In-Depth Case Study: Finance for Non-Finance Managers Analysis

VerifiedAdded on 2023/06/12

|9

|2057

|86

Report

AI Summary

This assignment presents a detailed analysis of finance for non-finance managers through several case scenarios. It includes the preparation and analysis of financial statements such as the Statement of Financial Position, Cash Flow Statement, and Profit and Loss Statement. Key financial ratios like gross and net profit margins are computed and interpreted. The report provides recommendations for improving cash flow, managing profitability, and addressing potential issues in business operations. It also offers advice on taxes and financing options relevant to businesses. The case studies cover diverse aspects of financial management, offering practical insights for non-finance managers. Desklib offers a wealth of similar solved assignments and past papers to aid student learning.

Finance for Non

finance Managers

finance Managers

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Contents

Case Scenario 1 - HIEN...................................................................................................................3

a) Statement of Financial Position for the year ended 30th June 20X3........................................3

b) Give a brief discussion about the cash position of Hien and suggestions for other

information that would be valuable to Hien................................................................................3

Case Scenario 2 – WAZIR..............................................................................................................4

a) Compute the net and gross profit margin................................................................................4

b) Write a brief report..................................................................................................................4

Case Scenario 3 - MODUPE...........................................................................................................5

a) Prepare the Cash Flow statement for the year.........................................................................5

b) Write a brief report on the causes of declining cash and bank balances, as well as

recommendations for how to improve them................................................................................5

Case Scenario 4 - CAROLINE........................................................................................................6

a) Budgeted cash flow statement:................................................................................................6

b) Budgeted profit and loss statement.........................................................................................7

c) Prepare the Budgeted statement of financial position.............................................................7

d) Discuss about the issues that could be faced by Caroline’s business......................................8

Case Scenario 5 – TAWAS.............................................................................................................8

Give Tawas advice on the taxes and other banking and financing related which could be

helpful to Tawas in the corporate world......................................................................................8

REFERNCES...................................................................................................................................9

Case Scenario 1 - HIEN...................................................................................................................3

a) Statement of Financial Position for the year ended 30th June 20X3........................................3

b) Give a brief discussion about the cash position of Hien and suggestions for other

information that would be valuable to Hien................................................................................3

Case Scenario 2 – WAZIR..............................................................................................................4

a) Compute the net and gross profit margin................................................................................4

b) Write a brief report..................................................................................................................4

Case Scenario 3 - MODUPE...........................................................................................................5

a) Prepare the Cash Flow statement for the year.........................................................................5

b) Write a brief report on the causes of declining cash and bank balances, as well as

recommendations for how to improve them................................................................................5

Case Scenario 4 - CAROLINE........................................................................................................6

a) Budgeted cash flow statement:................................................................................................6

b) Budgeted profit and loss statement.........................................................................................7

c) Prepare the Budgeted statement of financial position.............................................................7

d) Discuss about the issues that could be faced by Caroline’s business......................................8

Case Scenario 5 – TAWAS.............................................................................................................8

Give Tawas advice on the taxes and other banking and financing related which could be

helpful to Tawas in the corporate world......................................................................................8

REFERNCES...................................................................................................................................9

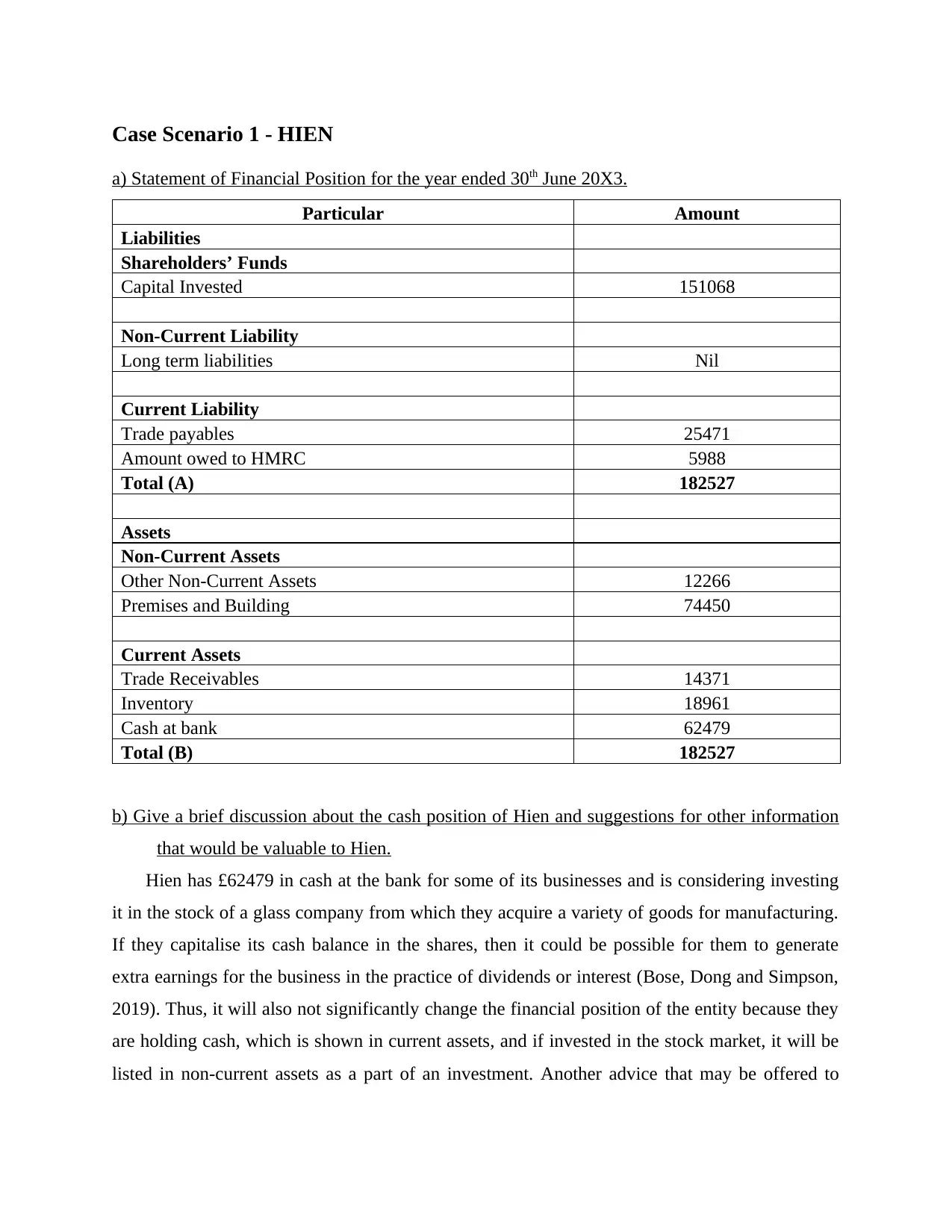

Case Scenario 1 - HIEN

a) Statement of Financial Position for the year ended 30th June 20X3.

Particular Amount

Liabilities

Shareholders’ Funds

Capital Invested 151068

Non-Current Liability

Long term liabilities Nil

Current Liability

Trade payables 25471

Amount owed to HMRC 5988

Total (A) 182527

Assets

Non-Current Assets

Other Non-Current Assets 12266

Premises and Building 74450

Current Assets

Trade Receivables 14371

Inventory 18961

Cash at bank 62479

Total (B) 182527

b) Give a brief discussion about the cash position of Hien and suggestions for other information

that would be valuable to Hien.

Hien has £62479 in cash at the bank for some of its businesses and is considering investing

it in the stock of a glass company from which they acquire a variety of goods for manufacturing.

If they capitalise its cash balance in the shares, then it could be possible for them to generate

extra earnings for the business in the practice of dividends or interest (Bose, Dong and Simpson,

2019). Thus, it will also not significantly change the financial position of the entity because they

are holding cash, which is shown in current assets, and if invested in the stock market, it will be

listed in non-current assets as a part of an investment. Another advice that may be offered to

a) Statement of Financial Position for the year ended 30th June 20X3.

Particular Amount

Liabilities

Shareholders’ Funds

Capital Invested 151068

Non-Current Liability

Long term liabilities Nil

Current Liability

Trade payables 25471

Amount owed to HMRC 5988

Total (A) 182527

Assets

Non-Current Assets

Other Non-Current Assets 12266

Premises and Building 74450

Current Assets

Trade Receivables 14371

Inventory 18961

Cash at bank 62479

Total (B) 182527

b) Give a brief discussion about the cash position of Hien and suggestions for other information

that would be valuable to Hien.

Hien has £62479 in cash at the bank for some of its businesses and is considering investing

it in the stock of a glass company from which they acquire a variety of goods for manufacturing.

If they capitalise its cash balance in the shares, then it could be possible for them to generate

extra earnings for the business in the practice of dividends or interest (Bose, Dong and Simpson,

2019). Thus, it will also not significantly change the financial position of the entity because they

are holding cash, which is shown in current assets, and if invested in the stock market, it will be

listed in non-current assets as a part of an investment. Another advice that may be offered to

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Hien is that they have spent roughly £74450 in premises and property, which can be rented out if

the firm is not fully occupied such that rental yield can support the operation.

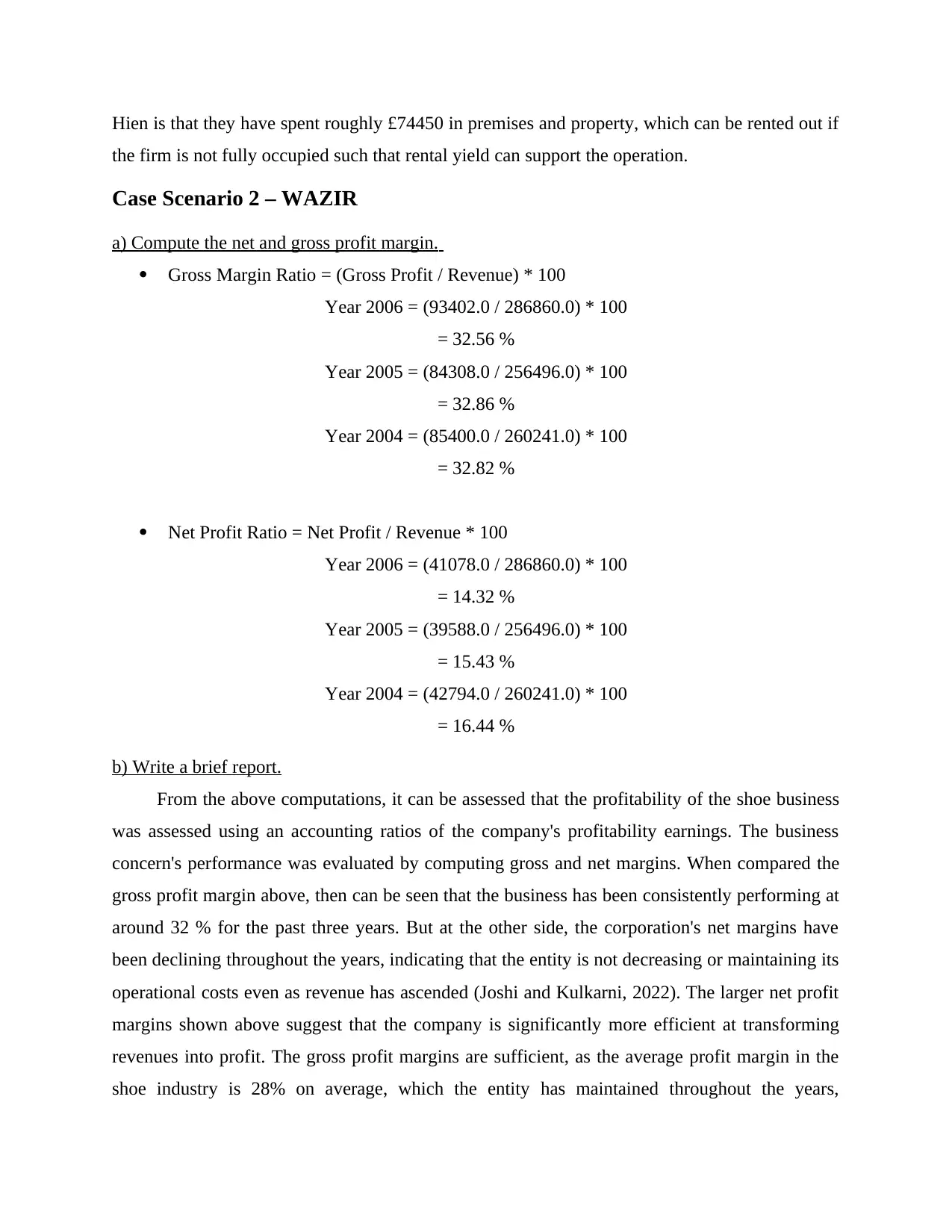

Case Scenario 2 – WAZIR

a) Compute the net and gross profit margin.

Gross Margin Ratio = (Gross Profit / Revenue) * 100

Year 2006 = (93402.0 / 286860.0) * 100

= 32.56 %

Year 2005 = (84308.0 / 256496.0) * 100

= 32.86 %

Year 2004 = (85400.0 / 260241.0) * 100

= 32.82 %

Net Profit Ratio = Net Profit / Revenue * 100

Year 2006 = (41078.0 / 286860.0) * 100

= 14.32 %

Year 2005 = (39588.0 / 256496.0) * 100

= 15.43 %

Year 2004 = (42794.0 / 260241.0) * 100

= 16.44 %

b) Write a brief report.

From the above computations, it can be assessed that the profitability of the shoe business

was assessed using an accounting ratios of the company's profitability earnings. The business

concern's performance was evaluated by computing gross and net margins. When compared the

gross profit margin above, then can be seen that the business has been consistently performing at

around 32 % for the past three years. But at the other side, the corporation's net margins have

been declining throughout the years, indicating that the entity is not decreasing or maintaining its

operational costs even as revenue has ascended (Joshi and Kulkarni, 2022). The larger net profit

margins shown above suggest that the company is significantly more efficient at transforming

revenues into profit. The gross profit margins are sufficient, as the average profit margin in the

shoe industry is 28% on average, which the entity has maintained throughout the years,

the firm is not fully occupied such that rental yield can support the operation.

Case Scenario 2 – WAZIR

a) Compute the net and gross profit margin.

Gross Margin Ratio = (Gross Profit / Revenue) * 100

Year 2006 = (93402.0 / 286860.0) * 100

= 32.56 %

Year 2005 = (84308.0 / 256496.0) * 100

= 32.86 %

Year 2004 = (85400.0 / 260241.0) * 100

= 32.82 %

Net Profit Ratio = Net Profit / Revenue * 100

Year 2006 = (41078.0 / 286860.0) * 100

= 14.32 %

Year 2005 = (39588.0 / 256496.0) * 100

= 15.43 %

Year 2004 = (42794.0 / 260241.0) * 100

= 16.44 %

b) Write a brief report.

From the above computations, it can be assessed that the profitability of the shoe business

was assessed using an accounting ratios of the company's profitability earnings. The business

concern's performance was evaluated by computing gross and net margins. When compared the

gross profit margin above, then can be seen that the business has been consistently performing at

around 32 % for the past three years. But at the other side, the corporation's net margins have

been declining throughout the years, indicating that the entity is not decreasing or maintaining its

operational costs even as revenue has ascended (Joshi and Kulkarni, 2022). The larger net profit

margins shown above suggest that the company is significantly more efficient at transforming

revenues into profit. The gross profit margins are sufficient, as the average profit margin in the

shoe industry is 28% on average, which the entity has maintained throughout the years,

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

demonstrating that the company's assets are effectively and efficiently used to contribute to the

company's profit.

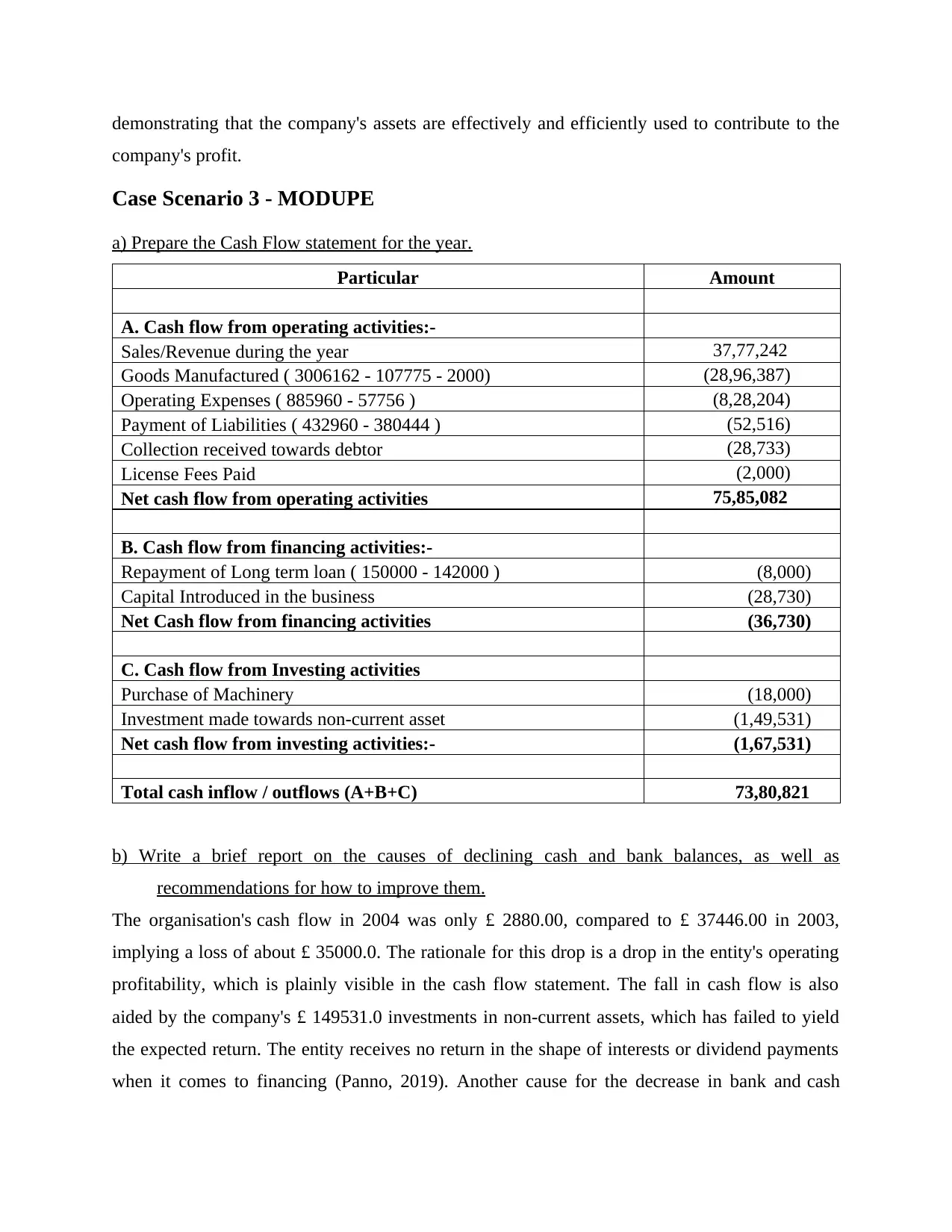

Case Scenario 3 - MODUPE

a) Prepare the Cash Flow statement for the year.

Particular Amount

A. Cash flow from operating activities:-

Sales/Revenue during the year 37,77,242

Goods Manufactured ( 3006162 - 107775 - 2000) (28,96,387)

Operating Expenses ( 885960 - 57756 ) (8,28,204)

Payment of Liabilities ( 432960 - 380444 ) (52,516)

Collection received towards debtor (28,733)

License Fees Paid (2,000)

Net cash flow from operating activities 75,85,082

B. Cash flow from financing activities:-

Repayment of Long term loan ( 150000 - 142000 ) (8,000)

Capital Introduced in the business (28,730)

Net Cash flow from financing activities (36,730)

C. Cash flow from Investing activities

Purchase of Machinery (18,000)

Investment made towards non-current asset (1,49,531)

Net cash flow from investing activities:- (1,67,531)

Total cash inflow / outflows (A+B+C) 73,80,821

b) Write a brief report on the causes of declining cash and bank balances, as well as

recommendations for how to improve them.

The organisation's cash flow in 2004 was only £ 2880.00, compared to £ 37446.00 in 2003,

implying a loss of about £ 35000.0. The rationale for this drop is a drop in the entity's operating

profitability, which is plainly visible in the cash flow statement. The fall in cash flow is also

aided by the company's £ 149531.0 investments in non-current assets, which has failed to yield

the expected return. The entity receives no return in the shape of interests or dividend payments

when it comes to financing (Panno, 2019). Another cause for the decrease in bank and cash

company's profit.

Case Scenario 3 - MODUPE

a) Prepare the Cash Flow statement for the year.

Particular Amount

A. Cash flow from operating activities:-

Sales/Revenue during the year 37,77,242

Goods Manufactured ( 3006162 - 107775 - 2000) (28,96,387)

Operating Expenses ( 885960 - 57756 ) (8,28,204)

Payment of Liabilities ( 432960 - 380444 ) (52,516)

Collection received towards debtor (28,733)

License Fees Paid (2,000)

Net cash flow from operating activities 75,85,082

B. Cash flow from financing activities:-

Repayment of Long term loan ( 150000 - 142000 ) (8,000)

Capital Introduced in the business (28,730)

Net Cash flow from financing activities (36,730)

C. Cash flow from Investing activities

Purchase of Machinery (18,000)

Investment made towards non-current asset (1,49,531)

Net cash flow from investing activities:- (1,67,531)

Total cash inflow / outflows (A+B+C) 73,80,821

b) Write a brief report on the causes of declining cash and bank balances, as well as

recommendations for how to improve them.

The organisation's cash flow in 2004 was only £ 2880.00, compared to £ 37446.00 in 2003,

implying a loss of about £ 35000.0. The rationale for this drop is a drop in the entity's operating

profitability, which is plainly visible in the cash flow statement. The fall in cash flow is also

aided by the company's £ 149531.0 investments in non-current assets, which has failed to yield

the expected return. The entity receives no return in the shape of interests or dividend payments

when it comes to financing (Panno, 2019). Another cause for the decrease in bank and cash

balances is that the corporation's operating expenses have risen over the accounting cycle,

totalling roughly £ 828204.00 in 2004 and 2005. It is vital to highlight that, in comparison to

prior years, roughly £ 56000 has already been extracted from the firm in the name of drawings,

which has impacted the organization's cash position. The recommendation that can be provided

to an entity to enhance their cash balance is that they spend their excess cash in productive

operations and in diverse funds so that the funds can earn the necessary return and be useful to

the company. Here below are some factors which could be taken into consideration for elevating

the flow of cash:

It is critical to submit bill on time such that settlements could be completed in a timely

manner, since it is evident that a significant amount of capital is engaged with in book of

accounts receivables in current assets (Patalano and Roulet, 2020).

If the company is experiencing a cash shortfall, the pricing policy should be reviewed and

re-priced, as costs may not be able to match income generated.

In order to boost cash flow, it is necessary to grow business activities by pursuing a

diversification strategy, which allows for market expansion by location or product.

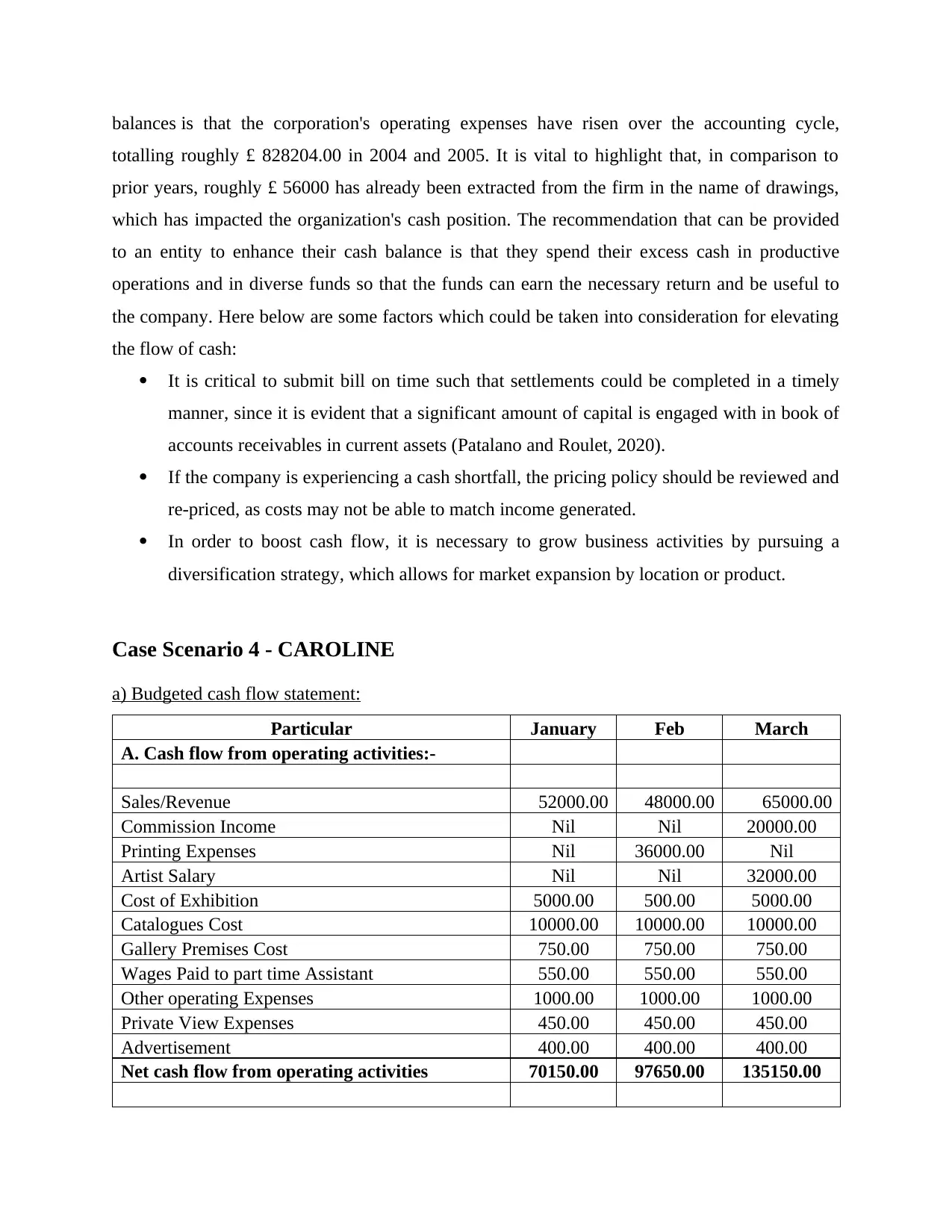

Case Scenario 4 - CAROLINE

a) Budgeted cash flow statement:

Particular January Feb March

A. Cash flow from operating activities:-

Sales/Revenue 52000.00 48000.00 65000.00

Commission Income Nil Nil 20000.00

Printing Expenses Nil 36000.00 Nil

Artist Salary Nil Nil 32000.00

Cost of Exhibition 5000.00 500.00 5000.00

Catalogues Cost 10000.00 10000.00 10000.00

Gallery Premises Cost 750.00 750.00 750.00

Wages Paid to part time Assistant 550.00 550.00 550.00

Other operating Expenses 1000.00 1000.00 1000.00

Private View Expenses 450.00 450.00 450.00

Advertisement 400.00 400.00 400.00

Net cash flow from operating activities 70150.00 97650.00 135150.00

totalling roughly £ 828204.00 in 2004 and 2005. It is vital to highlight that, in comparison to

prior years, roughly £ 56000 has already been extracted from the firm in the name of drawings,

which has impacted the organization's cash position. The recommendation that can be provided

to an entity to enhance their cash balance is that they spend their excess cash in productive

operations and in diverse funds so that the funds can earn the necessary return and be useful to

the company. Here below are some factors which could be taken into consideration for elevating

the flow of cash:

It is critical to submit bill on time such that settlements could be completed in a timely

manner, since it is evident that a significant amount of capital is engaged with in book of

accounts receivables in current assets (Patalano and Roulet, 2020).

If the company is experiencing a cash shortfall, the pricing policy should be reviewed and

re-priced, as costs may not be able to match income generated.

In order to boost cash flow, it is necessary to grow business activities by pursuing a

diversification strategy, which allows for market expansion by location or product.

Case Scenario 4 - CAROLINE

a) Budgeted cash flow statement:

Particular January Feb March

A. Cash flow from operating activities:-

Sales/Revenue 52000.00 48000.00 65000.00

Commission Income Nil Nil 20000.00

Printing Expenses Nil 36000.00 Nil

Artist Salary Nil Nil 32000.00

Cost of Exhibition 5000.00 500.00 5000.00

Catalogues Cost 10000.00 10000.00 10000.00

Gallery Premises Cost 750.00 750.00 750.00

Wages Paid to part time Assistant 550.00 550.00 550.00

Other operating Expenses 1000.00 1000.00 1000.00

Private View Expenses 450.00 450.00 450.00

Advertisement 400.00 400.00 400.00

Net cash flow from operating activities 70150.00 97650.00 135150.00

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

B. Cash flow from financing activities 0.00 0.00 0.00

Interest payments for mortgage loan 561.00 561.00 561.00

Net Cash flow from financing activities 561.00 561.00 561.00

C. Cash flow from Investing activities

Initial investment made 0.00 0.00 0.00

Net cash flow from investing activities 0.00 0.00 0.00

Total cash inflow / outflows (A+B+C) 70711.00 98211.00 135711.00

b) Budgeted profit and loss statement

Particulars January February March

Revenue 52000.00 48000.00 65000.00

Commission Income Nil Nil 20000.00

GROSS PROFIT 52000.00 48000.00 85000.00

Operating Expenses

Printing Expenses Nil 36000.00 Nil

Artist Salary Nil Nil 32000.00

Cost of Exhibition 5000.00 5000.00 5000.00

Cost of Catalogues 10000.00 10000.00 10000.00

Gallery Premises Cost 750.00 750.00 750.00

Electricity Cost 60.00 60.00 60.00

Wages paid to part time assistant 550.00 550.00 550.00

Other Expenses 1000.00 1000.00 1000.00

Private view Expenses 450.00 450.00 450.00

Advertisement 400.00 400.00 400.00

TOTAL EXPENSES £ 18210.00 54210.00 50210.00

Net Profit (Loss) 33790.00 -6210.00 34790.00

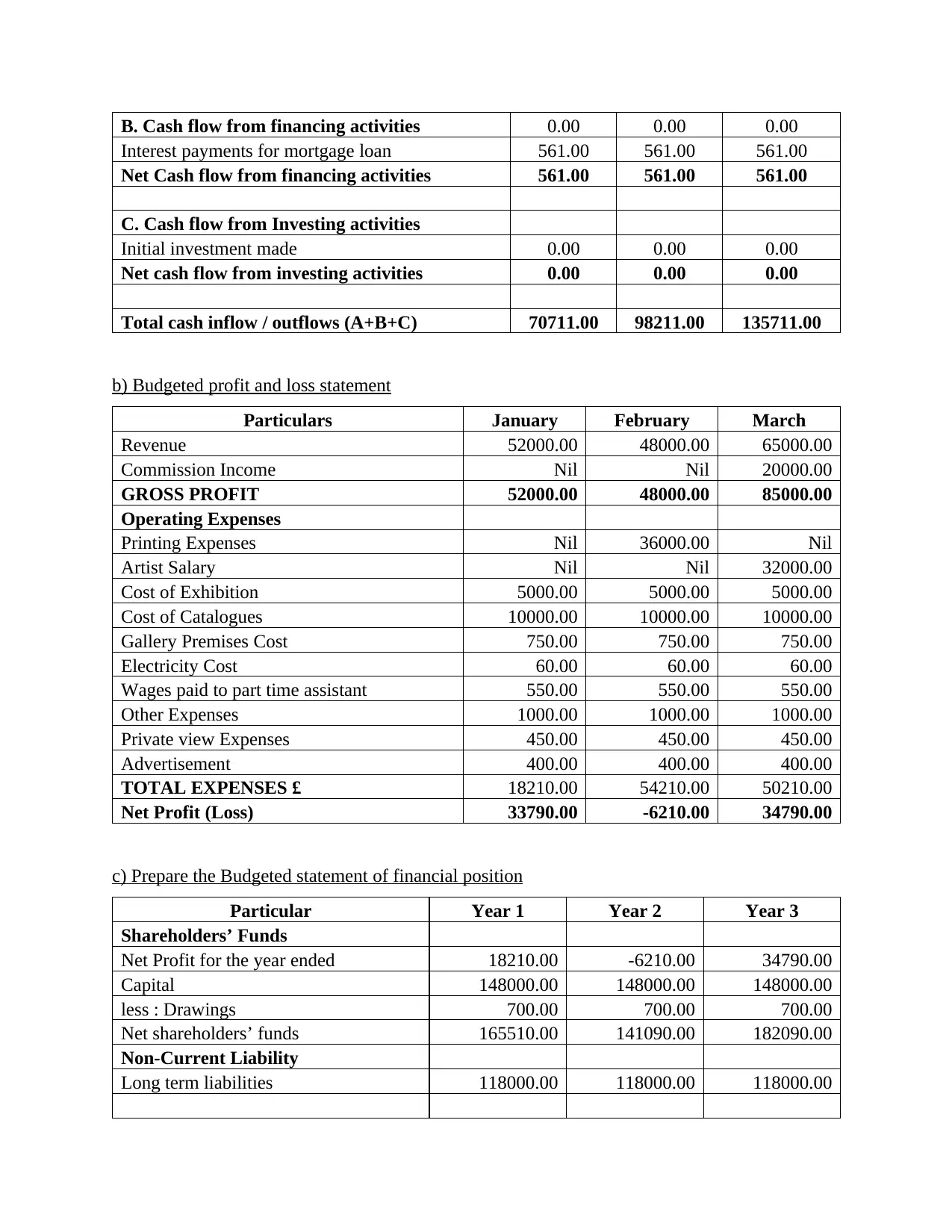

c) Prepare the Budgeted statement of financial position

Particular Year 1 Year 2 Year 3

Shareholders’ Funds

Net Profit for the year ended 18210.00 -6210.00 34790.00

Capital 148000.00 148000.00 148000.00

less : Drawings 700.00 700.00 700.00

Net shareholders’ funds 165510.00 141090.00 182090.00

Non-Current Liability

Long term liabilities 118000.00 118000.00 118000.00

Interest payments for mortgage loan 561.00 561.00 561.00

Net Cash flow from financing activities 561.00 561.00 561.00

C. Cash flow from Investing activities

Initial investment made 0.00 0.00 0.00

Net cash flow from investing activities 0.00 0.00 0.00

Total cash inflow / outflows (A+B+C) 70711.00 98211.00 135711.00

b) Budgeted profit and loss statement

Particulars January February March

Revenue 52000.00 48000.00 65000.00

Commission Income Nil Nil 20000.00

GROSS PROFIT 52000.00 48000.00 85000.00

Operating Expenses

Printing Expenses Nil 36000.00 Nil

Artist Salary Nil Nil 32000.00

Cost of Exhibition 5000.00 5000.00 5000.00

Cost of Catalogues 10000.00 10000.00 10000.00

Gallery Premises Cost 750.00 750.00 750.00

Electricity Cost 60.00 60.00 60.00

Wages paid to part time assistant 550.00 550.00 550.00

Other Expenses 1000.00 1000.00 1000.00

Private view Expenses 450.00 450.00 450.00

Advertisement 400.00 400.00 400.00

TOTAL EXPENSES £ 18210.00 54210.00 50210.00

Net Profit (Loss) 33790.00 -6210.00 34790.00

c) Prepare the Budgeted statement of financial position

Particular Year 1 Year 2 Year 3

Shareholders’ Funds

Net Profit for the year ended 18210.00 -6210.00 34790.00

Capital 148000.00 148000.00 148000.00

less : Drawings 700.00 700.00 700.00

Net shareholders’ funds 165510.00 141090.00 182090.00

Non-Current Liability

Long term liabilities 118000.00 118000.00 118000.00

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Current Liability

Total (A) 283510.00 259090.00 300090.00

Non- Current Assets

Other Non - Current Assets 281510.00 257090.00 298090.00

Current Assets

Inventory Nil Nil Nil

Cash and Cash Equivalent 2000.00 2000.00 2000.00

Total (B) 283510.00 259090.00 300090.00

d) Discuss about the issues that could be faced by Caroline’s business.

Cash flow issues in the following areas

When the profits and losses are minimal (Ragas and Culp, 2021).

In comparison to capacity, there has been an excess of investment made.

When the goods are over stocked.

The customer has been given far too much credit.

Demand for goods and services on a regular basis.

Case Scenario 5 – TAWAS

Give Tawas advice on the taxes and other banking and financing related which could be helpful

to Tawas in the corporate world.

The new beginning of an IT consulting firm may be required to pay corporate tax and

VAT, which every business must pay in order to provide services. Tawas should seek the

assistance of a competent tax professional with extensive knowledge in this subject. The line of

credit that Tawas will take to invest capital in the business at an interest rate that will be

disclosed to the company's management (Ramlall, 2018).

Total (A) 283510.00 259090.00 300090.00

Non- Current Assets

Other Non - Current Assets 281510.00 257090.00 298090.00

Current Assets

Inventory Nil Nil Nil

Cash and Cash Equivalent 2000.00 2000.00 2000.00

Total (B) 283510.00 259090.00 300090.00

d) Discuss about the issues that could be faced by Caroline’s business.

Cash flow issues in the following areas

When the profits and losses are minimal (Ragas and Culp, 2021).

In comparison to capacity, there has been an excess of investment made.

When the goods are over stocked.

The customer has been given far too much credit.

Demand for goods and services on a regular basis.

Case Scenario 5 – TAWAS

Give Tawas advice on the taxes and other banking and financing related which could be helpful

to Tawas in the corporate world.

The new beginning of an IT consulting firm may be required to pay corporate tax and

VAT, which every business must pay in order to provide services. Tawas should seek the

assistance of a competent tax professional with extensive knowledge in this subject. The line of

credit that Tawas will take to invest capital in the business at an interest rate that will be

disclosed to the company's management (Ramlall, 2018).

REFERNCES

Books and Journals

Bose, S., Dong, G. and Simpson, A., 2019. Accounting for Sustainability: Frameworks for the

Aggregation of Financial and Non-financial Metrics. In The Financial Ecosystem (pp. 83-

109). Palgrave Macmillan, Cham.

Joshi, V.C. and Kulkarni, L., 2022. State of the Financial System: Strengths and Weaknesses.

In The Future of Indian Banking (pp. 11-23). Palgrave Macmillan, Singapore.

Panno, A., 2019. Performance measurement and management in small companies of the service

sector; evidence from a sample of Italian hotels. Measuring business excellence.

Patalano, R. and Roulet, C., 2020. Structural developments in global financial intermediation:

The rise of debt and non-bank credit intermediation.

Ragas, M.W. and Culp, R., 2021. Financial Statements and Valuation Essentials. In Business

Acumen for Strategic Communicators: A Primer. Emerald Publishing Limited.

Ramlall, I., 2018. Ratios/Metrics of Financial Stability Assessment. In Tools and Techniques for

Financial Stability Analysis. Emerald Publishing Limited.

Books and Journals

Bose, S., Dong, G. and Simpson, A., 2019. Accounting for Sustainability: Frameworks for the

Aggregation of Financial and Non-financial Metrics. In The Financial Ecosystem (pp. 83-

109). Palgrave Macmillan, Cham.

Joshi, V.C. and Kulkarni, L., 2022. State of the Financial System: Strengths and Weaknesses.

In The Future of Indian Banking (pp. 11-23). Palgrave Macmillan, Singapore.

Panno, A., 2019. Performance measurement and management in small companies of the service

sector; evidence from a sample of Italian hotels. Measuring business excellence.

Patalano, R. and Roulet, C., 2020. Structural developments in global financial intermediation:

The rise of debt and non-bank credit intermediation.

Ragas, M.W. and Culp, R., 2021. Financial Statements and Valuation Essentials. In Business

Acumen for Strategic Communicators: A Primer. Emerald Publishing Limited.

Ramlall, I., 2018. Ratios/Metrics of Financial Stability Assessment. In Tools and Techniques for

Financial Stability Analysis. Emerald Publishing Limited.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 9

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.