Kaplan Diploma of Finance and Mortgage Broking Management Assignment

VerifiedAdded on 2020/06/05

|53

|15679

|195

Homework Assignment

AI Summary

This assignment is for the Diploma of Finance and Mortgage Broking Management course, focusing on complex lending, broking, and business management skills. The assignment is divided into two sections. Section 1 requires answering questions based on case studies related to different lending scenarios. Section 2 involves completing tasks related to business management skills. The assignment includes details about Capital City Finance and Mortgage Brokers (CCF & MB), its services, partners, and team members, along with instructions for completion, submission, and grading. The goal is to apply knowledge of financial principles and demonstrate competence in broking and business management practices, with a focus on strategic alliances and business expansion.

Finance and Mortgage Broking Management

(DIPMB_AS_v1A3)

Please complete the fields shaded grey.

result (assessor to complete)

Parts that must be resubmitted:

Result — resubmission (if applicable)

(DIPMB_AS_v1A3)

Please complete the fields shaded grey.

result (assessor to complete)

Parts that must be resubmitted:

Result — resubmission (if applicable)

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

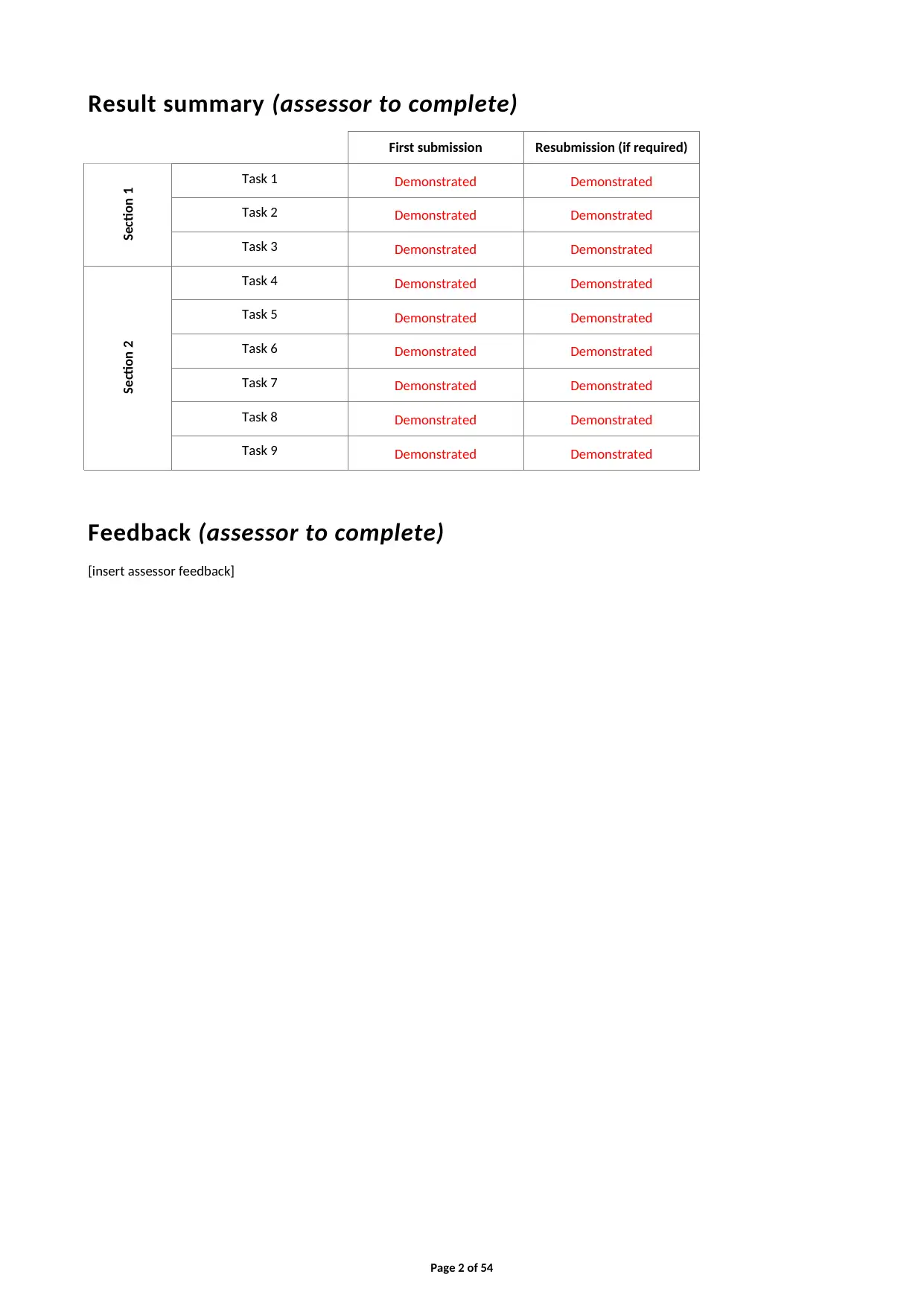

Result summary (assessor to complete)

First submission Resubmission (if required)

Section 1 Task 1 Demonstrated Demonstrated

Task 2 Demonstrated Demonstrated

Task 3 Demonstrated Demonstrated

Section 2

Task 4 Demonstrated Demonstrated

Task 5 Demonstrated Demonstrated

Task 6 Demonstrated Demonstrated

Task 7 Demonstrated Demonstrated

Task 8 Demonstrated Demonstrated

Task 9 Demonstrated Demonstrated

Feedback (assessor to complete)

[insert assessor feedback]

Page 2 of 54

First submission Resubmission (if required)

Section 1 Task 1 Demonstrated Demonstrated

Task 2 Demonstrated Demonstrated

Task 3 Demonstrated Demonstrated

Section 2

Task 4 Demonstrated Demonstrated

Task 5 Demonstrated Demonstrated

Task 6 Demonstrated Demonstrated

Task 7 Demonstrated Demonstrated

Task 8 Demonstrated Demonstrated

Task 9 Demonstrated Demonstrated

Feedback (assessor to complete)

[insert assessor feedback]

Page 2 of 54

Before you begin

Read everything in this document before you start your projectforDiploma of Finance and Mortgage

Broking Management.

About this document

This document includes the following parts:

• Instructions for completing and submitting this assignment

• Results and feedback

• Section 1: Complex lending and broking

• Section 2: Business management skills

Instructions for completing and submitting this assignment

How to use the study plan

We recommend that you use the study plan for this subject to help you manage your time to complete

the projectwithin your enrolment period. Your study plan is in the KapLearnDiploma of Finance and

Mortgage Broking Management subject room.

Completing the assignment

The assignment

This projectis split over 2 sections. The information and data you need to complete Sections 1 & 2 is

presented in case studies at the beginning of those sections and each task.

Section 1: Complex Lending and Broking

The first section on complex lending and broking, requires you to answer the questions for one (1) of the

three (3) available case studies. Each case study focuses on different lending scenario, (see diagram below).

Page 3 of 54

Read everything in this document before you start your projectforDiploma of Finance and Mortgage

Broking Management.

About this document

This document includes the following parts:

• Instructions for completing and submitting this assignment

• Results and feedback

• Section 1: Complex lending and broking

• Section 2: Business management skills

Instructions for completing and submitting this assignment

How to use the study plan

We recommend that you use the study plan for this subject to help you manage your time to complete

the projectwithin your enrolment period. Your study plan is in the KapLearnDiploma of Finance and

Mortgage Broking Management subject room.

Completing the assignment

The assignment

This projectis split over 2 sections. The information and data you need to complete Sections 1 & 2 is

presented in case studies at the beginning of those sections and each task.

Section 1: Complex Lending and Broking

The first section on complex lending and broking, requires you to answer the questions for one (1) of the

three (3) available case studies. Each case study focuses on different lending scenario, (see diagram below).

Page 3 of 54

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Section 2: Business management skills

Section 2 requires you to complete the six (6) tasks as listed in this template.

SECTION 1 SECTION 2

3 questions 6 questions

Choose

one path PLUS

Case Study A

Case Study B

Case Study C

Investment Property Finance

Commercial Equipment Finance

Commercial Premises Finance

OR

OR

Task 4–9

Business

Word count

The word count shown with each question is indicative only. You will not be penalised for exceeding the

suggested word count. Please do not include additional information which is outside the scope of the

question.

Additional research

When completing this assignment, assumptions are permitted although they must not be in conflict with

the information provided in the Case Studies.

You may also be required to source additional information from other organisations in the finance industry

to find the right products or services to meet your client’s requirements, or to calculate any service fees

that may be applicable.

Saving your work

Download this document to your desktop, type your answers in the spaces provided and save your work

regularly.

• Use the template provided, as other formats will not be accepted for these assignments.

• Name your file as follows: Clienttnumber_SubjectCode_Submissionnumber

(e.g. 12345678_DFP1B_Submission1).

• Include your clientt ID on the first page of the assignment.

Before you submit your work, please do a spell check and proofread your work to ensure that everything is

clear and unambiguous.

Do not delete/remove any sections of the document template.

Do not save your completed projectas a PDF.

The projectmust be completed before submitting it to Kaplan Professional Education.

Incomplete assignments will be returned to you unmarked.

Page 4 of 54

Section 2 requires you to complete the six (6) tasks as listed in this template.

SECTION 1 SECTION 2

3 questions 6 questions

Choose

one path PLUS

Case Study A

Case Study B

Case Study C

Investment Property Finance

Commercial Equipment Finance

Commercial Premises Finance

OR

OR

Task 4–9

Business

Word count

The word count shown with each question is indicative only. You will not be penalised for exceeding the

suggested word count. Please do not include additional information which is outside the scope of the

question.

Additional research

When completing this assignment, assumptions are permitted although they must not be in conflict with

the information provided in the Case Studies.

You may also be required to source additional information from other organisations in the finance industry

to find the right products or services to meet your client’s requirements, or to calculate any service fees

that may be applicable.

Saving your work

Download this document to your desktop, type your answers in the spaces provided and save your work

regularly.

• Use the template provided, as other formats will not be accepted for these assignments.

• Name your file as follows: Clienttnumber_SubjectCode_Submissionnumber

(e.g. 12345678_DFP1B_Submission1).

• Include your clientt ID on the first page of the assignment.

Before you submit your work, please do a spell check and proofread your work to ensure that everything is

clear and unambiguous.

Do not delete/remove any sections of the document template.

Do not save your completed projectas a PDF.

The projectmust be completed before submitting it to Kaplan Professional Education.

Incomplete assignments will be returned to you unmarked.

Page 4 of 54

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

The maximum file size is 5MB. Once you submit your projectfor marking you will be unable to make any

further changes to it.

You are able to submit your projectearlier than the deadline if you are confident you have completed all

parts and have prepared a quality submission.

The projectmarking process

You have 12 weeks from the date of your enrolment in this subject to submit your completed assignment.

Should your projectbe deemed ‘not yet competent’ you will be give an additional four (4) weeks to

resubmit your assignment.

Your assessor will mark your projectand return it to you in the Diploma of Finance and Mortgage Broking

Management subject room in KapLearn under the ‘Assessment’ tab.

Make a reasonable attempt

You must demonstrate that you have made a reasonable attempt to answer all of the questions in

your assignment. Failure to do so will mean that your projectwill not be accepted for marking;

therefore you will not receive the benefit of feedback on your submission.

If you do not meet these requirements, you will be notified. You will then have until your submission

deadline to submit your completed assignment.

How your projectis graded

Projecttasks are used to determine your ‘competence’ in demonstrating the required knowledge and/or

skills for each subject. As a result, you will be graded as either competent or not yet competent.

Your assessor will follow the below process when marking your assignment:

• Assess your responses to each question, and sub-parts if applicable, and then determine whether you

have demonstrated competence in each question.

• Determine if, on a holistic basis, your responses to the questions have demonstrated overall

competence.

Page 5 of 54

further changes to it.

You are able to submit your projectearlier than the deadline if you are confident you have completed all

parts and have prepared a quality submission.

The projectmarking process

You have 12 weeks from the date of your enrolment in this subject to submit your completed assignment.

Should your projectbe deemed ‘not yet competent’ you will be give an additional four (4) weeks to

resubmit your assignment.

Your assessor will mark your projectand return it to you in the Diploma of Finance and Mortgage Broking

Management subject room in KapLearn under the ‘Assessment’ tab.

Make a reasonable attempt

You must demonstrate that you have made a reasonable attempt to answer all of the questions in

your assignment. Failure to do so will mean that your projectwill not be accepted for marking;

therefore you will not receive the benefit of feedback on your submission.

If you do not meet these requirements, you will be notified. You will then have until your submission

deadline to submit your completed assignment.

How your projectis graded

Projecttasks are used to determine your ‘competence’ in demonstrating the required knowledge and/or

skills for each subject. As a result, you will be graded as either competent or not yet competent.

Your assessor will follow the below process when marking your assignment:

• Assess your responses to each question, and sub-parts if applicable, and then determine whether you

have demonstrated competence in each question.

• Determine if, on a holistic basis, your responses to the questions have demonstrated overall

competence.

Page 5 of 54

‘Not yet competent’ and resubmissions

Should sections of your projectbe marked as ‘not yet competent’ you will be given an additional

opportunity to amend your responses so that you can demonstrate your competency to the required level.

You must address the assessor’s feedback in your amended responses. You only need amend those sections

where the assessor has determined you are ‘not yet competent’.

Make changes to your original submission. Use a different text colour for your resubmission. Your assessor

will be in a better position to gauge the quality and nature of your changes. Ensure you leave your first

assessor’s comments in your assignment, so your second assessor can see the instructions that were

originally provided for you. Do not change any comments made by a Kaplan assessor.

We are here to help

If you have any questions about this projectyou can post your query at the ‘Ask your Tutor’ forum in your

subject room. You can expect an answer within 24 hours of your posting from one of our technical advisers

or clientt support staff.

Page 6 of 54

Should sections of your projectbe marked as ‘not yet competent’ you will be given an additional

opportunity to amend your responses so that you can demonstrate your competency to the required level.

You must address the assessor’s feedback in your amended responses. You only need amend those sections

where the assessor has determined you are ‘not yet competent’.

Make changes to your original submission. Use a different text colour for your resubmission. Your assessor

will be in a better position to gauge the quality and nature of your changes. Ensure you leave your first

assessor’s comments in your assignment, so your second assessor can see the instructions that were

originally provided for you. Do not change any comments made by a Kaplan assessor.

We are here to help

If you have any questions about this projectyou can post your query at the ‘Ask your Tutor’ forum in your

subject room. You can expect an answer within 24 hours of your posting from one of our technical advisers

or clientt support staff.

Page 6 of 54

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Capital City Finance and Mortgage Brokers (CCF & MB)

George and Mildred are very happy with the way you service your clients and are sure that you are a good

fit for the team. They now want you to turn your focus to your primary task which is to assist in expanding

the business by building relationships with selected real estate agents, accountants and legal firms through

strategic alliances. They also want you to consider how CCF & MB can consolidate its relationships with its

existing strategic partners.

Let’s recap on what you already know about Capital City Finance and Mortgage Brokers (CCF & MB).

It’s a family owned business providing a range of mortgage and finance broking services to the business and

private sectors, with experience in all facets of finance and insurance providing expert advice covering a

multitude of products and options existing within the market.

CCF & MB specialises in home loans, commercial lending, business lending, personal and motor vehicle

finance and insurance (life and general), and focuses on helping clients find the finance service suited to

their individual circumstances.

It provides its services through its association with the following partners:

• Australian Aggregators, a rising business in the aggregation business with an extensive panel of

residential and commercial lenders, and asset finance.

• ABC General Insurance, a boutique insurance company specialising in a full range of general insurances.

• XYZ Life a small family-owned insurance brokerage specialising in the full range of life insurance

products.

Based in the city, CCF & MB has the capacity to service clients from their office or anywhere at their clients’

convenience through its team of mobile brokers.

CCF & MB does not hold a credit license but operates as a credit representative of Australian Aggregators.

Since its inception 13 years ago CCF & MB has built a loan book of almost $1.2 billion and averages over

$120 million in new loans annually.

CCF &MB’s vision is to be the mortgage and finance broker of choice in the greater metropolitan area

CCF & MB’s mission statement is to operate professionally in accordance with legislation, our licence and

professional standards

CCF & MB’s values are as follows:

• to act with honesty and integrity at all times

• to provide unbiased advice and conduct business, free from any conflict of interest

• to maintain confidentiality in all dealings

• to meet all NCCP regulatory requirements

• to comply with all mortgage industry laws and regulations

• ensure quality and efficiency in its loan processes.

Page 7 of 54

George and Mildred are very happy with the way you service your clients and are sure that you are a good

fit for the team. They now want you to turn your focus to your primary task which is to assist in expanding

the business by building relationships with selected real estate agents, accountants and legal firms through

strategic alliances. They also want you to consider how CCF & MB can consolidate its relationships with its

existing strategic partners.

Let’s recap on what you already know about Capital City Finance and Mortgage Brokers (CCF & MB).

It’s a family owned business providing a range of mortgage and finance broking services to the business and

private sectors, with experience in all facets of finance and insurance providing expert advice covering a

multitude of products and options existing within the market.

CCF & MB specialises in home loans, commercial lending, business lending, personal and motor vehicle

finance and insurance (life and general), and focuses on helping clients find the finance service suited to

their individual circumstances.

It provides its services through its association with the following partners:

• Australian Aggregators, a rising business in the aggregation business with an extensive panel of

residential and commercial lenders, and asset finance.

• ABC General Insurance, a boutique insurance company specialising in a full range of general insurances.

• XYZ Life a small family-owned insurance brokerage specialising in the full range of life insurance

products.

Based in the city, CCF & MB has the capacity to service clients from their office or anywhere at their clients’

convenience through its team of mobile brokers.

CCF & MB does not hold a credit license but operates as a credit representative of Australian Aggregators.

Since its inception 13 years ago CCF & MB has built a loan book of almost $1.2 billion and averages over

$120 million in new loans annually.

CCF &MB’s vision is to be the mortgage and finance broker of choice in the greater metropolitan area

CCF & MB’s mission statement is to operate professionally in accordance with legislation, our licence and

professional standards

CCF & MB’s values are as follows:

• to act with honesty and integrity at all times

• to provide unbiased advice and conduct business, free from any conflict of interest

• to maintain confidentiality in all dealings

• to meet all NCCP regulatory requirements

• to comply with all mortgage industry laws and regulations

• ensure quality and efficiency in its loan processes.

Page 7 of 54

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

CCF & MB’s people

CCF & MB is owned by husband and wife, George and Mildred Spencer.

With over 35 years’ experience in finance and business ownership, George established and built a

successful business dedicated to assisting clients with managing their finances effectively. Starting the

business with his wife Mildred 13 years ago, George gained immense satisfaction in seeing it expand to

service more and more clients across the city and greater metropolitan area. Although in recent years he

has stepped back from dealing directly with clients, he still maintains a small select clientele. He also takes

great pride in training and mentoring his team to enhance their performance.

Mildred has over 22 years of lending experience and is qualified not only to assist her clients with their

mortgage requirements but also to assist them with their commercial finance requirements. She also holds

financial planning qualifications. She specialises in asset finance.

The company has a small team of five additional consultants and two administration staff members.

Profiles for the team is as follows:

• Jennifer Dee is recognised as one of the top female brokers in Australia. She has been in the broking

industry for over 10 years and has a passion and dedication to assist and accommodate all of her clients’

needs with their financial dreams. Jennifer is an Accredited Mortgage Consultant with the Mortgage and

Finance Association of Australia (MFAA).

• Louise Spencer (George and Mildred’s eldest daughter) is an Accredited Mortgage Consultant with the

Mortgage and Finance Association of Australia (MFAA) and has been working as a loan consultant for

almost two years. Louise started off in the lending industry in the office as an administrator to gain as

much experience and knowledge as possible before taking a broking role. Her passion for helping her

clients ensures that she is always available to her clients at a time and place convenient for them.

• Michael Spencer is George’s younger brother and is CCF & MB’s equipment finance specialist. He has

over 25 years working in the equipment finance industry. He has developed an in depth understanding

of the transport and agricultural industries, and also provides finance for general equipment,

motor vehicles and computer equipment.

• Martin Long has specialised in equipment finance for the last three years, but prior to this he spent

five years operating his own retail food business. This practical experience allows him to see things from

his client’s point of view, including experience with equipment finance. He specialises in plant and

equipment in the machinery, woodworking and packaging industries. Examples of some of the

equipment he has financed are farm machinery, extrusion lines, plastic injection moulders,

commercial catering equipment, woodworking plant, packaging lines, forklifts, office fit-outs and many

different motor vehicles.

• Luis Ramirez migrated to Australia in 25 years ago as a young boy with his family. After completing

high school he graduated from university with an accounting degree and worked in ANZ in commercial

lending. He joined CCF & MB 4 years ago and specialises in vehicle and capital equipment financing.

He provides ITC and general equipment lease funding options for clients. By providing better outcomes,

both during and at the end of their equipment leases, Luis’ many clients have been able to reduce costs

and maximise the value of their available budgets.

CCF & MB is a member of the MFAA as a broking business dealing directly with the public. Both George and

Mildred are fellows of the MFAA. CCF & MB is also a corporate member of the FBAA.

All staff members, including consultants, are paid an annual salary plus superannuation. Consultants also

receive a car allowance plus a percentage of trail commissions that are paid quarterly based on their

performance targets.

Page 8 of 54

CCF & MB is owned by husband and wife, George and Mildred Spencer.

With over 35 years’ experience in finance and business ownership, George established and built a

successful business dedicated to assisting clients with managing their finances effectively. Starting the

business with his wife Mildred 13 years ago, George gained immense satisfaction in seeing it expand to

service more and more clients across the city and greater metropolitan area. Although in recent years he

has stepped back from dealing directly with clients, he still maintains a small select clientele. He also takes

great pride in training and mentoring his team to enhance their performance.

Mildred has over 22 years of lending experience and is qualified not only to assist her clients with their

mortgage requirements but also to assist them with their commercial finance requirements. She also holds

financial planning qualifications. She specialises in asset finance.

The company has a small team of five additional consultants and two administration staff members.

Profiles for the team is as follows:

• Jennifer Dee is recognised as one of the top female brokers in Australia. She has been in the broking

industry for over 10 years and has a passion and dedication to assist and accommodate all of her clients’

needs with their financial dreams. Jennifer is an Accredited Mortgage Consultant with the Mortgage and

Finance Association of Australia (MFAA).

• Louise Spencer (George and Mildred’s eldest daughter) is an Accredited Mortgage Consultant with the

Mortgage and Finance Association of Australia (MFAA) and has been working as a loan consultant for

almost two years. Louise started off in the lending industry in the office as an administrator to gain as

much experience and knowledge as possible before taking a broking role. Her passion for helping her

clients ensures that she is always available to her clients at a time and place convenient for them.

• Michael Spencer is George’s younger brother and is CCF & MB’s equipment finance specialist. He has

over 25 years working in the equipment finance industry. He has developed an in depth understanding

of the transport and agricultural industries, and also provides finance for general equipment,

motor vehicles and computer equipment.

• Martin Long has specialised in equipment finance for the last three years, but prior to this he spent

five years operating his own retail food business. This practical experience allows him to see things from

his client’s point of view, including experience with equipment finance. He specialises in plant and

equipment in the machinery, woodworking and packaging industries. Examples of some of the

equipment he has financed are farm machinery, extrusion lines, plastic injection moulders,

commercial catering equipment, woodworking plant, packaging lines, forklifts, office fit-outs and many

different motor vehicles.

• Luis Ramirez migrated to Australia in 25 years ago as a young boy with his family. After completing

high school he graduated from university with an accounting degree and worked in ANZ in commercial

lending. He joined CCF & MB 4 years ago and specialises in vehicle and capital equipment financing.

He provides ITC and general equipment lease funding options for clients. By providing better outcomes,

both during and at the end of their equipment leases, Luis’ many clients have been able to reduce costs

and maximise the value of their available budgets.

CCF & MB is a member of the MFAA as a broking business dealing directly with the public. Both George and

Mildred are fellows of the MFAA. CCF & MB is also a corporate member of the FBAA.

All staff members, including consultants, are paid an annual salary plus superannuation. Consultants also

receive a car allowance plus a percentage of trail commissions that are paid quarterly based on their

performance targets.

Page 8 of 54

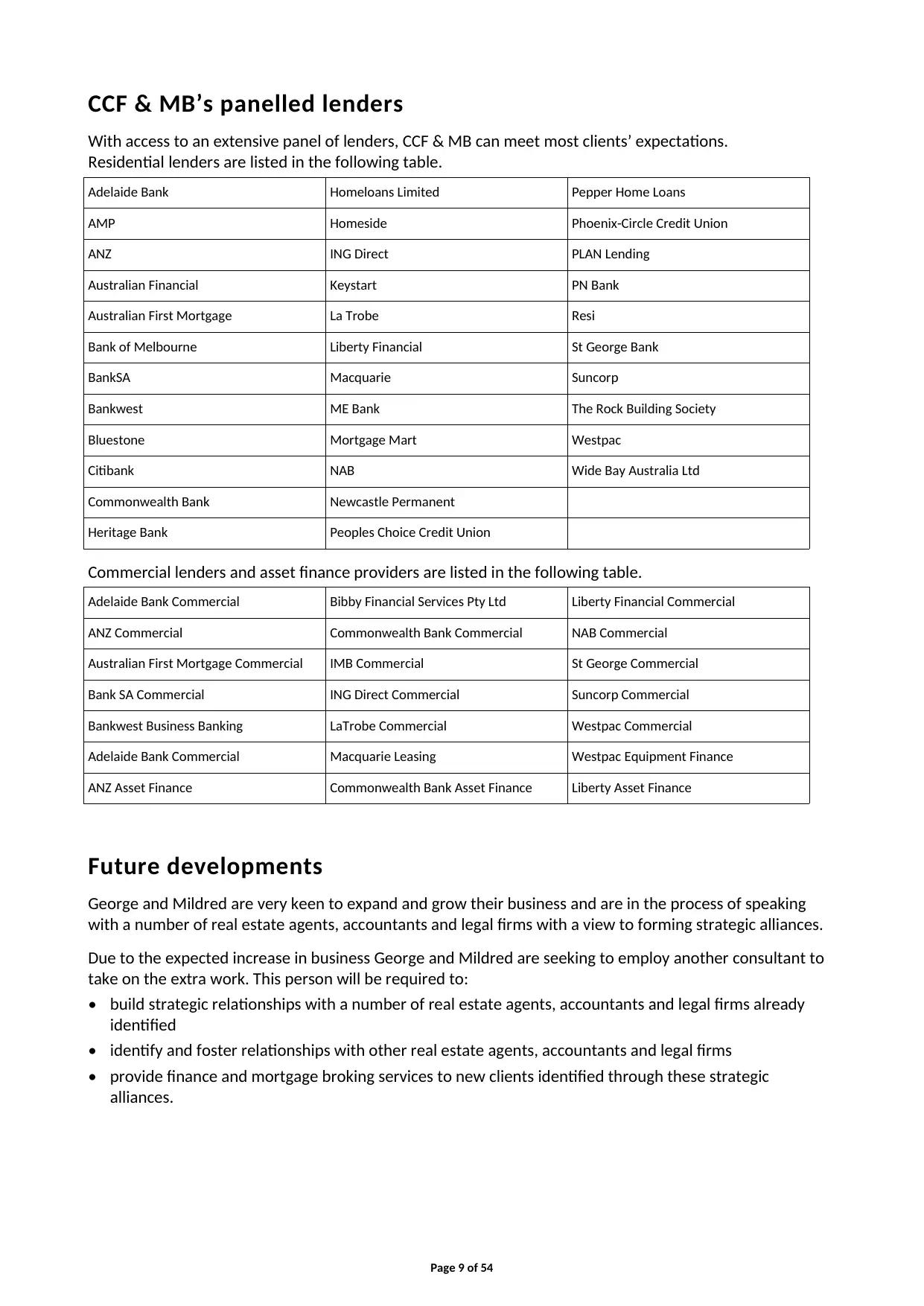

CCF & MB’s panelled lenders

With access to an extensive panel of lenders, CCF & MB can meet most clients’ expectations.

Residential lenders are listed in the following table.

Adelaide Bank Homeloans Limited Pepper Home Loans

AMP Homeside Phoenix-Circle Credit Union

ANZ ING Direct PLAN Lending

Australian Financial Keystart PN Bank

Australian First Mortgage La Trobe Resi

Bank of Melbourne Liberty Financial St George Bank

BankSA Macquarie Suncorp

Bankwest ME Bank The Rock Building Society

Bluestone Mortgage Mart Westpac

Citibank NAB Wide Bay Australia Ltd

Commonwealth Bank Newcastle Permanent

Heritage Bank Peoples Choice Credit Union

Commercial lenders and asset finance providers are listed in the following table.

Adelaide Bank Commercial Bibby Financial Services Pty Ltd Liberty Financial Commercial

ANZ Commercial Commonwealth Bank Commercial NAB Commercial

Australian First Mortgage Commercial IMB Commercial St George Commercial

Bank SA Commercial ING Direct Commercial Suncorp Commercial

Bankwest Business Banking LaTrobe Commercial Westpac Commercial

Adelaide Bank Commercial Macquarie Leasing Westpac Equipment Finance

ANZ Asset Finance Commonwealth Bank Asset Finance Liberty Asset Finance

Future developments

George and Mildred are very keen to expand and grow their business and are in the process of speaking

with a number of real estate agents, accountants and legal firms with a view to forming strategic alliances.

Due to the expected increase in business George and Mildred are seeking to employ another consultant to

take on the extra work. This person will be required to:

• build strategic relationships with a number of real estate agents, accountants and legal firms already

identified

• identify and foster relationships with other real estate agents, accountants and legal firms

• provide finance and mortgage broking services to new clients identified through these strategic

alliances.

Page 9 of 54

With access to an extensive panel of lenders, CCF & MB can meet most clients’ expectations.

Residential lenders are listed in the following table.

Adelaide Bank Homeloans Limited Pepper Home Loans

AMP Homeside Phoenix-Circle Credit Union

ANZ ING Direct PLAN Lending

Australian Financial Keystart PN Bank

Australian First Mortgage La Trobe Resi

Bank of Melbourne Liberty Financial St George Bank

BankSA Macquarie Suncorp

Bankwest ME Bank The Rock Building Society

Bluestone Mortgage Mart Westpac

Citibank NAB Wide Bay Australia Ltd

Commonwealth Bank Newcastle Permanent

Heritage Bank Peoples Choice Credit Union

Commercial lenders and asset finance providers are listed in the following table.

Adelaide Bank Commercial Bibby Financial Services Pty Ltd Liberty Financial Commercial

ANZ Commercial Commonwealth Bank Commercial NAB Commercial

Australian First Mortgage Commercial IMB Commercial St George Commercial

Bank SA Commercial ING Direct Commercial Suncorp Commercial

Bankwest Business Banking LaTrobe Commercial Westpac Commercial

Adelaide Bank Commercial Macquarie Leasing Westpac Equipment Finance

ANZ Asset Finance Commonwealth Bank Asset Finance Liberty Asset Finance

Future developments

George and Mildred are very keen to expand and grow their business and are in the process of speaking

with a number of real estate agents, accountants and legal firms with a view to forming strategic alliances.

Due to the expected increase in business George and Mildred are seeking to employ another consultant to

take on the extra work. This person will be required to:

• build strategic relationships with a number of real estate agents, accountants and legal firms already

identified

• identify and foster relationships with other real estate agents, accountants and legal firms

• provide finance and mortgage broking services to new clients identified through these strategic

alliances.

Page 9 of 54

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

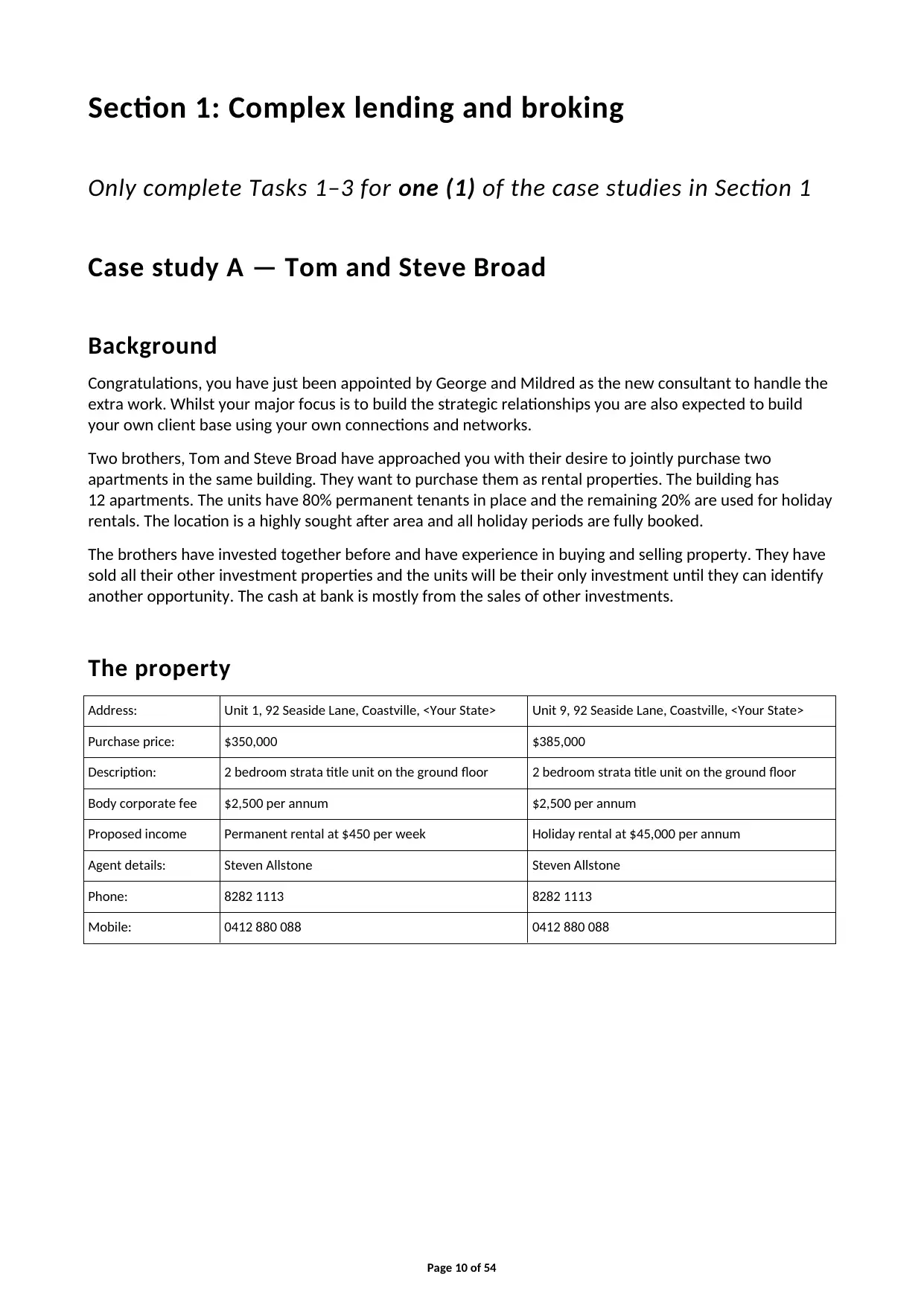

Section 1: Complex lending and broking

Only complete Tasks 1–3 for one (1) of the case studies in Section 1

Case study A — Tom and Steve Broad

Background

Congratulations, you have just been appointed by George and Mildred as the new consultant to handle the

extra work. Whilst your major focus is to build the strategic relationships you are also expected to build

your own client base using your own connections and networks.

Two brothers, Tom and Steve Broad have approached you with their desire to jointly purchase two

apartments in the same building. They want to purchase them as rental properties. The building has

12 apartments. The units have 80% permanent tenants in place and the remaining 20% are used for holiday

rentals. The location is a highly sought after area and all holiday periods are fully booked.

The brothers have invested together before and have experience in buying and selling property. They have

sold all their other investment properties and the units will be their only investment until they can identify

another opportunity. The cash at bank is mostly from the sales of other investments.

The property

Address: Unit 1, 92 Seaside Lane, Coastville, <Your State> Unit 9, 92 Seaside Lane, Coastville, <Your State>

Purchase price: $350,000 $385,000

Description: 2 bedroom strata title unit on the ground floor 2 bedroom strata title unit on the ground floor

Body corporate fee $2,500 per annum $2,500 per annum

Proposed income Permanent rental at $450 per week Holiday rental at $45,000 per annum

Agent details: Steven Allstone Steven Allstone

Phone: 8282 1113 8282 1113

Mobile: 0412 880 088 0412 880 088

Page 10 of 54

Only complete Tasks 1–3 for one (1) of the case studies in Section 1

Case study A — Tom and Steve Broad

Background

Congratulations, you have just been appointed by George and Mildred as the new consultant to handle the

extra work. Whilst your major focus is to build the strategic relationships you are also expected to build

your own client base using your own connections and networks.

Two brothers, Tom and Steve Broad have approached you with their desire to jointly purchase two

apartments in the same building. They want to purchase them as rental properties. The building has

12 apartments. The units have 80% permanent tenants in place and the remaining 20% are used for holiday

rentals. The location is a highly sought after area and all holiday periods are fully booked.

The brothers have invested together before and have experience in buying and selling property. They have

sold all their other investment properties and the units will be their only investment until they can identify

another opportunity. The cash at bank is mostly from the sales of other investments.

The property

Address: Unit 1, 92 Seaside Lane, Coastville, <Your State> Unit 9, 92 Seaside Lane, Coastville, <Your State>

Purchase price: $350,000 $385,000

Description: 2 bedroom strata title unit on the ground floor 2 bedroom strata title unit on the ground floor

Body corporate fee $2,500 per annum $2,500 per annum

Proposed income Permanent rental at $450 per week Holiday rental at $45,000 per annum

Agent details: Steven Allstone Steven Allstone

Phone: 8282 1113 8282 1113

Mobile: 0412 880 088 0412 880 088

Page 10 of 54

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

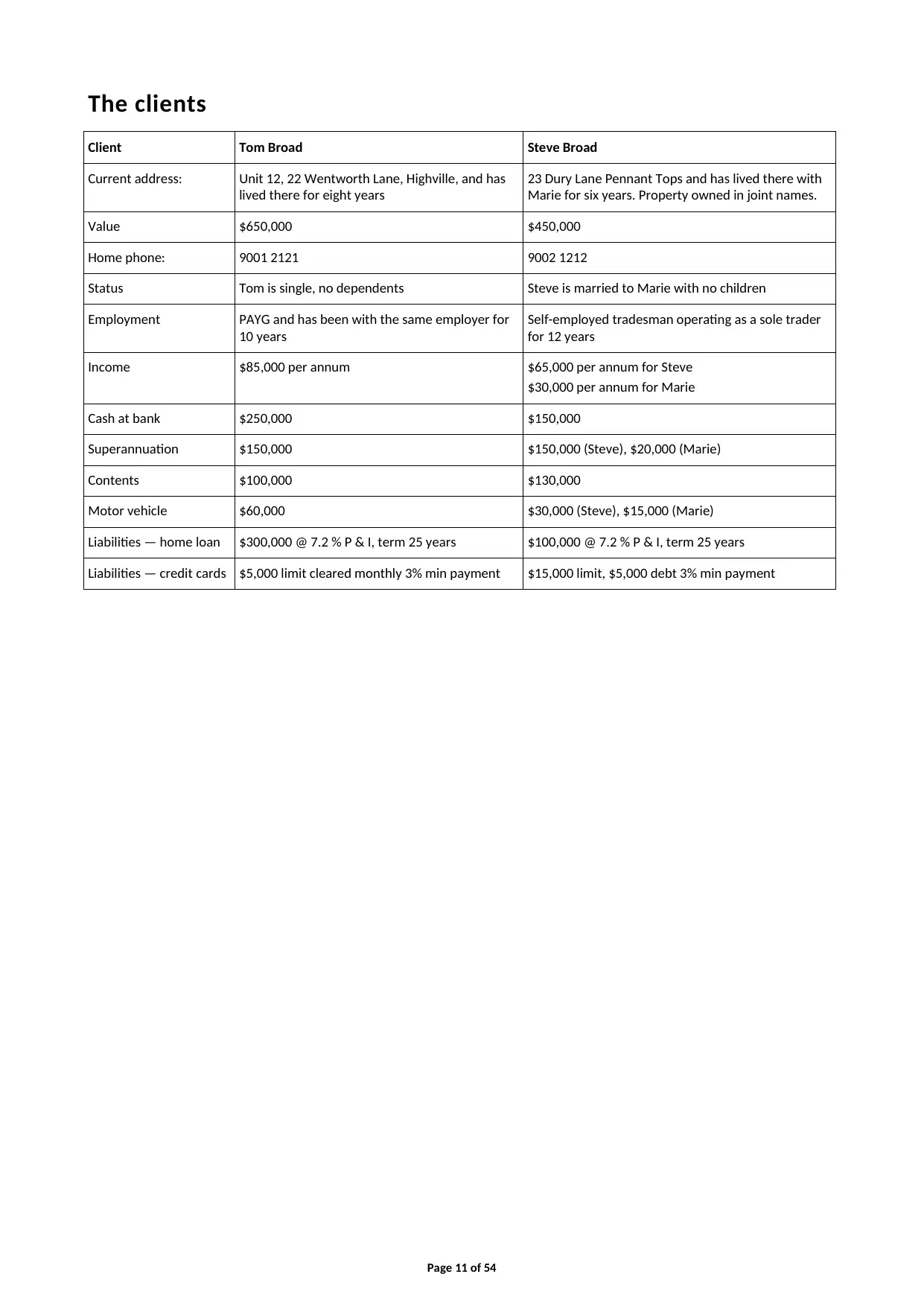

The clients

Client Tom Broad Steve Broad

Current address: Unit 12, 22 Wentworth Lane, Highville, and has

lived there for eight years

23 Dury Lane Pennant Tops and has lived there with

Marie for six years. Property owned in joint names.

Value $650,000 $450,000

Home phone: 9001 2121 9002 1212

Status Tom is single, no dependents Steve is married to Marie with no children

Employment PAYG and has been with the same employer for

10 years

Self-employed tradesman operating as a sole trader

for 12 years

Income $85,000 per annum $65,000 per annum for Steve

$30,000 per annum for Marie

Cash at bank $250,000 $150,000

Superannuation $150,000 $150,000 (Steve), $20,000 (Marie)

Contents $100,000 $130,000

Motor vehicle $60,000 $30,000 (Steve), $15,000 (Marie)

Liabilities — home loan $300,000 @ 7.2 % P & I, term 25 years $100,000 @ 7.2 % P & I, term 25 years

Liabilities — credit cards $5,000 limit cleared monthly 3% min payment $15,000 limit, $5,000 debt 3% min payment

Page 11 of 54

Client Tom Broad Steve Broad

Current address: Unit 12, 22 Wentworth Lane, Highville, and has

lived there for eight years

23 Dury Lane Pennant Tops and has lived there with

Marie for six years. Property owned in joint names.

Value $650,000 $450,000

Home phone: 9001 2121 9002 1212

Status Tom is single, no dependents Steve is married to Marie with no children

Employment PAYG and has been with the same employer for

10 years

Self-employed tradesman operating as a sole trader

for 12 years

Income $85,000 per annum $65,000 per annum for Steve

$30,000 per annum for Marie

Cash at bank $250,000 $150,000

Superannuation $150,000 $150,000 (Steve), $20,000 (Marie)

Contents $100,000 $130,000

Motor vehicle $60,000 $30,000 (Steve), $15,000 (Marie)

Liabilities — home loan $300,000 @ 7.2 % P & I, term 25 years $100,000 @ 7.2 % P & I, term 25 years

Liabilities — credit cards $5,000 limit cleared monthly 3% min payment $15,000 limit, $5,000 debt 3% min payment

Page 11 of 54

Projecttasks(clientt to complete)

Task 1a — Identify the clients’ complex broking needs

Prepare a list of questions that you would need to ask Tom and Steve about their history and experience,

and the unit purchase.

In preparing your list of questions you should ensure that you cover the following:

• The complex features of Tom’s and Steve’s situation and objectives.

• Potential risks and Tom’s and Steve’s tolerance of risk. In considering risk you should consider:

– how you would identify the risks and the criteria you used to evaluate these risks

– how you would assess their current exposure, the tools you would use in terms of probability,

impact and the consequences.

(800 words)

Clientt response to Task 1a

Answer here

Assessor feedback: Resubmission required?

No

Page 12 of 54

Task 1a — Identify the clients’ complex broking needs

Prepare a list of questions that you would need to ask Tom and Steve about their history and experience,

and the unit purchase.

In preparing your list of questions you should ensure that you cover the following:

• The complex features of Tom’s and Steve’s situation and objectives.

• Potential risks and Tom’s and Steve’s tolerance of risk. In considering risk you should consider:

– how you would identify the risks and the criteria you used to evaluate these risks

– how you would assess their current exposure, the tools you would use in terms of probability,

impact and the consequences.

(800 words)

Clientt response to Task 1a

Answer here

Assessor feedback: Resubmission required?

No

Page 12 of 54

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 53

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.