Analysis of Operations and Finance: A Report on Cucumber Ltd (ACC4029)

VerifiedAdded on 2023/01/11

|18

|3391

|42

Report

AI Summary

This report, focusing on Cucumber Ltd, a smartphone manufacturer, delves into various aspects of financial and operational management. It begins by defining management accounting and contrasting it with financial accounting, exploring different costing models like absorption costing, marginal costing, breakeven analysis, and activity-based costing. The report then applies investment appraisal techniques, including Accounting Rate of Return (ARR), Payback Period, Net Present Value (NPV), and Internal Rate of Return (IRR), to evaluate potential investment proposals, recommending the most financially viable options for the company. Furthermore, the report discusses the role of budgeting in operational management, analyzing variances in Cucumber Ltd's budget and proposing a flexible budgeting approach for improved accuracy. Finally, it examines the usefulness of the balanced scorecard, potentially creating a balanced scorecard for Cucumber Ltd to assess its performance across various dimensions. The analysis provides insights into financial planning, investment decisions, and performance evaluation within the context of a real-world case study.

Running head: MANAGE OPERATIONS AND FINANCE

Manage Operations and Finance

Name of the Student:

Name of the University:

Author’s Note

Manage Operations and Finance

Name of the Student:

Name of the University:

Author’s Note

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

1

MANAGE OPERATIONS AND FINANCE

Table of Contents

Role of Management Accounting in Business..........................................................................2

Difference between Management and Financial Accounting...................................................3

Different Models of Costing which is used in Operational Management.................................4

Application of Investment Appraisal Techniques.....................................................................5

Budgeting process and its Role in Business............................................................................10

Usefulness of Balanced Scorecard......................................................................................13

Balanced Scorecard of Cucumber Ltd.....................................................................................14

Reference.................................................................................................................................16

MANAGE OPERATIONS AND FINANCE

Table of Contents

Role of Management Accounting in Business..........................................................................2

Difference between Management and Financial Accounting...................................................3

Different Models of Costing which is used in Operational Management.................................4

Application of Investment Appraisal Techniques.....................................................................5

Budgeting process and its Role in Business............................................................................10

Usefulness of Balanced Scorecard......................................................................................13

Balanced Scorecard of Cucumber Ltd.....................................................................................14

Reference.................................................................................................................................16

2

MANAGE OPERATIONS AND FINANCE

Role of Management Accounting in Business

Management accounting may be defined as the process by which the top-level

management of a company takes appropriate decisions regarding the operations of the business.

In other words, management accounting process is used by top level managers of a business for

the purpose of analyzing, planning, identifying key financial information on the basis of which

the management of the company would be taking major decisions for the business (Sunarni

2013).

Management accounting system in today’s world is significant as many organization has

different set of goals and objectives which can be effectively considered with the help of

management accounting tools. Management accounting tools effectively help in the planning

process and also allocation of resources of the business in order to generate maximum results

from the same (Hilton and Platt 2013). The main objective of management accounting system is

to achieve the strategic goals of the business which would in turn help the business to achieve the

desired profits and also meet the quality which is expected by the customers of the business

(Fullerton, Kennedy and Widener 2014). Therefore, it can be said that management accounting

process provides the means to the management of the company for taking major decisions of the

business.

Difference between Management and Financial Accounting

Basis of Comparisons Financial Accounting Management Accounting

Definition Financial accounting may be

described as the process

which is used for classifying

and presenting financial

Management accounting

provides relevant information

to the top-level management

of a company so that major

MANAGE OPERATIONS AND FINANCE

Role of Management Accounting in Business

Management accounting may be defined as the process by which the top-level

management of a company takes appropriate decisions regarding the operations of the business.

In other words, management accounting process is used by top level managers of a business for

the purpose of analyzing, planning, identifying key financial information on the basis of which

the management of the company would be taking major decisions for the business (Sunarni

2013).

Management accounting system in today’s world is significant as many organization has

different set of goals and objectives which can be effectively considered with the help of

management accounting tools. Management accounting tools effectively help in the planning

process and also allocation of resources of the business in order to generate maximum results

from the same (Hilton and Platt 2013). The main objective of management accounting system is

to achieve the strategic goals of the business which would in turn help the business to achieve the

desired profits and also meet the quality which is expected by the customers of the business

(Fullerton, Kennedy and Widener 2014). Therefore, it can be said that management accounting

process provides the means to the management of the company for taking major decisions of the

business.

Difference between Management and Financial Accounting

Basis of Comparisons Financial Accounting Management Accounting

Definition Financial accounting may be

described as the process

which is used for classifying

and presenting financial

Management accounting

provides relevant information

to the top-level management

of a company so that major

You're viewing a preview

Unlock full access by subscribing today!

3

MANAGE OPERATIONS AND FINANCE

information in the financial

statements which is prepared

by the business (Francis,

Hasan and Wu 2013).

decisions can be taken by the

management of the company

regarding the operations of

the business.

Need The financial accounting

process is considered to be

compulsory and it is

mandatory for the

management to use the same

for preparing the financial

statements of the business

(Henderson et al. 2015).

Management accounting

process is used for collecting

information regarding the

business and on the basis of

the same important decisions

are taken by the management

of the company.

Nature of Information Monetary Information is

collected

Non-Monetary Information

and Monetary information are

also collected.

Time Frame The financial reports are

prepared at the end of each

financial year

Management reports are

prepared by the business

whenever the management

feels the need to prepare the

same.

Regulated Financial reports of a

business are highly regulated

Management reports of a

business are not regulated and

are used by internal

MANAGE OPERATIONS AND FINANCE

information in the financial

statements which is prepared

by the business (Francis,

Hasan and Wu 2013).

decisions can be taken by the

management of the company

regarding the operations of

the business.

Need The financial accounting

process is considered to be

compulsory and it is

mandatory for the

management to use the same

for preparing the financial

statements of the business

(Henderson et al. 2015).

Management accounting

process is used for collecting

information regarding the

business and on the basis of

the same important decisions

are taken by the management

of the company.

Nature of Information Monetary Information is

collected

Non-Monetary Information

and Monetary information are

also collected.

Time Frame The financial reports are

prepared at the end of each

financial year

Management reports are

prepared by the business

whenever the management

feels the need to prepare the

same.

Regulated Financial reports of a

business are highly regulated

Management reports of a

business are not regulated and

are used by internal

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

4

MANAGE OPERATIONS AND FINANCE

management of the company.

Different Models of Costing which is used in Operational Management

There are different models of costing available to the management of the company for

appropriate measuring the costs of the business (Warren, Reeve and Duchac 2013). In order to

effectively measure the costs of the business different costing techniques are applied by the

management of the company and some of the same are discussed below in details:

Absorption costing: As per this costing technique all costs of the business from

manufacturing would be assigned to the units which is produced by the business.

Absorption costing effectively allows a business to prepare financial reporting and income

tax reporting.

Marginal Costing: Marginal Costing is a technique which is used by the management of a

company for identifying the marginal costs of the business and charging the same to the

units which is produced while at the same time not considering the fixed costs of the

business (Macuda, Matuszak and Różańska 2015).

Breakeven Analysis: This is another technique which is used for identifying the sales figure

which the business needs to achieve for effectively for meeting the costs of the business in

such a manner that there is no profit, no loss situation in the business. The formula which is

used for computing the breakeven units is

B reakeven Point (units )=Total ¿ costs ¿

Contribution per unit

MANAGE OPERATIONS AND FINANCE

management of the company.

Different Models of Costing which is used in Operational Management

There are different models of costing available to the management of the company for

appropriate measuring the costs of the business (Warren, Reeve and Duchac 2013). In order to

effectively measure the costs of the business different costing techniques are applied by the

management of the company and some of the same are discussed below in details:

Absorption costing: As per this costing technique all costs of the business from

manufacturing would be assigned to the units which is produced by the business.

Absorption costing effectively allows a business to prepare financial reporting and income

tax reporting.

Marginal Costing: Marginal Costing is a technique which is used by the management of a

company for identifying the marginal costs of the business and charging the same to the

units which is produced while at the same time not considering the fixed costs of the

business (Macuda, Matuszak and Różańska 2015).

Breakeven Analysis: This is another technique which is used for identifying the sales figure

which the business needs to achieve for effectively for meeting the costs of the business in

such a manner that there is no profit, no loss situation in the business. The formula which is

used for computing the breakeven units is

B reakeven Point (units )=Total ¿ costs ¿

Contribution per unit

5

MANAGE OPERATIONS AND FINANCE

Activity Based Costing: This is a costing technique which effectively identifies the costs

and effectively assigns the costs to overhead activities and then the same is allocated to the

product which is produced by the business.

Application of Investment Appraisal Techniques

Investment appraisal techniques are used by the management of a company in order

identify the worth of the project which is being considered by the management of a company.

The company which is considered for the application of Investment appraisal techniques is

cucumber ltd which is engaged in the business producing smart phones. The management of the

company wants to improve the financial position of the business and thereby also enhance the

efficiency of the business (Hodder, Hopkins and Schipper 2014). Some of the important

investment appraisal techniques which is followed by the Accounting rate of return, Net Present

Value (NPV), Payback period and internal rate of return.

As per the management of the company, there are four options available to the

management of the company for making improvement in the business structure. In order to

assess the various proposals which is available to the management would be assessed by

applying investment proposal techniques.

Accounting Rate of Return

MANAGE OPERATIONS AND FINANCE

Activity Based Costing: This is a costing technique which effectively identifies the costs

and effectively assigns the costs to overhead activities and then the same is allocated to the

product which is produced by the business.

Application of Investment Appraisal Techniques

Investment appraisal techniques are used by the management of a company in order

identify the worth of the project which is being considered by the management of a company.

The company which is considered for the application of Investment appraisal techniques is

cucumber ltd which is engaged in the business producing smart phones. The management of the

company wants to improve the financial position of the business and thereby also enhance the

efficiency of the business (Hodder, Hopkins and Schipper 2014). Some of the important

investment appraisal techniques which is followed by the Accounting rate of return, Net Present

Value (NPV), Payback period and internal rate of return.

As per the management of the company, there are four options available to the

management of the company for making improvement in the business structure. In order to

assess the various proposals which is available to the management would be assessed by

applying investment proposal techniques.

Accounting Rate of Return

You're viewing a preview

Unlock full access by subscribing today!

6

MANAGE OPERATIONS AND FINANCE

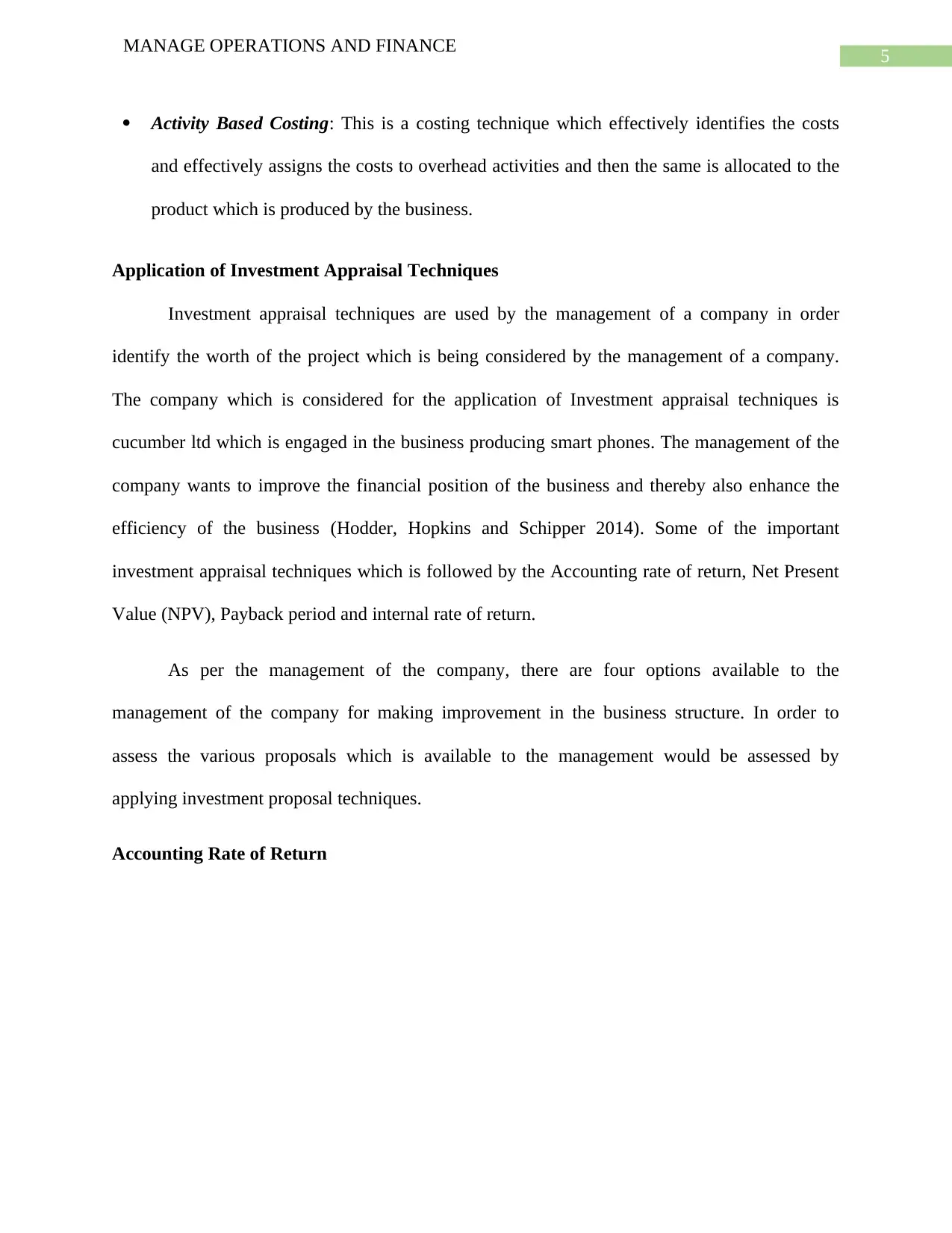

Figure 1: Accounting Rate of Return

Source: (Created by the Author)

The ARR is the rate of return which is expected out of an asset or an investment in

comparisons to the initial investment costs. The ARR of an investment considers the return

which effectively over the lifetime of the investments of the business (Coleman et al. 2013). The

ARR of proposal 2 is shown to be most appropriate from the point of view of the business.

Payback Period

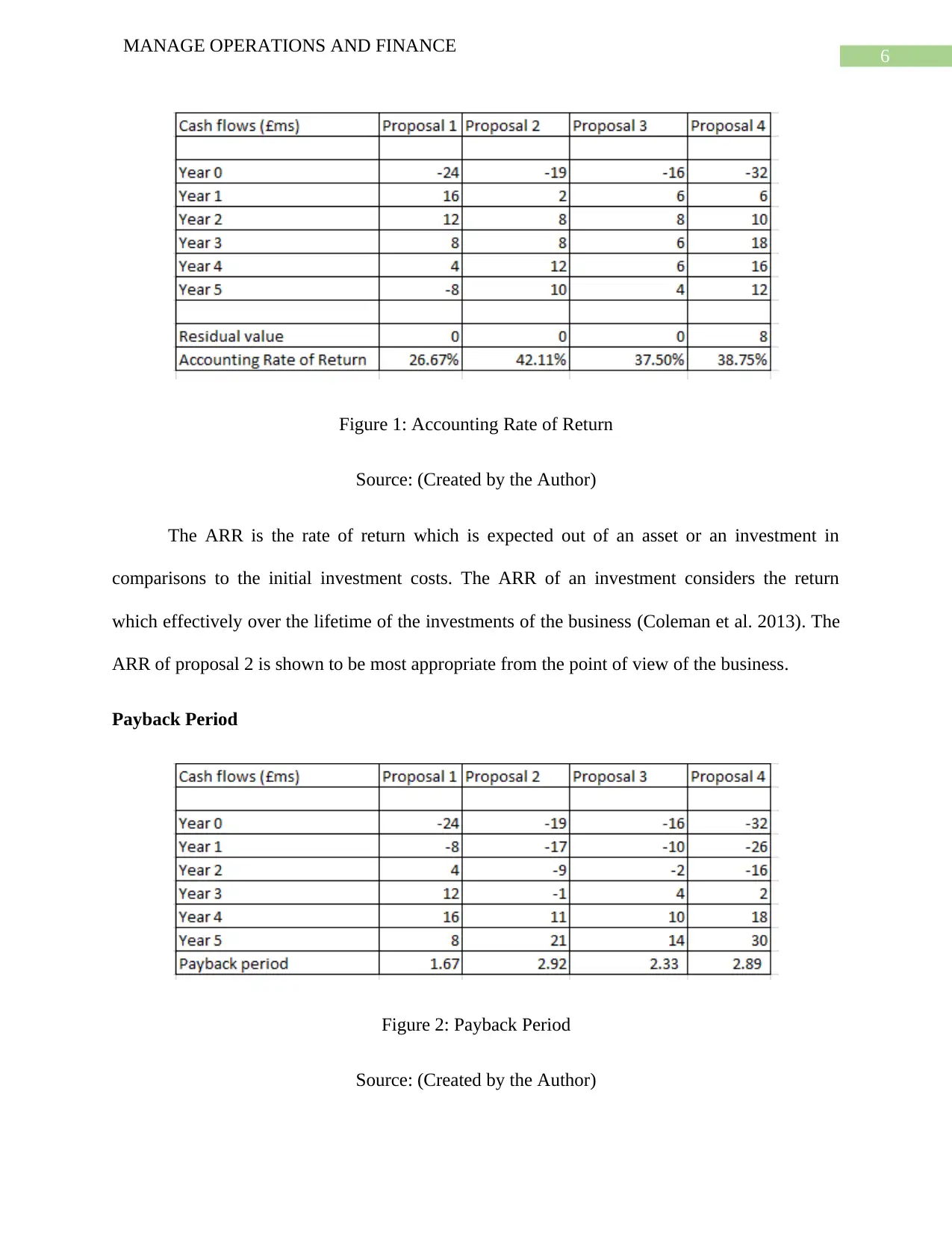

Figure 2: Payback Period

Source: (Created by the Author)

MANAGE OPERATIONS AND FINANCE

Figure 1: Accounting Rate of Return

Source: (Created by the Author)

The ARR is the rate of return which is expected out of an asset or an investment in

comparisons to the initial investment costs. The ARR of an investment considers the return

which effectively over the lifetime of the investments of the business (Coleman et al. 2013). The

ARR of proposal 2 is shown to be most appropriate from the point of view of the business.

Payback Period

Figure 2: Payback Period

Source: (Created by the Author)

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

7

MANAGE OPERATIONS AND FINANCE

Payback period is another investment appraisal technique which is used to determine the

time period which would be taken by the investment to cover up the initial cash outflows of the

business (Harris 2017). As per the figure which is shown above, the most appropriate payback

period is for proposal 1 which shows that it would take around 1.67 years to cover up the

outflows of the business.

Net Present Value (NPV)

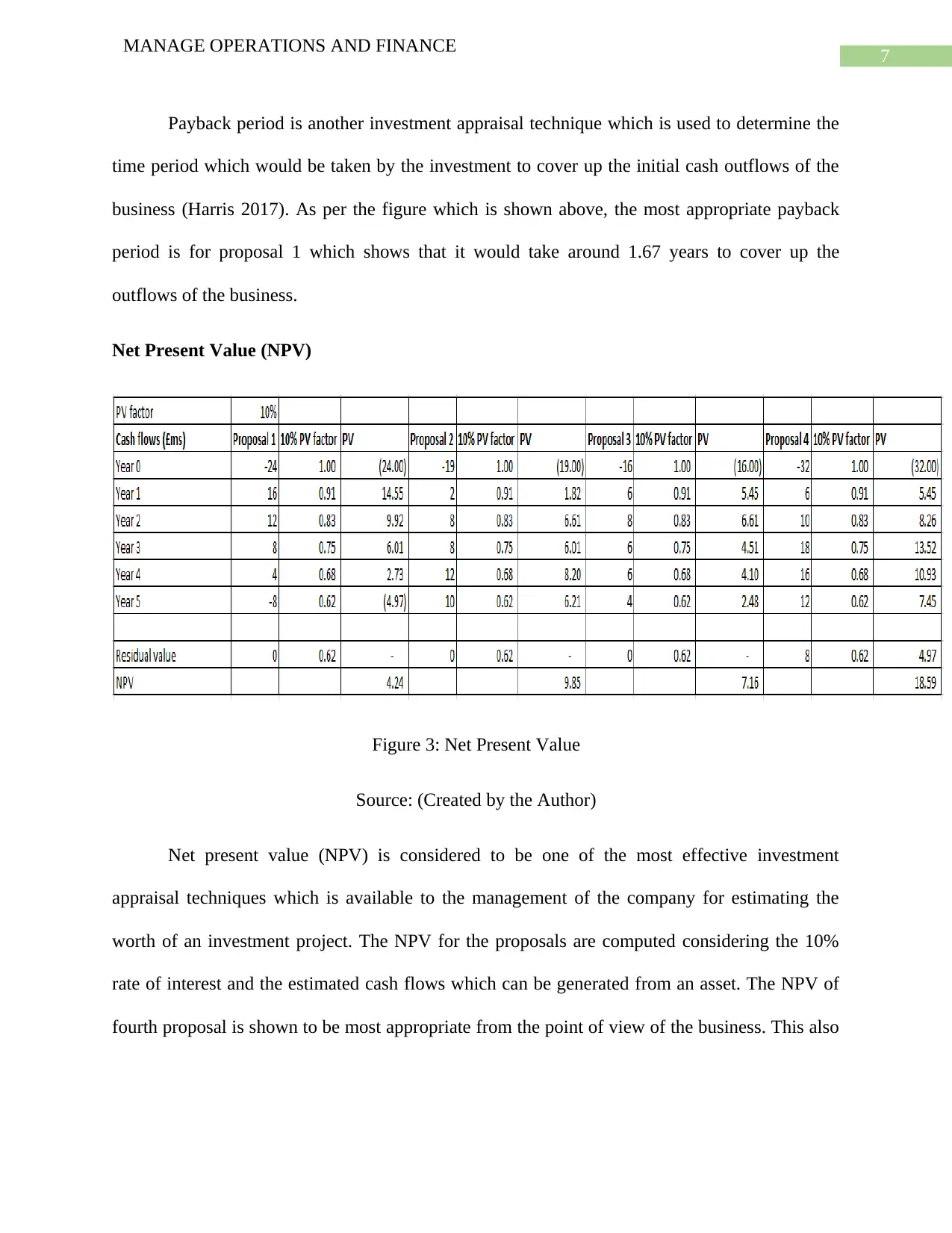

Figure 3: Net Present Value

Source: (Created by the Author)

Net present value (NPV) is considered to be one of the most effective investment

appraisal techniques which is available to the management of the company for estimating the

worth of an investment project. The NPV for the proposals are computed considering the 10%

rate of interest and the estimated cash flows which can be generated from an asset. The NPV of

fourth proposal is shown to be most appropriate from the point of view of the business. This also

MANAGE OPERATIONS AND FINANCE

Payback period is another investment appraisal technique which is used to determine the

time period which would be taken by the investment to cover up the initial cash outflows of the

business (Harris 2017). As per the figure which is shown above, the most appropriate payback

period is for proposal 1 which shows that it would take around 1.67 years to cover up the

outflows of the business.

Net Present Value (NPV)

Figure 3: Net Present Value

Source: (Created by the Author)

Net present value (NPV) is considered to be one of the most effective investment

appraisal techniques which is available to the management of the company for estimating the

worth of an investment project. The NPV for the proposals are computed considering the 10%

rate of interest and the estimated cash flows which can be generated from an asset. The NPV of

fourth proposal is shown to be most appropriate from the point of view of the business. This also

8

MANAGE OPERATIONS AND FINANCE

indicates that the management of Cucumber ltd can expect effective cash inflows if proposal 4 is

selected by the management of the company.

Internal Rate of Return

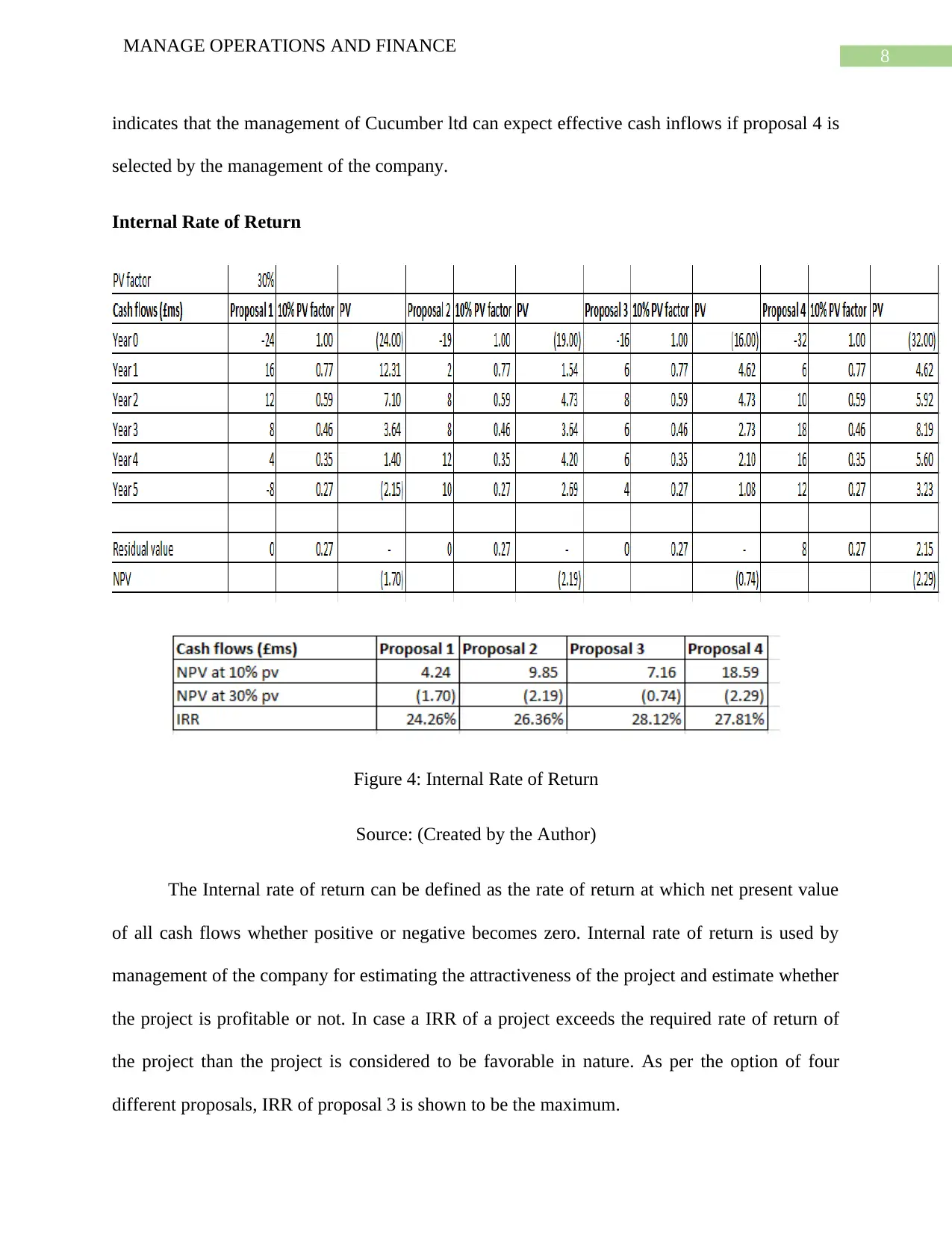

Figure 4: Internal Rate of Return

Source: (Created by the Author)

The Internal rate of return can be defined as the rate of return at which net present value

of all cash flows whether positive or negative becomes zero. Internal rate of return is used by

management of the company for estimating the attractiveness of the project and estimate whether

the project is profitable or not. In case a IRR of a project exceeds the required rate of return of

the project than the project is considered to be favorable in nature. As per the option of four

different proposals, IRR of proposal 3 is shown to be the maximum.

MANAGE OPERATIONS AND FINANCE

indicates that the management of Cucumber ltd can expect effective cash inflows if proposal 4 is

selected by the management of the company.

Internal Rate of Return

Figure 4: Internal Rate of Return

Source: (Created by the Author)

The Internal rate of return can be defined as the rate of return at which net present value

of all cash flows whether positive or negative becomes zero. Internal rate of return is used by

management of the company for estimating the attractiveness of the project and estimate whether

the project is profitable or not. In case a IRR of a project exceeds the required rate of return of

the project than the project is considered to be favorable in nature. As per the option of four

different proposals, IRR of proposal 3 is shown to be the maximum.

You're viewing a preview

Unlock full access by subscribing today!

9

MANAGE OPERATIONS AND FINANCE

Analysis of Results

On the basis of application of different investment appraisal techniques decisions need to

be taken by the management of the company as to which proposal is most suitable for the

business. The payback period results show that proposal 1 has the lowest time frame for recover

the outflows of the business and the same is shown to be 1.67 years. On the other hand, the IRR

of the business which is considered to be a better option than payback period reveals that

proposal 3 is most appropriate as the same has the highest return in the business. In addition to

this, analysis of the estimates which are present for NPV analysis shows that proposal 4 is most

appropriate and would definitely generate more cash inflows for the business in comparisons to

other options which is available to the management of the company. In addition to this, NPV

results are considered to be the most reliable investment appraisal process and therefore on the

basis of the NPV results, the management should proceed with proposal 4. This is considered to

be the most viable option available to the management of the company as per the investment

appraisal techniques which is applied.

Budgeting process and its Role in Business

Budgets can be defined as a tool which is available to the management of the company

for planning, forecasting and controlling the activities of the business (Jones et al. 2013). In a

business, the management prepares different kinds of budgets relating to different area of

performance of the business. The reasons due to which budgeting process is required in a

business are provided below:

Budgets are prepared by the management of the company for planning and forecasting the

activities of the business.

MANAGE OPERATIONS AND FINANCE

Analysis of Results

On the basis of application of different investment appraisal techniques decisions need to

be taken by the management of the company as to which proposal is most suitable for the

business. The payback period results show that proposal 1 has the lowest time frame for recover

the outflows of the business and the same is shown to be 1.67 years. On the other hand, the IRR

of the business which is considered to be a better option than payback period reveals that

proposal 3 is most appropriate as the same has the highest return in the business. In addition to

this, analysis of the estimates which are present for NPV analysis shows that proposal 4 is most

appropriate and would definitely generate more cash inflows for the business in comparisons to

other options which is available to the management of the company. In addition to this, NPV

results are considered to be the most reliable investment appraisal process and therefore on the

basis of the NPV results, the management should proceed with proposal 4. This is considered to

be the most viable option available to the management of the company as per the investment

appraisal techniques which is applied.

Budgeting process and its Role in Business

Budgets can be defined as a tool which is available to the management of the company

for planning, forecasting and controlling the activities of the business (Jones et al. 2013). In a

business, the management prepares different kinds of budgets relating to different area of

performance of the business. The reasons due to which budgeting process is required in a

business are provided below:

Budgets are prepared by the management of the company for planning and forecasting the

activities of the business.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

10

MANAGE OPERATIONS AND FINANCE

Budgeting process is also used by the management of the company for controlling the

activities of the business and maintaining proper supervision in the operational process of

the business.

Budgets are also used in a business for allocation of resources to different departments and

controlling the costs of the business.

It is to be noted that budgeting process plays a very important role in forecasting the

activities of the business and estimating how much funds would be required for a project; how

much revenue can be generated from the project and what is the estimate of the cost incurred in

the project. It is on the basis of such information that the management take decision regarding

implementation of the project or not. In most of the business a master budget is prepared by the

management of the company which covers different area of performance of the business.

The budgeting process of Cucumber ltd is considered and the same shows that there are

certain variances present in the budgets which is prepared by the management of the company. In

order to effectively understand the main reasons for the variances which has affected the

business is shown in the figure below:

MANAGE OPERATIONS AND FINANCE

Budgeting process is also used by the management of the company for controlling the

activities of the business and maintaining proper supervision in the operational process of

the business.

Budgets are also used in a business for allocation of resources to different departments and

controlling the costs of the business.

It is to be noted that budgeting process plays a very important role in forecasting the

activities of the business and estimating how much funds would be required for a project; how

much revenue can be generated from the project and what is the estimate of the cost incurred in

the project. It is on the basis of such information that the management take decision regarding

implementation of the project or not. In most of the business a master budget is prepared by the

management of the company which covers different area of performance of the business.

The budgeting process of Cucumber ltd is considered and the same shows that there are

certain variances present in the budgets which is prepared by the management of the company. In

order to effectively understand the main reasons for the variances which has affected the

business is shown in the figure below:

11

MANAGE OPERATIONS AND FINANCE

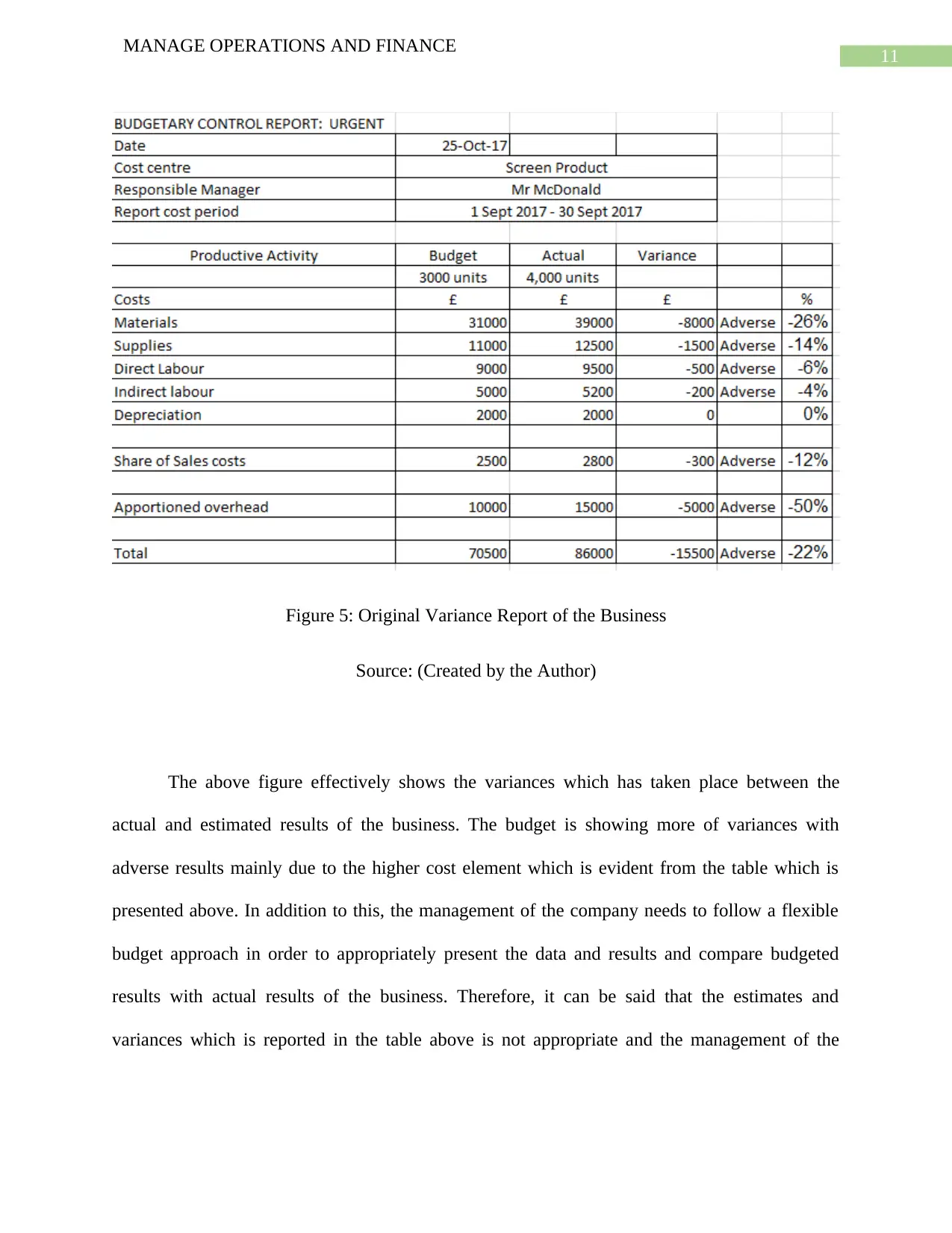

Figure 5: Original Variance Report of the Business

Source: (Created by the Author)

The above figure effectively shows the variances which has taken place between the

actual and estimated results of the business. The budget is showing more of variances with

adverse results mainly due to the higher cost element which is evident from the table which is

presented above. In addition to this, the management of the company needs to follow a flexible

budget approach in order to appropriately present the data and results and compare budgeted

results with actual results of the business. Therefore, it can be said that the estimates and

variances which is reported in the table above is not appropriate and the management of the

MANAGE OPERATIONS AND FINANCE

Figure 5: Original Variance Report of the Business

Source: (Created by the Author)

The above figure effectively shows the variances which has taken place between the

actual and estimated results of the business. The budget is showing more of variances with

adverse results mainly due to the higher cost element which is evident from the table which is

presented above. In addition to this, the management of the company needs to follow a flexible

budget approach in order to appropriately present the data and results and compare budgeted

results with actual results of the business. Therefore, it can be said that the estimates and

variances which is reported in the table above is not appropriate and the management of the

You're viewing a preview

Unlock full access by subscribing today!

12

MANAGE OPERATIONS AND FINANCE

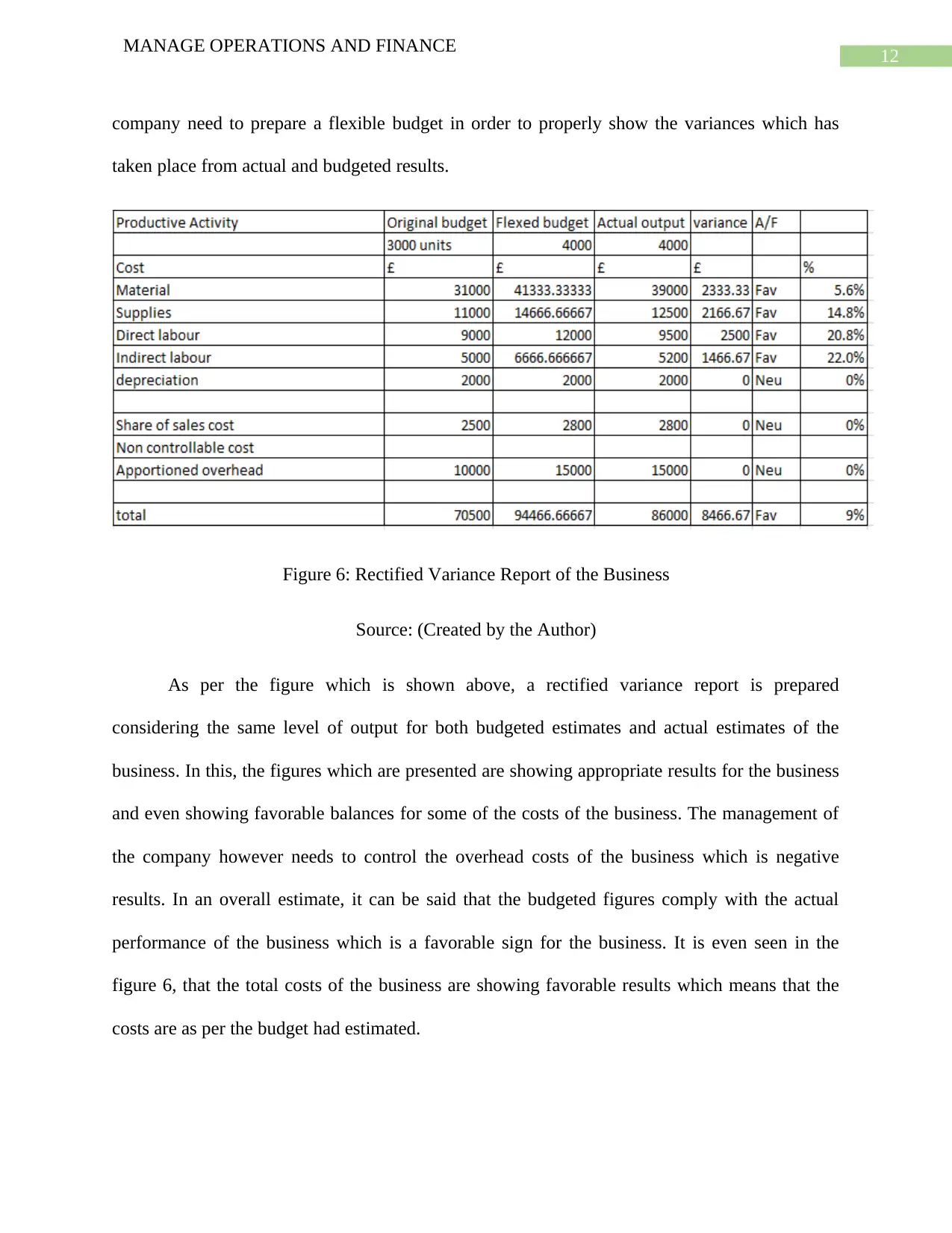

company need to prepare a flexible budget in order to properly show the variances which has

taken place from actual and budgeted results.

Figure 6: Rectified Variance Report of the Business

Source: (Created by the Author)

As per the figure which is shown above, a rectified variance report is prepared

considering the same level of output for both budgeted estimates and actual estimates of the

business. In this, the figures which are presented are showing appropriate results for the business

and even showing favorable balances for some of the costs of the business. The management of

the company however needs to control the overhead costs of the business which is negative

results. In an overall estimate, it can be said that the budgeted figures comply with the actual

performance of the business which is a favorable sign for the business. It is even seen in the

figure 6, that the total costs of the business are showing favorable results which means that the

costs are as per the budget had estimated.

MANAGE OPERATIONS AND FINANCE

company need to prepare a flexible budget in order to properly show the variances which has

taken place from actual and budgeted results.

Figure 6: Rectified Variance Report of the Business

Source: (Created by the Author)

As per the figure which is shown above, a rectified variance report is prepared

considering the same level of output for both budgeted estimates and actual estimates of the

business. In this, the figures which are presented are showing appropriate results for the business

and even showing favorable balances for some of the costs of the business. The management of

the company however needs to control the overhead costs of the business which is negative

results. In an overall estimate, it can be said that the budgeted figures comply with the actual

performance of the business which is a favorable sign for the business. It is even seen in the

figure 6, that the total costs of the business are showing favorable results which means that the

costs are as per the budget had estimated.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

13

MANAGE OPERATIONS AND FINANCE

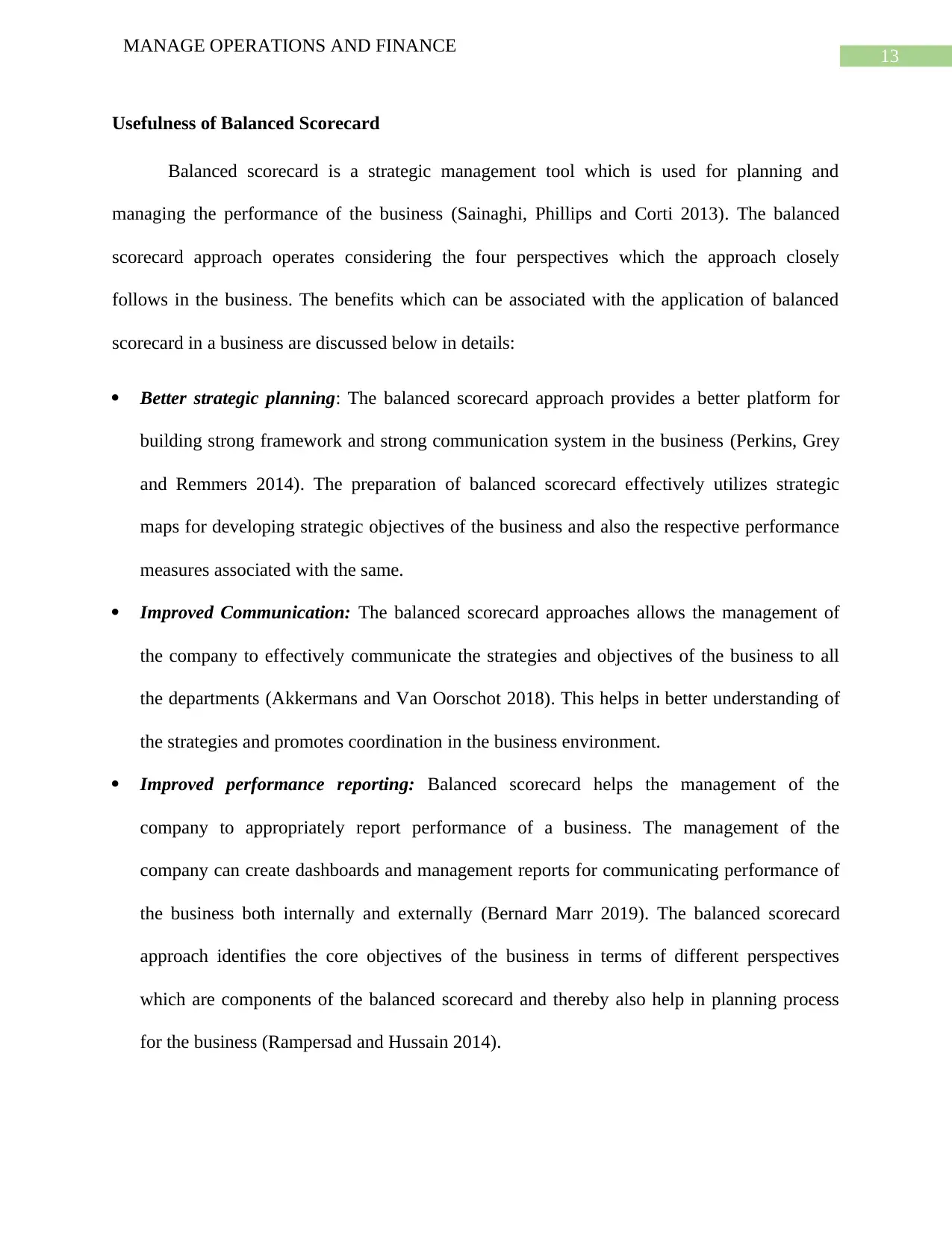

Usefulness of Balanced Scorecard

Balanced scorecard is a strategic management tool which is used for planning and

managing the performance of the business (Sainaghi, Phillips and Corti 2013). The balanced

scorecard approach operates considering the four perspectives which the approach closely

follows in the business. The benefits which can be associated with the application of balanced

scorecard in a business are discussed below in details:

Better strategic planning: The balanced scorecard approach provides a better platform for

building strong framework and strong communication system in the business (Perkins, Grey

and Remmers 2014). The preparation of balanced scorecard effectively utilizes strategic

maps for developing strategic objectives of the business and also the respective performance

measures associated with the same.

Improved Communication: The balanced scorecard approaches allows the management of

the company to effectively communicate the strategies and objectives of the business to all

the departments (Akkermans and Van Oorschot 2018). This helps in better understanding of

the strategies and promotes coordination in the business environment.

Improved performance reporting: Balanced scorecard helps the management of the

company to appropriately report performance of a business. The management of the

company can create dashboards and management reports for communicating performance of

the business both internally and externally (Bernard Marr 2019). The balanced scorecard

approach identifies the core objectives of the business in terms of different perspectives

which are components of the balanced scorecard and thereby also help in planning process

for the business (Rampersad and Hussain 2014).

MANAGE OPERATIONS AND FINANCE

Usefulness of Balanced Scorecard

Balanced scorecard is a strategic management tool which is used for planning and

managing the performance of the business (Sainaghi, Phillips and Corti 2013). The balanced

scorecard approach operates considering the four perspectives which the approach closely

follows in the business. The benefits which can be associated with the application of balanced

scorecard in a business are discussed below in details:

Better strategic planning: The balanced scorecard approach provides a better platform for

building strong framework and strong communication system in the business (Perkins, Grey

and Remmers 2014). The preparation of balanced scorecard effectively utilizes strategic

maps for developing strategic objectives of the business and also the respective performance

measures associated with the same.

Improved Communication: The balanced scorecard approaches allows the management of

the company to effectively communicate the strategies and objectives of the business to all

the departments (Akkermans and Van Oorschot 2018). This helps in better understanding of

the strategies and promotes coordination in the business environment.

Improved performance reporting: Balanced scorecard helps the management of the

company to appropriately report performance of a business. The management of the

company can create dashboards and management reports for communicating performance of

the business both internally and externally (Bernard Marr 2019). The balanced scorecard

approach identifies the core objectives of the business in terms of different perspectives

which are components of the balanced scorecard and thereby also help in planning process

for the business (Rampersad and Hussain 2014).

14

MANAGE OPERATIONS AND FINANCE

Figure 7: Different Perspective of Balanced Scorecard

Source: (Bernard Marr 2019)

Balanced Scorecard of Cucumber Ltd

KRA (key

result area)

Target KPI (key

performance

indicator)

Result

Financial

Perspective

The plan of the business

is to enhance the profitability

of the business more in

comparisons to previous

year’s figures

Increase in Net

profit of the

bsuiness

Increase in profit

Business

Process

Perspective

Improving the

operational efficiency in the

business by ensuring that the

departments of the business

functions appropriately

High rate of

success in

Converting

Business

opportunities

Greater efficiency

and communication

development

Learning

and Growth

Perspective

Better quality of staff

who have necessary skills

and talent would be available

to the business and

introduction of training

program for development of

Competent

Staff

Increase in

employee efficiency

and less production

time, cost savings

MANAGE OPERATIONS AND FINANCE

Figure 7: Different Perspective of Balanced Scorecard

Source: (Bernard Marr 2019)

Balanced Scorecard of Cucumber Ltd

KRA (key

result area)

Target KPI (key

performance

indicator)

Result

Financial

Perspective

The plan of the business

is to enhance the profitability

of the business more in

comparisons to previous

year’s figures

Increase in Net

profit of the

bsuiness

Increase in profit

Business

Process

Perspective

Improving the

operational efficiency in the

business by ensuring that the

departments of the business

functions appropriately

High rate of

success in

Converting

Business

opportunities

Greater efficiency

and communication

development

Learning

and Growth

Perspective

Better quality of staff

who have necessary skills

and talent would be available

to the business and

introduction of training

program for development of

Competent

Staff

Increase in

employee efficiency

and less production

time, cost savings

You're viewing a preview

Unlock full access by subscribing today!

15

MANAGE OPERATIONS AND FINANCE

human resources

Customer

Perspective

Improve the quality of

goods offered to the

customers and ensuring that

the customers are satisfied

with the products which is

offered by the business.

Positive

Feedback,

Improvement in

Brand loyalty

Improvement in

brand image and

enhancement of

customer base of the

company.

MANAGE OPERATIONS AND FINANCE

human resources

Customer

Perspective

Improve the quality of

goods offered to the

customers and ensuring that

the customers are satisfied

with the products which is

offered by the business.

Positive

Feedback,

Improvement in

Brand loyalty

Improvement in

brand image and

enhancement of

customer base of the

company.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

16

MANAGE OPERATIONS AND FINANCE

Reference

Akkermans, H.A. and Van Oorschot, K.E., 2018. Relevance assumed: a case study of balanced

scorecard development using system dynamics. In System Dynamics (pp. 107-132). Palgrave

Macmillan, London.

Bernard Marr. (2019). The Benefits of a Balanced Scorecard. [online] Available at:

https://bernardmarr.com/default.asp?contentID=1478 [Accessed 10 May 2019].

Coleman, C., Crosby, N., McAllister, P. and Wyatt, P., 2013. Development appraisal in practice:

some evidence from the planning system. Journal of Property Research, 30(2), pp.144-165.

Dyckman, T.R. and Zeff, S.A., 2015. Accounting research: past, present, and

future. Abacus, 51(4), pp.511-524.

Francis, B., Hasan, I. and Wu, Q., 2013. The benefits of conservative accounting to shareholders:

Evidence from the financial crisis. Accounting Horizons, 27(2), pp.319-346.

Fullerton, R.R., Kennedy, F.A. and Widener, S.K., 2014. Lean manufacturing and firm

performance: The incremental contribution of lean management accounting practices. Journal of

Operations Management, 32(7-8), pp.414-428.

Harris, E., 2017. Strategic project risk appraisal and management. Routledge.

Henderson, S., Peirson, G., Herbohn, K. and Howieson, B., 2015. Issues in financial accounting.

Pearson Higher Education AU.

Hilton, R.W. and Platt, D.E., 2013. Managerial accounting: creating value in a dynamic

business environment. McGraw-Hill Education.

MANAGE OPERATIONS AND FINANCE

Reference

Akkermans, H.A. and Van Oorschot, K.E., 2018. Relevance assumed: a case study of balanced

scorecard development using system dynamics. In System Dynamics (pp. 107-132). Palgrave

Macmillan, London.

Bernard Marr. (2019). The Benefits of a Balanced Scorecard. [online] Available at:

https://bernardmarr.com/default.asp?contentID=1478 [Accessed 10 May 2019].

Coleman, C., Crosby, N., McAllister, P. and Wyatt, P., 2013. Development appraisal in practice:

some evidence from the planning system. Journal of Property Research, 30(2), pp.144-165.

Dyckman, T.R. and Zeff, S.A., 2015. Accounting research: past, present, and

future. Abacus, 51(4), pp.511-524.

Francis, B., Hasan, I. and Wu, Q., 2013. The benefits of conservative accounting to shareholders:

Evidence from the financial crisis. Accounting Horizons, 27(2), pp.319-346.

Fullerton, R.R., Kennedy, F.A. and Widener, S.K., 2014. Lean manufacturing and firm

performance: The incremental contribution of lean management accounting practices. Journal of

Operations Management, 32(7-8), pp.414-428.

Harris, E., 2017. Strategic project risk appraisal and management. Routledge.

Henderson, S., Peirson, G., Herbohn, K. and Howieson, B., 2015. Issues in financial accounting.

Pearson Higher Education AU.

Hilton, R.W. and Platt, D.E., 2013. Managerial accounting: creating value in a dynamic

business environment. McGraw-Hill Education.

17

MANAGE OPERATIONS AND FINANCE

Hodder, L., Hopkins, P. and Schipper, K., 2014. Fair value measurement in financial

reporting. Foundations and Trends® in Accounting, 8(3-4), pp.143-270.

Jones, R., Lande, E., Lüder, K. and Portal, M., 2013. A comparison of budgeting and accounting

reforms in the national governments of France, Germany, the UK and the US. Financial

Accountability & Management, 29(4), pp.419-441.

Macuda, M., Matuszak, Ł. and Różańska, E., 2015. The concept of CSR in accounting theory

and practice in Poland: an empirical study. Zeszyty Teoretyczne Rachunkowosci, 84(140).

Perkins, M., Grey, A. and Remmers, H., 2014. What do we really mean by “Balanced

Scorecard”?. International Journal of Productivity and Performance Management, 63(2),

pp.148-169.

Rampersad, H. and Hussain, S., 2014. Personal balanced scorecard. In Authentic

Governance (pp. 29-38). Springer, Cham.

Sainaghi, R., Phillips, P. and Corti, V., 2013. Measuring hotel performance: Using a balanced

scorecard perspectives’ approach. International Journal of Hospitality Management, 34, pp.150-

159.

Sunarni, C.W., 2013. Management accounting practices and the role of management accountant:

Evidence from manufacturing companies throughout Yogyakarta, Indonesia. Review of

Integrative Business and Economics Research, 2(2), p.616.

Warren, C., Reeve, J.M. and Duchac, J., 2013. Financial & managerial accounting. Cengage

Learning.

MANAGE OPERATIONS AND FINANCE

Hodder, L., Hopkins, P. and Schipper, K., 2014. Fair value measurement in financial

reporting. Foundations and Trends® in Accounting, 8(3-4), pp.143-270.

Jones, R., Lande, E., Lüder, K. and Portal, M., 2013. A comparison of budgeting and accounting

reforms in the national governments of France, Germany, the UK and the US. Financial

Accountability & Management, 29(4), pp.419-441.

Macuda, M., Matuszak, Ł. and Różańska, E., 2015. The concept of CSR in accounting theory

and practice in Poland: an empirical study. Zeszyty Teoretyczne Rachunkowosci, 84(140).

Perkins, M., Grey, A. and Remmers, H., 2014. What do we really mean by “Balanced

Scorecard”?. International Journal of Productivity and Performance Management, 63(2),

pp.148-169.

Rampersad, H. and Hussain, S., 2014. Personal balanced scorecard. In Authentic

Governance (pp. 29-38). Springer, Cham.

Sainaghi, R., Phillips, P. and Corti, V., 2013. Measuring hotel performance: Using a balanced

scorecard perspectives’ approach. International Journal of Hospitality Management, 34, pp.150-

159.

Sunarni, C.W., 2013. Management accounting practices and the role of management accountant:

Evidence from manufacturing companies throughout Yogyakarta, Indonesia. Review of

Integrative Business and Economics Research, 2(2), p.616.

Warren, C., Reeve, J.M. and Duchac, J., 2013. Financial & managerial accounting. Cengage

Learning.

You're viewing a preview

Unlock full access by subscribing today!

1 out of 18

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

© 2024 | Zucol Services PVT LTD | All rights reserved.