Finance and Mortgage Brooking Management Report: Loan Assessment

VerifiedAdded on 2020/07/22

|35

|13311

|77

Report

AI Summary

This report focuses on finance and mortgage broking management, specifically addressing a loan application scenario for a metal pallet manufacturing business. It details the questions a loan executive should ask potential borrowers, including the purpose of the loan, preferred loan options, repayment capacity, and collateral. The report calculates the debt service ratio for the borrowers, highlighting their current financial liabilities and potential risks associated with the loan. It also outlines the steps involved in the loan application process, from preparing a budget to submitting necessary documentation, and the importance of understanding loan terms and conditions. Finally, the report discusses the risks associated with taking out a loan, such as obsolescence of the machinery and the impact on the company's liquidity and profitability.

Finance and Mortgage

Brooking Management

Brooking Management

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Table of Contents

SECTION 1......................................................................................................................................3

TASK 1(b).......................................................................................................................................3

TASK 2(b).......................................................................................................................................5

TASK 3(b).......................................................................................................................................6

SECTION 2......................................................................................................................................9

TASK 4............................................................................................................................................9

TASK 5..........................................................................................................................................12

TASK 6..........................................................................................................................................15

TASK 7..........................................................................................................................................20

TASK 8..........................................................................................................................................22

TASK 9..........................................................................................................................................26

REFERENCES..............................................................................................................................31

SECTION 1......................................................................................................................................3

TASK 1(b).......................................................................................................................................3

TASK 2(b).......................................................................................................................................5

TASK 3(b).......................................................................................................................................6

SECTION 2......................................................................................................................................9

TASK 4............................................................................................................................................9

TASK 5..........................................................................................................................................12

TASK 6..........................................................................................................................................15

TASK 7..........................................................................................................................................20

TASK 8..........................................................................................................................................22

TASK 9..........................................................................................................................................26

REFERENCES..............................................................................................................................31

SECTION 1

TASK 1(b)

Answer: Ray Murdoch and Steve brown are jointly running a business which is related to

manufacturing metal pallets. They are planning to purchase a sophisticated machine with the help of

technical platform system CNC. It will help them to rapidly fabricate multiple components. As they

require loan assistance with respect to this. As a loan assistance executive there are various

questions that can be asked from Ray and Steve before proving them any suggestion with respect to

the loan. Some questions are stated below:

It is important to understand that for what purpose a person need loan for. It will help in

understanding the basic requirement of loan. Moreover, it will be easy to provide assistance

as well.

There are various loan options that are available in the market it is important to ask the client

that what all option they find suitable for taking loan. It will help to assess that whether they

have earlier taken any loan or not (Turan & Koskija, 2014).

Another question that can be asked is upto what duration they will able to repay that amount.

It is an important question to assess the time duration of the loan and suggest based on it that

whether the client want long term loan or short term loan. Moreover, different loan options

can be extended to Ray and Steve based on it.

One must be aware of paying capacity of the client as well. It helps to assess that whether

the client will be able to payback the loan amount with interest or not.

Moreover, what mortgage are they thinking for in lieu of the loan if loan mortgage is

suggested to them?.

What is the address of the current premises where the company is conducting its operations.

What is the interest rate they are expecting out of the loan? It is an important question as

different sources of loans will be suggested on this basis.

Is their profits are enough to bear the liability of loan where the payment of instalment is

required to be made after a specific period.

What are the income sources of Ray and Steve through the activities they are involved in ?

What is the source of income of the spouse of Steve i.e. Kate's income and whether she is

eligible to become one of the guarantors of the loan?

If the income of Kate will support the high loan burden or not if Ray and Steve become

3

TASK 1(b)

Answer: Ray Murdoch and Steve brown are jointly running a business which is related to

manufacturing metal pallets. They are planning to purchase a sophisticated machine with the help of

technical platform system CNC. It will help them to rapidly fabricate multiple components. As they

require loan assistance with respect to this. As a loan assistance executive there are various

questions that can be asked from Ray and Steve before proving them any suggestion with respect to

the loan. Some questions are stated below:

It is important to understand that for what purpose a person need loan for. It will help in

understanding the basic requirement of loan. Moreover, it will be easy to provide assistance

as well.

There are various loan options that are available in the market it is important to ask the client

that what all option they find suitable for taking loan. It will help to assess that whether they

have earlier taken any loan or not (Turan & Koskija, 2014).

Another question that can be asked is upto what duration they will able to repay that amount.

It is an important question to assess the time duration of the loan and suggest based on it that

whether the client want long term loan or short term loan. Moreover, different loan options

can be extended to Ray and Steve based on it.

One must be aware of paying capacity of the client as well. It helps to assess that whether

the client will be able to payback the loan amount with interest or not.

Moreover, what mortgage are they thinking for in lieu of the loan if loan mortgage is

suggested to them?.

What is the address of the current premises where the company is conducting its operations.

What is the interest rate they are expecting out of the loan? It is an important question as

different sources of loans will be suggested on this basis.

Is their profits are enough to bear the liability of loan where the payment of instalment is

required to be made after a specific period.

What are the income sources of Ray and Steve through the activities they are involved in ?

What is the source of income of the spouse of Steve i.e. Kate's income and whether she is

eligible to become one of the guarantors of the loan?

If the income of Kate will support the high loan burden or not if Ray and Steve become

3

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

defaulters?

There are higher chances if Ray and Steve have any old relationship with the bank. Hence, it

id to be asked that if they have any history of relationship with bank?

Have they ever become the defaulter of the loan in previous years?

If Ray and Steve have any other loan burden apart from the loan they are going to extend

now?

If Ray and Steve will halve surplus income after fulfilling the requirement of instalment of

the bank? It depicts healthy financial life of the parties.

What is the profitability and liquidity state of Ray and Steve in order to understand their

financial ability?

These questions will help in assessing that what kind of loan should be extended to Ray and Steve.

Moreover, considering the answers of all the questions, assistance and suggestions will be provided

based on the same. Further, the loan assistance will help them in choosing one of the best alternative

available so that the purpose of loan can be fulfilled.

Debt service is the requirement where cash is the main requirement to cover the principal and

interest amount of the loan amount for a specific period. It helps in assessing that whether the

company will be able to make the payment in the specific period or not. If the company is not

generating enough profits it means that it will be unable to service one debt.

Total debt service ratio is calculated with the below formula:

(Annual mortgage payments + Property taxes + Other debt payments ) / Gross family income

Based on the given information it can be calculated for Ray and Steve as:

Annual Mortgage payment of Ray =

Home loan = 18000

Annual mortgage payment of Steve =

Home loan = 25200

Car loan = 1350

Creditors = 100000

Total Annual mortgage payment plus debt payment = 144550

Gross family income = 200000

Hence, Debt service ratio = 144550 / 200000 = 0.72

Therefore, Total debt service is 72%.

4

There are higher chances if Ray and Steve have any old relationship with the bank. Hence, it

id to be asked that if they have any history of relationship with bank?

Have they ever become the defaulter of the loan in previous years?

If Ray and Steve have any other loan burden apart from the loan they are going to extend

now?

If Ray and Steve will halve surplus income after fulfilling the requirement of instalment of

the bank? It depicts healthy financial life of the parties.

What is the profitability and liquidity state of Ray and Steve in order to understand their

financial ability?

These questions will help in assessing that what kind of loan should be extended to Ray and Steve.

Moreover, considering the answers of all the questions, assistance and suggestions will be provided

based on the same. Further, the loan assistance will help them in choosing one of the best alternative

available so that the purpose of loan can be fulfilled.

Debt service is the requirement where cash is the main requirement to cover the principal and

interest amount of the loan amount for a specific period. It helps in assessing that whether the

company will be able to make the payment in the specific period or not. If the company is not

generating enough profits it means that it will be unable to service one debt.

Total debt service ratio is calculated with the below formula:

(Annual mortgage payments + Property taxes + Other debt payments ) / Gross family income

Based on the given information it can be calculated for Ray and Steve as:

Annual Mortgage payment of Ray =

Home loan = 18000

Annual mortgage payment of Steve =

Home loan = 25200

Car loan = 1350

Creditors = 100000

Total Annual mortgage payment plus debt payment = 144550

Gross family income = 200000

Hence, Debt service ratio = 144550 / 200000 = 0.72

Therefore, Total debt service is 72%.

4

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Both Ray and Steve are on home loan which shows that they are already under one certain liability

with is required to be paid after a certain period. However, the profits their business have grown in

comparison to that of previous year. It shows that the profits of the enterprise is on increasing phase.

Moreover, the current assets amounting to $245,000 is already present with the organization whose

payment will be received in near future. They also have order of $1 million for next three months

which will help their gross profit margin to grow immensely.

It shows that the financial condition of the company is convincing enough to extend loan and

company will be able to payback loan after the specific period. Further, it reveals that the lender

must be comfortable enough extend the loan based on the financial position reflected by ray and

Steve.

There are various risks that are involved in taking loan with which Ray and Steve must be aware of.

Some of them are mentioned below:

They are taking loan for a machinery which can become obsolete after a specific period.

Further, it requires up gradation after a specific period as well. It shows that making such

huge investment can be risky for Ray and Steve and it may not prove to be fruitful enough

Once the loan is extended by any party, Ray and Steve become liable to pay that amount

even if the entity is not generating any profit. It cannot be shifted to next period and

transferred to the other person as well.

It would be difficult to extend the machinery on lease if it becomes obsolete over a period.

Hence, making such a big investment may become a burden of the enterprise.

It may affect the liquidity of the organization as a huge amount is required to be paid by

them as installant and interest after a specific period each year. Further, it may also affect the

profits as well. Ray and Steve should make this decision only of the situation in the

enterprise is manageable and they will be able to cope up with the burden.

TASK 2(b)

Answer:

5

with is required to be paid after a certain period. However, the profits their business have grown in

comparison to that of previous year. It shows that the profits of the enterprise is on increasing phase.

Moreover, the current assets amounting to $245,000 is already present with the organization whose

payment will be received in near future. They also have order of $1 million for next three months

which will help their gross profit margin to grow immensely.

It shows that the financial condition of the company is convincing enough to extend loan and

company will be able to payback loan after the specific period. Further, it reveals that the lender

must be comfortable enough extend the loan based on the financial position reflected by ray and

Steve.

There are various risks that are involved in taking loan with which Ray and Steve must be aware of.

Some of them are mentioned below:

They are taking loan for a machinery which can become obsolete after a specific period.

Further, it requires up gradation after a specific period as well. It shows that making such

huge investment can be risky for Ray and Steve and it may not prove to be fruitful enough

Once the loan is extended by any party, Ray and Steve become liable to pay that amount

even if the entity is not generating any profit. It cannot be shifted to next period and

transferred to the other person as well.

It would be difficult to extend the machinery on lease if it becomes obsolete over a period.

Hence, making such a big investment may become a burden of the enterprise.

It may affect the liquidity of the organization as a huge amount is required to be paid by

them as installant and interest after a specific period each year. Further, it may also affect the

profits as well. Ray and Steve should make this decision only of the situation in the

enterprise is manageable and they will be able to cope up with the burden.

TASK 2(b)

Answer:

5

REPORT

To

Ray and Steve

Date: 6th September, 2017

As you have accepted all the terms and condition laid down by loan assistance executive. There are

few of the points that are required to be communicated to you.

It is important for the managers that they keep themselves updated and find a source whose funding

is advantageous for the company. In the process of loan assignment, there are three parties

which are involved. One in the loan receiver, that is, Ray and Steve under the name of their

trade, Pallets – R – Us Pty Ltd. The second party is the loan agent who is not directly

associated but is playing a key role in loan assistance. The third party is the one who is

extending loan which can be bank, creditor or other financial institution. There is a step by

step process which is to be followed by Ray and Steve while taking loan from bank. The steps

are mentioned below:

Preparing the budget and deciding that for how much amount the loan will be required by Ray and

Steve. Under assumption of loan amount can lead to lack of financing and overestimation can bring

question over credibility of business owner. Hence, the overall amount of loan decided to sanction is

12240000 for the duration of 10 years. Another step is to take assistance from the loan assistant so

that the person can guide that what type of loan will be beneficial for them based on the purpose for

which the loan has been taken.

The loan is extended by the bank in the name of an entity only when enterprise is having sound

financial statement. It gives surety to the bank that they give get their money bank. Therefore,

financial statement are also demanded by the bank before giving loan to any party. Further, loan

amount and percentage of interest is also decided based on the type of loan and prevailing interest

rate of the market as well. For instance the interest rate percentage may be different for car loan,

home loan, education loan etc. An interest rate of 12% have been decided by the bank to extend loan

to Ray and Steve

Bank also assess that whether the reason stated by the enterprise is valid enough. Moreover, the

reason may be good or bad for business loan. Since, Ray and Steve are taking loan for equipment

purpose, it will be considered as a good reason for taking loan. Further, they use credit score to

6

To

Ray and Steve

Date: 6th September, 2017

As you have accepted all the terms and condition laid down by loan assistance executive. There are

few of the points that are required to be communicated to you.

It is important for the managers that they keep themselves updated and find a source whose funding

is advantageous for the company. In the process of loan assignment, there are three parties

which are involved. One in the loan receiver, that is, Ray and Steve under the name of their

trade, Pallets – R – Us Pty Ltd. The second party is the loan agent who is not directly

associated but is playing a key role in loan assistance. The third party is the one who is

extending loan which can be bank, creditor or other financial institution. There is a step by

step process which is to be followed by Ray and Steve while taking loan from bank. The steps

are mentioned below:

Preparing the budget and deciding that for how much amount the loan will be required by Ray and

Steve. Under assumption of loan amount can lead to lack of financing and overestimation can bring

question over credibility of business owner. Hence, the overall amount of loan decided to sanction is

12240000 for the duration of 10 years. Another step is to take assistance from the loan assistant so

that the person can guide that what type of loan will be beneficial for them based on the purpose for

which the loan has been taken.

The loan is extended by the bank in the name of an entity only when enterprise is having sound

financial statement. It gives surety to the bank that they give get their money bank. Therefore,

financial statement are also demanded by the bank before giving loan to any party. Further, loan

amount and percentage of interest is also decided based on the type of loan and prevailing interest

rate of the market as well. For instance the interest rate percentage may be different for car loan,

home loan, education loan etc. An interest rate of 12% have been decided by the bank to extend loan

to Ray and Steve

Bank also assess that whether the reason stated by the enterprise is valid enough. Moreover, the

reason may be good or bad for business loan. Since, Ray and Steve are taking loan for equipment

purpose, it will be considered as a good reason for taking loan. Further, they use credit score to

6

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

judge the reliability on the owners of the business. Based on which, high credit score id given to

Ray and Steve for credit

Understanding the loan in appropriate manner is an important task that is required to be performed

by Ray and Steve before getting the loan sanctioned. It will help to decide whether they want to take

loan from the bank or not.Moreover, the agent also discusses other sources of finance that can be

opted by the entity.

Ray and Steve must also have a mortgage that will be kept in the lieu of the loan. The mortgage's

value must be equal or more than the amount the company is taking loan for. On the basis of which

the bank decide that whether the loan will be provided to the enterprise or not. Hence, the decided

mortgage by ray and Steve is a building in which they are functioning their business.

The key document while taking loan from the bank which are required to be submitted includes,

personal identification proof which will be of Ray and Steve in this case, income details of the entity

which they are running, credit and debit card statements, rental receipts, guarantor affidavit etc. It

will help the bank to assess that whether the person and enterprise is authentic enough (Campbell,

2012). Only after getting satisfied with all the documents, a loan document is issued stating that a

loan of a specific amount and duration has been taken by the concerned person. It also addresses, all

the term and condition which have been issued by the bank on that particular loan. It also contains

as annexure where repayment details are mentioned including installment period and amount as well

This loan document is required to be sighed by the concerned person whose copy remains with the

individual or the entity and the original document is sent to the bank for further process. The final

loan certificate is issued to the company after all formalities which says that a loan amount has been

issued to a concerned party for specified period.

However, it is important for the company to make prudent decision with respect to this. It will help

in assessing that whether the loan will prove to be fruitful or not. Moreover, other options of

financing can also be used where the company can get financing from relatives, family, friends etc.

It can go for the loan whose interest rate is low and formalities are nominal (Woodward & Hall,

2012). Different types of fees are also charged by the bank while issuing loan which includes loan

processing fees, mortgage charges and other fees as well while issuing loan to a borrower.

There are different types of fees that will be charged from the borrower by the bank which includes,

loan assistance fees amounting to $1500, loan charges for $1500, fees of the loan assistance

7

Ray and Steve for credit

Understanding the loan in appropriate manner is an important task that is required to be performed

by Ray and Steve before getting the loan sanctioned. It will help to decide whether they want to take

loan from the bank or not.Moreover, the agent also discusses other sources of finance that can be

opted by the entity.

Ray and Steve must also have a mortgage that will be kept in the lieu of the loan. The mortgage's

value must be equal or more than the amount the company is taking loan for. On the basis of which

the bank decide that whether the loan will be provided to the enterprise or not. Hence, the decided

mortgage by ray and Steve is a building in which they are functioning their business.

The key document while taking loan from the bank which are required to be submitted includes,

personal identification proof which will be of Ray and Steve in this case, income details of the entity

which they are running, credit and debit card statements, rental receipts, guarantor affidavit etc. It

will help the bank to assess that whether the person and enterprise is authentic enough (Campbell,

2012). Only after getting satisfied with all the documents, a loan document is issued stating that a

loan of a specific amount and duration has been taken by the concerned person. It also addresses, all

the term and condition which have been issued by the bank on that particular loan. It also contains

as annexure where repayment details are mentioned including installment period and amount as well

This loan document is required to be sighed by the concerned person whose copy remains with the

individual or the entity and the original document is sent to the bank for further process. The final

loan certificate is issued to the company after all formalities which says that a loan amount has been

issued to a concerned party for specified period.

However, it is important for the company to make prudent decision with respect to this. It will help

in assessing that whether the loan will prove to be fruitful or not. Moreover, other options of

financing can also be used where the company can get financing from relatives, family, friends etc.

It can go for the loan whose interest rate is low and formalities are nominal (Woodward & Hall,

2012). Different types of fees are also charged by the bank while issuing loan which includes loan

processing fees, mortgage charges and other fees as well while issuing loan to a borrower.

There are different types of fees that will be charged from the borrower by the bank which includes,

loan assistance fees amounting to $1500, loan charges for $1500, fees of the loan assistance

7

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

executive, $2000, Preparation of loan papers, i.e. $1000 and mortgage fees amounting to $2000.

TASK 3(b)

Answer here: The loan can be taken by Ray and Steve from the bank where the prevailing interest

rate id 12%. It is planning to take loan for the duration of 10 years. There are various assumptions

that have been taken into consideration while calculating serviceability of the entity. Some of them

are mentioned below:

It does not take into account any fees which is related to loan.

There is no change in the interest rate over the period of the loan

Loan from the bank is issued at the rate of 12% where interest is calculated based on

compounding the same repayment frequency.

It has been assumed that there are 26 fortnights, 52 weeks and 364 days in a year.

No rounding offs the figures to the near decimal place.

The loan has been taken for 10 years

Based on the above assumptions it can be analysed that the loan amount will be calculated based on

the expenses required to be made by the entity or Ray and Steve. These expenses include, credit

card bills, car loan repayment, salary of Ray and Steve etc.

Total debt service ratio is calculated with the below formula:

(Annual mortgage payments + Property taxes + Other debt payments ) / Gross family income

Total Annual mortgage payment plus debt payment = 144550

Gross family income = 200000

Hence, Debt service ratio = 144550 / 200000 = 0.72

Therefore, Total debt service is 72%.

Based on the above figures the calculated serviceability is as under:

Monthly repayment: $17,560.84

Fortnightly repayment: $8,105

8

TASK 3(b)

Answer here: The loan can be taken by Ray and Steve from the bank where the prevailing interest

rate id 12%. It is planning to take loan for the duration of 10 years. There are various assumptions

that have been taken into consideration while calculating serviceability of the entity. Some of them

are mentioned below:

It does not take into account any fees which is related to loan.

There is no change in the interest rate over the period of the loan

Loan from the bank is issued at the rate of 12% where interest is calculated based on

compounding the same repayment frequency.

It has been assumed that there are 26 fortnights, 52 weeks and 364 days in a year.

No rounding offs the figures to the near decimal place.

The loan has been taken for 10 years

Based on the above assumptions it can be analysed that the loan amount will be calculated based on

the expenses required to be made by the entity or Ray and Steve. These expenses include, credit

card bills, car loan repayment, salary of Ray and Steve etc.

Total debt service ratio is calculated with the below formula:

(Annual mortgage payments + Property taxes + Other debt payments ) / Gross family income

Total Annual mortgage payment plus debt payment = 144550

Gross family income = 200000

Hence, Debt service ratio = 144550 / 200000 = 0.72

Therefore, Total debt service is 72%.

Based on the above figures the calculated serviceability is as under:

Monthly repayment: $17,560.84

Fortnightly repayment: $8,105

8

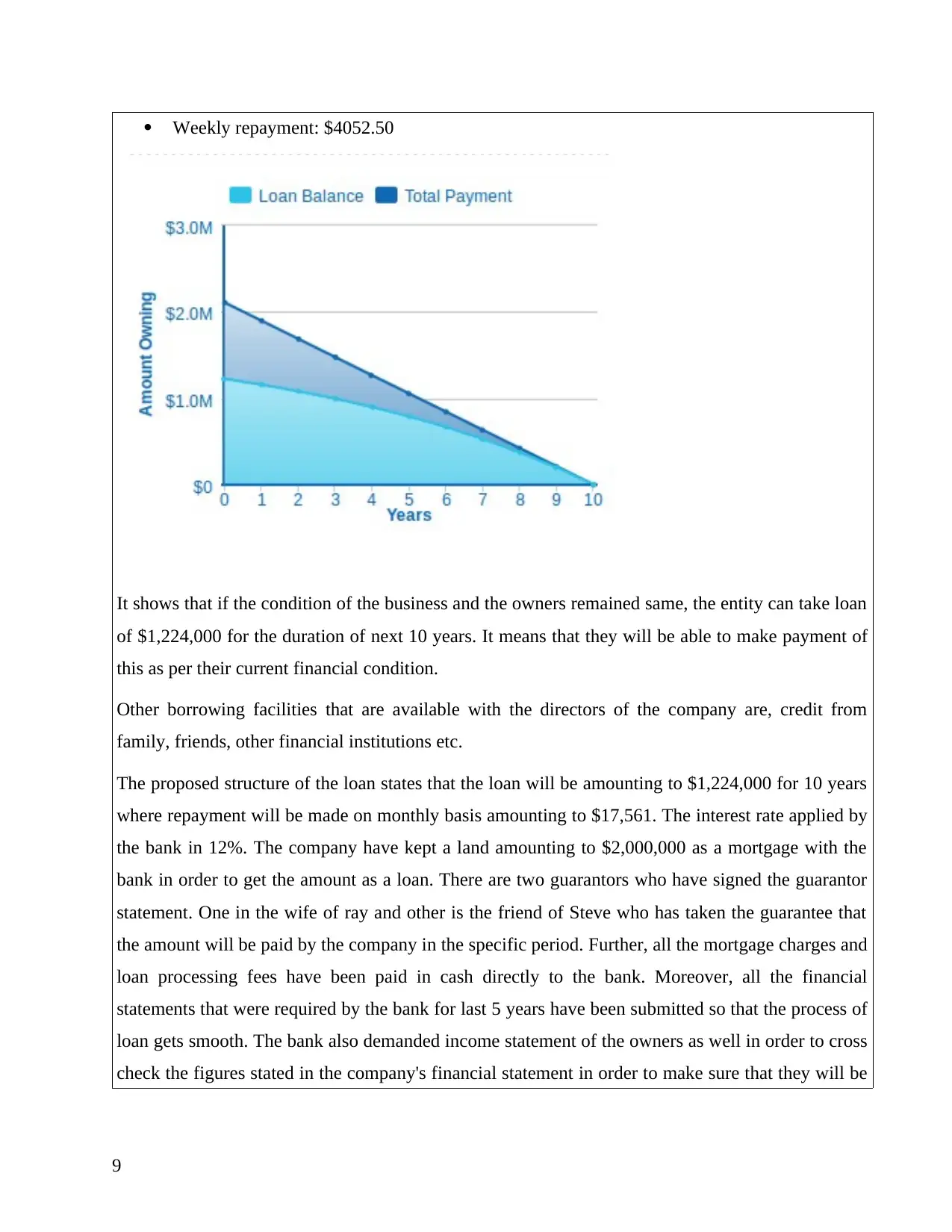

Weekly repayment: $4052.50

It shows that if the condition of the business and the owners remained same, the entity can take loan

of $1,224,000 for the duration of next 10 years. It means that they will be able to make payment of

this as per their current financial condition.

Other borrowing facilities that are available with the directors of the company are, credit from

family, friends, other financial institutions etc.

The proposed structure of the loan states that the loan will be amounting to $1,224,000 for 10 years

where repayment will be made on monthly basis amounting to $17,561. The interest rate applied by

the bank in 12%. The company have kept a land amounting to $2,000,000 as a mortgage with the

bank in order to get the amount as a loan. There are two guarantors who have signed the guarantor

statement. One in the wife of ray and other is the friend of Steve who has taken the guarantee that

the amount will be paid by the company in the specific period. Further, all the mortgage charges and

loan processing fees have been paid in cash directly to the bank. Moreover, all the financial

statements that were required by the bank for last 5 years have been submitted so that the process of

loan gets smooth. The bank also demanded income statement of the owners as well in order to cross

check the figures stated in the company's financial statement in order to make sure that they will be

9

It shows that if the condition of the business and the owners remained same, the entity can take loan

of $1,224,000 for the duration of next 10 years. It means that they will be able to make payment of

this as per their current financial condition.

Other borrowing facilities that are available with the directors of the company are, credit from

family, friends, other financial institutions etc.

The proposed structure of the loan states that the loan will be amounting to $1,224,000 for 10 years

where repayment will be made on monthly basis amounting to $17,561. The interest rate applied by

the bank in 12%. The company have kept a land amounting to $2,000,000 as a mortgage with the

bank in order to get the amount as a loan. There are two guarantors who have signed the guarantor

statement. One in the wife of ray and other is the friend of Steve who has taken the guarantee that

the amount will be paid by the company in the specific period. Further, all the mortgage charges and

loan processing fees have been paid in cash directly to the bank. Moreover, all the financial

statements that were required by the bank for last 5 years have been submitted so that the process of

loan gets smooth. The bank also demanded income statement of the owners as well in order to cross

check the figures stated in the company's financial statement in order to make sure that they will be

9

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

able to get their amount bank after specific duration (Agarwal, Chang & Yavas, 2012).

A person involved in loan assistance have various responsibilities. One of the major concern is to

provide appropriate credit assistance with respect to credit contracts. Further, the aim is to provide

better information to the customers and preventing them from contracts which are unsuitable. A

preliminary assessment of every contract must be made so that effective contracts reach to the end

customer which helps in disclosing authentic information to them. All the information in relation

with the documents must also be disclosed and should find whether it is appropriate or not. As per

the rules, unsuitable information and incorrect facts must not be presented. Not following these rules

may leave the credit assistant into illegal boundaries where he would have to pay 2000 penalty units

as per civil penalty issued by the Australian government. All the information provided must be in

writing any not verbally. Further, all the rules and regulation with respect to credit assistance must

be duly complied with.

The maximum loan amount is decided based on the serviceability calculation which was $1,224,000

in the present case of Ray and Steve. More than this amount can not be extended by the bank to the

borrower. It shows that based on the profits, the company will be able to make payment for this

specific amount in the years for which the loan has been taken. It assures the bank as well that they

will be able to get the amount back in the specific period for which the loan has been issued. The

term of the loan is decided by the company itself based on the payment capacity and belief that they

will be able to pay the amount to the bank.

As per the specifications of Australian tax Office (ATO), the loan taken by Ray and Steve is Trade

Support Loans (TSL) where eligible apprentices are offered loan whose payment is administered by

Australian Apprenticeships Centres and Department of Education and training. Hence, all the rules

and regulation issued by the concerned department is required to be followed while providing credit

assistance to the entity (Chatterjee & Eyigungor, 2015).

NCCP Act 2009 all the reasonable enquiries must be made by the loan assistance executive which

can affect the repayment of loan. Moreover, preliminary assessment of the borrower is also

important to ensure that loan has not been taken to fulfil illegal purposes.

As per the guidelines of Australian Tax Office(ATO), it is also important to assess that how much

tax has been paid by the borrower in last 3 years in order to ensure its financial abilities. As per

10

A person involved in loan assistance have various responsibilities. One of the major concern is to

provide appropriate credit assistance with respect to credit contracts. Further, the aim is to provide

better information to the customers and preventing them from contracts which are unsuitable. A

preliminary assessment of every contract must be made so that effective contracts reach to the end

customer which helps in disclosing authentic information to them. All the information in relation

with the documents must also be disclosed and should find whether it is appropriate or not. As per

the rules, unsuitable information and incorrect facts must not be presented. Not following these rules

may leave the credit assistant into illegal boundaries where he would have to pay 2000 penalty units

as per civil penalty issued by the Australian government. All the information provided must be in

writing any not verbally. Further, all the rules and regulation with respect to credit assistance must

be duly complied with.

The maximum loan amount is decided based on the serviceability calculation which was $1,224,000

in the present case of Ray and Steve. More than this amount can not be extended by the bank to the

borrower. It shows that based on the profits, the company will be able to make payment for this

specific amount in the years for which the loan has been taken. It assures the bank as well that they

will be able to get the amount back in the specific period for which the loan has been issued. The

term of the loan is decided by the company itself based on the payment capacity and belief that they

will be able to pay the amount to the bank.

As per the specifications of Australian tax Office (ATO), the loan taken by Ray and Steve is Trade

Support Loans (TSL) where eligible apprentices are offered loan whose payment is administered by

Australian Apprenticeships Centres and Department of Education and training. Hence, all the rules

and regulation issued by the concerned department is required to be followed while providing credit

assistance to the entity (Chatterjee & Eyigungor, 2015).

NCCP Act 2009 all the reasonable enquiries must be made by the loan assistance executive which

can affect the repayment of loan. Moreover, preliminary assessment of the borrower is also

important to ensure that loan has not been taken to fulfil illegal purposes.

As per the guidelines of Australian Tax Office(ATO), it is also important to assess that how much

tax has been paid by the borrower in last 3 years in order to ensure its financial abilities. As per

10

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Office of State Revenue (OSR) mortgage can be calculated based on the calculator issued by the

authorities. Moreover, it also essential to calculate interest rates ans amount as well. It is also to

ensure that the borrower can not take another loan on the property that has been kept as a mortgage

with the bank on the current loan.

To

The director

Below are the important details that are required to known about the borrowers of the loan:

The borrowers are Ray and Steve

Address of Ray is Unit 43, 25 High St Northville, Australia and has lived there for six years

and address of Steve is 23 Desmond Lane Northville, Australia and has lived there with Kate

for seven years. They own property jointly.

Home Phone numbers are, 9001 2121 and 9002 1212

The purpose of loan is to buy an equipment

The amount to be sanctioned from the bank is 1,224,000.

They have kept their building in which they conduct the business as a mortgage which

situated at, Unit 54, 69 High St Northville, Australia

The security kept is amounting to 1,400,000

The borrowers are self employed business owners.

The loan will be repaid in 10 years with equal instalments every year. Based on the servicing

calculations, it can be assessed that repayment criteria should be as Monthly repayment:

$17,560.84, Fortnightly repayment: $8,105, Weekly repayment: $4052.50.

It is recommended that all the required documents are collected within time and keep a track

of al the repayments and interest payments made by the borrowers.

11

authorities. Moreover, it also essential to calculate interest rates ans amount as well. It is also to

ensure that the borrower can not take another loan on the property that has been kept as a mortgage

with the bank on the current loan.

To

The director

Below are the important details that are required to known about the borrowers of the loan:

The borrowers are Ray and Steve

Address of Ray is Unit 43, 25 High St Northville, Australia and has lived there for six years

and address of Steve is 23 Desmond Lane Northville, Australia and has lived there with Kate

for seven years. They own property jointly.

Home Phone numbers are, 9001 2121 and 9002 1212

The purpose of loan is to buy an equipment

The amount to be sanctioned from the bank is 1,224,000.

They have kept their building in which they conduct the business as a mortgage which

situated at, Unit 54, 69 High St Northville, Australia

The security kept is amounting to 1,400,000

The borrowers are self employed business owners.

The loan will be repaid in 10 years with equal instalments every year. Based on the servicing

calculations, it can be assessed that repayment criteria should be as Monthly repayment:

$17,560.84, Fortnightly repayment: $8,105, Weekly repayment: $4052.50.

It is recommended that all the required documents are collected within time and keep a track

of al the repayments and interest payments made by the borrowers.

11

SECTION 2

TASK 4

Answer: There are various policies and procedures that are followed by the CCF and MB. It

includes legislative, regulatory and professional code of practice. It has a greater impact on

developing and nurturing relationships (Demiroglu & James, 2012). All customers coming to the

organization are treated as same and are handled in such way that they visit to the entity again and

again. Suitable employees are issued in order to handle certain kind of clients at the workplace in

order to rise the satisfaction level of the customers. A building relationship is established with the

other agents as well (Hilber & Turner, 2014). It does not hold any license however, operates as a

credit representative of Australian Aggregator. Based on which the company have been able to build

a loan book of approximately $1.2 billion and an average over $120 million new loans are issued

annually.

The activities that are conducted by the organization are ethical enough as its mission statement says

that they act professionally considering all the rules and regulations issued by the Australian

government (Krainer & Laderman, 2014). The main values that are followed by CCF and MB

includes, that they act with honesty and integrity at all times when they deal with the client or at the

workplace with their teammates as well. They provide unbiased advise to their clients while

conducting their business so that the interest of the customer and the company is free from any

conflict. They maintain the confidentially of the data that has been provided by the client for which

a particular database is used whose security and firewall policy is strict enough so that none can go

through the data without the permission of head of the company. Moreover, The company also

ensures that all the rules and regulations that are issued by NCCP is followed. Further, make sure

that a track record is maintained where all the policies are re checked after every a certain interval.

Being involved in mortgage industry, it makes sure that all the laws and regulations are followed

that are issued by it in order to fulfil the requirements. It ensures that the client get quality loans and

the loan assistant works as per the interest of the customers. The loan which is beneficial for the

client is given to him and all the information related to it is disclosed without any biasness. It helps

to maintain the client base and ensures that quality loans are provided to the customers (Salleh &

et.al, 2013).

It is important to develop a confidentiality while dealing with the clients, colleagues and other

12

TASK 4

Answer: There are various policies and procedures that are followed by the CCF and MB. It

includes legislative, regulatory and professional code of practice. It has a greater impact on

developing and nurturing relationships (Demiroglu & James, 2012). All customers coming to the

organization are treated as same and are handled in such way that they visit to the entity again and

again. Suitable employees are issued in order to handle certain kind of clients at the workplace in

order to rise the satisfaction level of the customers. A building relationship is established with the

other agents as well (Hilber & Turner, 2014). It does not hold any license however, operates as a

credit representative of Australian Aggregator. Based on which the company have been able to build

a loan book of approximately $1.2 billion and an average over $120 million new loans are issued

annually.

The activities that are conducted by the organization are ethical enough as its mission statement says

that they act professionally considering all the rules and regulations issued by the Australian

government (Krainer & Laderman, 2014). The main values that are followed by CCF and MB

includes, that they act with honesty and integrity at all times when they deal with the client or at the

workplace with their teammates as well. They provide unbiased advise to their clients while

conducting their business so that the interest of the customer and the company is free from any

conflict. They maintain the confidentially of the data that has been provided by the client for which

a particular database is used whose security and firewall policy is strict enough so that none can go

through the data without the permission of head of the company. Moreover, The company also

ensures that all the rules and regulations that are issued by NCCP is followed. Further, make sure

that a track record is maintained where all the policies are re checked after every a certain interval.

Being involved in mortgage industry, it makes sure that all the laws and regulations are followed

that are issued by it in order to fulfil the requirements. It ensures that the client get quality loans and

the loan assistant works as per the interest of the customers. The loan which is beneficial for the

client is given to him and all the information related to it is disclosed without any biasness. It helps

to maintain the client base and ensures that quality loans are provided to the customers (Salleh &

et.al, 2013).

It is important to develop a confidentiality while dealing with the clients, colleagues and other

12

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 35

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.