University Finance Case 2: Options Analysis and Hedging Strategies

VerifiedAdded on 2022/08/26

|11

|1591

|31

Case Study

AI Summary

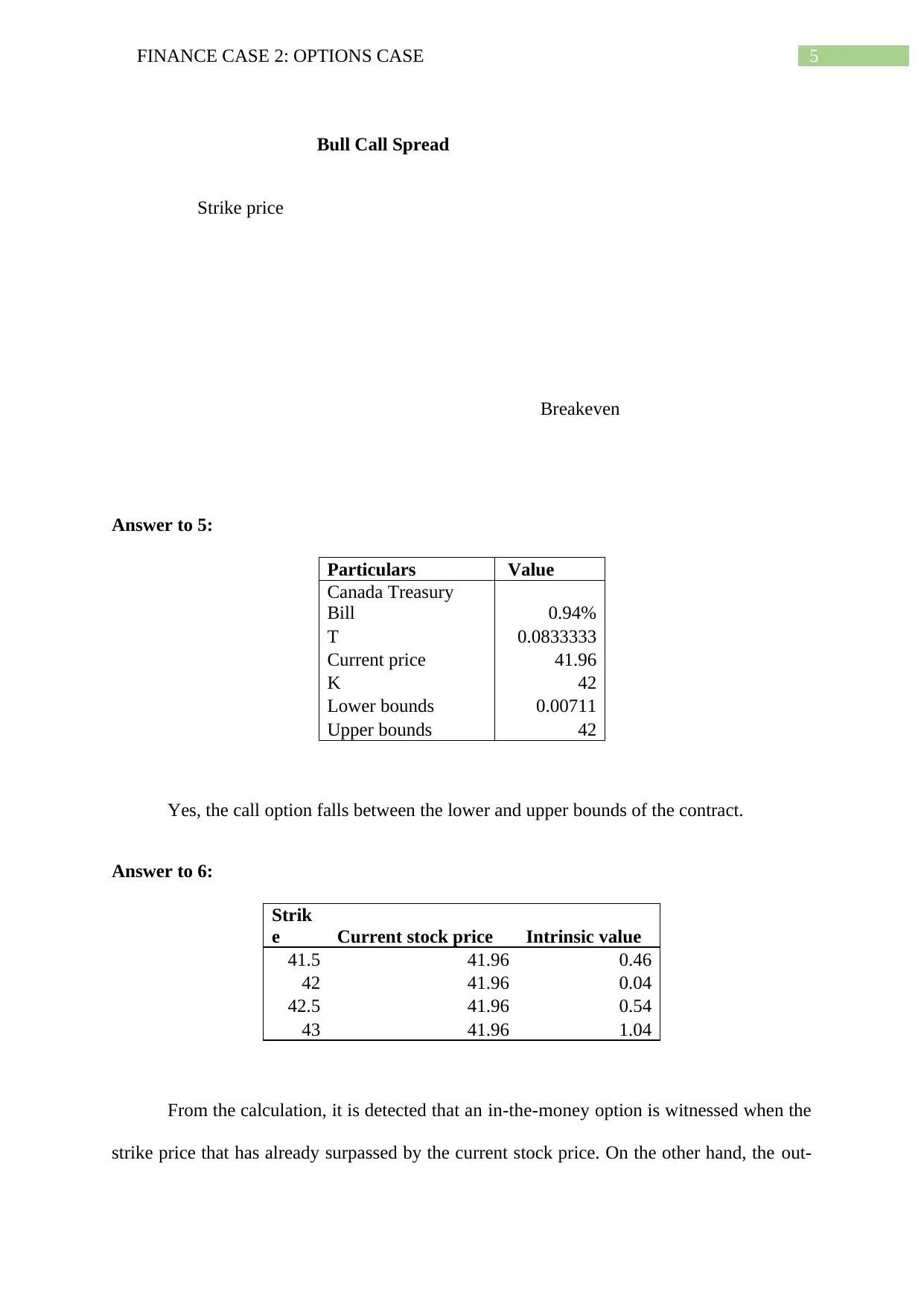

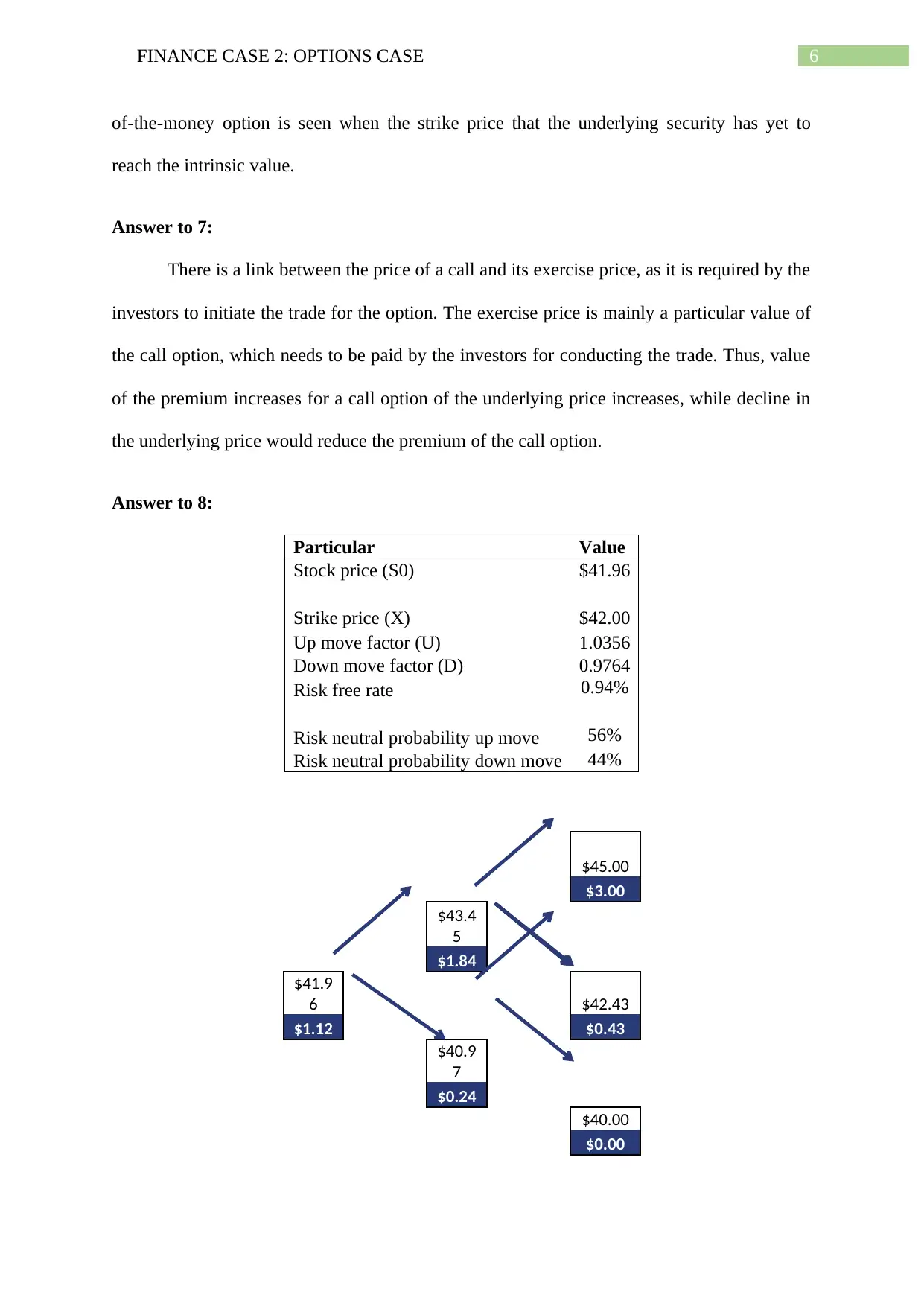

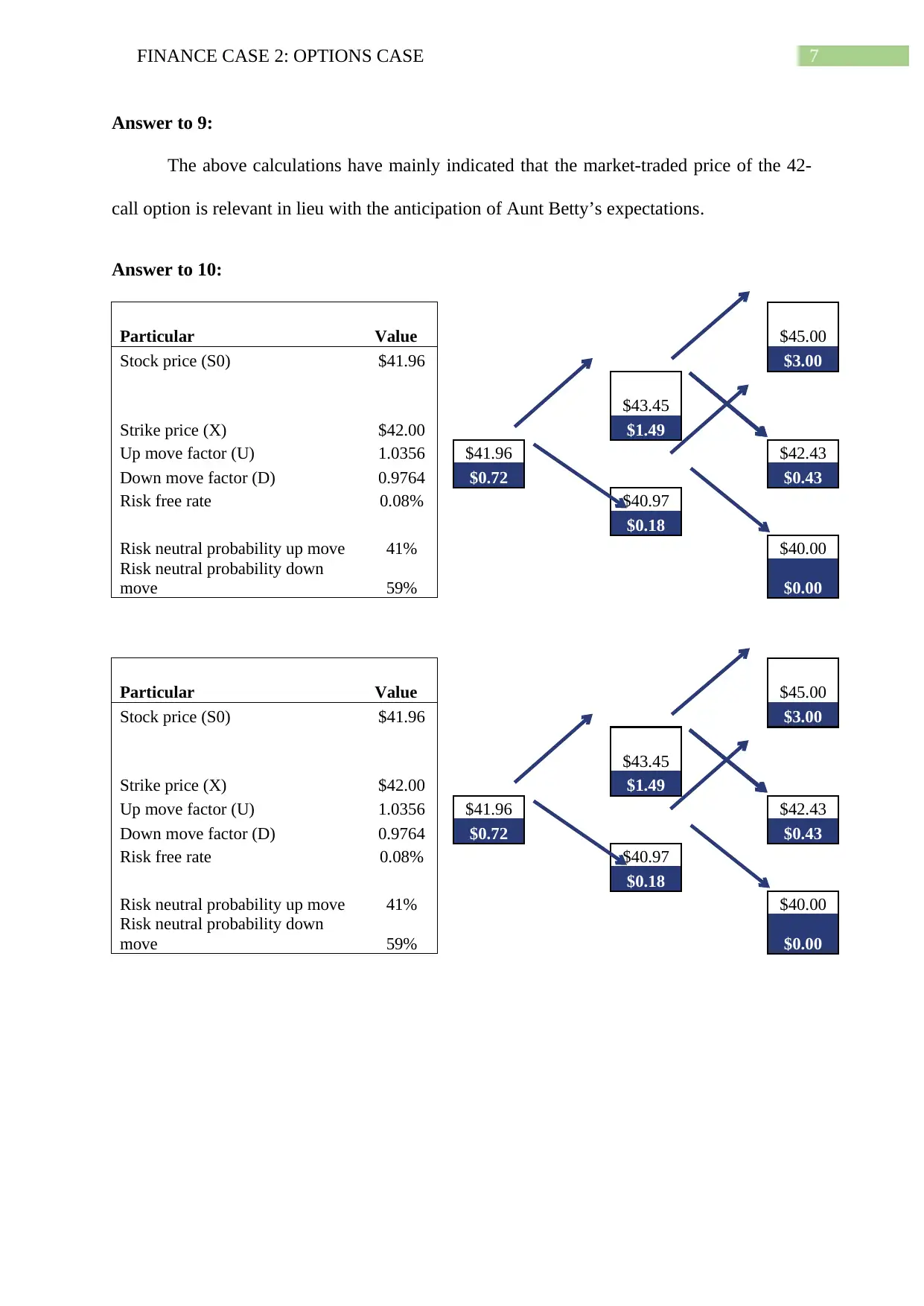

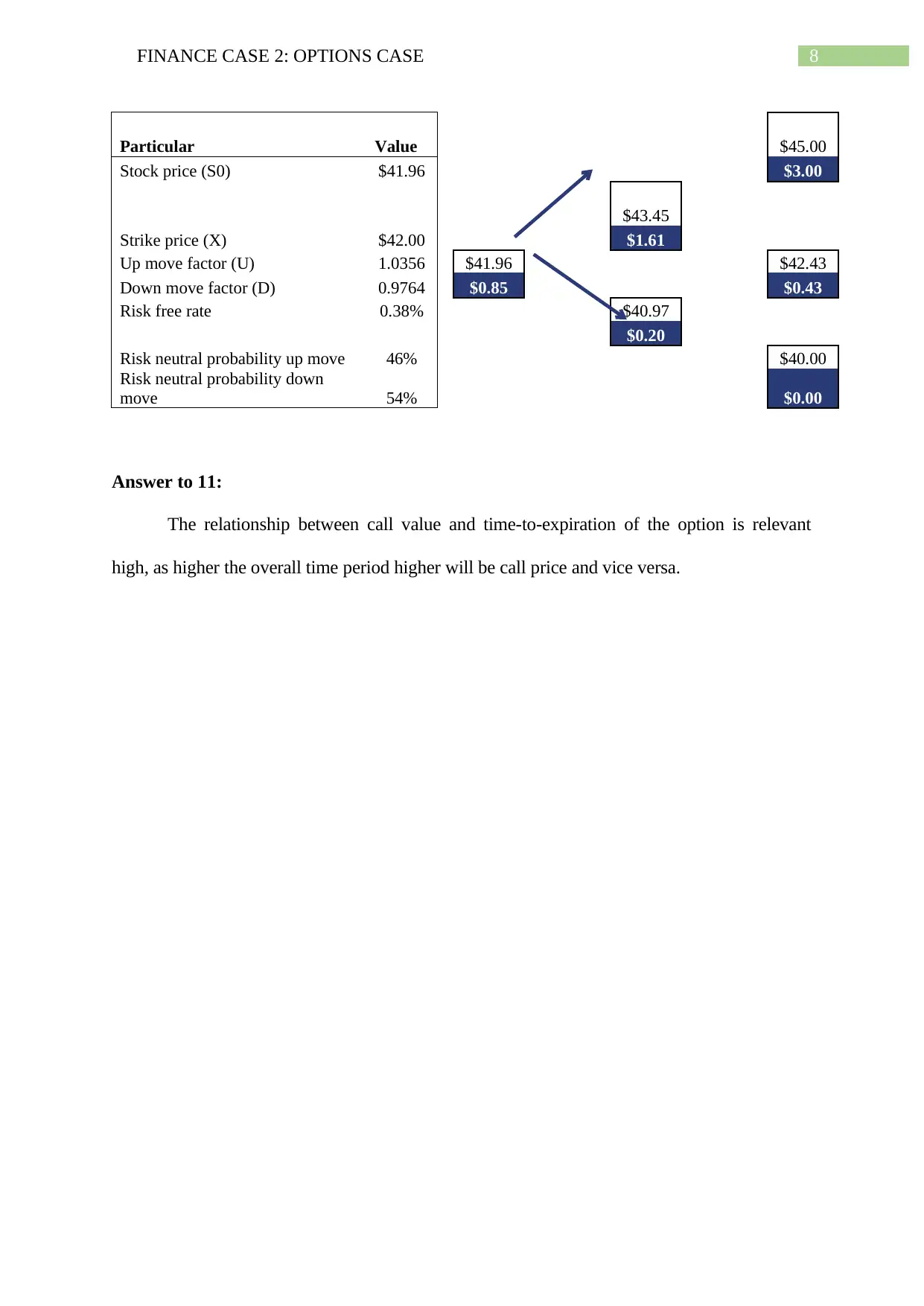

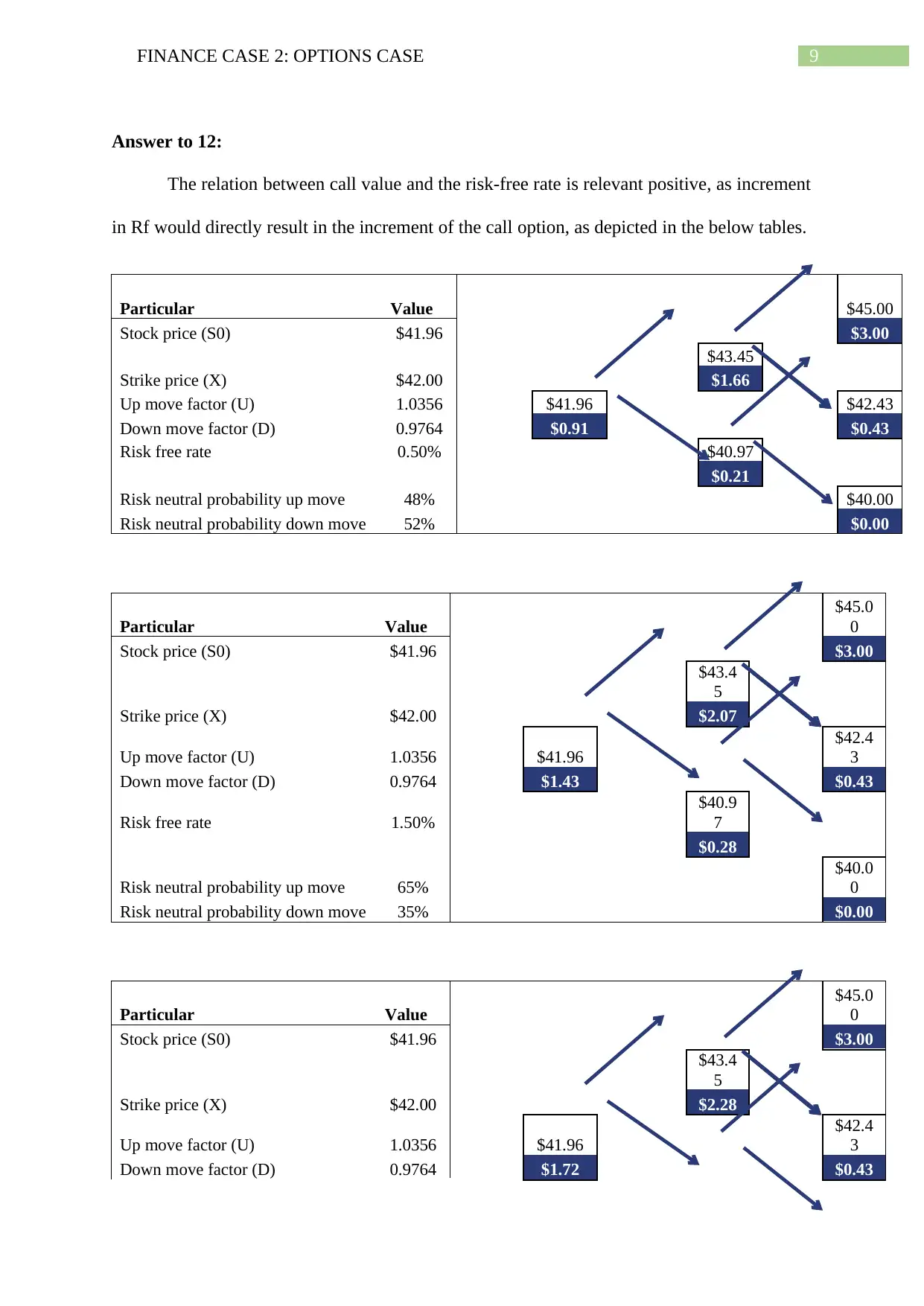

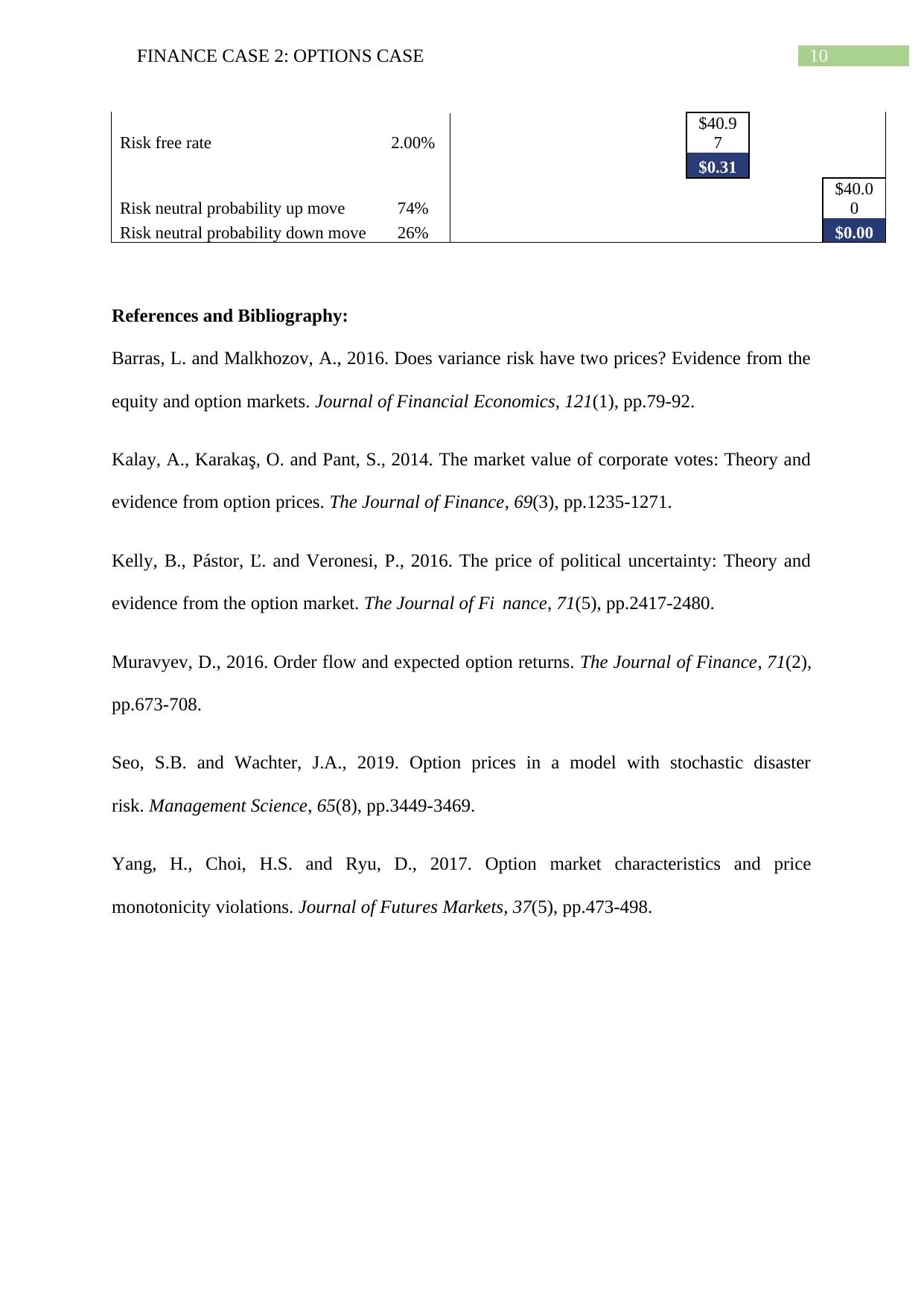

This finance case study examines Aunt Betty's investment portfolio and the use of options to mitigate risk. The analysis covers call and put options, their pricing, and how they can be used to hedge against potential losses in Suncor shares. The case study explores the impact of strike prices, current stock prices, and time to expiration on option values. Additionally, it delves into the use of futures contracts for hedging crude oil price exposure, analyzing contract details and potential hedging strategies for Canuck Oil Corporation. The document provides detailed calculations and explanations to support the analysis, offering insights into portfolio management and risk mitigation techniques. The case covers topics such as call and put options, intrinsic value, and the relationship between call value and time to expiration and risk-free rate. Finally, it evaluates the effectiveness of different hedging strategies and provides recommendations for Aunt Betty and Canuck Oil Corporation.

1 out of 11

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.