Finance for Managers: Cochlear Capital Structure and Capital Budgeting

VerifiedAdded on 2023/03/17

|20

|3030

|63

Report

AI Summary

This report provides a comprehensive financial analysis of Cochlear Limited, focusing on its capital structure and payout policies from 2016 to 2018. The analysis utilizes various financial ratios, including debt ratio, equity ratio, and dividend payout ratio, to evaluate the company's financial health and dividend distribution strategy. Additionally, the report includes a capital budgeting case study for OnePack Limited, evaluating a proposed commercial scale plant investment. The capital budgeting analysis employs net present value (NPV), internal rate of return (IRR), payback period, and profitability index to assess the project's feasibility, along with sensitivity analysis to account for different scenarios. Based on the findings, the report offers recommendations regarding the investment decision for OnePack Limited.

Running head: FINANCE FOR MANAGERS

Finance for Managers

Name of the Student:

Name of the University:

Author’s Note:

Course ID:

Finance for Managers

Name of the Student:

Name of the University:

Author’s Note:

Course ID:

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

1FINANCE FOR MANAGERS

Table of Contents

Introduction:...............................................................................................................................2

Task 1: Capital Structure and Payout Policy Analysis...............................................................2

Quantitative analysis:.............................................................................................................2

Qualitative analysis:...............................................................................................................5

Task 2: Capital Budgeting Task.................................................................................................5

1. Explanation of the chosen methods:..................................................................................6

2. Inputs and assumptions made:...........................................................................................7

3. Summary of findings:.........................................................................................................8

4. Sensitivity analysis:............................................................................................................9

5. Recommendations:.............................................................................................................9

6. Further or follow-up matters:.............................................................................................9

Conclusion:................................................................................................................................9

References:...............................................................................................................................11

Appendices:..............................................................................................................................13

Table of Contents

Introduction:...............................................................................................................................2

Task 1: Capital Structure and Payout Policy Analysis...............................................................2

Quantitative analysis:.............................................................................................................2

Qualitative analysis:...............................................................................................................5

Task 2: Capital Budgeting Task.................................................................................................5

1. Explanation of the chosen methods:..................................................................................6

2. Inputs and assumptions made:...........................................................................................7

3. Summary of findings:.........................................................................................................8

4. Sensitivity analysis:............................................................................................................9

5. Recommendations:.............................................................................................................9

6. Further or follow-up matters:.............................................................................................9

Conclusion:................................................................................................................................9

References:...............................................................................................................................11

Appendices:..............................................................................................................................13

2FINANCE FOR MANAGERS

Introduction:

The current assignment intends to provide an in-depth analysis of the capital structure

payout policy of Cochlear Limited. For this analysis, the aspects considered include the

capital structure policy of the organisation based on current and historical data and its

theoretical evaluation. The second section of the assignment consists of preparing a memo for

the CEO of OnePack Limited, which is operating in the packaged food industry. The

organisation is planning to undertake a decision regarding the development of a commercial

sale plant. In order to assist in the decision-making process, different capital budgeting

techniques have been used that mainly comprise of net present value, internal rate of return,

payback period and profitability index. For better evaluation of the concerned project,

sensitivity analysis has been used as well based on which final recommendation has been

provided to the CEO of OnePack Limited.

Task 1: Capital Structure and Payout Policy Analysis

For analysing the capital structure and payout policy of Cochlear Limited, the data of

the past three years have been taken into consideration. Moreover, certain ratios have been

used for evaluating the policies and they primarily include debt ratio, equity ratio, debt to

equity ratio and dividend payout ratio. The results of these ratios would be evaluated and they

would be supported by adequate theoretical justifications in the following sections.

Quantitative analysis:

As discussed above, there are four ratios used for analysing the capital structure and

payout policies of Cochlear Limited and they are evaluated briefly as follows:

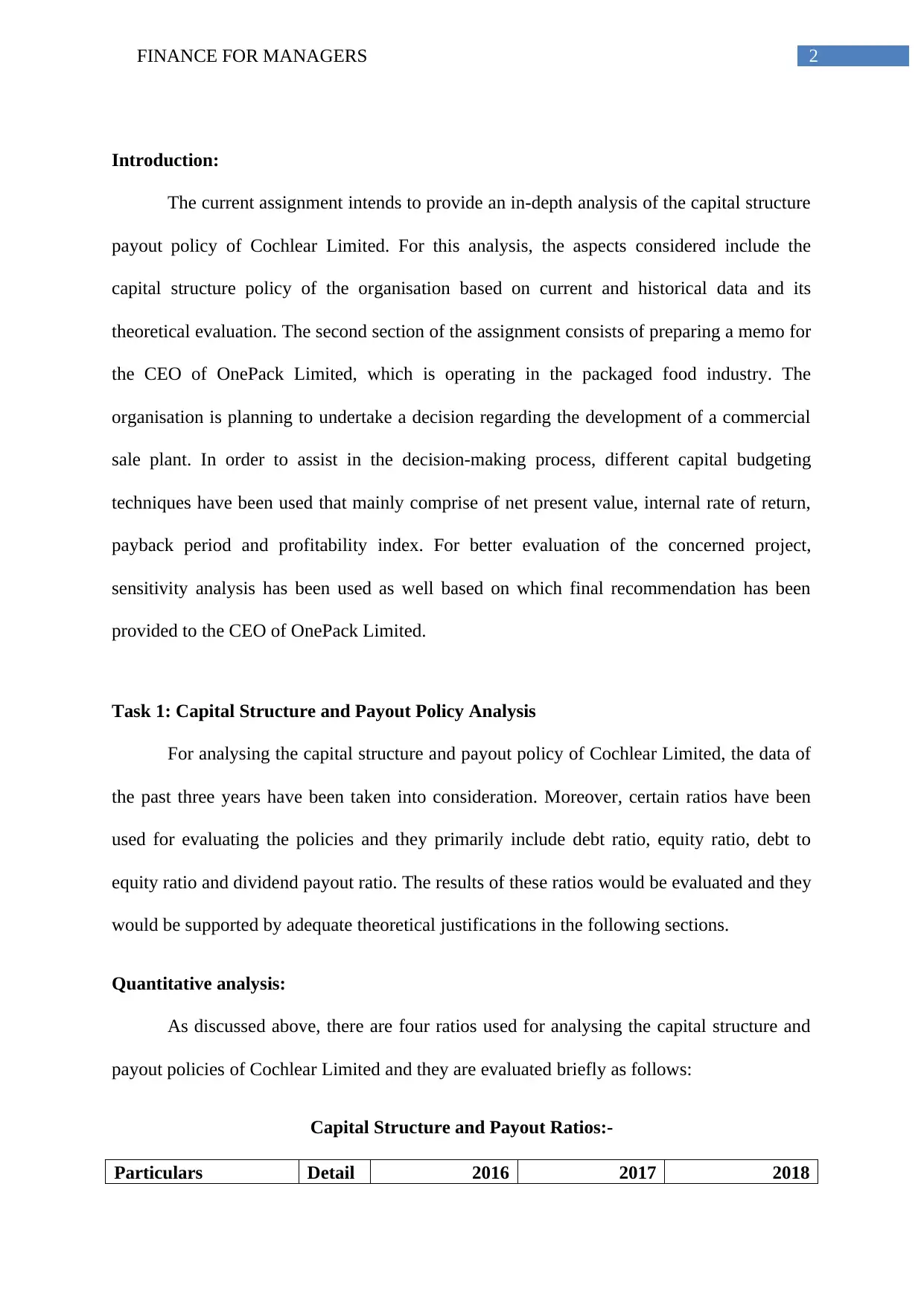

Capital Structure and Payout Ratios:-

Particulars Detail 2016 2017 2018

Introduction:

The current assignment intends to provide an in-depth analysis of the capital structure

payout policy of Cochlear Limited. For this analysis, the aspects considered include the

capital structure policy of the organisation based on current and historical data and its

theoretical evaluation. The second section of the assignment consists of preparing a memo for

the CEO of OnePack Limited, which is operating in the packaged food industry. The

organisation is planning to undertake a decision regarding the development of a commercial

sale plant. In order to assist in the decision-making process, different capital budgeting

techniques have been used that mainly comprise of net present value, internal rate of return,

payback period and profitability index. For better evaluation of the concerned project,

sensitivity analysis has been used as well based on which final recommendation has been

provided to the CEO of OnePack Limited.

Task 1: Capital Structure and Payout Policy Analysis

For analysing the capital structure and payout policy of Cochlear Limited, the data of

the past three years have been taken into consideration. Moreover, certain ratios have been

used for evaluating the policies and they primarily include debt ratio, equity ratio, debt to

equity ratio and dividend payout ratio. The results of these ratios would be evaluated and they

would be supported by adequate theoretical justifications in the following sections.

Quantitative analysis:

As discussed above, there are four ratios used for analysing the capital structure and

payout policies of Cochlear Limited and they are evaluated briefly as follows:

Capital Structure and Payout Ratios:-

Particulars Detail 2016 2017 2018

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

3FINANCE FOR MANAGERS

s

Total assets A $ 957,363,000 $ 1,136,300,000 $ 1,156,900,000

Total liabilities B $ 508,806,000 $ 592,700,000 $ 546,100,000

Total equity C $ 448,557,000 $ 543,600,000 $ 610,800,000

Dividend per share D $ 2.30 $ 2.70 $ 3.00

Earnings per share E $ 3.31 $ 3.90 $ 4.27

Debt ratio B/A 0.53 0.52 0.47

Equity ratio C/A 0.47 0.48 0.53

Debt to equity ratio B/C 1.13 1.09 0.89

Dividend payout ratio D/E 69.49% 69.23% 70.26%

Table 1: Capital structure and payout ratios of Cochlear Limited for the years 2016-

2018

(Source: Cochlear.com 2019)

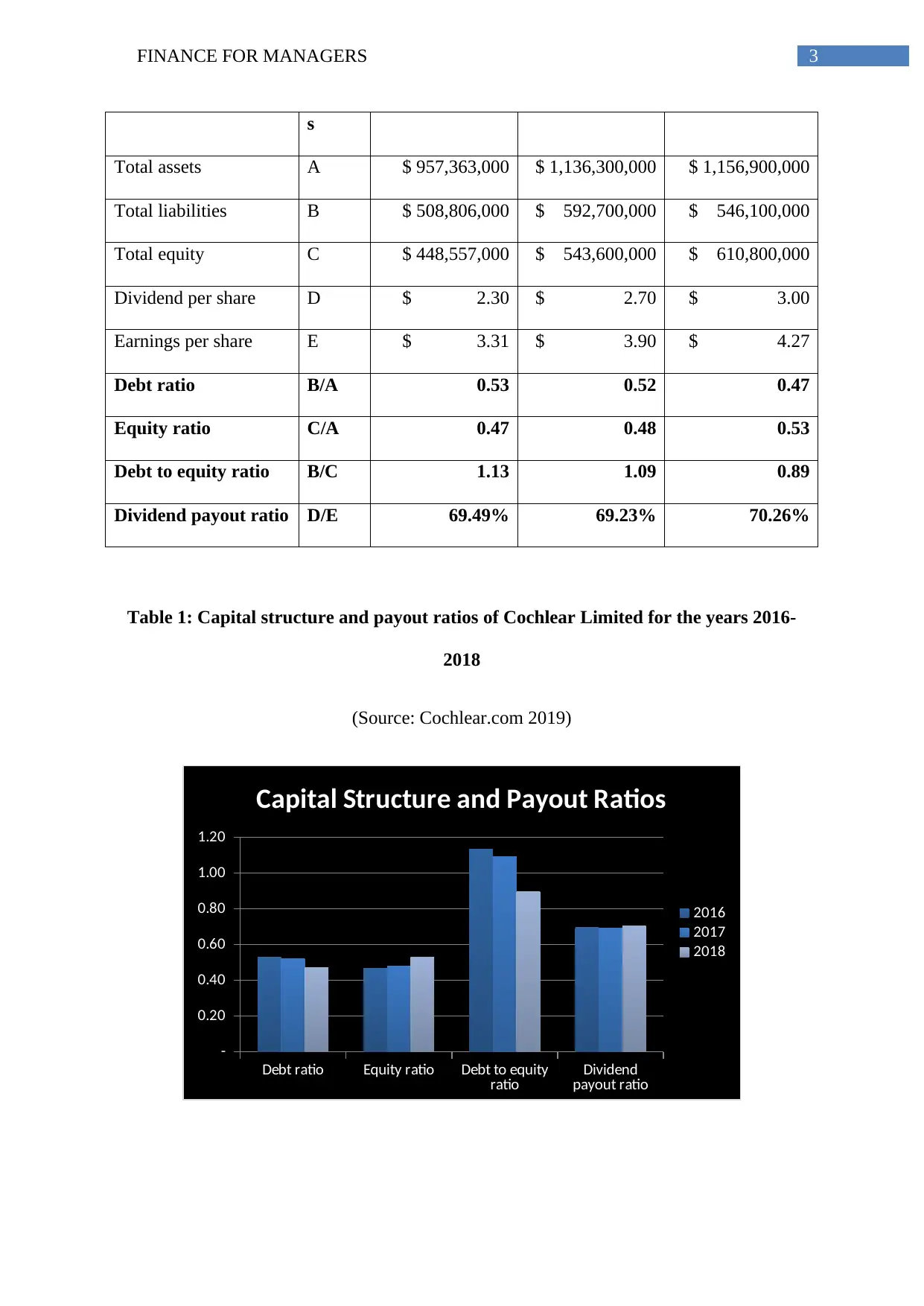

Debt ratio Equity ratio Debt to equity

ratio Dividend

payout ratio

-

0.20

0.40

0.60

0.80

1.00

1.20

Capital Structure and Payout Ratios

2016

2017

2018

s

Total assets A $ 957,363,000 $ 1,136,300,000 $ 1,156,900,000

Total liabilities B $ 508,806,000 $ 592,700,000 $ 546,100,000

Total equity C $ 448,557,000 $ 543,600,000 $ 610,800,000

Dividend per share D $ 2.30 $ 2.70 $ 3.00

Earnings per share E $ 3.31 $ 3.90 $ 4.27

Debt ratio B/A 0.53 0.52 0.47

Equity ratio C/A 0.47 0.48 0.53

Debt to equity ratio B/C 1.13 1.09 0.89

Dividend payout ratio D/E 69.49% 69.23% 70.26%

Table 1: Capital structure and payout ratios of Cochlear Limited for the years 2016-

2018

(Source: Cochlear.com 2019)

Debt ratio Equity ratio Debt to equity

ratio Dividend

payout ratio

-

0.20

0.40

0.60

0.80

1.00

1.20

Capital Structure and Payout Ratios

2016

2017

2018

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

4FINANCE FOR MANAGERS

Figure 1: Capital structure and payout ratios of Cochlear Limited for the years 2016-

2018

(Source: Cochlear.com 2019)

Debt ratio denotes the proportion of assets of an organisation, which is funded by

loans and other borrowings (Robb and Robinson 2014). In case of Cochlear Limited, it could

be seen that the debt ratio has fallen slightly from 0.53 in 2016 to 0.52 in 2017 and the

decline is further inherent to 0.47 in 2018. The lowering ratio implies sound and stable

business having the potential of longevity for Cochlear Limited. Moreover, the ratio below

0.5 is considered as less risky, as the organisation has above twice assets compared to

liabilities.

On the other hand, equity ratio denotes the proportion of assets of an organisation,

which is funded by the shareholders and the investors (Graham, Leary and Roberts 2015).

Contrary to debt ratio, equity ratio of Cochlear Limited is observed to increase from 0.47 in

2016 to 0.48 in 2018 and further increase could be observed to 0.53 in 2018. This clearly

implies that the organisation has focused on raising more funds through debt for minimising

its solvency risk.

Debt to equity ratio denotes the proportion of company financing, which is coming

from the investors and the creditors. This ratio is observed to decline from 1.13 in 2016 to

0.89 in 2018 implying stable financial position for Cochlear Limited. In addition, this ratio

implies that the investors have more stakes in Cochlear Limited than the creditors and thus,

the organisation is perceived as less risky from the perspectives of both the creditors and the

investors.

Figure 1: Capital structure and payout ratios of Cochlear Limited for the years 2016-

2018

(Source: Cochlear.com 2019)

Debt ratio denotes the proportion of assets of an organisation, which is funded by

loans and other borrowings (Robb and Robinson 2014). In case of Cochlear Limited, it could

be seen that the debt ratio has fallen slightly from 0.53 in 2016 to 0.52 in 2017 and the

decline is further inherent to 0.47 in 2018. The lowering ratio implies sound and stable

business having the potential of longevity for Cochlear Limited. Moreover, the ratio below

0.5 is considered as less risky, as the organisation has above twice assets compared to

liabilities.

On the other hand, equity ratio denotes the proportion of assets of an organisation,

which is funded by the shareholders and the investors (Graham, Leary and Roberts 2015).

Contrary to debt ratio, equity ratio of Cochlear Limited is observed to increase from 0.47 in

2016 to 0.48 in 2018 and further increase could be observed to 0.53 in 2018. This clearly

implies that the organisation has focused on raising more funds through debt for minimising

its solvency risk.

Debt to equity ratio denotes the proportion of company financing, which is coming

from the investors and the creditors. This ratio is observed to decline from 1.13 in 2016 to

0.89 in 2018 implying stable financial position for Cochlear Limited. In addition, this ratio

implies that the investors have more stakes in Cochlear Limited than the creditors and thus,

the organisation is perceived as less risky from the perspectives of both the creditors and the

investors.

5FINANCE FOR MANAGERS

Dividend payout ratio signifies the proportion of net profit distributed to the

shareholders as dividends during the period (Faccio and Xu 2015). This ratio has increased

slightly from 69.49% in 2016 to 70.26% in 2018, which implies that the organisation has

focused more on paying dividends to its shareholders.

Based on the above quantitative analysis, improvements could be observed in the

capital structure and dividend payout policy of Cochlear Limited from 2016 to 2018.

Qualitative analysis:

According to the Modigliani and Miller theorem of capital structure, there is no

importance of debt in the capital structure of an organisation. This statement is based on two

assumptions, which are provided as follows:

There is no impact of financing structure on cash flows generated by an organisation.

Financial markets are perfect because there is no trading cost (Öztekin 2015).

However, in reality, if there is absence of any financial leverage, the weighted average

cost of capital would remain the same. Moreover, if the managers of Cochlear Limited

choose an inappropriate capital structure, it could have severe adverse consequences and

hence, one of the assumptions of the Modigliani and Miller theorem would be violated.

Dividend policy could be defined as the policy, which an organisation utilises for

structuring its dividend payment to the shareholders. In case of Cochlear Limited, the

dividend policy is observed to be constant, as it is distributing a fixed portion of its earnings

in the form of dividends each year. Thus, it is following a constant dividend policy, in which

the investors are encountering overall volatility of the earnings of the organisation (Kurshev

Strebulaev 2015).

Dividend payout ratio signifies the proportion of net profit distributed to the

shareholders as dividends during the period (Faccio and Xu 2015). This ratio has increased

slightly from 69.49% in 2016 to 70.26% in 2018, which implies that the organisation has

focused more on paying dividends to its shareholders.

Based on the above quantitative analysis, improvements could be observed in the

capital structure and dividend payout policy of Cochlear Limited from 2016 to 2018.

Qualitative analysis:

According to the Modigliani and Miller theorem of capital structure, there is no

importance of debt in the capital structure of an organisation. This statement is based on two

assumptions, which are provided as follows:

There is no impact of financing structure on cash flows generated by an organisation.

Financial markets are perfect because there is no trading cost (Öztekin 2015).

However, in reality, if there is absence of any financial leverage, the weighted average

cost of capital would remain the same. Moreover, if the managers of Cochlear Limited

choose an inappropriate capital structure, it could have severe adverse consequences and

hence, one of the assumptions of the Modigliani and Miller theorem would be violated.

Dividend policy could be defined as the policy, which an organisation utilises for

structuring its dividend payment to the shareholders. In case of Cochlear Limited, the

dividend policy is observed to be constant, as it is distributing a fixed portion of its earnings

in the form of dividends each year. Thus, it is following a constant dividend policy, in which

the investors are encountering overall volatility of the earnings of the organisation (Kurshev

Strebulaev 2015).

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

6FINANCE FOR MANAGERS

Task 2: Capital Budgeting Task

Memorandum

To,

The CEO,

OnePack Limited

From: The Manager

Date: 26th May 2019

Subject: Evaluation of the proposed investment

The memo is prepared with the goal for aiding the CEO of OnePack Limited in

undertaking the final decision regarding whether to invest or not in the concerned project.

Currently, the organisation is experiencing an issue in deciding whether to develop a

commercial scale plant along with producing recycled sachet plastic for usage in packaging

its own products. Therefore, it is essential to analyse the probable aspects before undertaking

the final decision.

1. Explanation of the chosen methods:

In order to ascertain the viability of the proposed project, the capital budgeting

methods used include net present value, internal rate of return, payback period and

profitability index. It has been identified that a company is prone to certain uses like

maintaining the motivation level of the staffs or obtaining materials from suppliers in case of

failure of making timely payments although they have considerable amount of profit (Andor,

Mohanty and Toth 2015). Therefore, annual cash flows of the proposed project are computed

for determining the cash flow position before making the final decision.

Task 2: Capital Budgeting Task

Memorandum

To,

The CEO,

OnePack Limited

From: The Manager

Date: 26th May 2019

Subject: Evaluation of the proposed investment

The memo is prepared with the goal for aiding the CEO of OnePack Limited in

undertaking the final decision regarding whether to invest or not in the concerned project.

Currently, the organisation is experiencing an issue in deciding whether to develop a

commercial scale plant along with producing recycled sachet plastic for usage in packaging

its own products. Therefore, it is essential to analyse the probable aspects before undertaking

the final decision.

1. Explanation of the chosen methods:

In order to ascertain the viability of the proposed project, the capital budgeting

methods used include net present value, internal rate of return, payback period and

profitability index. It has been identified that a company is prone to certain uses like

maintaining the motivation level of the staffs or obtaining materials from suppliers in case of

failure of making timely payments although they have considerable amount of profit (Andor,

Mohanty and Toth 2015). Therefore, annual cash flows of the proposed project are computed

for determining the cash flow position before making the final decision.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

7FINANCE FOR MANAGERS

On the other hand, the capital budgeting techniques are considered as extremely

useful tools for analysing the profitability of proposed investment. This is because these

methods consider cash flows along with risk and return position of the organisation (Rossi

2014). Finally, with the help of NPV, it becomes possible for any organisation to increase its

value.

2. Inputs and assumptions made:

Base case:

It has been identified that OnePack Limited needs to invest $30,000,000 on this

project for purchasing plant and equipment, which would have a useful life of six years with

no residual value after the project completion. The revenue is expected to grow by 2% per

year and there would be further growth in revenue by 2.5% owing to investment in marketing

activity over the initial forecasts. The variable costs are expected to rise by 2% from the

second year; however, there would be decline of 10% on the current forecasts owing to

energy efficiency program. For financing the equipment, OnePack Limited has to obtain bank

loan resulted in interest costs of $1,200,000 million per annum. However, it is not considered

in the cash flow calculation, since it would double count the financing cost of investment (De

Andrés, De Fuente and San Martín 2015). Moreover, depreciation expense is deducted from

revenue for computing net income; however, it is added back with net income for computing

the yearly cash flows.

Optimistic case and pessimistic case:

All the above assumptions would remain the same in the two cases, except certain

changes in the value drivers, which are stated as follows:

2% increase in revenue for optimistic case and 2% decrease in pessimistic case

On the other hand, the capital budgeting techniques are considered as extremely

useful tools for analysing the profitability of proposed investment. This is because these

methods consider cash flows along with risk and return position of the organisation (Rossi

2014). Finally, with the help of NPV, it becomes possible for any organisation to increase its

value.

2. Inputs and assumptions made:

Base case:

It has been identified that OnePack Limited needs to invest $30,000,000 on this

project for purchasing plant and equipment, which would have a useful life of six years with

no residual value after the project completion. The revenue is expected to grow by 2% per

year and there would be further growth in revenue by 2.5% owing to investment in marketing

activity over the initial forecasts. The variable costs are expected to rise by 2% from the

second year; however, there would be decline of 10% on the current forecasts owing to

energy efficiency program. For financing the equipment, OnePack Limited has to obtain bank

loan resulted in interest costs of $1,200,000 million per annum. However, it is not considered

in the cash flow calculation, since it would double count the financing cost of investment (De

Andrés, De Fuente and San Martín 2015). Moreover, depreciation expense is deducted from

revenue for computing net income; however, it is added back with net income for computing

the yearly cash flows.

Optimistic case and pessimistic case:

All the above assumptions would remain the same in the two cases, except certain

changes in the value drivers, which are stated as follows:

2% increase in revenue for optimistic case and 2% decrease in pessimistic case

8FINANCE FOR MANAGERS

2% additional growth in revenue owing to marketing costs and 2% lower revenue

growth for optimistic and pessimistic cases respectively

There would no increase in variable costs and reduction is expected to rise further by

12% for optimistic case and variable costs would rise to 4% and decline is reduced to

8% for pessimistic case.

3. Summary of findings:

The outcomes of the capital budgeting techniques are presented in the form of tables

for the base case (Refer to Appendices, Appendix 1). From the tables, it could be clearly seen

that the net present value (NPV) of the proposed project is computed as $1,414,456,128. In

this context, it is necessary to mention that the higher the NPV of a project, the better it is in

terms of investment (Daunfeldt and Hartwig 2014). Thus, from the perspective of NPV, the

concerned project would fetch profits to OnePack Limited.

Internal rate of return (IRR) assists in determining the overall rate of return on

investment and if it is higher than the cost of capital, the project is feasible to be undertaken

(Chittenden and Derregia 2015). In this case, the IRR is computed as 795%, which is

significantly higher than the cost of capital of 9%. Thus, in terms of IRR, the project would

maximise overall return on investment for OnePack Limited.

Payback period is used for finding out the amount of time required for recouping the

initial investment made in a project (Rossi 2015). In this case, the payback period is

computed as 0.13 years and the economic life of the project is 6 years. This implies that

OnePack Limited would be able to recover its initial investment of $35,450,000 even before

the completion of the first year; thereby, denoting the feasibility of the project.

Profitability index (PI) denotes the ratio of payoff to investment of any particular

project and if it has value of above 1, it implies that the project would yield significant

2% additional growth in revenue owing to marketing costs and 2% lower revenue

growth for optimistic and pessimistic cases respectively

There would no increase in variable costs and reduction is expected to rise further by

12% for optimistic case and variable costs would rise to 4% and decline is reduced to

8% for pessimistic case.

3. Summary of findings:

The outcomes of the capital budgeting techniques are presented in the form of tables

for the base case (Refer to Appendices, Appendix 1). From the tables, it could be clearly seen

that the net present value (NPV) of the proposed project is computed as $1,414,456,128. In

this context, it is necessary to mention that the higher the NPV of a project, the better it is in

terms of investment (Daunfeldt and Hartwig 2014). Thus, from the perspective of NPV, the

concerned project would fetch profits to OnePack Limited.

Internal rate of return (IRR) assists in determining the overall rate of return on

investment and if it is higher than the cost of capital, the project is feasible to be undertaken

(Chittenden and Derregia 2015). In this case, the IRR is computed as 795%, which is

significantly higher than the cost of capital of 9%. Thus, in terms of IRR, the project would

maximise overall return on investment for OnePack Limited.

Payback period is used for finding out the amount of time required for recouping the

initial investment made in a project (Rossi 2015). In this case, the payback period is

computed as 0.13 years and the economic life of the project is 6 years. This implies that

OnePack Limited would be able to recover its initial investment of $35,450,000 even before

the completion of the first year; thereby, denoting the feasibility of the project.

Profitability index (PI) denotes the ratio of payoff to investment of any particular

project and if it has value of above 1, it implies that the project would yield significant

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

9FINANCE FOR MANAGERS

benefits to the organisation (Bierman Jr and Smidt 2014). In this case, PI is computed as

40.90, which denotes that the project would result in significant benefits for OnePack

Limited.

4. Sensitivity analysis:

The outcomes of the capital budgeting techniques are presented in the form of tables

for the optimistic case and the pessimistic case (Refer to Appendices, Appendix 2 and

Appendix 3). For optimistic case, there has been increase in all the above capital budgeting

techniques, except payback period owing to the fact that this method ignores the time value

of money (Wnuk-Pel 2014). On the other hand, despite the fall in the above capital budgeting

techniques except payback period, all values are well above the ideal standard and hence,

they imply the feasibility of the project for OnePack Limited.

5. Recommendations:

Based on the above analyses, it has been found that the significant generation of

expected revenue would be able to offset the project costs and initial investments by a

significant margin. This has been further validated with the use of capital budgeting

techniques and therefore, it is recommended to proceed with the project for increasing its

profitability in future.

6. Further or follow-up matters:

There are certain uncertainties associated with a project, which mainly interruptions

and delays and the quality of materials required for the project. For avoiding any

interruptions and delays, a project team needs to be formed and there should be appropriate

delegation of authority to the respective personnel (Nurullah and Kengatharan 2015). In order

to ensure material quality, a special team has to be formed that would visit the sites of the

supplier by conducting frequent audits (Schlegel, Frank and Britzelmaier 2016).

benefits to the organisation (Bierman Jr and Smidt 2014). In this case, PI is computed as

40.90, which denotes that the project would result in significant benefits for OnePack

Limited.

4. Sensitivity analysis:

The outcomes of the capital budgeting techniques are presented in the form of tables

for the optimistic case and the pessimistic case (Refer to Appendices, Appendix 2 and

Appendix 3). For optimistic case, there has been increase in all the above capital budgeting

techniques, except payback period owing to the fact that this method ignores the time value

of money (Wnuk-Pel 2014). On the other hand, despite the fall in the above capital budgeting

techniques except payback period, all values are well above the ideal standard and hence,

they imply the feasibility of the project for OnePack Limited.

5. Recommendations:

Based on the above analyses, it has been found that the significant generation of

expected revenue would be able to offset the project costs and initial investments by a

significant margin. This has been further validated with the use of capital budgeting

techniques and therefore, it is recommended to proceed with the project for increasing its

profitability in future.

6. Further or follow-up matters:

There are certain uncertainties associated with a project, which mainly interruptions

and delays and the quality of materials required for the project. For avoiding any

interruptions and delays, a project team needs to be formed and there should be appropriate

delegation of authority to the respective personnel (Nurullah and Kengatharan 2015). In order

to ensure material quality, a special team has to be formed that would visit the sites of the

supplier by conducting frequent audits (Schlegel, Frank and Britzelmaier 2016).

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

10FINANCE FOR MANAGERS

Conclusion:

It is apparent from the above discussion that Cochlear Limited follows appropriate

capital structure and constant dividend policy. On the other hand, the use of capital budgeting

techniques suggesta that OnePack Limited should undertake the project for maximising its

profitability.

Conclusion:

It is apparent from the above discussion that Cochlear Limited follows appropriate

capital structure and constant dividend policy. On the other hand, the use of capital budgeting

techniques suggesta that OnePack Limited should undertake the project for maximising its

profitability.

11FINANCE FOR MANAGERS

References:

Andor, G., Mohanty, S.K. and Toth, T., 2015. Capital budgeting practices: A survey of

Central and Eastern European firms. Emerging Markets Review, 23, pp.148-172.

Bierman Jr, H. and Smidt, S., 2014. Advanced capital budgeting: Refinements in the

economic analysis of investment projects. Routledge.

Chittenden, F. and Derregia, M., 2015. Uncertainty, irreversibility and the use of ‘rules of

thumb’in capital budgeting. The British Accounting Review, 47(3), pp.225-236.

Cochlear.com., 2019. [online] Available at: https://www.cochlear.com/43d56bcc-d510-4a20-

ab70-6208fa5af77e/en_annualreport2018_cochlear2018annualreport_5.69mb.pdf?

MOD=AJPERES&CONVERT_TO=url&CACHEID=ROOTWORKSPACE-

43d56bcc-d510-4a20-ab70-6208fa5af77e-mkRS5RK [Accessed 26 May 2019].

Daunfeldt, S.O. and Hartwig, F., 2014. What determines the use of capital budgeting

methods?: Evidence from Swedish listed companies. Journal of Finance and

Economics, 2(4), pp.101-112.

De Andrés, P., De Fuente, G. and San Martín, P., 2015. Capital budgeting practices in

Spain. BRQ Business Research Quarterly, 18(1), pp.37-56.

Faccio, M. and Xu, J., 2015. Taxes and capital structure. Journal of Financial and

Quantitative Analysis, 50(3), pp.277-300.

Graham, J.R., Leary, M.T. and Roberts, M.R., 2015. A century of capital structure: The

leveraging of corporate America. Journal of Financial Economics, 118(3), pp.658-683.

Kurshev, A. and Strebulaev, I.A., 2015. Firm size and capital structure. Quarterly Journal of

Finance, 5(03), p.155-168.

References:

Andor, G., Mohanty, S.K. and Toth, T., 2015. Capital budgeting practices: A survey of

Central and Eastern European firms. Emerging Markets Review, 23, pp.148-172.

Bierman Jr, H. and Smidt, S., 2014. Advanced capital budgeting: Refinements in the

economic analysis of investment projects. Routledge.

Chittenden, F. and Derregia, M., 2015. Uncertainty, irreversibility and the use of ‘rules of

thumb’in capital budgeting. The British Accounting Review, 47(3), pp.225-236.

Cochlear.com., 2019. [online] Available at: https://www.cochlear.com/43d56bcc-d510-4a20-

ab70-6208fa5af77e/en_annualreport2018_cochlear2018annualreport_5.69mb.pdf?

MOD=AJPERES&CONVERT_TO=url&CACHEID=ROOTWORKSPACE-

43d56bcc-d510-4a20-ab70-6208fa5af77e-mkRS5RK [Accessed 26 May 2019].

Daunfeldt, S.O. and Hartwig, F., 2014. What determines the use of capital budgeting

methods?: Evidence from Swedish listed companies. Journal of Finance and

Economics, 2(4), pp.101-112.

De Andrés, P., De Fuente, G. and San Martín, P., 2015. Capital budgeting practices in

Spain. BRQ Business Research Quarterly, 18(1), pp.37-56.

Faccio, M. and Xu, J., 2015. Taxes and capital structure. Journal of Financial and

Quantitative Analysis, 50(3), pp.277-300.

Graham, J.R., Leary, M.T. and Roberts, M.R., 2015. A century of capital structure: The

leveraging of corporate America. Journal of Financial Economics, 118(3), pp.658-683.

Kurshev, A. and Strebulaev, I.A., 2015. Firm size and capital structure. Quarterly Journal of

Finance, 5(03), p.155-168.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 20

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.