Management Accounting Report: Analysis for Mittelstand Business

VerifiedAdded on 2020/07/23

|18

|4999

|33

Report

AI Summary

This report provides a detailed analysis of management accounting principles and their application within Mittelstand businesses. It begins with an introduction to management accounting and its significance, differentiating it from financial accounting. The report then explores various methods crucial for management accounting, including budgeting, marginal costing, and ratio analysis. It critically evaluates the benefits of a management accounting system, such as budgeting control, marginal costing, standard costing, and ratio analysis. The report delves into specific techniques like absorption and marginal costing, comparing their approaches and highlighting their respective advantages. Furthermore, it examines methods to prevent financial problems within Mittelstand businesses, offering practical insights for improved financial management. Overall, the report offers a comprehensive overview of management accounting, providing valuable information for understanding and implementing effective financial strategies.

Management Accounting

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Table of Contents

INTRODUCTION...........................................................................................................................1

SECTION 1......................................................................................................................................1

PART A...........................................................................................................................................1

P1 Management accounting and its essential roles in it..............................................................1

2 Methods that are required for management accounting in the Mittelstand..............................3

3 Critically evaluates the benefits of system of management accounting...................................4

4 (a) Techniques for absorption and marginal costing................................................................5

4 b) Absorbed .............................................................................................................................8

4 c) Profit under absorption and production of reconciled statements of the profit and loss.....8

SECTION 2......................................................................................................................................9

PART A...........................................................................................................................................9

(a) Comparison of management accounting methods.................................................................9

(b) Methods to prevent financial problems which take place in Mittelstand............................12

CONCLUSION..............................................................................................................................13

REFERENCES..............................................................................................................................14

INTRODUCTION...........................................................................................................................1

SECTION 1......................................................................................................................................1

PART A...........................................................................................................................................1

P1 Management accounting and its essential roles in it..............................................................1

2 Methods that are required for management accounting in the Mittelstand..............................3

3 Critically evaluates the benefits of system of management accounting...................................4

4 (a) Techniques for absorption and marginal costing................................................................5

4 b) Absorbed .............................................................................................................................8

4 c) Profit under absorption and production of reconciled statements of the profit and loss.....8

SECTION 2......................................................................................................................................9

PART A...........................................................................................................................................9

(a) Comparison of management accounting methods.................................................................9

(b) Methods to prevent financial problems which take place in Mittelstand............................12

CONCLUSION..............................................................................................................................13

REFERENCES..............................................................................................................................14

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

INTRODUCTION

The organisation can be develop their functions and operations to provide goods and

services to consumers. In this aspect, management accounting play very important role for

ascertain effective functions and operations. In this way, different types of plan undertake such

as short and long term profits (Nuhu, Bala Appuhamilage and Bala Appuhamilage, 2017). With

this regard, present report based on Mittelstand that deals in manufacturing of machinery,

electrical equipments and many other elements. In order to gain insight knowledge of the chosen

business, report covers management accounting system. Moreover, it includes planning tools

which can be used to make effective functions and operations at workplace. In addition to this, it

determines importance of management accounting in respect to make decisions with improve

performances.

SECTION 1

PART A

P1 Management accounting and its essential roles in it.

There are different types of accounting has been taken which assists to grow effective

results in the business unit. They are as follows:

Management accounting: Management accounting includes process in which various reports

prepares to get outcomes on time and accurate information of the statistical and financial system.

Within the Mittelstand, information assists to make short and long term decisions which enhance

profitability results in successful manner. For example, sales report generated through using

management accounting which utilise through different stakeholder in respect to gain knowledge

in systematic way. These type of report typically present the data that are related to the payables,

cash receivable, etc. (Nuhu, Bala Appuhamilage and Bala Appuhamilage, 2017).

Financial accounting: However, financial accounting include a process that develop through

ascertain financial transaction in systematic way. It is produces by financial accounting system

where different types of transaction recorded. It can be summarised in the systematic way which

could be present in well and proper format. For instance, report make for income and

expenditure calculation, balance sheet, etc. (Cullen, Tsamenyi and Gorst, 2013).

Differences between management accounting and financial accounting

1

The organisation can be develop their functions and operations to provide goods and

services to consumers. In this aspect, management accounting play very important role for

ascertain effective functions and operations. In this way, different types of plan undertake such

as short and long term profits (Nuhu, Bala Appuhamilage and Bala Appuhamilage, 2017). With

this regard, present report based on Mittelstand that deals in manufacturing of machinery,

electrical equipments and many other elements. In order to gain insight knowledge of the chosen

business, report covers management accounting system. Moreover, it includes planning tools

which can be used to make effective functions and operations at workplace. In addition to this, it

determines importance of management accounting in respect to make decisions with improve

performances.

SECTION 1

PART A

P1 Management accounting and its essential roles in it.

There are different types of accounting has been taken which assists to grow effective

results in the business unit. They are as follows:

Management accounting: Management accounting includes process in which various reports

prepares to get outcomes on time and accurate information of the statistical and financial system.

Within the Mittelstand, information assists to make short and long term decisions which enhance

profitability results in successful manner. For example, sales report generated through using

management accounting which utilise through different stakeholder in respect to gain knowledge

in systematic way. These type of report typically present the data that are related to the payables,

cash receivable, etc. (Nuhu, Bala Appuhamilage and Bala Appuhamilage, 2017).

Financial accounting: However, financial accounting include a process that develop through

ascertain financial transaction in systematic way. It is produces by financial accounting system

where different types of transaction recorded. It can be summarised in the systematic way which

could be present in well and proper format. For instance, report make for income and

expenditure calculation, balance sheet, etc. (Cullen, Tsamenyi and Gorst, 2013).

Differences between management accounting and financial accounting

1

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

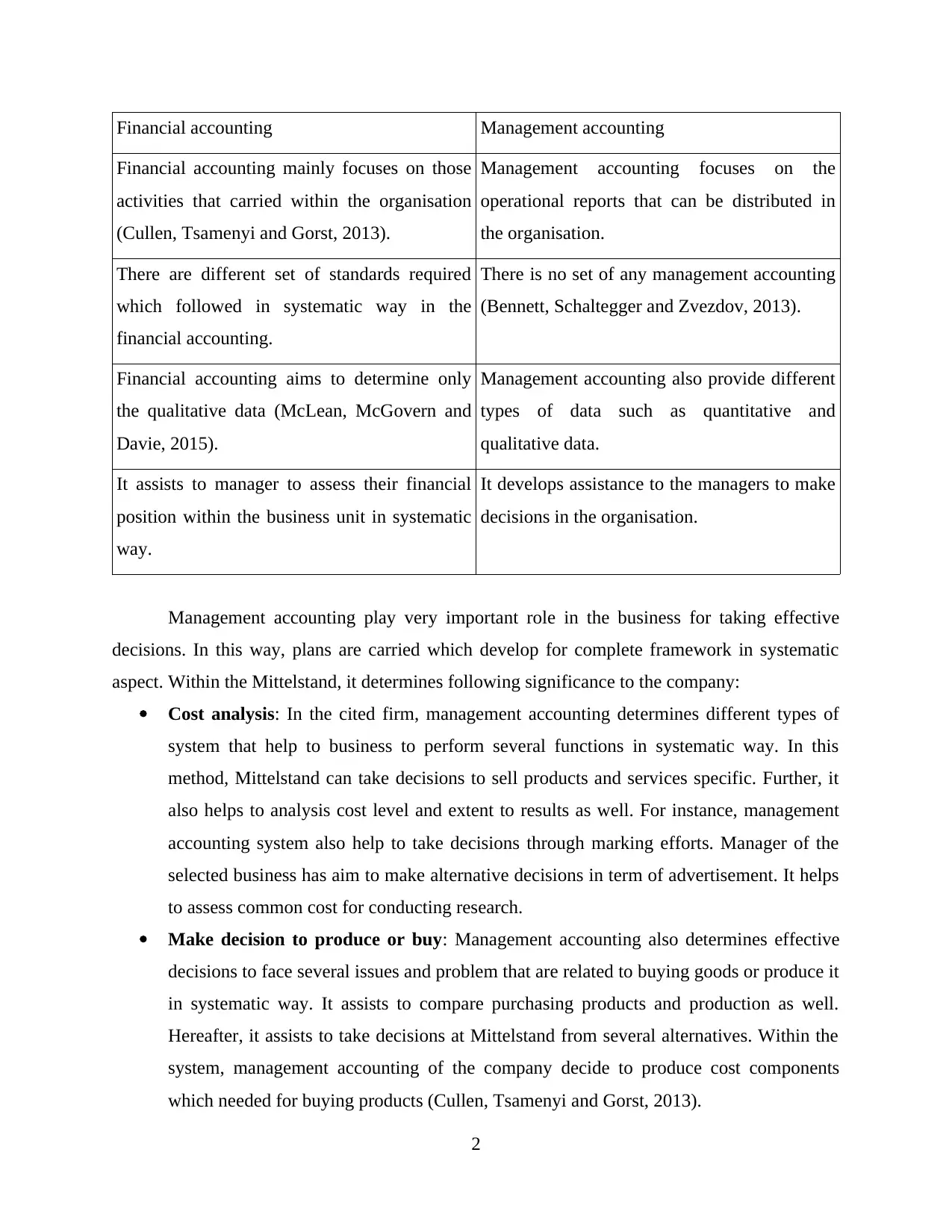

Financial accounting Management accounting

Financial accounting mainly focuses on those

activities that carried within the organisation

(Cullen, Tsamenyi and Gorst, 2013).

Management accounting focuses on the

operational reports that can be distributed in

the organisation.

There are different set of standards required

which followed in systematic way in the

financial accounting.

There is no set of any management accounting

(Bennett, Schaltegger and Zvezdov, 2013).

Financial accounting aims to determine only

the qualitative data (McLean, McGovern and

Davie, 2015).

Management accounting also provide different

types of data such as quantitative and

qualitative data.

It assists to manager to assess their financial

position within the business unit in systematic

way.

It develops assistance to the managers to make

decisions in the organisation.

Management accounting play very important role in the business for taking effective

decisions. In this way, plans are carried which develop for complete framework in systematic

aspect. Within the Mittelstand, it determines following significance to the company:

Cost analysis: In the cited firm, management accounting determines different types of

system that help to business to perform several functions in systematic way. In this

method, Mittelstand can take decisions to sell products and services specific. Further, it

also helps to analysis cost level and extent to results as well. For instance, management

accounting system also help to take decisions through marking efforts. Manager of the

selected business has aim to make alternative decisions in term of advertisement. It helps

to assess common cost for conducting research.

Make decision to produce or buy: Management accounting also determines effective

decisions to face several issues and problem that are related to buying goods or produce it

in systematic way. It assists to compare purchasing products and production as well.

Hereafter, it assists to take decisions at Mittelstand from several alternatives. Within the

system, management accounting of the company decide to produce cost components

which needed for buying products (Cullen, Tsamenyi and Gorst, 2013).

2

Financial accounting mainly focuses on those

activities that carried within the organisation

(Cullen, Tsamenyi and Gorst, 2013).

Management accounting focuses on the

operational reports that can be distributed in

the organisation.

There are different set of standards required

which followed in systematic way in the

financial accounting.

There is no set of any management accounting

(Bennett, Schaltegger and Zvezdov, 2013).

Financial accounting aims to determine only

the qualitative data (McLean, McGovern and

Davie, 2015).

Management accounting also provide different

types of data such as quantitative and

qualitative data.

It assists to manager to assess their financial

position within the business unit in systematic

way.

It develops assistance to the managers to make

decisions in the organisation.

Management accounting play very important role in the business for taking effective

decisions. In this way, plans are carried which develop for complete framework in systematic

aspect. Within the Mittelstand, it determines following significance to the company:

Cost analysis: In the cited firm, management accounting determines different types of

system that help to business to perform several functions in systematic way. In this

method, Mittelstand can take decisions to sell products and services specific. Further, it

also helps to analysis cost level and extent to results as well. For instance, management

accounting system also help to take decisions through marking efforts. Manager of the

selected business has aim to make alternative decisions in term of advertisement. It helps

to assess common cost for conducting research.

Make decision to produce or buy: Management accounting also determines effective

decisions to face several issues and problem that are related to buying goods or produce it

in systematic way. It assists to compare purchasing products and production as well.

Hereafter, it assists to take decisions at Mittelstand from several alternatives. Within the

system, management accounting of the company decide to produce cost components

which needed for buying products (Cullen, Tsamenyi and Gorst, 2013).

2

Data utilization: There are several tools and techniques in the management accounting

such as variance analysis, budget assessment and many more things which need to be

calculated to take decisions for future results (Nuhu, Bala Appuhamilage and Bala

Appuhamilage, 2017). Therefore, employees of Mittelstand take participation for

collecting information. For instance, comparing actual performances and standards with

standards to measure monetary outcomes.

Activity based costing: In this type of technique, the chosen business assess their

activities that are needed to perform several functions and operations (McLean,

McGovern and Davie, 2015). Specific products and services could be enhance in

systematic way through information can be getting about the customer of Mittelstand.

2 Methods that are required for management accounting in the Mittelstand

Management accounting is used to enhance help to small organisation owners to monitor

company activities and performances. In continue monitoring, accounting period needed by the

client to develop effective results and functions. Mittelstand generally depend on the project that

provide effective functioning in business unit (Lapsley and Rekers, 2017). Following are

different types of management accounting system carries in the chosen organisation:

Budget and budgeting: In this aspect, every business has to prepare budget plan through

estimating expenses and income. Within the budget, managers arrange and then allocate fund to

perform several activities (Nuhu, Bala Appuhamilage and Bala Appuhamilage, 2017). It makes

smooth functioning within Mittelstand to produce effective results. It creates direction for

employees to make investment in systematic way. Therefore, budgeting tools and techniques

helps to gain more profits and revenue to make effective framework. In the chosen business unit,

it is highly possible to predict for future to make right direction. Uncertainties also determines

effective influences to make successful budgetary system. As results, it makes positive top

management functions and operations (Chan, Wang and Raffoni, 2014). As results, higher

management fails to determine appropriate amount in each department. Main advantages of this

system is that it efficient allocate the resources which helps to plan the investment. Further, it

also enables to the business management to assess various risk and assess opportunities which

provide a way to capture different types of opportunities (Cullen, Tsamenyi and Gorst, 2013).

For instance, prevention and cure from the different risks. With the help of budgetary-control

system several activities can be control which impact to the planning process. It determines

3

such as variance analysis, budget assessment and many more things which need to be

calculated to take decisions for future results (Nuhu, Bala Appuhamilage and Bala

Appuhamilage, 2017). Therefore, employees of Mittelstand take participation for

collecting information. For instance, comparing actual performances and standards with

standards to measure monetary outcomes.

Activity based costing: In this type of technique, the chosen business assess their

activities that are needed to perform several functions and operations (McLean,

McGovern and Davie, 2015). Specific products and services could be enhance in

systematic way through information can be getting about the customer of Mittelstand.

2 Methods that are required for management accounting in the Mittelstand

Management accounting is used to enhance help to small organisation owners to monitor

company activities and performances. In continue monitoring, accounting period needed by the

client to develop effective results and functions. Mittelstand generally depend on the project that

provide effective functioning in business unit (Lapsley and Rekers, 2017). Following are

different types of management accounting system carries in the chosen organisation:

Budget and budgeting: In this aspect, every business has to prepare budget plan through

estimating expenses and income. Within the budget, managers arrange and then allocate fund to

perform several activities (Nuhu, Bala Appuhamilage and Bala Appuhamilage, 2017). It makes

smooth functioning within Mittelstand to produce effective results. It creates direction for

employees to make investment in systematic way. Therefore, budgeting tools and techniques

helps to gain more profits and revenue to make effective framework. In the chosen business unit,

it is highly possible to predict for future to make right direction. Uncertainties also determines

effective influences to make successful budgetary system. As results, it makes positive top

management functions and operations (Chan, Wang and Raffoni, 2014). As results, higher

management fails to determine appropriate amount in each department. Main advantages of this

system is that it efficient allocate the resources which helps to plan the investment. Further, it

also enables to the business management to assess various risk and assess opportunities which

provide a way to capture different types of opportunities (Cullen, Tsamenyi and Gorst, 2013).

For instance, prevention and cure from the different risks. With the help of budgetary-control

system several activities can be control which impact to the planning process. It determines

3

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

direction that covert resources into the profitable channel. It helps to decentralised authority

without losing the control system. However, it possesses disadvantages which based the

estimation at workplace. This system also consume a lot time to make decisions in systematic

manner (McLean, McGovern and Davie, 2015).

Marginal cost: Marginal cost analysis used in the organisation to assess their pricing

strategy to determine break-even point and assessment of actual profit. In order to determine

break-even analysis in Mittelstand, actual profits and loss easily encounter that assists to make

effective results. With driving of several numbers of units, the chosen organisation can produce

effective functions for desired results (Kokubu and Kitada, 2015). Therefore, marginal costing

provide freedom in the over and under the absorption of overhead. In this way, several

advantages included in the chosen business such as it is the best system which make simple and

easy outcomes to operate effective functions (Van der Stede, 2015). It also assists to the

company to compare their cost in systematic way. It helps to the organisation to take effective

decisions. Therefore, it analysis contribution of the different products that generates more

money. Beside this, it includes the data which related to total cost. It is not providing separate

data which related to fixed and variable costs. This system not includes evaluation of the variable

overhead (Bouten and Hoozée, 2013).

Ratio analysis: This tool helps to the business to asses their performances in effective

manner. It assists to forecast, determine plans and perform so many activities together

Mittelstand. With the help of ratio analysis, information can be getting that generates more

profits and revenue within the selected business. Beside this, liquidity ratio also entails to extent

in which business has enough amount of money through they are able to meet with their current

liabilities and obligations. Ratio analysis also perform in respect to control directly and measure

expenses in the method to use performance analysis (Christ and Burritt, 2017).

3 Critically evaluates the benefits of system of management accounting

In this way, following are such benefits in the management accounting information of the

Mittelstand:

Budgeting control: In this technique, management accounting help to encourage several

people to do their work in systematic way (Bennett, Schaltegger and Zvezdov, 2013). It assists to

accomplish goals and objectives in systematic way at workplace of Mittelstand. Through

performing several activities, the chosen enterprise has opportunity to control their activities

4

without losing the control system. However, it possesses disadvantages which based the

estimation at workplace. This system also consume a lot time to make decisions in systematic

manner (McLean, McGovern and Davie, 2015).

Marginal cost: Marginal cost analysis used in the organisation to assess their pricing

strategy to determine break-even point and assessment of actual profit. In order to determine

break-even analysis in Mittelstand, actual profits and loss easily encounter that assists to make

effective results. With driving of several numbers of units, the chosen organisation can produce

effective functions for desired results (Kokubu and Kitada, 2015). Therefore, marginal costing

provide freedom in the over and under the absorption of overhead. In this way, several

advantages included in the chosen business such as it is the best system which make simple and

easy outcomes to operate effective functions (Van der Stede, 2015). It also assists to the

company to compare their cost in systematic way. It helps to the organisation to take effective

decisions. Therefore, it analysis contribution of the different products that generates more

money. Beside this, it includes the data which related to total cost. It is not providing separate

data which related to fixed and variable costs. This system not includes evaluation of the variable

overhead (Bouten and Hoozée, 2013).

Ratio analysis: This tool helps to the business to asses their performances in effective

manner. It assists to forecast, determine plans and perform so many activities together

Mittelstand. With the help of ratio analysis, information can be getting that generates more

profits and revenue within the selected business. Beside this, liquidity ratio also entails to extent

in which business has enough amount of money through they are able to meet with their current

liabilities and obligations. Ratio analysis also perform in respect to control directly and measure

expenses in the method to use performance analysis (Christ and Burritt, 2017).

3 Critically evaluates the benefits of system of management accounting

In this way, following are such benefits in the management accounting information of the

Mittelstand:

Budgeting control: In this technique, management accounting help to encourage several

people to do their work in systematic way (Bennett, Schaltegger and Zvezdov, 2013). It assists to

accomplish goals and objectives in systematic way at workplace of Mittelstand. Through

performing several activities, the chosen enterprise has opportunity to control their activities

4

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

which could be perform in the large context. Budgetary control is the effective tool that help to

provide proper assistance. It helps to increase coordination among the employees of the business.

As results, performances level assessed according to the expectation level of management

(DRURY, 2013).

Marginal costing: This type of costing assists to the chosen business to control over the

cost level at large aspect. Within the marginal costing, allocations of the fixed cost can be

ignored. Along with this, it is the easiest method which determines several numbers of units that

offered by the Mittelstand. When the chosen business exceed their level, the business will able to

accomplish effective profit margin. This type of technique helps to make effective relationship

among the cost and volume of profit margin (Bennett, Schaltegger and Zvezdov, 2013).

Standard costing: It determines as the tool to prepare, control, manage and ascertain cost

management performances. It includes estimation of the cost of material and other elements

which required in the production process (Bebbington, Unerman and O'Dwyer, 2014). For

example, setting of the standards includes in the money which required for product process for

specific item. Main advantages of the standard costing is that it reduce various cost that assists to

control different types of expenses. Further, it helps to manager to determines several types of

decisions in the production process. However, it also includes different types of disadvantages

such as it taking more time and costing system also needed regular updates. Due to requirement

of the several resources costing system needed labour, time, etc. This system of the costing is

quite expensive (Johnson, 2013).

Ratio analysis: Ratio analysis is the another important aspect which assists to promote

facts and figures which present in the financial assessment. It also includes observation in the

income statement which assists to identify cost and evaluate cost of the production in systematic

way. It can be develop enterprise performances which assists to frame objectives and goals

(Ratio Analysis, 2017).

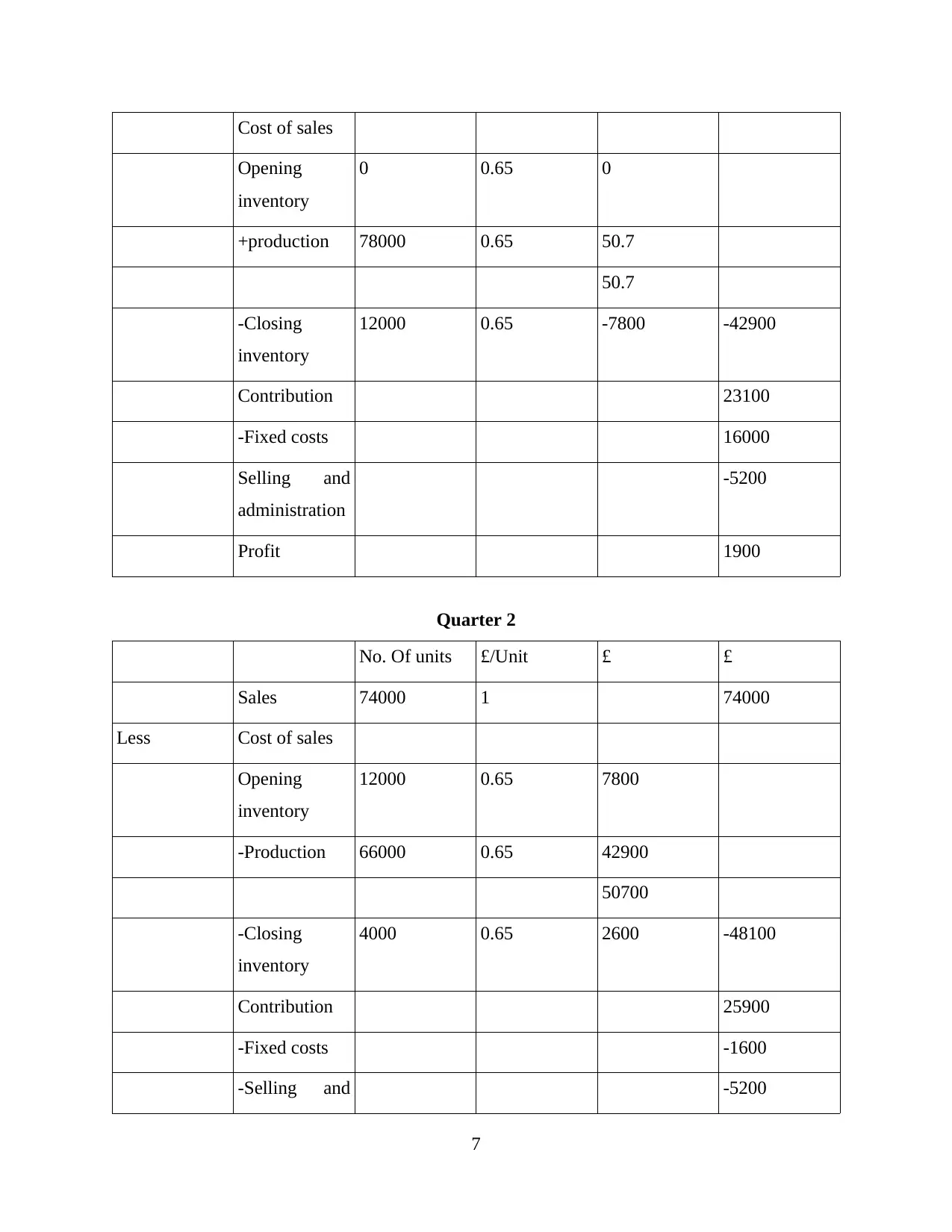

4 (a) Techniques for absorption and marginal costing

Absorption costing: There are several names in which absorption costing has been

determines. In this way, several types of the costs has been taken in the account which names as

fixed and variable cost (McLean, McGovern and Davie, 2015). Along with this, variable

expenses can also gather that changed continuously and observed in the manufacturing of

products and services. In the present analysis of costing, different types of things demonstrates

5

provide proper assistance. It helps to increase coordination among the employees of the business.

As results, performances level assessed according to the expectation level of management

(DRURY, 2013).

Marginal costing: This type of costing assists to the chosen business to control over the

cost level at large aspect. Within the marginal costing, allocations of the fixed cost can be

ignored. Along with this, it is the easiest method which determines several numbers of units that

offered by the Mittelstand. When the chosen business exceed their level, the business will able to

accomplish effective profit margin. This type of technique helps to make effective relationship

among the cost and volume of profit margin (Bennett, Schaltegger and Zvezdov, 2013).

Standard costing: It determines as the tool to prepare, control, manage and ascertain cost

management performances. It includes estimation of the cost of material and other elements

which required in the production process (Bebbington, Unerman and O'Dwyer, 2014). For

example, setting of the standards includes in the money which required for product process for

specific item. Main advantages of the standard costing is that it reduce various cost that assists to

control different types of expenses. Further, it helps to manager to determines several types of

decisions in the production process. However, it also includes different types of disadvantages

such as it taking more time and costing system also needed regular updates. Due to requirement

of the several resources costing system needed labour, time, etc. This system of the costing is

quite expensive (Johnson, 2013).

Ratio analysis: Ratio analysis is the another important aspect which assists to promote

facts and figures which present in the financial assessment. It also includes observation in the

income statement which assists to identify cost and evaluate cost of the production in systematic

way. It can be develop enterprise performances which assists to frame objectives and goals

(Ratio Analysis, 2017).

4 (a) Techniques for absorption and marginal costing

Absorption costing: There are several names in which absorption costing has been

determines. In this way, several types of the costs has been taken in the account which names as

fixed and variable cost (McLean, McGovern and Davie, 2015). Along with this, variable

expenses can also gather that changed continuously and observed in the manufacturing of

products and services. In the present analysis of costing, different types of things demonstrates

5

for absorption for the specific job at production place. It creates major attention with distribution

including varied sort of expenses in business unit.

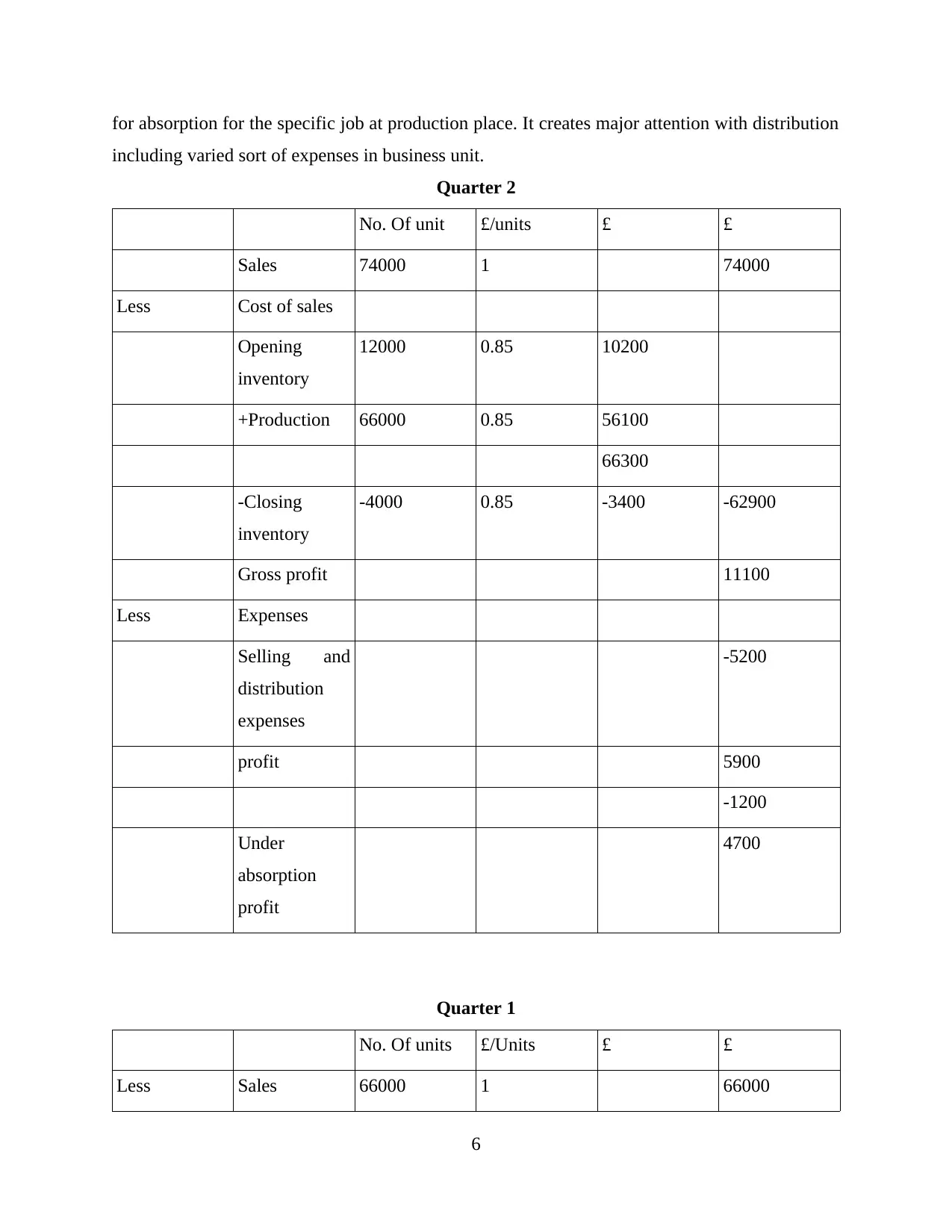

Quarter 2

No. Of unit £/units £ £

Sales 74000 1 74000

Less Cost of sales

Opening

inventory

12000 0.85 10200

+Production 66000 0.85 56100

66300

-Closing

inventory

-4000 0.85 -3400 -62900

Gross profit 11100

Less Expenses

Selling and

distribution

expenses

-5200

profit 5900

-1200

Under

absorption

profit

4700

Quarter 1

No. Of units £/Units £ £

Less Sales 66000 1 66000

6

including varied sort of expenses in business unit.

Quarter 2

No. Of unit £/units £ £

Sales 74000 1 74000

Less Cost of sales

Opening

inventory

12000 0.85 10200

+Production 66000 0.85 56100

66300

-Closing

inventory

-4000 0.85 -3400 -62900

Gross profit 11100

Less Expenses

Selling and

distribution

expenses

-5200

profit 5900

-1200

Under

absorption

profit

4700

Quarter 1

No. Of units £/Units £ £

Less Sales 66000 1 66000

6

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Cost of sales

Opening

inventory

0 0.65 0

+production 78000 0.65 50.7

50.7

-Closing

inventory

12000 0.65 -7800 -42900

Contribution 23100

-Fixed costs 16000

Selling and

administration

-5200

Profit 1900

Quarter 2

No. Of units £/Unit £ £

Sales 74000 1 74000

Less Cost of sales

Opening

inventory

12000 0.65 7800

-Production 66000 0.65 42900

50700

-Closing

inventory

4000 0.65 2600 -48100

Contribution 25900

-Fixed costs -1600

-Selling and -5200

7

Opening

inventory

0 0.65 0

+production 78000 0.65 50.7

50.7

-Closing

inventory

12000 0.65 -7800 -42900

Contribution 23100

-Fixed costs 16000

Selling and

administration

-5200

Profit 1900

Quarter 2

No. Of units £/Unit £ £

Sales 74000 1 74000

Less Cost of sales

Opening

inventory

12000 0.65 7800

-Production 66000 0.65 42900

50700

-Closing

inventory

4000 0.65 2600 -48100

Contribution 25900

-Fixed costs -1600

-Selling and -5200

7

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

administration

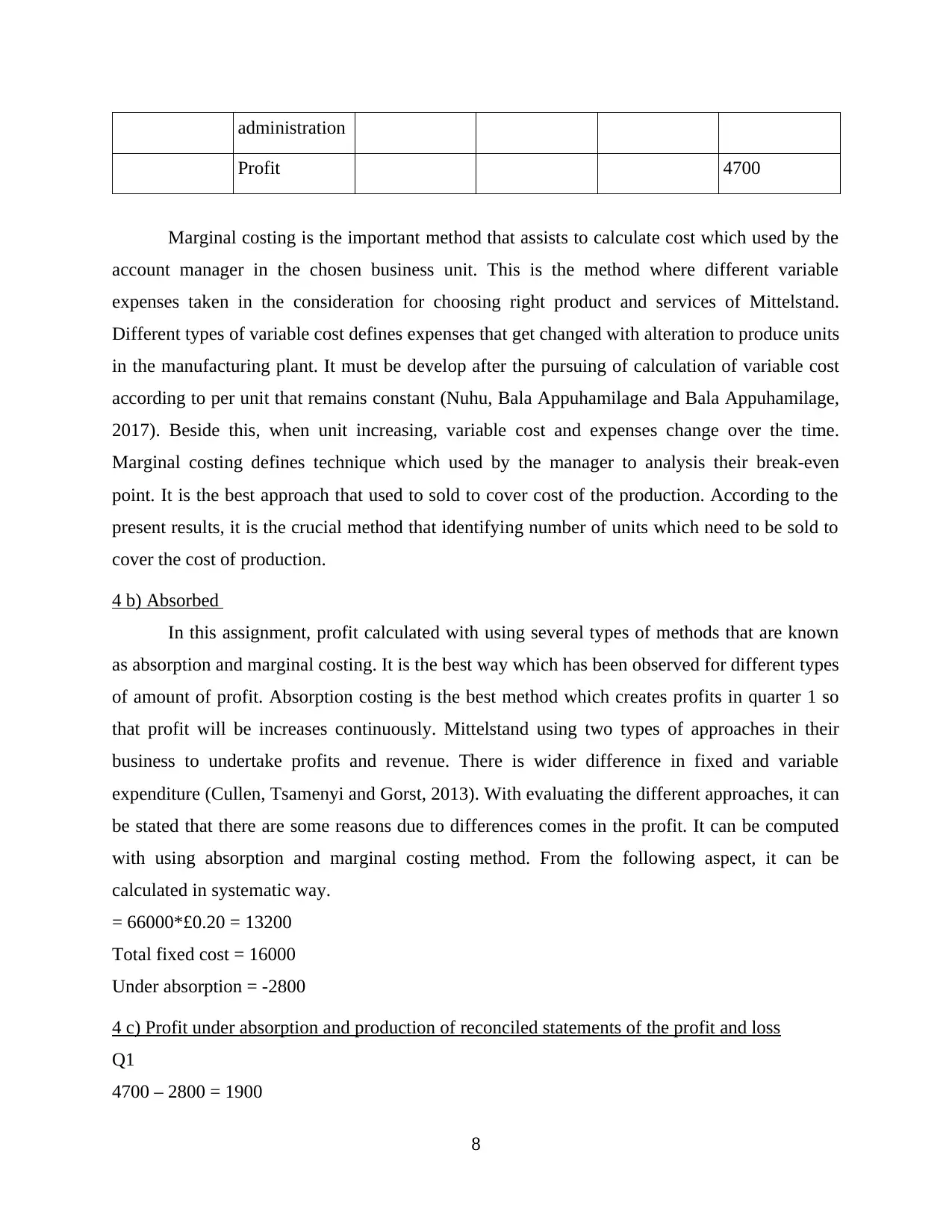

Profit 4700

Marginal costing is the important method that assists to calculate cost which used by the

account manager in the chosen business unit. This is the method where different variable

expenses taken in the consideration for choosing right product and services of Mittelstand.

Different types of variable cost defines expenses that get changed with alteration to produce units

in the manufacturing plant. It must be develop after the pursuing of calculation of variable cost

according to per unit that remains constant (Nuhu, Bala Appuhamilage and Bala Appuhamilage,

2017). Beside this, when unit increasing, variable cost and expenses change over the time.

Marginal costing defines technique which used by the manager to analysis their break-even

point. It is the best approach that used to sold to cover cost of the production. According to the

present results, it is the crucial method that identifying number of units which need to be sold to

cover the cost of production.

4 b) Absorbed

In this assignment, profit calculated with using several types of methods that are known

as absorption and marginal costing. It is the best way which has been observed for different types

of amount of profit. Absorption costing is the best method which creates profits in quarter 1 so

that profit will be increases continuously. Mittelstand using two types of approaches in their

business to undertake profits and revenue. There is wider difference in fixed and variable

expenditure (Cullen, Tsamenyi and Gorst, 2013). With evaluating the different approaches, it can

be stated that there are some reasons due to differences comes in the profit. It can be computed

with using absorption and marginal costing method. From the following aspect, it can be

calculated in systematic way.

= 66000*£0.20 = 13200

Total fixed cost = 16000

Under absorption = -2800

4 c) Profit under absorption and production of reconciled statements of the profit and loss

Q1

4700 – 2800 = 1900

8

Profit 4700

Marginal costing is the important method that assists to calculate cost which used by the

account manager in the chosen business unit. This is the method where different variable

expenses taken in the consideration for choosing right product and services of Mittelstand.

Different types of variable cost defines expenses that get changed with alteration to produce units

in the manufacturing plant. It must be develop after the pursuing of calculation of variable cost

according to per unit that remains constant (Nuhu, Bala Appuhamilage and Bala Appuhamilage,

2017). Beside this, when unit increasing, variable cost and expenses change over the time.

Marginal costing defines technique which used by the manager to analysis their break-even

point. It is the best approach that used to sold to cover cost of the production. According to the

present results, it is the crucial method that identifying number of units which need to be sold to

cover the cost of production.

4 b) Absorbed

In this assignment, profit calculated with using several types of methods that are known

as absorption and marginal costing. It is the best way which has been observed for different types

of amount of profit. Absorption costing is the best method which creates profits in quarter 1 so

that profit will be increases continuously. Mittelstand using two types of approaches in their

business to undertake profits and revenue. There is wider difference in fixed and variable

expenditure (Cullen, Tsamenyi and Gorst, 2013). With evaluating the different approaches, it can

be stated that there are some reasons due to differences comes in the profit. It can be computed

with using absorption and marginal costing method. From the following aspect, it can be

calculated in systematic way.

= 66000*£0.20 = 13200

Total fixed cost = 16000

Under absorption = -2800

4 c) Profit under absorption and production of reconciled statements of the profit and loss

Q1

4700 – 2800 = 1900

8

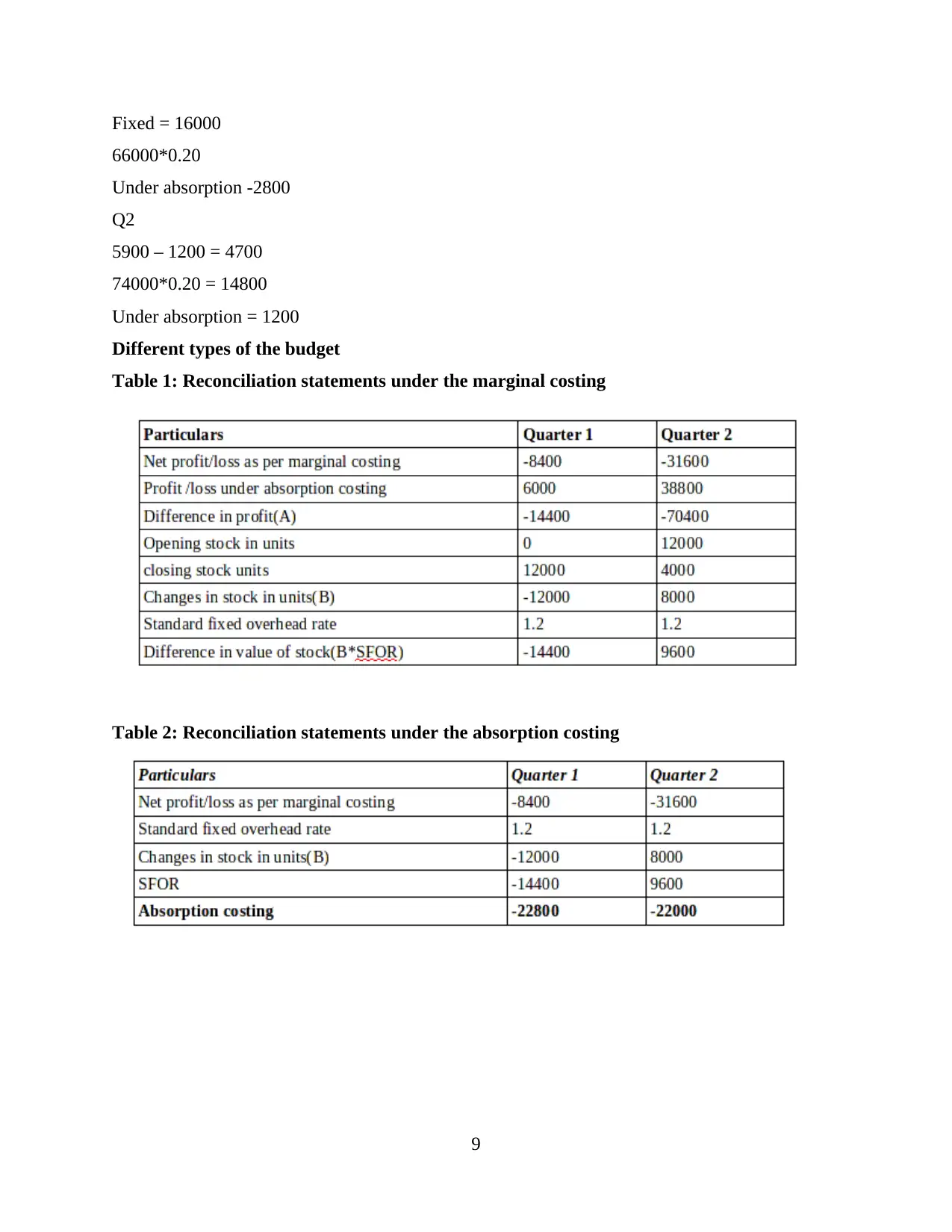

Fixed = 16000

66000*0.20

Under absorption -2800

Q2

5900 – 1200 = 4700

74000*0.20 = 14800

Under absorption = 1200

Different types of the budget

Table 1: Reconciliation statements under the marginal costing

Table 2: Reconciliation statements under the absorption costing

9

66000*0.20

Under absorption -2800

Q2

5900 – 1200 = 4700

74000*0.20 = 14800

Under absorption = 1200

Different types of the budget

Table 1: Reconciliation statements under the marginal costing

Table 2: Reconciliation statements under the absorption costing

9

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 18

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.