Comprehensive Finance Assignment: Portfolio and Cash Flow Analysis

VerifiedAdded on 2022/10/12

|6

|862

|121

Homework Assignment

AI Summary

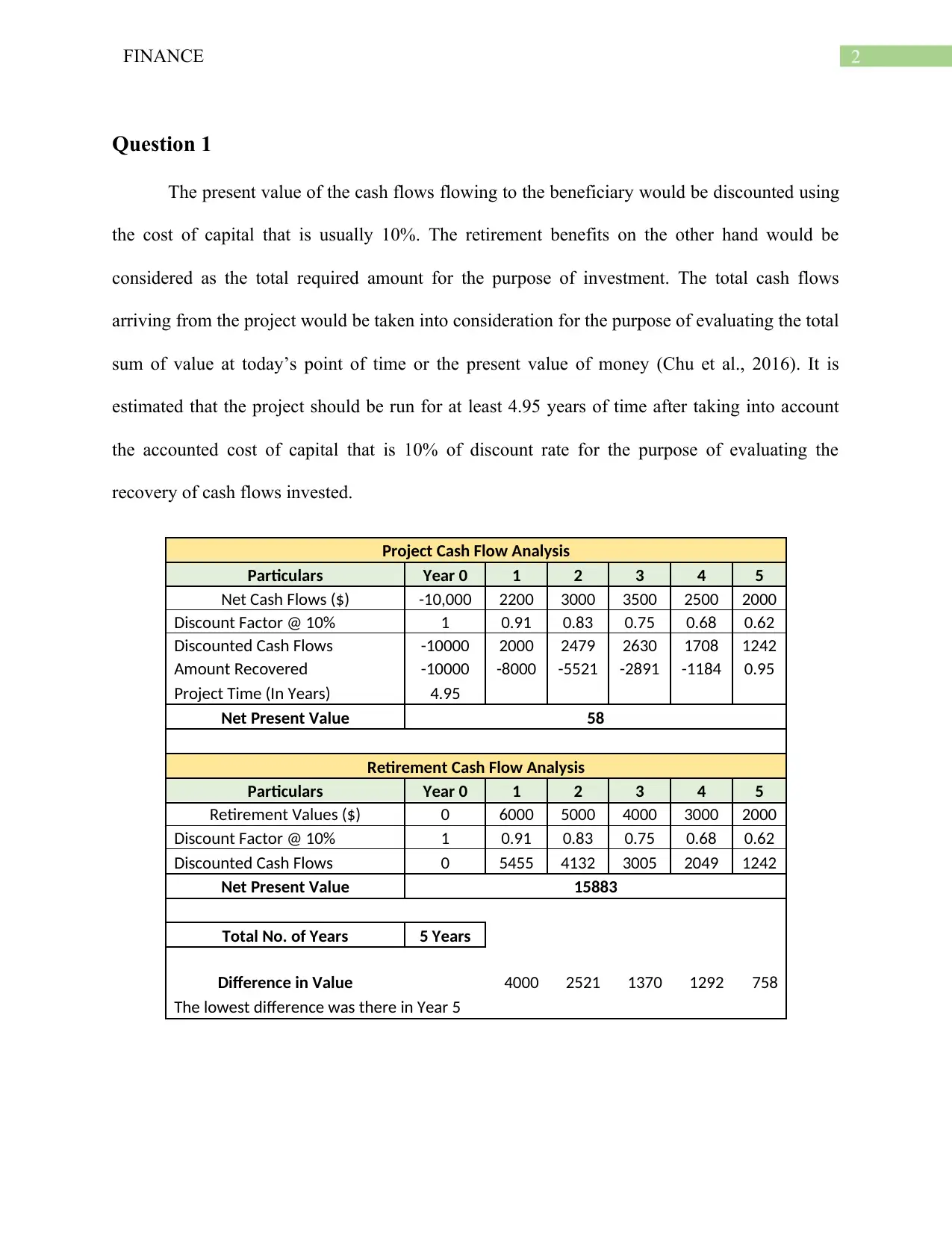

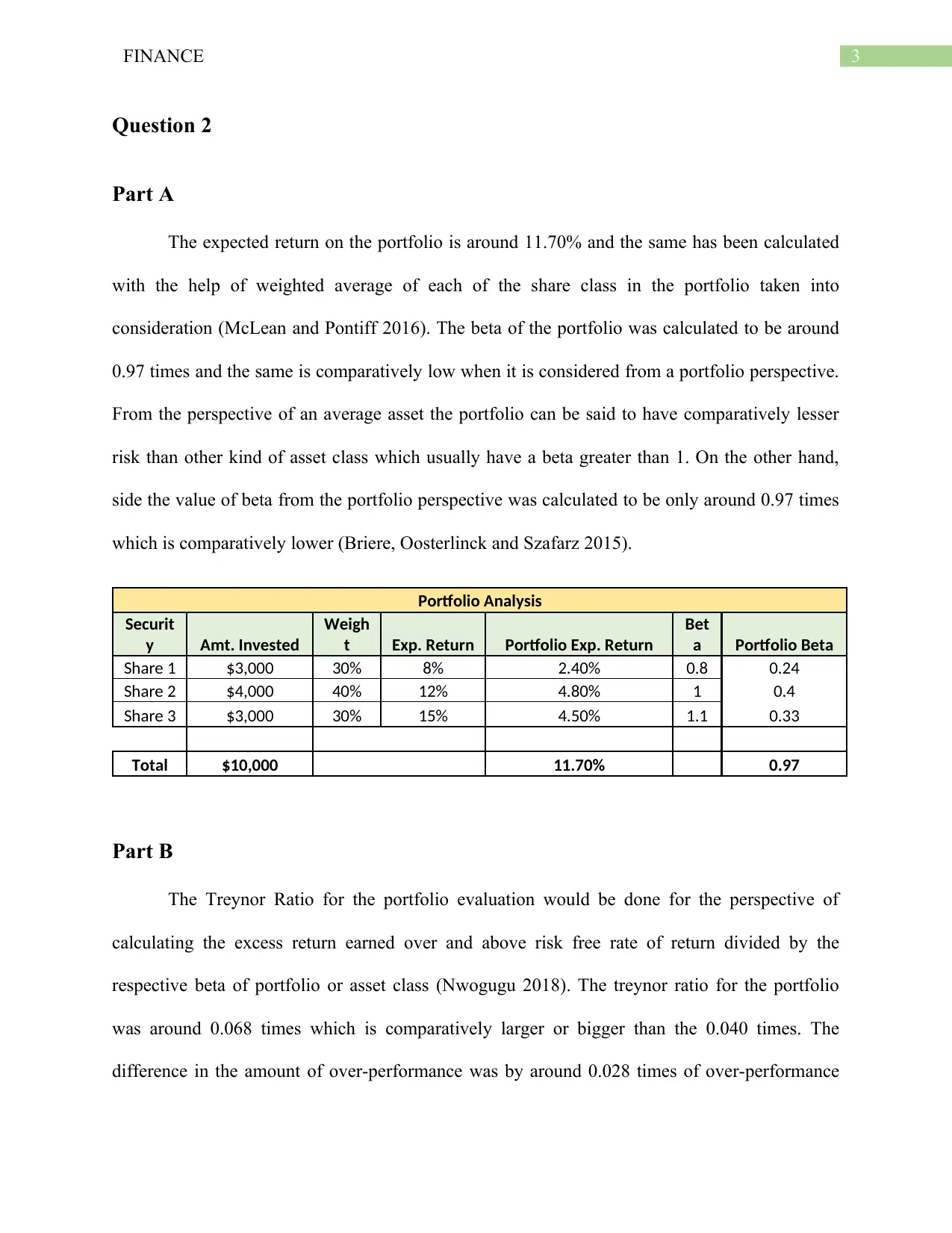

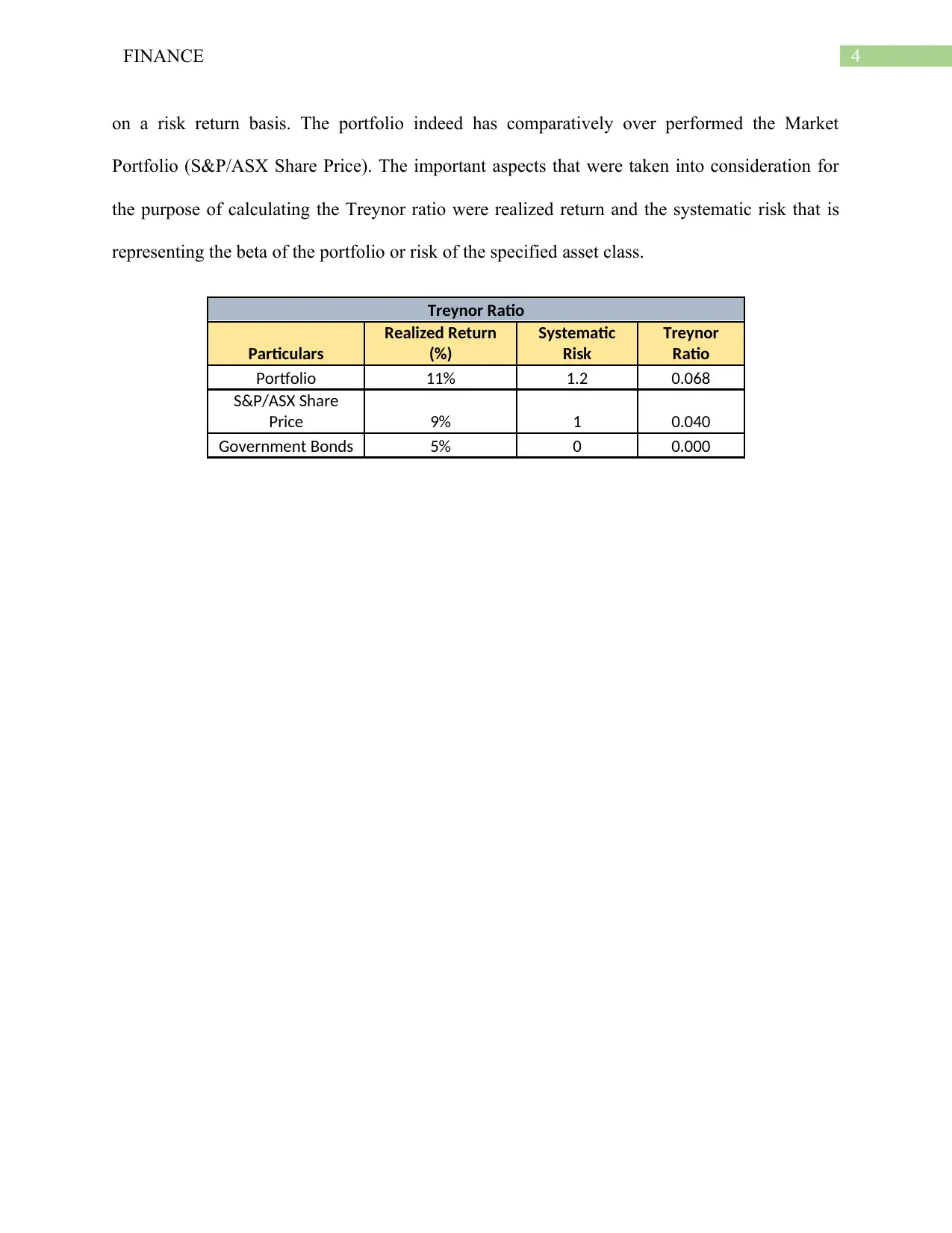

This finance assignment solution provides a detailed analysis of two key financial concepts: cash flow and portfolio management. The first section analyzes a project's cash flows to determine its present value and investment recovery period, considering a 10% discount rate. It calculates the net present value (NPV) and identifies the project's time frame. The second section delves into portfolio analysis, calculating the expected return and beta of a portfolio comprising three different shares. The assignment also determines the Treynor ratio to evaluate the portfolio's performance compared to a market portfolio (S&P/ASX Share Price) and government bonds, assessing the excess return relative to systematic risk.

1 out of 6

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.