Business Finance Report: Financial Analysis and Cash Flow Management

VerifiedAdded on 2022/12/15

|12

|3302

|454

Report

AI Summary

This report analyzes two case studies related to business finance. The first part focuses on Trend Ltd, a gym clothing and footwear manufacturer, examining profit, cash flow, working capital components (receivables, inventory, payables), and the impact of working capital changes on cash flow. It analyzes the company's financial results, including investment decisions, debt, and disputes with customers and suppliers, and offers recommendations to improve cash flow through better working capital management. The second part involves Thorne Estates Limited, a real estate company, where a monthly cash budget from January to April 2021 is prepared. Based on the cash budget, the report provides observations and recommendations to the management of Thorne Estate Limited, considering factors like sales, fees charged, expenses, and loan payments. The report aims to provide a comprehensive understanding of financial analysis and cash flow management in business.

Business Finance

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Contents

Introduction..............................................................................................................................................3

Task 1 3

Explain:................................................................................................................................................3

Analysis of management of company financial results in the wake of above components................5

Recommendation to improve company’s cash flow through better working capital management.....6

Introduction..............................................................................................................................................7

Task 2 7

1. Monthly Cash budget from 1st January to 1st April, 2021................................................................7

2. Observations and recommendations to the management of Thorne Estate Limited.......................8

References..............................................................................................................................................11

Introduction..............................................................................................................................................3

Task 1 3

Explain:................................................................................................................................................3

Analysis of management of company financial results in the wake of above components................5

Recommendation to improve company’s cash flow through better working capital management.....6

Introduction..............................................................................................................................................7

Task 2 7

1. Monthly Cash budget from 1st January to 1st April, 2021................................................................7

2. Observations and recommendations to the management of Thorne Estate Limited.......................8

References..............................................................................................................................................11

Introduction

Business finance is that function of business which pertains to draw up activities that

are related to financial health of the business. It includes recording and assessing information

of financial nature for the business (Zherlitsyn and Kravchenko, 2016). This task is about

preparing a report for shareholders explaining the meaning and differences of the various

components related to the financial accounts and working capital management of Trend Ltd

(“TL”). On the basis of this information, financial results and operational management of the

company is analyzed to recommend steps that company management can take to improve cash

flow through better working capital management.

Task 1

Explain:

1. Profit and Cashflow

Profit: Profit in a business is an accounting term that is used to represent net income

over expenses. Net expenses over income are known as loss. Profit are one of the basic

benchmarks that an investor looks for whenever seeking information of a company to

ascertain potential investment in it. It is further divided to pay out dividends to

shareholders and remaining amount is retained in business.

Cashflow: Cash is basic necessity of business operations and cashflow refers to the

net movement of the cash in and out of the business during a specific period of time (Akan

and Tevfik, 2020). It can be both positive and negative in a business. Positive cashflow

refers to surplus of inflow over outflow while negative cashflow refers to surplus of

outflow over inflow. Cashflow in a business is ascertained through cashflow statement in

an organization. Cashflow statement is further divided into operating cashflow, financing

cashflow and investing cashflow.

Difference:

Particulars Profit Cashflow

Term Accounting term and created

only for accounting in books

of account.

Physical term as involved

with checking physical

movement of cash and

cash equivalents.

Focuses on Tracking income and

expenses

Tracking inflow and

outflow of cash

Business finance is that function of business which pertains to draw up activities that

are related to financial health of the business. It includes recording and assessing information

of financial nature for the business (Zherlitsyn and Kravchenko, 2016). This task is about

preparing a report for shareholders explaining the meaning and differences of the various

components related to the financial accounts and working capital management of Trend Ltd

(“TL”). On the basis of this information, financial results and operational management of the

company is analyzed to recommend steps that company management can take to improve cash

flow through better working capital management.

Task 1

Explain:

1. Profit and Cashflow

Profit: Profit in a business is an accounting term that is used to represent net income

over expenses. Net expenses over income are known as loss. Profit are one of the basic

benchmarks that an investor looks for whenever seeking information of a company to

ascertain potential investment in it. It is further divided to pay out dividends to

shareholders and remaining amount is retained in business.

Cashflow: Cash is basic necessity of business operations and cashflow refers to the

net movement of the cash in and out of the business during a specific period of time (Akan

and Tevfik, 2020). It can be both positive and negative in a business. Positive cashflow

refers to surplus of inflow over outflow while negative cashflow refers to surplus of

outflow over inflow. Cashflow in a business is ascertained through cashflow statement in

an organization. Cashflow statement is further divided into operating cashflow, financing

cashflow and investing cashflow.

Difference:

Particulars Profit Cashflow

Term Accounting term and created

only for accounting in books

of account.

Physical term as involved

with checking physical

movement of cash and

cash equivalents.

Focuses on Tracking income and

expenses

Tracking inflow and

outflow of cash

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Recorded on Accrual Concept Cash Concept

Includes Both cash and non-cash items Only cash items

2. Working Capital and its components – receivables, inventory and payables

Figure 1 Components of Working Capital, 2021 Source: WallStreetMojo

Working Capital: Working capital is an accounting concept which is used to denote

difference between the current assets and current liabilities of the company. It is calculated

by deducting current assets from current liabilities as well as through working capital ratio

which is also known as current ratio (Chung and et. al., 2016).

Receivables: These are part of current assets and includes all the debtors that

company have during its operational process. It also includes the amount that is due to

business to bills of exchange. These are managed through receivables’ management cycle

which is aimed at ensuing timely collection and avoidance of bad debts.

Inventory: These are also part of current assets and includes the stocks of all the raw

materials to the finished products that the company deals into. Inventory management forms

an integral part of the working capital management so that its ordering, handling and

delivering cost is optimized and company is saved from wasting any resource.

Payable: These are part of current liabilities and includes all the creditors that

company have during its operational process. It also includes the amount of bills of

exchange that is due to business to pay off. These are managed through payables’

management cycle which is aimed at ensuing timely payment so that credit worthiness of

company remains good.

Includes Both cash and non-cash items Only cash items

2. Working Capital and its components – receivables, inventory and payables

Figure 1 Components of Working Capital, 2021 Source: WallStreetMojo

Working Capital: Working capital is an accounting concept which is used to denote

difference between the current assets and current liabilities of the company. It is calculated

by deducting current assets from current liabilities as well as through working capital ratio

which is also known as current ratio (Chung and et. al., 2016).

Receivables: These are part of current assets and includes all the debtors that

company have during its operational process. It also includes the amount that is due to

business to bills of exchange. These are managed through receivables’ management cycle

which is aimed at ensuing timely collection and avoidance of bad debts.

Inventory: These are also part of current assets and includes the stocks of all the raw

materials to the finished products that the company deals into. Inventory management forms

an integral part of the working capital management so that its ordering, handling and

delivering cost is optimized and company is saved from wasting any resource.

Payable: These are part of current liabilities and includes all the creditors that

company have during its operational process. It also includes the amount of bills of

exchange that is due to business to pay off. These are managed through payables’

management cycle which is aimed at ensuing timely payment so that credit worthiness of

company remains good.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

3. Effect of changes in working capital over cashflow

As identified earlier, net working capital is the excess of current assets over current

liabilities. Cashflow is concerned about flow of cash and cash equivalents in the business

which are part of current assets. In other words, working capital is a broad term under

which four main components are integrally taken care of, which are inventory, trade

receivables, trade payables and cash and cash equivalents which form cashflow. All the

four components affect each other. For example, inventory ordering, holding and

delivering all incur a cost and any delay or excess in the cost is capable of disrupting

cashflow management of the business (Burns and Dewhurst, 2016).

Trade receivables’ cycle includes booking of debtors to collection of cash from them

while trade payables’ cycle includes booking of creditors to making cash payment to them.

Therefore, any change in both of these cycles directly affects cashflow cycle of the

organization. Every industry and every organization have their own trade cycles. However,

since debtors pay to organization and creditors have to be paid off, it is said that longer the

trade payables’ cycle is, better it is considered and shorter the trade receivables’ cycle is,

better it is considered.

Analysis of management of company financial results in the wake of above components

As provided in the case study, Trend Ltd. (hereinafter referred to as TL) is a gym

clothing and footwear manufacturing company. It is a family owned and managed

corporation, headed by Managing Director Arpha. Last year, it had reported turnover of more

than £300 million and an operating profit of £60 million. Its two key customers are Tkechers

Ltd and Sadidas Ltd.

Last year company had substantial changes in the cashflow management as it had

invested £20 million in a company to acquires its stakes as well as had agreed to pay it £5

million as supply for some exclusive products. In order to arrange for the money, it had taken

additional debt and the debt level of the company increased by additional £35 million last

year. Additional debt comes at a cost which will put additional burden over the cashflow of

the company as the revenue stream from the investment has not been specified (Heil, 2017).

Company could have saved this additional burden over its capital structure as well as

working capital management but it has an outstanding payment of £10 million from Tkechers

for an order placed by it, last year. Additionally, from its another key customer, Sadidas, it is

As identified earlier, net working capital is the excess of current assets over current

liabilities. Cashflow is concerned about flow of cash and cash equivalents in the business

which are part of current assets. In other words, working capital is a broad term under

which four main components are integrally taken care of, which are inventory, trade

receivables, trade payables and cash and cash equivalents which form cashflow. All the

four components affect each other. For example, inventory ordering, holding and

delivering all incur a cost and any delay or excess in the cost is capable of disrupting

cashflow management of the business (Burns and Dewhurst, 2016).

Trade receivables’ cycle includes booking of debtors to collection of cash from them

while trade payables’ cycle includes booking of creditors to making cash payment to them.

Therefore, any change in both of these cycles directly affects cashflow cycle of the

organization. Every industry and every organization have their own trade cycles. However,

since debtors pay to organization and creditors have to be paid off, it is said that longer the

trade payables’ cycle is, better it is considered and shorter the trade receivables’ cycle is,

better it is considered.

Analysis of management of company financial results in the wake of above components

As provided in the case study, Trend Ltd. (hereinafter referred to as TL) is a gym

clothing and footwear manufacturing company. It is a family owned and managed

corporation, headed by Managing Director Arpha. Last year, it had reported turnover of more

than £300 million and an operating profit of £60 million. Its two key customers are Tkechers

Ltd and Sadidas Ltd.

Last year company had substantial changes in the cashflow management as it had

invested £20 million in a company to acquires its stakes as well as had agreed to pay it £5

million as supply for some exclusive products. In order to arrange for the money, it had taken

additional debt and the debt level of the company increased by additional £35 million last

year. Additional debt comes at a cost which will put additional burden over the cashflow of

the company as the revenue stream from the investment has not been specified (Heil, 2017).

Company could have saved this additional burden over its capital structure as well as

working capital management but it has an outstanding payment of £10 million from Tkechers

for an order placed by it, last year. Additionally, from its another key customer, Sadidas, it is

in an outstanding dispute of about £12.5 million for a delivery completed in 2019. Payment is

stuck in legal arbitration. Furthermore, Managing Director Arpha believes that this dispute

has arose due to company using sub-standard materials from a supplier and hence, refused to

make payment to that supplier. The supplier is now threatening legal action which is neither

good for company’s cashflow nor for its goodwill. In anticipation of that threat, it has

accumulated more than required level of stock in warehouse, which is unnecessarily

increasing inventory holding cost. All this has stressed cash flow management of the

company and rather than arranging for inflow in such tight cash situation, Arpha has refused

to press major customers to pay off the money owed to TL (Tenca, Croce and Ughetto,

2018).

Recommendation to improve company’s cash flow through better working capital

management

From the above analysis, it can be seen that company leadership does not have good

management and operational practice in execution which has created such tight situations for

the company. Company is in dire need to improve its working capital practices so that its cash

flow can be improved.

First of all, management needs to bifurcate the transactions and events and then

assimilate their fate together to form effective working capital management practices. For

example, a sum of £10 million is due from Tkechers Ltd. from last year yet, the managing

director is not pressing for payment. This is not an effective debtor management practice and

this way TL management is increasing the chance of debtor being defaulter. Further, it is

embroiled in a dispute with Sadidas and the matter is pending at legal arbitration. It must be

concluded soon so that company can receive payment from debtor or at least be clear about the

fate of the case (van der Schans, 2015). Additionally, legal cost being incurred by TL will be

saved.

Furthermore, company has refused payment to creditor in some unsubstantiated

beliefs of managing director and again in anticipation of legal action, it has piled more than

required stock which has increased the cost unnecessarily. Rather than taking such hasty

decisions, company management shall involve in negotiation with supplier company so that

matter can be solved without going legal ways as it would have further repercussions for both

parties. Moreover, if things go wrong way, rather than accumulating stock, it can enter into

stuck in legal arbitration. Furthermore, Managing Director Arpha believes that this dispute

has arose due to company using sub-standard materials from a supplier and hence, refused to

make payment to that supplier. The supplier is now threatening legal action which is neither

good for company’s cashflow nor for its goodwill. In anticipation of that threat, it has

accumulated more than required level of stock in warehouse, which is unnecessarily

increasing inventory holding cost. All this has stressed cash flow management of the

company and rather than arranging for inflow in such tight cash situation, Arpha has refused

to press major customers to pay off the money owed to TL (Tenca, Croce and Ughetto,

2018).

Recommendation to improve company’s cash flow through better working capital

management

From the above analysis, it can be seen that company leadership does not have good

management and operational practice in execution which has created such tight situations for

the company. Company is in dire need to improve its working capital practices so that its cash

flow can be improved.

First of all, management needs to bifurcate the transactions and events and then

assimilate their fate together to form effective working capital management practices. For

example, a sum of £10 million is due from Tkechers Ltd. from last year yet, the managing

director is not pressing for payment. This is not an effective debtor management practice and

this way TL management is increasing the chance of debtor being defaulter. Further, it is

embroiled in a dispute with Sadidas and the matter is pending at legal arbitration. It must be

concluded soon so that company can receive payment from debtor or at least be clear about the

fate of the case (van der Schans, 2015). Additionally, legal cost being incurred by TL will be

saved.

Furthermore, company has refused payment to creditor in some unsubstantiated

beliefs of managing director and again in anticipation of legal action, it has piled more than

required stock which has increased the cost unnecessarily. Rather than taking such hasty

decisions, company management shall involve in negotiation with supplier company so that

matter can be solved without going legal ways as it would have further repercussions for both

parties. Moreover, if things go wrong way, rather than accumulating stock, it can enter into

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

negotiation with some supplier who can provide stock at emergency time, at a little higher

price, saving fixed and variable storing cost.

price, saving fixed and variable storing cost.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Introduction

Business finance includes performing various activities that help management

perform monitoring and controlling actions using various tools and techniques such as

budgetary control (Buckland and Davis, 2016). This task includes preparing cash budget for

the Thorne Estates Limited and on the basis of cash budget, observations have been drawn up

for management to provide recommendations.

Task 2

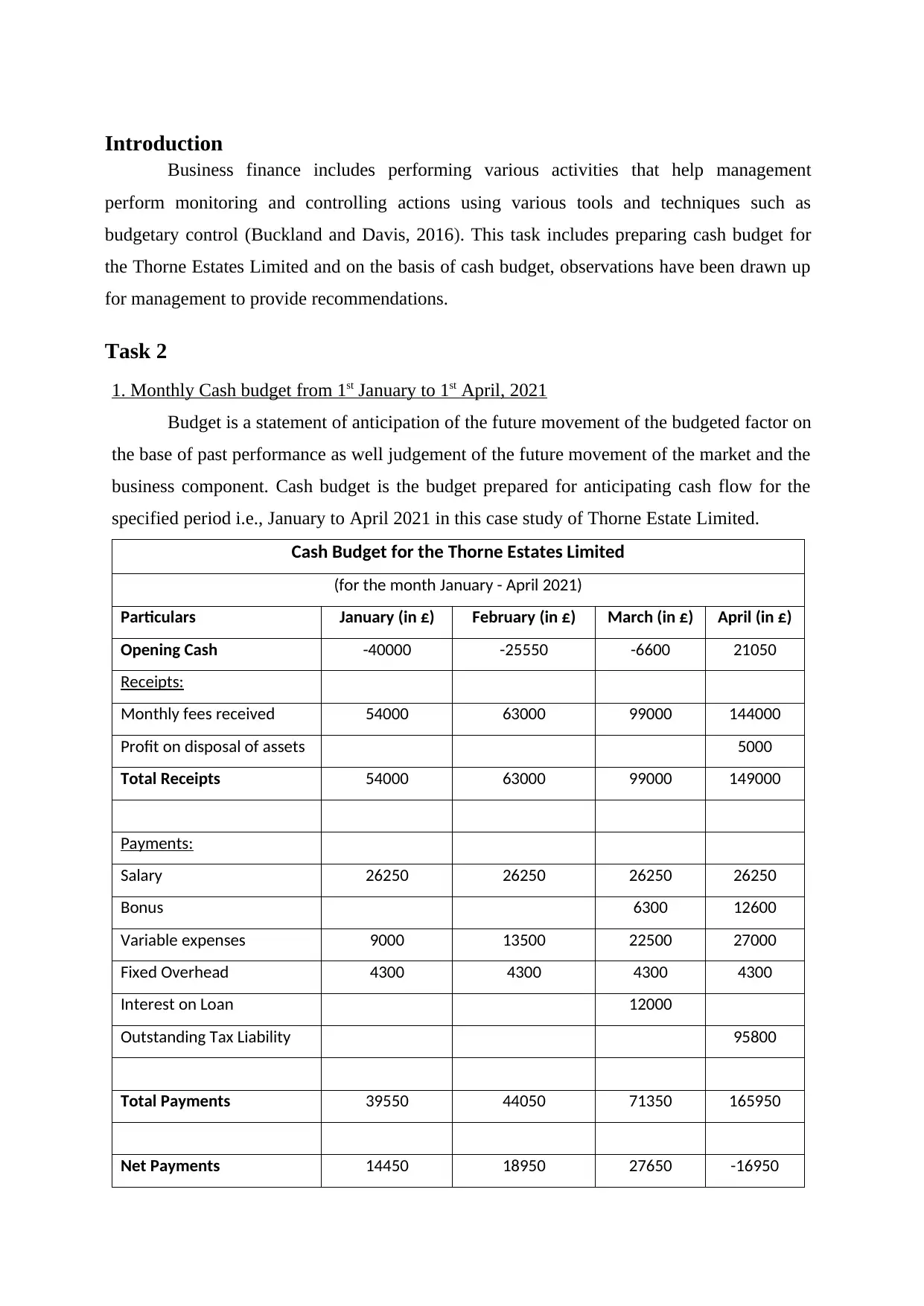

1. Monthly Cash budget from 1st January to 1st April, 2021

Budget is a statement of anticipation of the future movement of the budgeted factor on

the base of past performance as well judgement of the future movement of the market and the

business component. Cash budget is the budget prepared for anticipating cash flow for the

specified period i.e., January to April 2021 in this case study of Thorne Estate Limited.

Cash Budget for the Thorne Estates Limited

(for the month January - April 2021)

Particulars January (in £) February (in £) March (in £) April (in £)

Opening Cash -40000 -25550 -6600 21050

Receipts:

Monthly fees received 54000 63000 99000 144000

Profit on disposal of assets 5000

Total Receipts 54000 63000 99000 149000

Payments:

Salary 26250 26250 26250 26250

Bonus 6300 12600

Variable expenses 9000 13500 22500 27000

Fixed Overhead 4300 4300 4300 4300

Interest on Loan 12000

Outstanding Tax Liability 95800

Total Payments 39550 44050 71350 165950

Net Payments 14450 18950 27650 -16950

Business finance includes performing various activities that help management

perform monitoring and controlling actions using various tools and techniques such as

budgetary control (Buckland and Davis, 2016). This task includes preparing cash budget for

the Thorne Estates Limited and on the basis of cash budget, observations have been drawn up

for management to provide recommendations.

Task 2

1. Monthly Cash budget from 1st January to 1st April, 2021

Budget is a statement of anticipation of the future movement of the budgeted factor on

the base of past performance as well judgement of the future movement of the market and the

business component. Cash budget is the budget prepared for anticipating cash flow for the

specified period i.e., January to April 2021 in this case study of Thorne Estate Limited.

Cash Budget for the Thorne Estates Limited

(for the month January - April 2021)

Particulars January (in £) February (in £) March (in £) April (in £)

Opening Cash -40000 -25550 -6600 21050

Receipts:

Monthly fees received 54000 63000 99000 144000

Profit on disposal of assets 5000

Total Receipts 54000 63000 99000 149000

Payments:

Salary 26250 26250 26250 26250

Bonus 6300 12600

Variable expenses 9000 13500 22500 27000

Fixed Overhead 4300 4300 4300 4300

Interest on Loan 12000

Outstanding Tax Liability 95800

Total Payments 39550 44050 71350 165950

Net Payments 14450 18950 27650 -16950

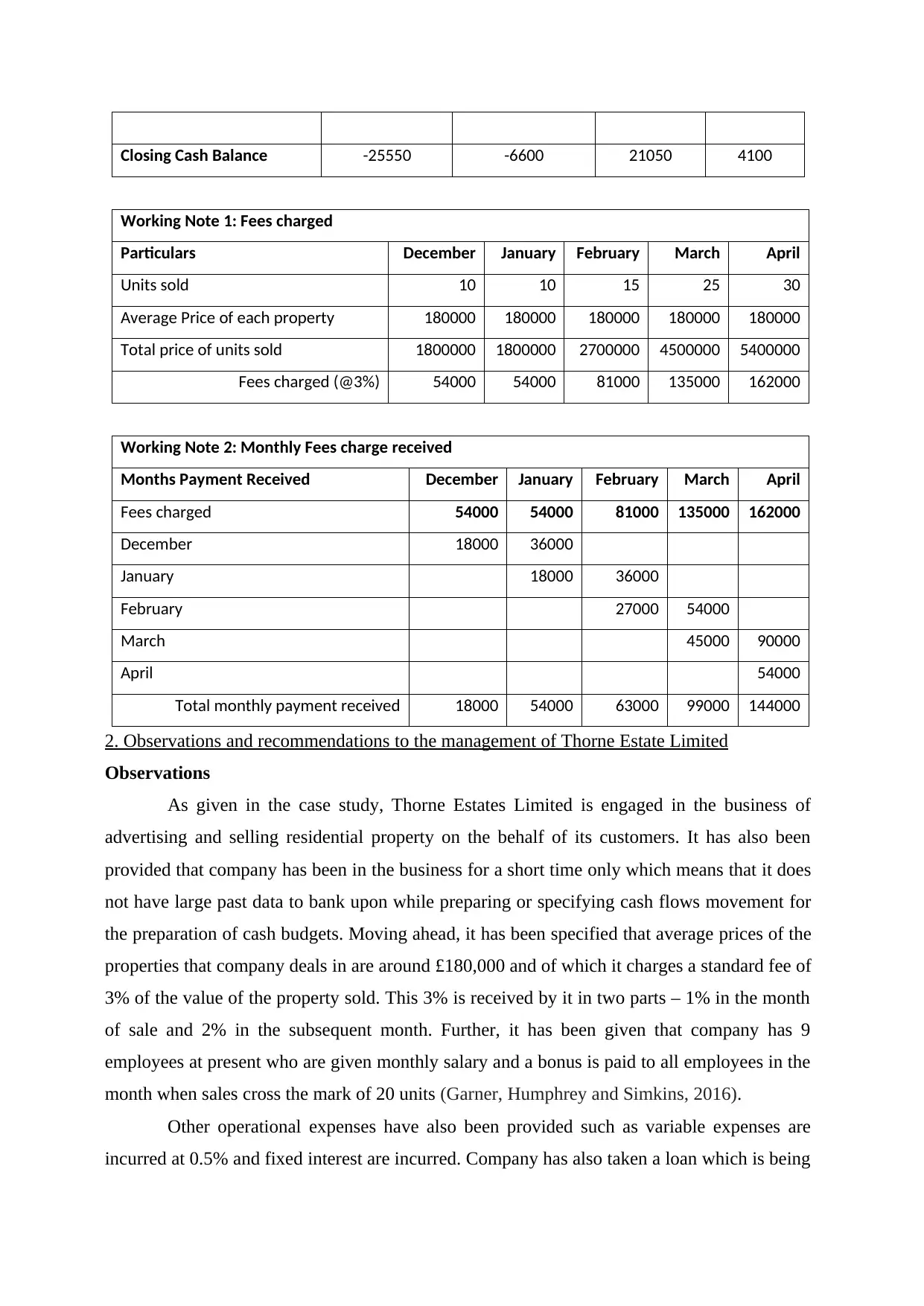

Closing Cash Balance -25550 -6600 21050 4100

Working Note 1: Fees charged

Particulars December January February March April

Units sold 10 10 15 25 30

Average Price of each property 180000 180000 180000 180000 180000

Total price of units sold 1800000 1800000 2700000 4500000 5400000

Fees charged (@3%) 54000 54000 81000 135000 162000

Working Note 2: Monthly Fees charge received

Months Payment Received December January February March April

Fees charged 54000 54000 81000 135000 162000

December 18000 36000

January 18000 36000

February 27000 54000

March 45000 90000

April 54000

Total monthly payment received 18000 54000 63000 99000 144000

2. Observations and recommendations to the management of Thorne Estate Limited

Observations

As given in the case study, Thorne Estates Limited is engaged in the business of

advertising and selling residential property on the behalf of its customers. It has also been

provided that company has been in the business for a short time only which means that it does

not have large past data to bank upon while preparing or specifying cash flows movement for

the preparation of cash budgets. Moving ahead, it has been specified that average prices of the

properties that company deals in are around £180,000 and of which it charges a standard fee of

3% of the value of the property sold. This 3% is received by it in two parts – 1% in the month

of sale and 2% in the subsequent month. Further, it has been given that company has 9

employees at present who are given monthly salary and a bonus is paid to all employees in the

month when sales cross the mark of 20 units (Garner, Humphrey and Simkins, 2016).

Other operational expenses have also been provided such as variable expenses are

incurred at 0.5% and fixed interest are incurred. Company has also taken a loan which is being

Working Note 1: Fees charged

Particulars December January February March April

Units sold 10 10 15 25 30

Average Price of each property 180000 180000 180000 180000 180000

Total price of units sold 1800000 1800000 2700000 4500000 5400000

Fees charged (@3%) 54000 54000 81000 135000 162000

Working Note 2: Monthly Fees charge received

Months Payment Received December January February March April

Fees charged 54000 54000 81000 135000 162000

December 18000 36000

January 18000 36000

February 27000 54000

March 45000 90000

April 54000

Total monthly payment received 18000 54000 63000 99000 144000

2. Observations and recommendations to the management of Thorne Estate Limited

Observations

As given in the case study, Thorne Estates Limited is engaged in the business of

advertising and selling residential property on the behalf of its customers. It has also been

provided that company has been in the business for a short time only which means that it does

not have large past data to bank upon while preparing or specifying cash flows movement for

the preparation of cash budgets. Moving ahead, it has been specified that average prices of the

properties that company deals in are around £180,000 and of which it charges a standard fee of

3% of the value of the property sold. This 3% is received by it in two parts – 1% in the month

of sale and 2% in the subsequent month. Further, it has been given that company has 9

employees at present who are given monthly salary and a bonus is paid to all employees in the

month when sales cross the mark of 20 units (Garner, Humphrey and Simkins, 2016).

Other operational expenses have also been provided such as variable expenses are

incurred at 0.5% and fixed interest are incurred. Company has also taken a loan which is being

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

paid quarterly. Company has an outstanding tax liability as well which is due to be paid in

April and company is planning to dispose of surplus vehicle at a book profit of £5,000.

Recommendations

From the above observations, it can be seen that company does have defined policies

and practices which it might have developed in accordance with the operational cycle it had

aimed and is agreed by business associates. However, at some places, this policy goes against

the interest of the business and this is where it seems wrong such as when cash budget had to

be started with deficit cash balance. This means that company is anticipating deficit cash in

closing balance of December and by no means is negative cash balance considered positive for

the company or the result of good efforts of the managerial and operational practices (Cleary

and Quinn, 2016). Therefore, keeping above observations under consideration, few

recommendations have been suggested to the management of Thorne Estate Limited so that it

can perform better cashflow management from here further.

It is good that company does not have large past data to bank upon as in such cases, it

is generally seen that factors used for forecasting business largely bank upon

historical data rather than trends in the general market conditions as well as the

industry norms. In absence of such information, company would use parameters that

are recommended to the company for preparing its cash budget on such as market

trends, industry norms, inter-personal relations, company operational practices not

only currently existing but also the ones the company has set aim to achieve, etc.

Moving ahead, company while preparing cash budget takes average of property under

consideration which can be considered a good practice for better presentation and

easy calculation. However, it can also classify the properties in different price range

and using this way company can further expand its range of products such as different

price ranges or different property range like not only residential property but also

commercial or abandoned or unused property.

Alike product classification, company can also classify fees from a standard rate of

3% to a variable rate as per the product classification. Further, 3% should rather than

1% + 2% shall be taken as 2% + 1% so that maximum part of fees is received first and

then rest is accommodated. Employees are paid regularly like on monthly basis.

However, bonus shall not be given to all employees when it crosses 20 as it is not

good practice if company intends to scale up its level of operations (Cheng, Li and

Tong, 2016). Rather, sales and promotions team shall be given bonus only or to the

employees directly involved in the sales. This would further promote competition

April and company is planning to dispose of surplus vehicle at a book profit of £5,000.

Recommendations

From the above observations, it can be seen that company does have defined policies

and practices which it might have developed in accordance with the operational cycle it had

aimed and is agreed by business associates. However, at some places, this policy goes against

the interest of the business and this is where it seems wrong such as when cash budget had to

be started with deficit cash balance. This means that company is anticipating deficit cash in

closing balance of December and by no means is negative cash balance considered positive for

the company or the result of good efforts of the managerial and operational practices (Cleary

and Quinn, 2016). Therefore, keeping above observations under consideration, few

recommendations have been suggested to the management of Thorne Estate Limited so that it

can perform better cashflow management from here further.

It is good that company does not have large past data to bank upon as in such cases, it

is generally seen that factors used for forecasting business largely bank upon

historical data rather than trends in the general market conditions as well as the

industry norms. In absence of such information, company would use parameters that

are recommended to the company for preparing its cash budget on such as market

trends, industry norms, inter-personal relations, company operational practices not

only currently existing but also the ones the company has set aim to achieve, etc.

Moving ahead, company while preparing cash budget takes average of property under

consideration which can be considered a good practice for better presentation and

easy calculation. However, it can also classify the properties in different price range

and using this way company can further expand its range of products such as different

price ranges or different property range like not only residential property but also

commercial or abandoned or unused property.

Alike product classification, company can also classify fees from a standard rate of

3% to a variable rate as per the product classification. Further, 3% should rather than

1% + 2% shall be taken as 2% + 1% so that maximum part of fees is received first and

then rest is accommodated. Employees are paid regularly like on monthly basis.

However, bonus shall not be given to all employees when it crosses 20 as it is not

good practice if company intends to scale up its level of operations (Cheng, Li and

Tong, 2016). Rather, sales and promotions team shall be given bonus only or to the

employees directly involved in the sales. This would further promote competition

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

amongst employees to outperform each other to earn maximum incentives. However,

company environment shall be tracked regularly in case company decides to

implement such policy so that it can ensure that competition for performance is not

spoiling company working culture.

Considering that company does not have fixed revenue level, it should also try to

optimize its fixed capital structure like going asset light or rather than owning fixed

assets which can be managed otherwise, it can go for lease rental options if they are

available at more economic rates than fixed prices are incurred at the present

(Kapinos, Gurley-Calvez and Kapinos, 2016). Moreover, company has a substantial

amount of tax liability due. Therefore, rather than leaving it to time, company shall

make estimate of tax liability in advance and create provision for it so that additional

burden is not created on the cashflow of the company. It is expected that using these

recommendations will help company in improving their cashflow management and it

will not come into deficit again.

company environment shall be tracked regularly in case company decides to

implement such policy so that it can ensure that competition for performance is not

spoiling company working culture.

Considering that company does not have fixed revenue level, it should also try to

optimize its fixed capital structure like going asset light or rather than owning fixed

assets which can be managed otherwise, it can go for lease rental options if they are

available at more economic rates than fixed prices are incurred at the present

(Kapinos, Gurley-Calvez and Kapinos, 2016). Moreover, company has a substantial

amount of tax liability due. Therefore, rather than leaving it to time, company shall

make estimate of tax liability in advance and create provision for it so that additional

burden is not created on the cashflow of the company. It is expected that using these

recommendations will help company in improving their cashflow management and it

will not come into deficit again.

References

Books and Journal

Akan, M. and Tevfik, A. T., 2020. Fundamentals of finance. In Fundamentals of Finance. De

Gruyter.

Buckland, R. and Davis, E. W. eds., 2016. Finance for growing Enterprises. Routledge.

Burns, P. and Dewhurst, J. eds., 2016. Small business and entrepreneurship. Macmillan

International Higher Education.

Cheng, P., Li, L. and Tong, W. H., 2016. Target information asymmetry and acquisition

price. Journal of Business Finance & Accounting. 43(7-8). pp.976-1016.

Chung, C. Y. and et. al., 2016. Institutional monitoring: Evidence from the F‐score. Journal of

Business Finance & Accounting. 42(7-8). pp.885-914.

Cleary, P. and Quinn, M., 2016. Intellectual capital and business performance: An exploratory

study of the impact of cloud-based accounting and finance infrastructure. Journal of

Intellectual Capital.

Garner, J., Humphrey, P. R. and Simkins, B., 2016. The business of sport and the sport of

business: A review of the compensation literature in finance and

sports. International Review of Financial Analysis. 47. pp.197-204.

Heil, M., 2017. Finance and productivity: A literature review.

Kapinos, P., Gurley-Calvez, T. and Kapinos, K., 2016. (Un) expected housing price changes:

Identifying the drivers of small business finance. Journal of Economics and

Business. 84. pp.79-94.

Tenca, F., Croce, A. and Ughetto, E., 2018. Business angels research in entrepreneurial

finance: A literature review and a research agenda. Journal of Economic

Surveys. 32(5). pp.1384-1413.

van der Schans, D., 2015. The British Business Bank's role in facilitating economic growth by

addressing imperfections in SME finance markets. Venture Capital. 17(1-2). pp.7-

25.

Zherlitsyn, D. and Kravchenko, V., 2016. Supply Chain Resilience Through Operations and

Finance Management. Scientific Letters of Academic Society of Michal

Baludansky. 4(1).

Online

Components of working capital. 2021. [Online]. Available through:<

https://www.wallstreetmojo.com/components-of-working-capital/ >

Books and Journal

Akan, M. and Tevfik, A. T., 2020. Fundamentals of finance. In Fundamentals of Finance. De

Gruyter.

Buckland, R. and Davis, E. W. eds., 2016. Finance for growing Enterprises. Routledge.

Burns, P. and Dewhurst, J. eds., 2016. Small business and entrepreneurship. Macmillan

International Higher Education.

Cheng, P., Li, L. and Tong, W. H., 2016. Target information asymmetry and acquisition

price. Journal of Business Finance & Accounting. 43(7-8). pp.976-1016.

Chung, C. Y. and et. al., 2016. Institutional monitoring: Evidence from the F‐score. Journal of

Business Finance & Accounting. 42(7-8). pp.885-914.

Cleary, P. and Quinn, M., 2016. Intellectual capital and business performance: An exploratory

study of the impact of cloud-based accounting and finance infrastructure. Journal of

Intellectual Capital.

Garner, J., Humphrey, P. R. and Simkins, B., 2016. The business of sport and the sport of

business: A review of the compensation literature in finance and

sports. International Review of Financial Analysis. 47. pp.197-204.

Heil, M., 2017. Finance and productivity: A literature review.

Kapinos, P., Gurley-Calvez, T. and Kapinos, K., 2016. (Un) expected housing price changes:

Identifying the drivers of small business finance. Journal of Economics and

Business. 84. pp.79-94.

Tenca, F., Croce, A. and Ughetto, E., 2018. Business angels research in entrepreneurial

finance: A literature review and a research agenda. Journal of Economic

Surveys. 32(5). pp.1384-1413.

van der Schans, D., 2015. The British Business Bank's role in facilitating economic growth by

addressing imperfections in SME finance markets. Venture Capital. 17(1-2). pp.7-

25.

Zherlitsyn, D. and Kravchenko, V., 2016. Supply Chain Resilience Through Operations and

Finance Management. Scientific Letters of Academic Society of Michal

Baludansky. 4(1).

Online

Components of working capital. 2021. [Online]. Available through:<

https://www.wallstreetmojo.com/components-of-working-capital/ >

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 12

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.