Detailed Finance and Operations Report: New Life Training PLC

VerifiedAdded on 2020/10/22

|11

|3206

|66

Report

AI Summary

This report provides a comprehensive analysis of the financial and operational aspects of New Life Training PLC. It begins with an evaluation of operational and regulatory factors considered by the board, including the company's vision to be listed on the London Stock Exchange. The report then estimates income and expenditure projections for the first four years, detailing expected revenues from franchise training, student sessions, and private hire. A critical evaluation of the financial worth of the current proposal is presented, including contribution analysis, break-even analysis, payback period, and average rate of return. The report provides a detailed financial analysis, including income statements, and concludes with recommendations for the board based on the financial projections and evaluations. The report assesses the financial stability and provides insights into the company's strategic financial planning, capital structure, and investment appraisal methods.

MANAGING FINANCE AND

OPERATIONS

OPERATIONS

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

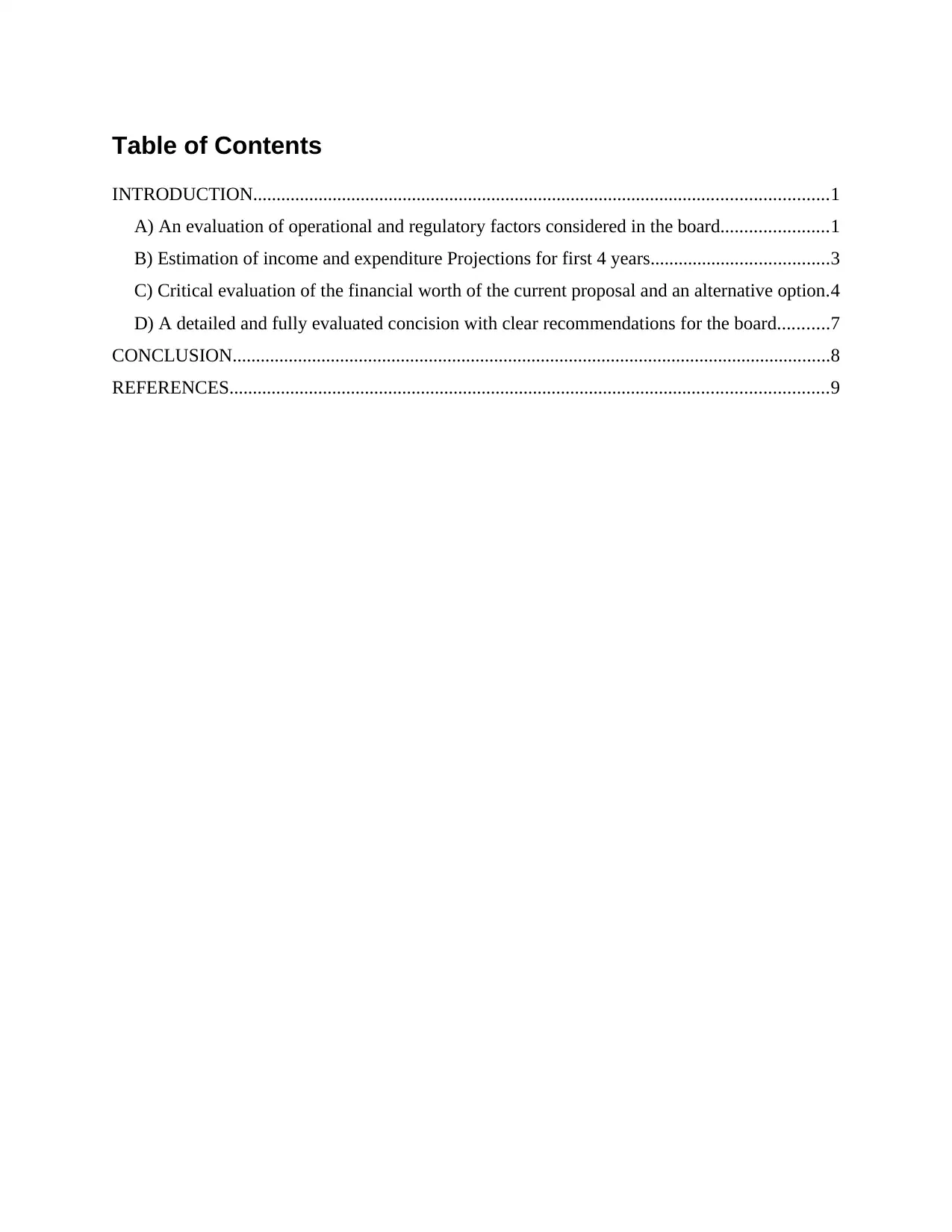

Table of Contents

INTRODUCTION...........................................................................................................................1

A) An evaluation of operational and regulatory factors considered in the board.......................1

B) Estimation of income and expenditure Projections for first 4 years......................................3

C) Critical evaluation of the financial worth of the current proposal and an alternative option.4

D) A detailed and fully evaluated concision with clear recommendations for the board...........7

CONCLUSION................................................................................................................................8

REFERENCES................................................................................................................................9

INTRODUCTION...........................................................................................................................1

A) An evaluation of operational and regulatory factors considered in the board.......................1

B) Estimation of income and expenditure Projections for first 4 years......................................3

C) Critical evaluation of the financial worth of the current proposal and an alternative option.4

D) A detailed and fully evaluated concision with clear recommendations for the board...........7

CONCLUSION................................................................................................................................8

REFERENCES................................................................................................................................9

INTRODUCTION

Management of finance operation and department are the essential requirement of

organisation. It is very important for an organisation to adhere the financial standards and rules

related to financial management and operation (Hettinger and Dolan-Heitlinger, 2011). There is a

financial projection and analysis of financial stability of New Life Training plc. There are

training and facility of growing company and the finance management and operations are

defined in this report. Financial management and operation assist the organisational structure to

determine the requirement of financial resources and managing the resources for better

understanding the financial management are defined in this context.

A) An evaluation of operational and regulatory factors considered in the board

Over view of case scenario

New Life Training is one of the growing and developing organisation which has an

authorised share capital of £50 million and paid up shares are £1 ordinary shares and retained

earning of £10 million. There are 20 shareholders are identical share holdings are included in this

structure. Sobia Schburt is the managing director of organisation and has a vision of the company

on the London stock exchange within 5 years. There are strategies and the plans for achieving

the targets are analysed in this context. Organisation is providing tuition services to students of

age group 5 years to 18 years of age. It is seen that the organisation is ruining its existing

business model fluently and effectively in terms of the quality control and curriculum designer of

courses with the operational aspects.

Board of the company analyse and reviewed the policies, procedures and protocols

related to building, Bespoke Training centre in East London. There are following activities will

be carried out like,

Compulsory franchisee training,

Evening sessions for East London School Children

Private letting facility to community group

It is analysed that the estimated set up cost of building small building on land will be

£1,100,000 in which reserves, over run and snagging of £100000 are included. The debt

position of organisation indicates towards following aspects such as

4 Full time equivalent tutors costing £30000 each per annum

FTE admission cost worth £18000 each per year

1

Management of finance operation and department are the essential requirement of

organisation. It is very important for an organisation to adhere the financial standards and rules

related to financial management and operation (Hettinger and Dolan-Heitlinger, 2011). There is a

financial projection and analysis of financial stability of New Life Training plc. There are

training and facility of growing company and the finance management and operations are

defined in this report. Financial management and operation assist the organisational structure to

determine the requirement of financial resources and managing the resources for better

understanding the financial management are defined in this context.

A) An evaluation of operational and regulatory factors considered in the board

Over view of case scenario

New Life Training is one of the growing and developing organisation which has an

authorised share capital of £50 million and paid up shares are £1 ordinary shares and retained

earning of £10 million. There are 20 shareholders are identical share holdings are included in this

structure. Sobia Schburt is the managing director of organisation and has a vision of the company

on the London stock exchange within 5 years. There are strategies and the plans for achieving

the targets are analysed in this context. Organisation is providing tuition services to students of

age group 5 years to 18 years of age. It is seen that the organisation is ruining its existing

business model fluently and effectively in terms of the quality control and curriculum designer of

courses with the operational aspects.

Board of the company analyse and reviewed the policies, procedures and protocols

related to building, Bespoke Training centre in East London. There are following activities will

be carried out like,

Compulsory franchisee training,

Evening sessions for East London School Children

Private letting facility to community group

It is analysed that the estimated set up cost of building small building on land will be

£1,100,000 in which reserves, over run and snagging of £100000 are included. The debt

position of organisation indicates towards following aspects such as

4 Full time equivalent tutors costing £30000 each per annum

FTE admission cost worth £18000 each per year

1

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

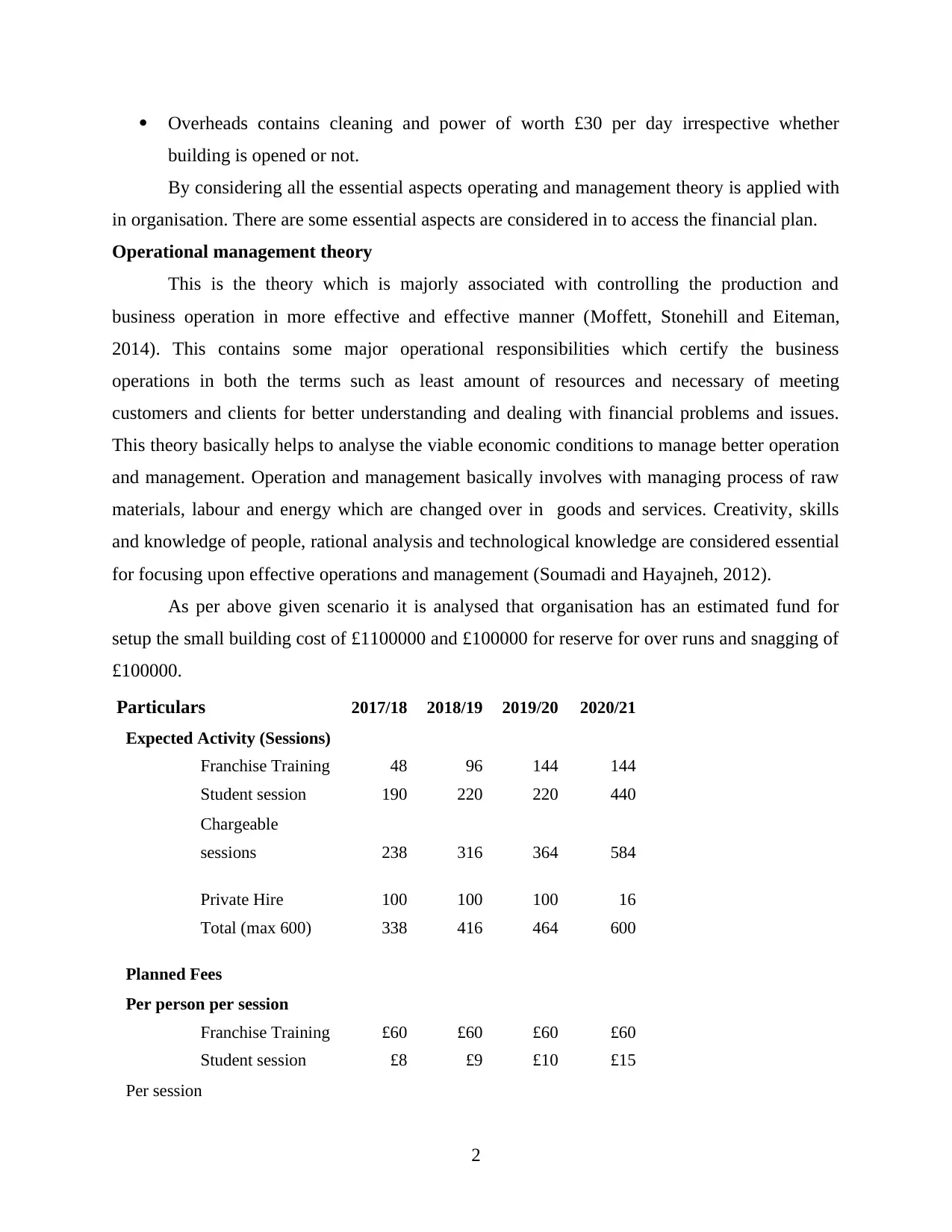

Overheads contains cleaning and power of worth £30 per day irrespective whether

building is opened or not.

By considering all the essential aspects operating and management theory is applied with

in organisation. There are some essential aspects are considered in to access the financial plan.

Operational management theory

This is the theory which is majorly associated with controlling the production and

business operation in more effective and effective manner (Moffett, Stonehill and Eiteman,

2014). This contains some major operational responsibilities which certify the business

operations in both the terms such as least amount of resources and necessary of meeting

customers and clients for better understanding and dealing with financial problems and issues.

This theory basically helps to analyse the viable economic conditions to manage better operation

and management. Operation and management basically involves with managing process of raw

materials, labour and energy which are changed over in goods and services. Creativity, skills

and knowledge of people, rational analysis and technological knowledge are considered essential

for focusing upon effective operations and management (Soumadi and Hayajneh, 2012).

As per above given scenario it is analysed that organisation has an estimated fund for

setup the small building cost of £1100000 and £100000 for reserve for over runs and snagging of

£100000.

Particulars 2017/18 2018/19 2019/20 2020/21

Expected Activity (Sessions)

Franchise Training 48 96 144 144

Student session 190 220 220 440

Chargeable

sessions 238 316 364 584

Private Hire 100 100 100 16

Total (max 600) 338 416 464 600

Planned Fees

Per person per session

Franchise Training £60 £60 £60 £60

Student session £8 £9 £10 £15

Per session

2

building is opened or not.

By considering all the essential aspects operating and management theory is applied with

in organisation. There are some essential aspects are considered in to access the financial plan.

Operational management theory

This is the theory which is majorly associated with controlling the production and

business operation in more effective and effective manner (Moffett, Stonehill and Eiteman,

2014). This contains some major operational responsibilities which certify the business

operations in both the terms such as least amount of resources and necessary of meeting

customers and clients for better understanding and dealing with financial problems and issues.

This theory basically helps to analyse the viable economic conditions to manage better operation

and management. Operation and management basically involves with managing process of raw

materials, labour and energy which are changed over in goods and services. Creativity, skills

and knowledge of people, rational analysis and technological knowledge are considered essential

for focusing upon effective operations and management (Soumadi and Hayajneh, 2012).

As per above given scenario it is analysed that organisation has an estimated fund for

setup the small building cost of £1100000 and £100000 for reserve for over runs and snagging of

£100000.

Particulars 2017/18 2018/19 2019/20 2020/21

Expected Activity (Sessions)

Franchise Training 48 96 144 144

Student session 190 220 220 440

Chargeable

sessions 238 316 364 584

Private Hire 100 100 100 16

Total (max 600) 338 416 464 600

Planned Fees

Per person per session

Franchise Training £60 £60 £60 £60

Student session £8 £9 £10 £15

Per session

2

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

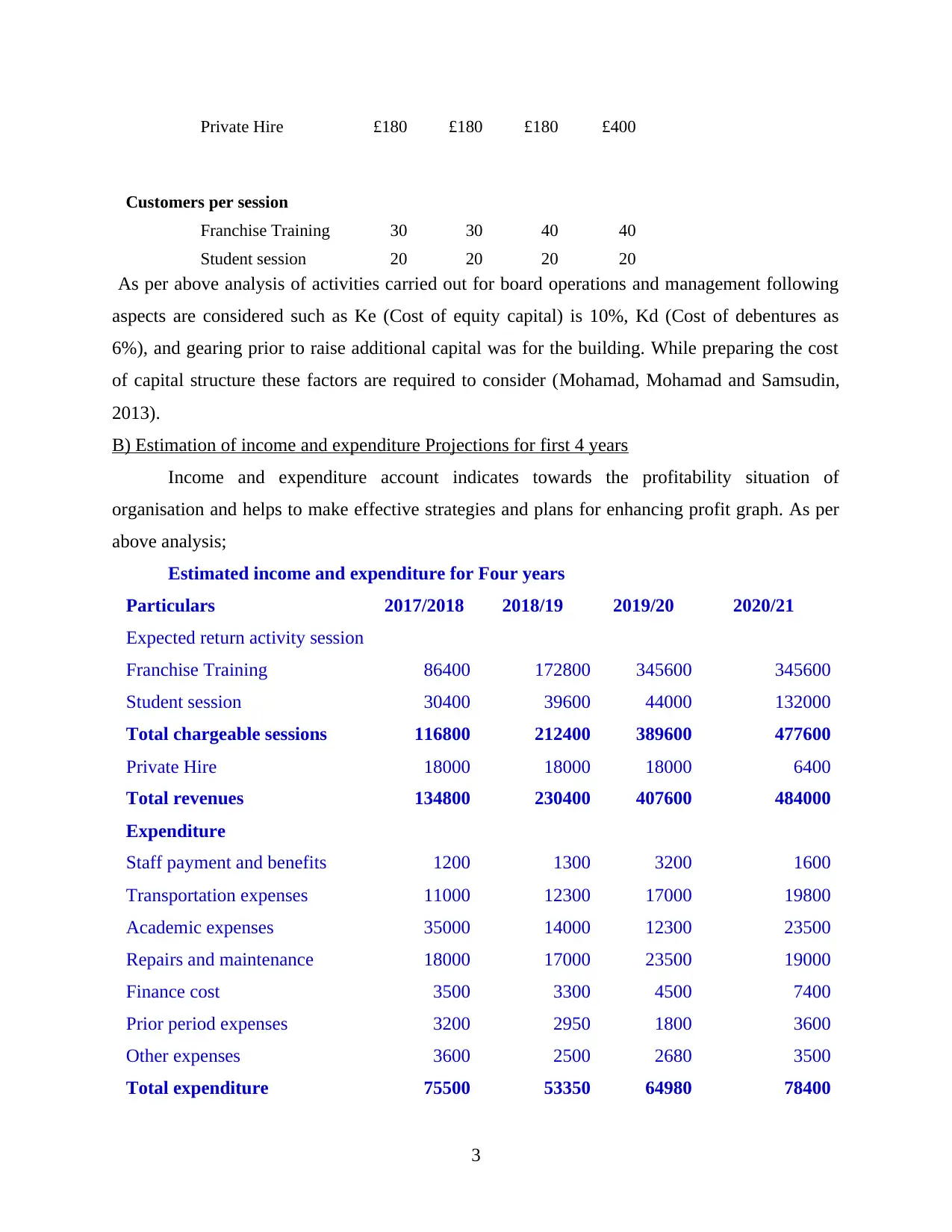

Private Hire £180 £180 £180 £400

Customers per session

Franchise Training 30 30 40 40

Student session 20 20 20 20

As per above analysis of activities carried out for board operations and management following

aspects are considered such as Ke (Cost of equity capital) is 10%, Kd (Cost of debentures as

6%), and gearing prior to raise additional capital was for the building. While preparing the cost

of capital structure these factors are required to consider (Mohamad, Mohamad and Samsudin,

2013).

B) Estimation of income and expenditure Projections for first 4 years

Income and expenditure account indicates towards the profitability situation of

organisation and helps to make effective strategies and plans for enhancing profit graph. As per

above analysis;

Estimated income and expenditure for Four years

Particulars 2017/2018 2018/19 2019/20 2020/21

Expected return activity session

Franchise Training 86400 172800 345600 345600

Student session 30400 39600 44000 132000

Total chargeable sessions 116800 212400 389600 477600

Private Hire 18000 18000 18000 6400

Total revenues 134800 230400 407600 484000

Expenditure

Staff payment and benefits 1200 1300 3200 1600

Transportation expenses 11000 12300 17000 19800

Academic expenses 35000 14000 12300 23500

Repairs and maintenance 18000 17000 23500 19000

Finance cost 3500 3300 4500 7400

Prior period expenses 3200 2950 1800 3600

Other expenses 3600 2500 2680 3500

Total expenditure 75500 53350 64980 78400

3

Customers per session

Franchise Training 30 30 40 40

Student session 20 20 20 20

As per above analysis of activities carried out for board operations and management following

aspects are considered such as Ke (Cost of equity capital) is 10%, Kd (Cost of debentures as

6%), and gearing prior to raise additional capital was for the building. While preparing the cost

of capital structure these factors are required to consider (Mohamad, Mohamad and Samsudin,

2013).

B) Estimation of income and expenditure Projections for first 4 years

Income and expenditure account indicates towards the profitability situation of

organisation and helps to make effective strategies and plans for enhancing profit graph. As per

above analysis;

Estimated income and expenditure for Four years

Particulars 2017/2018 2018/19 2019/20 2020/21

Expected return activity session

Franchise Training 86400 172800 345600 345600

Student session 30400 39600 44000 132000

Total chargeable sessions 116800 212400 389600 477600

Private Hire 18000 18000 18000 6400

Total revenues 134800 230400 407600 484000

Expenditure

Staff payment and benefits 1200 1300 3200 1600

Transportation expenses 11000 12300 17000 19800

Academic expenses 35000 14000 12300 23500

Repairs and maintenance 18000 17000 23500 19000

Finance cost 3500 3300 4500 7400

Prior period expenses 3200 2950 1800 3600

Other expenses 3600 2500 2680 3500

Total expenditure 75500 53350 64980 78400

3

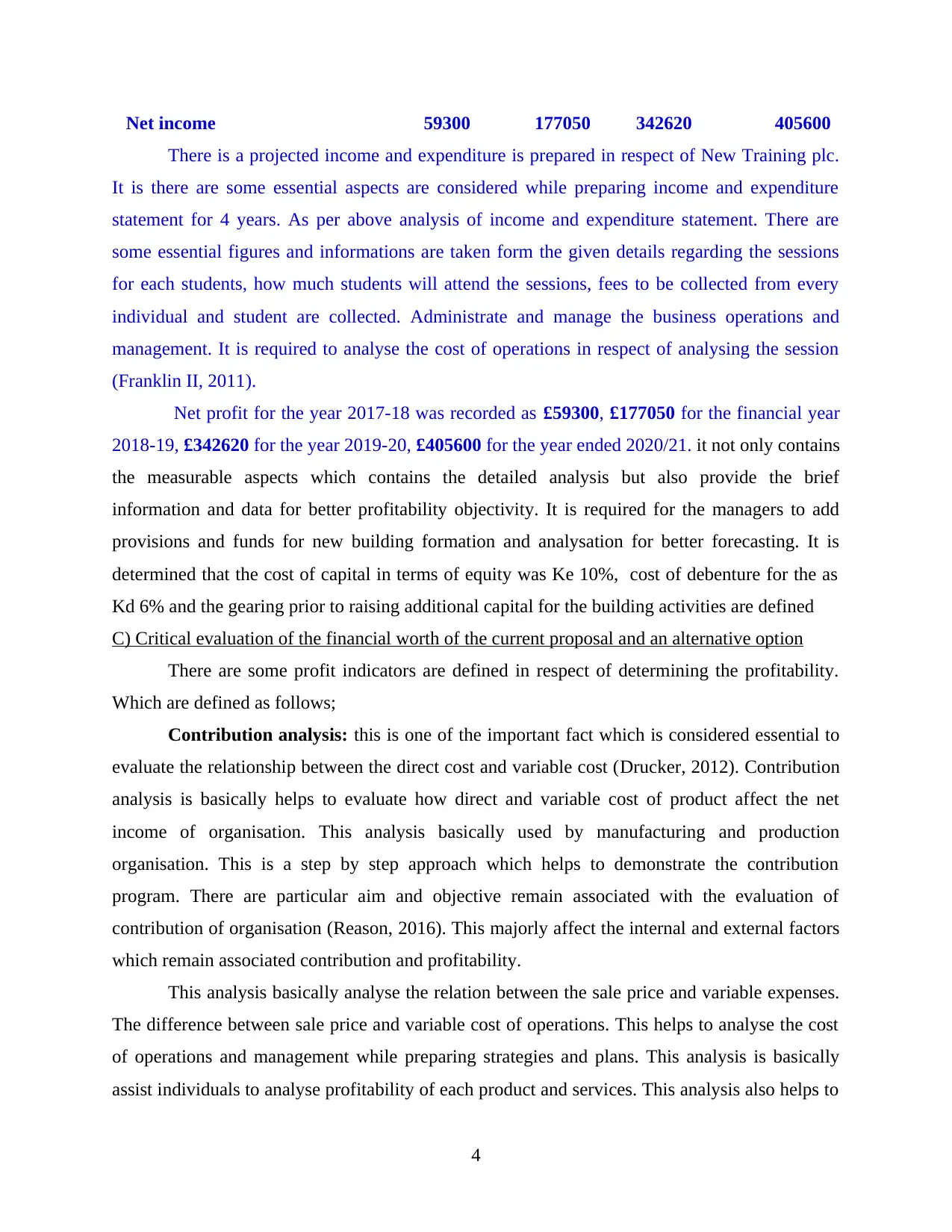

Net income 59300 177050 342620 405600

There is a projected income and expenditure is prepared in respect of New Training plc.

It is there are some essential aspects are considered while preparing income and expenditure

statement for 4 years. As per above analysis of income and expenditure statement. There are

some essential figures and informations are taken form the given details regarding the sessions

for each students, how much students will attend the sessions, fees to be collected from every

individual and student are collected. Administrate and manage the business operations and

management. It is required to analyse the cost of operations in respect of analysing the session

(Franklin II, 2011).

Net profit for the year 2017-18 was recorded as £59300, £177050 for the financial year

2018-19, £342620 for the year 2019-20, £405600 for the year ended 2020/21. it not only contains

the measurable aspects which contains the detailed analysis but also provide the brief

information and data for better profitability objectivity. It is required for the managers to add

provisions and funds for new building formation and analysation for better forecasting. It is

determined that the cost of capital in terms of equity was Ke 10%, cost of debenture for the as

Kd 6% and the gearing prior to raising additional capital for the building activities are defined

C) Critical evaluation of the financial worth of the current proposal and an alternative option

There are some profit indicators are defined in respect of determining the profitability.

Which are defined as follows;

Contribution analysis: this is one of the important fact which is considered essential to

evaluate the relationship between the direct cost and variable cost (Drucker, 2012). Contribution

analysis is basically helps to evaluate how direct and variable cost of product affect the net

income of organisation. This analysis basically used by manufacturing and production

organisation. This is a step by step approach which helps to demonstrate the contribution

program. There are particular aim and objective remain associated with the evaluation of

contribution of organisation (Reason, 2016). This majorly affect the internal and external factors

which remain associated contribution and profitability.

This analysis basically analyse the relation between the sale price and variable expenses.

The difference between sale price and variable cost of operations. This helps to analyse the cost

of operations and management while preparing strategies and plans. This analysis is basically

assist individuals to analyse profitability of each product and services. This analysis also helps to

4

There is a projected income and expenditure is prepared in respect of New Training plc.

It is there are some essential aspects are considered while preparing income and expenditure

statement for 4 years. As per above analysis of income and expenditure statement. There are

some essential figures and informations are taken form the given details regarding the sessions

for each students, how much students will attend the sessions, fees to be collected from every

individual and student are collected. Administrate and manage the business operations and

management. It is required to analyse the cost of operations in respect of analysing the session

(Franklin II, 2011).

Net profit for the year 2017-18 was recorded as £59300, £177050 for the financial year

2018-19, £342620 for the year 2019-20, £405600 for the year ended 2020/21. it not only contains

the measurable aspects which contains the detailed analysis but also provide the brief

information and data for better profitability objectivity. It is required for the managers to add

provisions and funds for new building formation and analysation for better forecasting. It is

determined that the cost of capital in terms of equity was Ke 10%, cost of debenture for the as

Kd 6% and the gearing prior to raising additional capital for the building activities are defined

C) Critical evaluation of the financial worth of the current proposal and an alternative option

There are some profit indicators are defined in respect of determining the profitability.

Which are defined as follows;

Contribution analysis: this is one of the important fact which is considered essential to

evaluate the relationship between the direct cost and variable cost (Drucker, 2012). Contribution

analysis is basically helps to evaluate how direct and variable cost of product affect the net

income of organisation. This analysis basically used by manufacturing and production

organisation. This is a step by step approach which helps to demonstrate the contribution

program. There are particular aim and objective remain associated with the evaluation of

contribution of organisation (Reason, 2016). This majorly affect the internal and external factors

which remain associated contribution and profitability.

This analysis basically analyse the relation between the sale price and variable expenses.

The difference between sale price and variable cost of operations. This helps to analyse the cost

of operations and management while preparing strategies and plans. This analysis is basically

assist individuals to analyse profitability of each product and services. This analysis also helps to

4

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

analyse the relation between the break even point and desired sales for organisation. It helps to

analyse that how much cost is utilised and cost to be recovered by utilising financial resporces.

This is calculated as follow;

Formula

Contribution = Selling price of product or services – Variable cost or cost of goods

sold

Contribution margin = (Contribution / sale prices) *100

Contribution margin helps to determine the margin which is retain in respect of sales.

these are analysed in order to determine the certain percentage on sales price and contribution

per unit. For example

Particulars Amount (£)

Sales 15000

(-) Variable cost -9000

Contribution 6000

Break even analysis: this analysis is one of the effective and useful analysis tool in

respect of determining the point of sales and units at which organisation earn optimum

profitability (Sanders, 2013). This is one of the essential tool for determining the point at which

the cost and revenues remain at same level. Break even analysis involves the economic order

quantity and cost accounting at which point the total cost and total revenue remain equal. This

helps to understand and analyse the overall cost of manufacturing and production process. This

analysis basically helps to correlate the relation between the fixed cost and contribution. Paid and

capital has received the risk adjustment and expected return are analysed in this context.

Break even analysis is the calculation of the optimum quantity of sales to generate

minimum requirement of profit and contribution. Break even analysis is analysed in two terms

such as Break even in units and break even in sales. This is calculated as per following formula;

Break Even analysis (in units) = Total Fixed cost / contribution per units

Break even analysis in sales (£) = Total Fixed cost / PV ratio

P.V. Ratio = (Contribution / Sales)*100

5

analyse that how much cost is utilised and cost to be recovered by utilising financial resporces.

This is calculated as follow;

Formula

Contribution = Selling price of product or services – Variable cost or cost of goods

sold

Contribution margin = (Contribution / sale prices) *100

Contribution margin helps to determine the margin which is retain in respect of sales.

these are analysed in order to determine the certain percentage on sales price and contribution

per unit. For example

Particulars Amount (£)

Sales 15000

(-) Variable cost -9000

Contribution 6000

Break even analysis: this analysis is one of the effective and useful analysis tool in

respect of determining the point of sales and units at which organisation earn optimum

profitability (Sanders, 2013). This is one of the essential tool for determining the point at which

the cost and revenues remain at same level. Break even analysis involves the economic order

quantity and cost accounting at which point the total cost and total revenue remain equal. This

helps to understand and analyse the overall cost of manufacturing and production process. This

analysis basically helps to correlate the relation between the fixed cost and contribution. Paid and

capital has received the risk adjustment and expected return are analysed in this context.

Break even analysis is the calculation of the optimum quantity of sales to generate

minimum requirement of profit and contribution. Break even analysis is analysed in two terms

such as Break even in units and break even in sales. This is calculated as per following formula;

Break Even analysis (in units) = Total Fixed cost / contribution per units

Break even analysis in sales (£) = Total Fixed cost / PV ratio

P.V. Ratio = (Contribution / Sales)*100

5

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Payback period: this is one of the method of capital investing appraisal method which

helps to determine the recovery cost of capital projects and plans after a particular time duration

(Vernimmen and et. al., 2014). This analysis basically helps to determine the period of analysing

the positive aspect in terms of cash outflows an investment to be expected and recovered from

the cash inflows generated by the investment appraisal techniques. inflows generated to be

covered from the cash generated for the inflows generated by the investment. It is evaluated as

follows;

This formula is also framed as per the cash flow per period form the project depends

remain even or uneven. In this case the formula are calculated as

Payback period = initial investment / Cash inflow per period

It is also analysed as per following aspect such as Payback period = A + ( B / C ). where A

indicates towards the last period with a negative cumulative cash flow, B indicates towards the

absolute of cumulative cash flow at the end of the period A and C indicates towards total cash

flow during the period A.

Average Rate of Return: This is also one of the essential investment appraisal technique

which is used to analyse the sustainability of capital project and investments (Hillier, 2012). It is

considered that the capital projects which remain associated with managing the capital project

are evaluated with the help of centralised rate of return. Average rate of return which is known as

ratios of estimating accounting profit of a project to the average investment made in the project.

ARR is mainly used in investment appraisal techniques. ARR is calculated as per following

formula

ARR = Average accounting profit / Average investment

This is the method which is considered as the arithmetic mean of accounting expected to

be earned for the specific duration (Thomé and et. al., 2012). Average investment is calculated

by totalling of the beginning and ending book value of the project which remain divided by 2.

Net Present Value: Net present value method is mainly helps to analyse the project

sustainability and consistency of capital project (Broadbent and Cullen, 2012). This method is

also the part of investment appraisal method which helps to analyse project sustainability. There

is an investment by the discounted sum of all cash flows are received from the period. Its is

calculated as analysing the profitability of organisation. Those projects which contains high

6

helps to determine the recovery cost of capital projects and plans after a particular time duration

(Vernimmen and et. al., 2014). This analysis basically helps to determine the period of analysing

the positive aspect in terms of cash outflows an investment to be expected and recovered from

the cash inflows generated by the investment appraisal techniques. inflows generated to be

covered from the cash generated for the inflows generated by the investment. It is evaluated as

follows;

This formula is also framed as per the cash flow per period form the project depends

remain even or uneven. In this case the formula are calculated as

Payback period = initial investment / Cash inflow per period

It is also analysed as per following aspect such as Payback period = A + ( B / C ). where A

indicates towards the last period with a negative cumulative cash flow, B indicates towards the

absolute of cumulative cash flow at the end of the period A and C indicates towards total cash

flow during the period A.

Average Rate of Return: This is also one of the essential investment appraisal technique

which is used to analyse the sustainability of capital project and investments (Hillier, 2012). It is

considered that the capital projects which remain associated with managing the capital project

are evaluated with the help of centralised rate of return. Average rate of return which is known as

ratios of estimating accounting profit of a project to the average investment made in the project.

ARR is mainly used in investment appraisal techniques. ARR is calculated as per following

formula

ARR = Average accounting profit / Average investment

This is the method which is considered as the arithmetic mean of accounting expected to

be earned for the specific duration (Thomé and et. al., 2012). Average investment is calculated

by totalling of the beginning and ending book value of the project which remain divided by 2.

Net Present Value: Net present value method is mainly helps to analyse the project

sustainability and consistency of capital project (Broadbent and Cullen, 2012). This method is

also the part of investment appraisal method which helps to analyse project sustainability. There

is an investment by the discounted sum of all cash flows are received from the period. Its is

calculated as analysing the profitability of organisation. Those projects which contains high

6

present value methods are evaluated with in organisational context. This can be understand as

per following example;

Year Cash Flow Present value factor 10% Present Value

0 -500000 1 -500000

1 59300 0.9090909091 53909.09

2 177050 0.826446281 146322.31

3 342620 0.7513148009 257415.48

4 405600 0.6830134554 277030.26

NPV 234677.14

As per above analysis the net present value of project is evaluate as £80015.03. it is

calculated as initial cash out flow – cash outflow.

D) A detailed and fully evaluated concision with clear recommendations for the board

As per above analysis of case scenario of New life Training plc following aspects are

considered in this context. It is concluded that there is a capital plan is proposed in respect of

expanding the business scale at next level. There are some essential aspects are analysed with the

help of determining the main aspects in terms of business expansion. There is profitability and

sustainability of capital projects are analysed in this context. There is a comparability of existing

business model is analysed in dramatic manner. There is a quality control and management are

required in terms of getting attention by the board.

Following activities need to carried out in terms of building new business model such as

mandatory franchisee training, evening session subject to East London school children and

private letting of facility to community group. These are the groups which are maintained to

elaborate the main aspect in terms of determining the activity to run operations and functions of

organisation.

Recommendations

Board directors set the funds as £1100000 and £100000 for running and snagging. It is

require to pay attention to operational cost. It is required to analyse the cost of operation and

management in terms of generating finance requirement form government grants and donation. It

is require to maintain separate accounts for retaining the records of staff salary and cost of tutors.

Staff salary, administration cost of £18000 of each per annum, overheads containing the cleaning

7

per following example;

Year Cash Flow Present value factor 10% Present Value

0 -500000 1 -500000

1 59300 0.9090909091 53909.09

2 177050 0.826446281 146322.31

3 342620 0.7513148009 257415.48

4 405600 0.6830134554 277030.26

NPV 234677.14

As per above analysis the net present value of project is evaluate as £80015.03. it is

calculated as initial cash out flow – cash outflow.

D) A detailed and fully evaluated concision with clear recommendations for the board

As per above analysis of case scenario of New life Training plc following aspects are

considered in this context. It is concluded that there is a capital plan is proposed in respect of

expanding the business scale at next level. There are some essential aspects are analysed with the

help of determining the main aspects in terms of business expansion. There is profitability and

sustainability of capital projects are analysed in this context. There is a comparability of existing

business model is analysed in dramatic manner. There is a quality control and management are

required in terms of getting attention by the board.

Following activities need to carried out in terms of building new business model such as

mandatory franchisee training, evening session subject to East London school children and

private letting of facility to community group. These are the groups which are maintained to

elaborate the main aspect in terms of determining the activity to run operations and functions of

organisation.

Recommendations

Board directors set the funds as £1100000 and £100000 for running and snagging. It is

require to pay attention to operational cost. It is required to analyse the cost of operation and

management in terms of generating finance requirement form government grants and donation. It

is require to maintain separate accounts for retaining the records of staff salary and cost of tutors.

Staff salary, administration cost of £18000 of each per annum, overheads containing the cleaning

7

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

and power are also need to adjust in profit statement. It is required to purpose of planning

purpose for the working year which remain split in to a maximum of 600 staffed session.

There is an income and expenditure projection for four years are prepared which

indicates towards favourable profitability position of organisation. Evaluation of alternative

methods related to capital projects are also defined in this context. It is required to analyse the

sustainability of project for building the capacity to develop the presenting financial plans are

defined in this context. A critical analysis done in respect of determining contribution, break

even, payback period, ARR and Net present value is evaluated in effective manner. Challenges

are also defined which may occurs while re-modeling the structure of business.

CONCLUSION

This report provides a summary in respect of management and operations of financial

resources and management. There is an operational and regulatory factors are analysed and

summarised in this context. Income and expenditure projection for the first 4 year incorporated

with operational and regulatory costs are defined in this context. Financial; stability of current

proposal and alternative methods are compared. A detailed conclusion in terms of

recommendations and suggestions are provided in this report.

8

purpose for the working year which remain split in to a maximum of 600 staffed session.

There is an income and expenditure projection for four years are prepared which

indicates towards favourable profitability position of organisation. Evaluation of alternative

methods related to capital projects are also defined in this context. It is required to analyse the

sustainability of project for building the capacity to develop the presenting financial plans are

defined in this context. A critical analysis done in respect of determining contribution, break

even, payback period, ARR and Net present value is evaluated in effective manner. Challenges

are also defined which may occurs while re-modeling the structure of business.

CONCLUSION

This report provides a summary in respect of management and operations of financial

resources and management. There is an operational and regulatory factors are analysed and

summarised in this context. Income and expenditure projection for the first 4 year incorporated

with operational and regulatory costs are defined in this context. Financial; stability of current

proposal and alternative methods are compared. A detailed conclusion in terms of

recommendations and suggestions are provided in this report.

8

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

REFERENCES

Books and Journals:

Hettinger, W. S. and Dolan-Heitlinger, J., 2011. Finance Without Fear: A Guide to Creating and

Managing a Profitable Business. Inst for Finance & Entrepre.

Moffett, M. H., Stonehill, A. I. and Eiteman, D. K., 2014. Fundamentals of multinational

finance. Prentice Hall.

Mohamad, A .A. S., Mohamad, M. T. and Samsudin, M. L., 2013. How Islamic banks of

Malaysia managing liquidity? an emphasis on confronting economic

cycles. International Journal of Business and Social Science. 4(7).

Franklin II, C. L., 2011. Managing risk in operations. Journal of Management Information and

Decision Sciences. 14(2). p.117.

Reason, J., 2016. Managing the risks of organizational accidents. Routledge.

Vernimmen, P. and et. al., 2014. Corporate finance: theory and practice. John Wiley & Sons.

Sanders, N. R., 2013. The Definitive Guide to Manufacturing and Service Operations: Master the

Strategies and Tactics for Planning, Organizing, and Managing How Products and

Services Are Produced. Pearson Education.

Hillier, F. S., 2012. Introduction to operations research. Tata McGraw-Hill Education.

Thomé, A. M. T. and et. al., 2012. Sales and operations planning: A research

synthesis. International Journal of Production Economics. 138(1). pp.1-13.

Broadbent, M. and Cullen, J., 2012. Managing financial resources. Routledge.

Soumadi, M. M. and Hayajneh, O. S., 2012. Capital structure and corporate performance

empirical study on the public Jordanian shareholdings firms listed in the Amman stock

market. European Scientific Journal, ESJ, 8(22).

Drucker, P., 2012. Managing in the next society. Routledge.

9

Books and Journals:

Hettinger, W. S. and Dolan-Heitlinger, J., 2011. Finance Without Fear: A Guide to Creating and

Managing a Profitable Business. Inst for Finance & Entrepre.

Moffett, M. H., Stonehill, A. I. and Eiteman, D. K., 2014. Fundamentals of multinational

finance. Prentice Hall.

Mohamad, A .A. S., Mohamad, M. T. and Samsudin, M. L., 2013. How Islamic banks of

Malaysia managing liquidity? an emphasis on confronting economic

cycles. International Journal of Business and Social Science. 4(7).

Franklin II, C. L., 2011. Managing risk in operations. Journal of Management Information and

Decision Sciences. 14(2). p.117.

Reason, J., 2016. Managing the risks of organizational accidents. Routledge.

Vernimmen, P. and et. al., 2014. Corporate finance: theory and practice. John Wiley & Sons.

Sanders, N. R., 2013. The Definitive Guide to Manufacturing and Service Operations: Master the

Strategies and Tactics for Planning, Organizing, and Managing How Products and

Services Are Produced. Pearson Education.

Hillier, F. S., 2012. Introduction to operations research. Tata McGraw-Hill Education.

Thomé, A. M. T. and et. al., 2012. Sales and operations planning: A research

synthesis. International Journal of Production Economics. 138(1). pp.1-13.

Broadbent, M. and Cullen, J., 2012. Managing financial resources. Routledge.

Soumadi, M. M. and Hayajneh, O. S., 2012. Capital structure and corporate performance

empirical study on the public Jordanian shareholdings firms listed in the Amman stock

market. European Scientific Journal, ESJ, 8(22).

Drucker, P., 2012. Managing in the next society. Routledge.

9

1 out of 11

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.