Finance: Portfolio Management, Investor Utility, Curves, Allocation

VerifiedAdded on 2023/06/15

|8

|939

|152

Practical Assignment

AI Summary

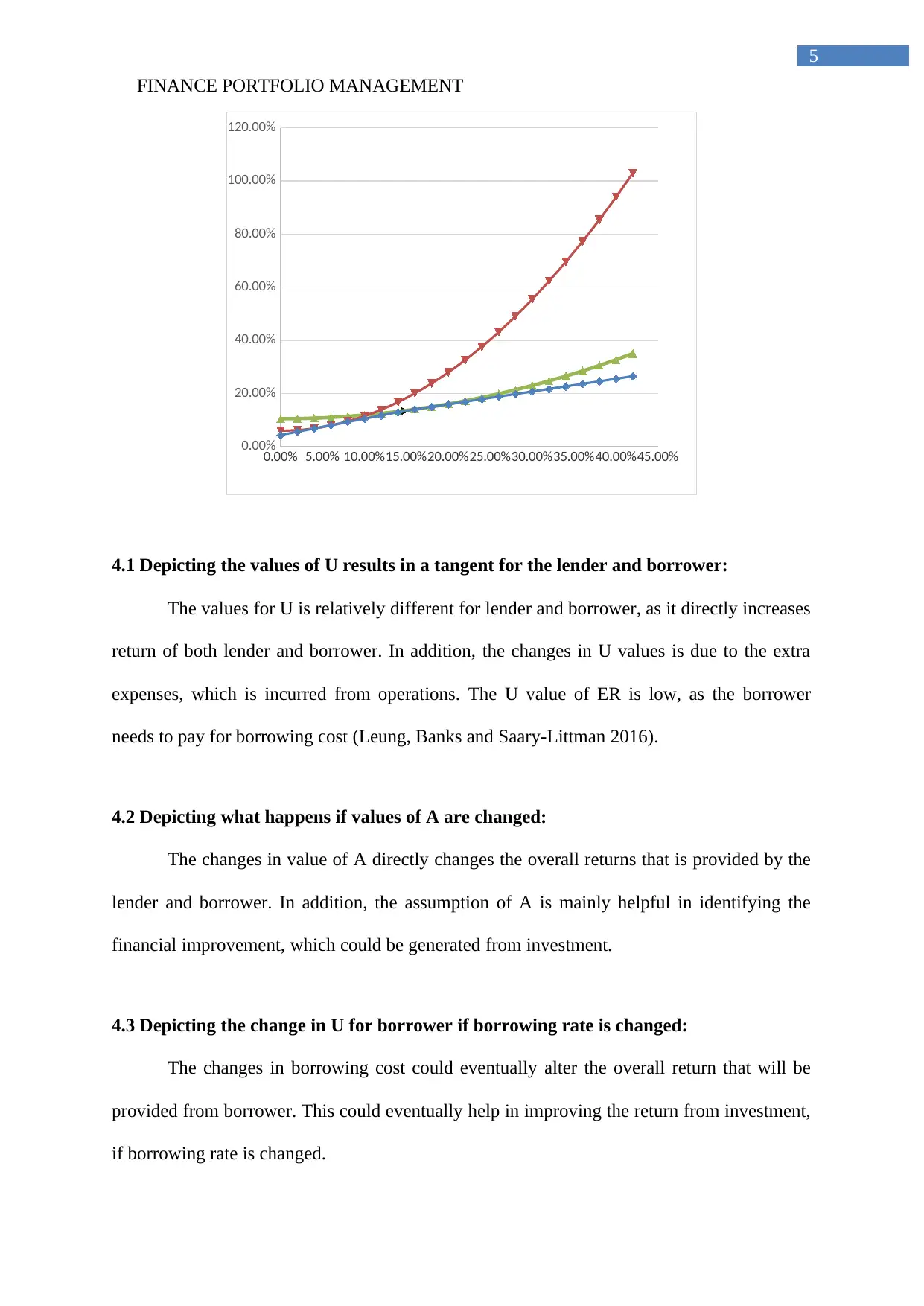

This assignment focuses on creating a portfolio management spreadsheet to plot utility curves and estimate the optimal combination of risky and risk-free assets based on an investor's risk aversion. The model uses historical data from the S&P 500 Index and T-Bills to calculate annual geometric mean returns and standard deviations. The spreadsheet includes calculations for borrowing costs, Sharpe ratios, and expected returns for both lenders and borrowers under varying risk percentages. It analyzes how changes in utility values (U) and risk aversion (A) impact investment returns, demonstrating the trade-offs between risk and return in asset allocation. The assignment also discusses the significance of the Sharpe ratio in evaluating portfolio performance relative to risk-free returns.

1 out of 8

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.