stakeholders indicates those who are not

directly a part of the organisation like, shareholders, customers, suppliers and others. All the

stakeholders are more conscious to get the information about their investment because financial

statements are beneficial for the business. In context of stakeholders, the usefulness of financial

statements are as following:

For directors and managers it is important so that they can know about new investment

and project appreciation decision.

It is useful for shareholders to make comparison in their investments and benefits with

other companies and industries.

For government, having proper information about financial statements is useful so that

they can gather and collect taxes on due dates from firms.

For having appropriate knowledge about the price information about the products or

goods and services that are producing by the organisation.

For employees, financial statements are useful because with the help of it they can secure

the fairness of the salaries and wages they get from the company according to their

income.

4

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

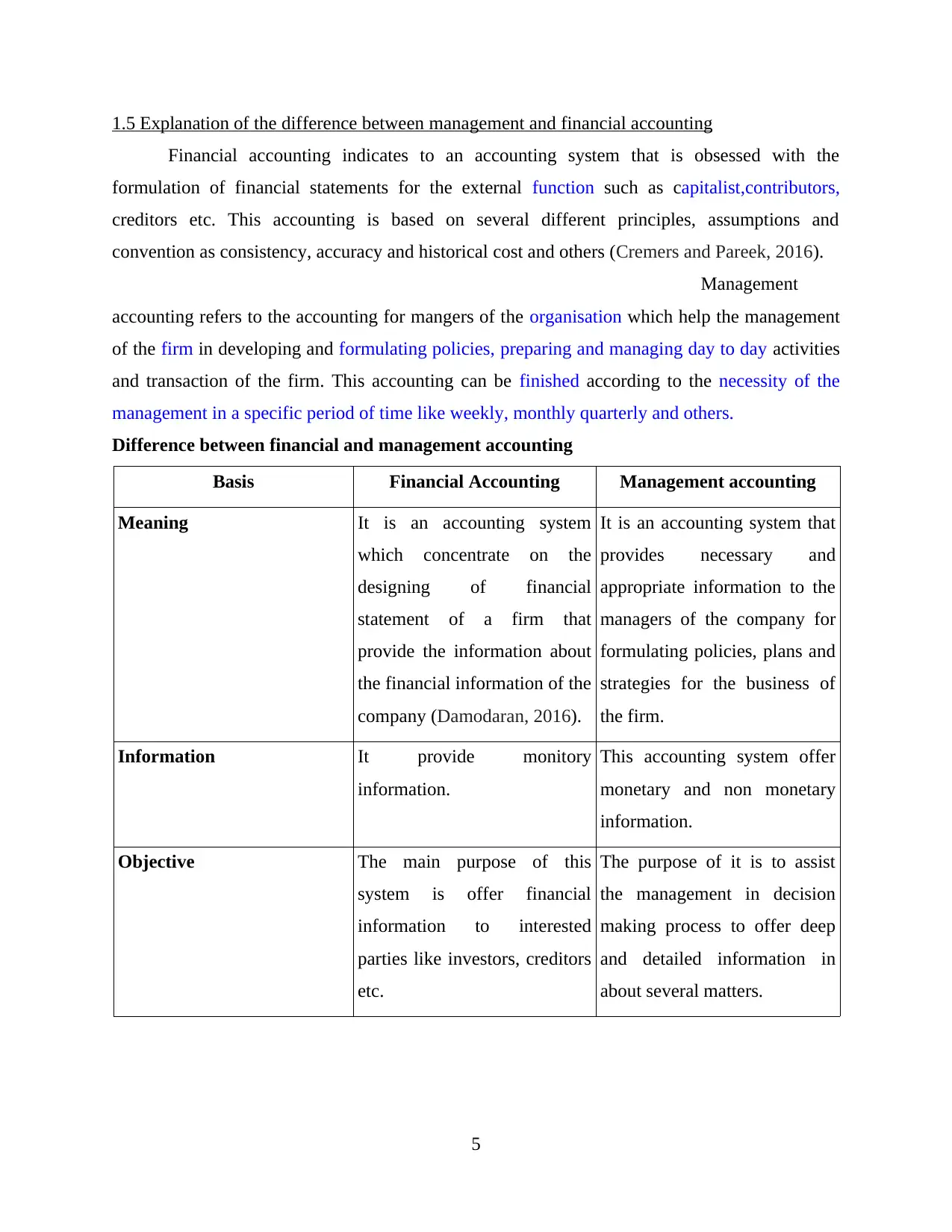

1.5 Explanation of the difference between management and financial accounting

Financial accounting indicates to an accounting system that is obsessed with the

formulation of financial statements for the external function such as capitalist,contributors,

creditors etc. This accounting is based on several different principles, assumptions and

convention as consistency, accuracy and historical cost and others (Cremers and Pareek, 2016).

Management

accounting refers to the accounting for mangers of the organisation which help the management

of the firm in developing and formulating policies, preparing and managing day to day activities

and transaction of the firm. This accounting can be finished according to the necessity of the

management in a specific period of time like weekly, monthly quarterly and others.

Difference between financial and management accounting

Basis Financial Accounting Management accounting

Meaning It is an accounting system

which concentrate on the

designing of financial

statement of a firm that

provide the information about

the financial information of the

company (Damodaran, 2016).

It is an accounting system that

provides necessary and

appropriate information to the

managers of the company for

formulating policies, plans and

strategies for the business of

the firm.

Information It provide monitory

information.

This accounting system offer

monetary and non monetary

information.

Objective The main purpose of this

system is offer financial

information to interested

parties like investors, creditors

etc.

The purpose of it is to assist

the management in decision

making process to offer deep

and detailed information in

about several matters.

5

Financial accounting indicates to an accounting system that is obsessed with the

formulation of financial statements for the external function such as capitalist,contributors,

creditors etc. This accounting is based on several different principles, assumptions and

convention as consistency, accuracy and historical cost and others (Cremers and Pareek, 2016).

Management

accounting refers to the accounting for mangers of the organisation which help the management

of the firm in developing and formulating policies, preparing and managing day to day activities

and transaction of the firm. This accounting can be finished according to the necessity of the

management in a specific period of time like weekly, monthly quarterly and others.

Difference between financial and management accounting

Basis Financial Accounting Management accounting

Meaning It is an accounting system

which concentrate on the

designing of financial

statement of a firm that

provide the information about

the financial information of the

company (Damodaran, 2016).

It is an accounting system that

provides necessary and

appropriate information to the

managers of the company for

formulating policies, plans and

strategies for the business of

the firm.

Information It provide monitory

information.

This accounting system offer

monetary and non monetary

information.

Objective The main purpose of this

system is offer financial

information to interested

parties like investors, creditors

etc.

The purpose of it is to assist

the management in decision

making process to offer deep

and detailed information in

about several matters.

5

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Time frame Financial statements are

equipped at the extremity of

the year usually in a year.

Management reports are

designed as per the

requirements of the company.

1.6 Explanation of the budgetary control process

Budget- It is a tool and technique that utilized by the mangers of the company to make

program and control the use of scarce resources. It refers to a plan that screening the objectives

of the firms that how the management attend to adopt and apply resources to achieve these

objectives.

Budgetary control- It refers to the process of monitoring different actual outcomes with

monetary fund illustration for the organisation for the upcoming time period and standards set

then examining the monetary fund figures with the existent performance for calculating

variances (Fields, 2016). There are various types of budget in business like purchasing budget,

advertising budget, sales monetary fund etc. there are some process for controlling budget are as:

Great coordination and communication between different department of the company can make

control on budget. With the help of it they can make plan and decide effective and efficient ways

for controlling the budget. Budget is important and essential for management because without

budgetary planning, it is hard to run and operate the business of the firm (Hempelmann and

Engelen, 2015). Zero based budgeting and incremental budgeting are some important process of

budgetary control because they help in prediction set overhead costs, computed by adding or

substantiating a planned from the existent reimbursement.

Advantages - It help the management of a company of a commercial enterprise

involvement to demeanor its business operations and actions. It help in creating and generating

suitable conditions for the use of standard costing system in the business of an organisation.

Objective- The major objective of budgetary control is to run and operate different cost

divisions with ratio and economic system

1.7 Evaluation of the use of different costing methods used for pricing purposes

In the business of a company, there are various form of reimbursement but for valuation

purpose business enterprises categorize their costs like direct cost, fixed cost, indirect cost etc.

for pricing motive, there are some essential costs that can be deliberate as marginal cost, price

6

equipped at the extremity of

the year usually in a year.

Management reports are

designed as per the

requirements of the company.

1.6 Explanation of the budgetary control process

Budget- It is a tool and technique that utilized by the mangers of the company to make

program and control the use of scarce resources. It refers to a plan that screening the objectives

of the firms that how the management attend to adopt and apply resources to achieve these

objectives.

Budgetary control- It refers to the process of monitoring different actual outcomes with

monetary fund illustration for the organisation for the upcoming time period and standards set

then examining the monetary fund figures with the existent performance for calculating

variances (Fields, 2016). There are various types of budget in business like purchasing budget,

advertising budget, sales monetary fund etc. there are some process for controlling budget are as:

Great coordination and communication between different department of the company can make

control on budget. With the help of it they can make plan and decide effective and efficient ways

for controlling the budget. Budget is important and essential for management because without

budgetary planning, it is hard to run and operate the business of the firm (Hempelmann and

Engelen, 2015). Zero based budgeting and incremental budgeting are some important process of

budgetary control because they help in prediction set overhead costs, computed by adding or

substantiating a planned from the existent reimbursement.

Advantages - It help the management of a company of a commercial enterprise

involvement to demeanor its business operations and actions. It help in creating and generating

suitable conditions for the use of standard costing system in the business of an organisation.

Objective- The major objective of budgetary control is to run and operate different cost

divisions with ratio and economic system

1.7 Evaluation of the use of different costing methods used for pricing purposes

In the business of a company, there are various form of reimbursement but for valuation

purpose business enterprises categorize their costs like direct cost, fixed cost, indirect cost etc.

for pricing motive, there are some essential costs that can be deliberate as marginal cost, price

6

taker and others. In an organisation, the management have to find out that which declarer is

cashed for the costs obtained and is compensated an united upon percentage of such costs as

contractors profit is known as cost plus. Apart from this a company compute marginal cost

which assign only variable costs like direct labour, direct material and direct expenses to the

manufacture. This kind of cost express the distinction between variable and fixed cost. In a

organisation, there are various investor and most of them are cost takers according to their

actions like selling and buying stocks and it is not enough to make change the price (Lekkakos

and Serrano, 2016). A firm can be regarded as a price taker when the price sets according to the

quantity of the products. A customer is also considered to be cost taker because the buying does

not impact the price of a company which are sets b y the management for its goods and services.

Another important method is break even and it means that the firm is not gaining profit and not

in loss both are adequate after reconciliation the costs.

TASK 2

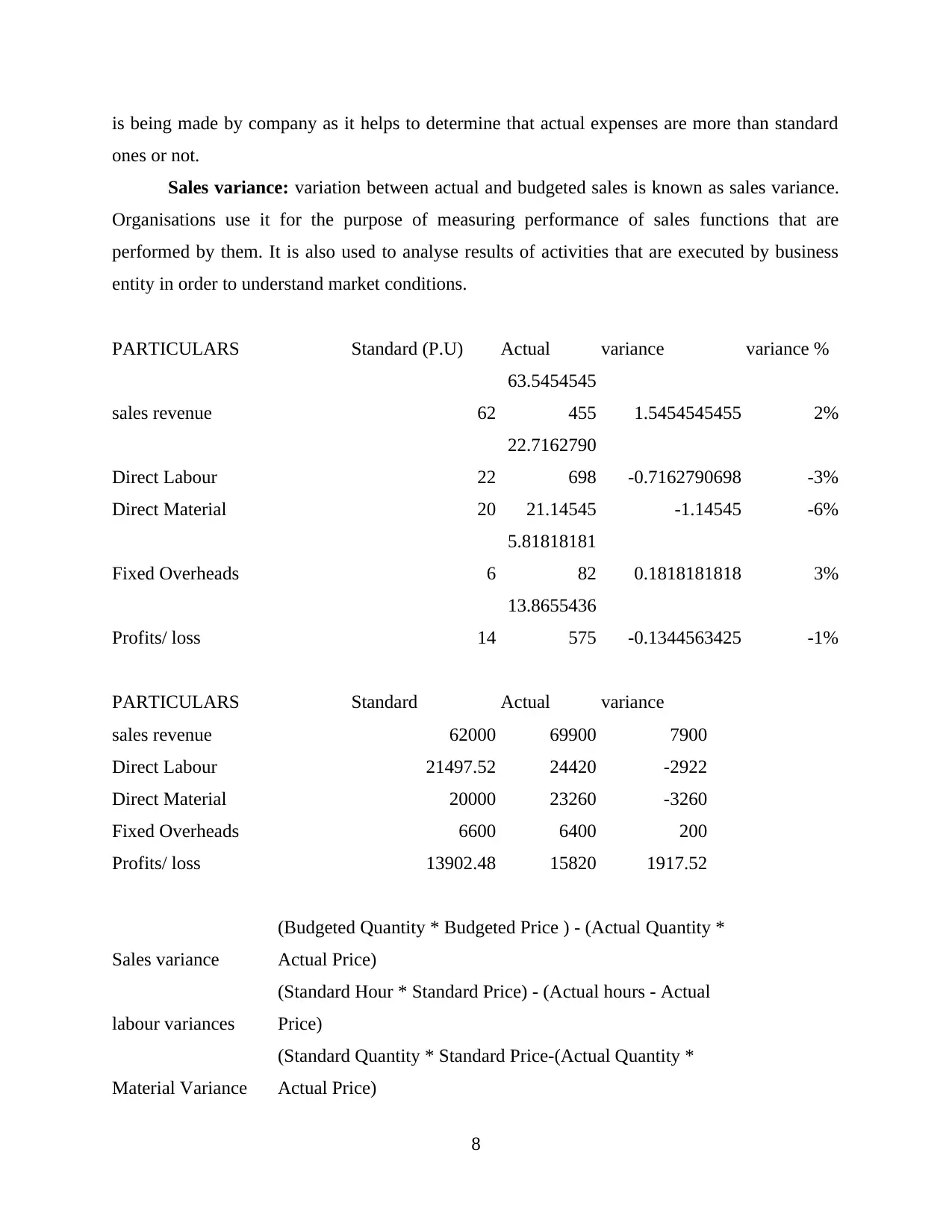

Variance analysis: The model which is used by business entities for the purpose of analysing

difference between actual and budgeted figures is known as variance analysis. It helps internal

stakeholders to determine that organisation is performing well or not. It also helps to evaluate the

ability of company to meet its targets that are set by top managers for the business entity. There

are various types of variances that are calculated by managers of enterprises in order to measure

actual performance of organisation. When budgeted figures are more than actual figures then it is

known as a favourable situation and when actual figures are higher than budget ones then it is

known as adverse situation. All of them are as follows:

Material variance: The process in which difference between actual and budget cost of

material is analysed in known as material variance. With the help of it managers can determine

efficiency of organisation.

Labour variance: The tool which helps to analyse difference between actual and

budgeted labour cost is known as labour variance. It guides top executives to measure

effectiveness of employees who are working within the company.

Overhead variance: The variance which is used for the purpose of analysing difference

between budgeted and actual rates of overheads faced by organisation is known as overhead

variance (Gitman, Juchau and Flanagan, 2015). It helps to analyse overspending of money which

7

cashed for the costs obtained and is compensated an united upon percentage of such costs as

contractors profit is known as cost plus. Apart from this a company compute marginal cost

which assign only variable costs like direct labour, direct material and direct expenses to the

manufacture. This kind of cost express the distinction between variable and fixed cost. In a

organisation, there are various investor and most of them are cost takers according to their

actions like selling and buying stocks and it is not enough to make change the price (Lekkakos

and Serrano, 2016). A firm can be regarded as a price taker when the price sets according to the

quantity of the products. A customer is also considered to be cost taker because the buying does

not impact the price of a company which are sets b y the management for its goods and services.

Another important method is break even and it means that the firm is not gaining profit and not

in loss both are adequate after reconciliation the costs.

TASK 2

Variance analysis: The model which is used by business entities for the purpose of analysing

difference between actual and budgeted figures is known as variance analysis. It helps internal

stakeholders to determine that organisation is performing well or not. It also helps to evaluate the

ability of company to meet its targets that are set by top managers for the business entity. There

are various types of variances that are calculated by managers of enterprises in order to measure

actual performance of organisation. When budgeted figures are more than actual figures then it is

known as a favourable situation and when actual figures are higher than budget ones then it is

known as adverse situation. All of them are as follows:

Material variance: The process in which difference between actual and budget cost of

material is analysed in known as material variance. With the help of it managers can determine

efficiency of organisation.

Labour variance: The tool which helps to analyse difference between actual and

budgeted labour cost is known as labour variance. It guides top executives to measure

effectiveness of employees who are working within the company.

Overhead variance: The variance which is used for the purpose of analysing difference

between budgeted and actual rates of overheads faced by organisation is known as overhead

variance (Gitman, Juchau and Flanagan, 2015). It helps to analyse overspending of money which

7

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

is being made by company as it helps to determine that actual expenses are more than standard

ones or not.

Sales variance: variation between actual and budgeted sales is known as sales variance.

Organisations use it for the purpose of measuring performance of sales functions that are

performed by them. It is also used to analyse results of activities that are executed by business

entity in order to understand market conditions.

PARTICULARS Standard (P.U) Actual variance variance %

sales revenue 62

63.5454545

455 1.5454545455 2%

Direct Labour 22

22.7162790

698 -0.7162790698 -3%

Direct Material 20 21.14545 -1.14545 -6%

Fixed Overheads 6

5.81818181

82 0.1818181818 3%

Profits/ loss 14

13.8655436

575 -0.1344563425 -1%

PARTICULARS Standard Actual variance

sales revenue 62000 69900 7900

Direct Labour 21497.52 24420 -2922

Direct Material 20000 23260 -3260

Fixed Overheads 6600 6400 200

Profits/ loss 13902.48 15820 1917.52

Sales variance

(Budgeted Quantity * Budgeted Price ) - (Actual Quantity *

Actual Price)

labour variances

(Standard Hour * Standard Price) - (Actual hours - Actual

Price)

Material Variance

(Standard Quantity * Standard Price-(Actual Quantity *

Actual Price)

8

ones or not.

Sales variance: variation between actual and budgeted sales is known as sales variance.

Organisations use it for the purpose of measuring performance of sales functions that are

performed by them. It is also used to analyse results of activities that are executed by business

entity in order to understand market conditions.

PARTICULARS Standard (P.U) Actual variance variance %

sales revenue 62

63.5454545

455 1.5454545455 2%

Direct Labour 22

22.7162790

698 -0.7162790698 -3%

Direct Material 20 21.14545 -1.14545 -6%

Fixed Overheads 6

5.81818181

82 0.1818181818 3%

Profits/ loss 14

13.8655436

575 -0.1344563425 -1%

PARTICULARS Standard Actual variance

sales revenue 62000 69900 7900

Direct Labour 21497.52 24420 -2922

Direct Material 20000 23260 -3260

Fixed Overheads 6600 6400 200

Profits/ loss 13902.48 15820 1917.52

Sales variance

(Budgeted Quantity * Budgeted Price ) - (Actual Quantity *

Actual Price)

labour variances

(Standard Hour * Standard Price) - (Actual hours - Actual

Price)

Material Variance

(Standard Quantity * Standard Price-(Actual Quantity *

Actual Price)

8

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Overhead variances (Actual Output * SR) - Actual fixed overhead

Sales variance (1000*62)-(1000*63.54) -1540

labour variances (977.27*22)-(1075*22.71) -2922

Material Variance (1000*20)-(1100*21.14545) -3259.995

Overhead variances (1100*6)-6400 200

Standard hours (1075/1100*1000) 977.17

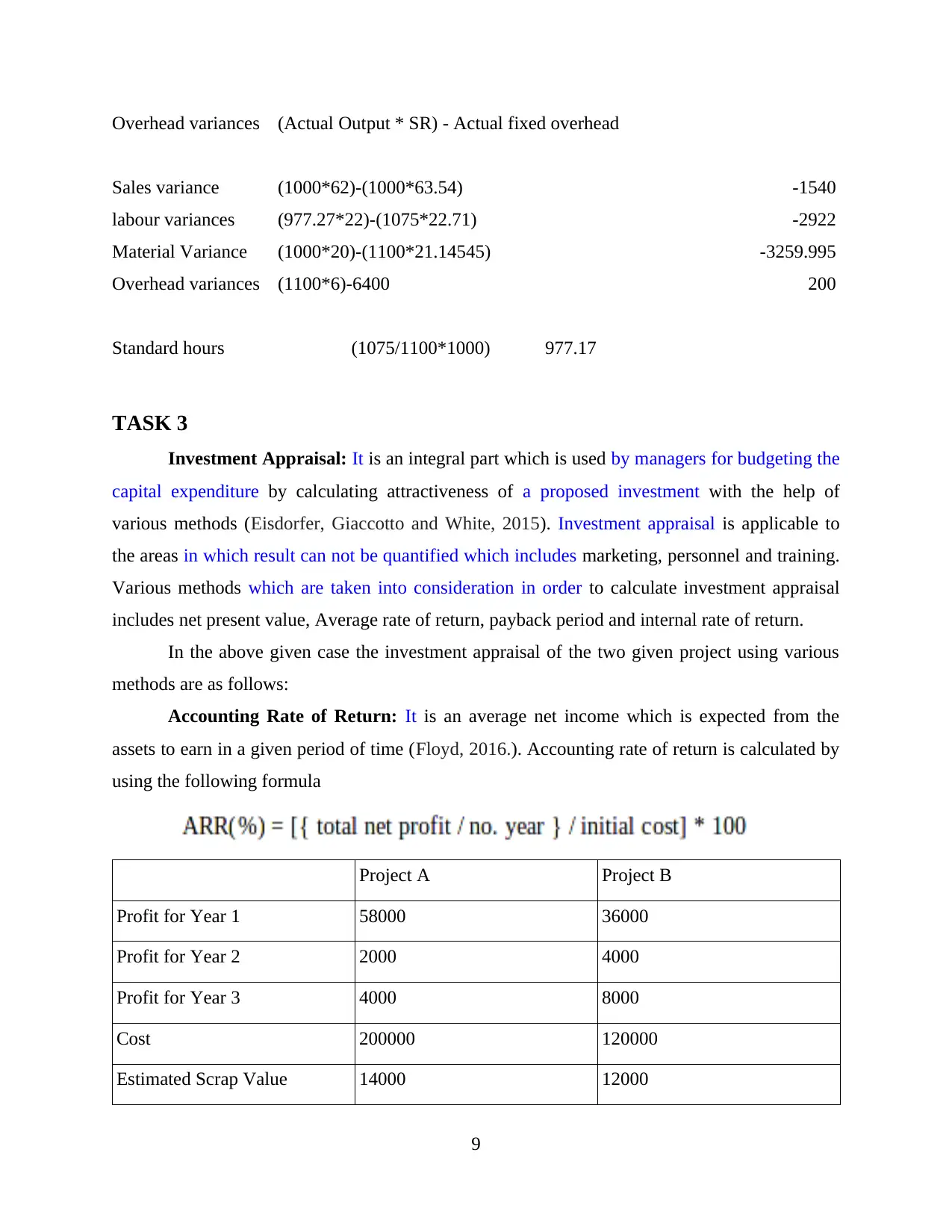

TASK 3

Investment Appraisal: It is an integral part which is used by managers for budgeting the

capital expenditure by calculating attractiveness of a proposed investment with the help of

various methods (Eisdorfer, Giaccotto and White, 2015). Investment appraisal is applicable to

the areas in which result can not be quantified which includes marketing, personnel and training.

Various methods which are taken into consideration in order to calculate investment appraisal

includes net present value, Average rate of return, payback period and internal rate of return.

In the above given case the investment appraisal of the two given project using various

methods are as follows:

Accounting Rate of Return: It is an average net income which is expected from the

assets to earn in a given period of time (Floyd, 2016.). Accounting rate of return is calculated by

using the following formula

Project A Project B

Profit for Year 1 58000 36000

Profit for Year 2 2000 4000

Profit for Year 3 4000 8000

Cost 200000 120000

Estimated Scrap Value 14000 12000

9

Sales variance (1000*62)-(1000*63.54) -1540

labour variances (977.27*22)-(1075*22.71) -2922

Material Variance (1000*20)-(1100*21.14545) -3259.995

Overhead variances (1100*6)-6400 200

Standard hours (1075/1100*1000) 977.17

TASK 3

Investment Appraisal: It is an integral part which is used by managers for budgeting the

capital expenditure by calculating attractiveness of a proposed investment with the help of

various methods (Eisdorfer, Giaccotto and White, 2015). Investment appraisal is applicable to

the areas in which result can not be quantified which includes marketing, personnel and training.

Various methods which are taken into consideration in order to calculate investment appraisal

includes net present value, Average rate of return, payback period and internal rate of return.

In the above given case the investment appraisal of the two given project using various

methods are as follows:

Accounting Rate of Return: It is an average net income which is expected from the

assets to earn in a given period of time (Floyd, 2016.). Accounting rate of return is calculated by

using the following formula

Project A Project B

Profit for Year 1 58000 36000

Profit for Year 2 2000 4000

Profit for Year 3 4000 8000

Cost 200000 120000

Estimated Scrap Value 14000 12000

9

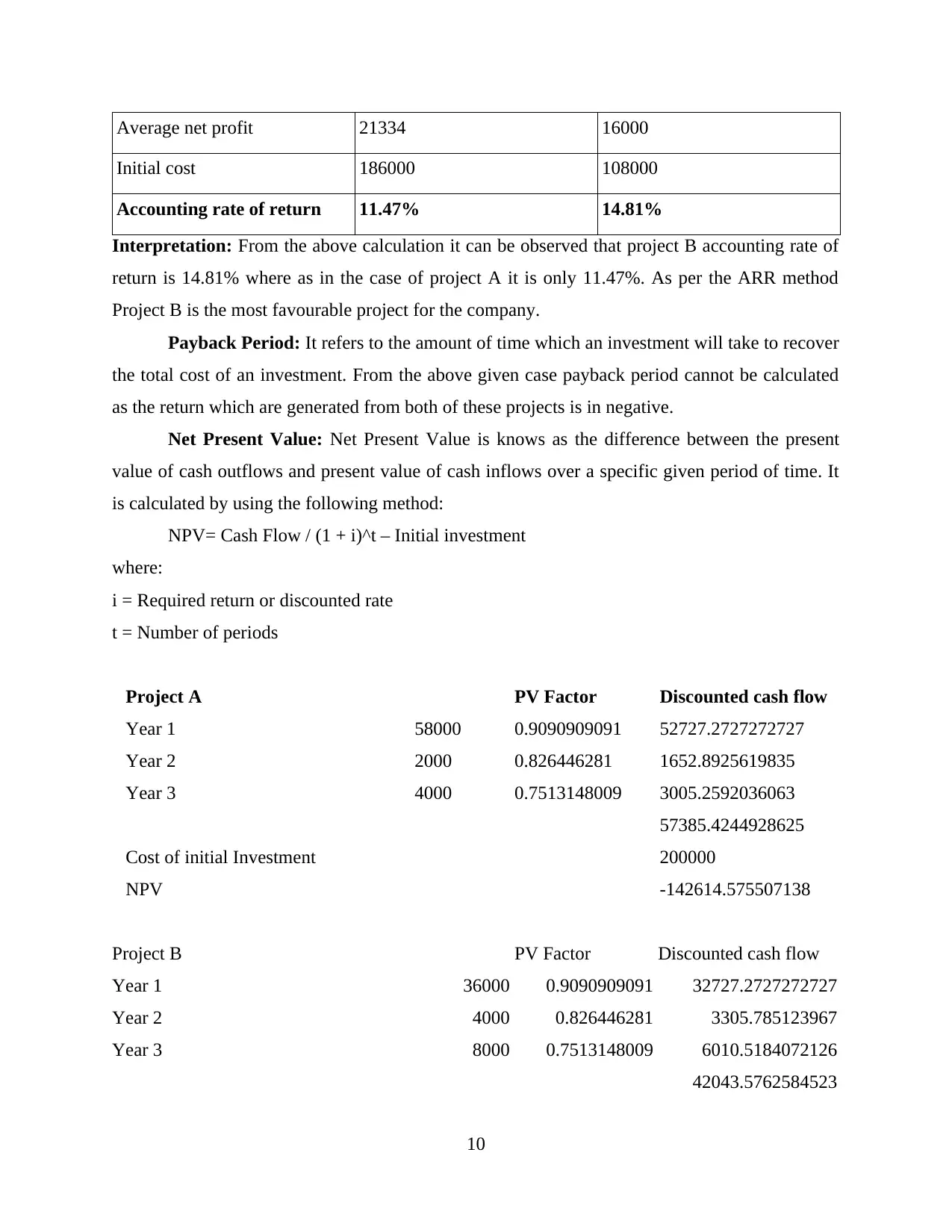

Average net profit 21334 16000

Initial cost 186000 108000

Accounting rate of return 11.47% 14.81%

Interpretation: From the above calculation it can be observed that project B accounting rate of

return is 14.81% where as in the case of project A it is only 11.47%. As per the ARR method

Project B is the most favourable project for the company.

Payback Period: It refers to the amount of time which an investment will take to recover

the total cost of an investment. From the above given case payback period cannot be calculated

as the return which are generated from both of these projects is in negative.

Net Present Value: Net Present Value is knows as the difference between the present

value of cash outflows and present value of cash inflows over a specific given period of time. It

is calculated by using the following method:

NPV= Cash Flow / (1 + i)^t – Initial investment

where:

i = Required return or discounted rate

t = Number of periods

Project A PV Factor Discounted cash flow

Year 1 58000 0.9090909091 52727.2727272727

Year 2 2000 0.826446281 1652.8925619835

Year 3 4000 0.7513148009 3005.2592036063

57385.4244928625

Cost of initial Investment 200000

NPV -142614.575507138

Project B PV Factor Discounted cash flow

Year 1 36000 0.9090909091 32727.2727272727

Year 2 4000 0.826446281 3305.785123967

Year 3 8000 0.7513148009 6010.5184072126

42043.5762584523

10

Initial cost 186000 108000

Accounting rate of return 11.47% 14.81%

Interpretation: From the above calculation it can be observed that project B accounting rate of

return is 14.81% where as in the case of project A it is only 11.47%. As per the ARR method

Project B is the most favourable project for the company.

Payback Period: It refers to the amount of time which an investment will take to recover

the total cost of an investment. From the above given case payback period cannot be calculated

as the return which are generated from both of these projects is in negative.

Net Present Value: Net Present Value is knows as the difference between the present

value of cash outflows and present value of cash inflows over a specific given period of time. It

is calculated by using the following method:

NPV= Cash Flow / (1 + i)^t – Initial investment

where:

i = Required return or discounted rate

t = Number of periods

Project A PV Factor Discounted cash flow

Year 1 58000 0.9090909091 52727.2727272727

Year 2 2000 0.826446281 1652.8925619835

Year 3 4000 0.7513148009 3005.2592036063

57385.4244928625

Cost of initial Investment 200000

NPV -142614.575507138

Project B PV Factor Discounted cash flow

Year 1 36000 0.9090909091 32727.2727272727

Year 2 4000 0.826446281 3305.785123967

Year 3 8000 0.7513148009 6010.5184072126

42043.5762584523

10

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 15

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.