Finance Management Report - Analysis of Secondary Sector

VerifiedAdded on 2022/12/28

|3

|338

|38

Report

AI Summary

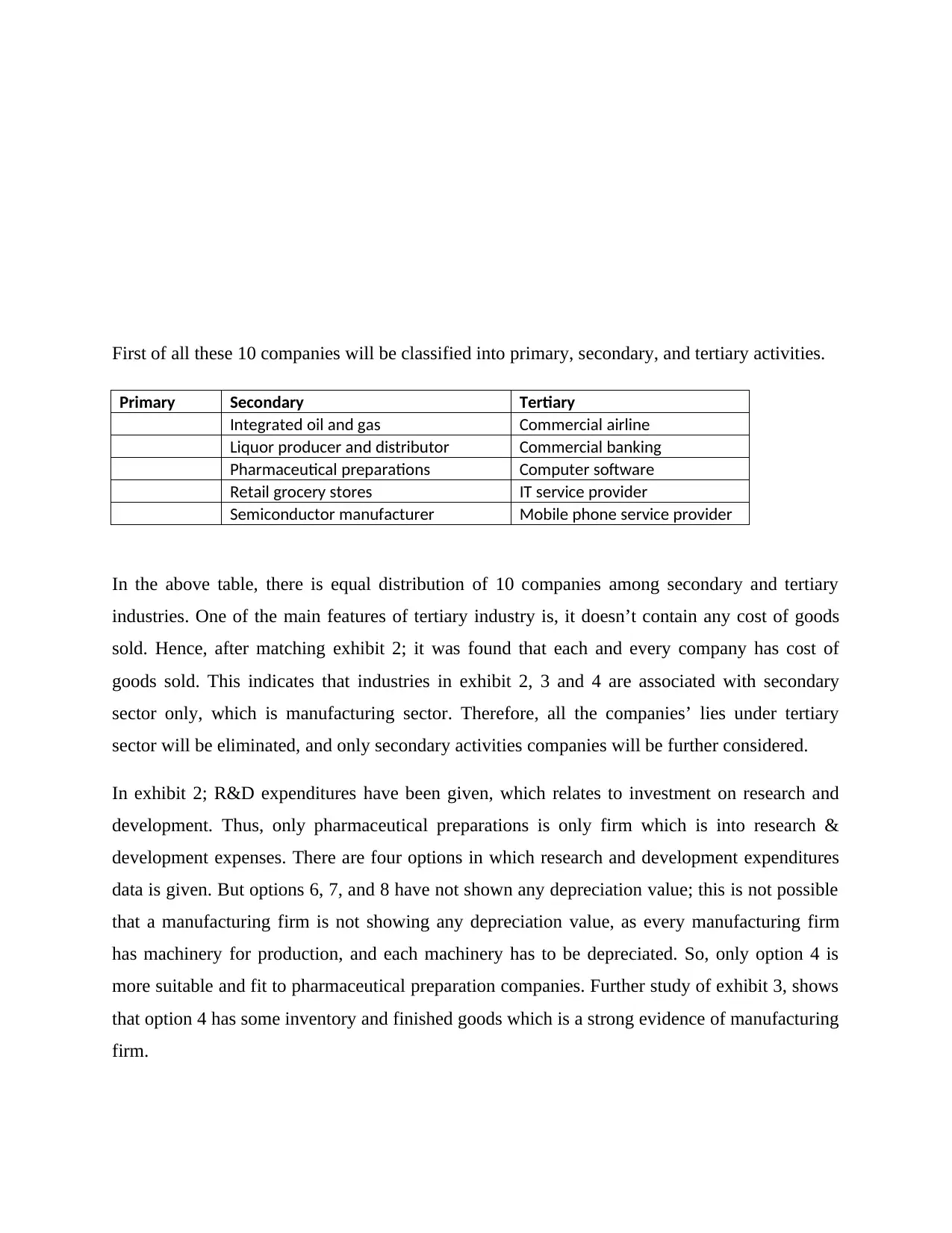

This report focuses on the financial management of companies, specifically analyzing those within the secondary sector. The analysis begins by classifying companies into primary, secondary, and tertiary sectors. The report then concentrates on the secondary sector due to the presence of cost of goods sold and manufacturing activities. The analysis further delves into research and development expenditures, identifying pharmaceutical preparations as a key area. The report examines various financial data options, selecting the most suitable one based on depreciation values, inventory, and financial ratios like the acid test ratio and current ratio. The conclusion is that the chosen option aligns with the characteristics of a manufacturing firm, highlighting the importance of inventory management in the analysis.

1 out of 3

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.