Business Finance Project: Analyzing Portfolio Risk and Return (FIN205)

VerifiedAdded on 2022/09/18

|9

|1405

|24

Project

AI Summary

This business finance project examines portfolio risk and return, comparing the performance of five companies with the ASX200 index. The analysis includes calculating average returns, standard deviations, and beta values to assess the risk and volatility of each company and the equally weighted portfolio. The project identifies that while some stocks outperformed the market, others underperformed, and the equally weighted portfolio demonstrated lower risk compared to individual stocks. The report provides recommendations for a client of Tri-Star Management, suggesting investment in the equally weighted portfolio and highlighting the importance of balancing risk and return. The project utilizes financial metrics to evaluate investment opportunities and provide actionable insights, with references to relevant academic literature.

Running head: BUSINESS FINANCE

Business Finance

Student Name:

Student Number:

Authors Note:

Business Finance

Student Name:

Student Number:

Authors Note:

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

BUSINESS FINANCE

Table of Contents

Part 1:.........................................................................................................................................2

a) Comparing the average return on the ASX200 with each company:.....................................2

b) Identifying the average return of the portfolio, while explaining how the output was

derived:.......................................................................................................................................2

Part 2:.........................................................................................................................................3

a) Calculating the standard deviation of returns for the five companies, while depicting about

the overall risk of the companies:..............................................................................................3

b) Computing the standard deviation of the portfolio, while comparing it with the risk of

individual companies:................................................................................................................3

c) Comparing the standard deviation of returns of the ASX200 index with that of individual

shares and the equally weighted portfolio:.................................................................................3

Part 3:.........................................................................................................................................4

a) Estimating the beta for each company:..................................................................................4

b) Briefly explaining why each company has high/low of beta:................................................4

Part 4:.........................................................................................................................................4

a) Providing a short report for the client of Tri-Star Management:...........................................4

b) Providing relevant recommendations for Client of Tri-Star Management to invest of these

five companies:..........................................................................................................................6

References:.................................................................................................................................7

Appendices:................................................................................................................................8

Table of Contents

Part 1:.........................................................................................................................................2

a) Comparing the average return on the ASX200 with each company:.....................................2

b) Identifying the average return of the portfolio, while explaining how the output was

derived:.......................................................................................................................................2

Part 2:.........................................................................................................................................3

a) Calculating the standard deviation of returns for the five companies, while depicting about

the overall risk of the companies:..............................................................................................3

b) Computing the standard deviation of the portfolio, while comparing it with the risk of

individual companies:................................................................................................................3

c) Comparing the standard deviation of returns of the ASX200 index with that of individual

shares and the equally weighted portfolio:.................................................................................3

Part 3:.........................................................................................................................................4

a) Estimating the beta for each company:..................................................................................4

b) Briefly explaining why each company has high/low of beta:................................................4

Part 4:.........................................................................................................................................4

a) Providing a short report for the client of Tri-Star Management:...........................................4

b) Providing relevant recommendations for Client of Tri-Star Management to invest of these

five companies:..........................................................................................................................6

References:.................................................................................................................................7

Appendices:................................................................................................................................8

BUSINESS FINANCE

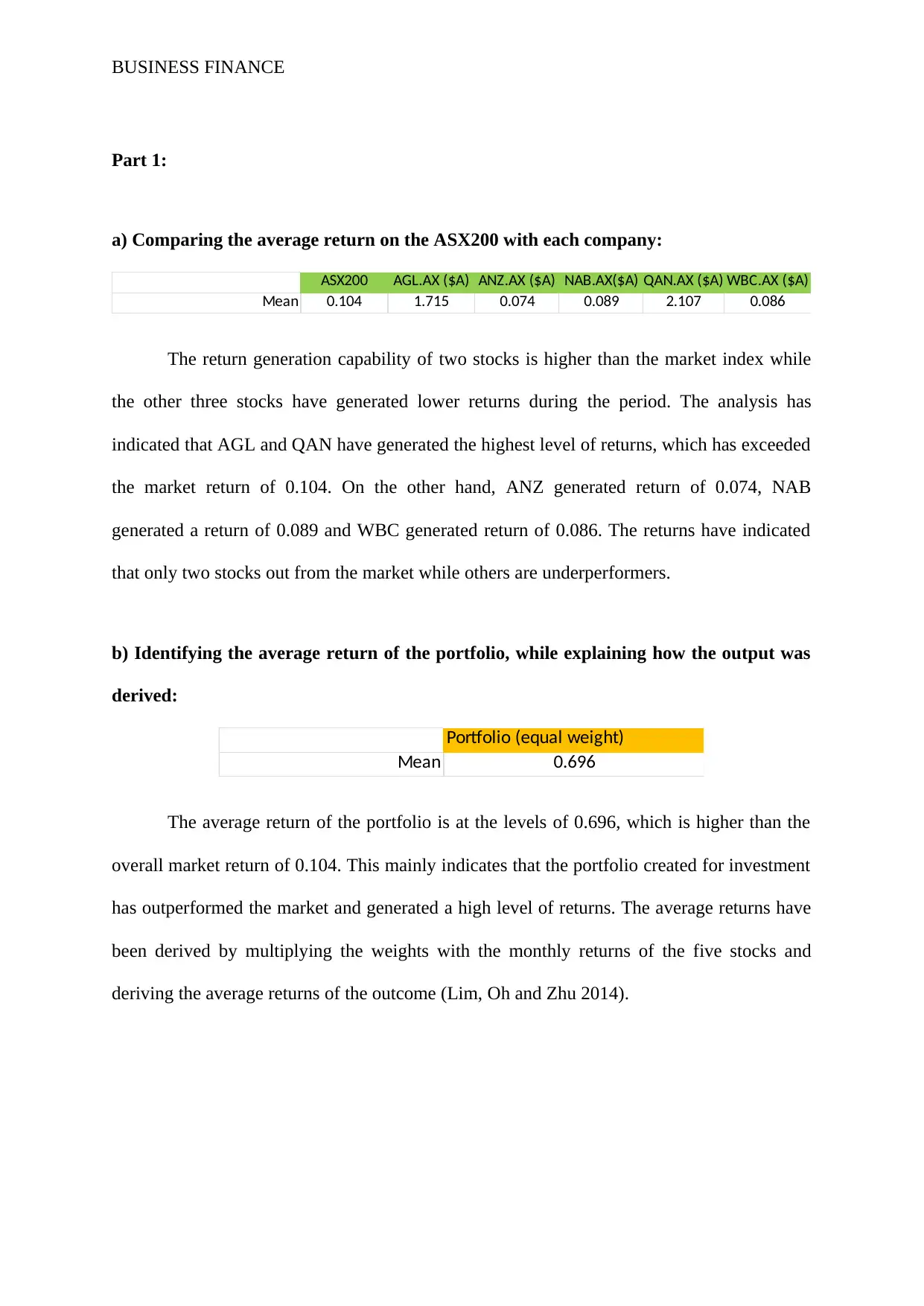

Part 1:

a) Comparing the average return on the ASX200 with each company:

ASX200 AGL.AX ($A) ANZ.AX ($A) NAB.AX($A) QAN.AX ($A) WBC.AX ($A)

Mean 0.104 1.715 0.074 0.089 2.107 0.086

The return generation capability of two stocks is higher than the market index while

the other three stocks have generated lower returns during the period. The analysis has

indicated that AGL and QAN have generated the highest level of returns, which has exceeded

the market return of 0.104. On the other hand, ANZ generated return of 0.074, NAB

generated a return of 0.089 and WBC generated return of 0.086. The returns have indicated

that only two stocks out from the market while others are underperformers.

b) Identifying the average return of the portfolio, while explaining how the output was

derived:

Portfolio (equal weight)

Mean 0.696

The average return of the portfolio is at the levels of 0.696, which is higher than the

overall market return of 0.104. This mainly indicates that the portfolio created for investment

has outperformed the market and generated a high level of returns. The average returns have

been derived by multiplying the weights with the monthly returns of the five stocks and

deriving the average returns of the outcome (Lim, Oh and Zhu 2014).

Part 1:

a) Comparing the average return on the ASX200 with each company:

ASX200 AGL.AX ($A) ANZ.AX ($A) NAB.AX($A) QAN.AX ($A) WBC.AX ($A)

Mean 0.104 1.715 0.074 0.089 2.107 0.086

The return generation capability of two stocks is higher than the market index while

the other three stocks have generated lower returns during the period. The analysis has

indicated that AGL and QAN have generated the highest level of returns, which has exceeded

the market return of 0.104. On the other hand, ANZ generated return of 0.074, NAB

generated a return of 0.089 and WBC generated return of 0.086. The returns have indicated

that only two stocks out from the market while others are underperformers.

b) Identifying the average return of the portfolio, while explaining how the output was

derived:

Portfolio (equal weight)

Mean 0.696

The average return of the portfolio is at the levels of 0.696, which is higher than the

overall market return of 0.104. This mainly indicates that the portfolio created for investment

has outperformed the market and generated a high level of returns. The average returns have

been derived by multiplying the weights with the monthly returns of the five stocks and

deriving the average returns of the outcome (Lim, Oh and Zhu 2014).

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

BUSINESS FINANCE

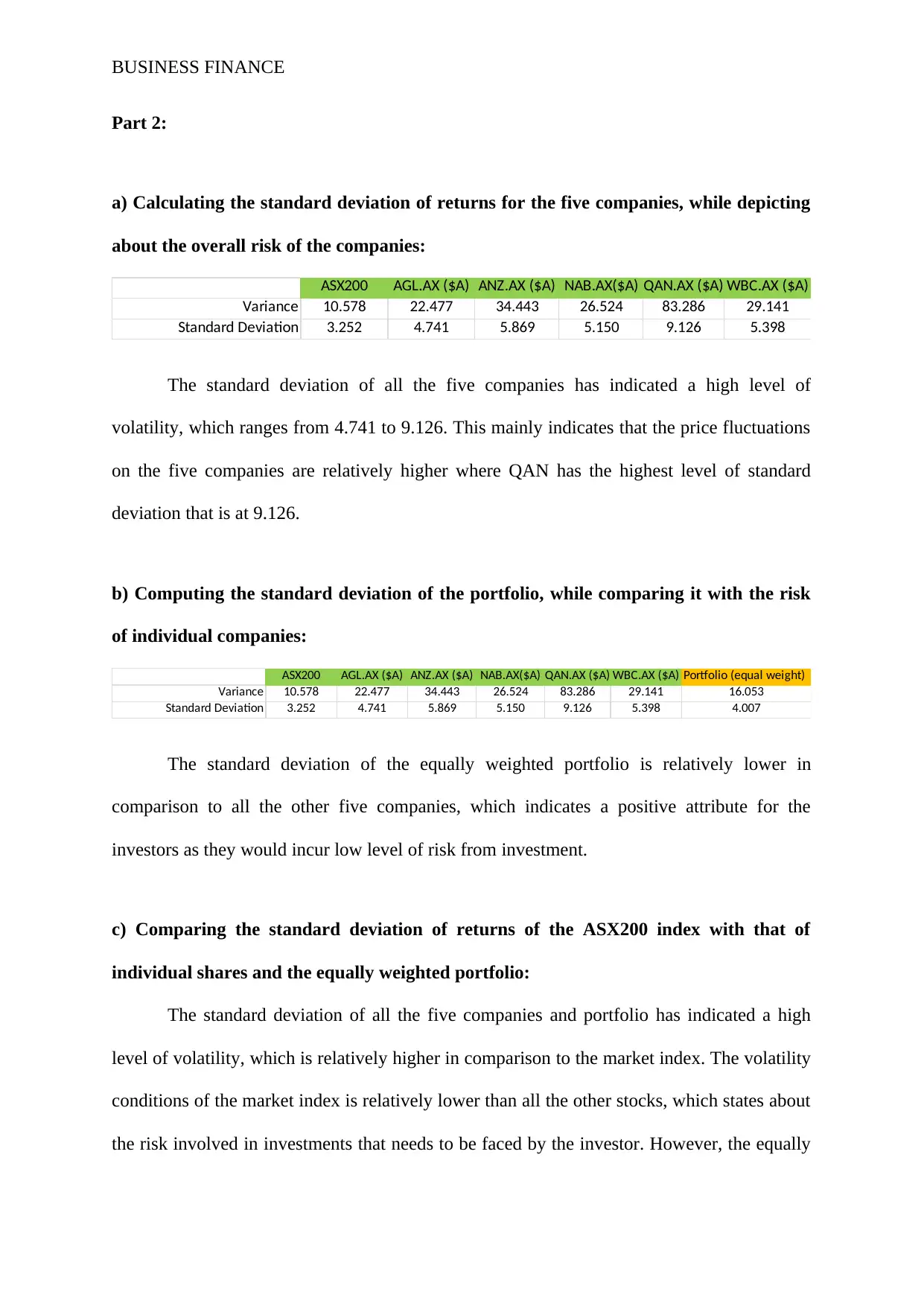

Part 2:

a) Calculating the standard deviation of returns for the five companies, while depicting

about the overall risk of the companies:

ASX200 AGL.AX ($A) ANZ.AX ($A) NAB.AX($A) QAN.AX ($A) WBC.AX ($A)

Variance 10.578 22.477 34.443 26.524 83.286 29.141

Standard Deviation 3.252 4.741 5.869 5.150 9.126 5.398

The standard deviation of all the five companies has indicated a high level of

volatility, which ranges from 4.741 to 9.126. This mainly indicates that the price fluctuations

on the five companies are relatively higher where QAN has the highest level of standard

deviation that is at 9.126.

b) Computing the standard deviation of the portfolio, while comparing it with the risk

of individual companies:

ASX200 AGL.AX ($A) ANZ.AX ($A) NAB.AX($A) QAN.AX ($A) WBC.AX ($A) Portfolio (equal weight)

Variance 10.578 22.477 34.443 26.524 83.286 29.141 16.053

Standard Deviation 3.252 4.741 5.869 5.150 9.126 5.398 4.007

The standard deviation of the equally weighted portfolio is relatively lower in

comparison to all the other five companies, which indicates a positive attribute for the

investors as they would incur low level of risk from investment.

c) Comparing the standard deviation of returns of the ASX200 index with that of

individual shares and the equally weighted portfolio:

The standard deviation of all the five companies and portfolio has indicated a high

level of volatility, which is relatively higher in comparison to the market index. The volatility

conditions of the market index is relatively lower than all the other stocks, which states about

the risk involved in investments that needs to be faced by the investor. However, the equally

Part 2:

a) Calculating the standard deviation of returns for the five companies, while depicting

about the overall risk of the companies:

ASX200 AGL.AX ($A) ANZ.AX ($A) NAB.AX($A) QAN.AX ($A) WBC.AX ($A)

Variance 10.578 22.477 34.443 26.524 83.286 29.141

Standard Deviation 3.252 4.741 5.869 5.150 9.126 5.398

The standard deviation of all the five companies has indicated a high level of

volatility, which ranges from 4.741 to 9.126. This mainly indicates that the price fluctuations

on the five companies are relatively higher where QAN has the highest level of standard

deviation that is at 9.126.

b) Computing the standard deviation of the portfolio, while comparing it with the risk

of individual companies:

ASX200 AGL.AX ($A) ANZ.AX ($A) NAB.AX($A) QAN.AX ($A) WBC.AX ($A) Portfolio (equal weight)

Variance 10.578 22.477 34.443 26.524 83.286 29.141 16.053

Standard Deviation 3.252 4.741 5.869 5.150 9.126 5.398 4.007

The standard deviation of the equally weighted portfolio is relatively lower in

comparison to all the other five companies, which indicates a positive attribute for the

investors as they would incur low level of risk from investment.

c) Comparing the standard deviation of returns of the ASX200 index with that of

individual shares and the equally weighted portfolio:

The standard deviation of all the five companies and portfolio has indicated a high

level of volatility, which is relatively higher in comparison to the market index. The volatility

conditions of the market index is relatively lower than all the other stocks, which states about

the risk involved in investments that needs to be faced by the investor. However, the equally

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

BUSINESS FINANCE

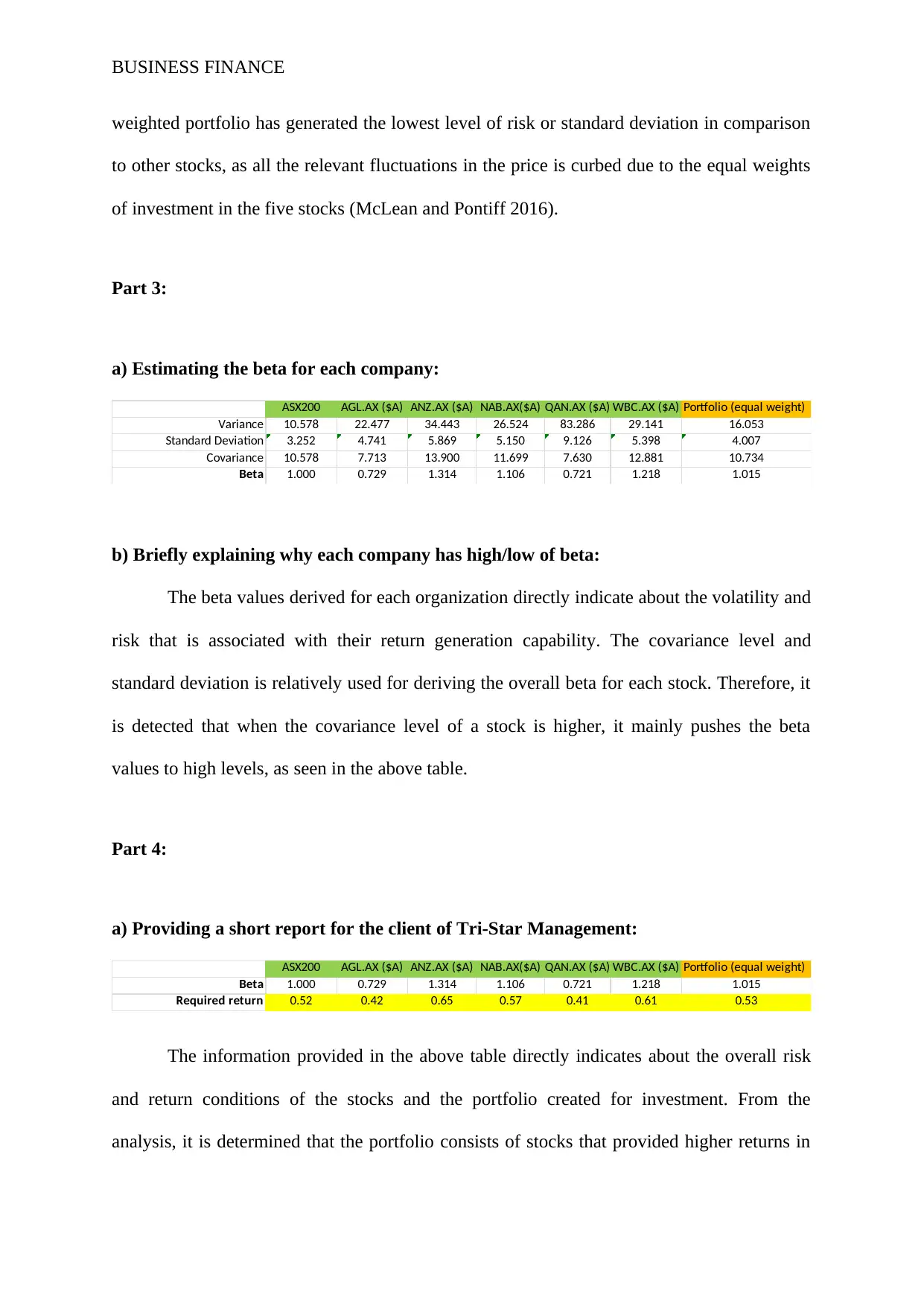

weighted portfolio has generated the lowest level of risk or standard deviation in comparison

to other stocks, as all the relevant fluctuations in the price is curbed due to the equal weights

of investment in the five stocks (McLean and Pontiff 2016).

Part 3:

a) Estimating the beta for each company:

ASX200 AGL.AX ($A) ANZ.AX ($A) NAB.AX($A) QAN.AX ($A) WBC.AX ($A) Portfolio (equal weight)

Variance 10.578 22.477 34.443 26.524 83.286 29.141 16.053

Standard Deviation 3.252 4.741 5.869 5.150 9.126 5.398 4.007

Covariance 10.578 7.713 13.900 11.699 7.630 12.881 10.734

Beta 1.000 0.729 1.314 1.106 0.721 1.218 1.015

b) Briefly explaining why each company has high/low of beta:

The beta values derived for each organization directly indicate about the volatility and

risk that is associated with their return generation capability. The covariance level and

standard deviation is relatively used for deriving the overall beta for each stock. Therefore, it

is detected that when the covariance level of a stock is higher, it mainly pushes the beta

values to high levels, as seen in the above table.

Part 4:

a) Providing a short report for the client of Tri-Star Management:

ASX200 AGL.AX ($A) ANZ.AX ($A) NAB.AX($A) QAN.AX ($A) WBC.AX ($A) Portfolio (equal weight)

Beta 1.000 0.729 1.314 1.106 0.721 1.218 1.015

Required return 0.52 0.42 0.65 0.57 0.41 0.61 0.53

The information provided in the above table directly indicates about the overall risk

and return conditions of the stocks and the portfolio created for investment. From the

analysis, it is determined that the portfolio consists of stocks that provided higher returns in

weighted portfolio has generated the lowest level of risk or standard deviation in comparison

to other stocks, as all the relevant fluctuations in the price is curbed due to the equal weights

of investment in the five stocks (McLean and Pontiff 2016).

Part 3:

a) Estimating the beta for each company:

ASX200 AGL.AX ($A) ANZ.AX ($A) NAB.AX($A) QAN.AX ($A) WBC.AX ($A) Portfolio (equal weight)

Variance 10.578 22.477 34.443 26.524 83.286 29.141 16.053

Standard Deviation 3.252 4.741 5.869 5.150 9.126 5.398 4.007

Covariance 10.578 7.713 13.900 11.699 7.630 12.881 10.734

Beta 1.000 0.729 1.314 1.106 0.721 1.218 1.015

b) Briefly explaining why each company has high/low of beta:

The beta values derived for each organization directly indicate about the volatility and

risk that is associated with their return generation capability. The covariance level and

standard deviation is relatively used for deriving the overall beta for each stock. Therefore, it

is detected that when the covariance level of a stock is higher, it mainly pushes the beta

values to high levels, as seen in the above table.

Part 4:

a) Providing a short report for the client of Tri-Star Management:

ASX200 AGL.AX ($A) ANZ.AX ($A) NAB.AX($A) QAN.AX ($A) WBC.AX ($A) Portfolio (equal weight)

Beta 1.000 0.729 1.314 1.106 0.721 1.218 1.015

Required return 0.52 0.42 0.65 0.57 0.41 0.61 0.53

The information provided in the above table directly indicates about the overall risk

and return conditions of the stocks and the portfolio created for investment. From the

analysis, it is determined that the portfolio consists of stocks that provided higher returns in

BUSINESS FINANCE

comparison to the index, as it outperformed the market itself. However, the risk factors are

relatively higher and can be determined from the above table. The combination of the stocks

in the portfolio has allowed the risk factor to deteriorate substantially and become close to the

levels of the actual market index. This is actually led to the increment in return generation

capability of the stock over a period of time.

The risk assessment of the stocks has directly indicated that ANZ, NAB and WBC are

highly risky investments in comparison to QAN and AGL, whose total beta values are lower

than 1. Therefore, it is detected that the lowest risk involved in investment is from AHL and

QAN, while the overall returns from the investment is also low in comparison to other

investments. This mainly indicates that if the investor intends to generate high level of returns

they have to increase their risk exposure, as higher risk would allow them to generate high

level of return in the process. Kumar (2014) stated that investors use the information about

the risk and return condition of a stock to prepare the portfolio, which has lowering exposure

to risk levels and higher return generation capability. From the relevant analysis, it could be

identified that the share price of the stock is correctly priced, as the value of the stocks is

altered due to the change in demand in the capital market.

Therefore, it could be understood that investments in AGL and QAN is more

advisable, as they have lowest risk attributes and adequate return generation capability.

However, evaluation of the portfolio has indicated the risk to return ratio where investors

generate appropriate level of returns, which is higher than the market, while risk is close to

the market levels. Thus, the investments in portfolio, AGL and QAN are recommended for

the investors.

comparison to the index, as it outperformed the market itself. However, the risk factors are

relatively higher and can be determined from the above table. The combination of the stocks

in the portfolio has allowed the risk factor to deteriorate substantially and become close to the

levels of the actual market index. This is actually led to the increment in return generation

capability of the stock over a period of time.

The risk assessment of the stocks has directly indicated that ANZ, NAB and WBC are

highly risky investments in comparison to QAN and AGL, whose total beta values are lower

than 1. Therefore, it is detected that the lowest risk involved in investment is from AHL and

QAN, while the overall returns from the investment is also low in comparison to other

investments. This mainly indicates that if the investor intends to generate high level of returns

they have to increase their risk exposure, as higher risk would allow them to generate high

level of return in the process. Kumar (2014) stated that investors use the information about

the risk and return condition of a stock to prepare the portfolio, which has lowering exposure

to risk levels and higher return generation capability. From the relevant analysis, it could be

identified that the share price of the stock is correctly priced, as the value of the stocks is

altered due to the change in demand in the capital market.

Therefore, it could be understood that investments in AGL and QAN is more

advisable, as they have lowest risk attributes and adequate return generation capability.

However, evaluation of the portfolio has indicated the risk to return ratio where investors

generate appropriate level of returns, which is higher than the market, while risk is close to

the market levels. Thus, the investments in portfolio, AGL and QAN are recommended for

the investors.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

BUSINESS FINANCE

b) Providing relevant recommendations for Client of Tri-Star Management to invest of

these five companies:

The client would be recommended for investing in the equally weighted portfolio, as

it would allow them to reduce the level of risk involved in investment and generate adequate

returns, which is higher than the overall market index. The portfolio directly reduces the level

of risk involved in investment and allows the investor to generate high level of returns, which

cannot be conducted in a single investment. However, changes to the portfolio weights can

also increase the level of returns and reduce the risk involved in investment for Tri-Star

management.

b) Providing relevant recommendations for Client of Tri-Star Management to invest of

these five companies:

The client would be recommended for investing in the equally weighted portfolio, as

it would allow them to reduce the level of risk involved in investment and generate adequate

returns, which is higher than the overall market index. The portfolio directly reduces the level

of risk involved in investment and allows the investor to generate high level of returns, which

cannot be conducted in a single investment. However, changes to the portfolio weights can

also increase the level of returns and reduce the risk involved in investment for Tri-Star

management.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

BUSINESS FINANCE

References:

Kumar, D., 2014. Return and volatility transmission between gold and stock sectors:

Application of portfolio management and hedging effectiveness. IIMB Management

Review, 26(1), pp.5-16.

Lim, S., Oh, K.W. and Zhu, J., 2014. Use of DEA cross-efficiency evaluation in portfolio

selection: An application to Korean stock market. European Journal of Operational

Research, 236(1), pp.361-368.

McLean, R.D. and Pontiff, J., 2016. Does academic research destroy stock return

predictability?. The Journal of Finance, 71(1), pp.5-32.

References:

Kumar, D., 2014. Return and volatility transmission between gold and stock sectors:

Application of portfolio management and hedging effectiveness. IIMB Management

Review, 26(1), pp.5-16.

Lim, S., Oh, K.W. and Zhu, J., 2014. Use of DEA cross-efficiency evaluation in portfolio

selection: An application to Korean stock market. European Journal of Operational

Research, 236(1), pp.361-368.

McLean, R.D. and Pontiff, J., 2016. Does academic research destroy stock return

predictability?. The Journal of Finance, 71(1), pp.5-32.

BUSINESS FINANCE

Appendices:

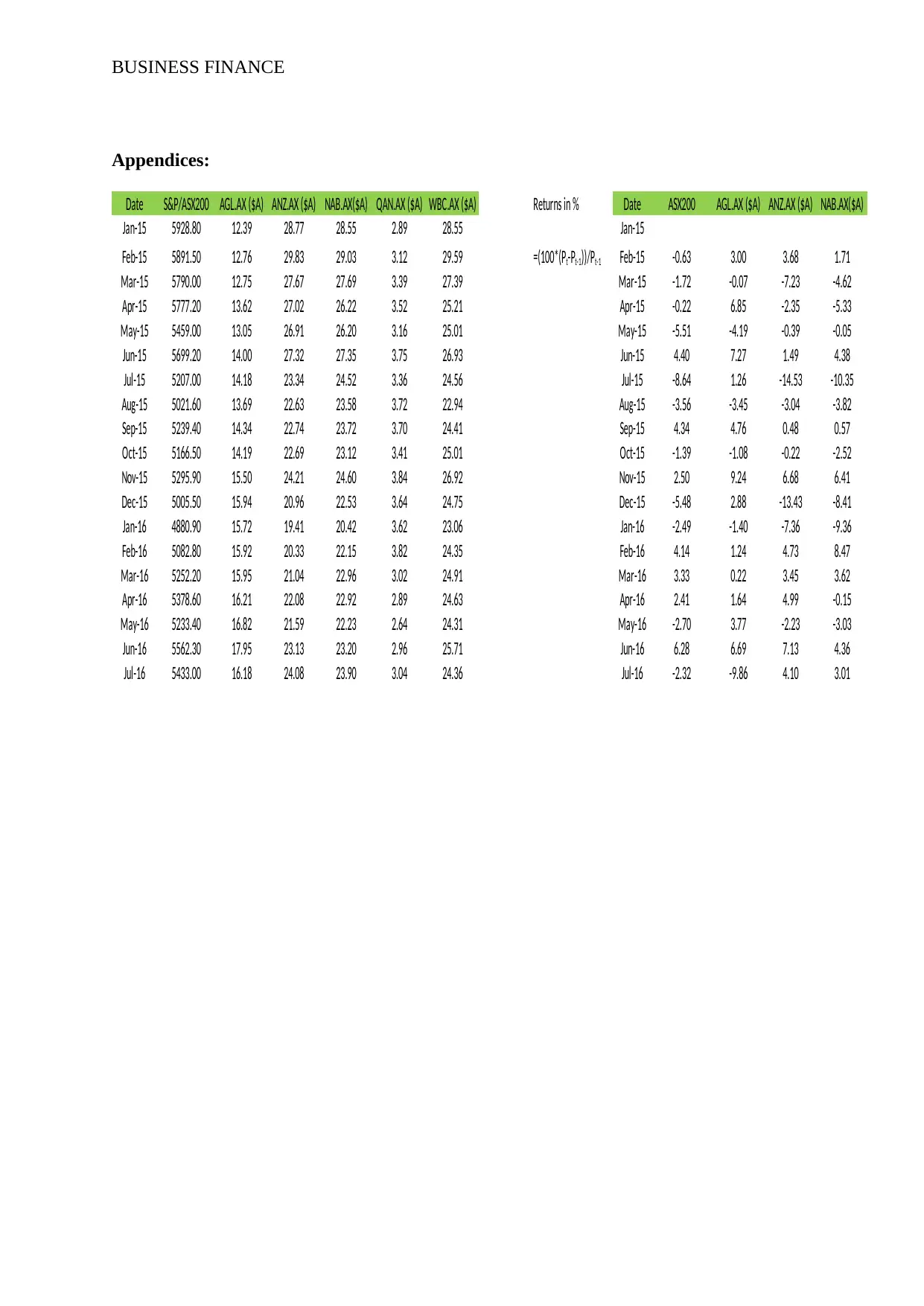

Date S&P/ASX200 AGL.AX ($A) ANZ.AX ($A) NAB.AX($A) QAN.AX ($A) WBC.AX ($A) Returns in % Date ASX200 AGL.AX ($A) ANZ.AX ($A) NAB.AX($A)

Jan-15 5928.80 12.39 28.77 28.55 2.89 28.55 Jan-15

Feb-15 5891.50 12.76 29.83 29.03 3.12 29.59 Feb-15 -0.63 3.00 3.68 1.71

Mar-15 5790.00 12.75 27.67 27.69 3.39 27.39 Mar-15 -1.72 -0.07 -7.23 -4.62

Apr-15 5777.20 13.62 27.02 26.22 3.52 25.21 Apr-15 -0.22 6.85 -2.35 -5.33

May-15 5459.00 13.05 26.91 26.20 3.16 25.01 May-15 -5.51 -4.19 -0.39 -0.05

Jun-15 5699.20 14.00 27.32 27.35 3.75 26.93 Jun-15 4.40 7.27 1.49 4.38

Jul-15 5207.00 14.18 23.34 24.52 3.36 24.56 Jul-15 -8.64 1.26 -14.53 -10.35

Aug-15 5021.60 13.69 22.63 23.58 3.72 22.94 Aug-15 -3.56 -3.45 -3.04 -3.82

Sep-15 5239.40 14.34 22.74 23.72 3.70 24.41 Sep-15 4.34 4.76 0.48 0.57

Oct-15 5166.50 14.19 22.69 23.12 3.41 25.01 Oct-15 -1.39 -1.08 -0.22 -2.52

Nov-15 5295.90 15.50 24.21 24.60 3.84 26.92 Nov-15 2.50 9.24 6.68 6.41

Dec-15 5005.50 15.94 20.96 22.53 3.64 24.75 Dec-15 -5.48 2.88 -13.43 -8.41

Jan-16 4880.90 15.72 19.41 20.42 3.62 23.06 Jan-16 -2.49 -1.40 -7.36 -9.36

Feb-16 5082.80 15.92 20.33 22.15 3.82 24.35 Feb-16 4.14 1.24 4.73 8.47

Mar-16 5252.20 15.95 21.04 22.96 3.02 24.91 Mar-16 3.33 0.22 3.45 3.62

Apr-16 5378.60 16.21 22.08 22.92 2.89 24.63 Apr-16 2.41 1.64 4.99 -0.15

May-16 5233.40 16.82 21.59 22.23 2.64 24.31 May-16 -2.70 3.77 -2.23 -3.03

Jun-16 5562.30 17.95 23.13 23.20 2.96 25.71 Jun-16 6.28 6.69 7.13 4.36

Jul-16 5433.00 16.18 24.08 23.90 3.04 24.36 Jul-16 -2.32 -9.86 4.10 3.01

=(100*(Pt-Pt-1))/Pt-1

Appendices:

Date S&P/ASX200 AGL.AX ($A) ANZ.AX ($A) NAB.AX($A) QAN.AX ($A) WBC.AX ($A) Returns in % Date ASX200 AGL.AX ($A) ANZ.AX ($A) NAB.AX($A)

Jan-15 5928.80 12.39 28.77 28.55 2.89 28.55 Jan-15

Feb-15 5891.50 12.76 29.83 29.03 3.12 29.59 Feb-15 -0.63 3.00 3.68 1.71

Mar-15 5790.00 12.75 27.67 27.69 3.39 27.39 Mar-15 -1.72 -0.07 -7.23 -4.62

Apr-15 5777.20 13.62 27.02 26.22 3.52 25.21 Apr-15 -0.22 6.85 -2.35 -5.33

May-15 5459.00 13.05 26.91 26.20 3.16 25.01 May-15 -5.51 -4.19 -0.39 -0.05

Jun-15 5699.20 14.00 27.32 27.35 3.75 26.93 Jun-15 4.40 7.27 1.49 4.38

Jul-15 5207.00 14.18 23.34 24.52 3.36 24.56 Jul-15 -8.64 1.26 -14.53 -10.35

Aug-15 5021.60 13.69 22.63 23.58 3.72 22.94 Aug-15 -3.56 -3.45 -3.04 -3.82

Sep-15 5239.40 14.34 22.74 23.72 3.70 24.41 Sep-15 4.34 4.76 0.48 0.57

Oct-15 5166.50 14.19 22.69 23.12 3.41 25.01 Oct-15 -1.39 -1.08 -0.22 -2.52

Nov-15 5295.90 15.50 24.21 24.60 3.84 26.92 Nov-15 2.50 9.24 6.68 6.41

Dec-15 5005.50 15.94 20.96 22.53 3.64 24.75 Dec-15 -5.48 2.88 -13.43 -8.41

Jan-16 4880.90 15.72 19.41 20.42 3.62 23.06 Jan-16 -2.49 -1.40 -7.36 -9.36

Feb-16 5082.80 15.92 20.33 22.15 3.82 24.35 Feb-16 4.14 1.24 4.73 8.47

Mar-16 5252.20 15.95 21.04 22.96 3.02 24.91 Mar-16 3.33 0.22 3.45 3.62

Apr-16 5378.60 16.21 22.08 22.92 2.89 24.63 Apr-16 2.41 1.64 4.99 -0.15

May-16 5233.40 16.82 21.59 22.23 2.64 24.31 May-16 -2.70 3.77 -2.23 -3.03

Jun-16 5562.30 17.95 23.13 23.20 2.96 25.71 Jun-16 6.28 6.69 7.13 4.36

Jul-16 5433.00 16.18 24.08 23.90 3.04 24.36 Jul-16 -2.32 -9.86 4.10 3.01

=(100*(Pt-Pt-1))/Pt-1

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 9

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.