Finance for Managers (ACC91210): Case Study 1 Risk and Return Analysis

VerifiedAdded on 2022/10/31

|9

|2272

|311

Report

AI Summary

This finance report presents a comprehensive risk and return analysis of JB Hi-Fi and a reference company, utilizing historical market data from October 2018 to November 2019. The analysis includes calculating monthly returns, average returns, and standard deviations for the case company, reference company, market index, and an equally weighted portfolio. The Capital Asset Pricing Model (CAPM) is applied to determine expected returns, followed by the calculation of portfolio expected return and beta. The report discusses the risk and return measures, highlighting the benefits of diversification and its impact on mitigating risk. It concludes that diversification is a viable method for increasing overall returns while minimizing risk. The report also incorporates an analysis of the CAPM, providing insights into the risk factors that are taken into consideration when determining the expected returns of an investment.

Running head: FINANCE FOR MANAGERS

Finance for Managers

Name of the Student:

Name of the University:

Authors Note:

Finance for Managers

Name of the Student:

Name of the University:

Authors Note:

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

FINANCE FOR MANAGERS

1

Table of Contents

a.1) Calculating the historical monthly rates of return of the market index:.............................2

a.2) Calculating the historical average rate of return and standard deviation of your case

company; ii) the reference company; iii) the market index; and iv) an equally weighted

portfolio:.....................................................................................................................................2

b.1) Calculating the CAPM returns of 1) your case company; and 2) the reference company: 4

b.2) Calculating the portfolio expected return and beta:............................................................5

c) Discussing the risk and return measures calculated for the company and portfolio:.............6

Reference and Bibliography:......................................................................................................7

1

Table of Contents

a.1) Calculating the historical monthly rates of return of the market index:.............................2

a.2) Calculating the historical average rate of return and standard deviation of your case

company; ii) the reference company; iii) the market index; and iv) an equally weighted

portfolio:.....................................................................................................................................2

b.1) Calculating the CAPM returns of 1) your case company; and 2) the reference company: 4

b.2) Calculating the portfolio expected return and beta:............................................................5

c) Discussing the risk and return measures calculated for the company and portfolio:.............6

Reference and Bibliography:......................................................................................................7

FINANCE FOR MANAGERS

2

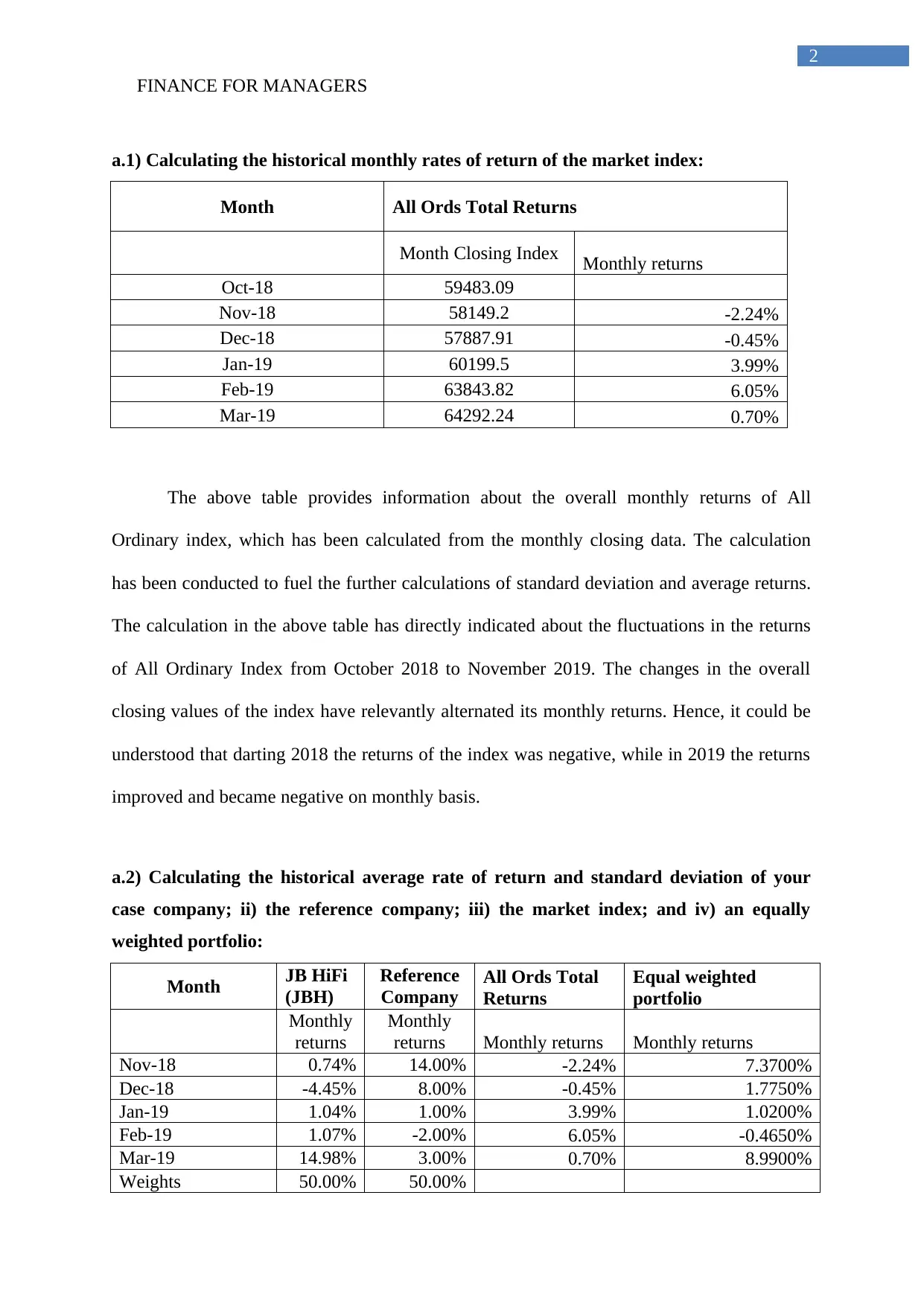

a.1) Calculating the historical monthly rates of return of the market index:

Month All Ords Total Returns

Month Closing Index Monthly returns

Oct-18 59483.09

Nov-18 58149.2 -2.24%

Dec-18 57887.91 -0.45%

Jan-19 60199.5 3.99%

Feb-19 63843.82 6.05%

Mar-19 64292.24 0.70%

The above table provides information about the overall monthly returns of All

Ordinary index, which has been calculated from the monthly closing data. The calculation

has been conducted to fuel the further calculations of standard deviation and average returns.

The calculation in the above table has directly indicated about the fluctuations in the returns

of All Ordinary Index from October 2018 to November 2019. The changes in the overall

closing values of the index have relevantly alternated its monthly returns. Hence, it could be

understood that darting 2018 the returns of the index was negative, while in 2019 the returns

improved and became negative on monthly basis.

a.2) Calculating the historical average rate of return and standard deviation of your

case company; ii) the reference company; iii) the market index; and iv) an equally

weighted portfolio:

Month JB HiFi

(JBH)

Reference

Company

All Ords Total

Returns

Equal weighted

portfolio

Monthly

returns

Monthly

returns Monthly returns Monthly returns

Nov-18 0.74% 14.00% -2.24% 7.3700%

Dec-18 -4.45% 8.00% -0.45% 1.7750%

Jan-19 1.04% 1.00% 3.99% 1.0200%

Feb-19 1.07% -2.00% 6.05% -0.4650%

Mar-19 14.98% 3.00% 0.70% 8.9900%

Weights 50.00% 50.00%

2

a.1) Calculating the historical monthly rates of return of the market index:

Month All Ords Total Returns

Month Closing Index Monthly returns

Oct-18 59483.09

Nov-18 58149.2 -2.24%

Dec-18 57887.91 -0.45%

Jan-19 60199.5 3.99%

Feb-19 63843.82 6.05%

Mar-19 64292.24 0.70%

The above table provides information about the overall monthly returns of All

Ordinary index, which has been calculated from the monthly closing data. The calculation

has been conducted to fuel the further calculations of standard deviation and average returns.

The calculation in the above table has directly indicated about the fluctuations in the returns

of All Ordinary Index from October 2018 to November 2019. The changes in the overall

closing values of the index have relevantly alternated its monthly returns. Hence, it could be

understood that darting 2018 the returns of the index was negative, while in 2019 the returns

improved and became negative on monthly basis.

a.2) Calculating the historical average rate of return and standard deviation of your

case company; ii) the reference company; iii) the market index; and iv) an equally

weighted portfolio:

Month JB HiFi

(JBH)

Reference

Company

All Ords Total

Returns

Equal weighted

portfolio

Monthly

returns

Monthly

returns Monthly returns Monthly returns

Nov-18 0.74% 14.00% -2.24% 7.3700%

Dec-18 -4.45% 8.00% -0.45% 1.7750%

Jan-19 1.04% 1.00% 3.99% 1.0200%

Feb-19 1.07% -2.00% 6.05% -0.4650%

Mar-19 14.98% 3.00% 0.70% 8.9900%

Weights 50.00% 50.00%

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

FINANCE FOR MANAGERS

3

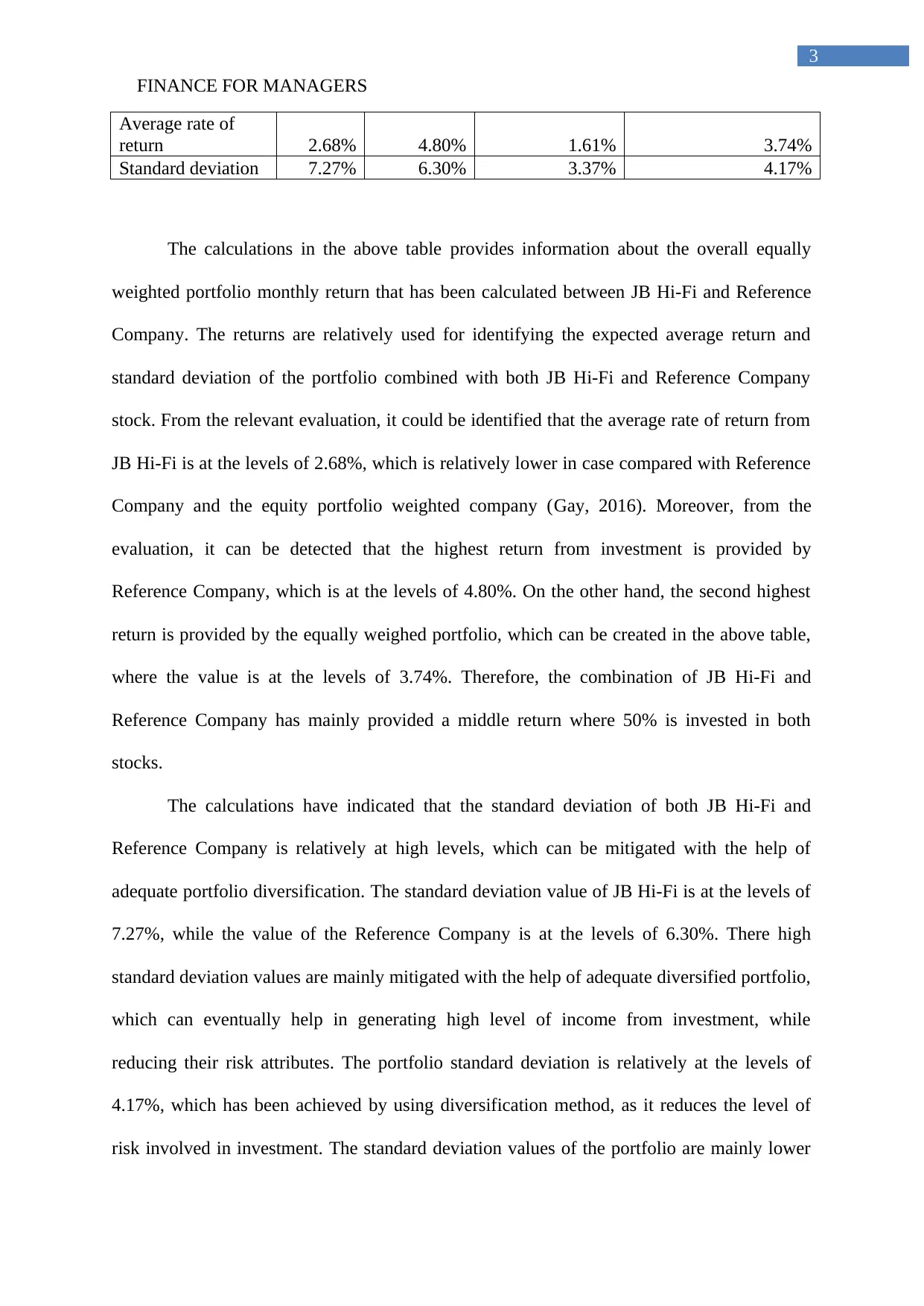

Average rate of

return 2.68% 4.80% 1.61% 3.74%

Standard deviation 7.27% 6.30% 3.37% 4.17%

The calculations in the above table provides information about the overall equally

weighted portfolio monthly return that has been calculated between JB Hi-Fi and Reference

Company. The returns are relatively used for identifying the expected average return and

standard deviation of the portfolio combined with both JB Hi-Fi and Reference Company

stock. From the relevant evaluation, it could be identified that the average rate of return from

JB Hi-Fi is at the levels of 2.68%, which is relatively lower in case compared with Reference

Company and the equity portfolio weighted company (Gay, 2016). Moreover, from the

evaluation, it can be detected that the highest return from investment is provided by

Reference Company, which is at the levels of 4.80%. On the other hand, the second highest

return is provided by the equally weighed portfolio, which can be created in the above table,

where the value is at the levels of 3.74%. Therefore, the combination of JB Hi-Fi and

Reference Company has mainly provided a middle return where 50% is invested in both

stocks.

The calculations have indicated that the standard deviation of both JB Hi-Fi and

Reference Company is relatively at high levels, which can be mitigated with the help of

adequate portfolio diversification. The standard deviation value of JB Hi-Fi is at the levels of

7.27%, while the value of the Reference Company is at the levels of 6.30%. There high

standard deviation values are mainly mitigated with the help of adequate diversified portfolio,

which can eventually help in generating high level of income from investment, while

reducing their risk attributes. The portfolio standard deviation is relatively at the levels of

4.17%, which has been achieved by using diversification method, as it reduces the level of

risk involved in investment. The standard deviation values of the portfolio are mainly lower

3

Average rate of

return 2.68% 4.80% 1.61% 3.74%

Standard deviation 7.27% 6.30% 3.37% 4.17%

The calculations in the above table provides information about the overall equally

weighted portfolio monthly return that has been calculated between JB Hi-Fi and Reference

Company. The returns are relatively used for identifying the expected average return and

standard deviation of the portfolio combined with both JB Hi-Fi and Reference Company

stock. From the relevant evaluation, it could be identified that the average rate of return from

JB Hi-Fi is at the levels of 2.68%, which is relatively lower in case compared with Reference

Company and the equity portfolio weighted company (Gay, 2016). Moreover, from the

evaluation, it can be detected that the highest return from investment is provided by

Reference Company, which is at the levels of 4.80%. On the other hand, the second highest

return is provided by the equally weighed portfolio, which can be created in the above table,

where the value is at the levels of 3.74%. Therefore, the combination of JB Hi-Fi and

Reference Company has mainly provided a middle return where 50% is invested in both

stocks.

The calculations have indicated that the standard deviation of both JB Hi-Fi and

Reference Company is relatively at high levels, which can be mitigated with the help of

adequate portfolio diversification. The standard deviation value of JB Hi-Fi is at the levels of

7.27%, while the value of the Reference Company is at the levels of 6.30%. There high

standard deviation values are mainly mitigated with the help of adequate diversified portfolio,

which can eventually help in generating high level of income from investment, while

reducing their risk attributes. The portfolio standard deviation is relatively at the levels of

4.17%, which has been achieved by using diversification method, as it reduces the level of

risk involved in investment. The standard deviation values of the portfolio are mainly lower

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

FINANCE FOR MANAGERS

4

than the initial values of the stock. This is due to the diversification method used for

mitigating the fluctuations in the price movement of the combined portfolio returns. The

reduction in the fluctuations of the returns has resulted in the lower standard deviation of the

portfolio. Moreover, the returns provided by this equal weighted portfolio are higher in

comparison to the standard deviation. Therefore, investment and Portfolio would eventually

help in generating high level of return for the investors, while minimize any kind of risk

involved in investments (Chapple & Humphrey, 2014). Therefore, it could be understood that

with the help of diversification the overall returns of the investment is increased while the

fluctuations in the risk factor decreases. Thus, diversification method is considered to be

more viable, as it will help in generating high level of income, while reducing the total risk

involved in the investments.

b.1) Calculating the CAPM returns of 1) your case company; and 2) the reference

company:

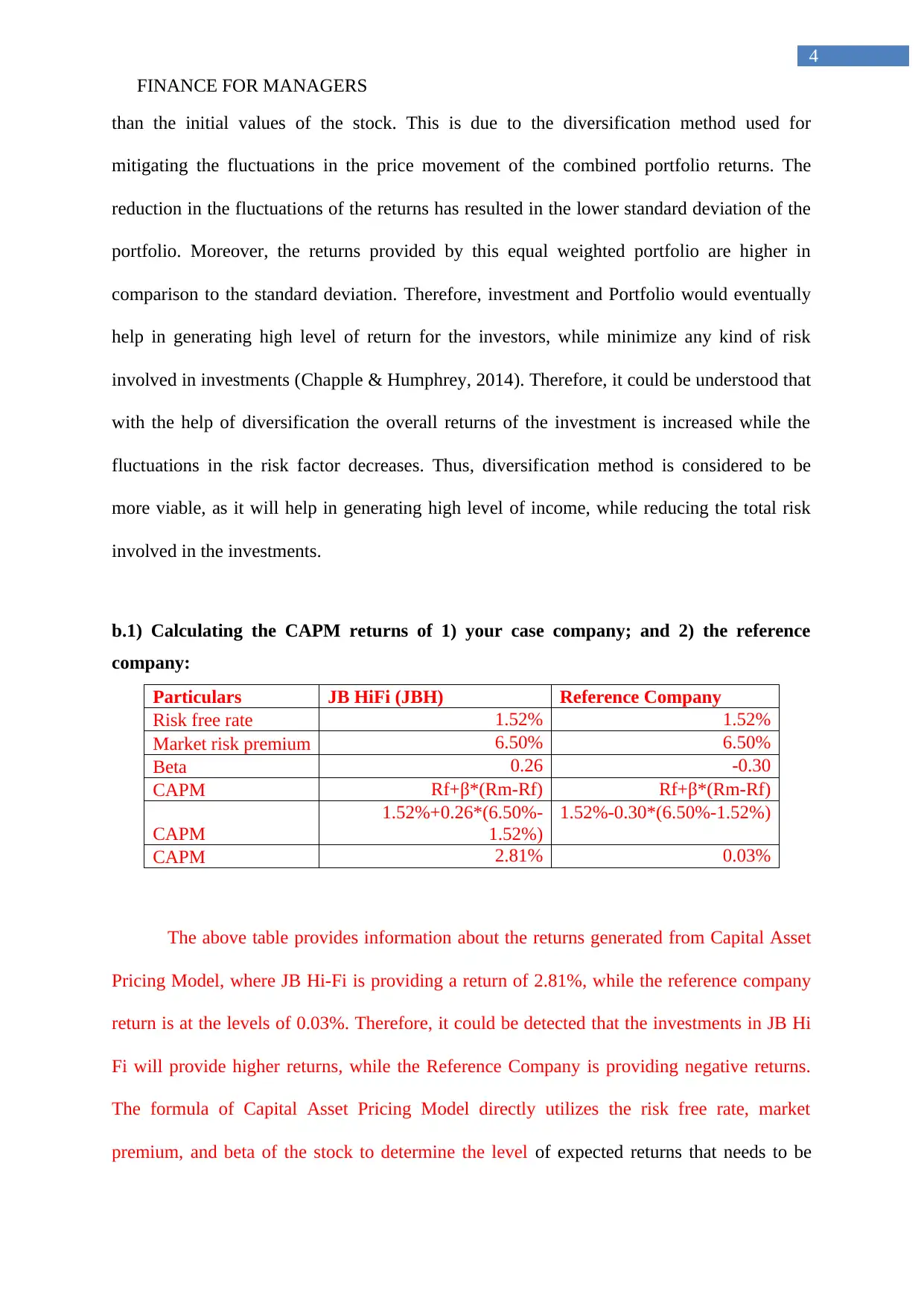

Particulars JB HiFi (JBH) Reference Company

Risk free rate 1.52% 1.52%

Market risk premium 6.50% 6.50%

Beta 0.26 -0.30

CAPM Rf+β*(Rm-Rf) Rf+β*(Rm-Rf)

CAPM

1.52%+0.26*(6.50%-

1.52%)

1.52%-0.30*(6.50%-1.52%)

CAPM 2.81% 0.03%

The above table provides information about the returns generated from Capital Asset

Pricing Model, where JB Hi-Fi is providing a return of 2.81%, while the reference company

return is at the levels of 0.03%. Therefore, it could be detected that the investments in JB Hi

Fi will provide higher returns, while the Reference Company is providing negative returns.

The formula of Capital Asset Pricing Model directly utilizes the risk free rate, market

premium, and beta of the stock to determine the level of expected returns that needs to be

4

than the initial values of the stock. This is due to the diversification method used for

mitigating the fluctuations in the price movement of the combined portfolio returns. The

reduction in the fluctuations of the returns has resulted in the lower standard deviation of the

portfolio. Moreover, the returns provided by this equal weighted portfolio are higher in

comparison to the standard deviation. Therefore, investment and Portfolio would eventually

help in generating high level of return for the investors, while minimize any kind of risk

involved in investments (Chapple & Humphrey, 2014). Therefore, it could be understood that

with the help of diversification the overall returns of the investment is increased while the

fluctuations in the risk factor decreases. Thus, diversification method is considered to be

more viable, as it will help in generating high level of income, while reducing the total risk

involved in the investments.

b.1) Calculating the CAPM returns of 1) your case company; and 2) the reference

company:

Particulars JB HiFi (JBH) Reference Company

Risk free rate 1.52% 1.52%

Market risk premium 6.50% 6.50%

Beta 0.26 -0.30

CAPM Rf+β*(Rm-Rf) Rf+β*(Rm-Rf)

CAPM

1.52%+0.26*(6.50%-

1.52%)

1.52%-0.30*(6.50%-1.52%)

CAPM 2.81% 0.03%

The above table provides information about the returns generated from Capital Asset

Pricing Model, where JB Hi-Fi is providing a return of 2.81%, while the reference company

return is at the levels of 0.03%. Therefore, it could be detected that the investments in JB Hi

Fi will provide higher returns, while the Reference Company is providing negative returns.

The formula of Capital Asset Pricing Model directly utilizes the risk free rate, market

premium, and beta of the stock to determine the level of expected returns that needs to be

FINANCE FOR MANAGERS

5

provided by company to their shareholders. Hence, from the relevant valuation, it can be

detected that with the high level of beta the overall stock of JB Hi-Fi needs to generate a

return of 2.81%, while the reference company needs to only provide 0.03%. Thus, the

combination of both the stock would eventually help the investors to mitigate the relevant

risk of price volatility that is conducted by the capital market fluctuations.

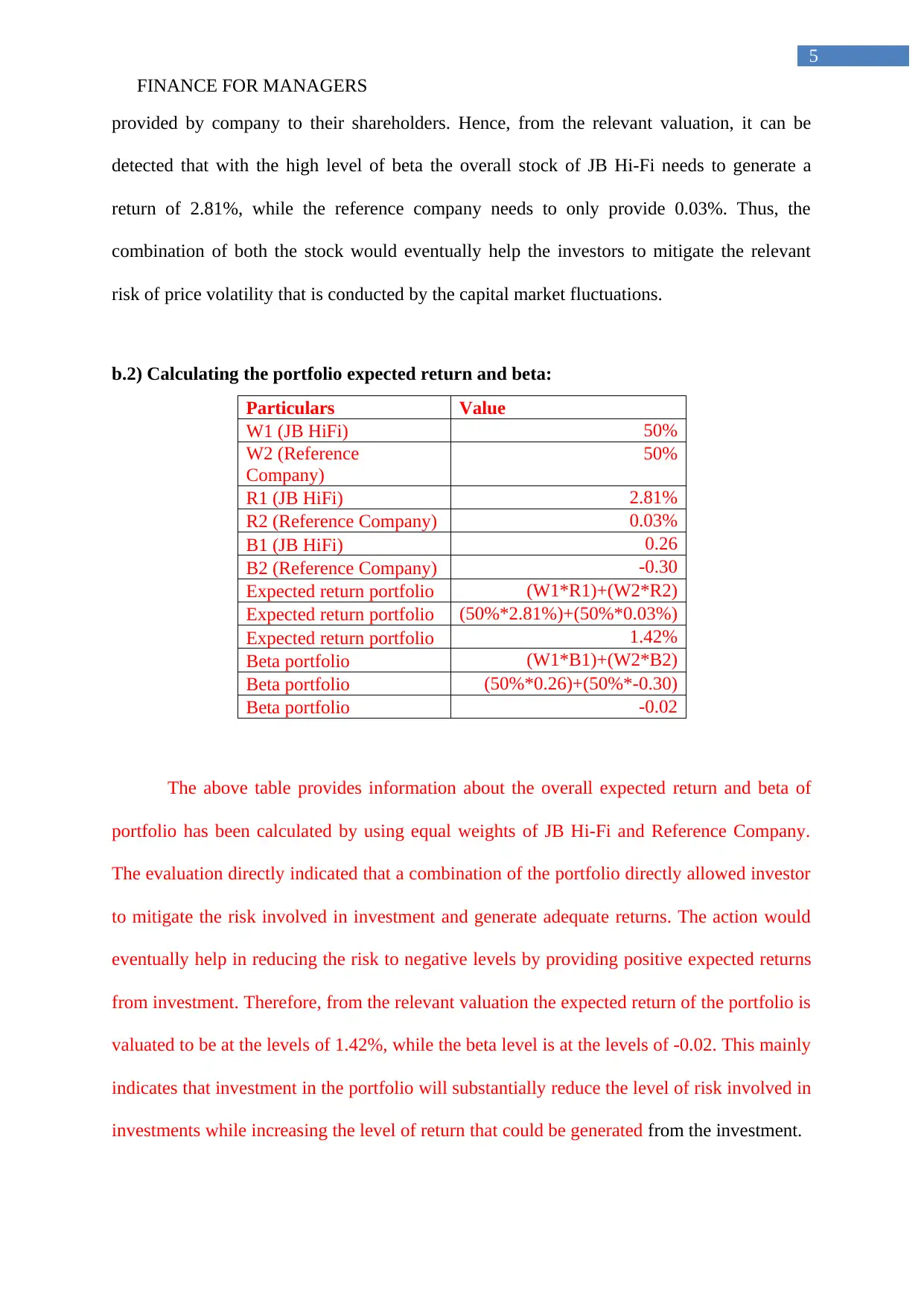

b.2) Calculating the portfolio expected return and beta:

Particulars Value

W1 (JB HiFi) 50%

W2 (Reference

Company)

50%

R1 (JB HiFi) 2.81%

R2 (Reference Company) 0.03%

B1 (JB HiFi) 0.26

B2 (Reference Company) -0.30

Expected return portfolio (W1*R1)+(W2*R2)

Expected return portfolio (50%*2.81%)+(50%*0.03%)

Expected return portfolio 1.42%

Beta portfolio (W1*B1)+(W2*B2)

Beta portfolio (50%*0.26)+(50%*-0.30)

Beta portfolio -0.02

The above table provides information about the overall expected return and beta of

portfolio has been calculated by using equal weights of JB Hi-Fi and Reference Company.

The evaluation directly indicated that a combination of the portfolio directly allowed investor

to mitigate the risk involved in investment and generate adequate returns. The action would

eventually help in reducing the risk to negative levels by providing positive expected returns

from investment. Therefore, from the relevant valuation the expected return of the portfolio is

valuated to be at the levels of 1.42%, while the beta level is at the levels of -0.02. This mainly

indicates that investment in the portfolio will substantially reduce the level of risk involved in

investments while increasing the level of return that could be generated from the investment.

5

provided by company to their shareholders. Hence, from the relevant valuation, it can be

detected that with the high level of beta the overall stock of JB Hi-Fi needs to generate a

return of 2.81%, while the reference company needs to only provide 0.03%. Thus, the

combination of both the stock would eventually help the investors to mitigate the relevant

risk of price volatility that is conducted by the capital market fluctuations.

b.2) Calculating the portfolio expected return and beta:

Particulars Value

W1 (JB HiFi) 50%

W2 (Reference

Company)

50%

R1 (JB HiFi) 2.81%

R2 (Reference Company) 0.03%

B1 (JB HiFi) 0.26

B2 (Reference Company) -0.30

Expected return portfolio (W1*R1)+(W2*R2)

Expected return portfolio (50%*2.81%)+(50%*0.03%)

Expected return portfolio 1.42%

Beta portfolio (W1*B1)+(W2*B2)

Beta portfolio (50%*0.26)+(50%*-0.30)

Beta portfolio -0.02

The above table provides information about the overall expected return and beta of

portfolio has been calculated by using equal weights of JB Hi-Fi and Reference Company.

The evaluation directly indicated that a combination of the portfolio directly allowed investor

to mitigate the risk involved in investment and generate adequate returns. The action would

eventually help in reducing the risk to negative levels by providing positive expected returns

from investment. Therefore, from the relevant valuation the expected return of the portfolio is

valuated to be at the levels of 1.42%, while the beta level is at the levels of -0.02. This mainly

indicates that investment in the portfolio will substantially reduce the level of risk involved in

investments while increasing the level of return that could be generated from the investment.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

FINANCE FOR MANAGERS

6

c) Discussing the risk and return measures calculated for the company and portfolio:

The above calculations provide information about the overall risk and return

conditions of the selected company and portfolio. JB Hi-Fi has been selected as the company,

which is used for analyzing and creating the portfolio with reference company. From the

relevant evaluation, it could be identified that beta of JB Hi-Fi is calculated to be at the levels

of 0.26. On the other hand, the beta of reference company is calculated at -0.30. In a similar

instance, the expected return of the portfolio is calculated with the CAPM formula, where the

return of JB Hi-Fi is at the levels of 2.81%, while the returns of Reference Company are the

levels 0.03%. This mainly comprises the total expected return of the portfolio, which is at the

levels of 1.42%. Therefore, from the relevant evaluation, it can be identified that the beta of

the portfolio is negative and indicates a relevant opposite price action than the All Ordinary

index of Australia (Fagereng, Gottlieb & Guiso, 2017). However, the combined portfolio is

relatively helpful in reducing the level of risk involved in Investments, as the total risk was

mitigated and the return increased for the combined investments in JB Hi-Fi and Reference

Company.

Hence, with a portfolio with negative beta adequate diversification can be presented

to the investment, which improves the scope of the investment. Furthermore, analysis of the

CAPM indicates about the risk factors, which is taken into consideration for determining the

expected returns of an investment. .

The combination of the overall portfolio would be beneficial for the investors, as the

total risk involved in investment is at minimum levels of -0.02, which indicates that

fluctuations from the volatile market will have low impact on the price variation of the

portfolio. This would secure the investments conducted in the portfolio and allow the investor

to generate higher return, while minimizing the negative impact on the investment capital.

6

c) Discussing the risk and return measures calculated for the company and portfolio:

The above calculations provide information about the overall risk and return

conditions of the selected company and portfolio. JB Hi-Fi has been selected as the company,

which is used for analyzing and creating the portfolio with reference company. From the

relevant evaluation, it could be identified that beta of JB Hi-Fi is calculated to be at the levels

of 0.26. On the other hand, the beta of reference company is calculated at -0.30. In a similar

instance, the expected return of the portfolio is calculated with the CAPM formula, where the

return of JB Hi-Fi is at the levels of 2.81%, while the returns of Reference Company are the

levels 0.03%. This mainly comprises the total expected return of the portfolio, which is at the

levels of 1.42%. Therefore, from the relevant evaluation, it can be identified that the beta of

the portfolio is negative and indicates a relevant opposite price action than the All Ordinary

index of Australia (Fagereng, Gottlieb & Guiso, 2017). However, the combined portfolio is

relatively helpful in reducing the level of risk involved in Investments, as the total risk was

mitigated and the return increased for the combined investments in JB Hi-Fi and Reference

Company.

Hence, with a portfolio with negative beta adequate diversification can be presented

to the investment, which improves the scope of the investment. Furthermore, analysis of the

CAPM indicates about the risk factors, which is taken into consideration for determining the

expected returns of an investment. .

The combination of the overall portfolio would be beneficial for the investors, as the

total risk involved in investment is at minimum levels of -0.02, which indicates that

fluctuations from the volatile market will have low impact on the price variation of the

portfolio. This would secure the investments conducted in the portfolio and allow the investor

to generate higher return, while minimizing the negative impact on the investment capital.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

FINANCE FOR MANAGERS

7

Reference and Bibliography:

Al-Khazali, O., Lean, H.H. & Samet, A., 2014. Do Islamic stock indexes outperform

conventional stock indexes? A stochastic dominance approach. Pacific-Basin Finance

Journal, 28, pp.29-46.

Bloomberg.com. 2019. Bloomberg - Are you a robot?. [online] Available at:

https://www.bloomberg.com/markets/rates-bonds/government-bonds/australia [Accessed 25

May 2019].

Chapple, L. & Humphrey, J.E., 2014. Does board gender diversity have a financial impact?

Evidence using stock portfolio performance. Journal of business ethics, 122(4), pp.709-723.

Ewing, B.T. & Malik, F., 2016. Volatility spillovers between oil prices and the stock market

under structural breaks. Global Finance Journal, 29, pp.12-23.

Fagereng, A., Gottlieb, C. & Guiso, L., 2017. Asset market participation and portfolio choice

over the life‐cycle. The Journal of Finance, 72(2), pp.705-750.

Gay, R.D., 2016. Effect of macroeconomic variables on stock market returns for four

emerging economies: Brazil, Russia, India, and China. The International Business &

Economics Research Journal (Online), 15(3), p.119.

Kumar, D., 2014. Return and volatility transmission between gold and stock sectors:

Application of portfolio management and hedging effectiveness. IIMB Management

Review, 26(1), pp.5-16.

7

Reference and Bibliography:

Al-Khazali, O., Lean, H.H. & Samet, A., 2014. Do Islamic stock indexes outperform

conventional stock indexes? A stochastic dominance approach. Pacific-Basin Finance

Journal, 28, pp.29-46.

Bloomberg.com. 2019. Bloomberg - Are you a robot?. [online] Available at:

https://www.bloomberg.com/markets/rates-bonds/government-bonds/australia [Accessed 25

May 2019].

Chapple, L. & Humphrey, J.E., 2014. Does board gender diversity have a financial impact?

Evidence using stock portfolio performance. Journal of business ethics, 122(4), pp.709-723.

Ewing, B.T. & Malik, F., 2016. Volatility spillovers between oil prices and the stock market

under structural breaks. Global Finance Journal, 29, pp.12-23.

Fagereng, A., Gottlieb, C. & Guiso, L., 2017. Asset market participation and portfolio choice

over the life‐cycle. The Journal of Finance, 72(2), pp.705-750.

Gay, R.D., 2016. Effect of macroeconomic variables on stock market returns for four

emerging economies: Brazil, Russia, India, and China. The International Business &

Economics Research Journal (Online), 15(3), p.119.

Kumar, D., 2014. Return and volatility transmission between gold and stock sectors:

Application of portfolio management and hedging effectiveness. IIMB Management

Review, 26(1), pp.5-16.

FINANCE FOR MANAGERS

8

Lim, S., Oh, K.W. & Zhu, J., 2014. Use of DEA cross-efficiency evaluation in portfolio

selection: An application to Korean stock market. European Journal of Operational

Research, 236(1), pp.361-368.

Lin, B., Wesseh Jr, P.K. & Appiah, M.O., 2014. Oil price fluctuation, volatility spillover and

the Ghanaian equity market: Implication for portfolio management and hedging

effectiveness. Energy Economics, 42, pp.172-182.

Mensi, W., Hammoudeh, S. & Kang, S.H., 2015. Precious metals, cereal, oil and stock

market linkages and portfolio risk management: Evidence from Saudi Arabia. Economic

Modelling, 51, pp.340-358.

Syriopoulos, T., Makram, B. & Boubaker, A., 2015. Stock market volatility spillovers and

portfolio hedging: BRICS and the financial crisis. International Review of Financial

Analysis, 39, pp.7-18.

Yao, J., Ma, C. & He, W.P., 2014. Investor herding behaviour of Chinese stock

market. International Review of Economics & Finance, 29, pp.12-29.

8

Lim, S., Oh, K.W. & Zhu, J., 2014. Use of DEA cross-efficiency evaluation in portfolio

selection: An application to Korean stock market. European Journal of Operational

Research, 236(1), pp.361-368.

Lin, B., Wesseh Jr, P.K. & Appiah, M.O., 2014. Oil price fluctuation, volatility spillover and

the Ghanaian equity market: Implication for portfolio management and hedging

effectiveness. Energy Economics, 42, pp.172-182.

Mensi, W., Hammoudeh, S. & Kang, S.H., 2015. Precious metals, cereal, oil and stock

market linkages and portfolio risk management: Evidence from Saudi Arabia. Economic

Modelling, 51, pp.340-358.

Syriopoulos, T., Makram, B. & Boubaker, A., 2015. Stock market volatility spillovers and

portfolio hedging: BRICS and the financial crisis. International Review of Financial

Analysis, 39, pp.7-18.

Yao, J., Ma, C. & He, W.P., 2014. Investor herding behaviour of Chinese stock

market. International Review of Economics & Finance, 29, pp.12-29.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 9

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.