Financial Analysis of Tesco PLC: Ratio, Budgeting, and Investment

VerifiedAdded on 2023/01/09

|18

|4221

|24

Report

AI Summary

This report provides a comprehensive financial analysis of Tesco PLC, focusing on key aspects relevant to finance managers. It begins with an introduction to the importance of finance in business organizations and its role in decision-making. The report then delves into a detailed examination of Tesco's financial performance, including an analysis of its mission and vision based on auditor reports and financial statements. It presents a thorough ratio analysis covering liquidity, profitability, efficiency, and stability ratios, comparing the company's performance over several years. The report also includes comparative analyses of the income statement and balance sheet, highlighting trends and significant changes. Furthermore, it explores budgeting plans, emphasizing the importance of SMART goals and the identification of limiting factors. Finally, the report discusses capital investment decisions and their impact on the company's financial health, providing a well-rounded perspective on Tesco's financial management practices and performance.

Finance for managers

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

TABLE OF CONTENTS

INTRODUCTION......................................................................................................................3

Task 1.........................................................................................................................................3

1.1...........................................................................................................................................3

1.2...........................................................................................................................................3

1.3...........................................................................................................................................5

1.4...........................................................................................................................................7

Task 2.........................................................................................................................................7

2.1...........................................................................................................................................7

2.2...........................................................................................................................................9

2.3...........................................................................................................................................9

Task 3.......................................................................................................................................10

3.1.........................................................................................................................................10

3.2.........................................................................................................................................10

3.3.........................................................................................................................................12

CONCLUSION........................................................................................................................13

REFERENCES.........................................................................................................................14

INTRODUCTION......................................................................................................................3

Task 1.........................................................................................................................................3

1.1...........................................................................................................................................3

1.2...........................................................................................................................................3

1.3...........................................................................................................................................5

1.4...........................................................................................................................................7

Task 2.........................................................................................................................................7

2.1...........................................................................................................................................7

2.2...........................................................................................................................................9

2.3...........................................................................................................................................9

Task 3.......................................................................................................................................10

3.1.........................................................................................................................................10

3.2.........................................................................................................................................10

3.3.........................................................................................................................................12

CONCLUSION........................................................................................................................13

REFERENCES.........................................................................................................................14

INTRODUCTION

The finance is the field of study which talks about the role and importance of finance

in a business organization along with its relevance to the users of its. It provides assistance to

the management in determining the financial performance and position of the company which

is used as the base for taking various business decisions. This report provides an insight about

the financial aspects of the Tesco plc company. It covers the ratio and comparative analysis

budgeting and capital investment decisions.

Task 1

1.1

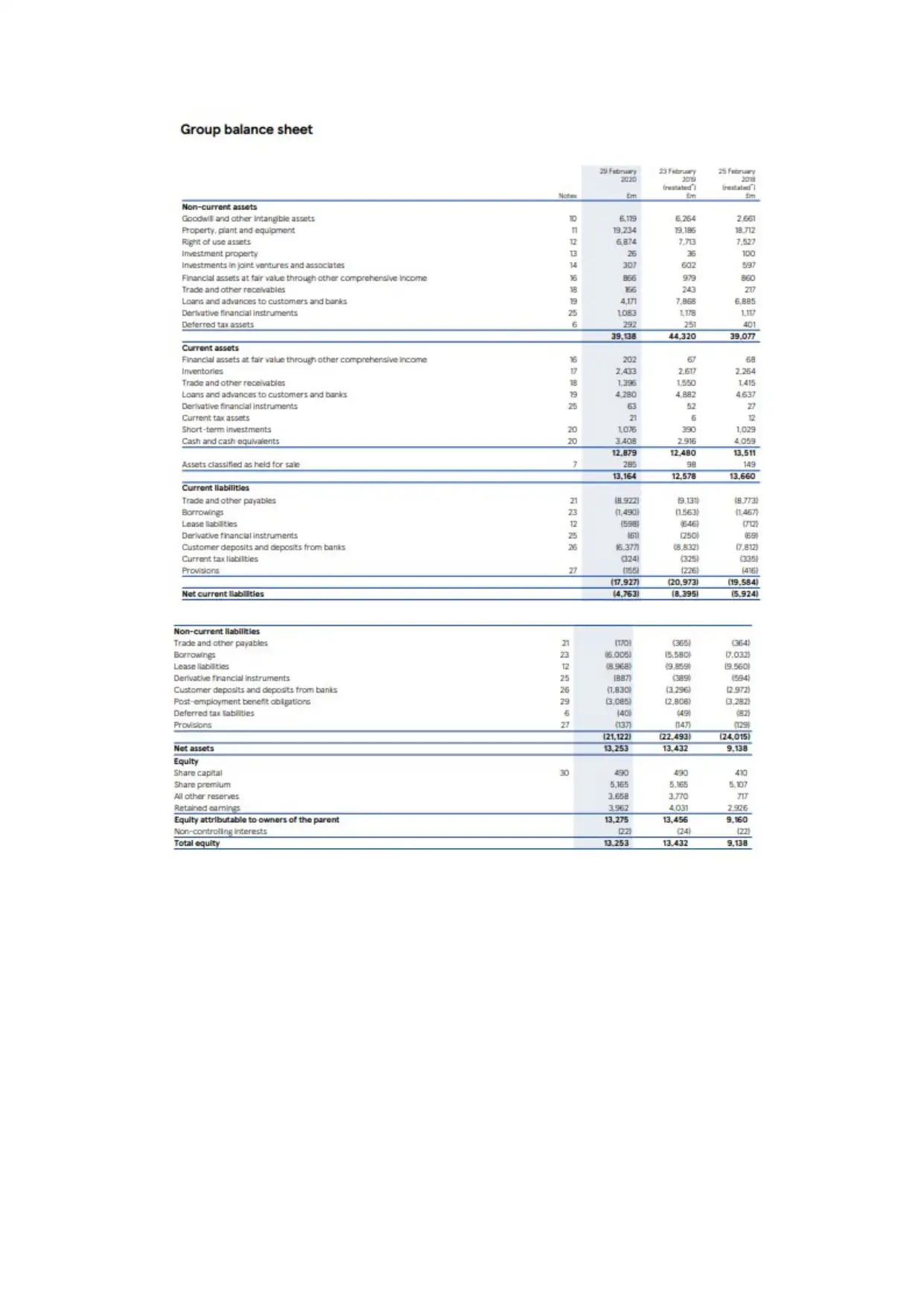

For evaluating the performance of the organization, it is very important to determine

the mission and vision of the organization which can be assessed looking at the auditors and

the director’s reports of the company (Lie and Sormin, 2016). The three important financial

statements of the company states about the flow of incomes and expenses of the company

whether it is flowing in the right direction or not. It is also used in gaining insight about the

assets and liabilities of the company. The information taken from the official website of the

company proves its validity and reliability. The three important statement are income

statement, balance sheet and the cashflow statement.

The finance is the field of study which talks about the role and importance of finance

in a business organization along with its relevance to the users of its. It provides assistance to

the management in determining the financial performance and position of the company which

is used as the base for taking various business decisions. This report provides an insight about

the financial aspects of the Tesco plc company. It covers the ratio and comparative analysis

budgeting and capital investment decisions.

Task 1

1.1

For evaluating the performance of the organization, it is very important to determine

the mission and vision of the organization which can be assessed looking at the auditors and

the director’s reports of the company (Lie and Sormin, 2016). The three important financial

statements of the company states about the flow of incomes and expenses of the company

whether it is flowing in the right direction or not. It is also used in gaining insight about the

assets and liabilities of the company. The information taken from the official website of the

company proves its validity and reliability. The three important statement are income

statement, balance sheet and the cashflow statement.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

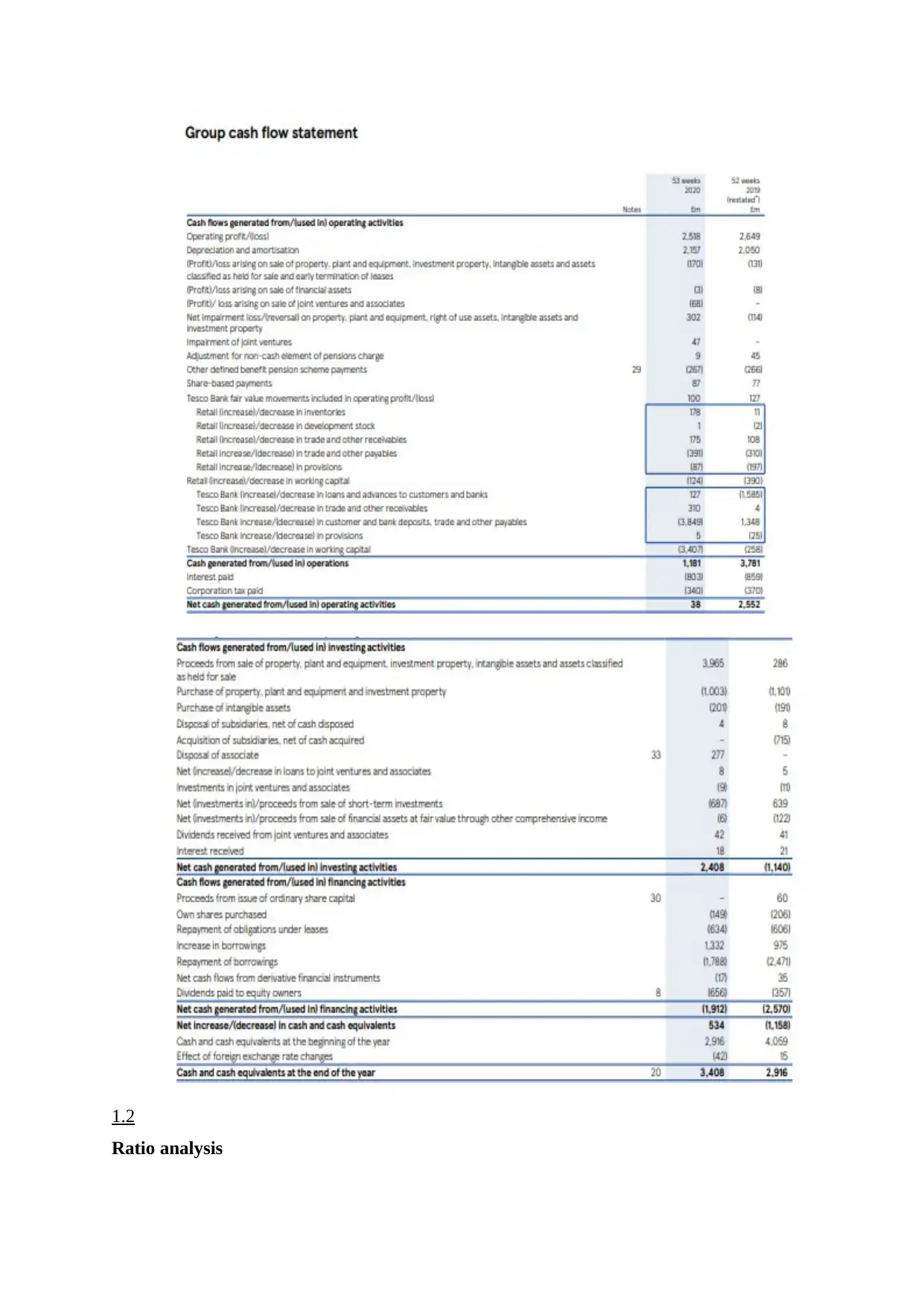

1.2

Ratio analysis

Ratio analysis

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

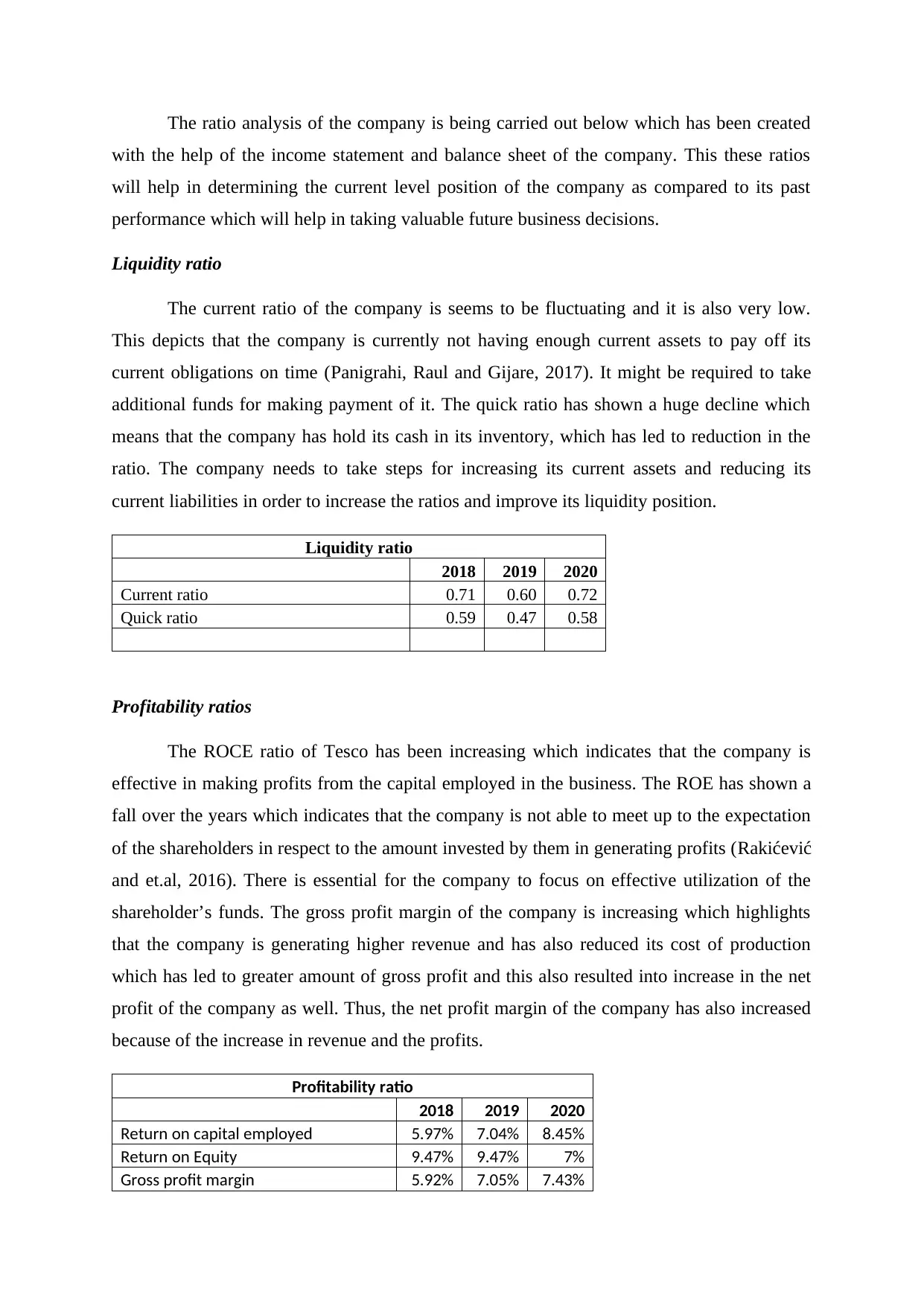

The ratio analysis of the company is being carried out below which has been created

with the help of the income statement and balance sheet of the company. This these ratios

will help in determining the current level position of the company as compared to its past

performance which will help in taking valuable future business decisions.

Liquidity ratio

The current ratio of the company is seems to be fluctuating and it is also very low.

This depicts that the company is currently not having enough current assets to pay off its

current obligations on time (Panigrahi, Raul and Gijare, 2017). It might be required to take

additional funds for making payment of it. The quick ratio has shown a huge decline which

means that the company has hold its cash in its inventory, which has led to reduction in the

ratio. The company needs to take steps for increasing its current assets and reducing its

current liabilities in order to increase the ratios and improve its liquidity position.

Liquidity ratio

2018 2019 2020

Current ratio 0.71 0.60 0.72

Quick ratio 0.59 0.47 0.58

Profitability ratios

The ROCE ratio of Tesco has been increasing which indicates that the company is

effective in making profits from the capital employed in the business. The ROE has shown a

fall over the years which indicates that the company is not able to meet up to the expectation

of the shareholders in respect to the amount invested by them in generating profits (Rakićević

and et.al, 2016). There is essential for the company to focus on effective utilization of the

shareholder’s funds. The gross profit margin of the company is increasing which highlights

that the company is generating higher revenue and has also reduced its cost of production

which has led to greater amount of gross profit and this also resulted into increase in the net

profit of the company as well. Thus, the net profit margin of the company has also increased

because of the increase in revenue and the profits.

Profitability ratio

2018 2019 2020

Return on capital employed 5.97% 7.04% 8.45%

Return on Equity 9.47% 9.47% 7%

Gross profit margin 5.92% 7.05% 7.43%

with the help of the income statement and balance sheet of the company. This these ratios

will help in determining the current level position of the company as compared to its past

performance which will help in taking valuable future business decisions.

Liquidity ratio

The current ratio of the company is seems to be fluctuating and it is also very low.

This depicts that the company is currently not having enough current assets to pay off its

current obligations on time (Panigrahi, Raul and Gijare, 2017). It might be required to take

additional funds for making payment of it. The quick ratio has shown a huge decline which

means that the company has hold its cash in its inventory, which has led to reduction in the

ratio. The company needs to take steps for increasing its current assets and reducing its

current liabilities in order to increase the ratios and improve its liquidity position.

Liquidity ratio

2018 2019 2020

Current ratio 0.71 0.60 0.72

Quick ratio 0.59 0.47 0.58

Profitability ratios

The ROCE ratio of Tesco has been increasing which indicates that the company is

effective in making profits from the capital employed in the business. The ROE has shown a

fall over the years which indicates that the company is not able to meet up to the expectation

of the shareholders in respect to the amount invested by them in generating profits (Rakićević

and et.al, 2016). There is essential for the company to focus on effective utilization of the

shareholder’s funds. The gross profit margin of the company is increasing which highlights

that the company is generating higher revenue and has also reduced its cost of production

which has led to greater amount of gross profit and this also resulted into increase in the net

profit of the company as well. Thus, the net profit margin of the company has also increased

because of the increase in revenue and the profits.

Profitability ratio

2018 2019 2020

Return on capital employed 5.97% 7.04% 8.45%

Return on Equity 9.47% 9.47% 7%

Gross profit margin 5.92% 7.05% 7.43%

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Net profit ratio 2.66% 3.96% 4.5%

Efficiency ratio:

The asset turnover ratio of Tesco has been fluctuating and in 2020 it has increased

from 2019 which means that the company is able to effectively utilize its assets in generating

higher revenue. Also, the inventory turnover ratio has increased over the period which depicts

that the company is able to sell out its stock in very quickly (Sunjoko, and ARILYN, 2016).

The a/c receivable turnover ratio has been rising but the too it is very low which means that

the organization is working on improving its credit policy and is having better collection

teams for collecting the due amount on time. On an overall basis the efficiency level of the

company is good.

Efficiency ratio

2018 2019 2020

Asset turnover ratio 1.28 1.12 1.24

Inventory turnover ratio

23.8

9

22.7

0

24.6

4

Account receivable turnover ratio 9.34 9.93

11.3

7

Stability ratio:

The Debt to equity ratio of the company has declined over the past 3 years which

means that the Tesco has started paying off its debt or has increased its equity base. This

indicates that the composition of debt in the capital structure of the company is reducing

which leads to reduction in financial burden.

Stability ratio

2018 2019 2020

Debt equity ratio 3.28 3.23 2.94

1.3

Comparative analysis

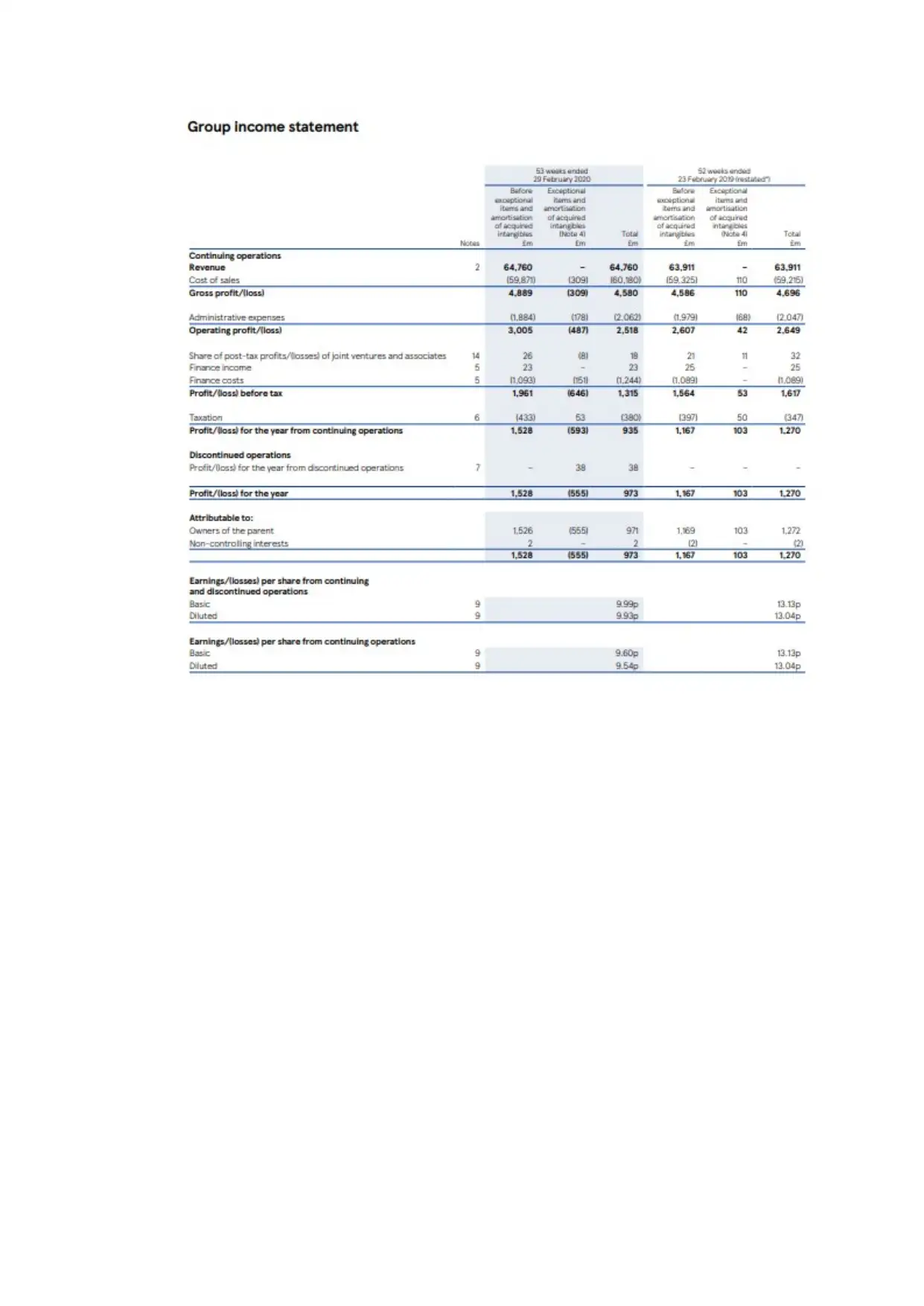

Income statement: Taking 2016 as the base year, the revenue of the company has shown an

increase of 20.07% but along with that there is an increase in the COGS by 15.83%. there is a

huge increase in the unusual expense by 135.29% which is appoint of concern for the

Efficiency ratio:

The asset turnover ratio of Tesco has been fluctuating and in 2020 it has increased

from 2019 which means that the company is able to effectively utilize its assets in generating

higher revenue. Also, the inventory turnover ratio has increased over the period which depicts

that the company is able to sell out its stock in very quickly (Sunjoko, and ARILYN, 2016).

The a/c receivable turnover ratio has been rising but the too it is very low which means that

the organization is working on improving its credit policy and is having better collection

teams for collecting the due amount on time. On an overall basis the efficiency level of the

company is good.

Efficiency ratio

2018 2019 2020

Asset turnover ratio 1.28 1.12 1.24

Inventory turnover ratio

23.8

9

22.7

0

24.6

4

Account receivable turnover ratio 9.34 9.93

11.3

7

Stability ratio:

The Debt to equity ratio of the company has declined over the past 3 years which

means that the Tesco has started paying off its debt or has increased its equity base. This

indicates that the composition of debt in the capital structure of the company is reducing

which leads to reduction in financial burden.

Stability ratio

2018 2019 2020

Debt equity ratio 3.28 3.23 2.94

1.3

Comparative analysis

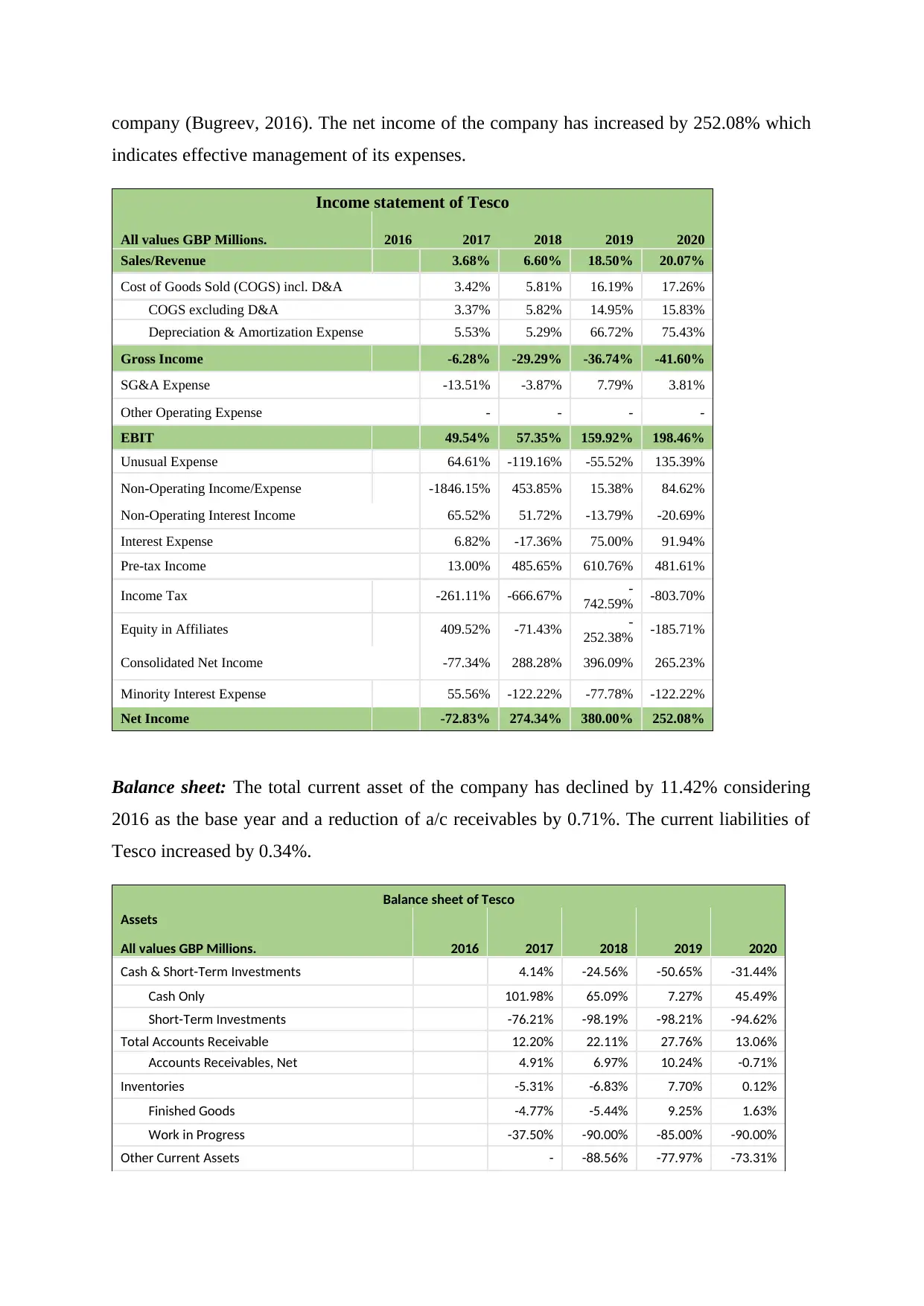

Income statement: Taking 2016 as the base year, the revenue of the company has shown an

increase of 20.07% but along with that there is an increase in the COGS by 15.83%. there is a

huge increase in the unusual expense by 135.29% which is appoint of concern for the

company (Bugreev, 2016). The net income of the company has increased by 252.08% which

indicates effective management of its expenses.

Income statement of Tesco

All values GBP Millions. 2016 2017 2018 2019 2020

Sales/Revenue 3.68% 6.60% 18.50% 20.07%

Cost of Goods Sold (COGS) incl. D&A 3.42% 5.81% 16.19% 17.26%

COGS excluding D&A 3.37% 5.82% 14.95% 15.83%

Depreciation & Amortization Expense 5.53% 5.29% 66.72% 75.43%

Gross Income -6.28% -29.29% -36.74% -41.60%

SG&A Expense -13.51% -3.87% 7.79% 3.81%

Other Operating Expense - - - -

EBIT 49.54% 57.35% 159.92% 198.46%

Unusual Expense 64.61% -119.16% -55.52% 135.39%

Non-Operating Income/Expense -1846.15% 453.85% 15.38% 84.62%

Non-Operating Interest Income 65.52% 51.72% -13.79% -20.69%

Interest Expense 6.82% -17.36% 75.00% 91.94%

Pre-tax Income 13.00% 485.65% 610.76% 481.61%

Income Tax -261.11% -666.67% -

742.59% -803.70%

Equity in Affiliates 409.52% -71.43% -

252.38% -185.71%

Consolidated Net Income -77.34% 288.28% 396.09% 265.23%

Minority Interest Expense 55.56% -122.22% -77.78% -122.22%

Net Income -72.83% 274.34% 380.00% 252.08%

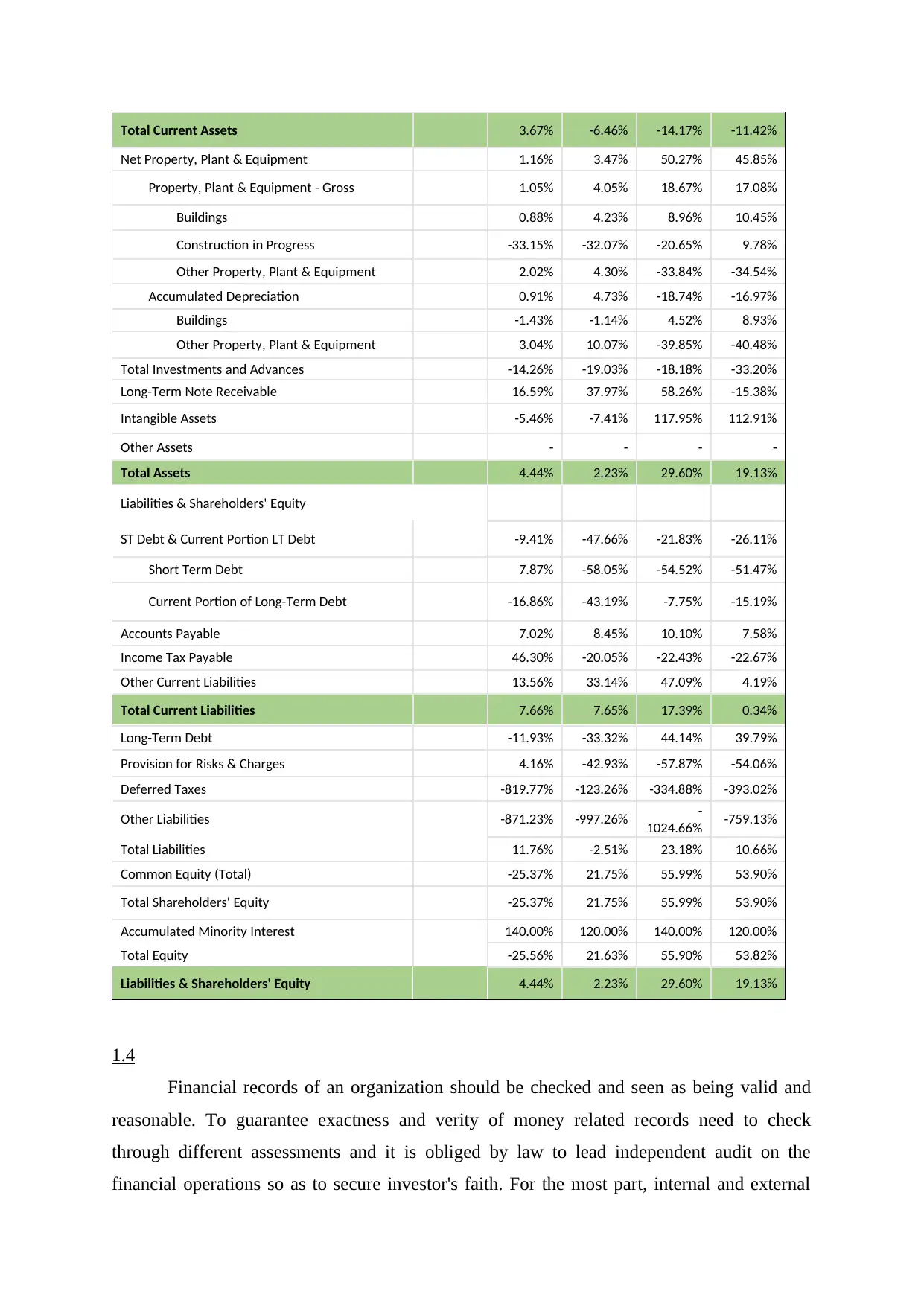

Balance sheet: The total current asset of the company has declined by 11.42% considering

2016 as the base year and a reduction of a/c receivables by 0.71%. The current liabilities of

Tesco increased by 0.34%.

Balance sheet of Tesco

Assets

All values GBP Millions. 2016 2017 2018 2019 2020

Cash & Short-Term Investments 4.14% -24.56% -50.65% -31.44%

Cash Only 101.98% 65.09% 7.27% 45.49%

Short-Term Investments -76.21% -98.19% -98.21% -94.62%

Total Accounts Receivable 12.20% 22.11% 27.76% 13.06%

Accounts Receivables, Net 4.91% 6.97% 10.24% -0.71%

Inventories -5.31% -6.83% 7.70% 0.12%

Finished Goods -4.77% -5.44% 9.25% 1.63%

Work in Progress -37.50% -90.00% -85.00% -90.00%

Other Current Assets - -88.56% -77.97% -73.31%

indicates effective management of its expenses.

Income statement of Tesco

All values GBP Millions. 2016 2017 2018 2019 2020

Sales/Revenue 3.68% 6.60% 18.50% 20.07%

Cost of Goods Sold (COGS) incl. D&A 3.42% 5.81% 16.19% 17.26%

COGS excluding D&A 3.37% 5.82% 14.95% 15.83%

Depreciation & Amortization Expense 5.53% 5.29% 66.72% 75.43%

Gross Income -6.28% -29.29% -36.74% -41.60%

SG&A Expense -13.51% -3.87% 7.79% 3.81%

Other Operating Expense - - - -

EBIT 49.54% 57.35% 159.92% 198.46%

Unusual Expense 64.61% -119.16% -55.52% 135.39%

Non-Operating Income/Expense -1846.15% 453.85% 15.38% 84.62%

Non-Operating Interest Income 65.52% 51.72% -13.79% -20.69%

Interest Expense 6.82% -17.36% 75.00% 91.94%

Pre-tax Income 13.00% 485.65% 610.76% 481.61%

Income Tax -261.11% -666.67% -

742.59% -803.70%

Equity in Affiliates 409.52% -71.43% -

252.38% -185.71%

Consolidated Net Income -77.34% 288.28% 396.09% 265.23%

Minority Interest Expense 55.56% -122.22% -77.78% -122.22%

Net Income -72.83% 274.34% 380.00% 252.08%

Balance sheet: The total current asset of the company has declined by 11.42% considering

2016 as the base year and a reduction of a/c receivables by 0.71%. The current liabilities of

Tesco increased by 0.34%.

Balance sheet of Tesco

Assets

All values GBP Millions. 2016 2017 2018 2019 2020

Cash & Short-Term Investments 4.14% -24.56% -50.65% -31.44%

Cash Only 101.98% 65.09% 7.27% 45.49%

Short-Term Investments -76.21% -98.19% -98.21% -94.62%

Total Accounts Receivable 12.20% 22.11% 27.76% 13.06%

Accounts Receivables, Net 4.91% 6.97% 10.24% -0.71%

Inventories -5.31% -6.83% 7.70% 0.12%

Finished Goods -4.77% -5.44% 9.25% 1.63%

Work in Progress -37.50% -90.00% -85.00% -90.00%

Other Current Assets - -88.56% -77.97% -73.31%

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Total Current Assets 3.67% -6.46% -14.17% -11.42%

Net Property, Plant & Equipment 1.16% 3.47% 50.27% 45.85%

Property, Plant & Equipment - Gross 1.05% 4.05% 18.67% 17.08%

Buildings 0.88% 4.23% 8.96% 10.45%

Construction in Progress -33.15% -32.07% -20.65% 9.78%

Other Property, Plant & Equipment 2.02% 4.30% -33.84% -34.54%

Accumulated Depreciation 0.91% 4.73% -18.74% -16.97%

Buildings -1.43% -1.14% 4.52% 8.93%

Other Property, Plant & Equipment 3.04% 10.07% -39.85% -40.48%

Total Investments and Advances -14.26% -19.03% -18.18% -33.20%

Long-Term Note Receivable 16.59% 37.97% 58.26% -15.38%

Intangible Assets -5.46% -7.41% 117.95% 112.91%

Other Assets - - - -

Total Assets 4.44% 2.23% 29.60% 19.13%

Liabilities & Shareholders' Equity

ST Debt & Current Portion LT Debt -9.41% -47.66% -21.83% -26.11%

Short Term Debt 7.87% -58.05% -54.52% -51.47%

Current Portion of Long-Term Debt -16.86% -43.19% -7.75% -15.19%

Accounts Payable 7.02% 8.45% 10.10% 7.58%

Income Tax Payable 46.30% -20.05% -22.43% -22.67%

Other Current Liabilities 13.56% 33.14% 47.09% 4.19%

Total Current Liabilities 7.66% 7.65% 17.39% 0.34%

Long-Term Debt -11.93% -33.32% 44.14% 39.79%

Provision for Risks & Charges 4.16% -42.93% -57.87% -54.06%

Deferred Taxes -819.77% -123.26% -334.88% -393.02%

Other Liabilities -871.23% -997.26% -

1024.66% -759.13%

Total Liabilities 11.76% -2.51% 23.18% 10.66%

Common Equity (Total) -25.37% 21.75% 55.99% 53.90%

Total Shareholders' Equity -25.37% 21.75% 55.99% 53.90%

Accumulated Minority Interest 140.00% 120.00% 140.00% 120.00%

Total Equity -25.56% 21.63% 55.90% 53.82%

Liabilities & Shareholders' Equity 4.44% 2.23% 29.60% 19.13%

1.4

Financial records of an organization should be checked and seen as being valid and

reasonable. To guarantee exactness and verity of money related records need to check

through different assessments and it is obliged by law to lead independent audit on the

financial operations so as to secure investor's faith. For the most part, internal and external

Net Property, Plant & Equipment 1.16% 3.47% 50.27% 45.85%

Property, Plant & Equipment - Gross 1.05% 4.05% 18.67% 17.08%

Buildings 0.88% 4.23% 8.96% 10.45%

Construction in Progress -33.15% -32.07% -20.65% 9.78%

Other Property, Plant & Equipment 2.02% 4.30% -33.84% -34.54%

Accumulated Depreciation 0.91% 4.73% -18.74% -16.97%

Buildings -1.43% -1.14% 4.52% 8.93%

Other Property, Plant & Equipment 3.04% 10.07% -39.85% -40.48%

Total Investments and Advances -14.26% -19.03% -18.18% -33.20%

Long-Term Note Receivable 16.59% 37.97% 58.26% -15.38%

Intangible Assets -5.46% -7.41% 117.95% 112.91%

Other Assets - - - -

Total Assets 4.44% 2.23% 29.60% 19.13%

Liabilities & Shareholders' Equity

ST Debt & Current Portion LT Debt -9.41% -47.66% -21.83% -26.11%

Short Term Debt 7.87% -58.05% -54.52% -51.47%

Current Portion of Long-Term Debt -16.86% -43.19% -7.75% -15.19%

Accounts Payable 7.02% 8.45% 10.10% 7.58%

Income Tax Payable 46.30% -20.05% -22.43% -22.67%

Other Current Liabilities 13.56% 33.14% 47.09% 4.19%

Total Current Liabilities 7.66% 7.65% 17.39% 0.34%

Long-Term Debt -11.93% -33.32% 44.14% 39.79%

Provision for Risks & Charges 4.16% -42.93% -57.87% -54.06%

Deferred Taxes -819.77% -123.26% -334.88% -393.02%

Other Liabilities -871.23% -997.26% -

1024.66% -759.13%

Total Liabilities 11.76% -2.51% 23.18% 10.66%

Common Equity (Total) -25.37% 21.75% 55.99% 53.90%

Total Shareholders' Equity -25.37% 21.75% 55.99% 53.90%

Accumulated Minority Interest 140.00% 120.00% 140.00% 120.00%

Total Equity -25.56% 21.63% 55.90% 53.82%

Liabilities & Shareholders' Equity 4.44% 2.23% 29.60% 19.13%

1.4

Financial records of an organization should be checked and seen as being valid and

reasonable. To guarantee exactness and verity of money related records need to check

through different assessments and it is obliged by law to lead independent audit on the

financial operations so as to secure investor's faith. For the most part, internal and external

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

reviewers (auditors) are answerable for guaranteeing precision and verity of money related

records. There are chances that the information presented in the financial records are

manipulated which result into depicting the wrong financial position and performance of the

business. Therefore, external auditing should be carried out.

Task 2

2.1

Budgeting plan gives extensive money related outline of planned organization

activity. An organization's targets budgeting plan is the general money related arrangement

demonstrating use of the accessible assets. Tesco’s financial plan is driven by the aims and

targets of the company along with what it can really achieve (Wang and Yao, 2017).

Numerous factors in a business can be planned which incorporates sales, yield, cost -

(variable and fixed), benefits, income, capital venture. Financial plan ought to be SMART,

that is, specific, feasible (measurable), achievable and reasonable, and with time bound or

else the budgeting will be inadequate.

Vital goal of Tesco is the principal factor that is required to be viewed as when

figuring budgeting plans in light of the fact that unaligned financial plan with vital aims and

objectives lead to disappointment. The subsequent stage of planning is recognizing the

limiting variable that the association is confronted with which is known as constraints which

might be a cut-off on the quantity of products a business could sell (demand is constraining

element) or on the quantity of hours a specific kind of workforce could work and so forth.

When association recognizes the limiting element, they set the budgetary guideline (Vidal-

Carreras, Garcia-Sabater and Garcia-Sabater, 2017). The subsequent stage is assessment and

coordination of inner elements for example abilities of representatives and assets and draft

departmental financial plan. After this progression, the association ought to evaluate the

outside affecting component, for example, estimated economic, political and global condition

which assists with limiting the risk associated with the financial plan. At last, organization

need to arrange the whole departmental budgeting plan for example sales plan, production

financial plan, material and labour spending plan, overhead budget which is called as the

master budget.

The master budget plan is a synopsis of an organization's arrangements that sets

explicit goals for the sales, manufacturing, appropriation and financing exercises which for

records. There are chances that the information presented in the financial records are

manipulated which result into depicting the wrong financial position and performance of the

business. Therefore, external auditing should be carried out.

Task 2

2.1

Budgeting plan gives extensive money related outline of planned organization

activity. An organization's targets budgeting plan is the general money related arrangement

demonstrating use of the accessible assets. Tesco’s financial plan is driven by the aims and

targets of the company along with what it can really achieve (Wang and Yao, 2017).

Numerous factors in a business can be planned which incorporates sales, yield, cost -

(variable and fixed), benefits, income, capital venture. Financial plan ought to be SMART,

that is, specific, feasible (measurable), achievable and reasonable, and with time bound or

else the budgeting will be inadequate.

Vital goal of Tesco is the principal factor that is required to be viewed as when

figuring budgeting plans in light of the fact that unaligned financial plan with vital aims and

objectives lead to disappointment. The subsequent stage of planning is recognizing the

limiting variable that the association is confronted with which is known as constraints which

might be a cut-off on the quantity of products a business could sell (demand is constraining

element) or on the quantity of hours a specific kind of workforce could work and so forth.

When association recognizes the limiting element, they set the budgetary guideline (Vidal-

Carreras, Garcia-Sabater and Garcia-Sabater, 2017). The subsequent stage is assessment and

coordination of inner elements for example abilities of representatives and assets and draft

departmental financial plan. After this progression, the association ought to evaluate the

outside affecting component, for example, estimated economic, political and global condition

which assists with limiting the risk associated with the financial plan. At last, organization

need to arrange the whole departmental budgeting plan for example sales plan, production

financial plan, material and labour spending plan, overhead budget which is called as the

master budget.

The master budget plan is a synopsis of an organization's arrangements that sets

explicit goals for the sales, manufacturing, appropriation and financing exercises which for

the most part comes full circle in a cash budgeting plan, a planned income statement and a

planned balance sheet report.

The master budget begins with sales anticipating which should be possible by top to

bottom investigation of past sales pattern, estimation made by the relevant business or

workforces, general monetary condition, contender's activities, change in the association's

costs, change in item mic, statistical surveying, publicizing and sales advancement plans.

Sales evaluating prompts the sales spending plan that is a definite timetable indicating the

expected sales for the spending time frame. It very well may be communicated in units and

money both. The sales financial plan is the fundamental pillar of the master budget (Marzlin

Marzuki and Ismail, 2019). The following financial plan is production budget which decides

amount of manufacturing relies on the quantity of units to be sold and upon the quantity of

units in the closure and opening inventories. Another segment of spending plan is material

budget plan which shows the amount and cost of buying material for planned production and

inventories. The labour budget shows the financial plan for all sort of work for example

skilled and unskilled which rely on the level of production. Another spending plan is the

overhead spending that shows amounts of an enormous number of items of expenses for

example compensation, power, lease, administrative costs. After this association get ready

projected income statement, balance sheet and the cash budget.

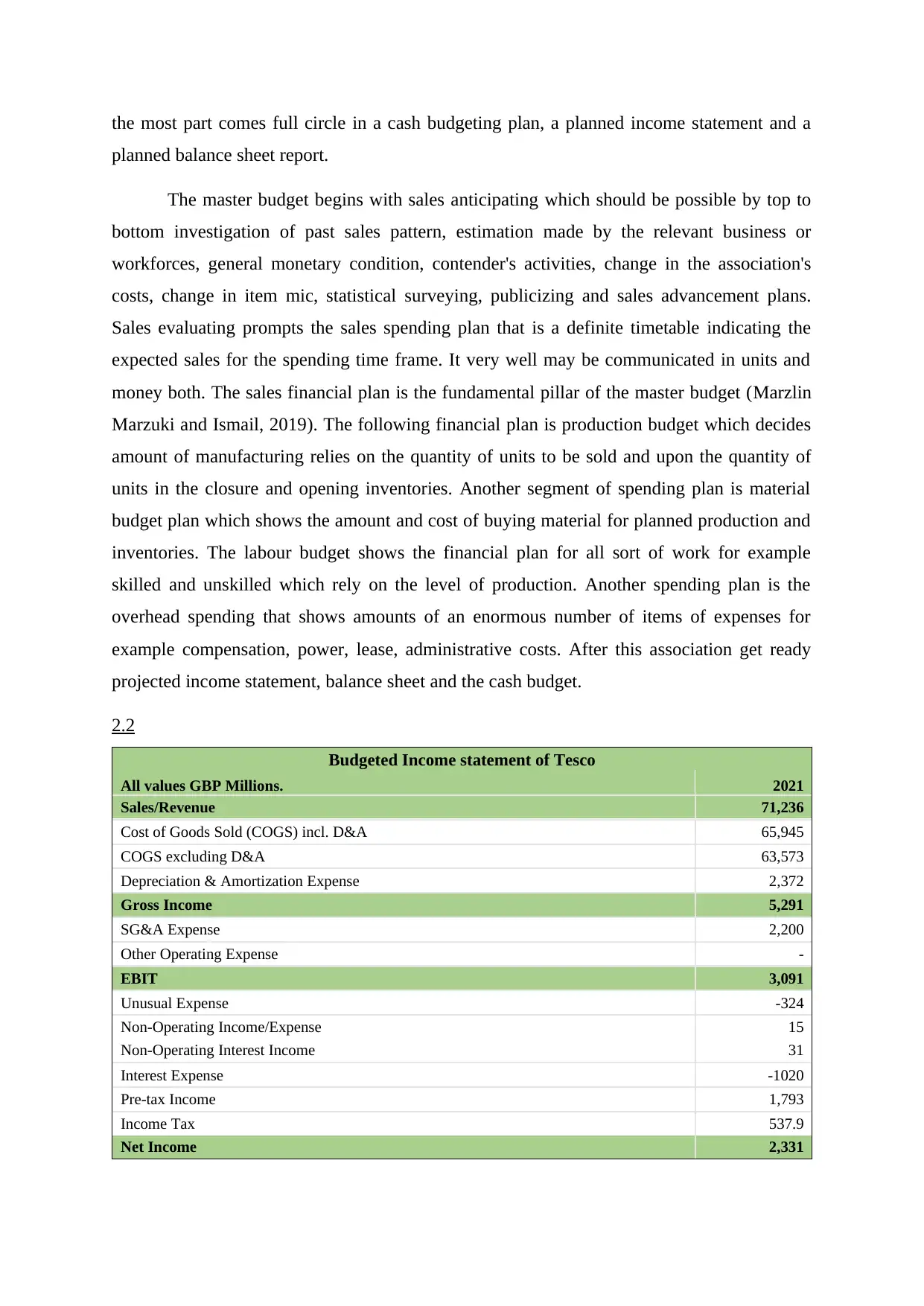

2.2

Budgeted Income statement of Tesco

All values GBP Millions. 2021

Sales/Revenue 71,236

Cost of Goods Sold (COGS) incl. D&A 65,945

COGS excluding D&A 63,573

Depreciation & Amortization Expense 2,372

Gross Income 5,291

SG&A Expense 2,200

Other Operating Expense -

EBIT 3,091

Unusual Expense -324

Non-Operating Income/Expense 15

Non-Operating Interest Income 31

Interest Expense -1020

Pre-tax Income 1,793

Income Tax 537.9

Net Income 2,331

planned balance sheet report.

The master budget begins with sales anticipating which should be possible by top to

bottom investigation of past sales pattern, estimation made by the relevant business or

workforces, general monetary condition, contender's activities, change in the association's

costs, change in item mic, statistical surveying, publicizing and sales advancement plans.

Sales evaluating prompts the sales spending plan that is a definite timetable indicating the

expected sales for the spending time frame. It very well may be communicated in units and

money both. The sales financial plan is the fundamental pillar of the master budget (Marzlin

Marzuki and Ismail, 2019). The following financial plan is production budget which decides

amount of manufacturing relies on the quantity of units to be sold and upon the quantity of

units in the closure and opening inventories. Another segment of spending plan is material

budget plan which shows the amount and cost of buying material for planned production and

inventories. The labour budget shows the financial plan for all sort of work for example

skilled and unskilled which rely on the level of production. Another spending plan is the

overhead spending that shows amounts of an enormous number of items of expenses for

example compensation, power, lease, administrative costs. After this association get ready

projected income statement, balance sheet and the cash budget.

2.2

Budgeted Income statement of Tesco

All values GBP Millions. 2021

Sales/Revenue 71,236

Cost of Goods Sold (COGS) incl. D&A 65,945

COGS excluding D&A 63,573

Depreciation & Amortization Expense 2,372

Gross Income 5,291

SG&A Expense 2,200

Other Operating Expense -

EBIT 3,091

Unusual Expense -324

Non-Operating Income/Expense 15

Non-Operating Interest Income 31

Interest Expense -1020

Pre-tax Income 1,793

Income Tax 537.9

Net Income 2,331

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 18

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.