Financial Analysis Report: Merlin Entertainments and TRG Performance

VerifiedAdded on 2020/01/15

|16

|5303

|158

Report

AI Summary

This report provides a comprehensive financial analysis of Merlin Entertainments Plc and The Restaurant Group (TRG) Plc. It begins with an introduction to the travel and tourism industry's contribution to the global economy and the importance of financial management in determining costs and pricing. The report delves into the significance of costs and volume in financial management, examining different cost types, allocation, and the volume concept, including break-even analysis and economies of scale, using Merlin Entertainments as a case study. It then explores various pricing methods employed in the travel and tourism sector, such as discounted pricing, cost-plus pricing, and return on capital employed, again using Merlin Entertainments. The report also covers different types of management accounting information, its use as a decision-making tool, and factors influencing profit for tourism businesses. Furthermore, it includes a case study of TRG Plc's financial accounts to aid decision-making and concludes with a discussion of funding sources and distribution for tourism development, both public and non-public.

Finance and Funding

1

1

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

TABLE OF CONTENTS

INTRODUCTION...........................................................................................................................3

Task 1...............................................................................................................................................3

1.1 Importance of costs and volume in financial management of travel and tourism businesses

using Merlin Entertainments Plc..................................................................................................3

1.2 Pricing methods used in the travel and tourism sector using Merlin Entertainments............6

1.3 Factors influencing profit for travel and tourism businesses using Merlin Entertainments

Plc................................................................................................................................................9

Task 2.............................................................................................................................................10

2.1 Different types of management accounting information that could be used in travel and

tourism businesses using Merlin Entertainments Plc................................................................10

2.2 Use of management accounting information as a decision-making tool for Merlin

Entertainments Plc.....................................................................................................................11

Task 3.............................................................................................................................................12

3.1 Financial accounts of The Restaurant Group (TRG) Plc for the year ended 28 December

2014 showing at least two years performance...........................................................................12

TASK 4..........................................................................................................................................13

4.1 Sources and distribution of funding.....................................................................................13

CONCLUSION..............................................................................................................................14

REFERENCES..............................................................................................................................15

2

INTRODUCTION...........................................................................................................................3

Task 1...............................................................................................................................................3

1.1 Importance of costs and volume in financial management of travel and tourism businesses

using Merlin Entertainments Plc..................................................................................................3

1.2 Pricing methods used in the travel and tourism sector using Merlin Entertainments............6

1.3 Factors influencing profit for travel and tourism businesses using Merlin Entertainments

Plc................................................................................................................................................9

Task 2.............................................................................................................................................10

2.1 Different types of management accounting information that could be used in travel and

tourism businesses using Merlin Entertainments Plc................................................................10

2.2 Use of management accounting information as a decision-making tool for Merlin

Entertainments Plc.....................................................................................................................11

Task 3.............................................................................................................................................12

3.1 Financial accounts of The Restaurant Group (TRG) Plc for the year ended 28 December

2014 showing at least two years performance...........................................................................12

TASK 4..........................................................................................................................................13

4.1 Sources and distribution of funding.....................................................................................13

CONCLUSION..............................................................................................................................14

REFERENCES..............................................................................................................................15

2

INTRODUCTION

Travel and tourism industry has contributed a lot to the world's economy in terms of high

contribution in GDP. The application of financial management is seen to be crucial within the

business environment in determining cost and taking pricing decisions. This unit is focused

towards the case of Merlin Entertainments, a leading entertainment company of United

Kingdom. As per the given information, company operates around 110 attractions in 23 countries

across four continents (Merlin Entertainments, 2016). The present report explains about the

importance of costs and volume in financial management of travel and tourism businesses as

well as the pricing methods that are used in this sector. However, the next section of study

represents the different types of management accounting and the use of management accounting

information as a decision making tool in travel and tourism businesses. Factors that are

influencing the profit of tourism entrepreneurs specially to Merlin Entertainments Plc are also

explained. In addition, case study of The Restaurant Group plc, a leading restaurant company is

taken into consideration for interpreting financial accounts to assist decision making in travel and

tourism businesses. At last, final section represents the sources and distribution of funding for

public and non-public tourism development.

TASK 1

1.1 Importance of costs and volume in financial management of travel and tourism businesses

using Merlin Entertainments Plc

In respect with the given case scenario, Merlin Entertainments Plc is a leading

entertainment company which aims at becoming a worldwide leader in branded, location-based,

family entertainment from which it creates a strategy to attain high growth, high return and a

family entertainment company (Bhowmik and Saha, 2013).

Cost concept

Before explaining the concept of cost and volume, this is important to identify various

kinds of costs as it is helpful in financial management of the report. Various types of costs are

explained in below:

Direct cost: Cost that is significantly associated with the production is called as direct

cost. Direct cost of production process include material, labor as well as many other direct

3

Travel and tourism industry has contributed a lot to the world's economy in terms of high

contribution in GDP. The application of financial management is seen to be crucial within the

business environment in determining cost and taking pricing decisions. This unit is focused

towards the case of Merlin Entertainments, a leading entertainment company of United

Kingdom. As per the given information, company operates around 110 attractions in 23 countries

across four continents (Merlin Entertainments, 2016). The present report explains about the

importance of costs and volume in financial management of travel and tourism businesses as

well as the pricing methods that are used in this sector. However, the next section of study

represents the different types of management accounting and the use of management accounting

information as a decision making tool in travel and tourism businesses. Factors that are

influencing the profit of tourism entrepreneurs specially to Merlin Entertainments Plc are also

explained. In addition, case study of The Restaurant Group plc, a leading restaurant company is

taken into consideration for interpreting financial accounts to assist decision making in travel and

tourism businesses. At last, final section represents the sources and distribution of funding for

public and non-public tourism development.

TASK 1

1.1 Importance of costs and volume in financial management of travel and tourism businesses

using Merlin Entertainments Plc

In respect with the given case scenario, Merlin Entertainments Plc is a leading

entertainment company which aims at becoming a worldwide leader in branded, location-based,

family entertainment from which it creates a strategy to attain high growth, high return and a

family entertainment company (Bhowmik and Saha, 2013).

Cost concept

Before explaining the concept of cost and volume, this is important to identify various

kinds of costs as it is helpful in financial management of the report. Various types of costs are

explained in below:

Direct cost: Cost that is significantly associated with the production is called as direct

cost. Direct cost of production process include material, labor as well as many other direct

3

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

expenditures. Direct cost can be in the form of human resources and materials. These costs are

mandatory to be bear at the time of manufacturing process (Adams, 2006).

Indirect cost: The cost which is not directly linked to the production process but it

indirectly links with the manufacturing unit is significantly known as indirect costs. Several

range of indirect cost are administration, personnel as well as security costs. In other words,

factory cost bear by business is known as indirect cost.

Fixed cost: In respect with the manufacturing unit, fixed cost is one which remains same

at any level of production. In other words, cost which does not change with the production level

is called as fixed cost. The fixed cost is going to be incurred at the production of single unit.

Variable cost: Another form of cost is variable which changes as per the level of

production. This cost has a changing nature as per the production volume (Halabi and Carroll,

2015). Dependent cost is said to be the variable cost. For an example: organization produces 100

units so it bears less cost, on the other hand, at the production of 1000 unit it bears increased

cost . Such kind of cost is said to be variable cost and has a relevant aspect in manufacturing

industry. Examples of variable cost are advertising, insurance and office supplies.

Allocation and appropriation of costs:

Main aim behind the allocation of cost is to identify, aggregate and access cost incurred

during manufacturing as per the objectives of costs. However, to calculate actual cost per unit,

this is too important to divide the cost within all the departments. In order to allocate cost, it is

the foremost important to take pricing decisions. In respect with the mentioned company, major

task is of dividing cost into various activities as per the requirements so that process of pricing

decision can become easier. For a service industry like as Tourism, It becomes difficult to set

price as per the cost occurred from different activities. The mentioned company is facing lot of

issues including more competition at the time of offering services to the customers of UK in

which prices of offering has become a foremost issue for the company. Allocation of cost is the

major concept so as to decide the actual pricing of products by assessing cost per unit (Hu, Tian

and Zhu, 2016). Within service industry, appropriation of cost is the actual allocation of cost and

assessment of cost per unit. However, it is easier to understand costing concept so that decision

over reducing expenses can be taken. However, this is all the round, mandatory to use different

costing methods including absorption costing, marginal costing, activity based costing and so on.

4

mandatory to be bear at the time of manufacturing process (Adams, 2006).

Indirect cost: The cost which is not directly linked to the production process but it

indirectly links with the manufacturing unit is significantly known as indirect costs. Several

range of indirect cost are administration, personnel as well as security costs. In other words,

factory cost bear by business is known as indirect cost.

Fixed cost: In respect with the manufacturing unit, fixed cost is one which remains same

at any level of production. In other words, cost which does not change with the production level

is called as fixed cost. The fixed cost is going to be incurred at the production of single unit.

Variable cost: Another form of cost is variable which changes as per the level of

production. This cost has a changing nature as per the production volume (Halabi and Carroll,

2015). Dependent cost is said to be the variable cost. For an example: organization produces 100

units so it bears less cost, on the other hand, at the production of 1000 unit it bears increased

cost . Such kind of cost is said to be variable cost and has a relevant aspect in manufacturing

industry. Examples of variable cost are advertising, insurance and office supplies.

Allocation and appropriation of costs:

Main aim behind the allocation of cost is to identify, aggregate and access cost incurred

during manufacturing as per the objectives of costs. However, to calculate actual cost per unit,

this is too important to divide the cost within all the departments. In order to allocate cost, it is

the foremost important to take pricing decisions. In respect with the mentioned company, major

task is of dividing cost into various activities as per the requirements so that process of pricing

decision can become easier. For a service industry like as Tourism, It becomes difficult to set

price as per the cost occurred from different activities. The mentioned company is facing lot of

issues including more competition at the time of offering services to the customers of UK in

which prices of offering has become a foremost issue for the company. Allocation of cost is the

major concept so as to decide the actual pricing of products by assessing cost per unit (Hu, Tian

and Zhu, 2016). Within service industry, appropriation of cost is the actual allocation of cost and

assessment of cost per unit. However, it is easier to understand costing concept so that decision

over reducing expenses can be taken. However, this is all the round, mandatory to use different

costing methods including absorption costing, marginal costing, activity based costing and so on.

4

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

With the help of such methods, organization can allocate cost to each activity in the most

appropriate manner and these arealso helpful in accessing cost per unit as well as making

appropriate pricing decision.

Volume concept

Volume, in terms of manufacturing unit is refereed as the level and units of production

that are produced in a specific time period. There are various concepts that are associated with

the volume of production such as break even analysis, economies of scale and dis economies of

scale. These all the concepts are discussed here under:

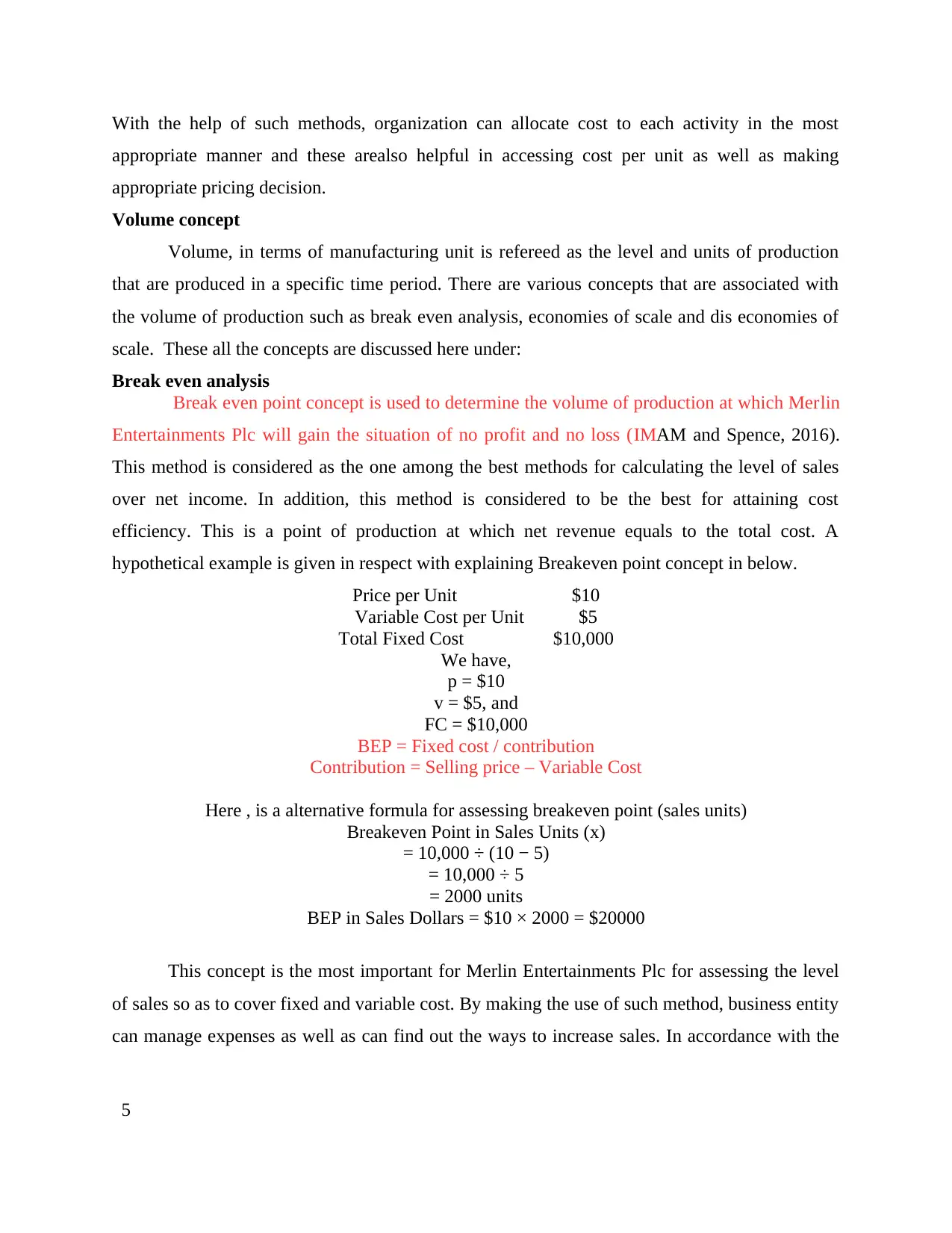

Break even analysis

Break even point concept is used to determine the volume of production at which Merlin

Entertainments Plc will gain the situation of no profit and no loss (IMAM and Spence, 2016).

This method is considered as the one among the best methods for calculating the level of sales

over net income. In addition, this method is considered to be the best for attaining cost

efficiency. This is a point of production at which net revenue equals to the total cost. A

hypothetical example is given in respect with explaining Breakeven point concept in below.

Price per Unit $10

Variable Cost per Unit $5

Total Fixed Cost $10,000

We have,

p = $10

v = $5, and

FC = $10,000

BEP = Fixed cost / contribution

Contribution = Selling price – Variable Cost

Here , is a alternative formula for assessing breakeven point (sales units)

Breakeven Point in Sales Units (x)

= 10,000 ÷ (10 − 5)

= 10,000 ÷ 5

= 2000 units

BEP in Sales Dollars = $10 × 2000 = $20000

This concept is the most important for Merlin Entertainments Plc for assessing the level

of sales so as to cover fixed and variable cost. By making the use of such method, business entity

can manage expenses as well as can find out the ways to increase sales. In accordance with the

5

appropriate manner and these arealso helpful in accessing cost per unit as well as making

appropriate pricing decision.

Volume concept

Volume, in terms of manufacturing unit is refereed as the level and units of production

that are produced in a specific time period. There are various concepts that are associated with

the volume of production such as break even analysis, economies of scale and dis economies of

scale. These all the concepts are discussed here under:

Break even analysis

Break even point concept is used to determine the volume of production at which Merlin

Entertainments Plc will gain the situation of no profit and no loss (IMAM and Spence, 2016).

This method is considered as the one among the best methods for calculating the level of sales

over net income. In addition, this method is considered to be the best for attaining cost

efficiency. This is a point of production at which net revenue equals to the total cost. A

hypothetical example is given in respect with explaining Breakeven point concept in below.

Price per Unit $10

Variable Cost per Unit $5

Total Fixed Cost $10,000

We have,

p = $10

v = $5, and

FC = $10,000

BEP = Fixed cost / contribution

Contribution = Selling price – Variable Cost

Here , is a alternative formula for assessing breakeven point (sales units)

Breakeven Point in Sales Units (x)

= 10,000 ÷ (10 − 5)

= 10,000 ÷ 5

= 2000 units

BEP in Sales Dollars = $10 × 2000 = $20000

This concept is the most important for Merlin Entertainments Plc for assessing the level

of sales so as to cover fixed and variable cost. By making the use of such method, business entity

can manage expenses as well as can find out the ways to increase sales. In accordance with the

5

results of Breakeven point method, decision of production level can be changed which will be

fruitful in generating higher sales as well as profit while making effective pricing decision.

Economies of scale

The cost advantage of manufacturing units are known as economics of scale which can be

attained by reducing the cost of production and increasing profits. Within the tourism industry,

the economies of scale can be achieved by increasing level of service hence, reducing cost. In

other words the economies of scale represents the relationship between quality production and

cost of production (Shim and et.al., 2008). In respect with the mentioned company, economies of

scale is all about increasing production volume and providing benefits through reduction in cost.

This is to bring into notice, when company achieves economies to scale, it become important to

separate the cost among the large number of units. At the same time, over a larger number of

goods it reduced the burden from the organization. Economies of scales help in decreasing the

variable cost per unit and increasing operational efficiency and synergies. While increasing the

production level company can attain economies of scale level and can attract more profits for the

organization.

Dis-economies of scale

From a in-depth indication, it has been noticed that in a long run economics of scale can

not be achieved however, while taking a huge initiatives the company has to make various

initiatives (Dlabay and Burrow, 2007). The marginal cost can be attained art the time increasing

the cost of production. There can be some reasons for achieving dis economies of scale that are

explained in the following points :

In case a company is focusing on same level of production then it cannot focus on same

level of production. However, the company cannot achieve economies of scale and it can

not always manufacture the same unit for every time.

This is all time negated that with an increase in production volume, the transportation and

warehousing cost also increases. This is a indication for organization to have dis

economies of scale.

1.2 Pricing methods used in the travel and tourism sector using Merlin Entertainments

Pricing decisions are the most crucial part for any industry as it determines the profit

level. However, to make a pricing decision is the most crucial aspect of an organization for

6

fruitful in generating higher sales as well as profit while making effective pricing decision.

Economies of scale

The cost advantage of manufacturing units are known as economics of scale which can be

attained by reducing the cost of production and increasing profits. Within the tourism industry,

the economies of scale can be achieved by increasing level of service hence, reducing cost. In

other words the economies of scale represents the relationship between quality production and

cost of production (Shim and et.al., 2008). In respect with the mentioned company, economies of

scale is all about increasing production volume and providing benefits through reduction in cost.

This is to bring into notice, when company achieves economies to scale, it become important to

separate the cost among the large number of units. At the same time, over a larger number of

goods it reduced the burden from the organization. Economies of scales help in decreasing the

variable cost per unit and increasing operational efficiency and synergies. While increasing the

production level company can attain economies of scale level and can attract more profits for the

organization.

Dis-economies of scale

From a in-depth indication, it has been noticed that in a long run economics of scale can

not be achieved however, while taking a huge initiatives the company has to make various

initiatives (Dlabay and Burrow, 2007). The marginal cost can be attained art the time increasing

the cost of production. There can be some reasons for achieving dis economies of scale that are

explained in the following points :

In case a company is focusing on same level of production then it cannot focus on same

level of production. However, the company cannot achieve economies of scale and it can

not always manufacture the same unit for every time.

This is all time negated that with an increase in production volume, the transportation and

warehousing cost also increases. This is a indication for organization to have dis

economies of scale.

1.2 Pricing methods used in the travel and tourism sector using Merlin Entertainments

Pricing decisions are the most crucial part for any industry as it determines the profit

level. However, to make a pricing decision is the most crucial aspect of an organization for

6

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

which it uses various pricing methods. The explanation of such pricing methods are explained

below along with practical examples:

Discounted pricing

Discounted pricing is an important pricing method that can be used by the mentioned

company so as to increase the number of customers (McLaney, 2009). The company provides

discounts on the actual market prices so as to attract the customers and creating awareness

among large number of visitors. Merlin Entertainments can offer services at lower prices in off

seasons so that minimum level of profits can be attained. He use of such pricing method allows

management to create a distinct image in marketplace.

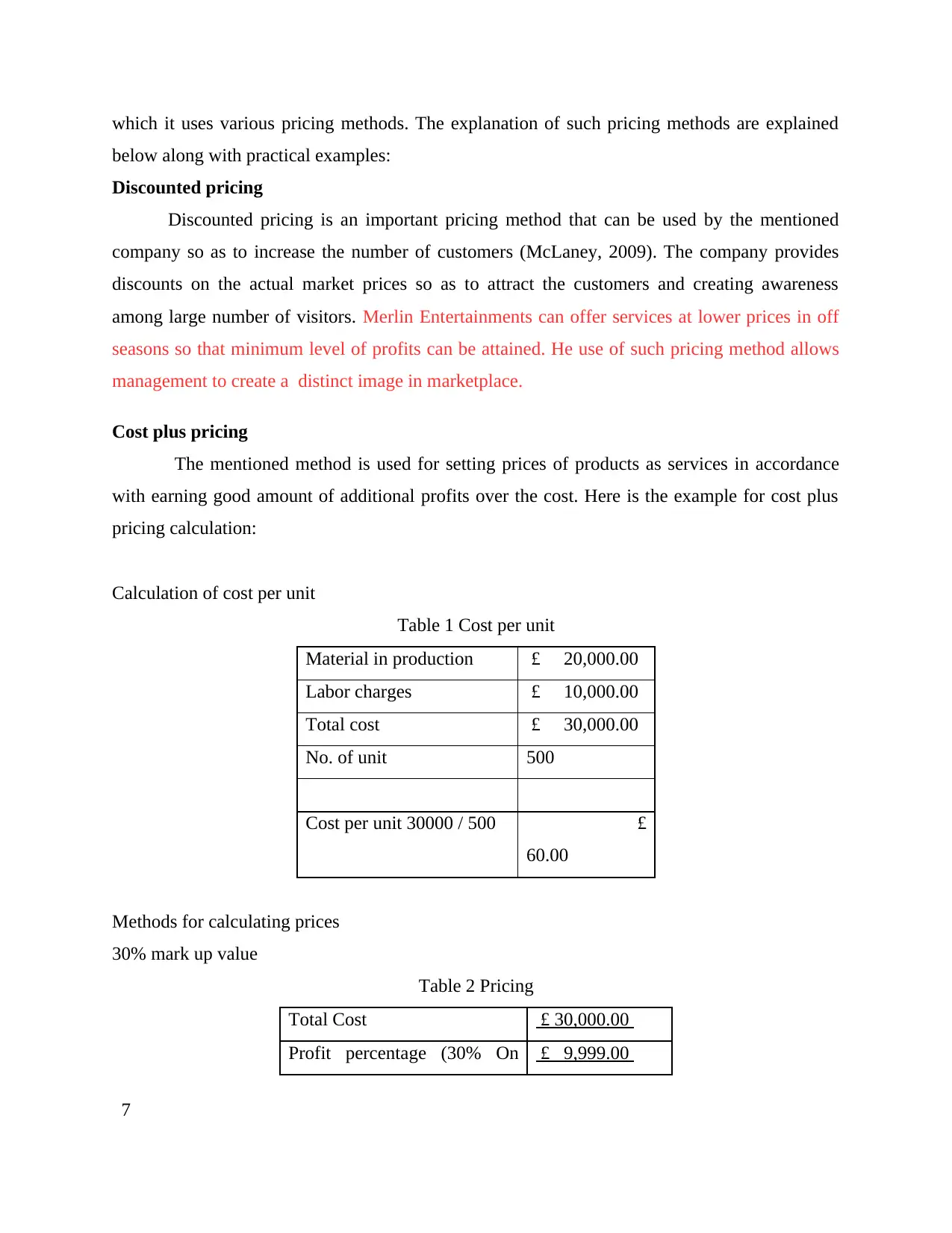

Cost plus pricing

The mentioned method is used for setting prices of products as services in accordance

with earning good amount of additional profits over the cost. Here is the example for cost plus

pricing calculation:

Calculation of cost per unit

Table 1 Cost per unit

Material in production £ 20,000.00

Labor charges £ 10,000.00

Total cost £ 30,000.00

No. of unit 500

Cost per unit 30000 / 500 £

60.00

Methods for calculating prices

30% mark up value

Table 2 Pricing

Total Cost £ 30,000.00

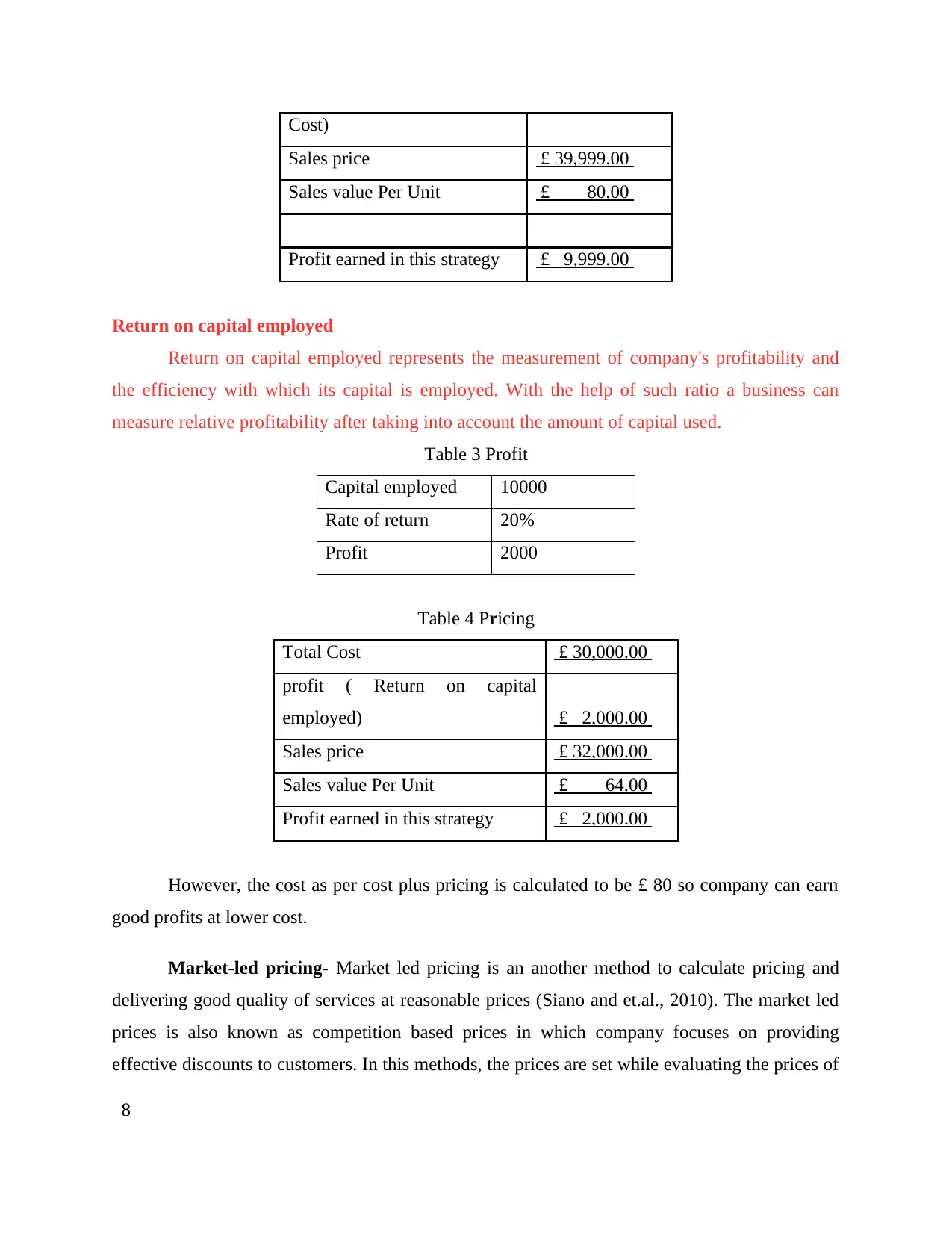

Profit percentage (30% On £ 9,999.00

7

below along with practical examples:

Discounted pricing

Discounted pricing is an important pricing method that can be used by the mentioned

company so as to increase the number of customers (McLaney, 2009). The company provides

discounts on the actual market prices so as to attract the customers and creating awareness

among large number of visitors. Merlin Entertainments can offer services at lower prices in off

seasons so that minimum level of profits can be attained. He use of such pricing method allows

management to create a distinct image in marketplace.

Cost plus pricing

The mentioned method is used for setting prices of products as services in accordance

with earning good amount of additional profits over the cost. Here is the example for cost plus

pricing calculation:

Calculation of cost per unit

Table 1 Cost per unit

Material in production £ 20,000.00

Labor charges £ 10,000.00

Total cost £ 30,000.00

No. of unit 500

Cost per unit 30000 / 500 £

60.00

Methods for calculating prices

30% mark up value

Table 2 Pricing

Total Cost £ 30,000.00

Profit percentage (30% On £ 9,999.00

7

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Cost)

Sales price £ 39,999.00

Sales value Per Unit £ 80.00

Profit earned in this strategy £ 9,999.00

Return on capital employed

Return on capital employed represents the measurement of company's profitability and

the efficiency with which its capital is employed. With the help of such ratio a business can

measure relative profitability after taking into account the amount of capital used.

Table 3 Profit

Capital employed 10000

Rate of return 20%

Profit 2000

Table 4 Pricing

Total Cost £ 30,000.00

profit ( Return on capital

employed) £ 2,000.00

Sales price £ 32,000.00

Sales value Per Unit £ 64.00

Profit earned in this strategy £ 2,000.00

However, the cost as per cost plus pricing is calculated to be £ 80 so company can earn

good profits at lower cost.

Market-led pricing- Market led pricing is an another method to calculate pricing and

delivering good quality of services at reasonable prices (Siano and et.al., 2010). The market led

prices is also known as competition based prices in which company focuses on providing

effective discounts to customers. In this methods, the prices are set while evaluating the prices of

8

Sales price £ 39,999.00

Sales value Per Unit £ 80.00

Profit earned in this strategy £ 9,999.00

Return on capital employed

Return on capital employed represents the measurement of company's profitability and

the efficiency with which its capital is employed. With the help of such ratio a business can

measure relative profitability after taking into account the amount of capital used.

Table 3 Profit

Capital employed 10000

Rate of return 20%

Profit 2000

Table 4 Pricing

Total Cost £ 30,000.00

profit ( Return on capital

employed) £ 2,000.00

Sales price £ 32,000.00

Sales value Per Unit £ 64.00

Profit earned in this strategy £ 2,000.00

However, the cost as per cost plus pricing is calculated to be £ 80 so company can earn

good profits at lower cost.

Market-led pricing- Market led pricing is an another method to calculate pricing and

delivering good quality of services at reasonable prices (Siano and et.al., 2010). The market led

prices is also known as competition based prices in which company focuses on providing

effective discounts to customers. In this methods, the prices are set while evaluating the prices of

8

similar products available in the market. However, on the basis of product status in terms of

features in competitive scenario, the company may set prices higher or lower than the competitor

pricing. For example : in case Merlin Entertainments Plc adopts Market-led pricing then the

company will only focus on pricing and delivering good quality of services at reasonable prices.

Value adding pricing method

Value adding prices methods is a major concept of pricing that is considered as important

so the company can deliver good quality of services to large number of visitors. The prices of

products and services are to be included in respect with the value added features of a product and

services (Jonsson, 2008). However, Merlin Entertainments Plc is always seen focusing towards

towards maximising the cost of production while adding addition features which are further

covered through increasing final prices. Hence, with the help of such pricing methods the

company increases the value of products.

1.3 Factors influencing profit for travel and tourism businesses using Merlin Entertainments Plc

Large numbers of factors are present which influences profit of travel and tourism firm

like Merlin Entertainment Plc. Such factors are as follows which business must consider with the

motive to enhance its profitability level: Social environment: Environment in which Merlin entertainment carries out its

operations is quite complex and large number of challenges have to be faced by business.

Further, taste and overall preference of target market changes rapidly due to which it is

required for business to modify its services accordingly (James and Mainam, 2012).

Sometime, it may be possible that company does not alter its services due to which

overall profitability level is affected. By offering services as per culture and religion of

target market business can easily deal with the issue of change in social environment. Economic environment: Economic condition of the country also affects profitability

level of Merlin Entertainment. Further, current state of economy is not in favourable

condition where inflation and recession are adversely affecting business operations.

Further, due to inflation purchasing power of customers is directly affected and due to

this reason company has to decrease price of its services and this has direct impact on

9

features in competitive scenario, the company may set prices higher or lower than the competitor

pricing. For example : in case Merlin Entertainments Plc adopts Market-led pricing then the

company will only focus on pricing and delivering good quality of services at reasonable prices.

Value adding pricing method

Value adding prices methods is a major concept of pricing that is considered as important

so the company can deliver good quality of services to large number of visitors. The prices of

products and services are to be included in respect with the value added features of a product and

services (Jonsson, 2008). However, Merlin Entertainments Plc is always seen focusing towards

towards maximising the cost of production while adding addition features which are further

covered through increasing final prices. Hence, with the help of such pricing methods the

company increases the value of products.

1.3 Factors influencing profit for travel and tourism businesses using Merlin Entertainments Plc

Large numbers of factors are present which influences profit of travel and tourism firm

like Merlin Entertainment Plc. Such factors are as follows which business must consider with the

motive to enhance its profitability level: Social environment: Environment in which Merlin entertainment carries out its

operations is quite complex and large number of challenges have to be faced by business.

Further, taste and overall preference of target market changes rapidly due to which it is

required for business to modify its services accordingly (James and Mainam, 2012).

Sometime, it may be possible that company does not alter its services due to which

overall profitability level is affected. By offering services as per culture and religion of

target market business can easily deal with the issue of change in social environment. Economic environment: Economic condition of the country also affects profitability

level of Merlin Entertainment. Further, current state of economy is not in favourable

condition where inflation and recession are adversely affecting business operations.

Further, due to inflation purchasing power of customers is directly affected and due to

this reason company has to decrease price of its services and this has direct impact on

9

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

profits earned by business. Therefore, it can be said that economic environment has also

direct impact on profits earned by business (Clark and Hallerberg, 2012). Current trends: In travel and tourism sector it is necessary for every business to offer

services to target market as per current trends in the market. Further, Merlin

Entertainment Plc has to consider current trends where services must be modified

accordingly (Hansen and Guan, 200). By offering services as per need of target market it

is possible for company to earn higher profits. On the other hand, in case if business is

not able to offer services as per current trends then it becomes difficult for firm to survive

in the market.

Poor planning: It is also regarded as one of the crucial factor which influences

profitability level of the business. Sometime, it may be possible that management of

Merlin entertainment is not able to prepare appropriate plans through which operations

can be carried out (Drake and Fabozzi, 2012). Further, practice of poor planning can lead

to decline in profitability level and staff members will not be able to carry out overall

operations which are also unfavourable for business.

Therefore, in this way these are some of the key factors which may influence profitability

level of the business and by considering them it is possible for company to deal with adverse

situation such as lower profits etc.

TASK 2

2.1 Different types of management accounting information that could be used in travel and

tourism businesses using Merlin Entertainments Plc.

Management accounting has significant presence in today's corporate scenario. The

management accounting includes various concepts such as budgets, variances as well as

allocating cost. The adoption of appropriate accounting method is important so as to attain the

business objectives (Cohen and Kaimenaki, 2011). The mentioned entertainment company is

going to take help of management accounting for satisfying the needs and wants of stakeholder

of business. This unit of accounting methods also helps in planning, formulating strategies and

adopting strict control of the company's operations. There can be various sources of information

10

direct impact on profits earned by business (Clark and Hallerberg, 2012). Current trends: In travel and tourism sector it is necessary for every business to offer

services to target market as per current trends in the market. Further, Merlin

Entertainment Plc has to consider current trends where services must be modified

accordingly (Hansen and Guan, 200). By offering services as per need of target market it

is possible for company to earn higher profits. On the other hand, in case if business is

not able to offer services as per current trends then it becomes difficult for firm to survive

in the market.

Poor planning: It is also regarded as one of the crucial factor which influences

profitability level of the business. Sometime, it may be possible that management of

Merlin entertainment is not able to prepare appropriate plans through which operations

can be carried out (Drake and Fabozzi, 2012). Further, practice of poor planning can lead

to decline in profitability level and staff members will not be able to carry out overall

operations which are also unfavourable for business.

Therefore, in this way these are some of the key factors which may influence profitability

level of the business and by considering them it is possible for company to deal with adverse

situation such as lower profits etc.

TASK 2

2.1 Different types of management accounting information that could be used in travel and

tourism businesses using Merlin Entertainments Plc.

Management accounting has significant presence in today's corporate scenario. The

management accounting includes various concepts such as budgets, variances as well as

allocating cost. The adoption of appropriate accounting method is important so as to attain the

business objectives (Cohen and Kaimenaki, 2011). The mentioned entertainment company is

going to take help of management accounting for satisfying the needs and wants of stakeholder

of business. This unit of accounting methods also helps in planning, formulating strategies and

adopting strict control of the company's operations. There can be various sources of information

10

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

that assist company in explaining the implications of management accounting. The information

sources are presented hereunder :

Financial statements: Financial statements are also known as financial reports that

pertains the financial performance of a company for a specified pried of time (Bhowmik and

Saha, 2013). However, it also include the information of profitability, stability and liquidity

position. With the help of various financial statements including balance sheets, income

statement and cash flow statement. The companies are able to judge efficiency of business

operations with the help of such reports. In addition the position of company can be ascertained

with the help of such statements and these statements are important for satisfying information

needs of stakeholders.

Cost allocation reports: The cost allocation report is important to identify the various

cost during the business affairs and the a,location of such cost. This helps in identifying the

utilization of resources as well as proper allocation of funds to each activity. In addition to that

the organization has to focus on cost allocation of reports so that effective utilization of resources

can be made (Pike & Neale, 2003). With the help of cost allocation report that company can find

the information which is in relation to various costs that are involved in operations. Hence, the

reports are highly valuable in satisfying the needs of stakeholders.

Budgets: For the purpose of setting benchmarks and targets as well as to identify the

feasibility of set targets, the tourism entrepreneurs use various tools of management accounting.

Budget are the financial plans that are prepared by the company in order to attain desired

financial goals of company (Adams, 2006). The budgeted figures are helpful in creating targets

and adopting strict control for attaining the budgeted figures of company. In addition to that

budget is a tool of munitioning the financial performance as compared to previous decided plans

as variance analysis. Hence, It could be said that with the help of budget the mentioned company

can design future plans or managing financial resources.

2.2 Use of management accounting information as a decision-making tool for Merlin

Entertainments Plc

The use of management accounting information helps the business entities in taking

decisions pertaining to business. The major aim of Merlin Entertainments to decide provide the

11

sources are presented hereunder :

Financial statements: Financial statements are also known as financial reports that

pertains the financial performance of a company for a specified pried of time (Bhowmik and

Saha, 2013). However, it also include the information of profitability, stability and liquidity

position. With the help of various financial statements including balance sheets, income

statement and cash flow statement. The companies are able to judge efficiency of business

operations with the help of such reports. In addition the position of company can be ascertained

with the help of such statements and these statements are important for satisfying information

needs of stakeholders.

Cost allocation reports: The cost allocation report is important to identify the various

cost during the business affairs and the a,location of such cost. This helps in identifying the

utilization of resources as well as proper allocation of funds to each activity. In addition to that

the organization has to focus on cost allocation of reports so that effective utilization of resources

can be made (Pike & Neale, 2003). With the help of cost allocation report that company can find

the information which is in relation to various costs that are involved in operations. Hence, the

reports are highly valuable in satisfying the needs of stakeholders.

Budgets: For the purpose of setting benchmarks and targets as well as to identify the

feasibility of set targets, the tourism entrepreneurs use various tools of management accounting.

Budget are the financial plans that are prepared by the company in order to attain desired

financial goals of company (Adams, 2006). The budgeted figures are helpful in creating targets

and adopting strict control for attaining the budgeted figures of company. In addition to that

budget is a tool of munitioning the financial performance as compared to previous decided plans

as variance analysis. Hence, It could be said that with the help of budget the mentioned company

can design future plans or managing financial resources.

2.2 Use of management accounting information as a decision-making tool for Merlin

Entertainments Plc

The use of management accounting information helps the business entities in taking

decisions pertaining to business. The major aim of Merlin Entertainments to decide provide the

11

quality services to the customers as well as to attain good profits. The management accounting

information is helpful for making decision in regard to the development of new products as well

as expansion of business (Mistry, Sharma and Low, 2014). The company can also take the

decisions for reducing cost of production while making use of such information contains in

management accounting tools. The information included in budgets is helpful in making

decisions over the future courses of actions and ways to cut down the variance in actual and

budgeted figures. The assessment of future income and expenses can be identified with the help

of budget. The negative variance can be worked upon as well as the future courses of actions can

be designed. The budget are also helpful in assessment of Further, the company can allocate

financial resources that surely facilitates a effective control on expenses. Furthermore ,financial

and accounting information is helpful in making effective investment decisions. On the basis of

management accounting information and availability of funds the company can decide over

investing funds in new project as well as making investment for growth and expansion decision.

The cost analysis of business can be done on the basis of such information and the company can

take decisions for selling and purchasing. The major decision in respect with prices of services

are taken (Halabi and Carroll, 2015). The preparation of budgets can be made on the basis of

financial information so as to make future plans and strategies. In respect with the Merlin

Entertainments Plc, this could be said that Budget will be helpful in assessing the availability of

finance as well as deficit or surplus.

TASK 3

3.1 Financial accounts of The Restaurant Group (TRG) Plc for the year ended 28 December 2014

showing at least two years performance

Ratios Formula 2013 2012

Profitability ratios

Gross profit 106 95

Operating profit 31 29

Net profit 108 96

Net Sales 580 533

Gross Profit Ratio (Gross Profit/ Net Sales) *100 18.28% 17.82%

Operating Profit Ratio (Operating Profit/ Net Sales) *100 5.34% 5.44%

12

information is helpful for making decision in regard to the development of new products as well

as expansion of business (Mistry, Sharma and Low, 2014). The company can also take the

decisions for reducing cost of production while making use of such information contains in

management accounting tools. The information included in budgets is helpful in making

decisions over the future courses of actions and ways to cut down the variance in actual and

budgeted figures. The assessment of future income and expenses can be identified with the help

of budget. The negative variance can be worked upon as well as the future courses of actions can

be designed. The budget are also helpful in assessment of Further, the company can allocate

financial resources that surely facilitates a effective control on expenses. Furthermore ,financial

and accounting information is helpful in making effective investment decisions. On the basis of

management accounting information and availability of funds the company can decide over

investing funds in new project as well as making investment for growth and expansion decision.

The cost analysis of business can be done on the basis of such information and the company can

take decisions for selling and purchasing. The major decision in respect with prices of services

are taken (Halabi and Carroll, 2015). The preparation of budgets can be made on the basis of

financial information so as to make future plans and strategies. In respect with the Merlin

Entertainments Plc, this could be said that Budget will be helpful in assessing the availability of

finance as well as deficit or surplus.

TASK 3

3.1 Financial accounts of The Restaurant Group (TRG) Plc for the year ended 28 December 2014

showing at least two years performance

Ratios Formula 2013 2012

Profitability ratios

Gross profit 106 95

Operating profit 31 29

Net profit 108 96

Net Sales 580 533

Gross Profit Ratio (Gross Profit/ Net Sales) *100 18.28% 17.82%

Operating Profit Ratio (Operating Profit/ Net Sales) *100 5.34% 5.44%

12

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 16

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.