Corporate Finance Project Report: Portfolio Risk and Management

VerifiedAdded on 2023/06/04

|8

|1502

|248

Project

AI Summary

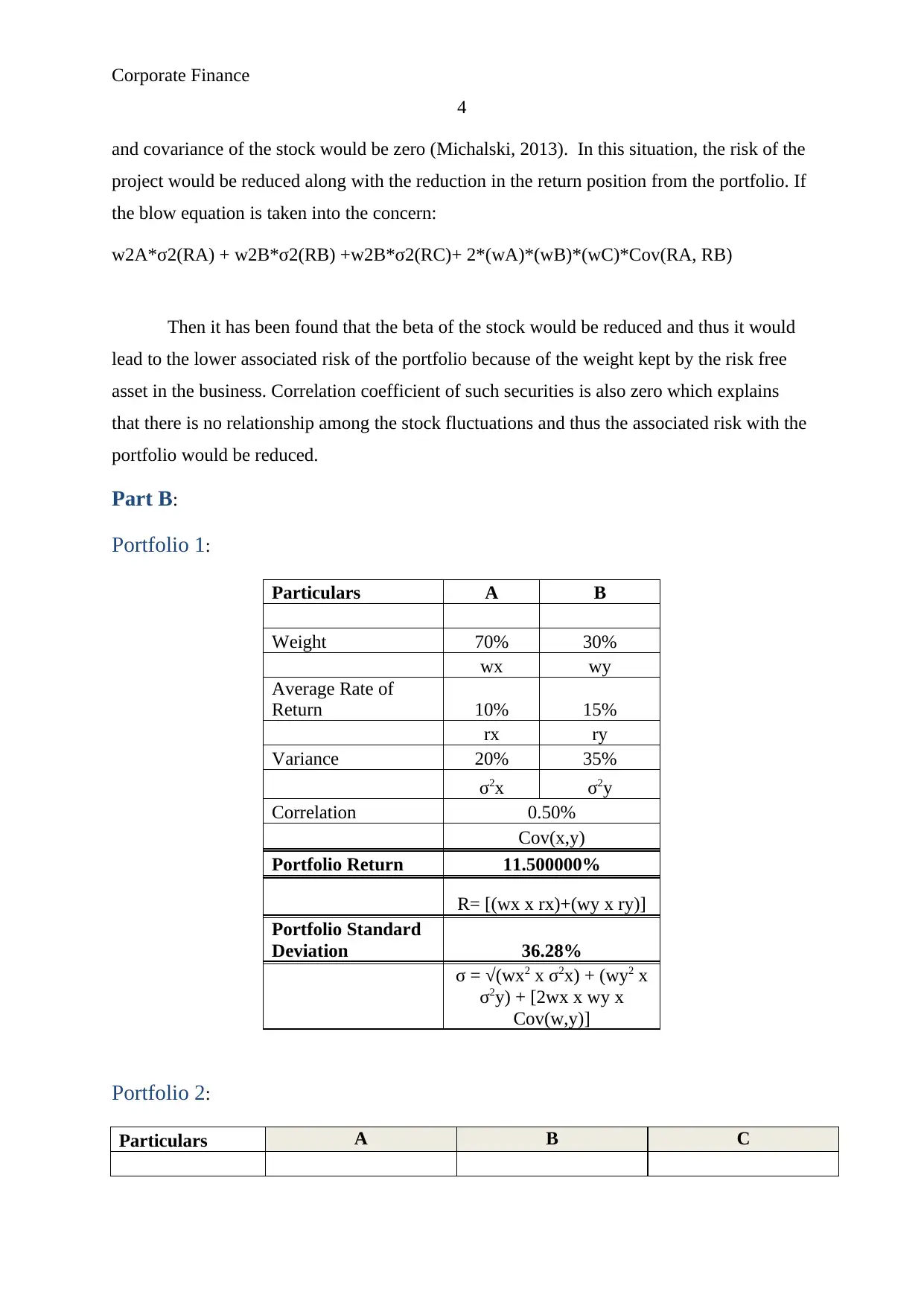

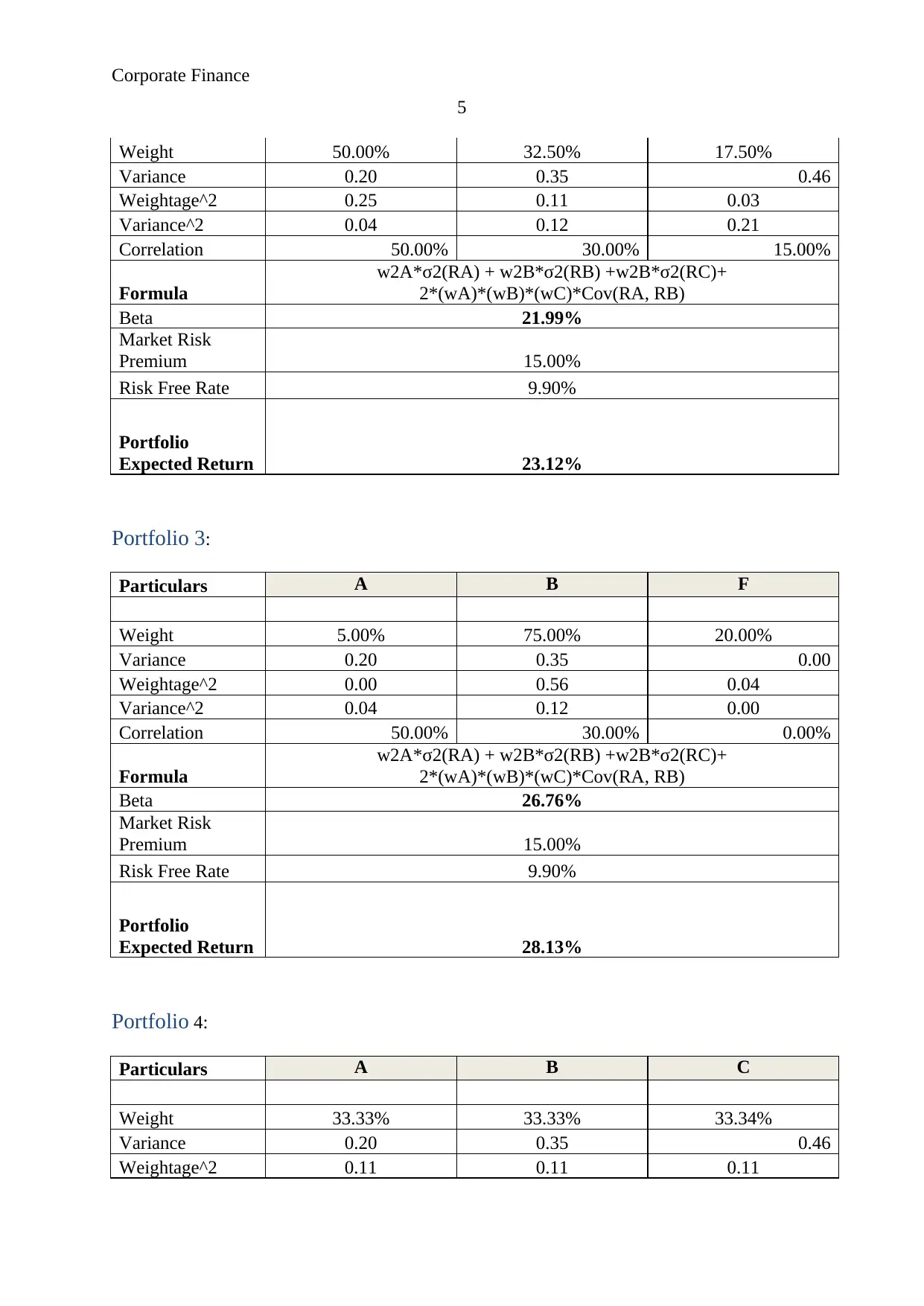

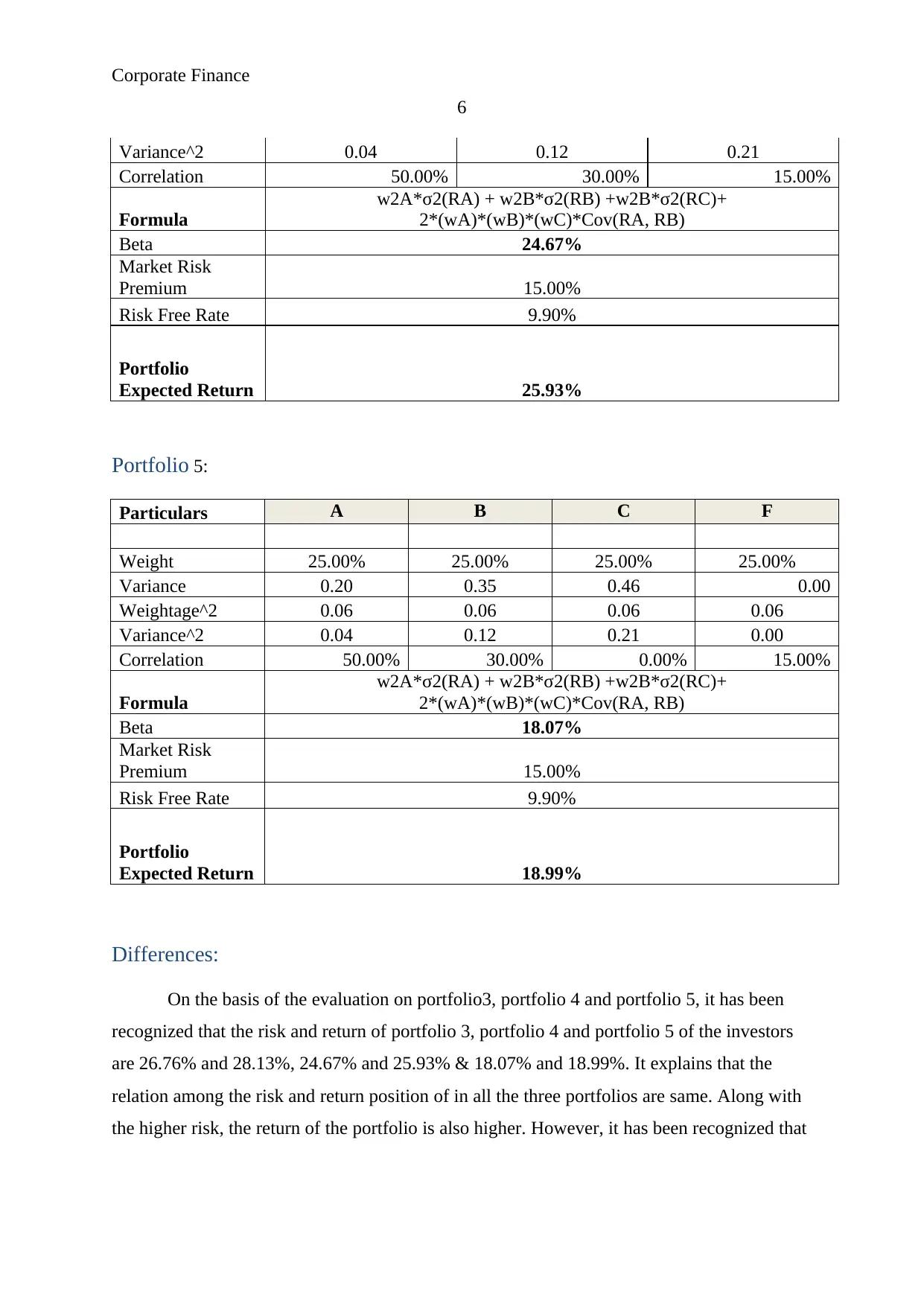

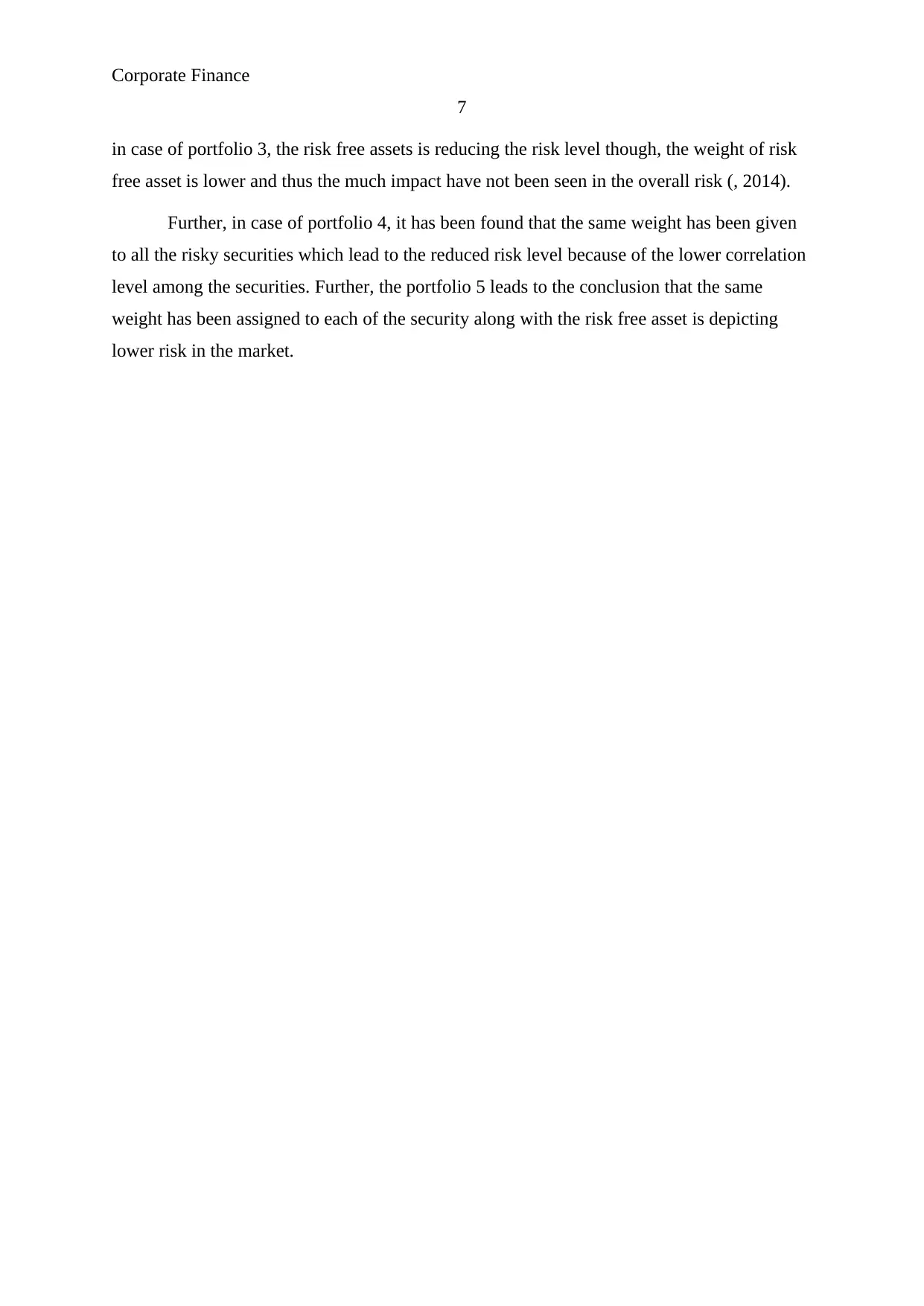

This corporate finance project report delves into the analysis of portfolio risk and return. Part A addresses key concepts such as standard deviation, risk reduction through portfolio diversification, and the impact of risk-free assets on portfolio risk. Part B presents five different portfolios with varying asset allocations, risk profiles, and expected returns. The analysis compares and contrasts the risk and return characteristics of portfolios 3, 4, and 5, highlighting the impact of risk-free assets and asset diversification on overall portfolio performance. The project employs standard deviation, correlation, and beta calculations to assess risk and return, providing insights into portfolio construction and risk management strategies.

1 out of 8

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.