Analysis of GST Registration, Budgeting, and Performance for ICL Cafe

VerifiedAdded on 2022/11/18

|5

|844

|79

Homework Assignment

AI Summary

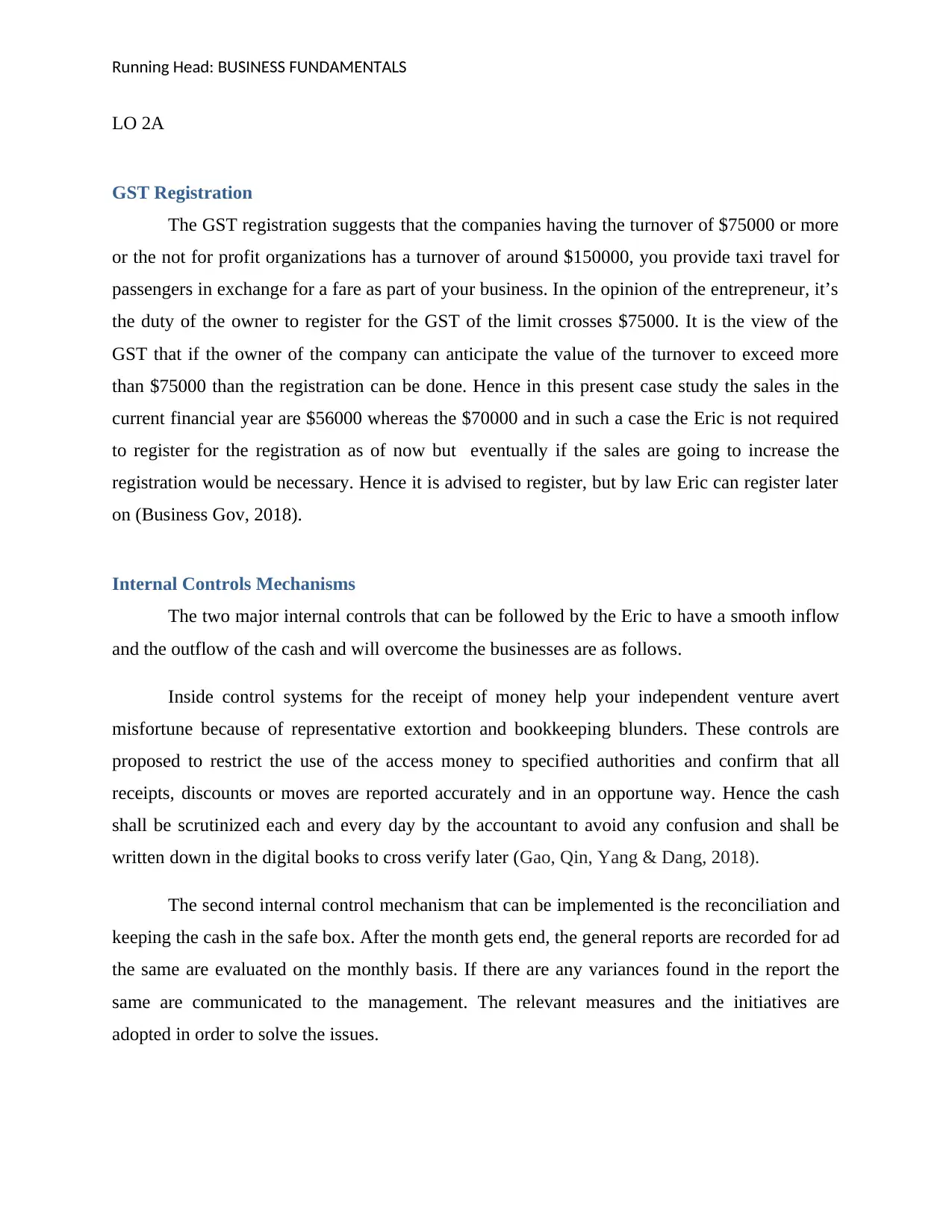

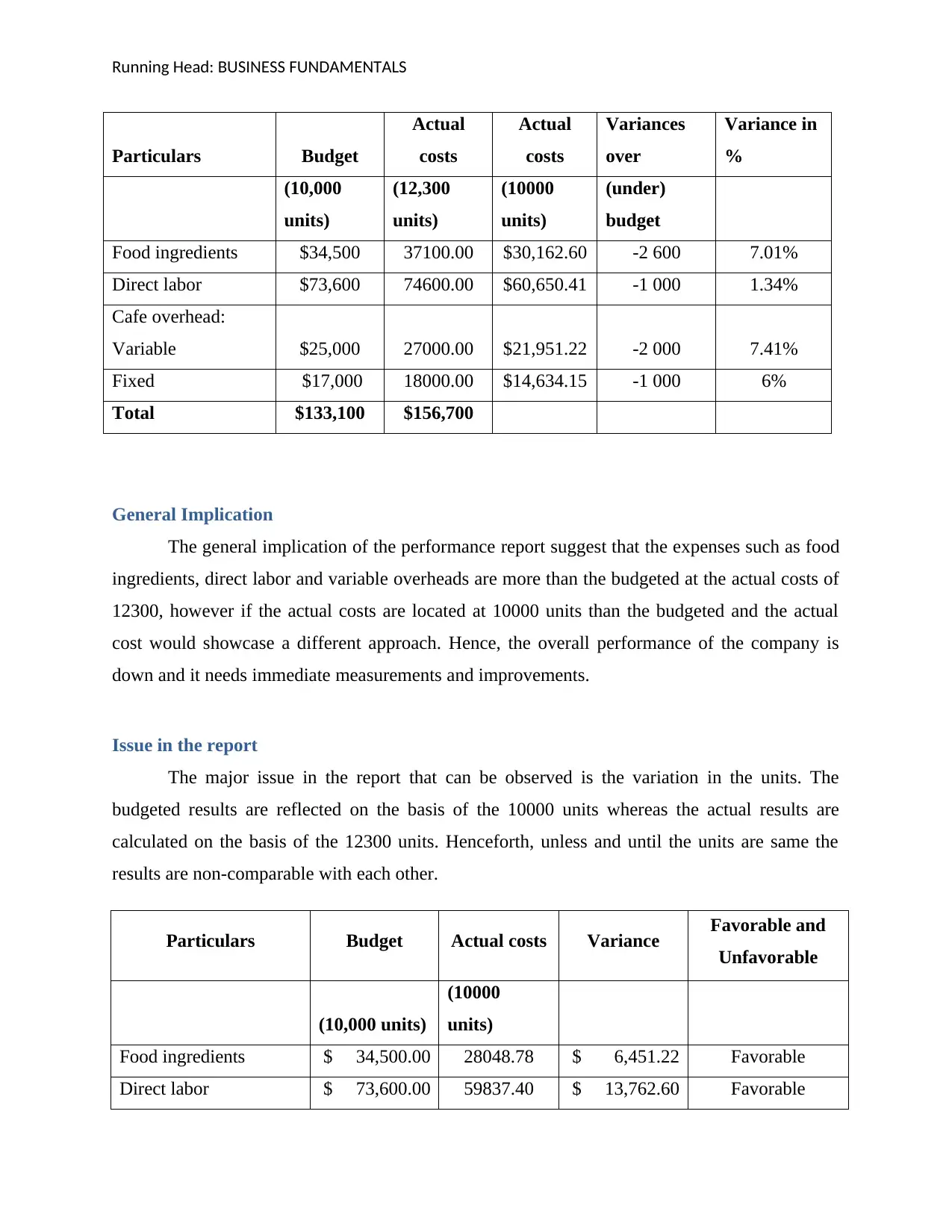

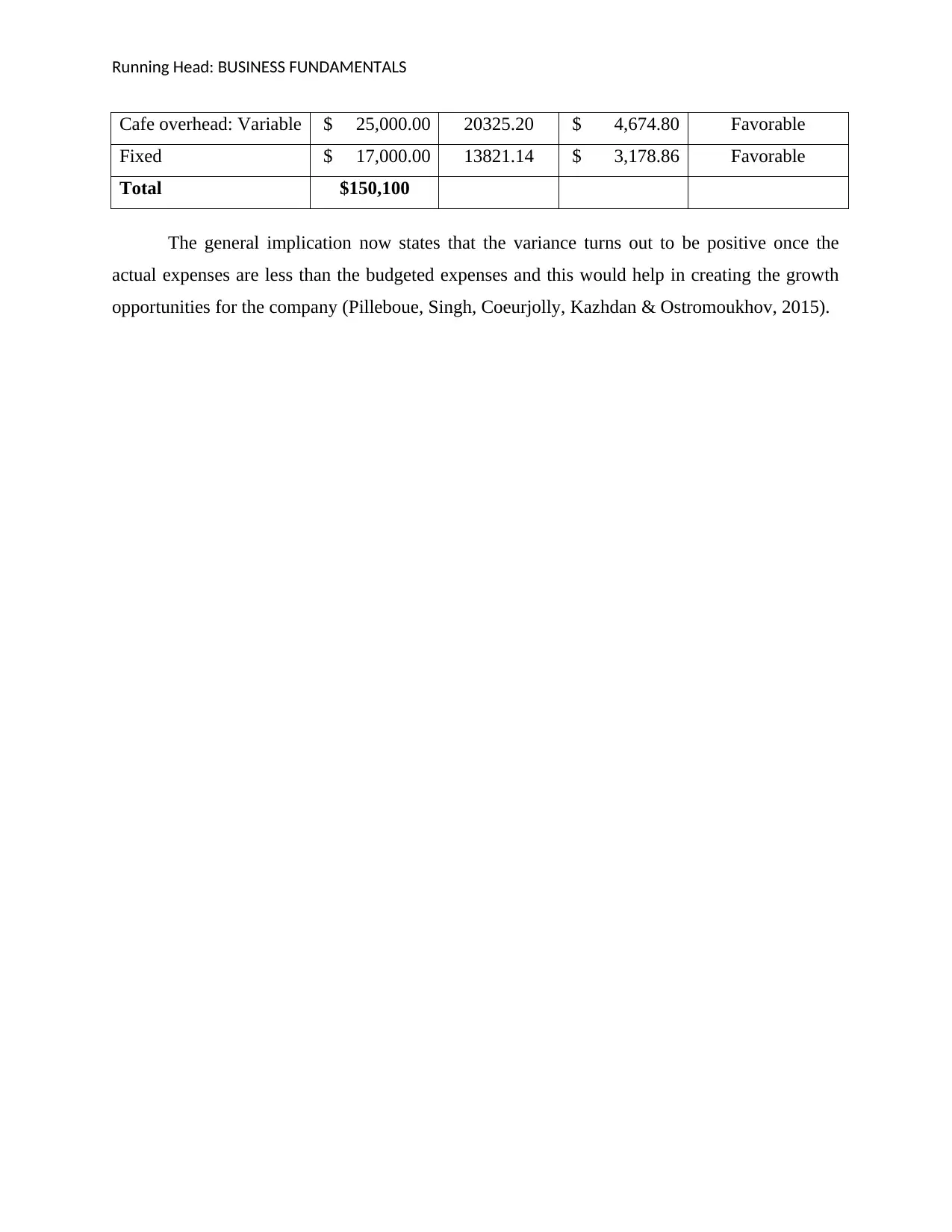

This assignment addresses business fundamentals, focusing on GST registration, internal control mechanisms, and performance reporting for the ICL Cafe. The solution advises the cafe manager, Eric, on GST registration based on projected sales figures, referencing relevant government guidelines. It outlines two key internal control mechanisms for managing cash flow: daily scrutiny by an accountant and reconciliation of cash with safe box records. The assignment includes a performance report analyzing budget variances in expenses like food ingredients, direct labor, and overheads, identifying issues related to unit discrepancies and offering a revised variance analysis with consistent units. The analysis highlights the implications of cost variances on the company's overall financial performance, offering insights into improving profitability and operational efficiency. References to relevant sources are also provided.

1 out of 5

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.