Finance Assignment 2: Asset-Liability Management and Binomial Trees

VerifiedAdded on 2023/01/18

|3

|295

|76

Project

AI Summary

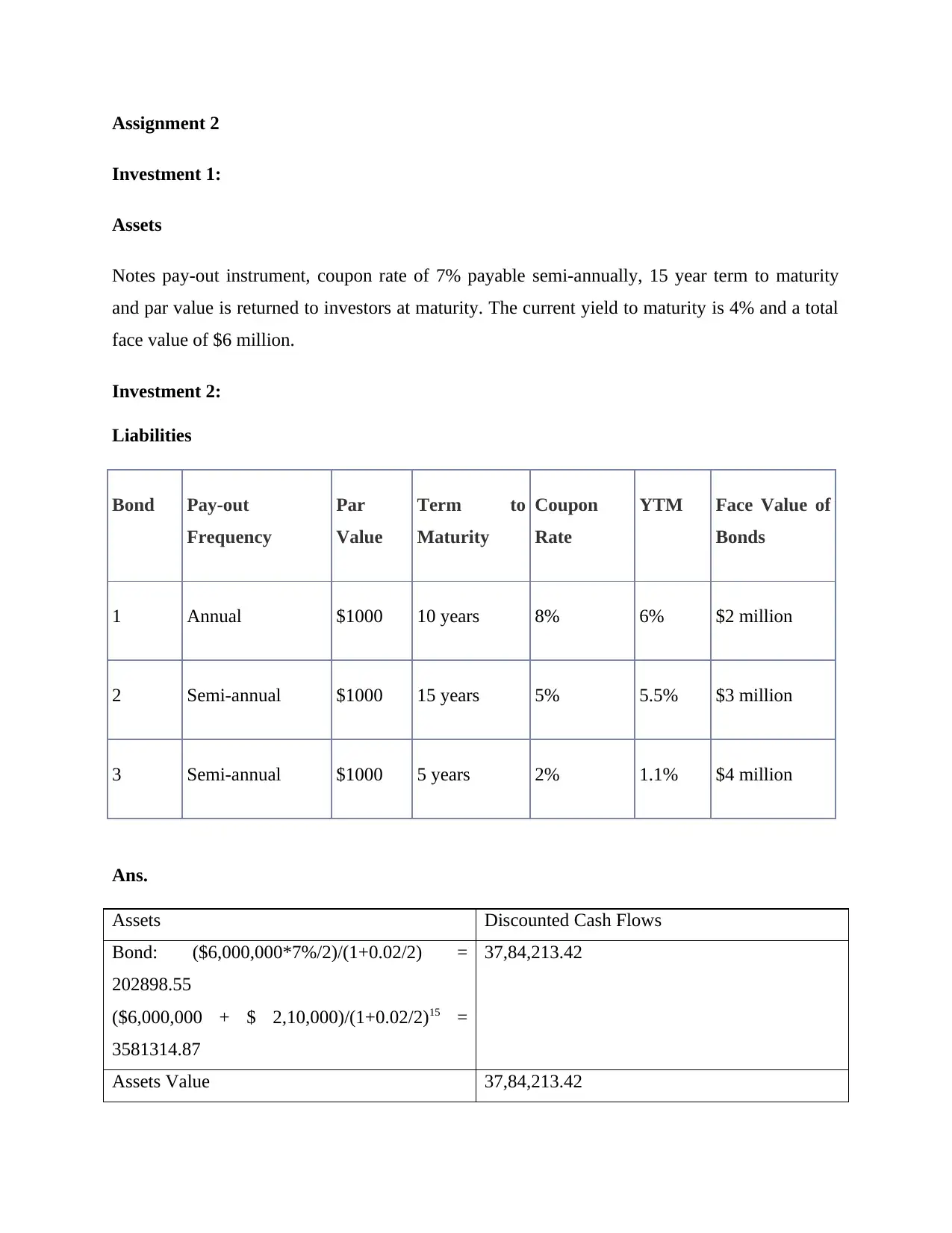

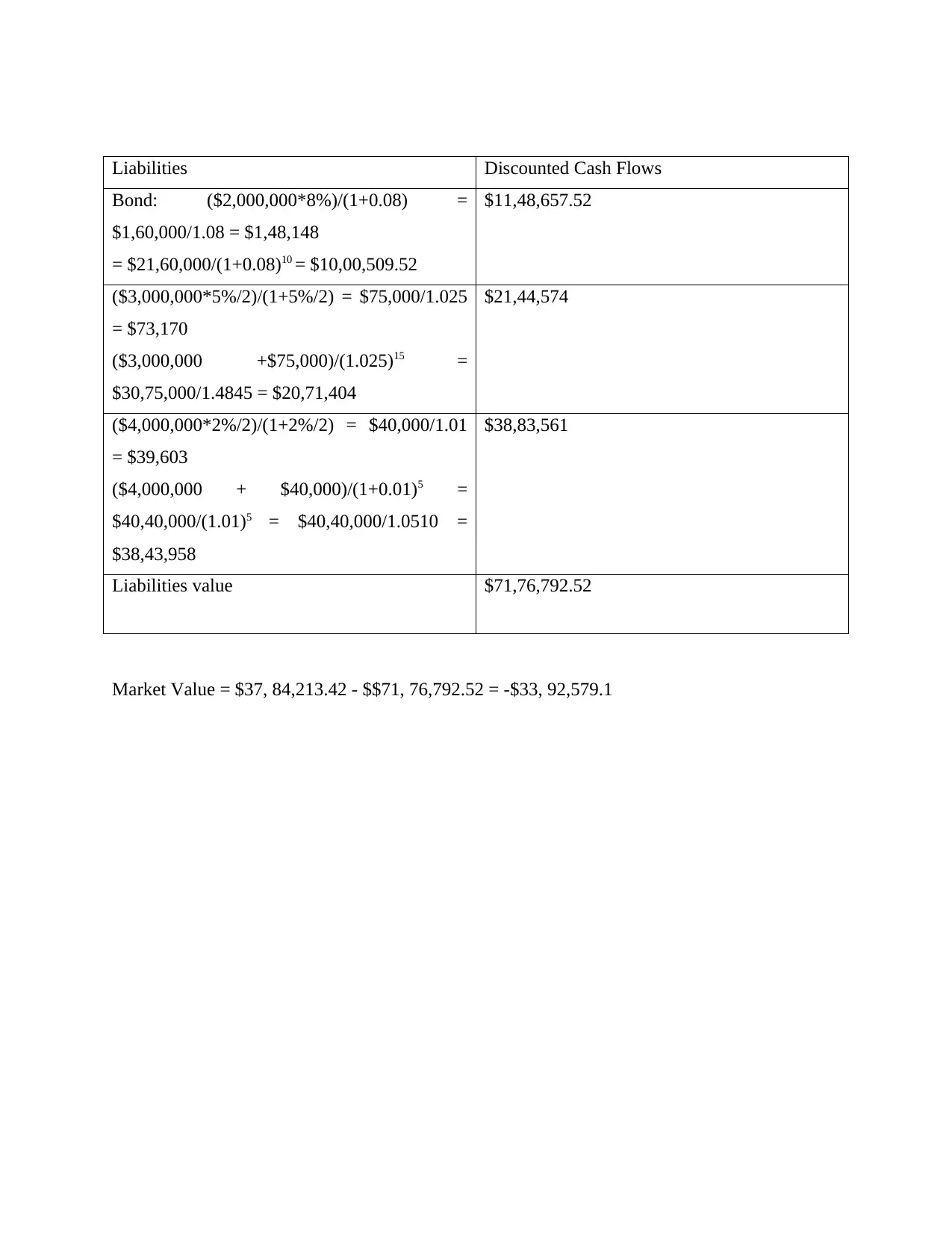

This finance assignment focuses on managing interest rate risk within a financial firm's asset and liability portfolio using a duration matching strategy. The assignment provides details on two investments and three bond liabilities, including coupon rates, terms to maturity, and yield to maturity. The solution involves calculating the present values of both assets and liabilities to balance the balance sheet. The calculations include discounted cash flows for the assets and liabilities, determining the market value of the portfolio. Furthermore, the assignment brief includes the construction of a three-year binomial interest rate tree using given spot rates, one-year forward rates, and volatility of the one-year forward rate to model interest rate movements over time. The goal is to balance the market value and duration of the investments to match the liabilities, effectively mitigating interest rate risk within the portfolio. The solution details the steps taken to calculate the bond values and the final market value of the portfolio, indicating a significant negative market value, highlighting the firm's potential exposure to interest rate fluctuations.

1 out of 3

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.