University Finance: Accounting and Finance for Managers Homework

VerifiedAdded on 2022/09/01

|14

|1304

|16

Homework Assignment

AI Summary

This document presents a comprehensive solution to an accounting and finance assignment designed for managers. The assignment covers a range of critical topics including the role of financial managers, capital requirements, and optimal financing sources. It delves into the application of ratio analysis for financial statement interpretation, the concept of annuity and time value of money. The solution further addresses investment decisions, capital budgeting techniques (NPV, IRR, payback period), and capital structure decisions. The assignment also explores cost of capital, cash management strategies, and break-even analysis. It concludes with a comparison of income statements and cash flow statements, along with the application of time value of money in capital budgeting.

Running head: ACCOUNITNG AND FINANCE FOR MANAGERS

Accounting and Finance for Managers

Name of the Student:

Name of the University:

Author’s Note:

Accounting and Finance for Managers

Name of the Student:

Name of the University:

Author’s Note:

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

1

ACCOUNTING AND FINANCE FOR MANAGERS

Table of Contents

Answer to question 1:......................................................................................................................3

Part a:...........................................................................................................................................3

Part b:...........................................................................................................................................3

Part c:...........................................................................................................................................3

Answer to question 2:......................................................................................................................4

Part a:...........................................................................................................................................4

Part b:...........................................................................................................................................5

Answer to question 3:......................................................................................................................7

Answer to question 4:......................................................................................................................8

Part a:...........................................................................................................................................8

Part b:...........................................................................................................................................8

Answer to question 5:......................................................................................................................9

Part a:...........................................................................................................................................9

Part b:.........................................................................................................................................10

Answer to question 6:....................................................................................................................10

Part a:.........................................................................................................................................10

Part b:.........................................................................................................................................10

Part c:.........................................................................................................................................10

Part d:.........................................................................................................................................11

ACCOUNTING AND FINANCE FOR MANAGERS

Table of Contents

Answer to question 1:......................................................................................................................3

Part a:...........................................................................................................................................3

Part b:...........................................................................................................................................3

Part c:...........................................................................................................................................3

Answer to question 2:......................................................................................................................4

Part a:...........................................................................................................................................4

Part b:...........................................................................................................................................5

Answer to question 3:......................................................................................................................7

Answer to question 4:......................................................................................................................8

Part a:...........................................................................................................................................8

Part b:...........................................................................................................................................8

Answer to question 5:......................................................................................................................9

Part a:...........................................................................................................................................9

Part b:.........................................................................................................................................10

Answer to question 6:....................................................................................................................10

Part a:.........................................................................................................................................10

Part b:.........................................................................................................................................10

Part c:.........................................................................................................................................10

Part d:.........................................................................................................................................11

2

ACCOUNTING AND FINANCE FOR MANAGERS

Part e:.........................................................................................................................................11

Answer to question 7:....................................................................................................................11

Part 1:.........................................................................................................................................11

Part 2:.........................................................................................................................................11

References and bibliography:........................................................................................................13

ACCOUNTING AND FINANCE FOR MANAGERS

Part e:.........................................................................................................................................11

Answer to question 7:....................................................................................................................11

Part 1:.........................................................................................................................................11

Part 2:.........................................................................................................................................11

References and bibliography:........................................................................................................13

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

3

ACCOUNTING AND FINANCE FOR MANAGERS

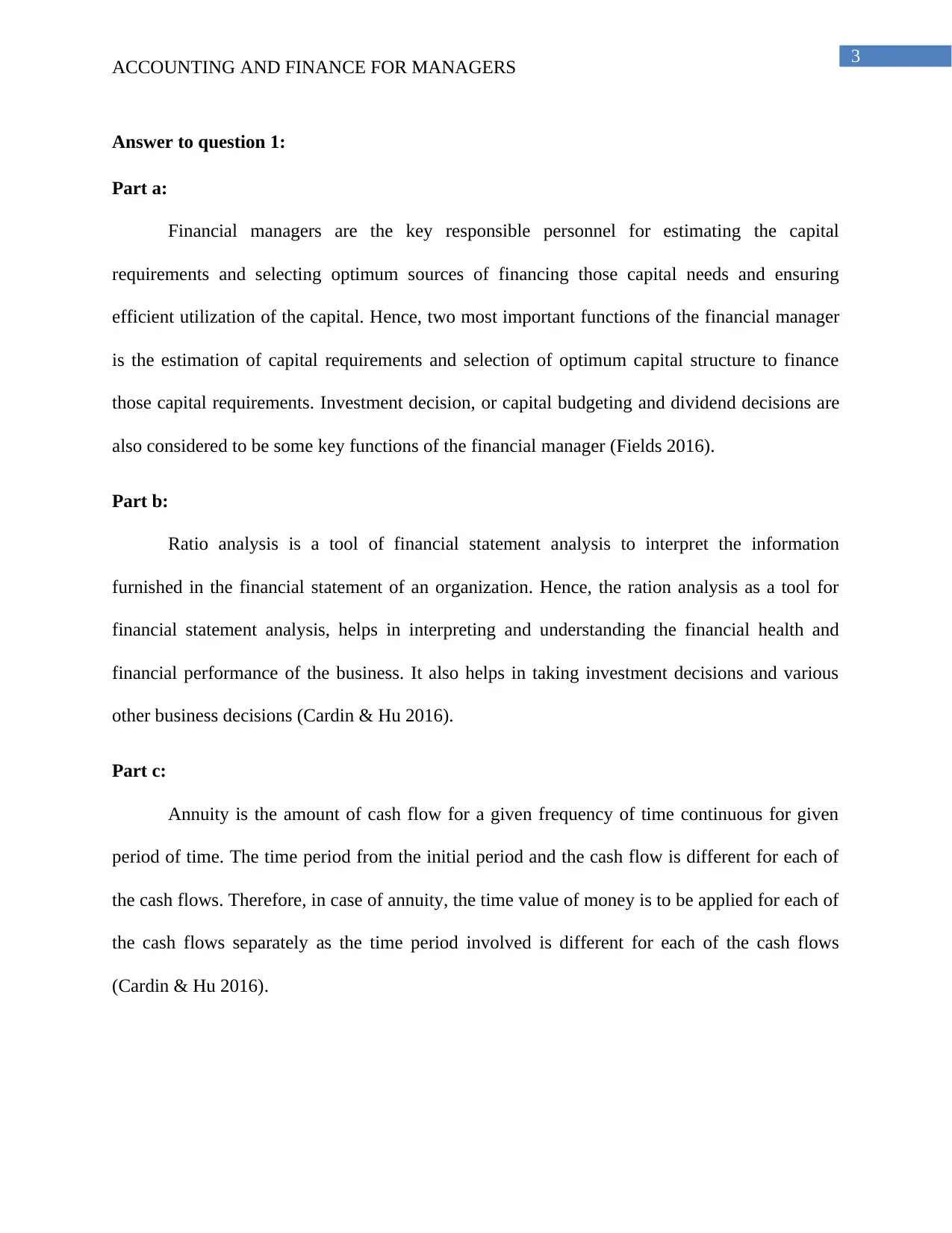

Answer to question 1:

Part a:

Financial managers are the key responsible personnel for estimating the capital

requirements and selecting optimum sources of financing those capital needs and ensuring

efficient utilization of the capital. Hence, two most important functions of the financial manager

is the estimation of capital requirements and selection of optimum capital structure to finance

those capital requirements. Investment decision, or capital budgeting and dividend decisions are

also considered to be some key functions of the financial manager (Fields 2016).

Part b:

Ratio analysis is a tool of financial statement analysis to interpret the information

furnished in the financial statement of an organization. Hence, the ration analysis as a tool for

financial statement analysis, helps in interpreting and understanding the financial health and

financial performance of the business. It also helps in taking investment decisions and various

other business decisions (Cardin & Hu 2016).

Part c:

Annuity is the amount of cash flow for a given frequency of time continuous for given

period of time. The time period from the initial period and the cash flow is different for each of

the cash flows. Therefore, in case of annuity, the time value of money is to be applied for each of

the cash flows separately as the time period involved is different for each of the cash flows

(Cardin & Hu 2016).

ACCOUNTING AND FINANCE FOR MANAGERS

Answer to question 1:

Part a:

Financial managers are the key responsible personnel for estimating the capital

requirements and selecting optimum sources of financing those capital needs and ensuring

efficient utilization of the capital. Hence, two most important functions of the financial manager

is the estimation of capital requirements and selection of optimum capital structure to finance

those capital requirements. Investment decision, or capital budgeting and dividend decisions are

also considered to be some key functions of the financial manager (Fields 2016).

Part b:

Ratio analysis is a tool of financial statement analysis to interpret the information

furnished in the financial statement of an organization. Hence, the ration analysis as a tool for

financial statement analysis, helps in interpreting and understanding the financial health and

financial performance of the business. It also helps in taking investment decisions and various

other business decisions (Cardin & Hu 2016).

Part c:

Annuity is the amount of cash flow for a given frequency of time continuous for given

period of time. The time period from the initial period and the cash flow is different for each of

the cash flows. Therefore, in case of annuity, the time value of money is to be applied for each of

the cash flows separately as the time period involved is different for each of the cash flows

(Cardin & Hu 2016).

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

4

ACCOUNTING AND FINANCE FOR MANAGERS

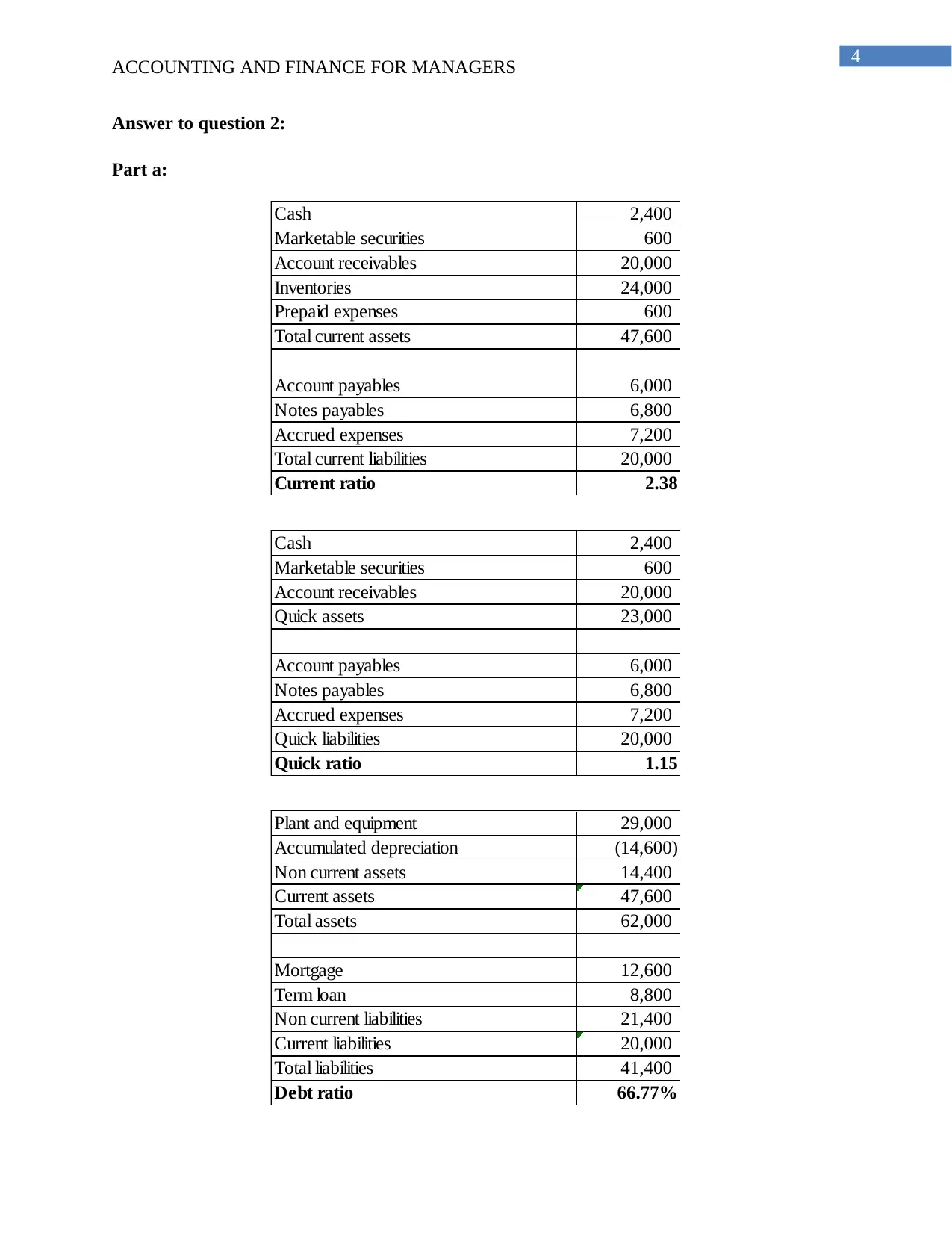

Answer to question 2:

Part a:

Cash 2,400

Marketable securities 600

Account receivables 20,000

Inventories 24,000

Prepaid expenses 600

Total current assets 47,600

Account payables 6,000

Notes payables 6,800

Accrued expenses 7,200

Total current liabilities 20,000

Current ratio 2.38

Cash 2,400

Marketable securities 600

Account receivables 20,000

Quick assets 23,000

Account payables 6,000

Notes payables 6,800

Accrued expenses 7,200

Quick liabilities 20,000

Quick ratio 1.15

Plant and equipment 29,000

Accumulated depreciation (14,600)

Non current assets 14,400

Current assets 47,600

Total assets 62,000

Mortgage 12,600

Term loan 8,800

Non current liabilities 21,400

Current liabilities 20,000

Total liabilities 41,400

Debt ratio 66.77%

ACCOUNTING AND FINANCE FOR MANAGERS

Answer to question 2:

Part a:

Cash 2,400

Marketable securities 600

Account receivables 20,000

Inventories 24,000

Prepaid expenses 600

Total current assets 47,600

Account payables 6,000

Notes payables 6,800

Accrued expenses 7,200

Total current liabilities 20,000

Current ratio 2.38

Cash 2,400

Marketable securities 600

Account receivables 20,000

Quick assets 23,000

Account payables 6,000

Notes payables 6,800

Accrued expenses 7,200

Quick liabilities 20,000

Quick ratio 1.15

Plant and equipment 29,000

Accumulated depreciation (14,600)

Non current assets 14,400

Current assets 47,600

Total assets 62,000

Mortgage 12,600

Term loan 8,800

Non current liabilities 21,400

Current liabilities 20,000

Total liabilities 41,400

Debt ratio 66.77%

5

ACCOUNTING AND FINANCE FOR MANAGERS

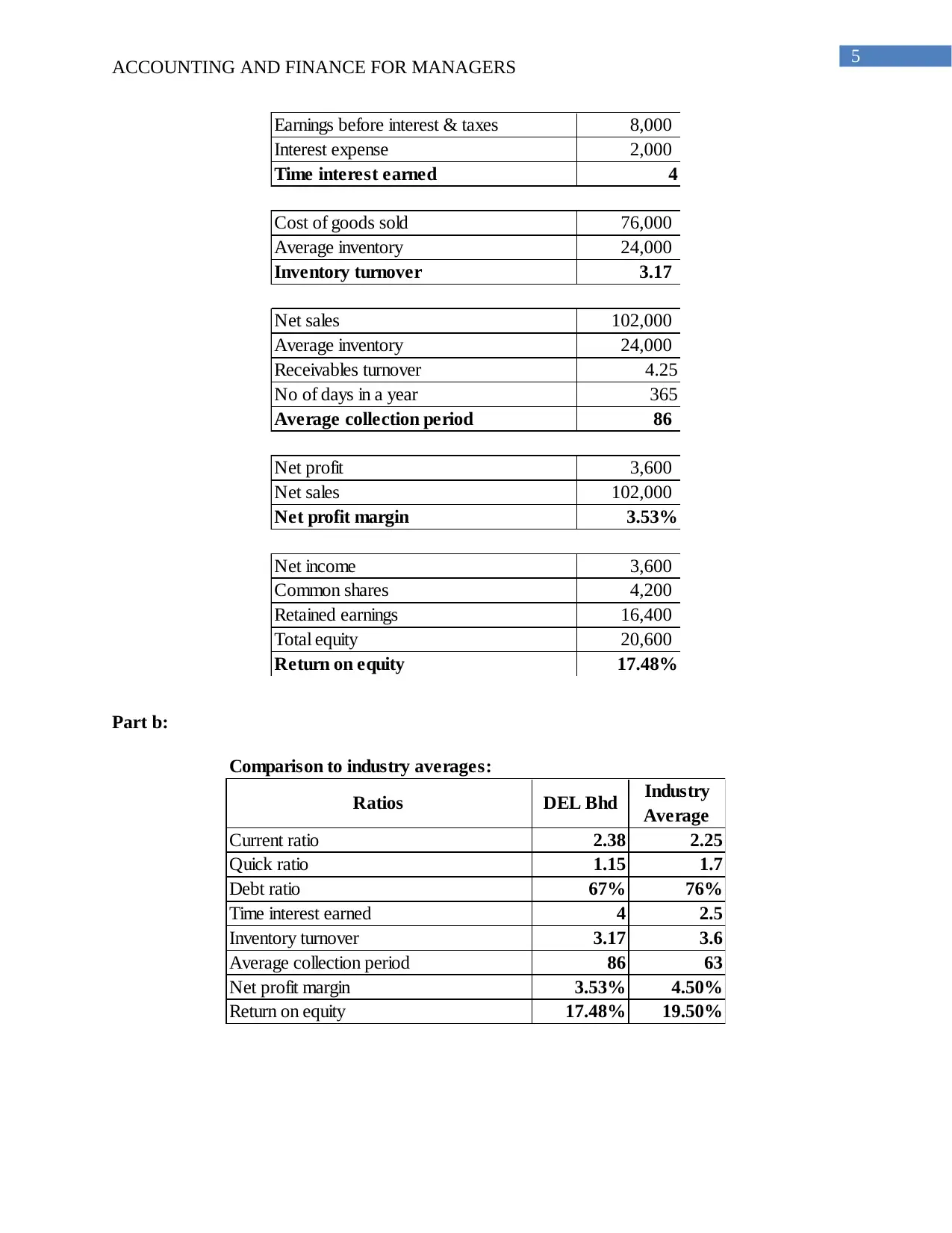

Earnings before interest & taxes 8,000

Interest expense 2,000

Time interest earned 4

Cost of goods sold 76,000

Average inventory 24,000

Inventory turnover 3.17

Net sales 102,000

Average inventory 24,000

Receivables turnover 4.25

No of days in a year 365

Average collection period 86

Net profit 3,600

Net sales 102,000

Net profit margin 3.53%

Net income 3,600

Common shares 4,200

Retained earnings 16,400

Total equity 20,600

Return on equity 17.48%

Part b:

Comparison to industry averages:

Ratios DEL Bhd Industry

Average

Current ratio 2.38 2.25

Quick ratio 1.15 1.7

Debt ratio 67% 76%

Time interest earned 4 2.5

Inventory turnover 3.17 3.6

Average collection period 86 63

Net profit margin 3.53% 4.50%

Return on equity 17.48% 19.50%

ACCOUNTING AND FINANCE FOR MANAGERS

Earnings before interest & taxes 8,000

Interest expense 2,000

Time interest earned 4

Cost of goods sold 76,000

Average inventory 24,000

Inventory turnover 3.17

Net sales 102,000

Average inventory 24,000

Receivables turnover 4.25

No of days in a year 365

Average collection period 86

Net profit 3,600

Net sales 102,000

Net profit margin 3.53%

Net income 3,600

Common shares 4,200

Retained earnings 16,400

Total equity 20,600

Return on equity 17.48%

Part b:

Comparison to industry averages:

Ratios DEL Bhd Industry

Average

Current ratio 2.38 2.25

Quick ratio 1.15 1.7

Debt ratio 67% 76%

Time interest earned 4 2.5

Inventory turnover 3.17 3.6

Average collection period 86 63

Net profit margin 3.53% 4.50%

Return on equity 17.48% 19.50%

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

6

ACCOUNTING AND FINANCE FOR MANAGERS

The current ratio of the company is higher than the industry average, which implies

higher liquidity of the company. In terms of quick ratio, the company is having less liquidity as

compared to industry average. The company is having lesser amount of debt capital in their total

capital structure, which implies higher long term solvency of the company as compared to the

industry average. The company is having an earnings of 4 times of their interest expense. It

implies they are able enough to pay interests expenses in time. The inventory turnover ratio of

the company is lesser than the industry average, it implies, they are holding higher amount of

stocks and having lesser sales revenue as compared to the industry average. In terms of profit

margin and efficiency, they are having poor performance as compared to the industry average

(Gitman, Juchau, & Flanagan 2015).

ACCOUNTING AND FINANCE FOR MANAGERS

The current ratio of the company is higher than the industry average, which implies

higher liquidity of the company. In terms of quick ratio, the company is having less liquidity as

compared to industry average. The company is having lesser amount of debt capital in their total

capital structure, which implies higher long term solvency of the company as compared to the

industry average. The company is having an earnings of 4 times of their interest expense. It

implies they are able enough to pay interests expenses in time. The inventory turnover ratio of

the company is lesser than the industry average, it implies, they are holding higher amount of

stocks and having lesser sales revenue as compared to the industry average. In terms of profit

margin and efficiency, they are having poor performance as compared to the industry average

(Gitman, Juchau, & Flanagan 2015).

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

7

ACCOUNTING AND FINANCE FOR MANAGERS

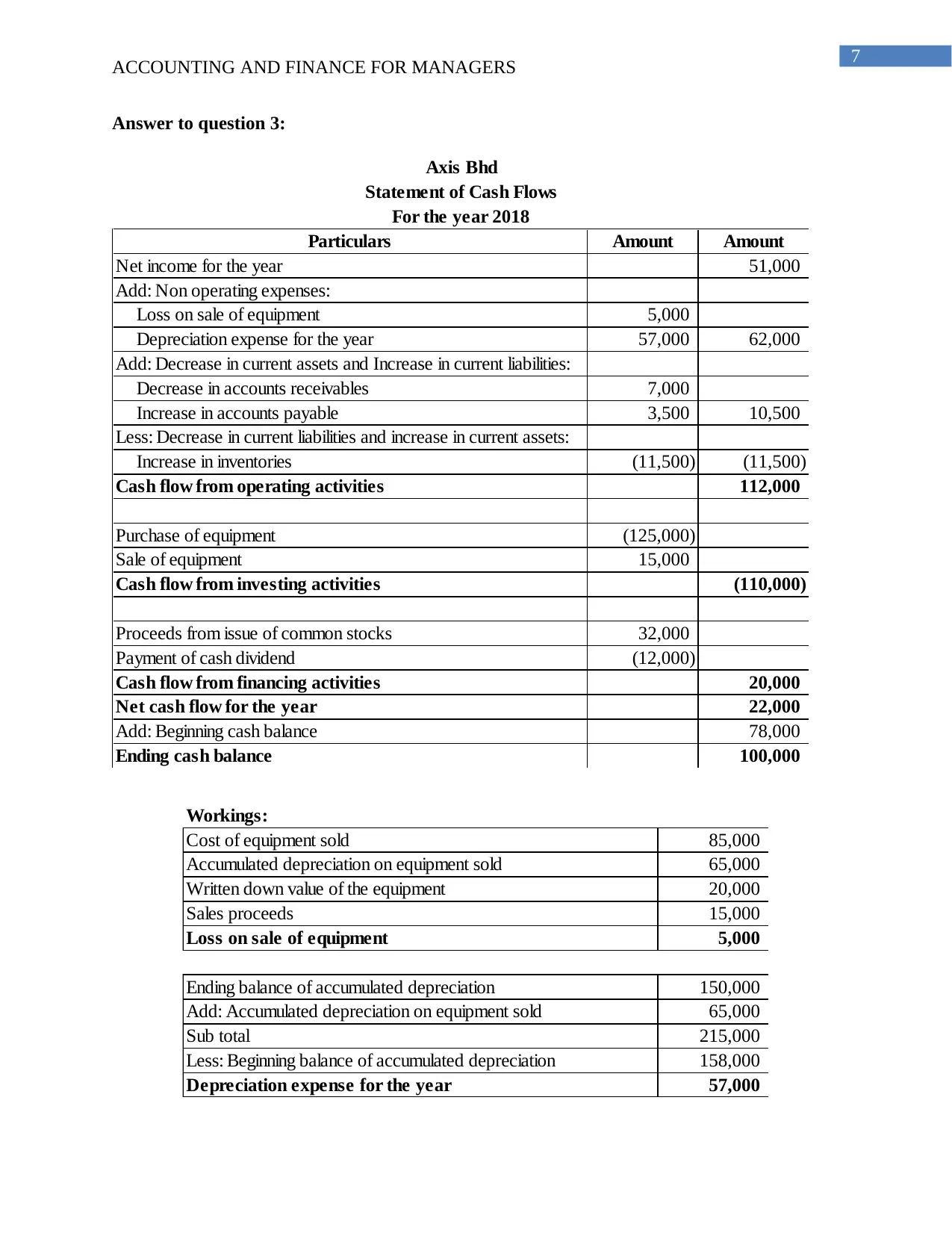

Answer to question 3:

Particulars Amount Amount

Net income for the year 51,000

Add: Non operating expenses:

Loss on sale of equipment 5,000

Depreciation expense for the year 57,000 62,000

Add: Decrease in current assets and Increase in current liabilities:

Decrease in accounts receivables 7,000

Increase in accounts payable 3,500 10,500

Less: Decrease in current liabilities and increase in current assets:

Increase in inventories (11,500) (11,500)

Cash flow from operating activities 112,000

Purchase of equipment (125,000)

Sale of equipment 15,000

Cash flow from investing activities (110,000)

Proceeds from issue of common stocks 32,000

Payment of cash dividend (12,000)

Cash flow from financing activities 20,000

Net cash flow for the year 22,000

Add: Beginning cash balance 78,000

Ending cash balance 100,000

Axis Bhd

Statement of Cash Flows

For the year 2018

Workings:

Cost of equipment sold 85,000

Accumulated depreciation on equipment sold 65,000

Written down value of the equipment 20,000

Sales proceeds 15,000

Loss on sale of equipment 5,000

Ending balance of accumulated depreciation 150,000

Add: Accumulated depreciation on equipment sold 65,000

Sub total 215,000

Less: Beginning balance of accumulated depreciation 158,000

Depreciation expense for the year 57,000

ACCOUNTING AND FINANCE FOR MANAGERS

Answer to question 3:

Particulars Amount Amount

Net income for the year 51,000

Add: Non operating expenses:

Loss on sale of equipment 5,000

Depreciation expense for the year 57,000 62,000

Add: Decrease in current assets and Increase in current liabilities:

Decrease in accounts receivables 7,000

Increase in accounts payable 3,500 10,500

Less: Decrease in current liabilities and increase in current assets:

Increase in inventories (11,500) (11,500)

Cash flow from operating activities 112,000

Purchase of equipment (125,000)

Sale of equipment 15,000

Cash flow from investing activities (110,000)

Proceeds from issue of common stocks 32,000

Payment of cash dividend (12,000)

Cash flow from financing activities 20,000

Net cash flow for the year 22,000

Add: Beginning cash balance 78,000

Ending cash balance 100,000

Axis Bhd

Statement of Cash Flows

For the year 2018

Workings:

Cost of equipment sold 85,000

Accumulated depreciation on equipment sold 65,000

Written down value of the equipment 20,000

Sales proceeds 15,000

Loss on sale of equipment 5,000

Ending balance of accumulated depreciation 150,000

Add: Accumulated depreciation on equipment sold 65,000

Sub total 215,000

Less: Beginning balance of accumulated depreciation 158,000

Depreciation expense for the year 57,000

8

ACCOUNTING AND FINANCE FOR MANAGERS

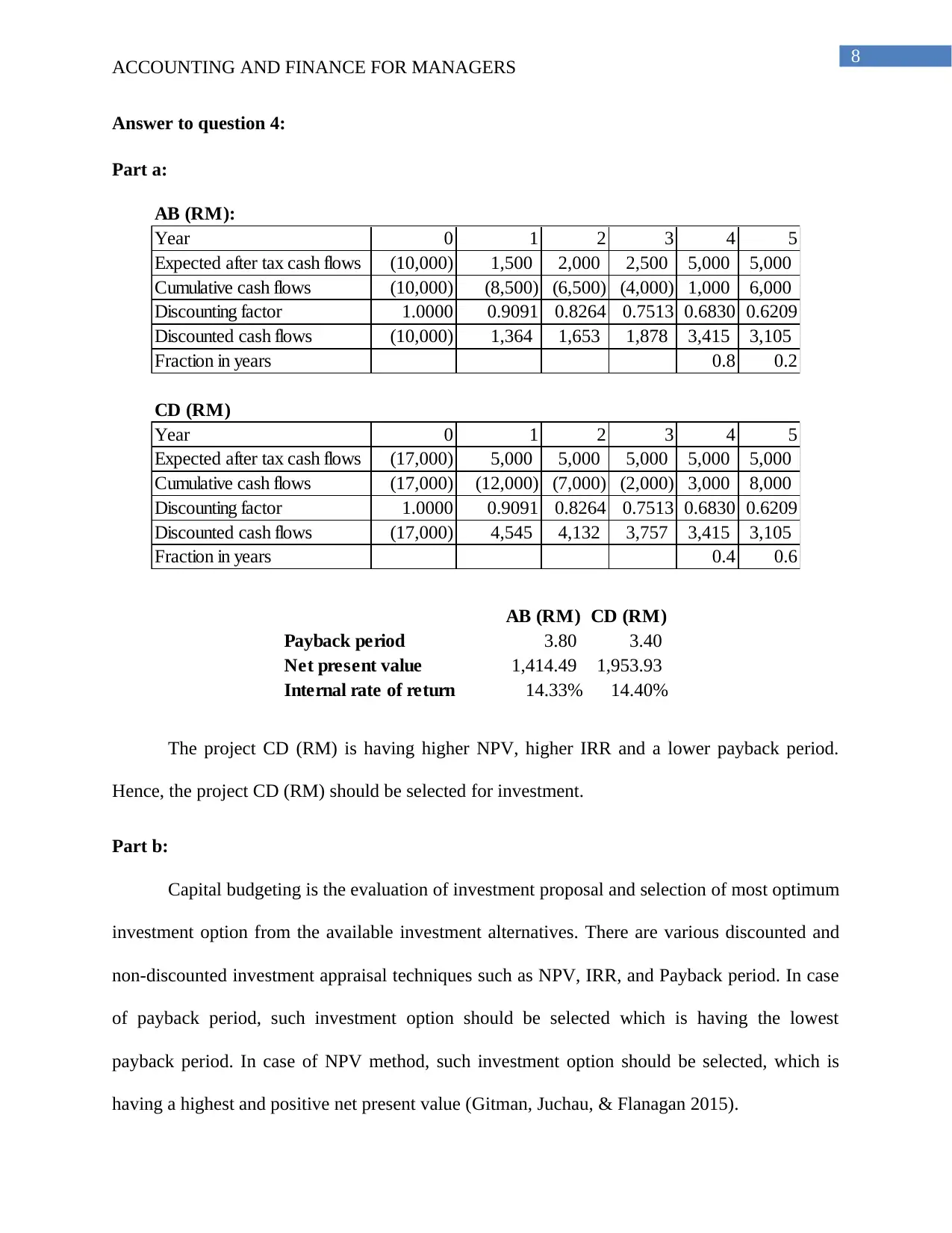

Answer to question 4:

Part a:

AB (RM):

Year 0 1 2 3 4 5

Expected after tax cash flows (10,000) 1,500 2,000 2,500 5,000 5,000

Cumulative cash flows (10,000) (8,500) (6,500) (4,000) 1,000 6,000

Discounting factor 1.0000 0.9091 0.8264 0.7513 0.6830 0.6209

Discounted cash flows (10,000) 1,364 1,653 1,878 3,415 3,105

Fraction in years 0.8 0.2

CD (RM)

Year 0 1 2 3 4 5

Expected after tax cash flows (17,000) 5,000 5,000 5,000 5,000 5,000

Cumulative cash flows (17,000) (12,000) (7,000) (2,000) 3,000 8,000

Discounting factor 1.0000 0.9091 0.8264 0.7513 0.6830 0.6209

Discounted cash flows (17,000) 4,545 4,132 3,757 3,415 3,105

Fraction in years 0.4 0.6

AB (RM) CD (RM)

Payback period 3.80 3.40

Net present value 1,414.49 1,953.93

Internal rate of return 14.33% 14.40%

The project CD (RM) is having higher NPV, higher IRR and a lower payback period.

Hence, the project CD (RM) should be selected for investment.

Part b:

Capital budgeting is the evaluation of investment proposal and selection of most optimum

investment option from the available investment alternatives. There are various discounted and

non-discounted investment appraisal techniques such as NPV, IRR, and Payback period. In case

of payback period, such investment option should be selected which is having the lowest

payback period. In case of NPV method, such investment option should be selected, which is

having a highest and positive net present value (Gitman, Juchau, & Flanagan 2015).

ACCOUNTING AND FINANCE FOR MANAGERS

Answer to question 4:

Part a:

AB (RM):

Year 0 1 2 3 4 5

Expected after tax cash flows (10,000) 1,500 2,000 2,500 5,000 5,000

Cumulative cash flows (10,000) (8,500) (6,500) (4,000) 1,000 6,000

Discounting factor 1.0000 0.9091 0.8264 0.7513 0.6830 0.6209

Discounted cash flows (10,000) 1,364 1,653 1,878 3,415 3,105

Fraction in years 0.8 0.2

CD (RM)

Year 0 1 2 3 4 5

Expected after tax cash flows (17,000) 5,000 5,000 5,000 5,000 5,000

Cumulative cash flows (17,000) (12,000) (7,000) (2,000) 3,000 8,000

Discounting factor 1.0000 0.9091 0.8264 0.7513 0.6830 0.6209

Discounted cash flows (17,000) 4,545 4,132 3,757 3,415 3,105

Fraction in years 0.4 0.6

AB (RM) CD (RM)

Payback period 3.80 3.40

Net present value 1,414.49 1,953.93

Internal rate of return 14.33% 14.40%

The project CD (RM) is having higher NPV, higher IRR and a lower payback period.

Hence, the project CD (RM) should be selected for investment.

Part b:

Capital budgeting is the evaluation of investment proposal and selection of most optimum

investment option from the available investment alternatives. There are various discounted and

non-discounted investment appraisal techniques such as NPV, IRR, and Payback period. In case

of payback period, such investment option should be selected which is having the lowest

payback period. In case of NPV method, such investment option should be selected, which is

having a highest and positive net present value (Gitman, Juchau, & Flanagan 2015).

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

9

ACCOUNTING AND FINANCE FOR MANAGERS

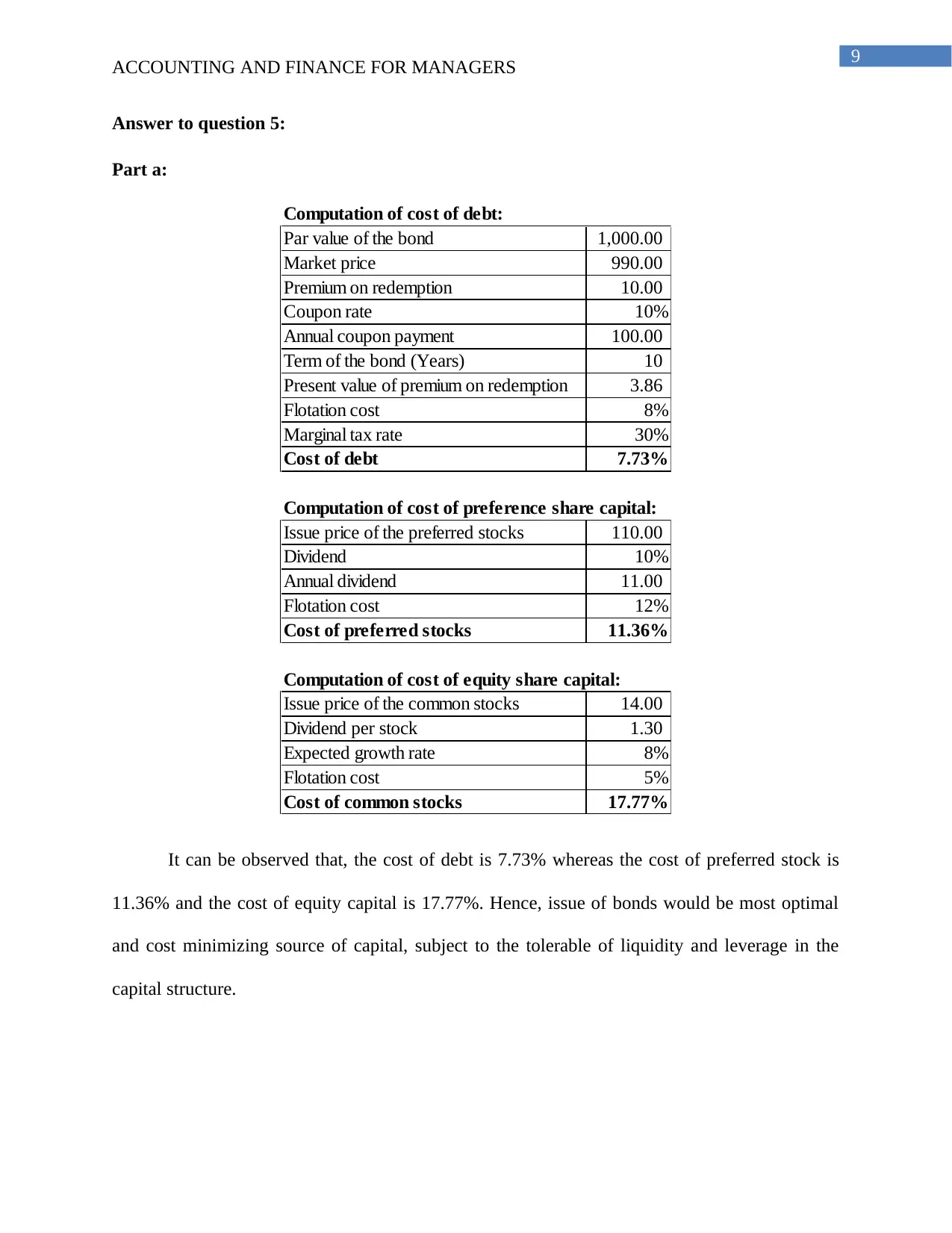

Answer to question 5:

Part a:

Computation of cost of debt:

Par value of the bond 1,000.00

Market price 990.00

Premium on redemption 10.00

Coupon rate 10%

Annual coupon payment 100.00

Term of the bond (Years) 10

Present value of premium on redemption 3.86

Flotation cost 8%

Marginal tax rate 30%

Cost of debt 7.73%

Computation of cost of preference share capital:

Issue price of the preferred stocks 110.00

Dividend 10%

Annual dividend 11.00

Flotation cost 12%

Cost of preferred stocks 11.36%

Computation of cost of equity share capital:

Issue price of the common stocks 14.00

Dividend per stock 1.30

Expected growth rate 8%

Flotation cost 5%

Cost of common stocks 17.77%

It can be observed that, the cost of debt is 7.73% whereas the cost of preferred stock is

11.36% and the cost of equity capital is 17.77%. Hence, issue of bonds would be most optimal

and cost minimizing source of capital, subject to the tolerable of liquidity and leverage in the

capital structure.

ACCOUNTING AND FINANCE FOR MANAGERS

Answer to question 5:

Part a:

Computation of cost of debt:

Par value of the bond 1,000.00

Market price 990.00

Premium on redemption 10.00

Coupon rate 10%

Annual coupon payment 100.00

Term of the bond (Years) 10

Present value of premium on redemption 3.86

Flotation cost 8%

Marginal tax rate 30%

Cost of debt 7.73%

Computation of cost of preference share capital:

Issue price of the preferred stocks 110.00

Dividend 10%

Annual dividend 11.00

Flotation cost 12%

Cost of preferred stocks 11.36%

Computation of cost of equity share capital:

Issue price of the common stocks 14.00

Dividend per stock 1.30

Expected growth rate 8%

Flotation cost 5%

Cost of common stocks 17.77%

It can be observed that, the cost of debt is 7.73% whereas the cost of preferred stock is

11.36% and the cost of equity capital is 17.77%. Hence, issue of bonds would be most optimal

and cost minimizing source of capital, subject to the tolerable of liquidity and leverage in the

capital structure.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

10

ACCOUNTING AND FINANCE FOR MANAGERS

Part b:

Cash management or cash flow management is a key responsibility of the financial

managers. To manage cash flows, they should ensure the timely collection of receivables and

credit policies. On the other hand, they need to ensure cost efficient short term financing to

manage the cash flow problems (Fields 2016).

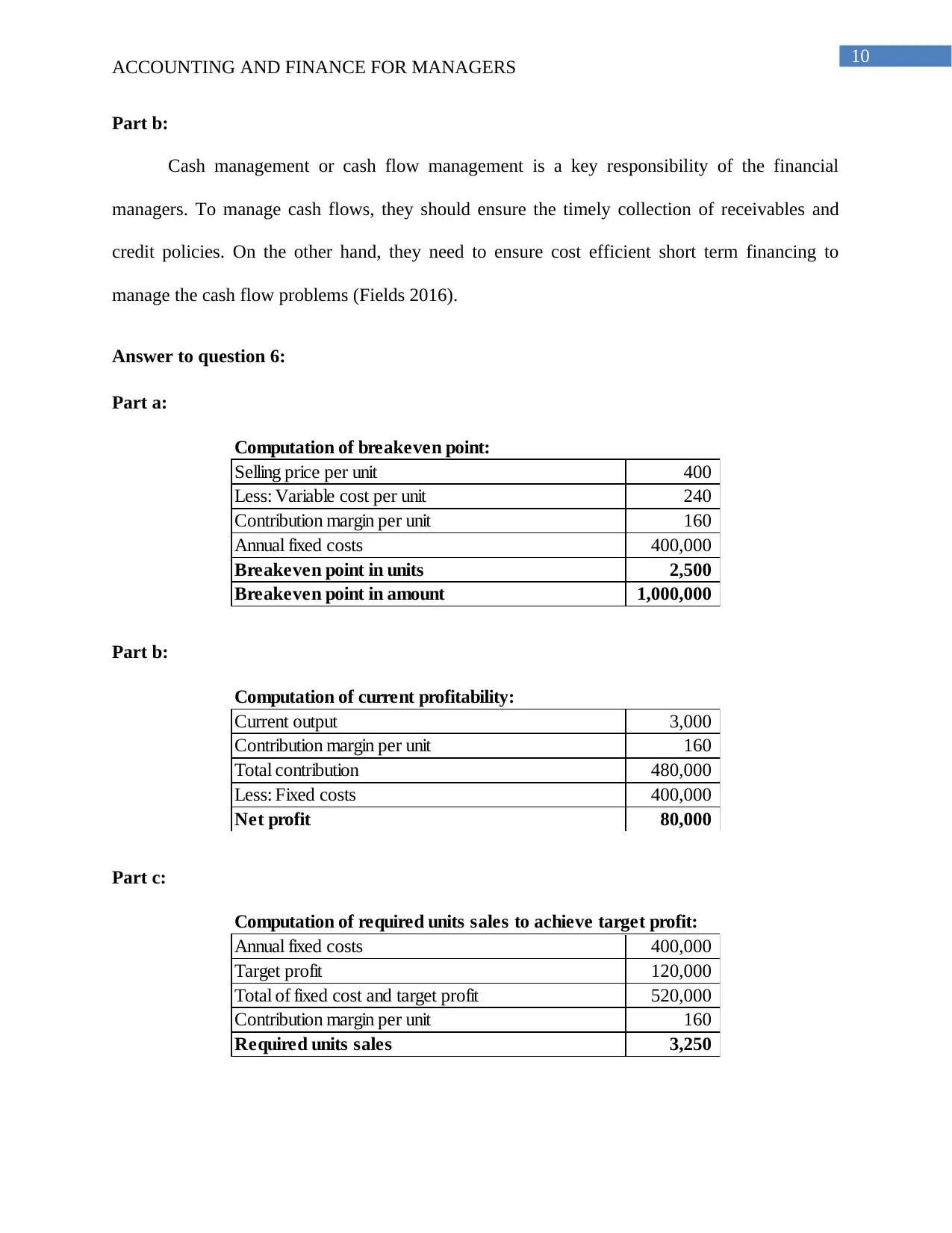

Answer to question 6:

Part a:

Computation of breakeven point:

Selling price per unit 400

Less: Variable cost per unit 240

Contribution margin per unit 160

Annual fixed costs 400,000

Breakeven point in units 2,500

Breakeven point in amount 1,000,000

Part b:

Computation of current profitability:

Current output 3,000

Contribution margin per unit 160

Total contribution 480,000

Less: Fixed costs 400,000

Net profit 80,000

Part c:

Computation of required units sales to achieve target profit:

Annual fixed costs 400,000

Target profit 120,000

Total of fixed cost and target profit 520,000

Contribution margin per unit 160

Required units sales 3,250

ACCOUNTING AND FINANCE FOR MANAGERS

Part b:

Cash management or cash flow management is a key responsibility of the financial

managers. To manage cash flows, they should ensure the timely collection of receivables and

credit policies. On the other hand, they need to ensure cost efficient short term financing to

manage the cash flow problems (Fields 2016).

Answer to question 6:

Part a:

Computation of breakeven point:

Selling price per unit 400

Less: Variable cost per unit 240

Contribution margin per unit 160

Annual fixed costs 400,000

Breakeven point in units 2,500

Breakeven point in amount 1,000,000

Part b:

Computation of current profitability:

Current output 3,000

Contribution margin per unit 160

Total contribution 480,000

Less: Fixed costs 400,000

Net profit 80,000

Part c:

Computation of required units sales to achieve target profit:

Annual fixed costs 400,000

Target profit 120,000

Total of fixed cost and target profit 520,000

Contribution margin per unit 160

Required units sales 3,250

11

ACCOUNTING AND FINANCE FOR MANAGERS

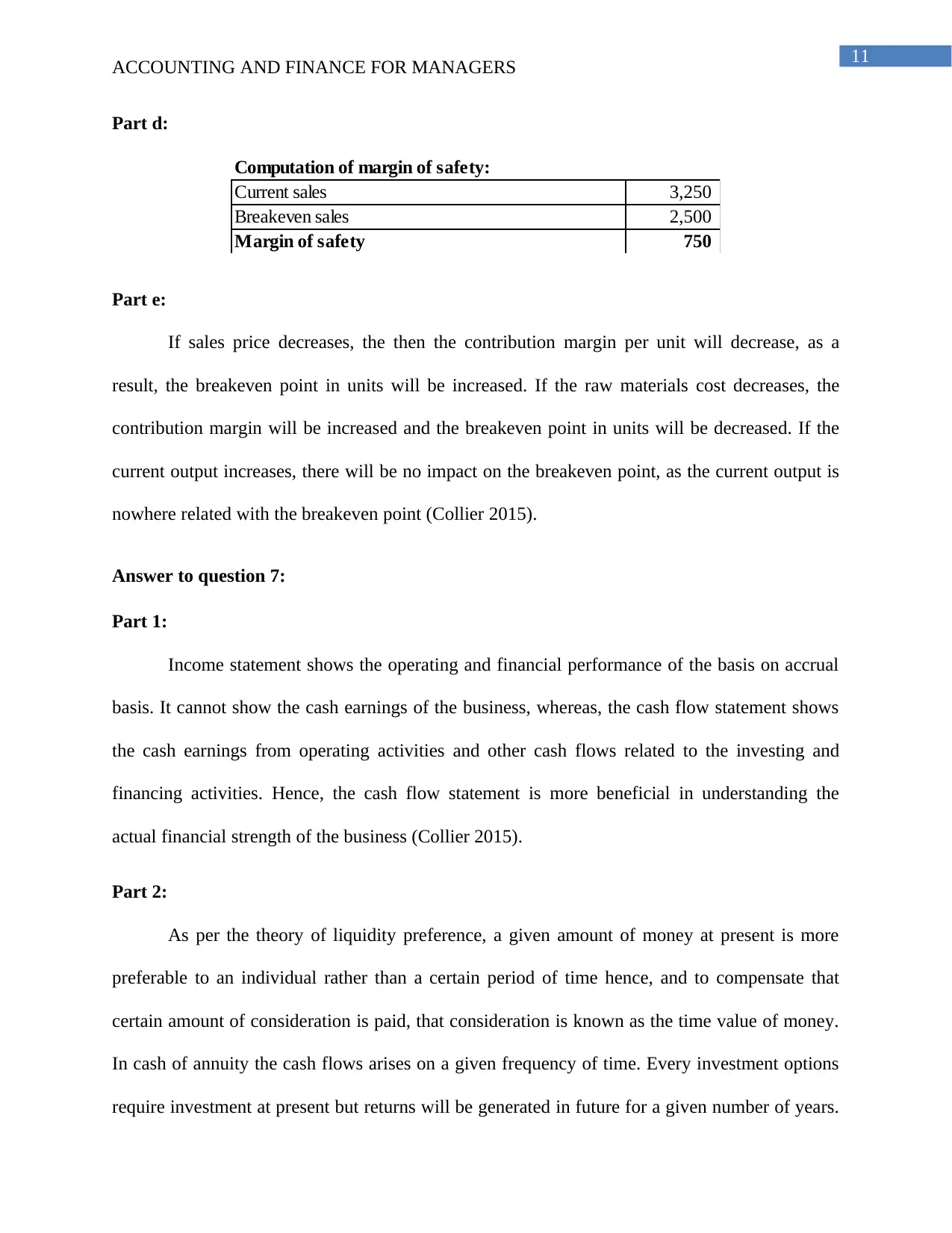

Part d:

Computation of margin of safety:

Current sales 3,250

Breakeven sales 2,500

Margin of safety 750

Part e:

If sales price decreases, the then the contribution margin per unit will decrease, as a

result, the breakeven point in units will be increased. If the raw materials cost decreases, the

contribution margin will be increased and the breakeven point in units will be decreased. If the

current output increases, there will be no impact on the breakeven point, as the current output is

nowhere related with the breakeven point (Collier 2015).

Answer to question 7:

Part 1:

Income statement shows the operating and financial performance of the basis on accrual

basis. It cannot show the cash earnings of the business, whereas, the cash flow statement shows

the cash earnings from operating activities and other cash flows related to the investing and

financing activities. Hence, the cash flow statement is more beneficial in understanding the

actual financial strength of the business (Collier 2015).

Part 2:

As per the theory of liquidity preference, a given amount of money at present is more

preferable to an individual rather than a certain period of time hence, and to compensate that

certain amount of consideration is paid, that consideration is known as the time value of money.

In cash of annuity the cash flows arises on a given frequency of time. Every investment options

require investment at present but returns will be generated in future for a given number of years.

ACCOUNTING AND FINANCE FOR MANAGERS

Part d:

Computation of margin of safety:

Current sales 3,250

Breakeven sales 2,500

Margin of safety 750

Part e:

If sales price decreases, the then the contribution margin per unit will decrease, as a

result, the breakeven point in units will be increased. If the raw materials cost decreases, the

contribution margin will be increased and the breakeven point in units will be decreased. If the

current output increases, there will be no impact on the breakeven point, as the current output is

nowhere related with the breakeven point (Collier 2015).

Answer to question 7:

Part 1:

Income statement shows the operating and financial performance of the basis on accrual

basis. It cannot show the cash earnings of the business, whereas, the cash flow statement shows

the cash earnings from operating activities and other cash flows related to the investing and

financing activities. Hence, the cash flow statement is more beneficial in understanding the

actual financial strength of the business (Collier 2015).

Part 2:

As per the theory of liquidity preference, a given amount of money at present is more

preferable to an individual rather than a certain period of time hence, and to compensate that

certain amount of consideration is paid, that consideration is known as the time value of money.

In cash of annuity the cash flows arises on a given frequency of time. Every investment options

require investment at present but returns will be generated in future for a given number of years.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 14

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.