Finance for Managers: Comprehensive Analysis of Financial Concepts

VerifiedAdded on 2020/01/28

|18

|5283

|116

Report

AI Summary

This report provides a comprehensive overview of finance for managers, covering essential concepts such as financial record-keeping, stakeholder analysis, and variance analysis. The introduction highlights the significance of financial resources in an organization and their role in decision-making. Task 1 delves into the importance of financial record-keeping, its requirements, and the common forms used, including income statements, balance sheets, and cash flow statements. It also discusses the role of stakeholders and their varying needs for financial information. Task 2 presents variance analysis and a reconciliation statement, offering insights into the business's financial performance. Finally, Task 3 explores budgeting processes and various pricing techniques. The report provides a detailed analysis of these core financial concepts, making it a valuable resource for students and professionals alike.

FINANCE FOR MANAGERS

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

TABLE OF CONTENTS

INTRODUCTION...........................................................................................................................1

TASK 1............................................................................................................................................1

1.1...........................................................................................................................................1

1.2...........................................................................................................................................2

1.3...........................................................................................................................................3

1.4...........................................................................................................................................4

1.5...........................................................................................................................................5

1.6...........................................................................................................................................5

TASK 2............................................................................................................................................6

2.1...........................................................................................................................................6

TASK 3............................................................................................................................................8

3.1...........................................................................................................................................8

3.2.........................................................................................................................................11

3.3.........................................................................................................................................13

3.4.........................................................................................................................................14

CONCLUSION..............................................................................................................................15

REFERENCES..............................................................................................................................16

INTRODUCTION...........................................................................................................................1

TASK 1............................................................................................................................................1

1.1...........................................................................................................................................1

1.2...........................................................................................................................................2

1.3...........................................................................................................................................3

1.4...........................................................................................................................................4

1.5...........................................................................................................................................5

1.6...........................................................................................................................................5

TASK 2............................................................................................................................................6

2.1...........................................................................................................................................6

TASK 3............................................................................................................................................8

3.1...........................................................................................................................................8

3.2.........................................................................................................................................11

3.3.........................................................................................................................................13

3.4.........................................................................................................................................14

CONCLUSION..............................................................................................................................15

REFERENCES..............................................................................................................................16

INTRODUCTION

The base of an organisation is in its financial resources that are utilised by the company, a

major focus of management. Financial management gives more importance to the financial

aspects involved in the business which helps administration to take decisions regarding cost

reduction by using finance in the form of business funding. It also stresses on costs determination

by using variance analysis in the business. Various project evaluation tools are also used in order

top assess the project viability in order to select or reject the certain proposals.

TASK 1

1.1

Financial record keeping plays a significant role in an enterprise as it covers the major

monetary business activities which helps the company to keep records for operational and legal

purposes (Denison, 2010). There are various requirements and purpose of the financial record

keeping which are given as below:

The records of different business transactions takes place in an entity is required for tax

preparation and filling as the basic requirement of the taxation authority is to submit all

the business records that reveals true income of the business entity. This is a legal

requirement, and limited companies can be fined for not complying.

The business records are helpful in negotiating with the banks for taking loans as their

main aim is to record each and every transaction that forms part of business activities.

The accrual concept of accounting also helps in recording every transactions of sale

without receiving payment in context for avoiding any forged vouchers and further future

consequences.

By keeping financial records in proper direction, the company able to assess its capability

in terms of generating sales and revenue at the end of an accounting period.

In addition to this, day-to-day costs, expenditures as well as the income can be easily

determined by the management when it keeps record of financial transactions.

For making comparison of current financial performance with the past, the financial

records are highly supportive. Along with this, through this particular procedure, the

company can compare with the competitor business entity as well.

1

The base of an organisation is in its financial resources that are utilised by the company, a

major focus of management. Financial management gives more importance to the financial

aspects involved in the business which helps administration to take decisions regarding cost

reduction by using finance in the form of business funding. It also stresses on costs determination

by using variance analysis in the business. Various project evaluation tools are also used in order

top assess the project viability in order to select or reject the certain proposals.

TASK 1

1.1

Financial record keeping plays a significant role in an enterprise as it covers the major

monetary business activities which helps the company to keep records for operational and legal

purposes (Denison, 2010). There are various requirements and purpose of the financial record

keeping which are given as below:

The records of different business transactions takes place in an entity is required for tax

preparation and filling as the basic requirement of the taxation authority is to submit all

the business records that reveals true income of the business entity. This is a legal

requirement, and limited companies can be fined for not complying.

The business records are helpful in negotiating with the banks for taking loans as their

main aim is to record each and every transaction that forms part of business activities.

The accrual concept of accounting also helps in recording every transactions of sale

without receiving payment in context for avoiding any forged vouchers and further future

consequences.

By keeping financial records in proper direction, the company able to assess its capability

in terms of generating sales and revenue at the end of an accounting period.

In addition to this, day-to-day costs, expenditures as well as the income can be easily

determined by the management when it keeps record of financial transactions.

For making comparison of current financial performance with the past, the financial

records are highly supportive. Along with this, through this particular procedure, the

company can compare with the competitor business entity as well.

1

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1.2

The common form used by an enterprise for recording financial information by preparing

financial statements such as income statements, balance sheet, cash flow statements and changes

in equity (Davis and Caldeira, 2010).

Incomes statement: In this type of the financial recording system, basically two kinds of

the transactions recorded. Further, those aspects which included in this process are such

as Sales or revenue and expenses.

Balance sheet: Under this particular system, assets, liabilities and equity amount which

is taken from the shareholders, these three transactions are recorded.

Cash flow statement: In order to record cash inflows or incomes and cash outflows or

expenses this particular process is considered by the management. Further, cash position

at the end of an accounting period is to be derived through this particular statement of the

financials.

These are the standard forms of techniques which are utilised by an enterprise to record

their financial information. The benefits include the ability to record business transactions that

reflects financial projections and to determine the financial position of an enterprise which helps

them make future business decisions. The basic tools involved in recording the information is

journal, ledger and day books and cash books.

In the company, Enterprise Resource Planning (ERP) system is one of the important as

well as useful for the management. It is a effective software under which financial transactions

can be easily recorded and assessed any malpractices also in appropriate ways.

The legal and operation requirement of the business is to follow all the prescribed

standards and procedures in order to facilitate the entity in order to fulfil financial reporting such

as IFRS whose guideline assists an entity in financial reporting.

According to the legal rule and regulations, it is mandatory to follow all the legislations

in legal manner while keeping record of the financial transactions and preparing the final

accounts. As a limited company, some necessary rules are given as below:

All the money must be either received or spent by the firm and then can include in the

financial statements.

2

The common form used by an enterprise for recording financial information by preparing

financial statements such as income statements, balance sheet, cash flow statements and changes

in equity (Davis and Caldeira, 2010).

Incomes statement: In this type of the financial recording system, basically two kinds of

the transactions recorded. Further, those aspects which included in this process are such

as Sales or revenue and expenses.

Balance sheet: Under this particular system, assets, liabilities and equity amount which

is taken from the shareholders, these three transactions are recorded.

Cash flow statement: In order to record cash inflows or incomes and cash outflows or

expenses this particular process is considered by the management. Further, cash position

at the end of an accounting period is to be derived through this particular statement of the

financials.

These are the standard forms of techniques which are utilised by an enterprise to record

their financial information. The benefits include the ability to record business transactions that

reflects financial projections and to determine the financial position of an enterprise which helps

them make future business decisions. The basic tools involved in recording the information is

journal, ledger and day books and cash books.

In the company, Enterprise Resource Planning (ERP) system is one of the important as

well as useful for the management. It is a effective software under which financial transactions

can be easily recorded and assessed any malpractices also in appropriate ways.

The legal and operation requirement of the business is to follow all the prescribed

standards and procedures in order to facilitate the entity in order to fulfil financial reporting such

as IFRS whose guideline assists an entity in financial reporting.

According to the legal rule and regulations, it is mandatory to follow all the legislations

in legal manner while keeping record of the financial transactions and preparing the final

accounts. As a limited company, some necessary rules are given as below:

All the money must be either received or spent by the firm and then can include in the

financial statements.

2

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Details of the fixed and current assets are necessary to owned by the business

organisation.

At the end of an accounting year, the inventory must be own by the firm and then can

include in the balance sheet.

Along with this, all the accounting principles as well as required standards musts be

followed by the firm while making financial reports.

1.3

Stakeholders are group of people who attached or joined with the business activities in

direct and indirect manner. These are of the basically two types such as internal and the external

stakeholders. Further, they play significant role in the business as the external changes may

occurred with the presence of several stakeholders which can affect the business performance in

two aspects such as internal and external ways (Edwards, 2013). Customers are one of the

important stakeholder for the firm who requires financial informatics in order to analyse business

performance at the of year in terms of profitability. When performance of the company is higher

at the end of financial year, then they predict that it will provide high quality of goods and

services at the lower prices.

The usefulness of financial statement is different for different persons, which are given as below:

Shareholders- The increased profitability and good status of the business in terms high financial

positive will assure investors that their wealth is secured with the business and they will get

higher future returns in form of dividends. Further, when new or potential shareholders going to

make investment in the company then easily able to assess with the financial statements that it is

viable for putting money or not. In addition to this, capability of the firm in terms of providing

dividend or return on the invested amount also can be determined in proper direction

(Bebbington, Unerman and O'Dwyer, 2014).

Creditors- the increased profits shown in the financial statement shows higher credibility of the

firm to pay all the creditors in given time without any kind of financial risks. The creditors use

the financial statements in order to analyse creditworthiness of the company and on the basis of

that, they able to purchase goods and services on the credit.

Employee- An employee is regarded as one of the most important stakeholders of an

organisation as their needs and expectations need to be fulfilled by the business. Financial

statements are useful to employees for job security, salary and employee benefits expectations.

3

organisation.

At the end of an accounting year, the inventory must be own by the firm and then can

include in the balance sheet.

Along with this, all the accounting principles as well as required standards musts be

followed by the firm while making financial reports.

1.3

Stakeholders are group of people who attached or joined with the business activities in

direct and indirect manner. These are of the basically two types such as internal and the external

stakeholders. Further, they play significant role in the business as the external changes may

occurred with the presence of several stakeholders which can affect the business performance in

two aspects such as internal and external ways (Edwards, 2013). Customers are one of the

important stakeholder for the firm who requires financial informatics in order to analyse business

performance at the of year in terms of profitability. When performance of the company is higher

at the end of financial year, then they predict that it will provide high quality of goods and

services at the lower prices.

The usefulness of financial statement is different for different persons, which are given as below:

Shareholders- The increased profitability and good status of the business in terms high financial

positive will assure investors that their wealth is secured with the business and they will get

higher future returns in form of dividends. Further, when new or potential shareholders going to

make investment in the company then easily able to assess with the financial statements that it is

viable for putting money or not. In addition to this, capability of the firm in terms of providing

dividend or return on the invested amount also can be determined in proper direction

(Bebbington, Unerman and O'Dwyer, 2014).

Creditors- the increased profits shown in the financial statement shows higher credibility of the

firm to pay all the creditors in given time without any kind of financial risks. The creditors use

the financial statements in order to analyse creditworthiness of the company and on the basis of

that, they able to purchase goods and services on the credit.

Employee- An employee is regarded as one of the most important stakeholders of an

organisation as their needs and expectations need to be fulfilled by the business. Financial

statements are useful to employees for job security, salary and employee benefits expectations.

3

Government & regulatory authorities – Government is one of the highly significant stakeholder

of the company which needs financial reports in order to assess tax payable of the firm in every

tax year. In addition to this, the regulatory framework easily able to derive that, management is

whether using all the legal rules and regulations while operating in the industry or not (Frieden ,

2016).

1.4

There are some differences among management and financial accounting which are

mentioned as below:

Definition- Management accounting of all the business transactions takes place by

emphasising more on the costs control approach adopted by an organisation (DRURY,

2013). On the other hand financial accounting helps to ascertain the amount of profit.

Parties involved- Management accounting is a kind of method that provides all

accounting information delivered to the management team in order to make decision

regarding costs control. On the contrary, financial accounting provides detailed oriented

results to the shareholders as their money are invested in the business.

Legal obligations- Under financial accounting there is a requirement to follow all the

standard accounting standards and practices imposed by external authorities on the

internal business in form of IFRS categories (Denison, 2010). On the other hand,

management accounting is required to fulfil all the requirements framed by the

management by considering different cost centres.

Information type- Management accountant focuses on both kinds of information

whether qualitative or quantitative information supplied from lower management to the

top level business managers. On the other hand, financial accountants only focuses on the

financial aspects of an entity.

Scope- The role of management accounting is higher compared to the financial

accountant as the focus of management accountancy is wider. Management accounting

covers each and every aspects of an organisation but in case of financial accounting only

monetary transactions are taken into consideration. Financial accounting is related to all

the transactions in monetary forms and rest all transactions are simply ignored by the

business concern.

4

of the company which needs financial reports in order to assess tax payable of the firm in every

tax year. In addition to this, the regulatory framework easily able to derive that, management is

whether using all the legal rules and regulations while operating in the industry or not (Frieden ,

2016).

1.4

There are some differences among management and financial accounting which are

mentioned as below:

Definition- Management accounting of all the business transactions takes place by

emphasising more on the costs control approach adopted by an organisation (DRURY,

2013). On the other hand financial accounting helps to ascertain the amount of profit.

Parties involved- Management accounting is a kind of method that provides all

accounting information delivered to the management team in order to make decision

regarding costs control. On the contrary, financial accounting provides detailed oriented

results to the shareholders as their money are invested in the business.

Legal obligations- Under financial accounting there is a requirement to follow all the

standard accounting standards and practices imposed by external authorities on the

internal business in form of IFRS categories (Denison, 2010). On the other hand,

management accounting is required to fulfil all the requirements framed by the

management by considering different cost centres.

Information type- Management accountant focuses on both kinds of information

whether qualitative or quantitative information supplied from lower management to the

top level business managers. On the other hand, financial accountants only focuses on the

financial aspects of an entity.

Scope- The role of management accounting is higher compared to the financial

accountant as the focus of management accountancy is wider. Management accounting

covers each and every aspects of an organisation but in case of financial accounting only

monetary transactions are taken into consideration. Financial accounting is related to all

the transactions in monetary forms and rest all transactions are simply ignored by the

business concern.

4

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1.5

The standard budgetary control process helps an entity to make good business decisions

by following a standard procedure which is outlined below:

Forecast- the primary nature of budgeting is to forecast future income and expenses by

preparing its existing business for the future (Davis and Caldeira, 2010). It is also known

as simulation technique which helps to bring all positive and negative aspects.

Determining values- It is essential to find out the components involved after forecasting

the business such as defining various standards in increasing the performance of an

entity.

Recording- It involves recording of actual figures in order to compare the actual output

with the budgeted output in comparison with the standard quality.

Corrective actions- Budget is one of the functions of controlling as the adverse

conditions found in the budget will be rectified by taking corrective actions in order to

ensure that the compliance is the basic policy of an enterprise. Budget, is to be prepared

for monthly basis and can be reviewed by the management on half yearly basis as well as

annually and both as well.

1.6

There are different kinds of pricing techniques which can be adopted by an organisation

which are given as below:

Cost plus pricing- It is commonly used technique as every business wants to earn profit by

incorporating some percentage of profit along with all the costs involved in producing product.

The cost of goods is included in the pricing with a profit percentage included on top of this cost

of goods price. For example: If cost is worth of 200 GBP and desired profit percentage are like

13% then price of the product will be worth of 226 GBP (200 + 13%).

Value based pricing- Another form of pricing involves perception of the value of the customers

such as tastes and preferences are taken into consideration in determining the prices (Investment

decisions, 2016). The budget and needs of customers are taken into considerations by

ascertaining prices.

5

The standard budgetary control process helps an entity to make good business decisions

by following a standard procedure which is outlined below:

Forecast- the primary nature of budgeting is to forecast future income and expenses by

preparing its existing business for the future (Davis and Caldeira, 2010). It is also known

as simulation technique which helps to bring all positive and negative aspects.

Determining values- It is essential to find out the components involved after forecasting

the business such as defining various standards in increasing the performance of an

entity.

Recording- It involves recording of actual figures in order to compare the actual output

with the budgeted output in comparison with the standard quality.

Corrective actions- Budget is one of the functions of controlling as the adverse

conditions found in the budget will be rectified by taking corrective actions in order to

ensure that the compliance is the basic policy of an enterprise. Budget, is to be prepared

for monthly basis and can be reviewed by the management on half yearly basis as well as

annually and both as well.

1.6

There are different kinds of pricing techniques which can be adopted by an organisation

which are given as below:

Cost plus pricing- It is commonly used technique as every business wants to earn profit by

incorporating some percentage of profit along with all the costs involved in producing product.

The cost of goods is included in the pricing with a profit percentage included on top of this cost

of goods price. For example: If cost is worth of 200 GBP and desired profit percentage are like

13% then price of the product will be worth of 226 GBP (200 + 13%).

Value based pricing- Another form of pricing involves perception of the value of the customers

such as tastes and preferences are taken into consideration in determining the prices (Investment

decisions, 2016). The budget and needs of customers are taken into considerations by

ascertaining prices.

5

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

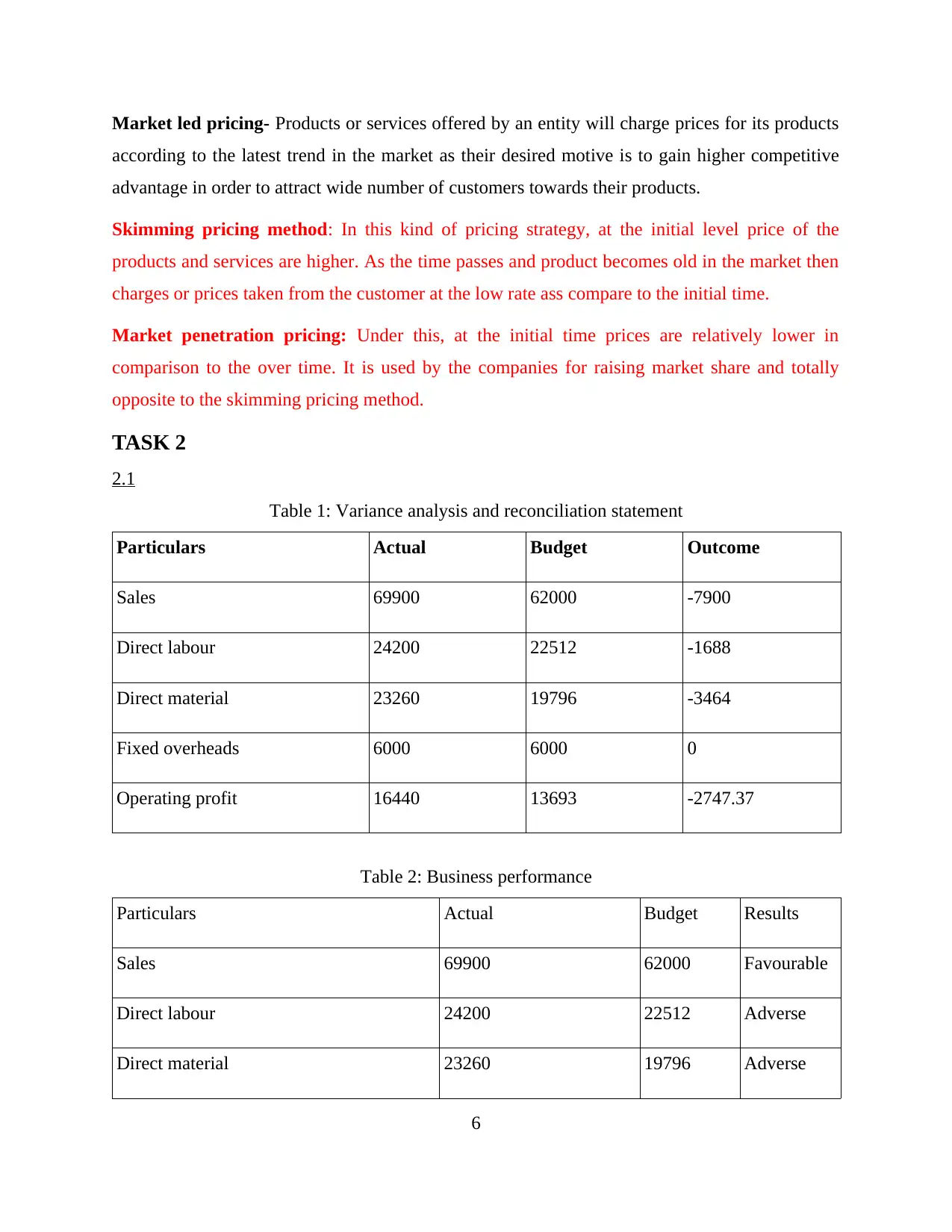

Market led pricing- Products or services offered by an entity will charge prices for its products

according to the latest trend in the market as their desired motive is to gain higher competitive

advantage in order to attract wide number of customers towards their products.

Skimming pricing method: In this kind of pricing strategy, at the initial level price of the

products and services are higher. As the time passes and product becomes old in the market then

charges or prices taken from the customer at the low rate ass compare to the initial time.

Market penetration pricing: Under this, at the initial time prices are relatively lower in

comparison to the over time. It is used by the companies for raising market share and totally

opposite to the skimming pricing method.

TASK 2

2.1

Table 1: Variance analysis and reconciliation statement

Particulars Actual Budget Outcome

Sales 69900 62000 -7900

Direct labour 24200 22512 -1688

Direct material 23260 19796 -3464

Fixed overheads 6000 6000 0

Operating profit 16440 13693 -2747.37

Table 2: Business performance

Particulars Actual Budget Results

Sales 69900 62000 Favourable

Direct labour 24200 22512 Adverse

Direct material 23260 19796 Adverse

6

according to the latest trend in the market as their desired motive is to gain higher competitive

advantage in order to attract wide number of customers towards their products.

Skimming pricing method: In this kind of pricing strategy, at the initial level price of the

products and services are higher. As the time passes and product becomes old in the market then

charges or prices taken from the customer at the low rate ass compare to the initial time.

Market penetration pricing: Under this, at the initial time prices are relatively lower in

comparison to the over time. It is used by the companies for raising market share and totally

opposite to the skimming pricing method.

TASK 2

2.1

Table 1: Variance analysis and reconciliation statement

Particulars Actual Budget Outcome

Sales 69900 62000 -7900

Direct labour 24200 22512 -1688

Direct material 23260 19796 -3464

Fixed overheads 6000 6000 0

Operating profit 16440 13693 -2747.37

Table 2: Business performance

Particulars Actual Budget Results

Sales 69900 62000 Favourable

Direct labour 24200 22512 Adverse

Direct material 23260 19796 Adverse

6

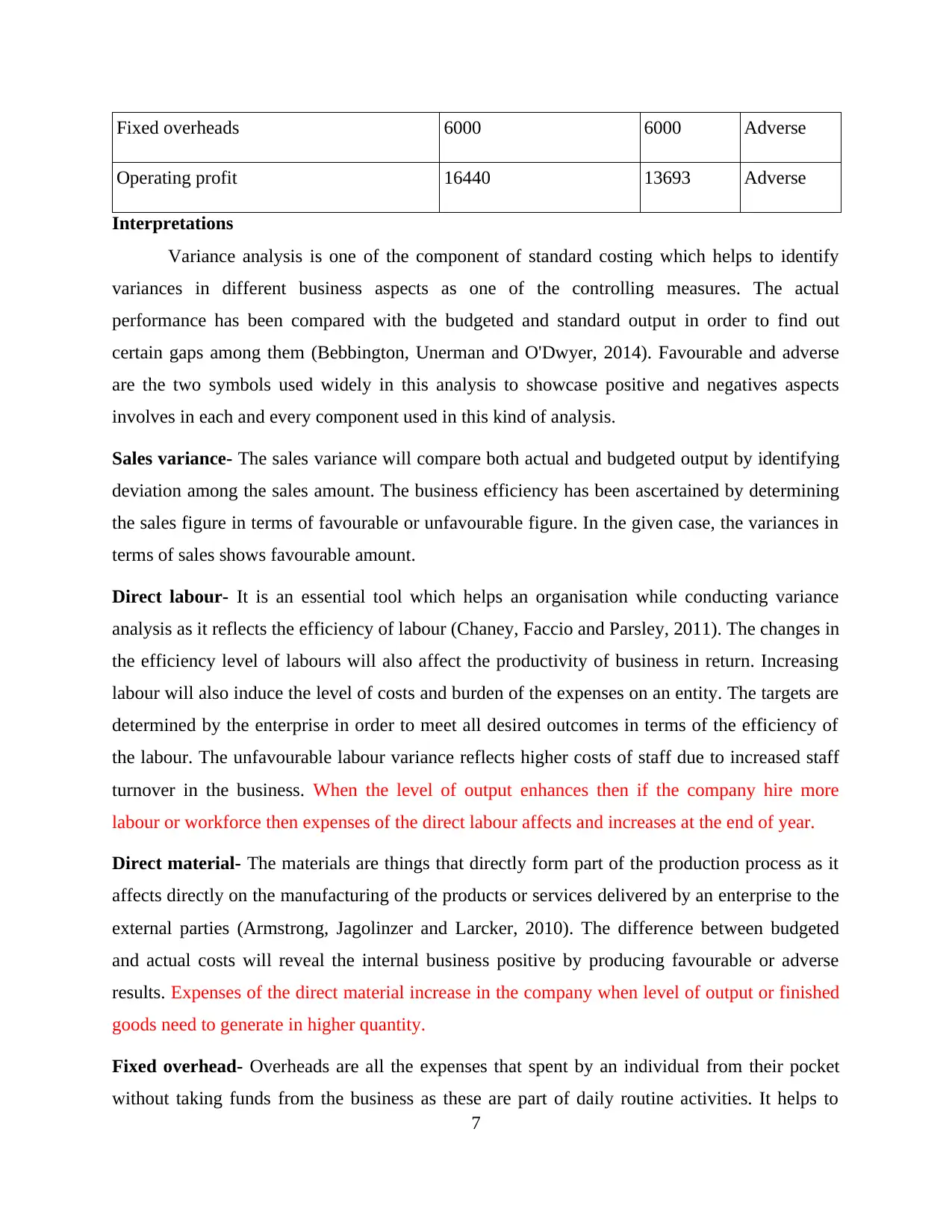

Fixed overheads 6000 6000 Adverse

Operating profit 16440 13693 Adverse

Interpretations

Variance analysis is one of the component of standard costing which helps to identify

variances in different business aspects as one of the controlling measures. The actual

performance has been compared with the budgeted and standard output in order to find out

certain gaps among them (Bebbington, Unerman and O'Dwyer, 2014). Favourable and adverse

are the two symbols used widely in this analysis to showcase positive and negatives aspects

involves in each and every component used in this kind of analysis.

Sales variance- The sales variance will compare both actual and budgeted output by identifying

deviation among the sales amount. The business efficiency has been ascertained by determining

the sales figure in terms of favourable or unfavourable figure. In the given case, the variances in

terms of sales shows favourable amount.

Direct labour- It is an essential tool which helps an organisation while conducting variance

analysis as it reflects the efficiency of labour (Chaney, Faccio and Parsley, 2011). The changes in

the efficiency level of labours will also affect the productivity of business in return. Increasing

labour will also induce the level of costs and burden of the expenses on an entity. The targets are

determined by the enterprise in order to meet all desired outcomes in terms of the efficiency of

the labour. The unfavourable labour variance reflects higher costs of staff due to increased staff

turnover in the business. When the level of output enhances then if the company hire more

labour or workforce then expenses of the direct labour affects and increases at the end of year.

Direct material- The materials are things that directly form part of the production process as it

affects directly on the manufacturing of the products or services delivered by an enterprise to the

external parties (Armstrong, Jagolinzer and Larcker, 2010). The difference between budgeted

and actual costs will reveal the internal business positive by producing favourable or adverse

results. Expenses of the direct material increase in the company when level of output or finished

goods need to generate in higher quantity.

Fixed overhead- Overheads are all the expenses that spent by an individual from their pocket

without taking funds from the business as these are part of daily routine activities. It helps to

7

Operating profit 16440 13693 Adverse

Interpretations

Variance analysis is one of the component of standard costing which helps to identify

variances in different business aspects as one of the controlling measures. The actual

performance has been compared with the budgeted and standard output in order to find out

certain gaps among them (Bebbington, Unerman and O'Dwyer, 2014). Favourable and adverse

are the two symbols used widely in this analysis to showcase positive and negatives aspects

involves in each and every component used in this kind of analysis.

Sales variance- The sales variance will compare both actual and budgeted output by identifying

deviation among the sales amount. The business efficiency has been ascertained by determining

the sales figure in terms of favourable or unfavourable figure. In the given case, the variances in

terms of sales shows favourable amount.

Direct labour- It is an essential tool which helps an organisation while conducting variance

analysis as it reflects the efficiency of labour (Chaney, Faccio and Parsley, 2011). The changes in

the efficiency level of labours will also affect the productivity of business in return. Increasing

labour will also induce the level of costs and burden of the expenses on an entity. The targets are

determined by the enterprise in order to meet all desired outcomes in terms of the efficiency of

the labour. The unfavourable labour variance reflects higher costs of staff due to increased staff

turnover in the business. When the level of output enhances then if the company hire more

labour or workforce then expenses of the direct labour affects and increases at the end of year.

Direct material- The materials are things that directly form part of the production process as it

affects directly on the manufacturing of the products or services delivered by an enterprise to the

external parties (Armstrong, Jagolinzer and Larcker, 2010). The difference between budgeted

and actual costs will reveal the internal business positive by producing favourable or adverse

results. Expenses of the direct material increase in the company when level of output or finished

goods need to generate in higher quantity.

Fixed overhead- Overheads are all the expenses that spent by an individual from their pocket

without taking funds from the business as these are part of daily routine activities. It helps to

7

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

found out increase or decrease in the fixed cost expenses that may occur in the products offered

by the firm to lure the customers. If expenses of the fixed overhead are higher and output is not

accordingly then it can be said that results of it are in the unfavourable conditions.

Strengths and weaknesses of budgeting:

Strengths:

It helps to the firm for deriving future financial performance of it at the current times.

Useful for allocating financial resources in adequate direction.

Supportive to establish effective co-ordination among organisational functions.

Provide the overall delegation framework within business enterprise.

Helpful to prepare effectual business strategies to meet with the desired objectives and

aims.

Weaknesses:

Based on assumptions rather than the actual figures by which effective business decisions

affect up to the certain extent.

It can create disputes and conflicts at workplace with different organisational

departments.

Some inaccuracies always remain with the budget which is one of the high negativity of

budgeting.

TASK 3

3.1

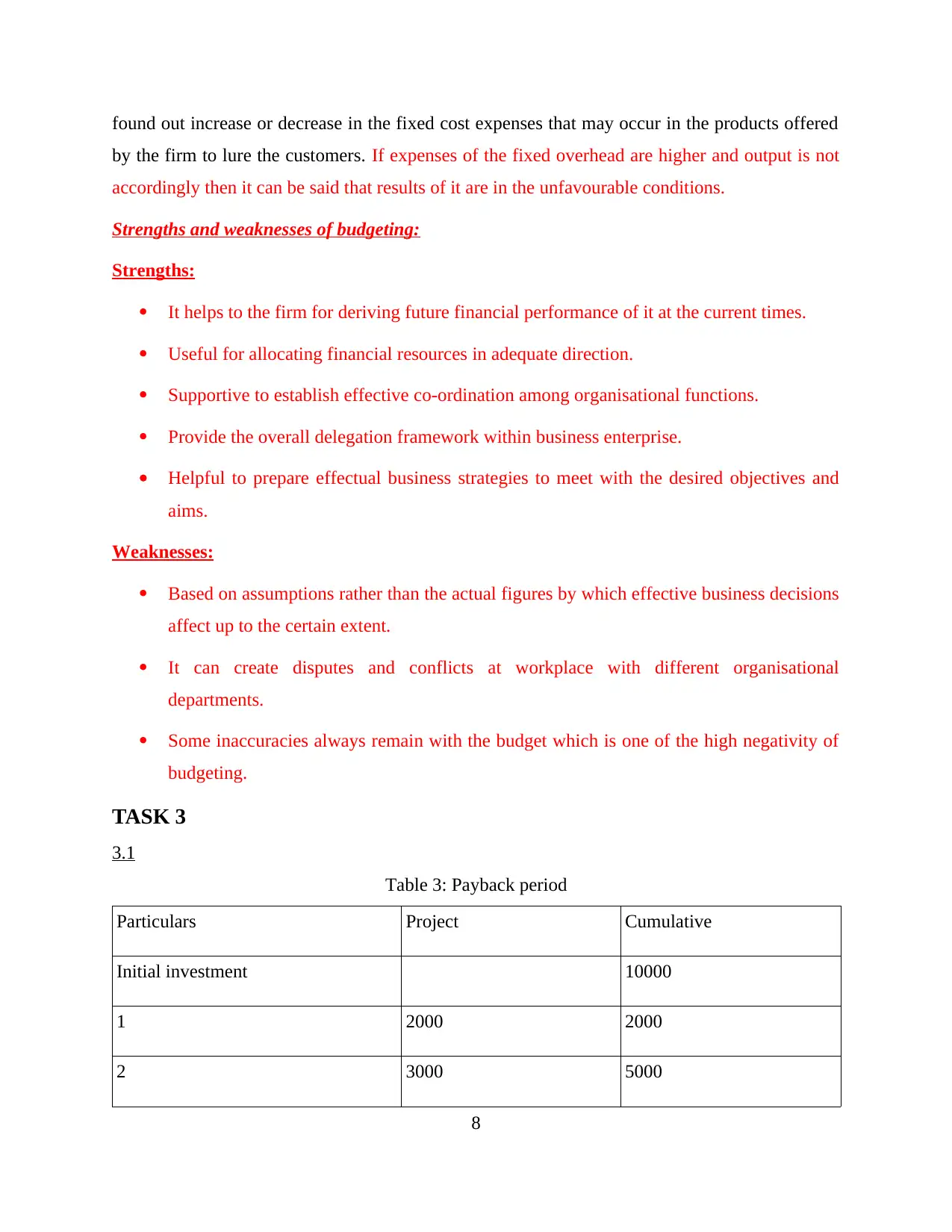

Table 3: Payback period

Particulars Project Cumulative

Initial investment 10000

1 2000 2000

2 3000 5000

8

by the firm to lure the customers. If expenses of the fixed overhead are higher and output is not

accordingly then it can be said that results of it are in the unfavourable conditions.

Strengths and weaknesses of budgeting:

Strengths:

It helps to the firm for deriving future financial performance of it at the current times.

Useful for allocating financial resources in adequate direction.

Supportive to establish effective co-ordination among organisational functions.

Provide the overall delegation framework within business enterprise.

Helpful to prepare effectual business strategies to meet with the desired objectives and

aims.

Weaknesses:

Based on assumptions rather than the actual figures by which effective business decisions

affect up to the certain extent.

It can create disputes and conflicts at workplace with different organisational

departments.

Some inaccuracies always remain with the budget which is one of the high negativity of

budgeting.

TASK 3

3.1

Table 3: Payback period

Particulars Project Cumulative

Initial investment 10000

1 2000 2000

2 3000 5000

8

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

3 3000 8000

4 5000 13000

5 5000 18000

6 3000 21000

Payback period= 3+ 8000/5000=4.6 years

Interpretations

Payback period is one of the technique of capital budgeting which help top assess the

viability of the project in terms of time factor (Dechow, 2011). It is the technique that helps to

evaluate the capacity of the proposal in order to generate higher profit returns in less period of

time in proportion to their initial investment imposed by an individual in a project (Denison,

2010). As per the above project, the payback period of the proposal is 4.6 years out of 6 years,

which is the overall life of a project so this should not be selected according to their payback

period as it is higher.

Traditional technique of capital budgeting states that an entity will generate higher sales

and the revenue from a particular business project in order to assess the overall returns produces

by the business in a particular time period. Lower the time period to recoup costs in a project, the

higher the overall return generated by them in a particular financial year.

Strengths of Payback period:

It is very simple to perform calculation as well as easy to determine interpretations.

Useful for managers in order to make quick evaluations and make decisions.

Risks of the investment can be easily derived along with the amount as well.

Weaknesses of Payback period:

It ignores cash flows of all the years which included in the company.

Not use time value of the money at the time of making calculation.

9

4 5000 13000

5 5000 18000

6 3000 21000

Payback period= 3+ 8000/5000=4.6 years

Interpretations

Payback period is one of the technique of capital budgeting which help top assess the

viability of the project in terms of time factor (Dechow, 2011). It is the technique that helps to

evaluate the capacity of the proposal in order to generate higher profit returns in less period of

time in proportion to their initial investment imposed by an individual in a project (Denison,

2010). As per the above project, the payback period of the proposal is 4.6 years out of 6 years,

which is the overall life of a project so this should not be selected according to their payback

period as it is higher.

Traditional technique of capital budgeting states that an entity will generate higher sales

and the revenue from a particular business project in order to assess the overall returns produces

by the business in a particular time period. Lower the time period to recoup costs in a project, the

higher the overall return generated by them in a particular financial year.

Strengths of Payback period:

It is very simple to perform calculation as well as easy to determine interpretations.

Useful for managers in order to make quick evaluations and make decisions.

Risks of the investment can be easily derived along with the amount as well.

Weaknesses of Payback period:

It ignores cash flows of all the years which included in the company.

Not use time value of the money at the time of making calculation.

9

Not effective to make comparison between two or more projects.

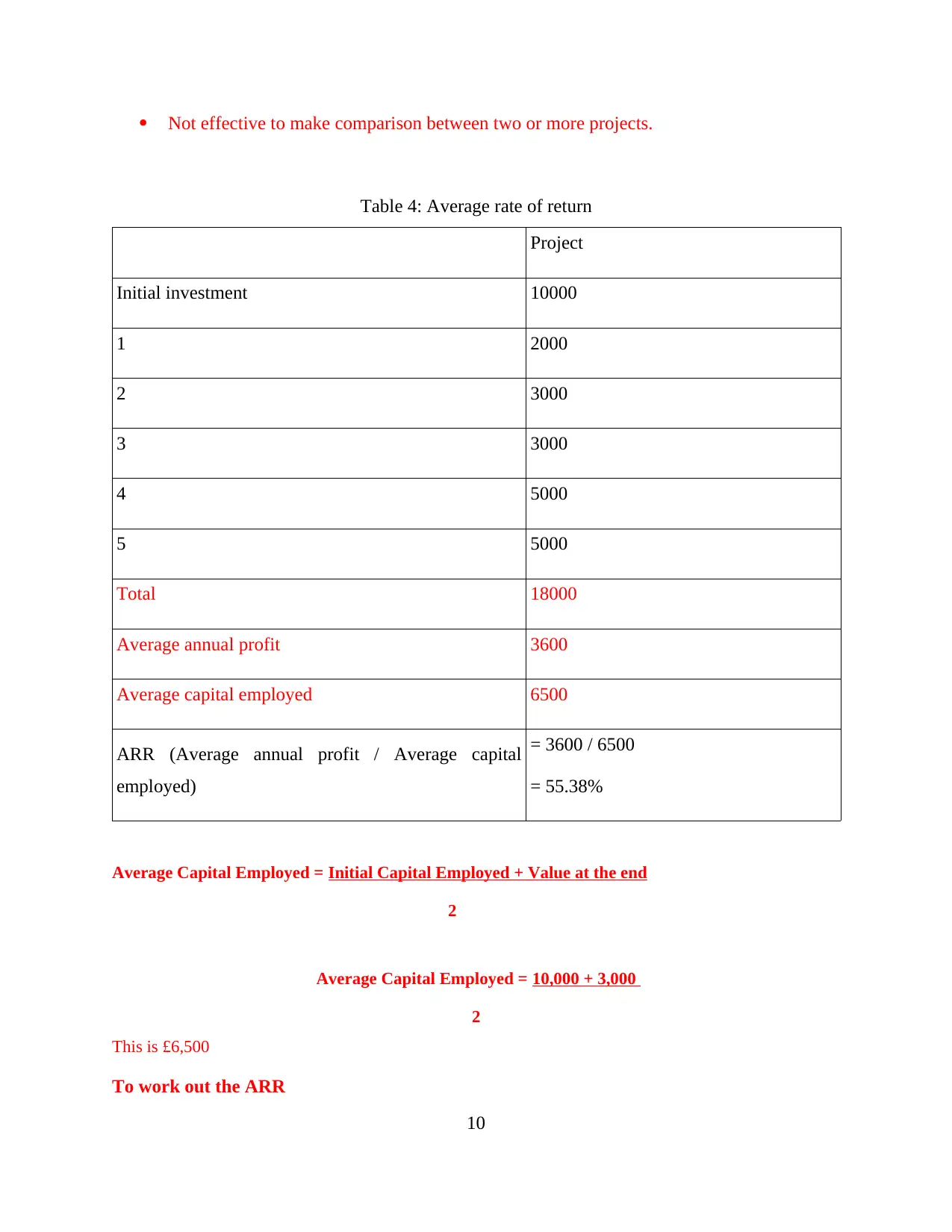

Table 4: Average rate of return

Project

Initial investment 10000

1 2000

2 3000

3 3000

4 5000

5 5000

Total 18000

Average annual profit 3600

Average capital employed 6500

ARR (Average annual profit / Average capital

employed)

= 3600 / 6500

= 55.38%

Average Capital Employed = Initial Capital Employed + Value at the end

2

Average Capital Employed = 10,000 + 3,000

2

This is £6,500

To work out the ARR

10

Table 4: Average rate of return

Project

Initial investment 10000

1 2000

2 3000

3 3000

4 5000

5 5000

Total 18000

Average annual profit 3600

Average capital employed 6500

ARR (Average annual profit / Average capital

employed)

= 3600 / 6500

= 55.38%

Average Capital Employed = Initial Capital Employed + Value at the end

2

Average Capital Employed = 10,000 + 3,000

2

This is £6,500

To work out the ARR

10

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 18

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.