Financial Performance and Management Strategies in Hospitality

VerifiedAdded on 2020/06/03

|18

|4135

|99

Report

AI Summary

This report provides a comprehensive analysis of financial management within the hospitality industry. It begins by exploring various sources of funding, both internal and external, available to businesses, including retained profits, family and friends, bank loans, and venture capitalists. The report then evaluates methods for income generation, such as focusing on attractive interior and exterior designs, employing skilled personnel, organizing events, sub-renting, and cost control. Financial accounting concepts like trial balance, income statements, and balance sheets are assessed, along with ratio analysis to evaluate business performance and recommend future management strategies. Cost classification, contribution per product calculations, and break-even point (BEP) analysis are also discussed to aid in short-term management decisions. The report concludes by summarizing the key findings and insights into the financial aspects of the hospitality sector, offering practical guidance for financial planning and decision-making.

Finance in the Hospitality Industry

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

TABLE OF CONTENTS

INTRODUCTION...........................................................................................................................1

TASK 1............................................................................................................................................1

1.1 Reviewing sources of funding which are available to business and service industries.........1

1.2 Evaluating range of methods that contribute in income generation......................................5

TASK 2............................................................................................................................................6

TASK 3............................................................................................................................................6

TASK 4............................................................................................................................................6

3.1 Assessing the sources and structure of trial balance..............................................................6

3.2 Evaluating business accounts, adjustments and notes...........................................................7

4.1 Calculating ratios to assess business performance................................................................9

4.2 Recommending appropriate future management strategies.................................................11

TASK 5..........................................................................................................................................12

5.1 Classifying cost in terms of fixed, variable and semi-variable............................................12

5.2 Calculating contribution per product and explaining CVP relationship..............................12

5.3 Taking short-term management decision on the basis of profit or loss potentials and BEP

analysis......................................................................................................................................14

CONCLUSION..............................................................................................................................15

REFERENCES..............................................................................................................................16

INTRODUCTION...........................................................................................................................1

TASK 1............................................................................................................................................1

1.1 Reviewing sources of funding which are available to business and service industries.........1

1.2 Evaluating range of methods that contribute in income generation......................................5

TASK 2............................................................................................................................................6

TASK 3............................................................................................................................................6

TASK 4............................................................................................................................................6

3.1 Assessing the sources and structure of trial balance..............................................................6

3.2 Evaluating business accounts, adjustments and notes...........................................................7

4.1 Calculating ratios to assess business performance................................................................9

4.2 Recommending appropriate future management strategies.................................................11

TASK 5..........................................................................................................................................12

5.1 Classifying cost in terms of fixed, variable and semi-variable............................................12

5.2 Calculating contribution per product and explaining CVP relationship..............................12

5.3 Taking short-term management decision on the basis of profit or loss potentials and BEP

analysis......................................................................................................................................14

CONCLUSION..............................................................................................................................15

REFERENCES..............................................................................................................................16

INTRODUCTION

Financial management is essential within the hospitality sector for the attainment of goals

and objectives. In the recent times, hotel unit can enhance productivity and profitability only

when it delivers high quality services to the customers. Further, level of competition is also stiff

in the hospitality sector which in turn directly influences profit margin of firm. In this regard,

finance manager of the firm has accountability to make suitable assessment of cost and lay high

level of emphasis on developing competent plan. Now, companies which are operating in

hospitality sector needs to conduct research for assessing the expectation level of customers.

Hence, by allocating funds to each business activity in a optimal way firm can attain success to a

great extent. The present report is based on different case scenarios which will provide deeper

insight about the sources that can be undertaken by business entity for meeting financial

requirement. Besides this, it will shed light on the sources that assists firm in generating more

income. It will also develop understanding about the aspects of financial accounting such as trial

balance, income statement and balance sheet. In this, report will highlight the extent to which

financial position and performance of R. Riggs is sound. Report will also entail how BEP

analysis aid in decision making and makes contribution in the attainment of goals.

TASK 1

1.1 Reviewing sources of funding which are available to business and service industries

On the basis of cited case situation, business entity of small business enterprise requires

£450000 for purchasing new building. In this, there are several internal and external sources

that can be undertaken by the firm for meeting monetary needs pertaining to capital expenditure

or investment. Hence, major internal and external sources which are suitable for this purpose

enumerated below:

Internal sources

Financial management is essential within the hospitality sector for the attainment of goals

and objectives. In the recent times, hotel unit can enhance productivity and profitability only

when it delivers high quality services to the customers. Further, level of competition is also stiff

in the hospitality sector which in turn directly influences profit margin of firm. In this regard,

finance manager of the firm has accountability to make suitable assessment of cost and lay high

level of emphasis on developing competent plan. Now, companies which are operating in

hospitality sector needs to conduct research for assessing the expectation level of customers.

Hence, by allocating funds to each business activity in a optimal way firm can attain success to a

great extent. The present report is based on different case scenarios which will provide deeper

insight about the sources that can be undertaken by business entity for meeting financial

requirement. Besides this, it will shed light on the sources that assists firm in generating more

income. It will also develop understanding about the aspects of financial accounting such as trial

balance, income statement and balance sheet. In this, report will highlight the extent to which

financial position and performance of R. Riggs is sound. Report will also entail how BEP

analysis aid in decision making and makes contribution in the attainment of goals.

TASK 1

1.1 Reviewing sources of funding which are available to business and service industries

On the basis of cited case situation, business entity of small business enterprise requires

£450000 for purchasing new building. In this, there are several internal and external sources

that can be undertaken by the firm for meeting monetary needs pertaining to capital expenditure

or investment. Hence, major internal and external sources which are suitable for this purpose

enumerated below:

Internal sources

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Retained profit: In order to deal with the undesirable situations business entity lays high

level of emphasis on retaining some amount rather than investing the whole. Hence, by using

such fund entrepreneur can meet financial needs and requirements to the significant level.

Advantages: Disadvantages

In this, owner of the firm is free from fixed

obligation in terms of interest payment (Brotherton,

2012).

When business unit uses whole retained profit for

meeting requirements then they would not be in

position to deal with the future contingent situation.

Friends and family members: By taking financial assistance from friends and family

members owner of small business unit can generate funds.

Advantages: Disadvantages

Less interference in decision making

Absence of both monetary and non-

monetary obligations

Sometimes, business entity faces difficulty in

convincing family members towards the plan. This

aspect imposes issue in front of firm pertaining to

raising funds.

Sales of fixed assets: Sole trader can also generate funds by selling fixed assets which

are not used in productive activities. Every business unit has some scrap in the form of

machinery, other equipments etc (Internal Source of Finance, 2017). In this regard, by selling

such unused assets entrepreneur can raise fund and thereby would become able to implement

plan.

Advantages: Disadvantages

Low cost is the main advantage which

is associated with the selling of assets.

Moreover, in this, by placing

advertisement in the newspaper firm

In the case of quick selling of assets, sometimes

business unit does not receive suitable amount.

level of emphasis on retaining some amount rather than investing the whole. Hence, by using

such fund entrepreneur can meet financial needs and requirements to the significant level.

Advantages: Disadvantages

In this, owner of the firm is free from fixed

obligation in terms of interest payment (Brotherton,

2012).

When business unit uses whole retained profit for

meeting requirements then they would not be in

position to deal with the future contingent situation.

Friends and family members: By taking financial assistance from friends and family

members owner of small business unit can generate funds.

Advantages: Disadvantages

Less interference in decision making

Absence of both monetary and non-

monetary obligations

Sometimes, business entity faces difficulty in

convincing family members towards the plan. This

aspect imposes issue in front of firm pertaining to

raising funds.

Sales of fixed assets: Sole trader can also generate funds by selling fixed assets which

are not used in productive activities. Every business unit has some scrap in the form of

machinery, other equipments etc (Internal Source of Finance, 2017). In this regard, by selling

such unused assets entrepreneur can raise fund and thereby would become able to implement

plan.

Advantages: Disadvantages

Low cost is the main advantage which

is associated with the selling of assets.

Moreover, in this, by placing

advertisement in the newspaper firm

In the case of quick selling of assets, sometimes

business unit does not receive suitable amount.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

can attract potential investors.

Facilitates quick generation of funds

Reduction or controlling of working capital: Business entity can meet monetary needs

and requirement by making control on working capital. In accordance with such aspects by

speeding up the time of receivables and stretching payables business entity can manage funds

more effectually and meet monetary aspects.

Advantages: Disadvantages

Assists in maintaining ownership

within the firm

No requirement of collateral security

(Working Capital Loans – The

Advantages and Disadvantages, 2017)

Negatively affects credit rating

High interest rates

External sources

Bank loan: It is one of the most preferred sources of finance which provides high level of

assistance to business entity in fulfilling monetary needs. Hence, by applying to banking

institution on the basis of collateral security owner of small business unit can generate funds.

Advantages: Disadvantages

This source of finance offer deduction

to the business entity in tax brackets.

In this, sole trader has convenience

pertaining to making payment in the

form of installments (Zhuang and et.al.,

2011).

In business loan, interest rates are

usually high which in turn imposes

burden on sole trader.

Sometimes, banks do not grant whole

amount for which business entity has

applied.

Facilitates quick generation of funds

Reduction or controlling of working capital: Business entity can meet monetary needs

and requirement by making control on working capital. In accordance with such aspects by

speeding up the time of receivables and stretching payables business entity can manage funds

more effectually and meet monetary aspects.

Advantages: Disadvantages

Assists in maintaining ownership

within the firm

No requirement of collateral security

(Working Capital Loans – The

Advantages and Disadvantages, 2017)

Negatively affects credit rating

High interest rates

External sources

Bank loan: It is one of the most preferred sources of finance which provides high level of

assistance to business entity in fulfilling monetary needs. Hence, by applying to banking

institution on the basis of collateral security owner of small business unit can generate funds.

Advantages: Disadvantages

This source of finance offer deduction

to the business entity in tax brackets.

In this, sole trader has convenience

pertaining to making payment in the

form of installments (Zhuang and et.al.,

2011).

In business loan, interest rates are

usually high which in turn imposes

burden on sole trader.

Sometimes, banks do not grant whole

amount for which business entity has

applied.

Leasing: For purchasing building business entity requires more funds, in this, by taking

concerned asset on lease entrepreneur can meet financial needs. Moreover, in leasing, by making

payment of rent owner of the firm can use building for performing business activities.

Advantages: Disadvantages

Such financial source offers tax

benefits to the entity.

Leasing source protects business entity

from the potential of loss such as

reduction in the value of assets.

Under leasing, entrepreneur is obliged

to make use of asset as per the terms

and conditions of lessor. This in turn

closely influences the strategies and

policies of firm.

Venture capitalists: In the recent times, venture capitalist is the main sources of finance

which can be undertaken by small business entities. Now, venture capitalists provide fund to the

entities that have sound plan and potential to grow.

Advantages: Disadvantages

Along with the financials, venture

capitalist source provides organization

with expert advice. Moreover, due to

having interest in the venture,

capitalists also offer legal and tax

assistance to business entities (How to

Finance Your Business Growth, 2017).

Further, in this, sole trader offers

return to the capitalists only when

enough profit is generated. In this way,

such source reduces fixed monetary

obligation of firm.

Loss of control is one of the main

drawbacks which are associated with

such source. Moreover, venture

capitalists act as a equity holders and

interferes in the decision making

aspect.

concerned asset on lease entrepreneur can meet financial needs. Moreover, in leasing, by making

payment of rent owner of the firm can use building for performing business activities.

Advantages: Disadvantages

Such financial source offers tax

benefits to the entity.

Leasing source protects business entity

from the potential of loss such as

reduction in the value of assets.

Under leasing, entrepreneur is obliged

to make use of asset as per the terms

and conditions of lessor. This in turn

closely influences the strategies and

policies of firm.

Venture capitalists: In the recent times, venture capitalist is the main sources of finance

which can be undertaken by small business entities. Now, venture capitalists provide fund to the

entities that have sound plan and potential to grow.

Advantages: Disadvantages

Along with the financials, venture

capitalist source provides organization

with expert advice. Moreover, due to

having interest in the venture,

capitalists also offer legal and tax

assistance to business entities (How to

Finance Your Business Growth, 2017).

Further, in this, sole trader offers

return to the capitalists only when

enough profit is generated. In this way,

such source reduces fixed monetary

obligation of firm.

Loss of control is one of the main

drawbacks which are associated with

such source. Moreover, venture

capitalists act as a equity holders and

interferes in the decision making

aspect.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Factoring: Each business has some receivables so by discounting the same from financial

institution owner of small business unit can generate funds.

Advantages: Disadvantages

It offers conveniences to business entity in relation

to getting fund pertaining to receivables before the

due date. This is main benefit which encourages

business unit to undertake such source.

In against to offering early payment of receivables

financial institution charges some discounting

prices which in turn impose cost in front of firm.

In conclusive form, it can be stated that sole trade can meet monetary requirement of

£450,000, pertaining to capital expenditure, through the means of venture capitalist and bank

loan. Both such sources will assist in fulfilling needs and help in developing highly optimal

structure.

1.2 Evaluating range of methods that contribute in income generation

There are several methods which large sized restaurant unit can undertake to generate

income such as:

High focus on attractive interior and exterior: In the context of restaurant sector, interior

and exterior is the main aspects that have significant impact on customer decision

making. Thus, by making focus on creativity in this regard owner of restaurant unit

would become able to attract more customers which in turn contributes in income

generation.

Selection of skilled and talented personnel: In the context of large sized restaurant unit,

employees are the one who offer and deliver services to the customers. Thus, satisfaction

level of customers is highly influences from the manner in which personnel deal with

them. In this regard, by selecting highly skilled and talented personnel business entity

would become able to enhance customer satisfaction and loyalty (Kizildag, 2015). This in

turn makes positive and significant contribution in the profit margin of firm.

Organizing events: Large unit of restaurant chain can enhance income by organizing

cultural events, exhibition and band performance (Nussbaum, 2012). All such events

enable business entity to generate more income and enhance its profitability aspect.

institution owner of small business unit can generate funds.

Advantages: Disadvantages

It offers conveniences to business entity in relation

to getting fund pertaining to receivables before the

due date. This is main benefit which encourages

business unit to undertake such source.

In against to offering early payment of receivables

financial institution charges some discounting

prices which in turn impose cost in front of firm.

In conclusive form, it can be stated that sole trade can meet monetary requirement of

£450,000, pertaining to capital expenditure, through the means of venture capitalist and bank

loan. Both such sources will assist in fulfilling needs and help in developing highly optimal

structure.

1.2 Evaluating range of methods that contribute in income generation

There are several methods which large sized restaurant unit can undertake to generate

income such as:

High focus on attractive interior and exterior: In the context of restaurant sector, interior

and exterior is the main aspects that have significant impact on customer decision

making. Thus, by making focus on creativity in this regard owner of restaurant unit

would become able to attract more customers which in turn contributes in income

generation.

Selection of skilled and talented personnel: In the context of large sized restaurant unit,

employees are the one who offer and deliver services to the customers. Thus, satisfaction

level of customers is highly influences from the manner in which personnel deal with

them. In this regard, by selecting highly skilled and talented personnel business entity

would become able to enhance customer satisfaction and loyalty (Kizildag, 2015). This in

turn makes positive and significant contribution in the profit margin of firm.

Organizing events: Large unit of restaurant chain can enhance income by organizing

cultural events, exhibition and band performance (Nussbaum, 2012). All such events

enable business entity to generate more income and enhance its profitability aspect.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Sub-renting: By giving some part of restaurant on rent to others entrepreneur can

enhance its income (Law and et.al., 2012). For instance: Owner of restaurant chain can

increase its income level by giving some part to the one who offer handicraft products. In

this way, by receiving rent from such entity owner can get more income.

Offering high quality and developing attractive ambiance: Now, customers prefer to

visit hotel or restaurant which lays high level of emphasis on hygiene. Thus, by providing

customers with high quality services and attractive ambiance business entity can

maximize both productivity as well as profitability.

Cost control: For enhancing the income level, it is highly required for the owner of large

chain of restaurant to exert control on cost aspect. In this regard, by applying the tool of

budgetary control manager of restaurant can assess financial deviations and thereby

would become able to take action for improvement (Luo, 2011). Thus, through the means

of such tool firm can avoid unnecessary expenses and thereby become able to enhance

income level.

TASK 2

Enclosed in PPT.

TASK 3

Enclosed in PPT.

TASK 4

3.1 Assessing the sources and structure of trial balance

Trial balance may be served as a statement which contains balances of all the ledger

accounts. It has two sides such as debit and credit that clearly reflects the figures of assets,

liabilities, income and cash flow statement (What is a Trial Balance, 2017). This statement is

highly significant which in turn provides input or financial assistance to R. Riggs in the

preparation of financial statements.

Sources and structure of trial balance

enhance its income (Law and et.al., 2012). For instance: Owner of restaurant chain can

increase its income level by giving some part to the one who offer handicraft products. In

this way, by receiving rent from such entity owner can get more income.

Offering high quality and developing attractive ambiance: Now, customers prefer to

visit hotel or restaurant which lays high level of emphasis on hygiene. Thus, by providing

customers with high quality services and attractive ambiance business entity can

maximize both productivity as well as profitability.

Cost control: For enhancing the income level, it is highly required for the owner of large

chain of restaurant to exert control on cost aspect. In this regard, by applying the tool of

budgetary control manager of restaurant can assess financial deviations and thereby

would become able to take action for improvement (Luo, 2011). Thus, through the means

of such tool firm can avoid unnecessary expenses and thereby become able to enhance

income level.

TASK 2

Enclosed in PPT.

TASK 3

Enclosed in PPT.

TASK 4

3.1 Assessing the sources and structure of trial balance

Trial balance may be served as a statement which contains balances of all the ledger

accounts. It has two sides such as debit and credit that clearly reflects the figures of assets,

liabilities, income and cash flow statement (What is a Trial Balance, 2017). This statement is

highly significant which in turn provides input or financial assistance to R. Riggs in the

preparation of financial statements.

Sources and structure of trial balance

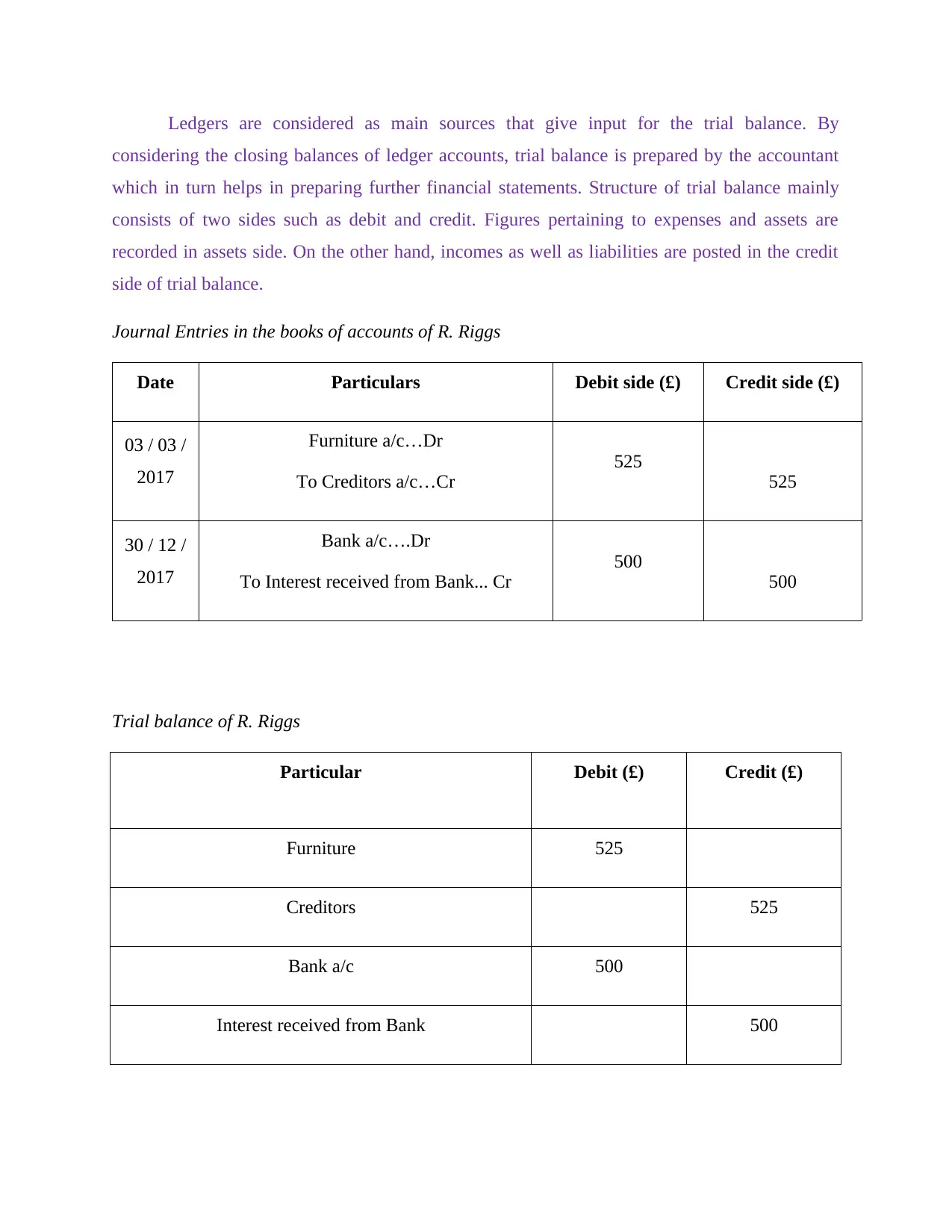

Ledgers are considered as main sources that give input for the trial balance. By

considering the closing balances of ledger accounts, trial balance is prepared by the accountant

which in turn helps in preparing further financial statements. Structure of trial balance mainly

consists of two sides such as debit and credit. Figures pertaining to expenses and assets are

recorded in assets side. On the other hand, incomes as well as liabilities are posted in the credit

side of trial balance.

Journal Entries in the books of accounts of R. Riggs

Date Particulars Debit side (£) Credit side (£)

03 / 03 /

2017

Furniture a/c…Dr

To Creditors a/c…Cr

525

525

30 / 12 /

2017

Bank a/c….Dr

To Interest received from Bank... Cr

500

500

Trial balance of R. Riggs

Particular Debit (£) Credit (£)

Furniture 525

Creditors 525

Bank a/c 500

Interest received from Bank 500

considering the closing balances of ledger accounts, trial balance is prepared by the accountant

which in turn helps in preparing further financial statements. Structure of trial balance mainly

consists of two sides such as debit and credit. Figures pertaining to expenses and assets are

recorded in assets side. On the other hand, incomes as well as liabilities are posted in the credit

side of trial balance.

Journal Entries in the books of accounts of R. Riggs

Date Particulars Debit side (£) Credit side (£)

03 / 03 /

2017

Furniture a/c…Dr

To Creditors a/c…Cr

525

525

30 / 12 /

2017

Bank a/c….Dr

To Interest received from Bank... Cr

500

500

Trial balance of R. Riggs

Particular Debit (£) Credit (£)

Furniture 525

Creditors 525

Bank a/c 500

Interest received from Bank 500

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

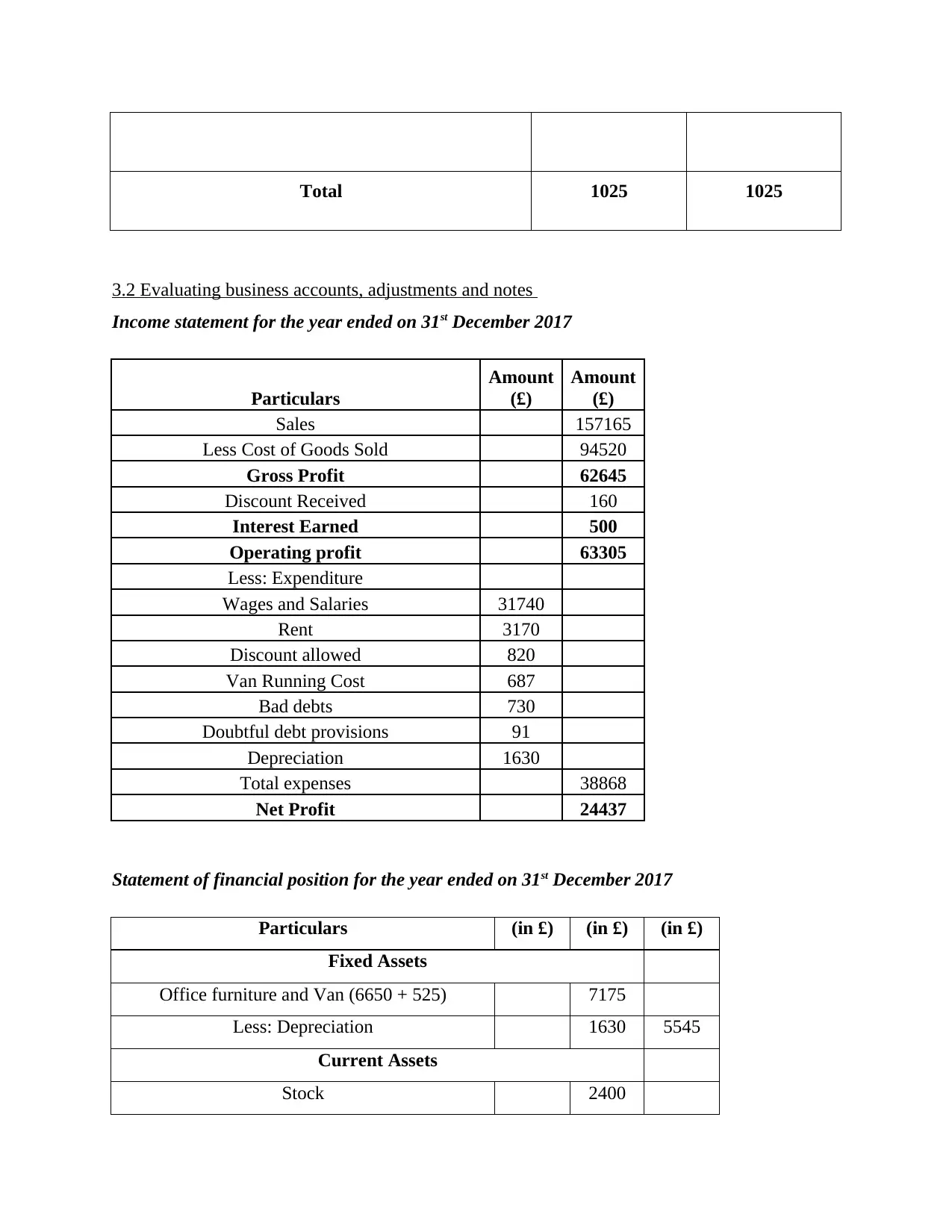

Total 1025 1025

3.2 Evaluating business accounts, adjustments and notes

Income statement for the year ended on 31st December 2017

Particulars

Amount

(£)

Amount

(£)

Sales 157165

Less Cost of Goods Sold 94520

Gross Profit 62645

Discount Received 160

Interest Earned 500

Operating profit 63305

Less: Expenditure

Wages and Salaries 31740

Rent 3170

Discount allowed 820

Van Running Cost 687

Bad debts 730

Doubtful debt provisions 91

Depreciation 1630

Total expenses 38868

Net Profit 24437

Statement of financial position for the year ended on 31st December 2017

Particulars (in £) (in £) (in £)

Fixed Assets

Office furniture and Van (6650 + 525) 7175

Less: Depreciation 1630 5545

Current Assets

Stock 2400

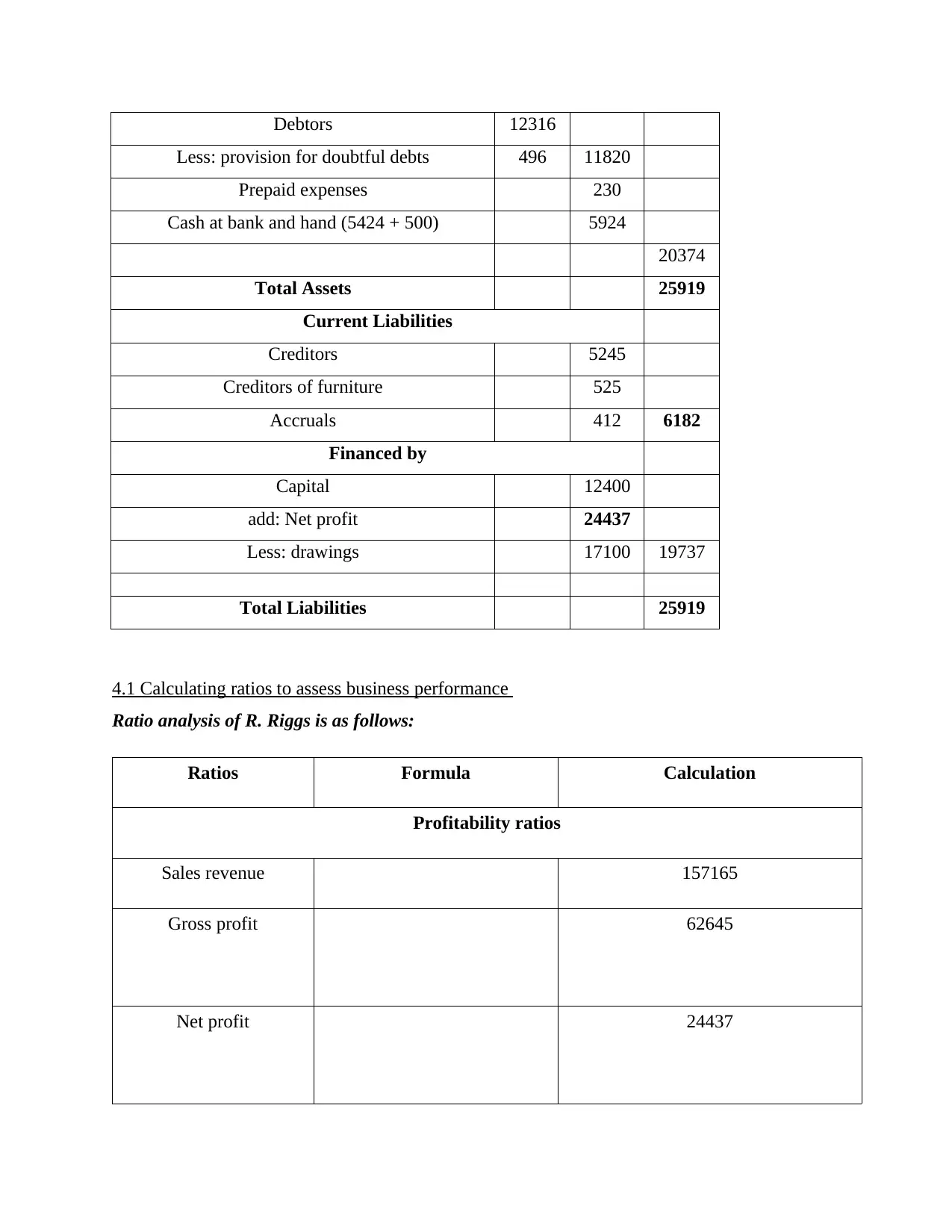

3.2 Evaluating business accounts, adjustments and notes

Income statement for the year ended on 31st December 2017

Particulars

Amount

(£)

Amount

(£)

Sales 157165

Less Cost of Goods Sold 94520

Gross Profit 62645

Discount Received 160

Interest Earned 500

Operating profit 63305

Less: Expenditure

Wages and Salaries 31740

Rent 3170

Discount allowed 820

Van Running Cost 687

Bad debts 730

Doubtful debt provisions 91

Depreciation 1630

Total expenses 38868

Net Profit 24437

Statement of financial position for the year ended on 31st December 2017

Particulars (in £) (in £) (in £)

Fixed Assets

Office furniture and Van (6650 + 525) 7175

Less: Depreciation 1630 5545

Current Assets

Stock 2400

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Debtors 12316

Less: provision for doubtful debts 496 11820

Prepaid expenses 230

Cash at bank and hand (5424 + 500) 5924

20374

Total Assets 25919

Current Liabilities

Creditors 5245

Creditors of furniture 525

Accruals 412 6182

Financed by

Capital 12400

add: Net profit 24437

Less: drawings 17100 19737

Total Liabilities 25919

4.1 Calculating ratios to assess business performance

Ratio analysis of R. Riggs is as follows:

Ratios Formula Calculation

Profitability ratios

Sales revenue 157165

Gross profit 62645

Net profit 24437

Less: provision for doubtful debts 496 11820

Prepaid expenses 230

Cash at bank and hand (5424 + 500) 5924

20374

Total Assets 25919

Current Liabilities

Creditors 5245

Creditors of furniture 525

Accruals 412 6182

Financed by

Capital 12400

add: Net profit 24437

Less: drawings 17100 19737

Total Liabilities 25919

4.1 Calculating ratios to assess business performance

Ratio analysis of R. Riggs is as follows:

Ratios Formula Calculation

Profitability ratios

Sales revenue 157165

Gross profit 62645

Net profit 24437

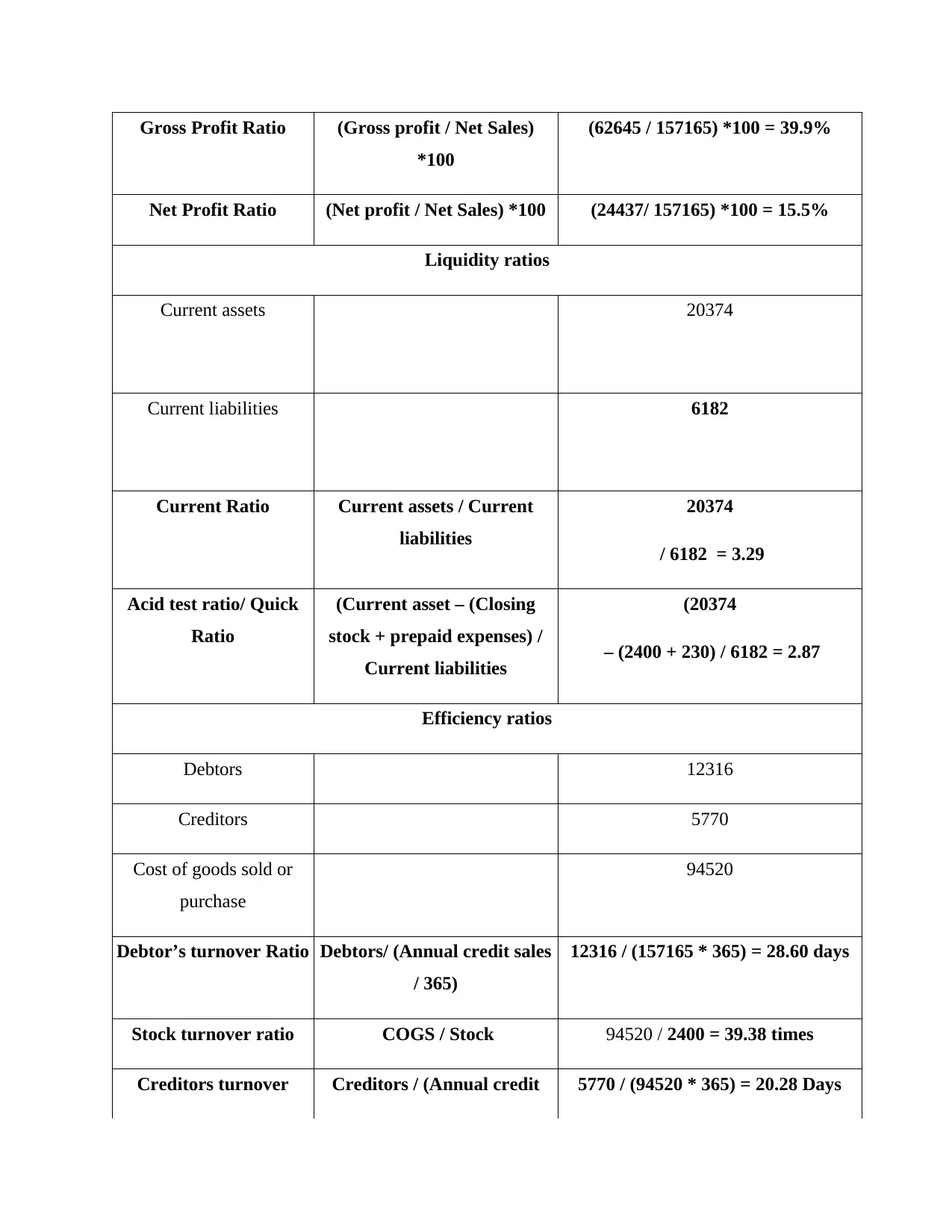

Gross Profit Ratio (Gross profit / Net Sales)

*100

(62645 / 157165) *100 = 39.9%

Net Profit Ratio (Net profit / Net Sales) *100 (24437/ 157165) *100 = 15.5%

Liquidity ratios

Current assets 20374

Current liabilities 6182

Current Ratio Current assets / Current

liabilities

20374

/ 6182 = 3.29

Acid test ratio/ Quick

Ratio

(Current asset – (Closing

stock + prepaid expenses) /

Current liabilities

(20374

– (2400 + 230) / 6182 = 2.87

Efficiency ratios

Debtors 12316

Creditors 5770

Cost of goods sold or

purchase

94520

Debtor’s turnover Ratio Debtors/ (Annual credit sales

/ 365)

12316 / (157165 * 365) = 28.60 days

Stock turnover ratio COGS / Stock 94520 / 2400 = 39.38 times

Creditors turnover Creditors / (Annual credit 5770 / (94520 * 365) = 20.28 Days

*100

(62645 / 157165) *100 = 39.9%

Net Profit Ratio (Net profit / Net Sales) *100 (24437/ 157165) *100 = 15.5%

Liquidity ratios

Current assets 20374

Current liabilities 6182

Current Ratio Current assets / Current

liabilities

20374

/ 6182 = 3.29

Acid test ratio/ Quick

Ratio

(Current asset – (Closing

stock + prepaid expenses) /

Current liabilities

(20374

– (2400 + 230) / 6182 = 2.87

Efficiency ratios

Debtors 12316

Creditors 5770

Cost of goods sold or

purchase

94520

Debtor’s turnover Ratio Debtors/ (Annual credit sales

/ 365)

12316 / (157165 * 365) = 28.60 days

Stock turnover ratio COGS / Stock 94520 / 2400 = 39.38 times

Creditors turnover Creditors / (Annual credit 5770 / (94520 * 365) = 20.28 Days

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 18

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.