ACC91210 Finance for Managers: Investment Risk & Return Case Study

VerifiedAdded on 2023/04/04

|6

|1178

|391

Case Study

AI Summary

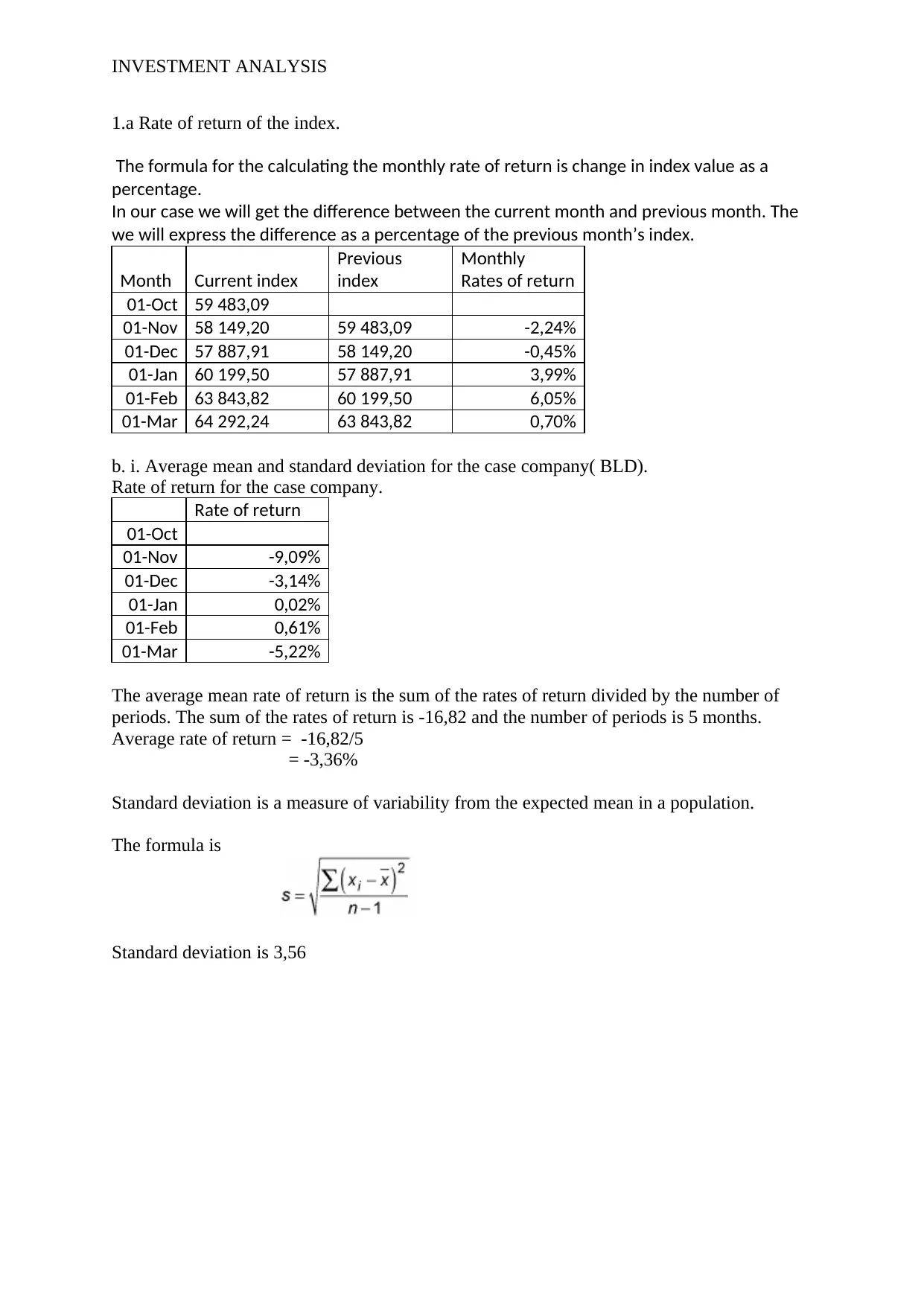

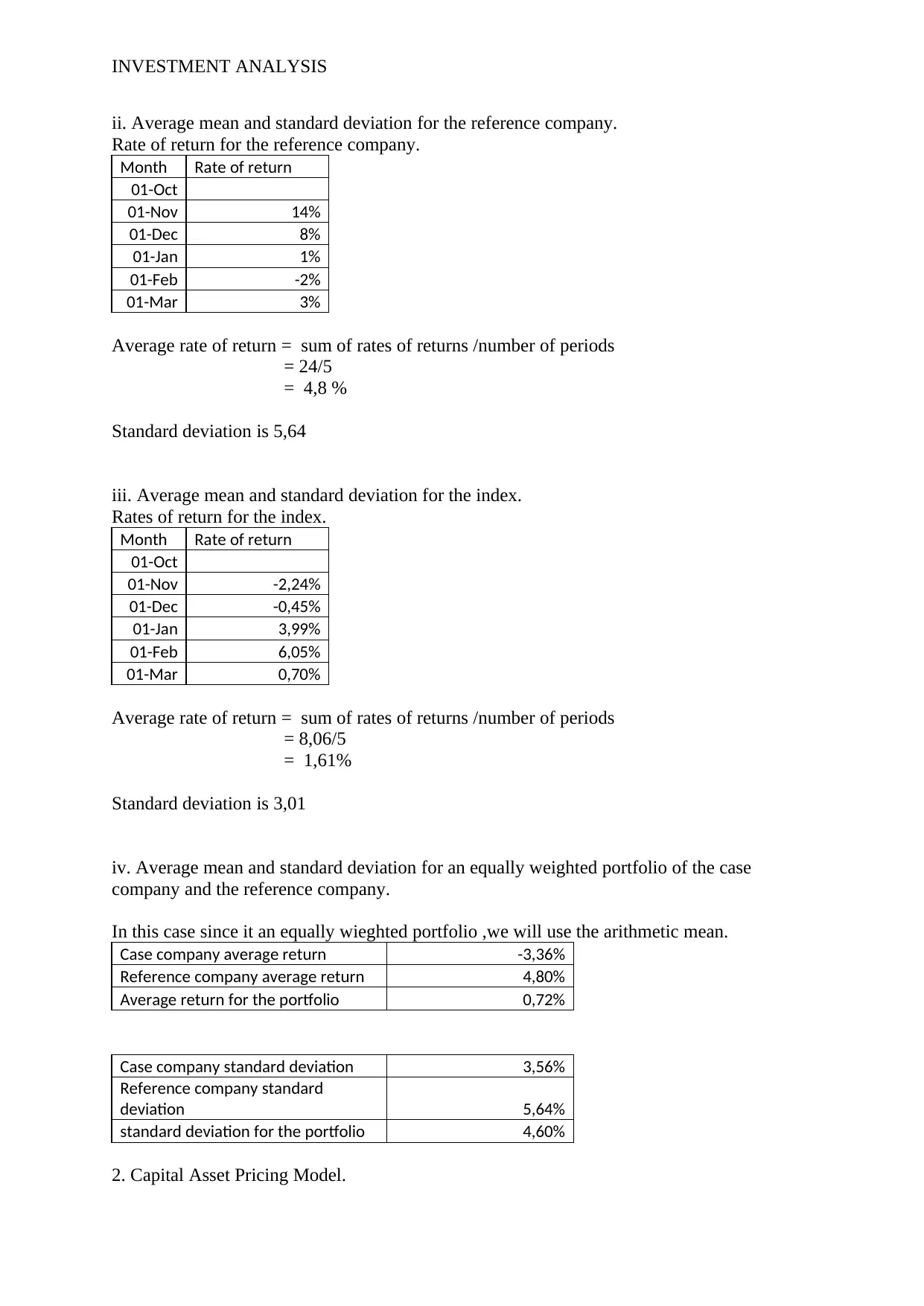

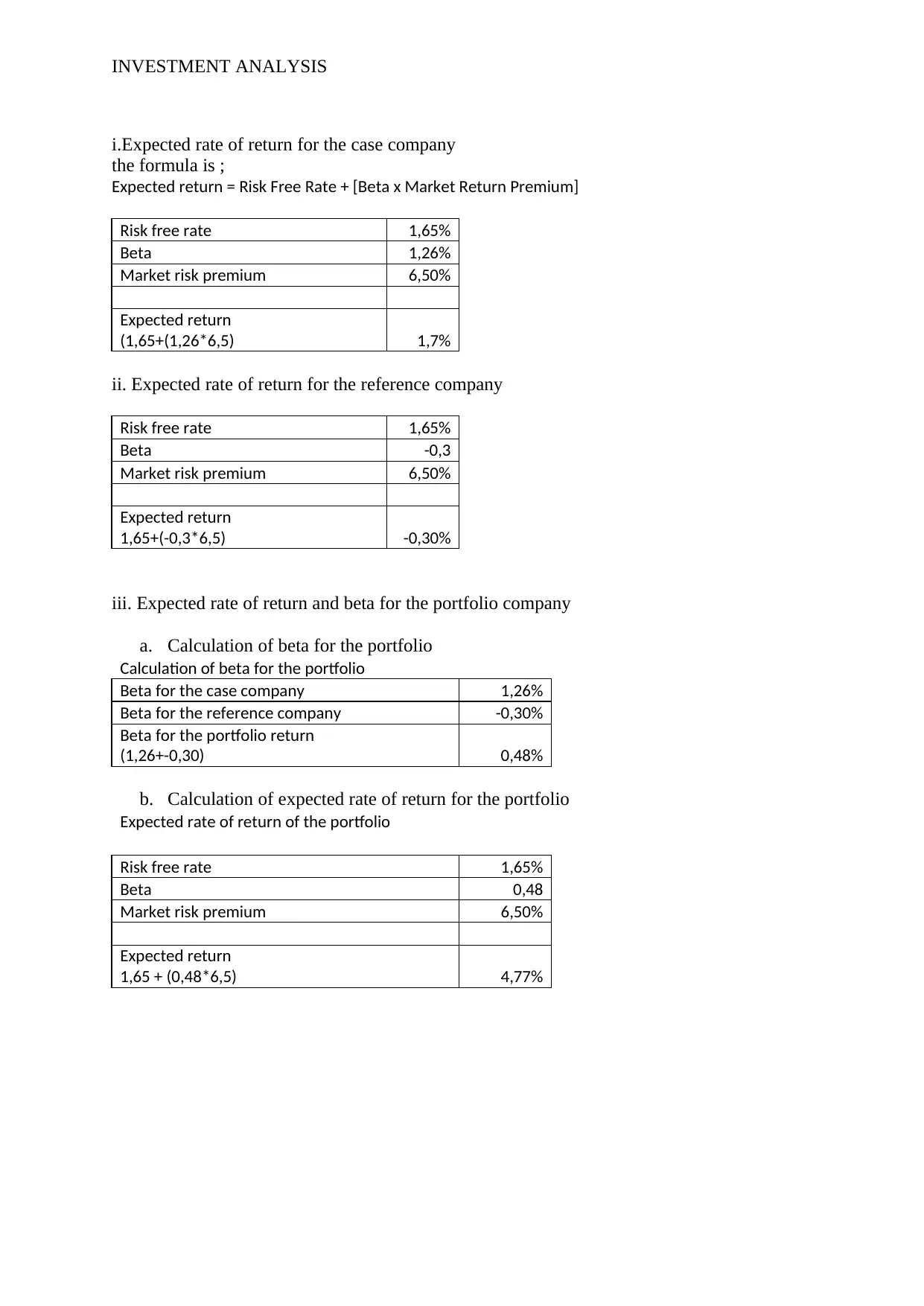

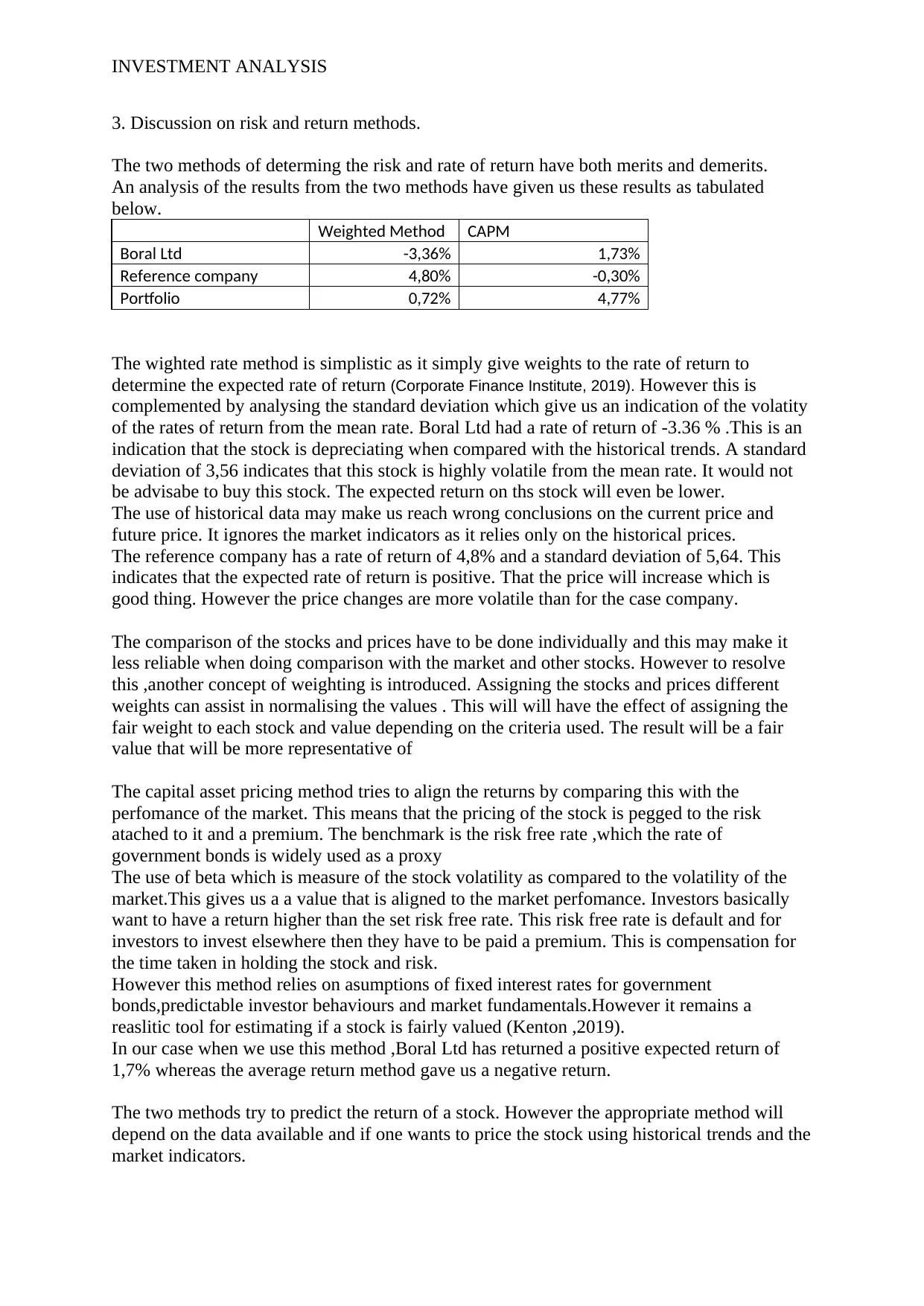

This case study provides an investment analysis of a case company (Boral Ltd) and a reference company, employing both weighted rate and Capital Asset Pricing Model (CAPM) methods to determine risk and expected rates of return. The analysis involves calculating monthly rates of return, average mean rates, and standard deviations for each company and a weighted portfolio. The CAPM is used to calculate expected rates of return based on risk-free rates, beta, and market risk premium. The study discusses the merits and demerits of both methods, highlighting that the weighted rate method is simplistic, while CAPM relies on assumptions of fixed interest rates and predictable market behavior. The results from both methods are compared, and the study concludes that the appropriate method depends on the available data and whether one wants to price the stock using historical trends or market indicators. Desklib provides access to similar solved assignments and resources for students.

1 out of 6

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.