Finance for Managers Project: Financial Records and Stakeholders

VerifiedAdded on 2020/07/23

|19

|6538

|38

Project

AI Summary

This finance project delves into the core aspects of financial management, covering the purpose and requirements of financial records, analyzing various financial techniques, and assessing their usefulness to stakeholders. It differentiates between management and financial accounting, explores budgetary control processes, and examines different costing methods used for product pricing. The project includes the calculation of variances from provided data and applies investment appraisal techniques, such as the Average Rate of Return (ARR) and the Payback period, to evaluate the viability of a project. The project provides a comprehensive overview of financial management, including balance sheets, income statements, cash flow statements, and statements of changes in equity. The report also analyzes the impact of financial records on stakeholders and how they are used to assess management performance. This project aims to give students a solid understanding of financial analysis, from basic principles to practical application, which is a key component of effective business management.

Finance for Managers

project

project

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Table of Contents

INTRODUCTION...........................................................................................................................1

TASK 1............................................................................................................................................1

1.1 Purpose and need of financial records..................................................................................1

1.2: Analyse the techniques required for financial information..................................................3

1.3: Analysing of usefulness to stakeholders..............................................................................4

1.4: Difference in management and financial accounting...........................................................6

1.5: Budgetary control process....................................................................................................8

1.6: Different costing methods which are used to determine product pricing..........................11

TASK 2..........................................................................................................................................12

Computation of variances ........................................................................................................12

TASK 3..........................................................................................................................................14

Calculation by using ARR and Payback period method...........................................................14

CONCLUSION..............................................................................................................................15

REFERENCES..............................................................................................................................17

INTRODUCTION...........................................................................................................................1

TASK 1............................................................................................................................................1

1.1 Purpose and need of financial records..................................................................................1

1.2: Analyse the techniques required for financial information..................................................3

1.3: Analysing of usefulness to stakeholders..............................................................................4

1.4: Difference in management and financial accounting...........................................................6

1.5: Budgetary control process....................................................................................................8

1.6: Different costing methods which are used to determine product pricing..........................11

TASK 2..........................................................................................................................................12

Computation of variances ........................................................................................................12

TASK 3..........................................................................................................................................14

Calculation by using ARR and Payback period method...........................................................14

CONCLUSION..............................................................................................................................15

REFERENCES..............................................................................................................................17

INTRODUCTION

Finance is the art to raise funds and effective allocation to attain organisation aims and

objectives. In other words, it is the branch of economics that deals with regulation of funds,

financial resources and other necessary assets of an organisation. However, financial managers

are responsible to plan and control funds of company which they are going to invest in various

projects. They are working with the objectives to make use of resources and capital so that short

and long term objectives can be achieved (Brealey and et. al., 2012). These are used for making

effective decision for making company more beneficial in future period of time. As, in each

company or organisation finance is the primary aspects which has to manage and operate in its

daily business functions.

They need to take decision in such a manner that organisation’s performance cannot get

affected. Under this report, a brief essay is prepared on the purpose and requirements of financial

records. Various techniques are used for recording financial information and its usefulness to

stakeholder. It also describe comparison among management accounting, financial accounting

and budgetary control process. Some costing methods are also used in order to determine the

product’s price. The report also covers calculation of variance from available data. Use of ARR

and Payback period as investment appraisal techniques for identifying the viability of a project i

TASK 1

1.1 Purpose and need of financial records

In an organisation, it has been seen that performance of company is elevated on the basis

of its performance that is represented through using financial records. It consists of information

related with the costs, expenses, profit and losses which are done by company during year. As, a

business enterprises it is an utmost responsibility of managers to keep record of business record

and other valuable documents for tax purposes. Keeping track of effective business transactions

and tax statements will be helpful in monitoring the financial performance of concerned

businesses (Tucker, 2011). Basically, it is important to keep company's written records for at-

least five years from the date managers lodge tax returns. Financial records are considered as

those records of profit and expenditure that are kept for tax intent. It consists of pay check

details, record of interest or dividends collected during the year and other records of tips,

bonuses, cash register receipts and credit card statements. It is a formal record of financial

1

Finance is the art to raise funds and effective allocation to attain organisation aims and

objectives. In other words, it is the branch of economics that deals with regulation of funds,

financial resources and other necessary assets of an organisation. However, financial managers

are responsible to plan and control funds of company which they are going to invest in various

projects. They are working with the objectives to make use of resources and capital so that short

and long term objectives can be achieved (Brealey and et. al., 2012). These are used for making

effective decision for making company more beneficial in future period of time. As, in each

company or organisation finance is the primary aspects which has to manage and operate in its

daily business functions.

They need to take decision in such a manner that organisation’s performance cannot get

affected. Under this report, a brief essay is prepared on the purpose and requirements of financial

records. Various techniques are used for recording financial information and its usefulness to

stakeholder. It also describe comparison among management accounting, financial accounting

and budgetary control process. Some costing methods are also used in order to determine the

product’s price. The report also covers calculation of variance from available data. Use of ARR

and Payback period as investment appraisal techniques for identifying the viability of a project i

TASK 1

1.1 Purpose and need of financial records

In an organisation, it has been seen that performance of company is elevated on the basis

of its performance that is represented through using financial records. It consists of information

related with the costs, expenses, profit and losses which are done by company during year. As, a

business enterprises it is an utmost responsibility of managers to keep record of business record

and other valuable documents for tax purposes. Keeping track of effective business transactions

and tax statements will be helpful in monitoring the financial performance of concerned

businesses (Tucker, 2011). Basically, it is important to keep company's written records for at-

least five years from the date managers lodge tax returns. Financial records are considered as

those records of profit and expenditure that are kept for tax intent. It consists of pay check

details, record of interest or dividends collected during the year and other records of tips,

bonuses, cash register receipts and credit card statements. It is a formal record of financial

1

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

transactions of activities and perspective of a business, individuals and other entities. Accurate

and reliable information is conferred in a well organised manner and in a form essay to

understand. There are mainly four types of statements which are prepared by the managers such

as:

Balance sheet: In a financial accounting, a balance sheet or records of position is detail

summary of financial transaction those are done during one accounting year (Gitman, Juchau

and Flanagan, 2015). It mainly consists of assets, liabilities and other shareholders equity at a

particular point of time. In common term it represent company's net worth.

Income statement: It is considered as one of the financial statements of company which

contains revenues and expenses incurred during a year. It is used to determine that how revenues

of company are transformed into net profit. It present financial outcome of a business for a

declared period of time.

Statement of cash-flows: In financial accounting, a cash-flows record are related with

the those transaction which are done in cash by the company. It shows cash and cash equivalent

effects on income generated by company during one financial year. It also identified cash

inflows and out flows those are received from various activities such as investing, operating and

financing.

Statement of changes in equity: It is mainly considered as a statement of retained

earnings. It is prepared in order to determine the changes for changing in the capital reserve of

the company (Fields, 2016). It is applied by sole traders, in which incomes are earned during the

period is included in starting capital balance.

Purpose of financial records:

The objective of financial records is to render information regarding financial position,

performances and other important changes happen in organisational context. It is all necessary to

have wide range of value that will be more helpful for taking effective decision making in

context to reach at a valid position. It is mostly related with those information that results with

various operations, financial position and cash-flows of organisation. Such kind of information is

necessary for company to make effective decisions in context of allocation of resources.

Requirement of using financial record: There are many prospective investors that use

financial statements in order to assess viability of a company before making any capital

investment decision. According to the financial statements, investors predict future dividends

2

and reliable information is conferred in a well organised manner and in a form essay to

understand. There are mainly four types of statements which are prepared by the managers such

as:

Balance sheet: In a financial accounting, a balance sheet or records of position is detail

summary of financial transaction those are done during one accounting year (Gitman, Juchau

and Flanagan, 2015). It mainly consists of assets, liabilities and other shareholders equity at a

particular point of time. In common term it represent company's net worth.

Income statement: It is considered as one of the financial statements of company which

contains revenues and expenses incurred during a year. It is used to determine that how revenues

of company are transformed into net profit. It present financial outcome of a business for a

declared period of time.

Statement of cash-flows: In financial accounting, a cash-flows record are related with

the those transaction which are done in cash by the company. It shows cash and cash equivalent

effects on income generated by company during one financial year. It also identified cash

inflows and out flows those are received from various activities such as investing, operating and

financing.

Statement of changes in equity: It is mainly considered as a statement of retained

earnings. It is prepared in order to determine the changes for changing in the capital reserve of

the company (Fields, 2016). It is applied by sole traders, in which incomes are earned during the

period is included in starting capital balance.

Purpose of financial records:

The objective of financial records is to render information regarding financial position,

performances and other important changes happen in organisational context. It is all necessary to

have wide range of value that will be more helpful for taking effective decision making in

context to reach at a valid position. It is mostly related with those information that results with

various operations, financial position and cash-flows of organisation. Such kind of information is

necessary for company to make effective decisions in context of allocation of resources.

Requirement of using financial record: There are many prospective investors that use

financial statements in order to assess viability of a company before making any capital

investment decision. According to the financial statements, investors predict future dividends

2

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

based on the profit disclosed under statements. It is considered as one of the important aspects of

decision making done for the purpose of increasing profit and growth.

1.2: Analyse the techniques required for financial information

In an small business organisation has a complete freedom in selecting the appropriate

techniques of handing its financial transaction than a larger one. There are so many options

available in front of company to decide how to keep track of income, expenditure and other

stocks informations (Shiller, 2013). By using actual accounting process which is more similar to

large organisation, the small business units can have the right to maintain more flexibility in an

accounting techniques. It is done while preparing a well organised reporting and recording of

financial transaction in the books of accounts so that company would able to attain its

profitability.

Cash or accrual: Businesses have the various option of using either cash or accrual

method of accounting while, recording transaction into company's books of accounts. Large

businesses required to use accrual based accounting techniques systems. But small businesses

have both the options.

Period and perpetual: The another important techniques of financial records which is

known as effective tools for small businesses. They have the option to select any one of them. A

periodic stock systems are used to record all finished product and service information when

placed in inventory. In that situation total amount remain in the accounts until a physical stocks

is not taken out of it. Basically, small scale business organisation are using this systems by taking

inventory account at once and twice in a accounting year. By this, the information about

inventory accounts are comedown to represent the actual cost of stock held by company.

Inventory techniques: It is known as an effective and important part of company. As

they account for the inventory they use to sell by selecting an stock controlling techniques. There

are various option available to the company in the form of FIFO(First in, First Out) or LIFO

(Last in, First out) and weighted average (Sandhu, Hussain and Matlay, 2012). These two

methods are used by company in order to determine its stock position with the company by

summarising opening and closing year.

Comparative financial statements analysis: With the name it is cleared that

comparative analysis provide year to year informations in order to review the financial

statements.

3

decision making done for the purpose of increasing profit and growth.

1.2: Analyse the techniques required for financial information

In an small business organisation has a complete freedom in selecting the appropriate

techniques of handing its financial transaction than a larger one. There are so many options

available in front of company to decide how to keep track of income, expenditure and other

stocks informations (Shiller, 2013). By using actual accounting process which is more similar to

large organisation, the small business units can have the right to maintain more flexibility in an

accounting techniques. It is done while preparing a well organised reporting and recording of

financial transaction in the books of accounts so that company would able to attain its

profitability.

Cash or accrual: Businesses have the various option of using either cash or accrual

method of accounting while, recording transaction into company's books of accounts. Large

businesses required to use accrual based accounting techniques systems. But small businesses

have both the options.

Period and perpetual: The another important techniques of financial records which is

known as effective tools for small businesses. They have the option to select any one of them. A

periodic stock systems are used to record all finished product and service information when

placed in inventory. In that situation total amount remain in the accounts until a physical stocks

is not taken out of it. Basically, small scale business organisation are using this systems by taking

inventory account at once and twice in a accounting year. By this, the information about

inventory accounts are comedown to represent the actual cost of stock held by company.

Inventory techniques: It is known as an effective and important part of company. As

they account for the inventory they use to sell by selecting an stock controlling techniques. There

are various option available to the company in the form of FIFO(First in, First Out) or LIFO

(Last in, First out) and weighted average (Sandhu, Hussain and Matlay, 2012). These two

methods are used by company in order to determine its stock position with the company by

summarising opening and closing year.

Comparative financial statements analysis: With the name it is cleared that

comparative analysis provide year to year informations in order to review the financial

statements.

3

Regression analysis: It is known as statistical tools which is used by company in order to

analyse a positive relationship among various variables. In case of financial statement evaluation

the dependent variables is associated with each other.

Trend analysis: It is known as trend analysis which is used to reveal the trend of product

and services related with the time passes (Bodie, 2013). It is used as statistical tools to define and

compare various observation.

Legal and organisational requirements of financial reporting:

It has been seen that most of the countries have developed their own accounting

techniques over the time and making global comparisons of institution those are facing

difficulties. To make sure uniformity and comparability among financial records formulated by

different companies. It consists of guidelines and regulation which are required to make effective

financial statements. For betterment of organisation managers need to use corrective measures in

order to prepared accurate statements that would be helpful for attaining organisational

objectives. Most of the company is using voluntarily disclose information beyond the nature of

its requirements. In the current scenario, they are reached towards standardising accounting rules

which are made on the basis of IASB(International accounting standard board). It help to

develop a particular standards that have been used by Australia, Malaysia, Canada and the

European Union. Many of the persons says that reporting system can be determine by its attitude

and behaviour of an economic agents and other managers (Embrechts, Klüppelberg and

Mikosch, 2013). The evaluation indicate that financial inflation will have huge impact over

accounting practices in which cited company are potentially facing following risks:

The maximum use of fair value of accounting systems

Credit failure recognition, and

Improper treatment for special objectives enterprises.

The above three are connected with legal obligation of reporting system that are managed

and control by business organisation.

1.3: Analysing of usefulness to stakeholders

As, it has been observed that stakeholder are those persons which are directly or

indirectly related with an organisation. A person or a team that has interest or faith in an

organisation is known to be stakeholders. It can affect or affected by the organisation policies,

objectives and other actions. Few examples of stakeholders are creditors, directors, employees,

4

analyse a positive relationship among various variables. In case of financial statement evaluation

the dependent variables is associated with each other.

Trend analysis: It is known as trend analysis which is used to reveal the trend of product

and services related with the time passes (Bodie, 2013). It is used as statistical tools to define and

compare various observation.

Legal and organisational requirements of financial reporting:

It has been seen that most of the countries have developed their own accounting

techniques over the time and making global comparisons of institution those are facing

difficulties. To make sure uniformity and comparability among financial records formulated by

different companies. It consists of guidelines and regulation which are required to make effective

financial statements. For betterment of organisation managers need to use corrective measures in

order to prepared accurate statements that would be helpful for attaining organisational

objectives. Most of the company is using voluntarily disclose information beyond the nature of

its requirements. In the current scenario, they are reached towards standardising accounting rules

which are made on the basis of IASB(International accounting standard board). It help to

develop a particular standards that have been used by Australia, Malaysia, Canada and the

European Union. Many of the persons says that reporting system can be determine by its attitude

and behaviour of an economic agents and other managers (Embrechts, Klüppelberg and

Mikosch, 2013). The evaluation indicate that financial inflation will have huge impact over

accounting practices in which cited company are potentially facing following risks:

The maximum use of fair value of accounting systems

Credit failure recognition, and

Improper treatment for special objectives enterprises.

The above three are connected with legal obligation of reporting system that are managed

and control by business organisation.

1.3: Analysing of usefulness to stakeholders

As, it has been observed that stakeholder are those persons which are directly or

indirectly related with an organisation. A person or a team that has interest or faith in an

organisation is known to be stakeholders. It can affect or affected by the organisation policies,

objectives and other actions. Few examples of stakeholders are creditors, directors, employees,

4

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

legal agencies and owners and other social community from which the business enterprise

allocate its resources. It has been seen that not all shareholders are common. A consumer can be

entitled to fair trading practices but they are not eligible to same consideration as other

employees of company are getting (Hens and Bachmann, 2011). In the business, it has been seen

that there are two types of stakeholders that are associated with the company as a part of team.

They all are fits to take participation in decision making process or further growth and

sustainable of business organisation. Internal and external stakeholder are the two part of

stakeholders.

Internal stakeholders: The are known as those people which are already related with the

administration. They have committed to serve their organisation such as managing directors,

staffs, and other parties.

External stakeholders: These are those people who are impacted by their work as

customers and other constituents. They are entities not inside a business itself but who aid about

or are struck by its action like for examples consumers, investors and other suppliers. Generally,

they are not directly the part of company (Deren, Le and Yunsen, 2012). All of them wants to

see the proper utilisation of their investments and hence, assess the management through the

financial statements. As because financial information are the most effective part of a company.

Some effective usefulness of stakeholder are as follows:

To know about total profit and losses in the business: As a part of groups they are

responsible to know that how much is the net profit and loss a company is getting from it

resources.

Total investment of capital: They have the usefulness to determine how much money is

invested by company for the betterment and to provided stability to stakeholder.

Information of assets and liabilities: They can also enhance their work by knowing

information about the total assets available with the company to meet out its liabilities.

There usefulness can also be determine by getting information about their capital

investment plan. The company must disclose all the necessary information about all capital plan

those are invested by outside customers.

Making good use of money: There usefulness can also be enhance through using good

and effective use of their money. They need to know each and every information about company

investment plans.

5

allocate its resources. It has been seen that not all shareholders are common. A consumer can be

entitled to fair trading practices but they are not eligible to same consideration as other

employees of company are getting (Hens and Bachmann, 2011). In the business, it has been seen

that there are two types of stakeholders that are associated with the company as a part of team.

They all are fits to take participation in decision making process or further growth and

sustainable of business organisation. Internal and external stakeholder are the two part of

stakeholders.

Internal stakeholders: The are known as those people which are already related with the

administration. They have committed to serve their organisation such as managing directors,

staffs, and other parties.

External stakeholders: These are those people who are impacted by their work as

customers and other constituents. They are entities not inside a business itself but who aid about

or are struck by its action like for examples consumers, investors and other suppliers. Generally,

they are not directly the part of company (Deren, Le and Yunsen, 2012). All of them wants to

see the proper utilisation of their investments and hence, assess the management through the

financial statements. As because financial information are the most effective part of a company.

Some effective usefulness of stakeholder are as follows:

To know about total profit and losses in the business: As a part of groups they are

responsible to know that how much is the net profit and loss a company is getting from it

resources.

Total investment of capital: They have the usefulness to determine how much money is

invested by company for the betterment and to provided stability to stakeholder.

Information of assets and liabilities: They can also enhance their work by knowing

information about the total assets available with the company to meet out its liabilities.

There usefulness can also be determine by getting information about their capital

investment plan. The company must disclose all the necessary information about all capital plan

those are invested by outside customers.

Making good use of money: There usefulness can also be enhance through using good

and effective use of their money. They need to know each and every information about company

investment plans.

5

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

If company reinvest all its profits: Whatever, profit generated by the company during the

year are need to be analysed by applying various tools (Besley and Brigham, 2013). It is done so

to determine whether entire profits are needed to be reinvested or to distribute it to other

shareholders as dividend.

Shareholders need financial statements to analyse their equity investments and help them

to make effective decision as to how to make use of corporate matters. There are so many tools

and techniques which are used by shareholders in order to make equity evaluation and its

importance for the analyse their stock using a variety of measurements. They are also known for

future stability which are based on decisions of the company. Shareholders are known as most

important part of stakeholder because they put wealth into the business. They are contributing as

capital in order to get some share in company's total profits.

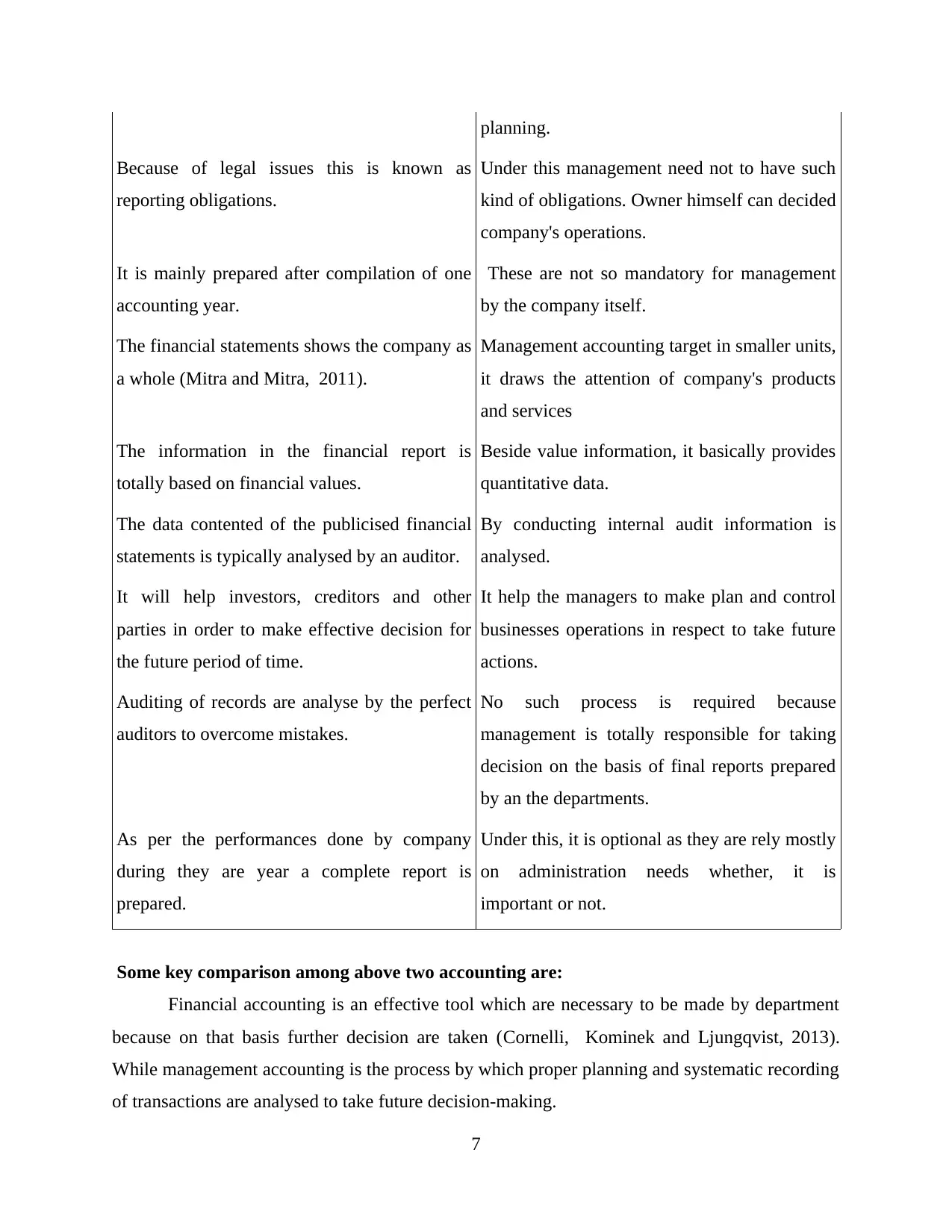

1.4: Difference in management and financial accounting

In an organisation, management accounting is related with operational reports that is only

distributed within a company. It is known as practical application of management tools use to

control and report on company health and current position. It consists of analysis, planning,

evaluation and control of various plan which is used to generate financial data in order to take

effective decision making (Pompian, 2011). Such kind of reports are basically directed to the

managers of a businesses rather than to any external business entity such as lenders or

shareholders. Whereas, financial accounting is a considered as specific branch of accounting that

keep track of a company's financial transactions. By using perfect guidelines the transaction of

business are recorded and reported in financial reports of the company. Such as income

statements and balance sheet.

Comparison among management and financial accounting

Financial accounting Management accounting

This kind of accounting is associated with a

particular laws and regulation which is in very

standardising format.

This particular accounting is formulated and

regulated by entrepreneurs. It does not have

standardising format.

These are primarily related with the past

economic information in which statements are

carried on historical data.

Under this accounting management have the

option to use future data as on assumption

basis not only historical data for the purpose of

6

year are need to be analysed by applying various tools (Besley and Brigham, 2013). It is done so

to determine whether entire profits are needed to be reinvested or to distribute it to other

shareholders as dividend.

Shareholders need financial statements to analyse their equity investments and help them

to make effective decision as to how to make use of corporate matters. There are so many tools

and techniques which are used by shareholders in order to make equity evaluation and its

importance for the analyse their stock using a variety of measurements. They are also known for

future stability which are based on decisions of the company. Shareholders are known as most

important part of stakeholder because they put wealth into the business. They are contributing as

capital in order to get some share in company's total profits.

1.4: Difference in management and financial accounting

In an organisation, management accounting is related with operational reports that is only

distributed within a company. It is known as practical application of management tools use to

control and report on company health and current position. It consists of analysis, planning,

evaluation and control of various plan which is used to generate financial data in order to take

effective decision making (Pompian, 2011). Such kind of reports are basically directed to the

managers of a businesses rather than to any external business entity such as lenders or

shareholders. Whereas, financial accounting is a considered as specific branch of accounting that

keep track of a company's financial transactions. By using perfect guidelines the transaction of

business are recorded and reported in financial reports of the company. Such as income

statements and balance sheet.

Comparison among management and financial accounting

Financial accounting Management accounting

This kind of accounting is associated with a

particular laws and regulation which is in very

standardising format.

This particular accounting is formulated and

regulated by entrepreneurs. It does not have

standardising format.

These are primarily related with the past

economic information in which statements are

carried on historical data.

Under this accounting management have the

option to use future data as on assumption

basis not only historical data for the purpose of

6

planning.

Because of legal issues this is known as

reporting obligations.

Under this management need not to have such

kind of obligations. Owner himself can decided

company's operations.

It is mainly prepared after compilation of one

accounting year.

These are not so mandatory for management

by the company itself.

The financial statements shows the company as

a whole (Mitra and Mitra, 2011).

Management accounting target in smaller units,

it draws the attention of company's products

and services

The information in the financial report is

totally based on financial values.

Beside value information, it basically provides

quantitative data.

The data contented of the publicised financial

statements is typically analysed by an auditor.

By conducting internal audit information is

analysed.

It will help investors, creditors and other

parties in order to make effective decision for

the future period of time.

It help the managers to make plan and control

businesses operations in respect to take future

actions.

Auditing of records are analyse by the perfect

auditors to overcome mistakes.

No such process is required because

management is totally responsible for taking

decision on the basis of final reports prepared

by an the departments.

As per the performances done by company

during they are year a complete report is

prepared.

Under this, it is optional as they are rely mostly

on administration needs whether, it is

important or not.

Some key comparison among above two accounting are:

Financial accounting is an effective tool which are necessary to be made by department

because on that basis further decision are taken (Cornelli, Kominek and Ljungqvist, 2013).

While management accounting is the process by which proper planning and systematic recording

of transactions are analysed to take future decision-making.

7

Because of legal issues this is known as

reporting obligations.

Under this management need not to have such

kind of obligations. Owner himself can decided

company's operations.

It is mainly prepared after compilation of one

accounting year.

These are not so mandatory for management

by the company itself.

The financial statements shows the company as

a whole (Mitra and Mitra, 2011).

Management accounting target in smaller units,

it draws the attention of company's products

and services

The information in the financial report is

totally based on financial values.

Beside value information, it basically provides

quantitative data.

The data contented of the publicised financial

statements is typically analysed by an auditor.

By conducting internal audit information is

analysed.

It will help investors, creditors and other

parties in order to make effective decision for

the future period of time.

It help the managers to make plan and control

businesses operations in respect to take future

actions.

Auditing of records are analyse by the perfect

auditors to overcome mistakes.

No such process is required because

management is totally responsible for taking

decision on the basis of final reports prepared

by an the departments.

As per the performances done by company

during they are year a complete report is

prepared.

Under this, it is optional as they are rely mostly

on administration needs whether, it is

important or not.

Some key comparison among above two accounting are:

Financial accounting is an effective tool which are necessary to be made by department

because on that basis further decision are taken (Cornelli, Kominek and Ljungqvist, 2013).

While management accounting is the process by which proper planning and systematic recording

of transactions are analysed to take future decision-making.

7

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

The information about both internal as well as external parts of businesses are

summarised under financial accounting. While, management accounting is mainly rely on

internal aspects of an organisation.

The best of both accounting is they are prepared through following proper standards

(Hein, 2012). The company can compare their position with other by using these important

tools.

1.5: Budgetary control process

Budgets: It is known as an estimation of future forecasted income and expenditure that is

going to be invested by the company. It is a financial framework for a set period of time,

generally a year. It consists of designed sales volumes and revenues, resource capacity, cost and

expenses and other cash-flows. An annual budget are used by an individuals, business

corporation, legal authorities and other types of administrations. In basic term, it is a plan to

spend company's capital over the production process. The major target of preparing budgets is to

make maximum profit with using minimum cost.

Budgetary control: It refers as a method of management control in which actual cost and

spending are differentiate with perfect planned income and related spending. It is used to

determine that, if plans are being followed in perfect manner or whether, plans required any

changes in order to attain profit for the company. It is a controlling techniques in which actual

results are compared with that of budgets (Liu and McConnell, 2013). Any changes in variances

are made huge responsibility of key people who can either have the option to workout control

action on the original budgets.

Advantages of budgetary control process:

The important of budgeting is that it is coordinates activities across other departments. It

means that it is prepared by using support of various departments.

Budgets translate strategic tasks into action. They particularly consists of resources,

revenues and other activities which is required to carry out the strategic actions for future.

It help an organisation to delivery an excellent records of departments activities.

By using an effective budgets it need to have perfect communication channel between

employees and other departments.

Disadvantage:

8

summarised under financial accounting. While, management accounting is mainly rely on

internal aspects of an organisation.

The best of both accounting is they are prepared through following proper standards

(Hein, 2012). The company can compare their position with other by using these important

tools.

1.5: Budgetary control process

Budgets: It is known as an estimation of future forecasted income and expenditure that is

going to be invested by the company. It is a financial framework for a set period of time,

generally a year. It consists of designed sales volumes and revenues, resource capacity, cost and

expenses and other cash-flows. An annual budget are used by an individuals, business

corporation, legal authorities and other types of administrations. In basic term, it is a plan to

spend company's capital over the production process. The major target of preparing budgets is to

make maximum profit with using minimum cost.

Budgetary control: It refers as a method of management control in which actual cost and

spending are differentiate with perfect planned income and related spending. It is used to

determine that, if plans are being followed in perfect manner or whether, plans required any

changes in order to attain profit for the company. It is a controlling techniques in which actual

results are compared with that of budgets (Liu and McConnell, 2013). Any changes in variances

are made huge responsibility of key people who can either have the option to workout control

action on the original budgets.

Advantages of budgetary control process:

The important of budgeting is that it is coordinates activities across other departments. It

means that it is prepared by using support of various departments.

Budgets translate strategic tasks into action. They particularly consists of resources,

revenues and other activities which is required to carry out the strategic actions for future.

It help an organisation to delivery an excellent records of departments activities.

By using an effective budgets it need to have perfect communication channel between

employees and other departments.

Disadvantage:

8

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Budget are always uncertain because, it is prepared on the basis of assumption. It is

difficult for the manages to determine positive outcome for the company.

Revision required: The biggest limitation of budgetary control is that it required regular

revision of statements that whether every thing is going in right direction of the company

(Fernandes, 2014).

Problem of co-ordination: It has been seen that without an effective coordination

company cannot be easy to get maximum results.

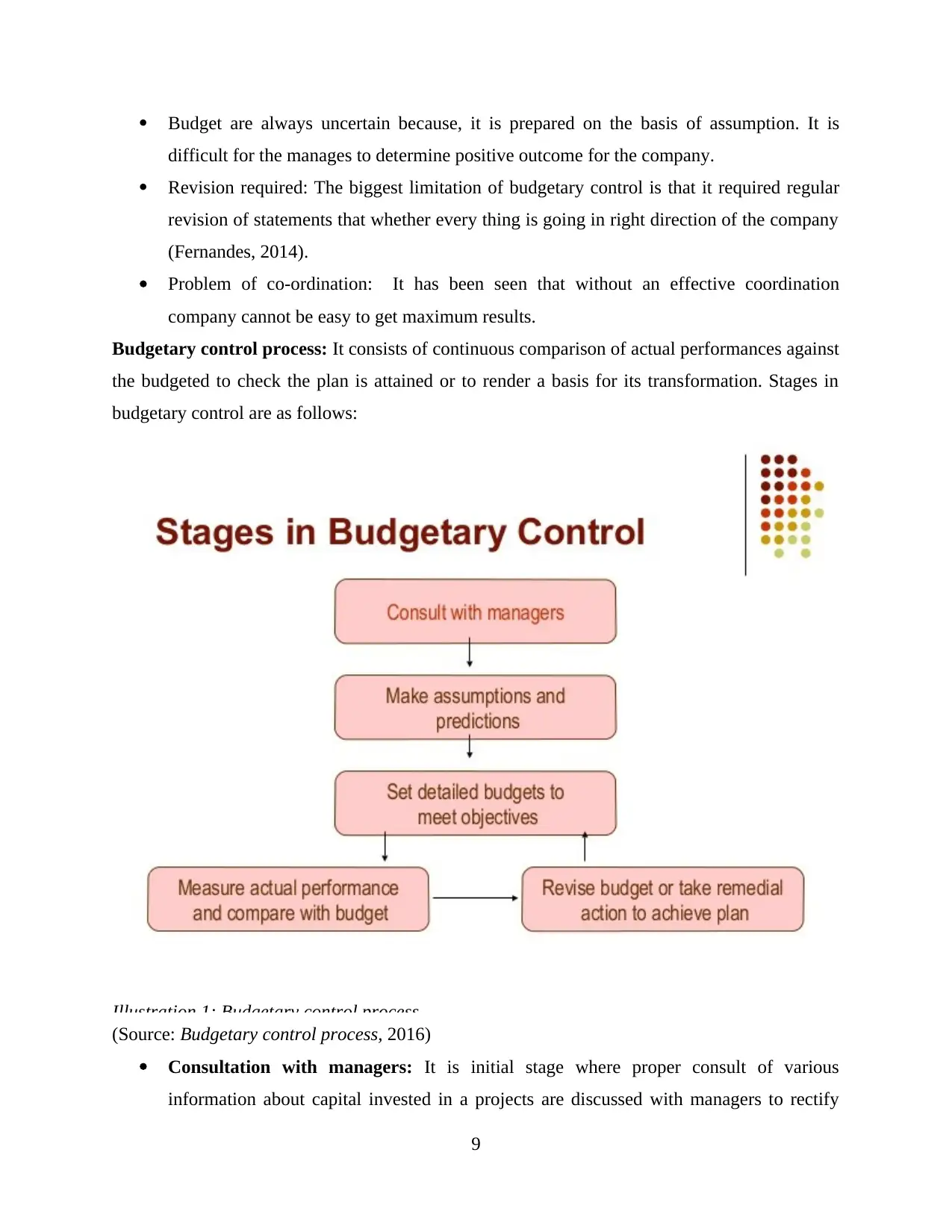

Budgetary control process: It consists of continuous comparison of actual performances against

the budgeted to check the plan is attained or to render a basis for its transformation. Stages in

budgetary control are as follows:

Illustration 1: Budgetary control process

(Source: Budgetary control process, 2016)

Consultation with managers: It is initial stage where proper consult of various

information about capital invested in a projects are discussed with managers to rectify

9

difficult for the manages to determine positive outcome for the company.

Revision required: The biggest limitation of budgetary control is that it required regular

revision of statements that whether every thing is going in right direction of the company

(Fernandes, 2014).

Problem of co-ordination: It has been seen that without an effective coordination

company cannot be easy to get maximum results.

Budgetary control process: It consists of continuous comparison of actual performances against

the budgeted to check the plan is attained or to render a basis for its transformation. Stages in

budgetary control are as follows:

Illustration 1: Budgetary control process

(Source: Budgetary control process, 2016)

Consultation with managers: It is initial stage where proper consult of various

information about capital invested in a projects are discussed with managers to rectify

9

future mistakes (De Bondt and et. al., 2015). Every data or information which is essential

for the development of departments are consulted with management prior budget

preparation.

Make assumption and predication: The next step in budgetary control is to make

assumption of cash-flows and expenses which are going to be incurred while production

of product and services. Predication of actual cost and profitability is also identified

before making budgets for the company. These assumption can make the business more

sustainable and effective for an organisation that would help them to attain there set

objectives.

Set detailed budgets to attain objectives: Under this process, managers need to set a

predetermine detail which are necessary while making budgets for the company. These

details are prepared through keeping future of business and its profitability. The

objectives can also be the key aspects that is need to be kept in the minds of concern

managers.

Measure actual performance and compare with budget: Budgets are prepared in order

to measure actual performances which are gathered during the year. It is based on sales

and profit they are getting from its available resources (Butler, 2016). The next portion

of this to analyse the budget by comparing it with other budgets.

Revise budget or take remedial action to achieve plan: It is considered as the final

step in the process of budget preparation which is done to check the viability of budgets.

The final submission of project are check and review properly by the managers before

making it to the action. It will help to accomplish organisational aims and objectives. If

everything is according to set standards then transfer to higher authority for further

approval or it not meeting requirement of management it will be transfer to initial stages

for correct those issues.

1.6: Different costing methods which are used to determine product pricing

Cost: It is the sum of money that has to be paid or given up in order to gain maximum

profit for the company. It can be invested on various factors such as purchase of raw material,

payment to suppliers and transformation of goods and services and many more.

Costing is the techniques for assigning cost to an element of a business (Vasant, 2012). The

calculation of cost of production or running a business, through allocating expenditure to various

10

for the development of departments are consulted with management prior budget

preparation.

Make assumption and predication: The next step in budgetary control is to make

assumption of cash-flows and expenses which are going to be incurred while production

of product and services. Predication of actual cost and profitability is also identified

before making budgets for the company. These assumption can make the business more

sustainable and effective for an organisation that would help them to attain there set

objectives.

Set detailed budgets to attain objectives: Under this process, managers need to set a

predetermine detail which are necessary while making budgets for the company. These

details are prepared through keeping future of business and its profitability. The

objectives can also be the key aspects that is need to be kept in the minds of concern

managers.

Measure actual performance and compare with budget: Budgets are prepared in order

to measure actual performances which are gathered during the year. It is based on sales

and profit they are getting from its available resources (Butler, 2016). The next portion

of this to analyse the budget by comparing it with other budgets.

Revise budget or take remedial action to achieve plan: It is considered as the final

step in the process of budget preparation which is done to check the viability of budgets.

The final submission of project are check and review properly by the managers before

making it to the action. It will help to accomplish organisational aims and objectives. If

everything is according to set standards then transfer to higher authority for further

approval or it not meeting requirement of management it will be transfer to initial stages

for correct those issues.

1.6: Different costing methods which are used to determine product pricing

Cost: It is the sum of money that has to be paid or given up in order to gain maximum

profit for the company. It can be invested on various factors such as purchase of raw material,

payment to suppliers and transformation of goods and services and many more.

Costing is the techniques for assigning cost to an element of a business (Vasant, 2012). The

calculation of cost of production or running a business, through allocating expenditure to various

10

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 19

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.