Business Finance Report: T-shirt Ltd Performance Analysis and Cash

VerifiedAdded on 2023/01/05

|12

|3327

|69

Report

AI Summary

This report provides a comprehensive analysis of business finance, focusing on the performance of T-shirt Ltd and its cash management strategies. It begins with an introduction to business financing and then delves into a detailed examination of the company's financial statements, including the profit and loss account and balance sheet. The report analyzes key financial ratios such as gross profit ratio, net profit ratio, current ratio, and receivable turnover ratio to assess the company's financial health. Furthermore, the report explores the differences between accrual and cash accounting methods, highlighting their advantages and disadvantages. It also discusses the relationship between profit and cash flow, emphasizing the importance of managing both effectively for business success. The analysis provides a clear understanding of financial statements, key ratios, and accounting methods, contributing to a deeper understanding of business finance.

Business Finance

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Table of Contents

INTRODUCTION...........................................................................................................................3

INTRODUCTION...........................................................................................................................3

INTRODUCTION

Business financing, is defined as the accumulation and administration by business

organisations of investments. The functioning of the business officer, who is typically right near

the top of a company's corporate structure, is to schedule, assess and manage activities. In this

report, two part of such as part 1 (business performance analysis) of T-shirt Ltd’s and part 2

(Understanding Financial Information & Management of Cash) is discussed.

PART 1

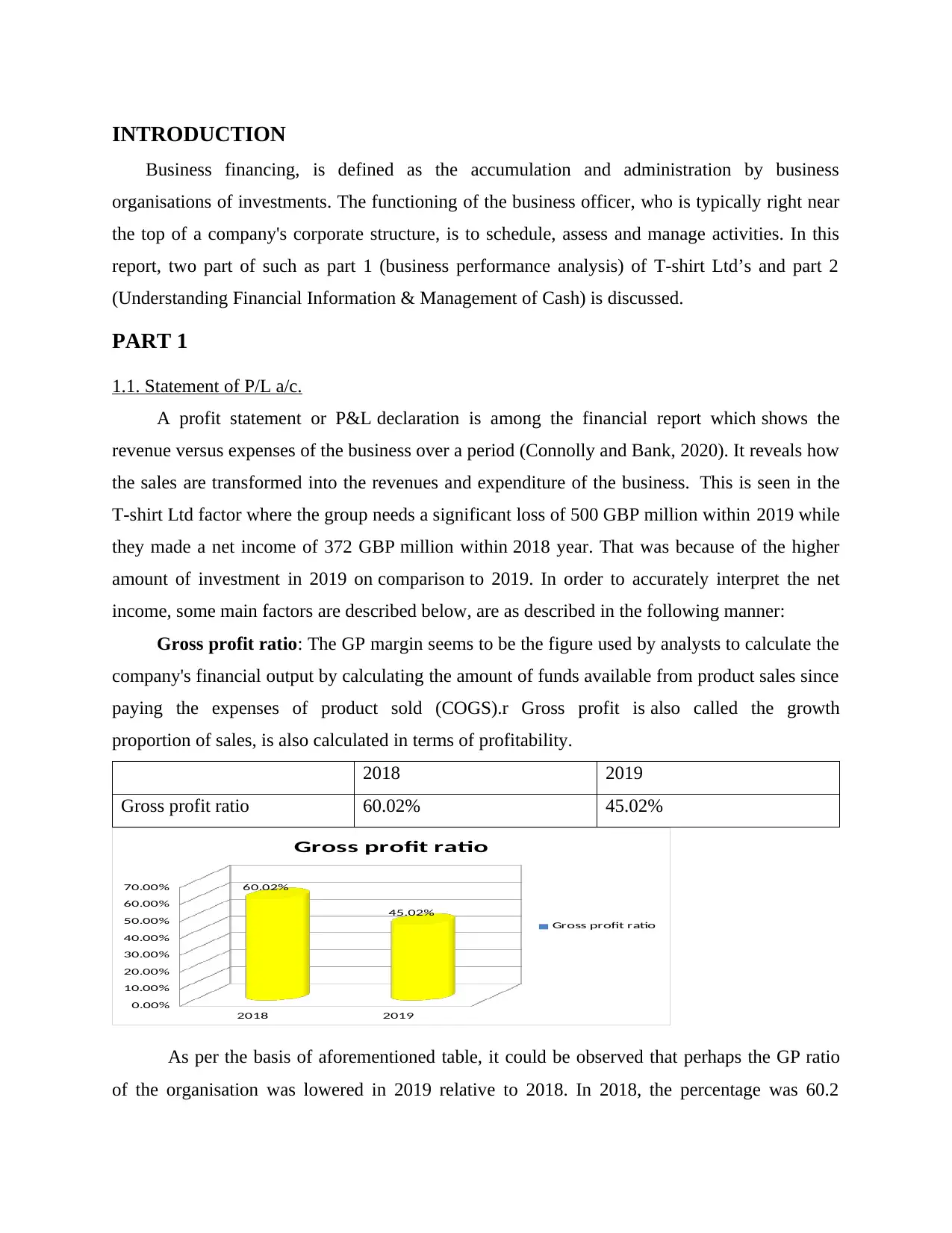

1.1. Statement of P/L a/c.

A profit statement or P&L declaration is among the financial report which shows the

revenue versus expenses of the business over a period (Connolly and Bank, 2020). It reveals how

the sales are transformed into the revenues and expenditure of the business. This is seen in the

T-shirt Ltd factor where the group needs a significant loss of 500 GBP million within 2019 while

they made a net income of 372 GBP million within 2018 year. That was because of the higher

amount of investment in 2019 on comparison to 2019. In order to accurately interpret the net

income, some main factors are described below, are as described in the following manner:

Gross profit ratio: The GP margin seems to be the figure used by analysts to calculate the

company's financial output by calculating the amount of funds available from product sales since

paying the expenses of product sold (COGS).r Gross profit is also called the growth

proportion of sales, is also calculated in terms of profitability.

2018 2019

Gross profit ratio 60.02% 45.02%

2018 2019

0.00%

10.00%

20.00%

30.00%

40.00%

50.00%

60.00%

70.00% 60.02%

45.02%

Gross profit ratio

Gross profit ratio

As per the basis of aforementioned table, it could be observed that perhaps the GP ratio

of the organisation was lowered in 2019 relative to 2018. In 2018, the percentage was 60.2

Business financing, is defined as the accumulation and administration by business

organisations of investments. The functioning of the business officer, who is typically right near

the top of a company's corporate structure, is to schedule, assess and manage activities. In this

report, two part of such as part 1 (business performance analysis) of T-shirt Ltd’s and part 2

(Understanding Financial Information & Management of Cash) is discussed.

PART 1

1.1. Statement of P/L a/c.

A profit statement or P&L declaration is among the financial report which shows the

revenue versus expenses of the business over a period (Connolly and Bank, 2020). It reveals how

the sales are transformed into the revenues and expenditure of the business. This is seen in the

T-shirt Ltd factor where the group needs a significant loss of 500 GBP million within 2019 while

they made a net income of 372 GBP million within 2018 year. That was because of the higher

amount of investment in 2019 on comparison to 2019. In order to accurately interpret the net

income, some main factors are described below, are as described in the following manner:

Gross profit ratio: The GP margin seems to be the figure used by analysts to calculate the

company's financial output by calculating the amount of funds available from product sales since

paying the expenses of product sold (COGS).r Gross profit is also called the growth

proportion of sales, is also calculated in terms of profitability.

2018 2019

Gross profit ratio 60.02% 45.02%

2018 2019

0.00%

10.00%

20.00%

30.00%

40.00%

50.00%

60.00%

70.00% 60.02%

45.02%

Gross profit ratio

Gross profit ratio

As per the basis of aforementioned table, it could be observed that perhaps the GP ratio

of the organisation was lowered in 2019 relative to 2018. In 2018, the percentage was 60.2

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

percent lower as well as 45.2 percent lower. That was because of reduced sales of products

produced in 2019 and increased costs. As well as noting that in an efficient year 2019 that is

contributing as smaller gross profit, the business is unable to control its cost.

Net profit ratio: The NP proportion is the ratio is after-tax profits to net sales. It shows

the remaining gain after all sales and approved capital gains are being withdrawn from

production, administration and finance expenses. However, it is one of the best measures of the

success in business of even a company, especially in conjunction with an assessment of how it

handles its capital investment. The variable is usually documented on a sequence map to judge

overall performance. It is also used to equate the profitability of a firm including its competitors.

2018 2019

Net profit ratio 17.71% -36.60

2018 2019

-4000.00%

-3500.00%

-3000.00%

-2500.00%

-2000.00%

-1500.00%

-1000.00%

-500.00%

0.00%

500.00% 17.71%

-36.6

Net profit ratio

Net profit ratio

As per the aforementioned table, it can be observed that perhaps the NP ratio of the

organisation was lowered in 2019 relative to 2018. The figure was 17.71 percent in 2018, which

declined and is now a -36.6 percent net negative rate. The reason for this is due to the larger

amount of costs in 2019 for administration and financing. This illustrates that the business is also

not helpful in combating its total costs and is unable to distribute its resources in an acceptable

manner.

Operating profit ratio: This margin is indeed a production or performance ratio that

reflects the level of revenue a company receives from its operations (Lewis and Liu, 2020) until

produced in 2019 and increased costs. As well as noting that in an efficient year 2019 that is

contributing as smaller gross profit, the business is unable to control its cost.

Net profit ratio: The NP proportion is the ratio is after-tax profits to net sales. It shows

the remaining gain after all sales and approved capital gains are being withdrawn from

production, administration and finance expenses. However, it is one of the best measures of the

success in business of even a company, especially in conjunction with an assessment of how it

handles its capital investment. The variable is usually documented on a sequence map to judge

overall performance. It is also used to equate the profitability of a firm including its competitors.

2018 2019

Net profit ratio 17.71% -36.60

2018 2019

-4000.00%

-3500.00%

-3000.00%

-2500.00%

-2000.00%

-1500.00%

-1000.00%

-500.00%

0.00%

500.00% 17.71%

-36.6

Net profit ratio

Net profit ratio

As per the aforementioned table, it can be observed that perhaps the NP ratio of the

organisation was lowered in 2019 relative to 2018. The figure was 17.71 percent in 2018, which

declined and is now a -36.6 percent net negative rate. The reason for this is due to the larger

amount of costs in 2019 for administration and financing. This illustrates that the business is also

not helpful in combating its total costs and is unable to distribute its resources in an acceptable

manner.

Operating profit ratio: This margin is indeed a production or performance ratio that

reflects the level of revenue a company receives from its operations (Lewis and Liu, 2020) until

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

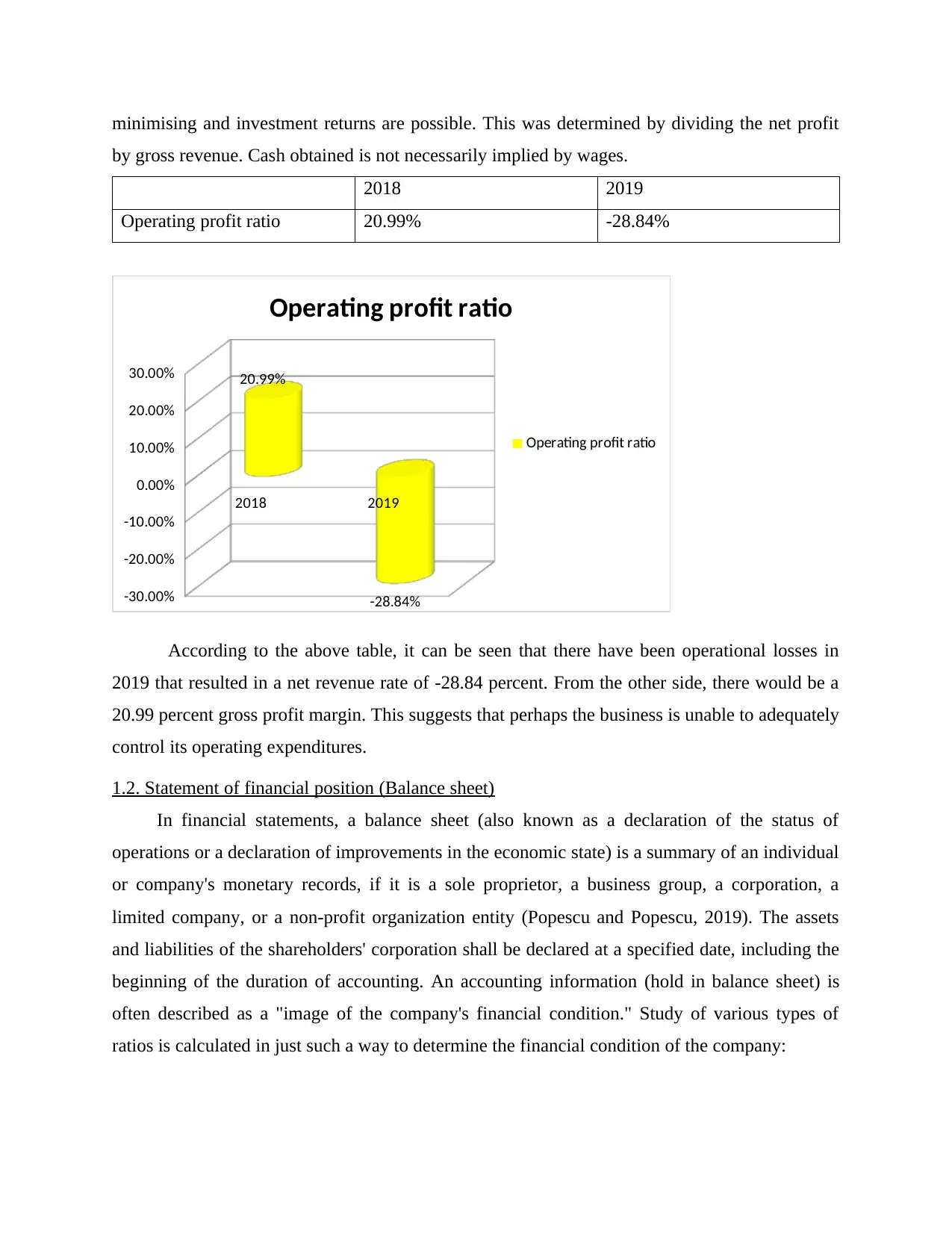

minimising and investment returns are possible. This was determined by dividing the net profit

by gross revenue. Cash obtained is not necessarily implied by wages.

2018 2019

Operating profit ratio 20.99% -28.84%

2018 2019

-30.00%

-20.00%

-10.00%

0.00%

10.00%

20.00%

30.00% 20.99%

-28.84%

Operating profit ratio

Operating profit ratio

According to the above table, it can be seen that there have been operational losses in

2019 that resulted in a net revenue rate of -28.84 percent. From the other side, there would be a

20.99 percent gross profit margin. This suggests that perhaps the business is unable to adequately

control its operating expenditures.

1.2. Statement of financial position (Balance sheet)

In financial statements, a balance sheet (also known as a declaration of the status of

operations or a declaration of improvements in the economic state) is a summary of an individual

or company's monetary records, if it is a sole proprietor, a business group, a corporation, a

limited company, or a non-profit organization entity (Popescu and Popescu, 2019). The assets

and liabilities of the shareholders' corporation shall be declared at a specified date, including the

beginning of the duration of accounting. An accounting information (hold in balance sheet) is

often described as a "image of the company's financial condition." Study of various types of

ratios is calculated in just such a way to determine the financial condition of the company:

by gross revenue. Cash obtained is not necessarily implied by wages.

2018 2019

Operating profit ratio 20.99% -28.84%

2018 2019

-30.00%

-20.00%

-10.00%

0.00%

10.00%

20.00%

30.00% 20.99%

-28.84%

Operating profit ratio

Operating profit ratio

According to the above table, it can be seen that there have been operational losses in

2019 that resulted in a net revenue rate of -28.84 percent. From the other side, there would be a

20.99 percent gross profit margin. This suggests that perhaps the business is unable to adequately

control its operating expenditures.

1.2. Statement of financial position (Balance sheet)

In financial statements, a balance sheet (also known as a declaration of the status of

operations or a declaration of improvements in the economic state) is a summary of an individual

or company's monetary records, if it is a sole proprietor, a business group, a corporation, a

limited company, or a non-profit organization entity (Popescu and Popescu, 2019). The assets

and liabilities of the shareholders' corporation shall be declared at a specified date, including the

beginning of the duration of accounting. An accounting information (hold in balance sheet) is

often described as a "image of the company's financial condition." Study of various types of

ratios is calculated in just such a way to determine the financial condition of the company:

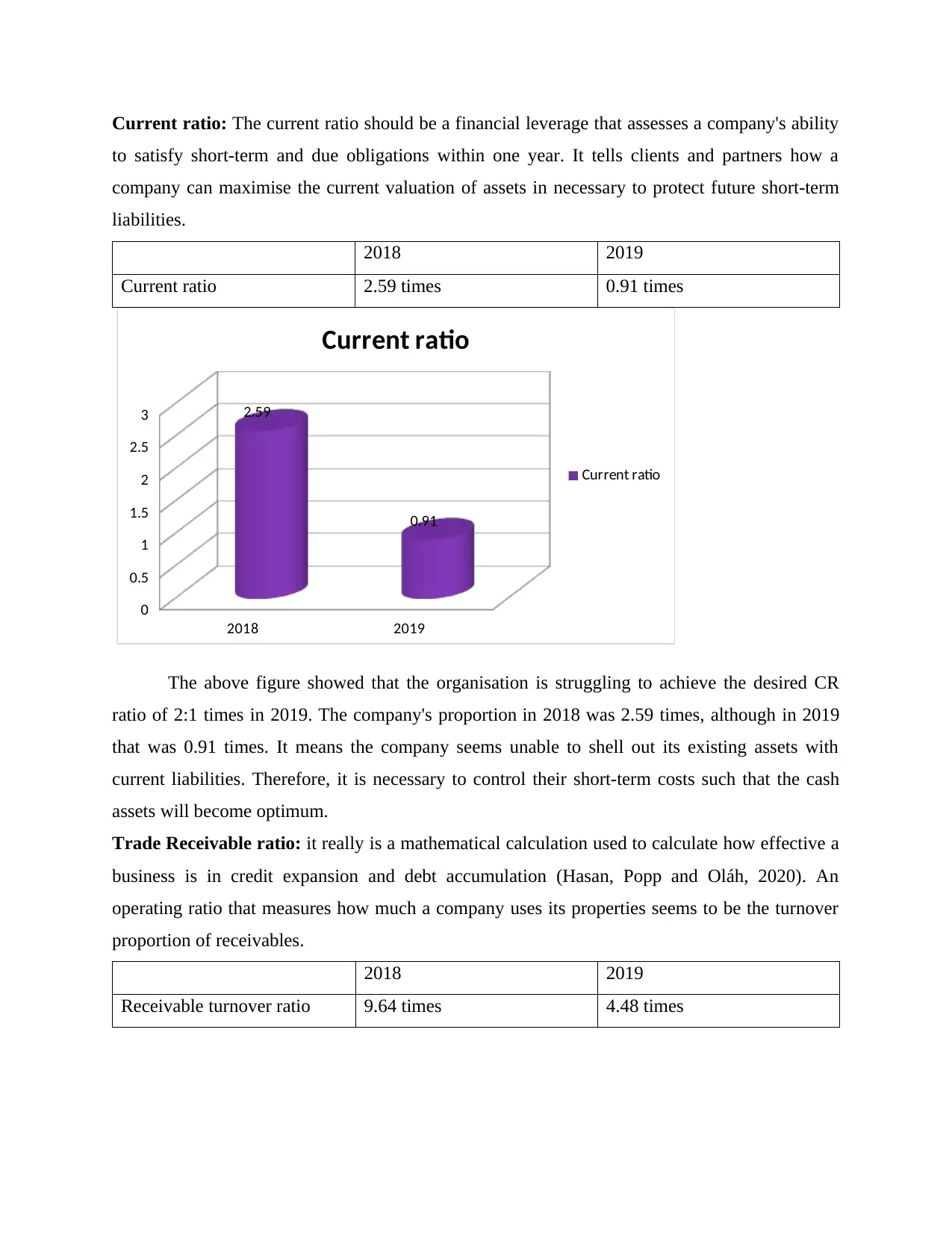

Current ratio: The current ratio should be a financial leverage that assesses a company's ability

to satisfy short-term and due obligations within one year. It tells clients and partners how a

company can maximise the current valuation of assets in necessary to protect future short-term

liabilities.

2018 2019

Current ratio 2.59 times 0.91 times

2018 2019

0

0.5

1

1.5

2

2.5

3 2.59

0.91

Current ratio

Current ratio

The above figure showed that the organisation is struggling to achieve the desired CR

ratio of 2:1 times in 2019. The company's proportion in 2018 was 2.59 times, although in 2019

that was 0.91 times. It means the company seems unable to shell out its existing assets with

current liabilities. Therefore, it is necessary to control their short-term costs such that the cash

assets will become optimum.

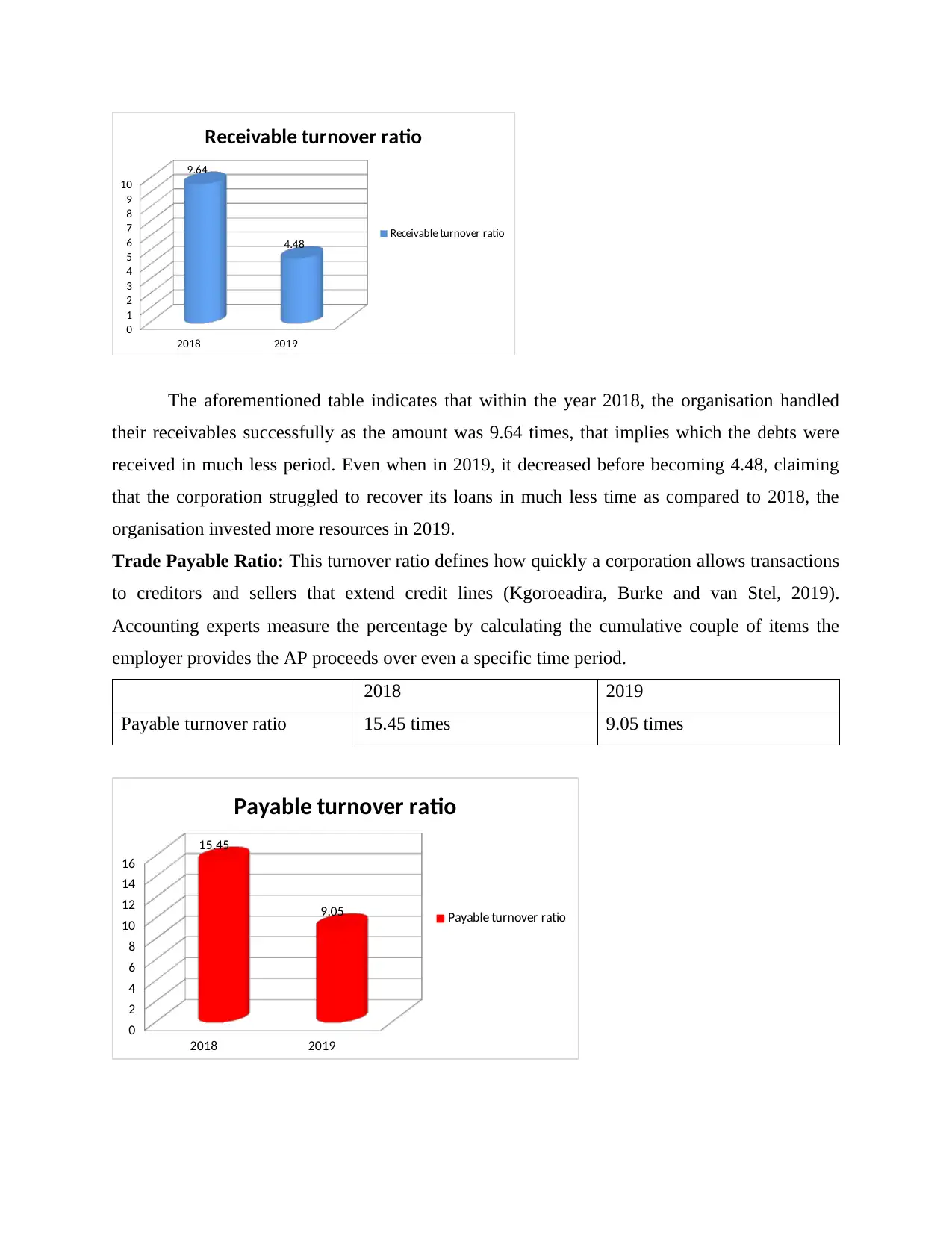

Trade Receivable ratio: it really is a mathematical calculation used to calculate how effective a

business is in credit expansion and debt accumulation (Hasan, Popp and Oláh, 2020). An

operating ratio that measures how much a company uses its properties seems to be the turnover

proportion of receivables.

2018 2019

Receivable turnover ratio 9.64 times 4.48 times

to satisfy short-term and due obligations within one year. It tells clients and partners how a

company can maximise the current valuation of assets in necessary to protect future short-term

liabilities.

2018 2019

Current ratio 2.59 times 0.91 times

2018 2019

0

0.5

1

1.5

2

2.5

3 2.59

0.91

Current ratio

Current ratio

The above figure showed that the organisation is struggling to achieve the desired CR

ratio of 2:1 times in 2019. The company's proportion in 2018 was 2.59 times, although in 2019

that was 0.91 times. It means the company seems unable to shell out its existing assets with

current liabilities. Therefore, it is necessary to control their short-term costs such that the cash

assets will become optimum.

Trade Receivable ratio: it really is a mathematical calculation used to calculate how effective a

business is in credit expansion and debt accumulation (Hasan, Popp and Oláh, 2020). An

operating ratio that measures how much a company uses its properties seems to be the turnover

proportion of receivables.

2018 2019

Receivable turnover ratio 9.64 times 4.48 times

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

2018 2019

0

1

2

3

4

5

6

7

8

9

10

9.64

4.48

Receivable turnover ratio

Receivable turnover ratio

The aforementioned table indicates that within the year 2018, the organisation handled

their receivables successfully as the amount was 9.64 times, that implies which the debts were

received in much less period. Even when in 2019, it decreased before becoming 4.48, claiming

that the corporation struggled to recover its loans in much less time as compared to 2018, the

organisation invested more resources in 2019.

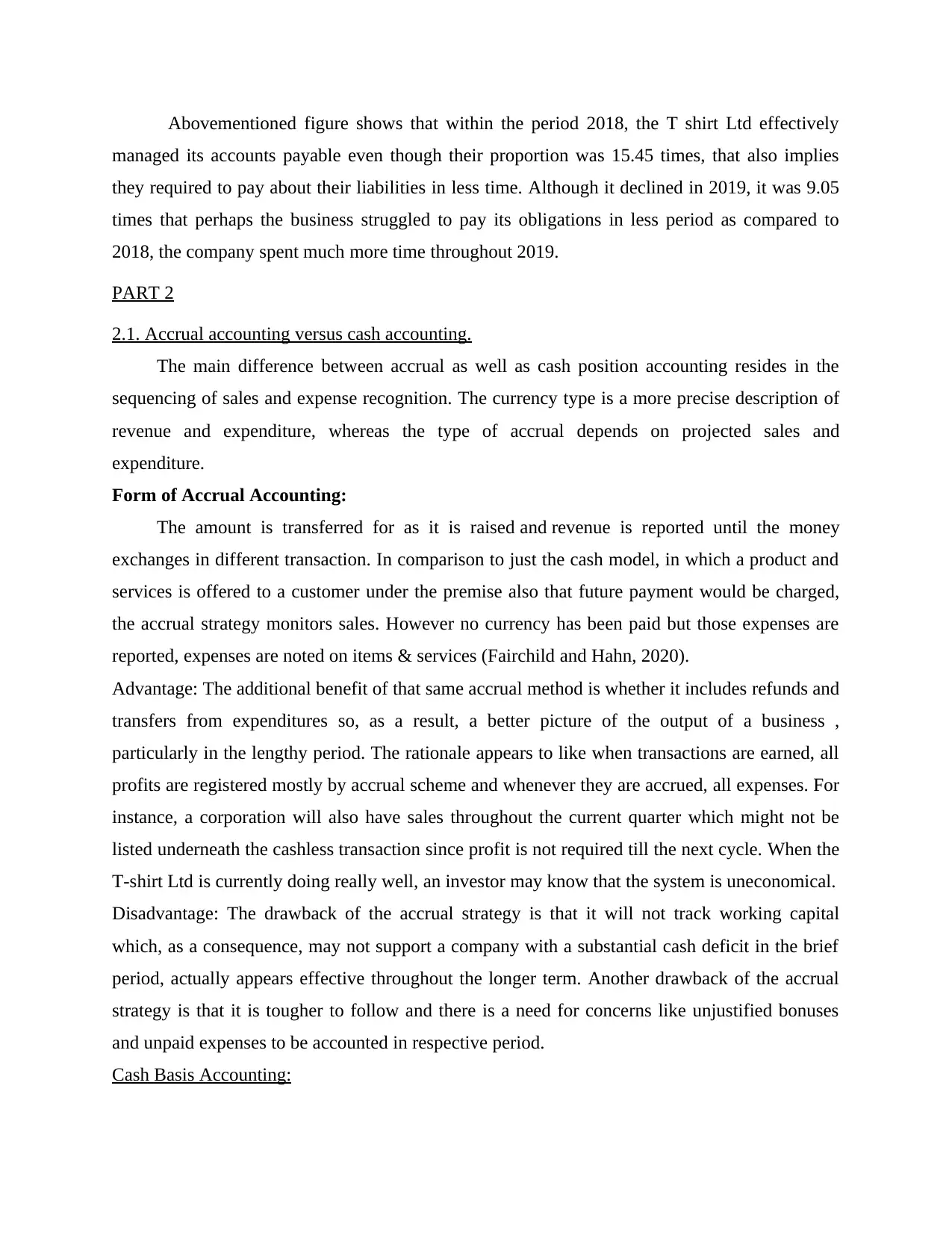

Trade Payable Ratio: This turnover ratio defines how quickly a corporation allows transactions

to creditors and sellers that extend credit lines (Kgoroeadira, Burke and van Stel, 2019).

Accounting experts measure the percentage by calculating the cumulative couple of items the

employer provides the AP proceeds over even a specific time period.

2018 2019

Payable turnover ratio 15.45 times 9.05 times

2018 2019

0

2

4

6

8

10

12

14

16

15.45

9.05

Payable turnover ratio

Payable turnover ratio

0

1

2

3

4

5

6

7

8

9

10

9.64

4.48

Receivable turnover ratio

Receivable turnover ratio

The aforementioned table indicates that within the year 2018, the organisation handled

their receivables successfully as the amount was 9.64 times, that implies which the debts were

received in much less period. Even when in 2019, it decreased before becoming 4.48, claiming

that the corporation struggled to recover its loans in much less time as compared to 2018, the

organisation invested more resources in 2019.

Trade Payable Ratio: This turnover ratio defines how quickly a corporation allows transactions

to creditors and sellers that extend credit lines (Kgoroeadira, Burke and van Stel, 2019).

Accounting experts measure the percentage by calculating the cumulative couple of items the

employer provides the AP proceeds over even a specific time period.

2018 2019

Payable turnover ratio 15.45 times 9.05 times

2018 2019

0

2

4

6

8

10

12

14

16

15.45

9.05

Payable turnover ratio

Payable turnover ratio

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Abovementioned figure shows that within the period 2018, the T shirt Ltd effectively

managed its accounts payable even though their proportion was 15.45 times, that also implies

they required to pay about their liabilities in less time. Although it declined in 2019, it was 9.05

times that perhaps the business struggled to pay its obligations in less period as compared to

2018, the company spent much more time throughout 2019.

PART 2

2.1. Accrual accounting versus cash accounting.

The main difference between accrual as well as cash position accounting resides in the

sequencing of sales and expense recognition. The currency type is a more precise description of

revenue and expenditure, whereas the type of accrual depends on projected sales and

expenditure.

Form of Accrual Accounting:

The amount is transferred for as it is raised and revenue is reported until the money

exchanges in different transaction. In comparison to just the cash model, in which a product and

services is offered to a customer under the premise also that future payment would be charged,

the accrual strategy monitors sales. However no currency has been paid but those expenses are

reported, expenses are noted on items & services (Fairchild and Hahn, 2020).

Advantage: The additional benefit of that same accrual method is whether it includes refunds and

transfers from expenditures so, as a result, a better picture of the output of a business ,

particularly in the lengthy period. The rationale appears to like when transactions are earned, all

profits are registered mostly by accrual scheme and whenever they are accrued, all expenses. For

instance, a corporation will also have sales throughout the current quarter which might not be

listed underneath the cashless transaction since profit is not required till the next cycle. When the

T-shirt Ltd is currently doing really well, an investor may know that the system is uneconomical.

Disadvantage: The drawback of the accrual strategy is that it will not track working capital

which, as a consequence, may not support a company with a substantial cash deficit in the brief

period, actually appears effective throughout the longer term. Another drawback of the accrual

strategy is that it is tougher to follow and there is a need for concerns like unjustified bonuses

and unpaid expenses to be accounted in respective period.

Cash Basis Accounting:

managed its accounts payable even though their proportion was 15.45 times, that also implies

they required to pay about their liabilities in less time. Although it declined in 2019, it was 9.05

times that perhaps the business struggled to pay its obligations in less period as compared to

2018, the company spent much more time throughout 2019.

PART 2

2.1. Accrual accounting versus cash accounting.

The main difference between accrual as well as cash position accounting resides in the

sequencing of sales and expense recognition. The currency type is a more precise description of

revenue and expenditure, whereas the type of accrual depends on projected sales and

expenditure.

Form of Accrual Accounting:

The amount is transferred for as it is raised and revenue is reported until the money

exchanges in different transaction. In comparison to just the cash model, in which a product and

services is offered to a customer under the premise also that future payment would be charged,

the accrual strategy monitors sales. However no currency has been paid but those expenses are

reported, expenses are noted on items & services (Fairchild and Hahn, 2020).

Advantage: The additional benefit of that same accrual method is whether it includes refunds and

transfers from expenditures so, as a result, a better picture of the output of a business ,

particularly in the lengthy period. The rationale appears to like when transactions are earned, all

profits are registered mostly by accrual scheme and whenever they are accrued, all expenses. For

instance, a corporation will also have sales throughout the current quarter which might not be

listed underneath the cashless transaction since profit is not required till the next cycle. When the

T-shirt Ltd is currently doing really well, an investor may know that the system is uneconomical.

Disadvantage: The drawback of the accrual strategy is that it will not track working capital

which, as a consequence, may not support a company with a substantial cash deficit in the brief

period, actually appears effective throughout the longer term. Another drawback of the accrual

strategy is that it is tougher to follow and there is a need for concerns like unjustified bonuses

and unpaid expenses to be accounted in respective period.

Cash Basis Accounting:

Money is expressed throughout the financial report only after payment is paid. Expenses are

recorded only when income is earned (Donald, 2020). The cash form is also used for tiny

entrepreneurs and also for financial wellbeing.

Advantage: The biggest advantage including the cash policy is its productivity. it pays only for

expended or won cash and measuring the cash flow of a company is much better in the goods

receipt.

Disadvantage: The drawback to the cash strategy being that it may overestimate the efficiency of

a organisation holding much cash with large amounts of financial documents that far exceed the

cash, mainly on reports and the company's real income stream. An investor may assume because

when, in reality, the firms makes a loss, the firm makes a lot of money.

EXAMPLE:

For instance, an individual owns a company that sells machinery. Throughout the cash system, if

a person buys machinery costing $5,000, the amount is also not listed in the records before the

customer takes the money or collects the payment. The $5,000 is directly notified as revenue

throughout the accrual phase because after booking is done, even when the customer collects

some cash some very weeks and months after. The same principle holds for prices. In the

relevant purchase, unless the company pays a $1,700 electricity bill, the balance is not recorded

as an expense till the bill is paid by the purchaser. The $1,700 is, however, listed as an expense

on the day you receive the invoice underneath the accrual scheme.

2.2 Profit and Cash flow

The primary difference between working capital as well as profit amount would be that

income is really the amount / image remaining in after company costs are provided, while

investment returns reflect the total value of working capital that comes in and goes bankrupt

(Ambadkar, 2020).

Cash is increasingly moving in and out of company as well. For example , if a company

buys stock, capital is sent to its suppliers from a commercial business. Cash flows further into

business through its customers since the same distributor sells this from inventory. Income

contributes to the receivable / debtors funds as the company spends its payroll or electrical bills.

If the merchant collects a monthly payout for the transaction funded by the customer 10 months

earlier, future profits in to business will arise.

recorded only when income is earned (Donald, 2020). The cash form is also used for tiny

entrepreneurs and also for financial wellbeing.

Advantage: The biggest advantage including the cash policy is its productivity. it pays only for

expended or won cash and measuring the cash flow of a company is much better in the goods

receipt.

Disadvantage: The drawback to the cash strategy being that it may overestimate the efficiency of

a organisation holding much cash with large amounts of financial documents that far exceed the

cash, mainly on reports and the company's real income stream. An investor may assume because

when, in reality, the firms makes a loss, the firm makes a lot of money.

EXAMPLE:

For instance, an individual owns a company that sells machinery. Throughout the cash system, if

a person buys machinery costing $5,000, the amount is also not listed in the records before the

customer takes the money or collects the payment. The $5,000 is directly notified as revenue

throughout the accrual phase because after booking is done, even when the customer collects

some cash some very weeks and months after. The same principle holds for prices. In the

relevant purchase, unless the company pays a $1,700 electricity bill, the balance is not recorded

as an expense till the bill is paid by the purchaser. The $1,700 is, however, listed as an expense

on the day you receive the invoice underneath the accrual scheme.

2.2 Profit and Cash flow

The primary difference between working capital as well as profit amount would be that

income is really the amount / image remaining in after company costs are provided, while

investment returns reflect the total value of working capital that comes in and goes bankrupt

(Ambadkar, 2020).

Cash is increasingly moving in and out of company as well. For example , if a company

buys stock, capital is sent to its suppliers from a commercial business. Cash flows further into

business through its customers since the same distributor sells this from inventory. Income

contributes to the receivable / debtors funds as the company spends its payroll or electrical bills.

If the merchant collects a monthly payout for the transaction funded by the customer 10 months

earlier, future profits in to business will arise.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Profits are described as the sum that remains after most of another company's operating

expenses are removed from profits. After the books are locked and the expenses are deducted

from the profits, that was what was left over. Profit will either be charged to business investors

and creditors, mostly by the payment of dividends, but it can also be got-invested in the business

operation. For example, revenues could be used to purchase new inventory for a business to sell

or finance research on new products and services (Hsuan-Chi, 2019).

3.1 Budget and purpose of planning

The budget involves a strategic planning / plan, articulated in monetary / quantitative

principles, generally in analysis and business, over a given time, such as a monthly or even a

year. Often companies refer to a budgetary budget as a benefit policy because it reveals the

planned costs that the company undertakes to conduct in its duty centres in order to achieve its

profit goals.

Budget is a organised mathematical description of administrative strategies in Charles

Horngren's claims. CIMA describes expenditures plan as a specific plan / proposed plan

calculated in numerical terms, planned and approved before every specified time, usually

showing the estimated income to be generated as well as expense to be invested during that time

span and the funds that will be used to achieve in respective time. The main purpose of Budget is

discussed below:

Budget is aid with shorter term plans / projects to be planned and handled.

This is a mechanism for distributing these commitments to the management of the

accountability centre.

Spending plan is the way leadership is motivated to meet the aims of their transparency

centres.

This is indeed a point of reference for this on-going activities monitoring (BÚT, 2019).

An appropriate basis for the evaluation of the effectiveness of the Performance Structures

as well as their managers is an expenditure schedule.

It is a means of educating an organisation's managers.

Standard effective planning expenses would harmonise to make planning and control

more effective in the right system.

expenses are removed from profits. After the books are locked and the expenses are deducted

from the profits, that was what was left over. Profit will either be charged to business investors

and creditors, mostly by the payment of dividends, but it can also be got-invested in the business

operation. For example, revenues could be used to purchase new inventory for a business to sell

or finance research on new products and services (Hsuan-Chi, 2019).

3.1 Budget and purpose of planning

The budget involves a strategic planning / plan, articulated in monetary / quantitative

principles, generally in analysis and business, over a given time, such as a monthly or even a

year. Often companies refer to a budgetary budget as a benefit policy because it reveals the

planned costs that the company undertakes to conduct in its duty centres in order to achieve its

profit goals.

Budget is a organised mathematical description of administrative strategies in Charles

Horngren's claims. CIMA describes expenditures plan as a specific plan / proposed plan

calculated in numerical terms, planned and approved before every specified time, usually

showing the estimated income to be generated as well as expense to be invested during that time

span and the funds that will be used to achieve in respective time. The main purpose of Budget is

discussed below:

Budget is aid with shorter term plans / projects to be planned and handled.

This is a mechanism for distributing these commitments to the management of the

accountability centre.

Spending plan is the way leadership is motivated to meet the aims of their transparency

centres.

This is indeed a point of reference for this on-going activities monitoring (BÚT, 2019).

An appropriate basis for the evaluation of the effectiveness of the Performance Structures

as well as their managers is an expenditure schedule.

It is a means of educating an organisation's managers.

Standard effective planning expenses would harmonise to make planning and control

more effective in the right system.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

3.3 Benefit of making Limited company

Across all shapes and sizes of industry the company offers, limited business is perhaps the most

popular legal category. This is due to the many technological and economic incentives it

delivers, each of which go well beyond those provided to independent retailers or consultants

working under the organisation.

The greatest benefit of starting Private Corporation is the freedom of personal company.

Simple language, if company is in trouble, owners' private properties will be secure. This is

because a limited partnership is deemed to be a separate legislative entity and its own legal

'individual'. As a consequence, the organisation is completely different than people who purchase

and operate it. "Any debt, obligations or legal conflict affecting the company is the responsibility

of the company itself, rarely of all the owners (stockholders / guarantees) or managers (Gordon,

2019). In the UK, limited firms currently pay just 19% corporation tax on revenue, while sole

traders face 20-45% business taxes on income. Which gives financial tax preparation more

flexibility. Instead of taking all the money available for each year and applying excessive

personal income taxes on top of the global tax requirement, one can retain the excess profits of

their business to cover for future operating expenditures and growth. This gives more sense than

removing all revenues, paying higher income taxes as well as investing that money the remaining

funds when additional revenue is needed by the business.

CONCLUSION

In the end of report, it concluded that corporation's stock on the Exchange trading site and

this is a fantastic way for a company to advance its growth and extension. This encourages a

company to collect capital while strengthening its structure and prestige. This provides liquidity

for consumers and helps the issuer's compliance and exchange of securities to be easily regulated

in the interests of shareholders.

Across all shapes and sizes of industry the company offers, limited business is perhaps the most

popular legal category. This is due to the many technological and economic incentives it

delivers, each of which go well beyond those provided to independent retailers or consultants

working under the organisation.

The greatest benefit of starting Private Corporation is the freedom of personal company.

Simple language, if company is in trouble, owners' private properties will be secure. This is

because a limited partnership is deemed to be a separate legislative entity and its own legal

'individual'. As a consequence, the organisation is completely different than people who purchase

and operate it. "Any debt, obligations or legal conflict affecting the company is the responsibility

of the company itself, rarely of all the owners (stockholders / guarantees) or managers (Gordon,

2019). In the UK, limited firms currently pay just 19% corporation tax on revenue, while sole

traders face 20-45% business taxes on income. Which gives financial tax preparation more

flexibility. Instead of taking all the money available for each year and applying excessive

personal income taxes on top of the global tax requirement, one can retain the excess profits of

their business to cover for future operating expenditures and growth. This gives more sense than

removing all revenues, paying higher income taxes as well as investing that money the remaining

funds when additional revenue is needed by the business.

CONCLUSION

In the end of report, it concluded that corporation's stock on the Exchange trading site and

this is a fantastic way for a company to advance its growth and extension. This encourages a

company to collect capital while strengthening its structure and prestige. This provides liquidity

for consumers and helps the issuer's compliance and exchange of securities to be easily regulated

in the interests of shareholders.

References

Book and Journals

Ambadkar, N., 2020. RECENT TRENDS IN BUSINESS FINANCE.

Hsuan-Chi, C., 2019. Introduction to the special issue of “Business Finance and Enterprise

Management”. Asia Pacific Management Review, 24(1), p.60.

BÚT, T.Đ., 2019. The Right to Autonomy in Business Finance in the National Financial Strategy

for the Years 2001-2010. Journal of Economic Development, pp.11-13.

Gordon, H., 2019. EMERGING TRENDS IN BUSINESS FINANCE: AFIA

PERSPECTIVE. AJAF, (2), pp.37-44.

Connolly, E. and Bank, J., 2020. Access to small business finance. RBA Bulletin, September,

viewed, 10.

Lewis, M. and Liu, Q., 2020. The COVID-19 Outbreak and Access to Small Business

Finance. 1. 1 Managing the Risks of Holding Self-securitisations as Collateral 2. 11

Government Bond Market Functioning and COVID-19 3. The Economic Effects of Low

Interest Rates and Unconventional 21 Monetary Policy 4. Retail Central Bank Digital

Currency: Design Considerations, Rationales, p.58.

Popescu, C.R.G. and Popescu, G.N., 2019. An exploratory study based on a questionnaire

concerning green and sustainable finance, corporate social responsibility, and

performance: Evidence from the Romanian business environment. Journal of Risk and

Financial Management, 12(4), p.162.

Kgoroeadira, R., Burke, A. and van Stel, A., 2019. Small business online loan crowdfunding:

who gets funded and what determines the rate of interest?. Small Business

Economics, 52(1), pp.67-87.

Fairchild, C. and Hahn, W., 2020. Accounting and finance majors outperform other majors on

the major field test in business and the Comprehensive Business Exam: An analysis of

exam performance drivers. Journal of Education for Business, 95(6), pp.345-350.

Donald, D.C., 2020. Smart precision finance for small businesses funding. European Business

Organization Law Review, pp.1-19.

Hasan, M.M., Popp, J. and Oláh, J., 2020. Current landscape and influence of big data on

finance. Journal of Big Data, 7(1), pp.1-17.

Book and Journals

Ambadkar, N., 2020. RECENT TRENDS IN BUSINESS FINANCE.

Hsuan-Chi, C., 2019. Introduction to the special issue of “Business Finance and Enterprise

Management”. Asia Pacific Management Review, 24(1), p.60.

BÚT, T.Đ., 2019. The Right to Autonomy in Business Finance in the National Financial Strategy

for the Years 2001-2010. Journal of Economic Development, pp.11-13.

Gordon, H., 2019. EMERGING TRENDS IN BUSINESS FINANCE: AFIA

PERSPECTIVE. AJAF, (2), pp.37-44.

Connolly, E. and Bank, J., 2020. Access to small business finance. RBA Bulletin, September,

viewed, 10.

Lewis, M. and Liu, Q., 2020. The COVID-19 Outbreak and Access to Small Business

Finance. 1. 1 Managing the Risks of Holding Self-securitisations as Collateral 2. 11

Government Bond Market Functioning and COVID-19 3. The Economic Effects of Low

Interest Rates and Unconventional 21 Monetary Policy 4. Retail Central Bank Digital

Currency: Design Considerations, Rationales, p.58.

Popescu, C.R.G. and Popescu, G.N., 2019. An exploratory study based on a questionnaire

concerning green and sustainable finance, corporate social responsibility, and

performance: Evidence from the Romanian business environment. Journal of Risk and

Financial Management, 12(4), p.162.

Kgoroeadira, R., Burke, A. and van Stel, A., 2019. Small business online loan crowdfunding:

who gets funded and what determines the rate of interest?. Small Business

Economics, 52(1), pp.67-87.

Fairchild, C. and Hahn, W., 2020. Accounting and finance majors outperform other majors on

the major field test in business and the Comprehensive Business Exam: An analysis of

exam performance drivers. Journal of Education for Business, 95(6), pp.345-350.

Donald, D.C., 2020. Smart precision finance for small businesses funding. European Business

Organization Law Review, pp.1-19.

Hasan, M.M., Popp, J. and Oláh, J., 2020. Current landscape and influence of big data on

finance. Journal of Big Data, 7(1), pp.1-17.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 12

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.