University of Bedfordshire: Corporate Finance Analysis of Netflix

VerifiedAdded on 2022/09/06

|17

|3821

|13

Report

AI Summary

This report provides a comprehensive financial analysis of Netflix, examining its capital structure, dividend policies, and corporate strategies based on its 2018 annual report and market data. The analysis includes an overview of Netflix's background, tracing its evolution from DVD rentals to a global media streaming leader. It delves into the company's capital structure, highlighting its increasing reliance on debt financing and analyzing its cost of capital. The report also explores Netflix's dividend policy, which has maintained a 0.00% dividend payout ratio in recent years. Furthermore, the report assesses capital needs and financing decisions, proposing a balanced approach to raising capital through a mix of equity and debt. Investment appraisal techniques, including Net Present Value (NPV), Internal Rate of Return (IRR), Discounted Payback Period, Accounting Rate of Return, and Profitability Index are discussed. Finally, the report concludes with a summary of the company's financial strengths and weaknesses, offering recommendations for improving financial and operational performance. This detailed analysis provides valuable insights into Netflix's financial health and strategic decision-making.

Running head: CORPORATE FINANCE

Corporate Finance

Name of the Student:

Name of the University:

Author’s Note:

Corporate Finance

Name of the Student:

Name of the University:

Author’s Note:

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

1CORPORATE FINANCE

Executive Summary:

This report is prepared to analysis the financial and operational performance of the Netflix a

listed company along with an analysis of its capital structure and dividend policies. Corporate

finance discuses about the capital structure, dividend policies and corporate strategies which

aims at maximising the shareholders’ wealth and helps in achieving the mission and vision of

the company. In this report the capital structure, dividend policies and corporate strategies of

the Netflix have been analysed taking information from the 2018 Annual report of the Netflix

along with some market related information. An in-depth analysis of the financial strategies

and comparative performance of the company has been conducted to find the investment

opportunities and challenges for the company. Various financing strategies have been

analysed and suggested for financing such investment and expansion opportunities for the

company. Though Netflix has been performing well financially for the last few years, still

there are some expansion opportunities which can be explored further. Lastly, the report

concludes with outlining the financial strength and weaknesses of the company along with

certain recommendations for improvement in the financial and operational performance of

the company.

Executive Summary:

This report is prepared to analysis the financial and operational performance of the Netflix a

listed company along with an analysis of its capital structure and dividend policies. Corporate

finance discuses about the capital structure, dividend policies and corporate strategies which

aims at maximising the shareholders’ wealth and helps in achieving the mission and vision of

the company. In this report the capital structure, dividend policies and corporate strategies of

the Netflix have been analysed taking information from the 2018 Annual report of the Netflix

along with some market related information. An in-depth analysis of the financial strategies

and comparative performance of the company has been conducted to find the investment

opportunities and challenges for the company. Various financing strategies have been

analysed and suggested for financing such investment and expansion opportunities for the

company. Though Netflix has been performing well financially for the last few years, still

there are some expansion opportunities which can be explored further. Lastly, the report

concludes with outlining the financial strength and weaknesses of the company along with

certain recommendations for improvement in the financial and operational performance of

the company.

2CORPORATE FINANCE

Table of Contents

1. Introduction:...........................................................................................................................3

2. Background to the company:.................................................................................................3

3. Analysis of capital structure and dividend policy of the Netflix:..........................................5

4. Capital needs and financing decisions:..................................................................................7

5. Application of the investment appraisal techniques:.............................................................9

Net present value method:....................................................................................................11

Internal rate of return method:.............................................................................................12

Discounted payback period method:....................................................................................12

Accounting rate of return method:.......................................................................................12

Profitability index method:..................................................................................................13

6. Conclusion and recommendation:........................................................................................13

References and bibliography:...................................................................................................15

Table of Contents

1. Introduction:...........................................................................................................................3

2. Background to the company:.................................................................................................3

3. Analysis of capital structure and dividend policy of the Netflix:..........................................5

4. Capital needs and financing decisions:..................................................................................7

5. Application of the investment appraisal techniques:.............................................................9

Net present value method:....................................................................................................11

Internal rate of return method:.............................................................................................12

Discounted payback period method:....................................................................................12

Accounting rate of return method:.......................................................................................12

Profitability index method:..................................................................................................13

6. Conclusion and recommendation:........................................................................................13

References and bibliography:...................................................................................................15

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

3CORPORATE FINANCE

1. Introduction:

Corporate finance is a special branch of financial accounting and financial

management, which discusses about the need of capital for a company, sources of raising

capital and ensures its efficient utilisation towards achieving the objective of shareholders’

wealth maximisation. Every business organizations require capital to finance their investment

activities and to run their business with sustainability. Selection of such sources of capital

which will be minimizing the overall cost of capital and will help in maximising the

shareholders’ wealth is known as capital structure. In the next stage, investment of funds in

better investment opportunities is known as the capital budgeting and lastly, decisions

relating to the dividend pay-out is known as the dividend policy. Dividend policies also have

an immense importance in corporate strategies as it is directly related with the own sources of

capital (Yapa 2017).

In this report the need for capital and its sources for the Netflix have been analysed

based on the information available in their 2018 annual report. Based on last few years’

dividend pay-outs, the dividend policies of the Netflix has been analysed and the overall

corporate strategies have been analysed to arrive at a conclusion about the financial

performance and financial position of the company(Liand Trutnevyte2017).

2. Background to the company:

Netflix Inc. is an American company providing media services across the world. The

company was founded in the year 1997 with their primary service of providing video

streaming on a paid subscription basis. Later on with its success in the media services

industry, it become one of the leader in the media service industry across the world. They

kept their business patter same as it was started with earlier. As of 2019 they had more than

1. Introduction:

Corporate finance is a special branch of financial accounting and financial

management, which discusses about the need of capital for a company, sources of raising

capital and ensures its efficient utilisation towards achieving the objective of shareholders’

wealth maximisation. Every business organizations require capital to finance their investment

activities and to run their business with sustainability. Selection of such sources of capital

which will be minimizing the overall cost of capital and will help in maximising the

shareholders’ wealth is known as capital structure. In the next stage, investment of funds in

better investment opportunities is known as the capital budgeting and lastly, decisions

relating to the dividend pay-out is known as the dividend policy. Dividend policies also have

an immense importance in corporate strategies as it is directly related with the own sources of

capital (Yapa 2017).

In this report the need for capital and its sources for the Netflix have been analysed

based on the information available in their 2018 annual report. Based on last few years’

dividend pay-outs, the dividend policies of the Netflix has been analysed and the overall

corporate strategies have been analysed to arrive at a conclusion about the financial

performance and financial position of the company(Liand Trutnevyte2017).

2. Background to the company:

Netflix Inc. is an American company providing media services across the world. The

company was founded in the year 1997 with their primary service of providing video

streaming on a paid subscription basis. Later on with its success in the media services

industry, it become one of the leader in the media service industry across the world. They

kept their business patter same as it was started with earlier. As of 2019 they had more than

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

4CORPORATE FINANCE

148 million subscriptions across the world. The company was listed as one of the fortune 500

companies in the year 208 in United States for their highest revenue(In.finance.yahoo.com

2019).

Initially they started their business with DVD sales and DVD rentals, later on with the

advancement and revolution in the technologies, they completely switched over to the online

video and media streaming business. It can be traced back to 1999 when they started the

media streaming business with the concept of paid subscription and in the year 2000 they

dropped the DVD rental model of their business. In that year with a drastic fall in their

operating and financial performance, they were offer with $50 million for acquisition by the

Blockbuster. They refused the proposal and experienced a rapid growth in their financial and

operation performance in the year 2001 with an increase in the paid subscription.

In May 2002, they went for initial public offering of their common stocks with a

volume of 5.5 million shares at an initial price of $15 per share. In the same year, in the

month of June they again issued additional 825,000 shares to raise more capital to finance

their business with an objective of global reach of their business. After making loss for last

few consecutive years, they reported a profit of $6.5 million in the year 2003 from a revenue

of $272 million.

In the year 2005 Netflix acquired several movie rights and they designed and

developed the box and service and were ready to going public for offering the service, but

with the inspiration from the You Tube, they scrapped their concept of hardware based and

high content based movie renting service and planned to introduce the service of video on

demand. In 2007 they moved away from their business of DVD rentals and executed their

plan to provide video on demand through internet. From 2006 to 2011, their DVD sales

148 million subscriptions across the world. The company was listed as one of the fortune 500

companies in the year 208 in United States for their highest revenue(In.finance.yahoo.com

2019).

Initially they started their business with DVD sales and DVD rentals, later on with the

advancement and revolution in the technologies, they completely switched over to the online

video and media streaming business. It can be traced back to 1999 when they started the

media streaming business with the concept of paid subscription and in the year 2000 they

dropped the DVD rental model of their business. In that year with a drastic fall in their

operating and financial performance, they were offer with $50 million for acquisition by the

Blockbuster. They refused the proposal and experienced a rapid growth in their financial and

operation performance in the year 2001 with an increase in the paid subscription.

In May 2002, they went for initial public offering of their common stocks with a

volume of 5.5 million shares at an initial price of $15 per share. In the same year, in the

month of June they again issued additional 825,000 shares to raise more capital to finance

their business with an objective of global reach of their business. After making loss for last

few consecutive years, they reported a profit of $6.5 million in the year 2003 from a revenue

of $272 million.

In the year 2005 Netflix acquired several movie rights and they designed and

developed the box and service and were ready to going public for offering the service, but

with the inspiration from the You Tube, they scrapped their concept of hardware based and

high content based movie renting service and planned to introduce the service of video on

demand. In 2007 they moved away from their business of DVD rentals and executed their

plan to provide video on demand through internet. From 2006 to 2011, their DVD sales

5CORPORATE FINANCE

decreased and with the increase in their online subscriptions for video on demand, they grew

up and made a worldwide presence (In.finance.yahoo.com 2019).

In 2014 the company reached to the 50 million global subscriptions and a 32.3%

market share in the United States video streaming industry. In that year they had been

operating in more than 41 countries, but still then they had most of the subscriptions from the

United States only. Almost 70% of their total subscribers were from United States. Hence,

they had to change and revise their marketing and corporate strategies to reach out to the

global market actually. In 2016 they announced an expansion of their services to 150 more

countries. In 2016 they increased their security measures and improved their services with a

remark of 74.8 million global subscriptions and in the next year it reached a subscription of

more than 100 million.

With the growth in their market share and improvement in their services, the market

capitalisation of the company crossed the $100 billion figure and their market price per share

surged to a high of $301.05 which was beyond their 12 months target. Therefore, the

company started with the objective of providing high quality media services initially through

the DVD sales and rental, and they changed their strategies timely with the change in

scenarios and improvement and advancement with the technologies. It paved the way for

their success and now, the Netflix can be considered as one of the global leader in

subscription based media streaming business.

3. Analysis of capital structure and dividend policy of the Netflix:

Capital structure is the combination of debt capital and equity capital in the total

capital base of the company. For use of capital, every company have to pay certain amount of

consideration, which is known as the cost of capital (Yapa 2017). An efficient capital

structure ensures the minimum overall cost of capital. Netflix is a global company and a

decreased and with the increase in their online subscriptions for video on demand, they grew

up and made a worldwide presence (In.finance.yahoo.com 2019).

In 2014 the company reached to the 50 million global subscriptions and a 32.3%

market share in the United States video streaming industry. In that year they had been

operating in more than 41 countries, but still then they had most of the subscriptions from the

United States only. Almost 70% of their total subscribers were from United States. Hence,

they had to change and revise their marketing and corporate strategies to reach out to the

global market actually. In 2016 they announced an expansion of their services to 150 more

countries. In 2016 they increased their security measures and improved their services with a

remark of 74.8 million global subscriptions and in the next year it reached a subscription of

more than 100 million.

With the growth in their market share and improvement in their services, the market

capitalisation of the company crossed the $100 billion figure and their market price per share

surged to a high of $301.05 which was beyond their 12 months target. Therefore, the

company started with the objective of providing high quality media services initially through

the DVD sales and rental, and they changed their strategies timely with the change in

scenarios and improvement and advancement with the technologies. It paved the way for

their success and now, the Netflix can be considered as one of the global leader in

subscription based media streaming business.

3. Analysis of capital structure and dividend policy of the Netflix:

Capital structure is the combination of debt capital and equity capital in the total

capital base of the company. For use of capital, every company have to pay certain amount of

consideration, which is known as the cost of capital (Yapa 2017). An efficient capital

structure ensures the minimum overall cost of capital. Netflix is a global company and a

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

6CORPORATE FINANCE

leader in the online media streaming industry. In the year 2002 they went for public offering

of their shares for the first time and raised total capital of $82.5 million as equity share

capital. Late on in the same year they raised additional $12.38 million equity share capital

through the issue of additional 825,000 equity shares. From the 2018 annual report of the

Netflix, it can be observed that the company is having a total debt capital of 10.36 billion and

a total equity capital of $5.24 billion. Hence, they are having a highly leveraged capital

structure. It can further be observed that, they have raised debt capital of $1 billion in the year

2016, 3.02 billion in the year 2017 and again they had raised $3.96 billion of debt capital in

the year 2018, whereas, proceeds from equity financing was only $36.97 million in the year

2016, $88.38 million in the year 2017 and $124.50 million in the year

2018(In.finance.yahoo.com 2019).

In the last three years, starting from 2016 to 2018, they met their financing needs

mostly through the issue of debt capital and a very small amount was from the equity issue.

Behind such a strategic decision of increasing more leverage in the capital structure might be

driven by the objective of minimisation of the cost of capital. Therefore an analysis of the

cost of capital is important which is presented as follows (In.finance.yahoo.com 2019).

It can be observed from the 2018 annual report and market information, that the

dividend yield for the company is 0.00% for the years starting from 2014 to 2018. It means

the dividend pay-out ratio of the company is 0.00% for the last three years. Therefore,

considering 2% risk free rate and risk coefficient of the company 1.30, the cost of equity

capital can be computed using the CAPM model. The after tax cost of debt can be computed

taking the total interest expenses and the long term debt with an assumption of 30% tax rate.

Then, the weighted average cost of capital have been computed considering the book value of

the equity and the book value of the long term as the weights for the equity capital and debt

capital. Though, there is no capital yield for the last three years, the risk free rate added up

leader in the online media streaming industry. In the year 2002 they went for public offering

of their shares for the first time and raised total capital of $82.5 million as equity share

capital. Late on in the same year they raised additional $12.38 million equity share capital

through the issue of additional 825,000 equity shares. From the 2018 annual report of the

Netflix, it can be observed that the company is having a total debt capital of 10.36 billion and

a total equity capital of $5.24 billion. Hence, they are having a highly leveraged capital

structure. It can further be observed that, they have raised debt capital of $1 billion in the year

2016, 3.02 billion in the year 2017 and again they had raised $3.96 billion of debt capital in

the year 2018, whereas, proceeds from equity financing was only $36.97 million in the year

2016, $88.38 million in the year 2017 and $124.50 million in the year

2018(In.finance.yahoo.com 2019).

In the last three years, starting from 2016 to 2018, they met their financing needs

mostly through the issue of debt capital and a very small amount was from the equity issue.

Behind such a strategic decision of increasing more leverage in the capital structure might be

driven by the objective of minimisation of the cost of capital. Therefore an analysis of the

cost of capital is important which is presented as follows (In.finance.yahoo.com 2019).

It can be observed from the 2018 annual report and market information, that the

dividend yield for the company is 0.00% for the years starting from 2014 to 2018. It means

the dividend pay-out ratio of the company is 0.00% for the last three years. Therefore,

considering 2% risk free rate and risk coefficient of the company 1.30, the cost of equity

capital can be computed using the CAPM model. The after tax cost of debt can be computed

taking the total interest expenses and the long term debt with an assumption of 30% tax rate.

Then, the weighted average cost of capital have been computed considering the book value of

the equity and the book value of the long term as the weights for the equity capital and debt

capital. Though, there is no capital yield for the last three years, the risk free rate added up

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

7CORPORATE FINANCE

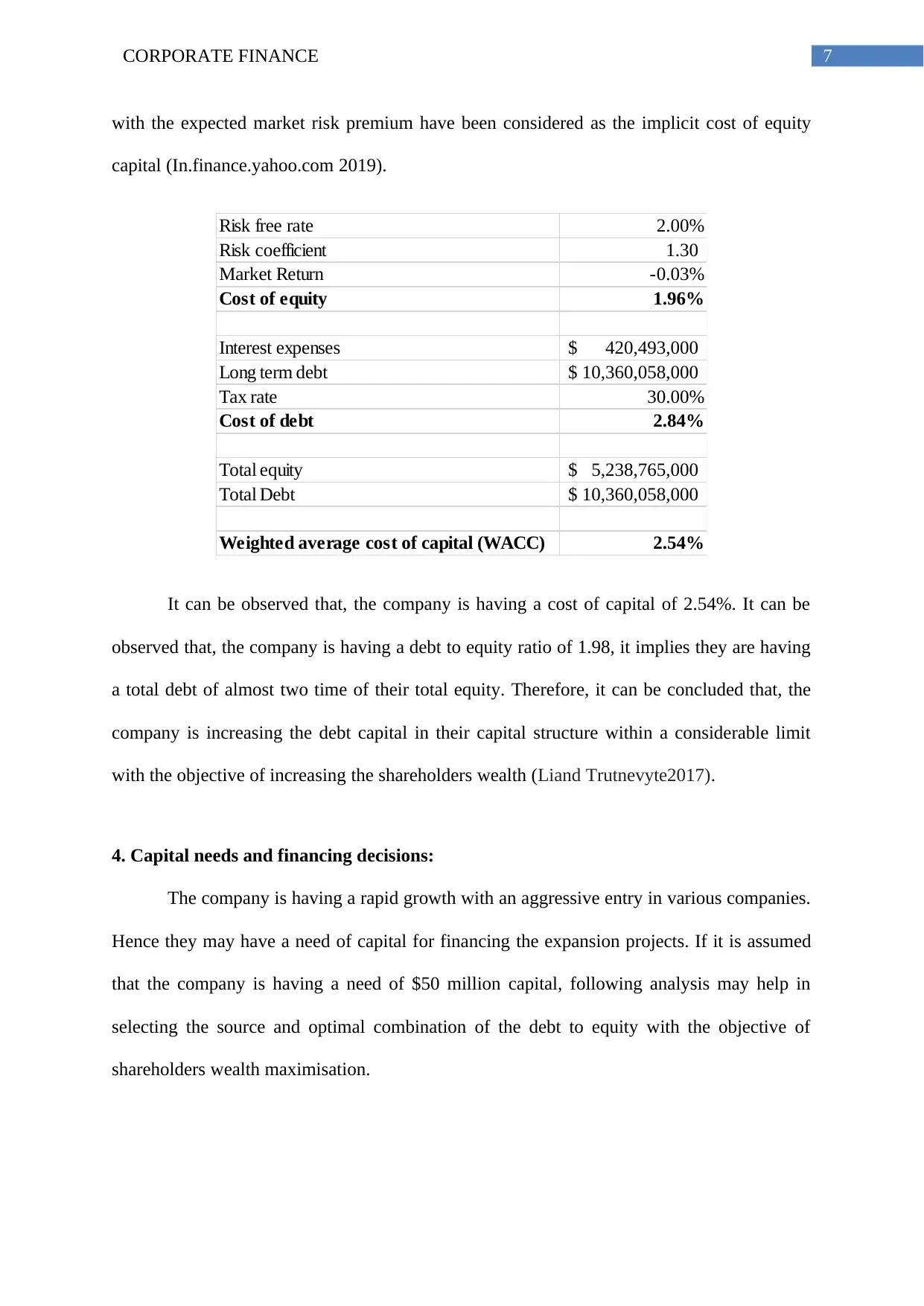

with the expected market risk premium have been considered as the implicit cost of equity

capital (In.finance.yahoo.com 2019).

Risk free rate 2.00%

Risk coefficient 1.30

Market Return -0.03%

Cost of equity 1.96%

Interest expenses 420,493,000$

Long term debt 10,360,058,000$

Tax rate 30.00%

Cost of debt 2.84%

Total equity 5,238,765,000$

Total Debt 10,360,058,000$

Weighted average cost of capital (WACC) 2.54%

It can be observed that, the company is having a cost of capital of 2.54%. It can be

observed that, the company is having a debt to equity ratio of 1.98, it implies they are having

a total debt of almost two time of their total equity. Therefore, it can be concluded that, the

company is increasing the debt capital in their capital structure within a considerable limit

with the objective of increasing the shareholders wealth (Liand Trutnevyte2017).

4. Capital needs and financing decisions:

The company is having a rapid growth with an aggressive entry in various companies.

Hence they may have a need of capital for financing the expansion projects. If it is assumed

that the company is having a need of $50 million capital, following analysis may help in

selecting the source and optimal combination of the debt to equity with the objective of

shareholders wealth maximisation.

with the expected market risk premium have been considered as the implicit cost of equity

capital (In.finance.yahoo.com 2019).

Risk free rate 2.00%

Risk coefficient 1.30

Market Return -0.03%

Cost of equity 1.96%

Interest expenses 420,493,000$

Long term debt 10,360,058,000$

Tax rate 30.00%

Cost of debt 2.84%

Total equity 5,238,765,000$

Total Debt 10,360,058,000$

Weighted average cost of capital (WACC) 2.54%

It can be observed that, the company is having a cost of capital of 2.54%. It can be

observed that, the company is having a debt to equity ratio of 1.98, it implies they are having

a total debt of almost two time of their total equity. Therefore, it can be concluded that, the

company is increasing the debt capital in their capital structure within a considerable limit

with the objective of increasing the shareholders wealth (Liand Trutnevyte2017).

4. Capital needs and financing decisions:

The company is having a rapid growth with an aggressive entry in various companies.

Hence they may have a need of capital for financing the expansion projects. If it is assumed

that the company is having a need of $50 million capital, following analysis may help in

selecting the source and optimal combination of the debt to equity with the objective of

shareholders wealth maximisation.

8CORPORATE FINANCE

1)

Source of financing Amount Weight Cost of

capital

Total Cost of

Capital

Equity Shares 50,000,000$ 100% 1.96% 978,822$

Preference Shares -$ 0% 1.96% -$

Debt Capital -$ 0% 2.84% -$

Total 50,000,000$ 100% 1.96% 978,822$

2)

Source of financing Amount Weight Cost of

capital

Total Cost of

Capital

Equity Shares -$ 0% 1.96% -$

Preference Shares 50,000,000$ 100% 1.96% 978,822$

Debt Capital -$ 0% 2.84% -$

Total 50,000,000$ 100% 1.96% 978,822$

3)

Source of financing Amount Weight Cost of

capital

Total Cost of

Capital

Equity Shares -$ 0% 1.96% -$

Preference Shares -$ 0% 1.96% -$

Debt Capital 50,000,000$ 100% 2.84% 1,420,577$

Total 50,000,000$ 100% 2.84% 1,420,577$

4)

Source of financing Amount Weight Cost of

capital

Total Cost of

Capital

Equity Shares 25,000,000$ 50% 1.96% 489,411$

Preference Shares 25,000,000$ 50% 1.96% 489,411$

Debt Capital -$ 0% 2.84% -$

Total 50,000,000$ 100% 1.96% 978,822$

5)

Source of financing Amount Weight Cost of

capital

Total Cost of

Capital

Equity Shares 25,000,000$ 50% 1.96% 489,411$

Preference Shares -$ 0% 1.96% -$

Debt Capital 25,000,000$ 50% 2.84% 710,288$

Total 50,000,000$ 100% 2.40% 1,199,699$

1)

Source of financing Amount Weight Cost of

capital

Total Cost of

Capital

Equity Shares 50,000,000$ 100% 1.96% 978,822$

Preference Shares -$ 0% 1.96% -$

Debt Capital -$ 0% 2.84% -$

Total 50,000,000$ 100% 1.96% 978,822$

2)

Source of financing Amount Weight Cost of

capital

Total Cost of

Capital

Equity Shares -$ 0% 1.96% -$

Preference Shares 50,000,000$ 100% 1.96% 978,822$

Debt Capital -$ 0% 2.84% -$

Total 50,000,000$ 100% 1.96% 978,822$

3)

Source of financing Amount Weight Cost of

capital

Total Cost of

Capital

Equity Shares -$ 0% 1.96% -$

Preference Shares -$ 0% 1.96% -$

Debt Capital 50,000,000$ 100% 2.84% 1,420,577$

Total 50,000,000$ 100% 2.84% 1,420,577$

4)

Source of financing Amount Weight Cost of

capital

Total Cost of

Capital

Equity Shares 25,000,000$ 50% 1.96% 489,411$

Preference Shares 25,000,000$ 50% 1.96% 489,411$

Debt Capital -$ 0% 2.84% -$

Total 50,000,000$ 100% 1.96% 978,822$

5)

Source of financing Amount Weight Cost of

capital

Total Cost of

Capital

Equity Shares 25,000,000$ 50% 1.96% 489,411$

Preference Shares -$ 0% 1.96% -$

Debt Capital 25,000,000$ 50% 2.84% 710,288$

Total 50,000,000$ 100% 2.40% 1,199,699$

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

9CORPORATE FINANCE

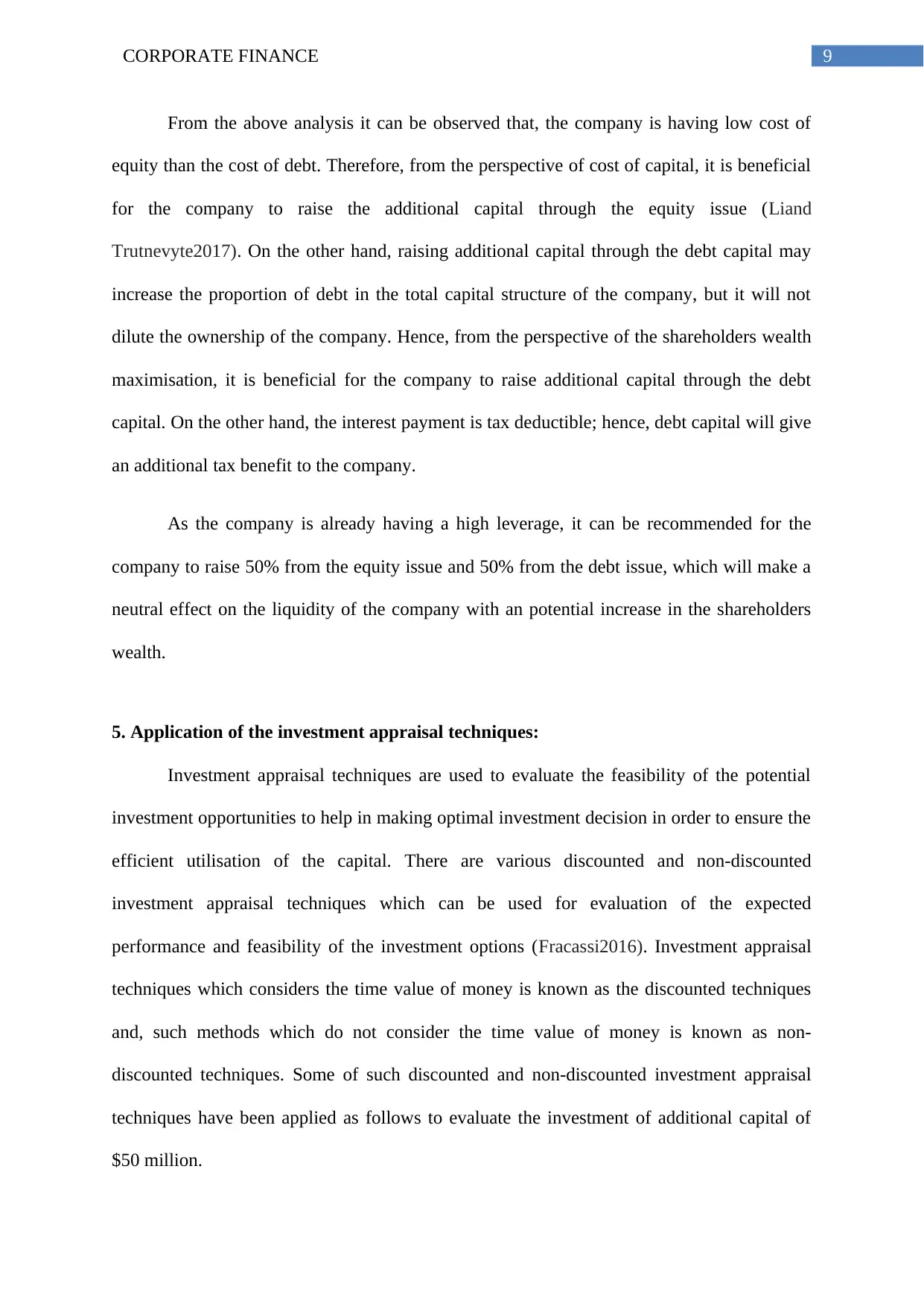

From the above analysis it can be observed that, the company is having low cost of

equity than the cost of debt. Therefore, from the perspective of cost of capital, it is beneficial

for the company to raise the additional capital through the equity issue (Liand

Trutnevyte2017). On the other hand, raising additional capital through the debt capital may

increase the proportion of debt in the total capital structure of the company, but it will not

dilute the ownership of the company. Hence, from the perspective of the shareholders wealth

maximisation, it is beneficial for the company to raise additional capital through the debt

capital. On the other hand, the interest payment is tax deductible; hence, debt capital will give

an additional tax benefit to the company.

As the company is already having a high leverage, it can be recommended for the

company to raise 50% from the equity issue and 50% from the debt issue, which will make a

neutral effect on the liquidity of the company with an potential increase in the shareholders

wealth.

5. Application of the investment appraisal techniques:

Investment appraisal techniques are used to evaluate the feasibility of the potential

investment opportunities to help in making optimal investment decision in order to ensure the

efficient utilisation of the capital. There are various discounted and non-discounted

investment appraisal techniques which can be used for evaluation of the expected

performance and feasibility of the investment options (Fracassi2016). Investment appraisal

techniques which considers the time value of money is known as the discounted techniques

and, such methods which do not consider the time value of money is known as non-

discounted techniques. Some of such discounted and non-discounted investment appraisal

techniques have been applied as follows to evaluate the investment of additional capital of

$50 million.

From the above analysis it can be observed that, the company is having low cost of

equity than the cost of debt. Therefore, from the perspective of cost of capital, it is beneficial

for the company to raise the additional capital through the equity issue (Liand

Trutnevyte2017). On the other hand, raising additional capital through the debt capital may

increase the proportion of debt in the total capital structure of the company, but it will not

dilute the ownership of the company. Hence, from the perspective of the shareholders wealth

maximisation, it is beneficial for the company to raise additional capital through the debt

capital. On the other hand, the interest payment is tax deductible; hence, debt capital will give

an additional tax benefit to the company.

As the company is already having a high leverage, it can be recommended for the

company to raise 50% from the equity issue and 50% from the debt issue, which will make a

neutral effect on the liquidity of the company with an potential increase in the shareholders

wealth.

5. Application of the investment appraisal techniques:

Investment appraisal techniques are used to evaluate the feasibility of the potential

investment opportunities to help in making optimal investment decision in order to ensure the

efficient utilisation of the capital. There are various discounted and non-discounted

investment appraisal techniques which can be used for evaluation of the expected

performance and feasibility of the investment options (Fracassi2016). Investment appraisal

techniques which considers the time value of money is known as the discounted techniques

and, such methods which do not consider the time value of money is known as non-

discounted techniques. Some of such discounted and non-discounted investment appraisal

techniques have been applied as follows to evaluate the investment of additional capital of

$50 million.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

10CORPORATE FINANCE

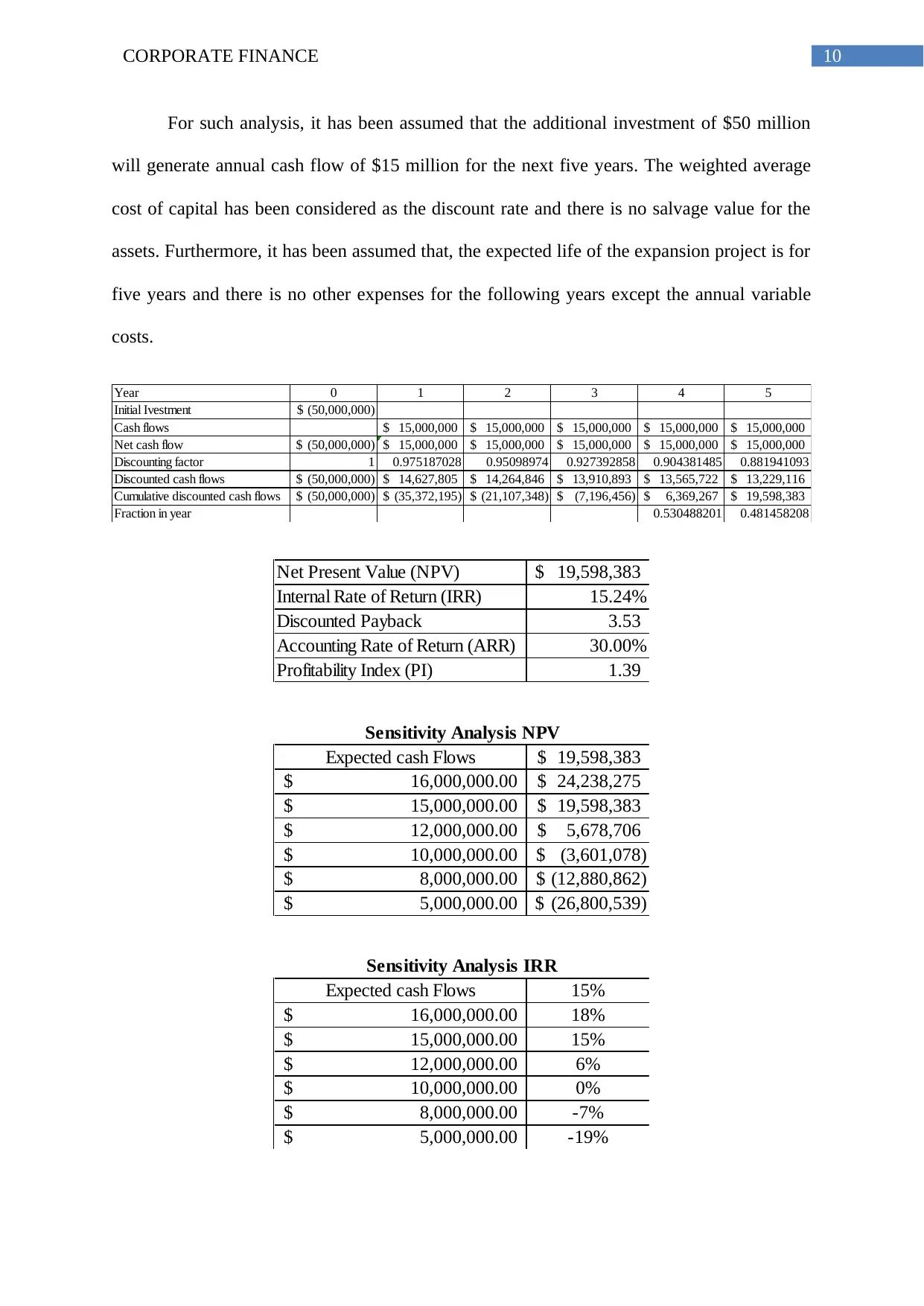

For such analysis, it has been assumed that the additional investment of $50 million

will generate annual cash flow of $15 million for the next five years. The weighted average

cost of capital has been considered as the discount rate and there is no salvage value for the

assets. Furthermore, it has been assumed that, the expected life of the expansion project is for

five years and there is no other expenses for the following years except the annual variable

costs.

Year 0 1 2 3 4 5

Initial Ivestment (50,000,000)$

Cash flows 15,000,000$ 15,000,000$ 15,000,000$ 15,000,000$ 15,000,000$

Net cash flow (50,000,000)$ 15,000,000$ 15,000,000$ 15,000,000$ 15,000,000$ 15,000,000$

Discounting factor 1 0.975187028 0.95098974 0.927392858 0.904381485 0.881941093

Discounted cash flows (50,000,000)$ 14,627,805$ 14,264,846$ 13,910,893$ 13,565,722$ 13,229,116$

Cumulative discounted cash flows (50,000,000)$ (35,372,195)$ (21,107,348)$ (7,196,456)$ 6,369,267$ 19,598,383$

Fraction in year 0.530488201 0.481458208

Net Present Value (NPV) 19,598,383$

Internal Rate of Return (IRR) 15.24%

Discounted Payback 3.53

Accounting Rate of Return (ARR) 30.00%

Profitability Index (PI) 1.39

Expected cash Flows 19,598,383$

16,000,000.00$ 24,238,275$

15,000,000.00$ 19,598,383$

12,000,000.00$ 5,678,706$

10,000,000.00$ (3,601,078)$

8,000,000.00$ (12,880,862)$

5,000,000.00$ (26,800,539)$

Sensitivity Analysis NPV

Expected cash Flows 15%

16,000,000.00$ 18%

15,000,000.00$ 15%

12,000,000.00$ 6%

10,000,000.00$ 0%

8,000,000.00$ -7%

5,000,000.00$ -19%

Sensitivity Analysis IRR

For such analysis, it has been assumed that the additional investment of $50 million

will generate annual cash flow of $15 million for the next five years. The weighted average

cost of capital has been considered as the discount rate and there is no salvage value for the

assets. Furthermore, it has been assumed that, the expected life of the expansion project is for

five years and there is no other expenses for the following years except the annual variable

costs.

Year 0 1 2 3 4 5

Initial Ivestment (50,000,000)$

Cash flows 15,000,000$ 15,000,000$ 15,000,000$ 15,000,000$ 15,000,000$

Net cash flow (50,000,000)$ 15,000,000$ 15,000,000$ 15,000,000$ 15,000,000$ 15,000,000$

Discounting factor 1 0.975187028 0.95098974 0.927392858 0.904381485 0.881941093

Discounted cash flows (50,000,000)$ 14,627,805$ 14,264,846$ 13,910,893$ 13,565,722$ 13,229,116$

Cumulative discounted cash flows (50,000,000)$ (35,372,195)$ (21,107,348)$ (7,196,456)$ 6,369,267$ 19,598,383$

Fraction in year 0.530488201 0.481458208

Net Present Value (NPV) 19,598,383$

Internal Rate of Return (IRR) 15.24%

Discounted Payback 3.53

Accounting Rate of Return (ARR) 30.00%

Profitability Index (PI) 1.39

Expected cash Flows 19,598,383$

16,000,000.00$ 24,238,275$

15,000,000.00$ 19,598,383$

12,000,000.00$ 5,678,706$

10,000,000.00$ (3,601,078)$

8,000,000.00$ (12,880,862)$

5,000,000.00$ (26,800,539)$

Sensitivity Analysis NPV

Expected cash Flows 15%

16,000,000.00$ 18%

15,000,000.00$ 15%

12,000,000.00$ 6%

10,000,000.00$ 0%

8,000,000.00$ -7%

5,000,000.00$ -19%

Sensitivity Analysis IRR

11CORPORATE FINANCE

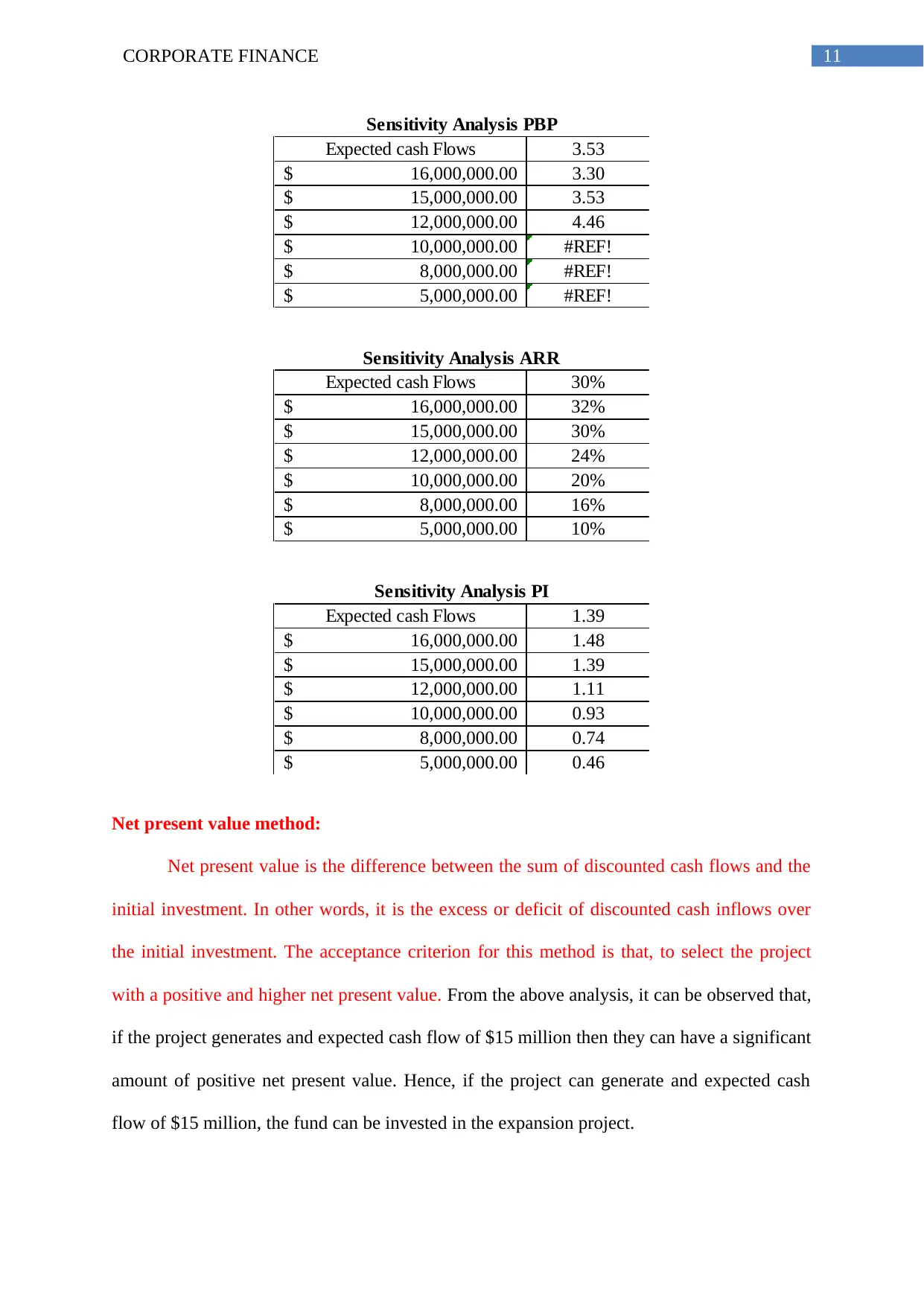

Expected cash Flows 3.53

16,000,000.00$ 3.30

15,000,000.00$ 3.53

12,000,000.00$ 4.46

10,000,000.00$ #REF!

8,000,000.00$ #REF!

5,000,000.00$ #REF!

Sensitivity Analysis PBP

Expected cash Flows 30%

16,000,000.00$ 32%

15,000,000.00$ 30%

12,000,000.00$ 24%

10,000,000.00$ 20%

8,000,000.00$ 16%

5,000,000.00$ 10%

Sensitivity Analysis ARR

Expected cash Flows 1.39

16,000,000.00$ 1.48

15,000,000.00$ 1.39

12,000,000.00$ 1.11

10,000,000.00$ 0.93

8,000,000.00$ 0.74

5,000,000.00$ 0.46

Sensitivity Analysis PI

Net present value method:

Net present value is the difference between the sum of discounted cash flows and the

initial investment. In other words, it is the excess or deficit of discounted cash inflows over

the initial investment. The acceptance criterion for this method is that, to select the project

with a positive and higher net present value. From the above analysis, it can be observed that,

if the project generates and expected cash flow of $15 million then they can have a significant

amount of positive net present value. Hence, if the project can generate and expected cash

flow of $15 million, the fund can be invested in the expansion project.

Expected cash Flows 3.53

16,000,000.00$ 3.30

15,000,000.00$ 3.53

12,000,000.00$ 4.46

10,000,000.00$ #REF!

8,000,000.00$ #REF!

5,000,000.00$ #REF!

Sensitivity Analysis PBP

Expected cash Flows 30%

16,000,000.00$ 32%

15,000,000.00$ 30%

12,000,000.00$ 24%

10,000,000.00$ 20%

8,000,000.00$ 16%

5,000,000.00$ 10%

Sensitivity Analysis ARR

Expected cash Flows 1.39

16,000,000.00$ 1.48

15,000,000.00$ 1.39

12,000,000.00$ 1.11

10,000,000.00$ 0.93

8,000,000.00$ 0.74

5,000,000.00$ 0.46

Sensitivity Analysis PI

Net present value method:

Net present value is the difference between the sum of discounted cash flows and the

initial investment. In other words, it is the excess or deficit of discounted cash inflows over

the initial investment. The acceptance criterion for this method is that, to select the project

with a positive and higher net present value. From the above analysis, it can be observed that,

if the project generates and expected cash flow of $15 million then they can have a significant

amount of positive net present value. Hence, if the project can generate and expected cash

flow of $15 million, the fund can be invested in the expansion project.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 17

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.