Applying Finance Models: A Market Valuation Analysis of TUI Group

VerifiedAdded on 2023/04/11

|22

|1854

|56

Report

AI Summary

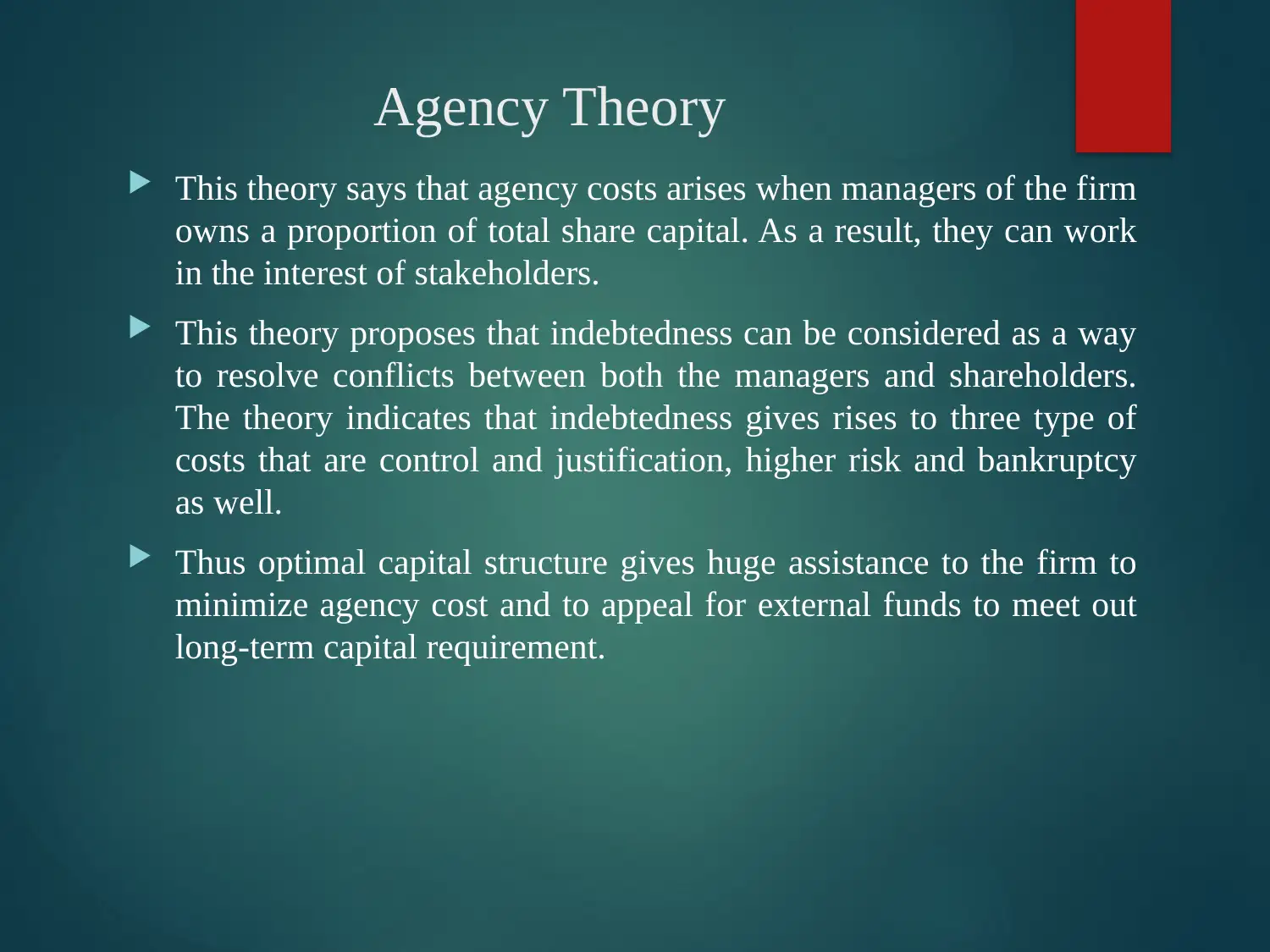

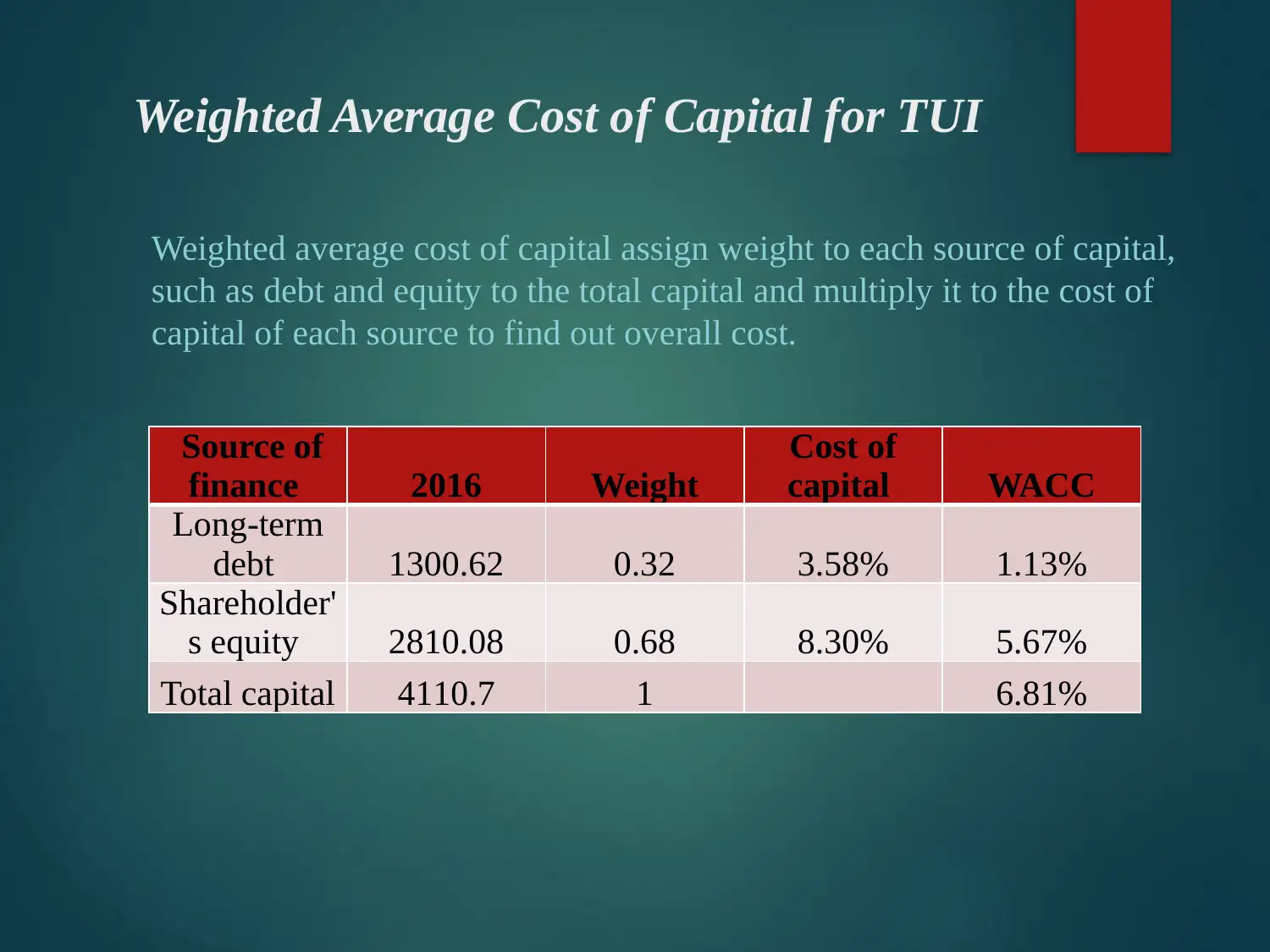

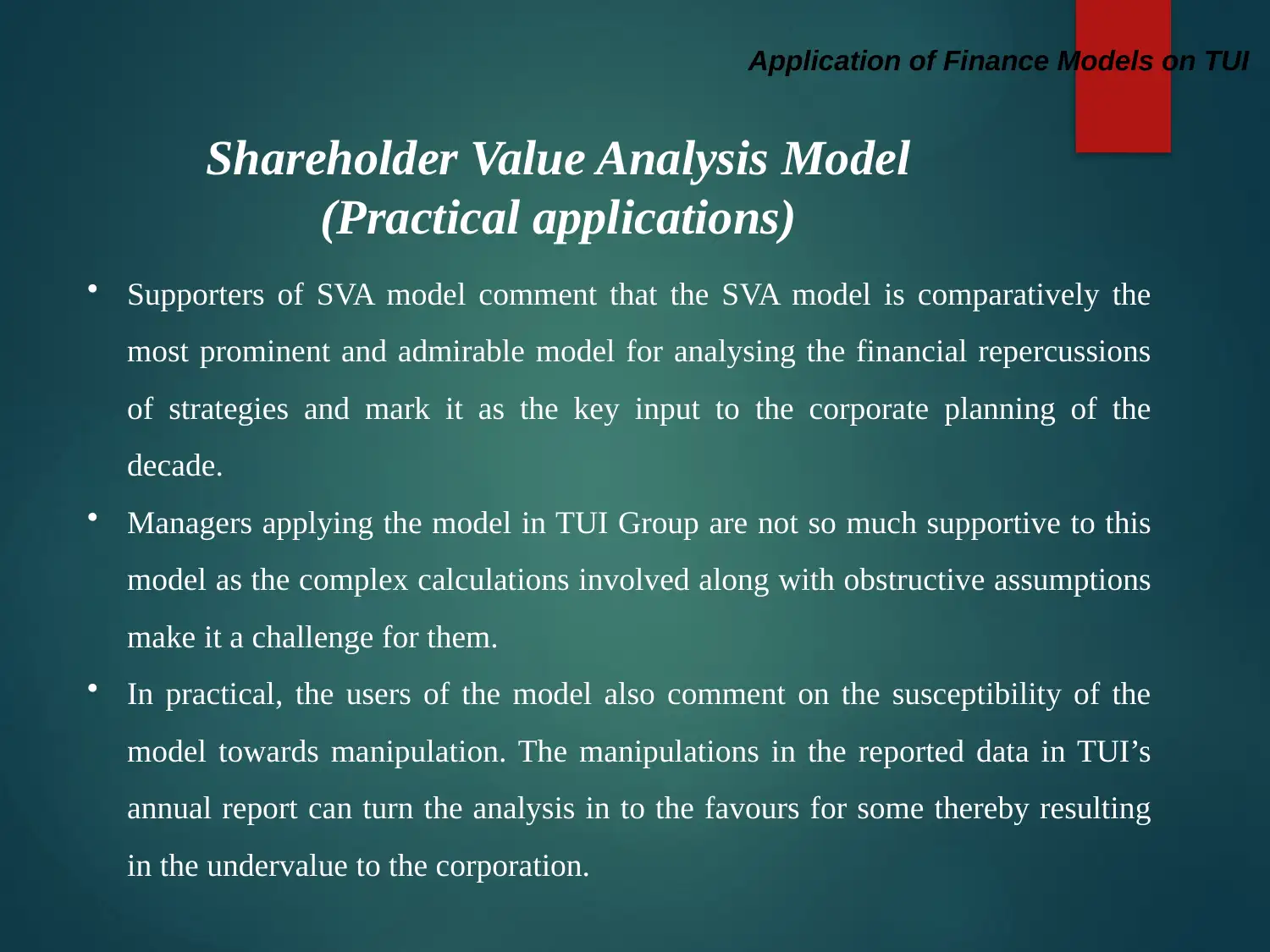

This report provides a comprehensive analysis of TUI Group's market valuation through the application of various financial models, including the Miller and Modigliani capital structure theorem, Pecking Order Theory, Agency Theory, Shareholder Value Analysis (SVA), and Discounted Cash Flow (DCF) model. It examines TUI's capital structure, market valuation, and shareholder value, considering factors such as debt, equity, weighted average cost of capital (WACC), sales growth, and operating profit margin. The report also includes a sensitivity analysis to assess the impact of changes in sales growth on shareholder value, ultimately concluding with a recommendation for institutional investors based on the predicted future performance and potential returns of TUI Group. Desklib provides access to this and other solved assignments for students.

1 out of 22

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.