Finance Portfolio Management Report: Employee Stock Options

VerifiedAdded on 2023/04/12

|11

|2238

|184

Report

AI Summary

This report provides a comprehensive analysis of finance portfolio management, addressing key aspects such as employee stock options and airline fuel cost hedging. Part 1 of the report focuses on employee stock options, utilizing the Black-Scholes model to determine option values and assess whether to exercise options immediately. It considers factors like the employee's potential departure and the inability to hedge the options. The report calculates the value of call options under different scenarios. Part 2 delves into the pros and cons of hedging airline fuel costs, examining the advantages of reducing costs, maximizing profits, and minimizing oil price volatility. It also discusses the disadvantages, including the downside of hedging when prices are favorable, the cost of hedges, potential for speculation, and the need for thorough research. The report provides insights into hedging strategies and their impact on airline profitability and risk management.

Running head: FINANCE PORTFOLIO MANAGEMENT

Finance Portfolio Management

Name of the Student:

Name of the University:

Authors Note:

Finance Portfolio Management

Name of the Student:

Name of the University:

Authors Note:

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

FINANCE PORTFOLIO MANAGEMENT

1

Table of Contents

Part 1:.........................................................................................................................................2

1 Indicating whether the options should be kept or exercised immediately, while detecting the

important determinants in making such decisions:....................................................................2

2 Indicating the minimum and maximum value assigned to the option:...................................3

Part 2: Discussing the pros and cons of hedging airline fuel costs by the airline companies....4

References and Bibliography:....................................................................................................9

1

Table of Contents

Part 1:.........................................................................................................................................2

1 Indicating whether the options should be kept or exercised immediately, while detecting the

important determinants in making such decisions:....................................................................2

2 Indicating the minimum and maximum value assigned to the option:...................................3

Part 2: Discussing the pros and cons of hedging airline fuel costs by the airline companies....4

References and Bibliography:....................................................................................................9

FINANCE PORTFOLIO MANAGEMENT

2

Part 1:

1 Indicating whether the options should be kept or exercised immediately, while

detecting the important determinants in making such decisions:

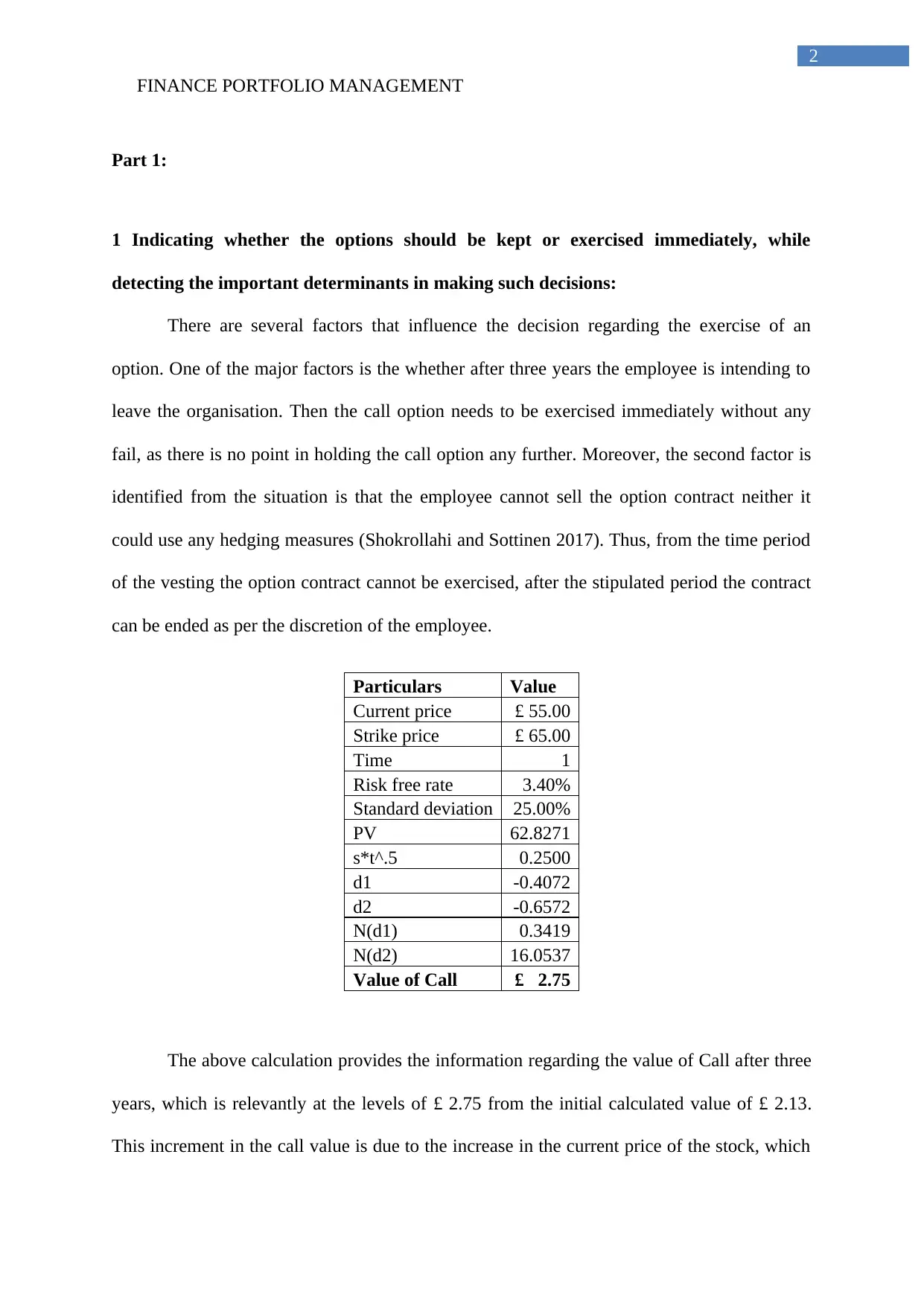

There are several factors that influence the decision regarding the exercise of an

option. One of the major factors is the whether after three years the employee is intending to

leave the organisation. Then the call option needs to be exercised immediately without any

fail, as there is no point in holding the call option any further. Moreover, the second factor is

identified from the situation is that the employee cannot sell the option contract neither it

could use any hedging measures (Shokrollahi and Sottinen 2017). Thus, from the time period

of the vesting the option contract cannot be exercised, after the stipulated period the contract

can be ended as per the discretion of the employee.

Particulars Value

Current price £ 55.00

Strike price £ 65.00

Time 1

Risk free rate 3.40%

Standard deviation 25.00%

PV 62.8271

s*t^.5 0.2500

d1 -0.4072

d2 -0.6572

N(d1) 0.3419

N(d2) 16.0537

Value of Call £ 2.75

The above calculation provides the information regarding the value of Call after three

years, which is relevantly at the levels of £ 2.75 from the initial calculated value of £ 2.13.

This increment in the call value is due to the increase in the current price of the stock, which

2

Part 1:

1 Indicating whether the options should be kept or exercised immediately, while

detecting the important determinants in making such decisions:

There are several factors that influence the decision regarding the exercise of an

option. One of the major factors is the whether after three years the employee is intending to

leave the organisation. Then the call option needs to be exercised immediately without any

fail, as there is no point in holding the call option any further. Moreover, the second factor is

identified from the situation is that the employee cannot sell the option contract neither it

could use any hedging measures (Shokrollahi and Sottinen 2017). Thus, from the time period

of the vesting the option contract cannot be exercised, after the stipulated period the contract

can be ended as per the discretion of the employee.

Particulars Value

Current price £ 55.00

Strike price £ 65.00

Time 1

Risk free rate 3.40%

Standard deviation 25.00%

PV 62.8271

s*t^.5 0.2500

d1 -0.4072

d2 -0.6572

N(d1) 0.3419

N(d2) 16.0537

Value of Call £ 2.75

The above calculation provides the information regarding the value of Call after three

years, which is relevantly at the levels of £ 2.75 from the initial calculated value of £ 2.13.

This increment in the call value is due to the increase in the current price of the stock, which

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

FINANCE PORTFOLIO MANAGEMENT

3

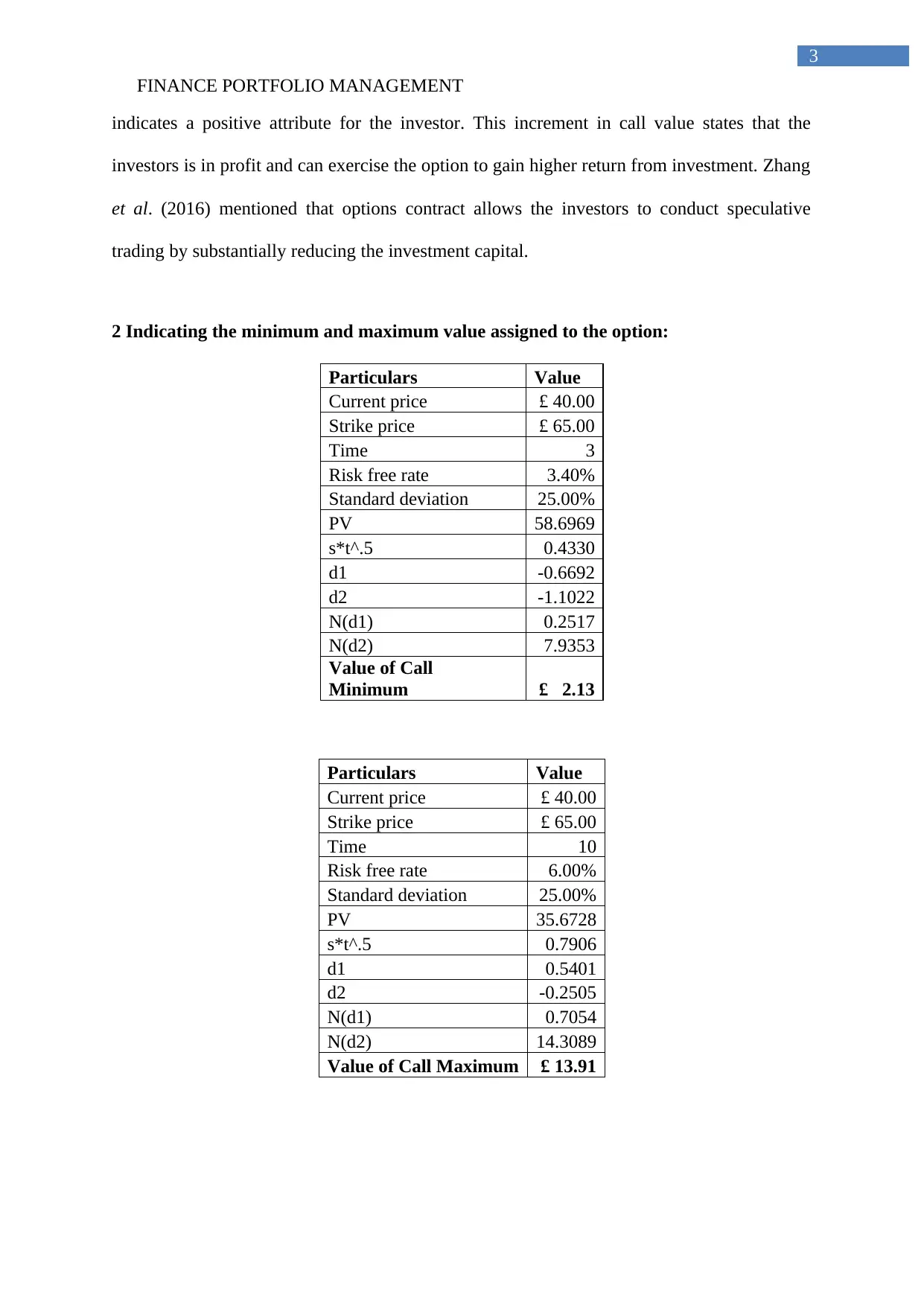

indicates a positive attribute for the investor. This increment in call value states that the

investors is in profit and can exercise the option to gain higher return from investment. Zhang

et al. (2016) mentioned that options contract allows the investors to conduct speculative

trading by substantially reducing the investment capital.

2 Indicating the minimum and maximum value assigned to the option:

Particulars Value

Current price £ 40.00

Strike price £ 65.00

Time 3

Risk free rate 3.40%

Standard deviation 25.00%

PV 58.6969

s*t^.5 0.4330

d1 -0.6692

d2 -1.1022

N(d1) 0.2517

N(d2) 7.9353

Value of Call

Minimum £ 2.13

Particulars Value

Current price £ 40.00

Strike price £ 65.00

Time 10

Risk free rate 6.00%

Standard deviation 25.00%

PV 35.6728

s*t^.5 0.7906

d1 0.5401

d2 -0.2505

N(d1) 0.7054

N(d2) 14.3089

Value of Call Maximum £ 13.91

3

indicates a positive attribute for the investor. This increment in call value states that the

investors is in profit and can exercise the option to gain higher return from investment. Zhang

et al. (2016) mentioned that options contract allows the investors to conduct speculative

trading by substantially reducing the investment capital.

2 Indicating the minimum and maximum value assigned to the option:

Particulars Value

Current price £ 40.00

Strike price £ 65.00

Time 3

Risk free rate 3.40%

Standard deviation 25.00%

PV 58.6969

s*t^.5 0.4330

d1 -0.6692

d2 -1.1022

N(d1) 0.2517

N(d2) 7.9353

Value of Call

Minimum £ 2.13

Particulars Value

Current price £ 40.00

Strike price £ 65.00

Time 10

Risk free rate 6.00%

Standard deviation 25.00%

PV 35.6728

s*t^.5 0.7906

d1 0.5401

d2 -0.2505

N(d1) 0.7054

N(d2) 14.3089

Value of Call Maximum £ 13.91

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

FINANCE PORTFOLIO MANAGEMENT

4

The above table provides information regarding the Black Scholes model, which is

used for detecting the value of the call option presented to the employees. The calculation has

used the time required for an employee in a call option, which is 3 years in minimum and

maximum time 10 years. The employee cannot exercise the call option during the vesting

period, as it will result in a loss, which indicates that a minimum investment period will be 3

years. Moreover, the maximum time allotted to the options is 10 years, as it is the expiration

date of the option (Sturm et al. 2017). This evaluation has helped in detecting the maximum

and minimum value of the call options presented to the employees. Thus, after using the

Black Scholes model the maximum value of call is detected as £ 13.91 and minimum value of

call is at £ 2.13.

Part 2: Discussing the pros and cons of hedging airline fuel costs by the airline

companies

Airline company managers rely on derivatives, options and swaps for limiting down

the risk involved in fuel cost and minimise the expenses involved in operations. The manager

has been using the hedging measure for accurately curbing the risk from volatile oil prices,

which changes due to the fluctuations in production and demand. Fuel cost is considered a

major expense for airline companies, as it is needed for running the airbus. Thus, hedging the

volatile cost of fuel is essential for the Airline companies, as it reduces the risk of increasing

the fuel cost, which is required to increase their operations. The hedging of oil prices locks

and stabilise the fuel cost of airline companies, as other costs related to operations are less

volatile. Therefore, manager use the hedging process to increase stability in cost and raise

stability in profits (Korkeamaki, Liljeblom and Pfister 2016). Airline companies mainly

hedge 2/3 of their expected fuel costs, which will be conducted within 6 months to 1 year.

4

The above table provides information regarding the Black Scholes model, which is

used for detecting the value of the call option presented to the employees. The calculation has

used the time required for an employee in a call option, which is 3 years in minimum and

maximum time 10 years. The employee cannot exercise the call option during the vesting

period, as it will result in a loss, which indicates that a minimum investment period will be 3

years. Moreover, the maximum time allotted to the options is 10 years, as it is the expiration

date of the option (Sturm et al. 2017). This evaluation has helped in detecting the maximum

and minimum value of the call options presented to the employees. Thus, after using the

Black Scholes model the maximum value of call is detected as £ 13.91 and minimum value of

call is at £ 2.13.

Part 2: Discussing the pros and cons of hedging airline fuel costs by the airline

companies

Airline company managers rely on derivatives, options and swaps for limiting down

the risk involved in fuel cost and minimise the expenses involved in operations. The manager

has been using the hedging measure for accurately curbing the risk from volatile oil prices,

which changes due to the fluctuations in production and demand. Fuel cost is considered a

major expense for airline companies, as it is needed for running the airbus. Thus, hedging the

volatile cost of fuel is essential for the Airline companies, as it reduces the risk of increasing

the fuel cost, which is required to increase their operations. The hedging of oil prices locks

and stabilise the fuel cost of airline companies, as other costs related to operations are less

volatile. Therefore, manager use the hedging process to increase stability in cost and raise

stability in profits (Korkeamaki, Liljeblom and Pfister 2016). Airline companies mainly

hedge 2/3 of their expected fuel costs, which will be conducted within 6 months to 1 year.

FINANCE PORTFOLIO MANAGEMENT

5

There are simply relevant pros and cons of hedging airline fuel cost by the airline companies,

which are depicted as follows.

Advantages of hedging airline fuel cost:

Reduction in cost:

The major benefit that will be generated from the hedging process used by Airline

companies is the reduction in cost levels. The oil prices are considered to be volatile in

nature, which relevantly changes over the period of time. Thus, the use of hedging process

can help in minimising the cost involved in fuel expenses. This reduction in the cost will

allow the Airline companies to minimise the expenses incurred in operations. Corley and

Advisors (2016) stated that hedging process allows the airline companies to mitigate the risk

that is projected from the fluctuating oil prices, which in turn reduces the total expenses

incurred by the company. However, without the hedging process the fluctuating price of oil

can increase the total expenses of the airline companies and reduce the total income that can

be generated from operations. The managers use hedging process such as forward contract,

future contract, swaps and collars for adequately reducing the risk involved in fuel cost.

Maximisation of profits:

The use of hedging process also allows the airline companies to maximise the profit

level and maintain adequate revenue from operations. The adoption of the hedging process

can benefit the airline companies immensely, as they would reduce the risk from volatile oil

prices and fixed the actual cost of fuel needed in the operations. Thus, it is essential for the

managers to use hedging process, as it fixes the cost of fuel and maximises the probability of

achieving higher profits from operations. The hedging process needs adequate anticipation of

oil prices in future, which can help in generating high level of income from operations. Thus,

5

There are simply relevant pros and cons of hedging airline fuel cost by the airline companies,

which are depicted as follows.

Advantages of hedging airline fuel cost:

Reduction in cost:

The major benefit that will be generated from the hedging process used by Airline

companies is the reduction in cost levels. The oil prices are considered to be volatile in

nature, which relevantly changes over the period of time. Thus, the use of hedging process

can help in minimising the cost involved in fuel expenses. This reduction in the cost will

allow the Airline companies to minimise the expenses incurred in operations. Corley and

Advisors (2016) stated that hedging process allows the airline companies to mitigate the risk

that is projected from the fluctuating oil prices, which in turn reduces the total expenses

incurred by the company. However, without the hedging process the fluctuating price of oil

can increase the total expenses of the airline companies and reduce the total income that can

be generated from operations. The managers use hedging process such as forward contract,

future contract, swaps and collars for adequately reducing the risk involved in fuel cost.

Maximisation of profits:

The use of hedging process also allows the airline companies to maximise the profit

level and maintain adequate revenue from operations. The adoption of the hedging process

can benefit the airline companies immensely, as they would reduce the risk from volatile oil

prices and fixed the actual cost of fuel needed in the operations. Thus, it is essential for the

managers to use hedging process, as it fixes the cost of fuel and maximises the probability of

achieving higher profits from operations. The hedging process needs adequate anticipation of

oil prices in future, which can help in generating high level of income from operations. Thus,

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

FINANCE PORTFOLIO MANAGEMENT

6

managers to maximise the profit level of airline companies use hedging process such as

forward contract, future contract, swaps and collars to reduce the actual cost and fix the total

expense of fuel. Turner and Lim (2015) indicated that hedging process also reduces the

benefit that can be generated from positive price movements.

Reducing the volatility in oil prices:

The hedging process is an adequate measure that is used by the airline companies for

adequately minimising the volatility in oil prices, which is a constant event in the oil market.

Oil prices having been fluctuating due to the contract shift in demand and production output.

This constant change in pricing of oil alternates the cost of fuel that is used by the airline

companies. Hence, the use of hedging instruments helps in minimising the volatility that is

present in oil prices, while fixing the actual price of oil. Airline companies use future

contracts for delivery of the oil at specific price regardless the fluctuations that occur and

change the oil prices. The airline companies are provided certainty regarding the cost of fuel

that is incurred to maintain the adequate level of productivity (Dafir and Gajjala 2016). Thus,

airline companies can reduce the price volatility of oil, which helps in maximising the profits

and minimising the cost involved in operations.

Disadvantages of hedging airline fuel cost:

Downside of hedging:

The major disadvantage of hedging airline fuel cost is when the prices are favouring

the company. The reducing value of oil prices would eventually increase the benefits that is

projected to the airline company. For example, during the period of 2014 to 2015 the oil

prices in the market reduced sharply, where the airline companies that hedged against the

volatility did not get the benefits of the reduced prices. This directly indicates that within

6

managers to maximise the profit level of airline companies use hedging process such as

forward contract, future contract, swaps and collars to reduce the actual cost and fix the total

expense of fuel. Turner and Lim (2015) indicated that hedging process also reduces the

benefit that can be generated from positive price movements.

Reducing the volatility in oil prices:

The hedging process is an adequate measure that is used by the airline companies for

adequately minimising the volatility in oil prices, which is a constant event in the oil market.

Oil prices having been fluctuating due to the contract shift in demand and production output.

This constant change in pricing of oil alternates the cost of fuel that is used by the airline

companies. Hence, the use of hedging instruments helps in minimising the volatility that is

present in oil prices, while fixing the actual price of oil. Airline companies use future

contracts for delivery of the oil at specific price regardless the fluctuations that occur and

change the oil prices. The airline companies are provided certainty regarding the cost of fuel

that is incurred to maintain the adequate level of productivity (Dafir and Gajjala 2016). Thus,

airline companies can reduce the price volatility of oil, which helps in maximising the profits

and minimising the cost involved in operations.

Disadvantages of hedging airline fuel cost:

Downside of hedging:

The major disadvantage of hedging airline fuel cost is when the prices are favouring

the company. The reducing value of oil prices would eventually increase the benefits that is

projected to the airline company. For example, during the period of 2014 to 2015 the oil

prices in the market reduced sharply, where the airline companies that hedged against the

volatility did not get the benefits of the reduced prices. This directly indicates that within

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

FINANCE PORTFOLIO MANAGEMENT

7

active hedging airline companies cannot benefit when the prices are moving at a favourable

point. This can be considered a major downside of hedging, as it fixes the fuel cost and

restricts the organisation to benefit from the favourable price action (Hu, Xiao and Jiang

2018).

Cost of hedges:

The second major drawback of hedging is the cost of hedges, which is considered to

be high, as banks providing the services of hedge needs premiums from the relevant traders

and airline companies. Thus, the high cost incurred by using the hedging process also raises

the cost of production, which in turn reduces the level of income that is generated from

operations. There are specific times when the prices of oil do not fluctuate and benefit the

airline companies. In these instances, the cost of hedge raises the total expenses of the airline

companies and is considered to be a major limitation to the organisation. The use of hedging

contract requires additional cost, which needs to be borne by the airline companies regardless

of the benefits that can be generated from operations (Fukui and Miyoshi 2017).

Speculations:

The hedging instruments such as forward contract, future contract, swaps and collars

can be used by investors for conducting relevant speculation investment strategy. The airline

companies use the hedging measure on the basis of their expected expenses that will be

incurred in near future. However, no delivery of the actual oil is conducted by the airline

companies, which is relevant considered as speculation trading. There are many investors

who use the speculative strategy for increasing their income from the trades. However, due to

the absence of the underlying product the risk can be more severe, which can hamper the

investment capital of the investors (Miyoshi and Fukui 2018). Thus, airline companies who

use speculative hedging process will have high risk involved with their hedging exposure.

7

active hedging airline companies cannot benefit when the prices are moving at a favourable

point. This can be considered a major downside of hedging, as it fixes the fuel cost and

restricts the organisation to benefit from the favourable price action (Hu, Xiao and Jiang

2018).

Cost of hedges:

The second major drawback of hedging is the cost of hedges, which is considered to

be high, as banks providing the services of hedge needs premiums from the relevant traders

and airline companies. Thus, the high cost incurred by using the hedging process also raises

the cost of production, which in turn reduces the level of income that is generated from

operations. There are specific times when the prices of oil do not fluctuate and benefit the

airline companies. In these instances, the cost of hedge raises the total expenses of the airline

companies and is considered to be a major limitation to the organisation. The use of hedging

contract requires additional cost, which needs to be borne by the airline companies regardless

of the benefits that can be generated from operations (Fukui and Miyoshi 2017).

Speculations:

The hedging instruments such as forward contract, future contract, swaps and collars

can be used by investors for conducting relevant speculation investment strategy. The airline

companies use the hedging measure on the basis of their expected expenses that will be

incurred in near future. However, no delivery of the actual oil is conducted by the airline

companies, which is relevant considered as speculation trading. There are many investors

who use the speculative strategy for increasing their income from the trades. However, due to

the absence of the underlying product the risk can be more severe, which can hamper the

investment capital of the investors (Miyoshi and Fukui 2018). Thus, airline companies who

use speculative hedging process will have high risk involved with their hedging exposure.

FINANCE PORTFOLIO MANAGEMENT

8

Lack of appropriate research:

The fourth major limitation of hedging process is the lack of appropriate research by

the airline companies. The low level of research on the fluctuations of the oil can be

conducted by the airline companies, which will directly result in higher cost of fuel. The

airline companies need adequate research to anticipate the future price action of oil, as

without the information the wrong hedging strategy could increase losses and also raise the

cost of fuel incurred by the organisation. One of the major failures in hedging process was

recorded by Delta Airlines, where the CEO admitted about the loss of $4 billion in oil hedges

that was incurred by the organisation (Forbes.com 2019). The high level of losses incurred by

Delta Airlines was from the wrong anticipation of the oil price movement and hedge strategy.

Thus, it can be estimated that the lack of appropriate knowledge and research can lead to

major loss for the airline company, while increasing the risk involved in operations.

8

Lack of appropriate research:

The fourth major limitation of hedging process is the lack of appropriate research by

the airline companies. The low level of research on the fluctuations of the oil can be

conducted by the airline companies, which will directly result in higher cost of fuel. The

airline companies need adequate research to anticipate the future price action of oil, as

without the information the wrong hedging strategy could increase losses and also raise the

cost of fuel incurred by the organisation. One of the major failures in hedging process was

recorded by Delta Airlines, where the CEO admitted about the loss of $4 billion in oil hedges

that was incurred by the organisation (Forbes.com 2019). The high level of losses incurred by

Delta Airlines was from the wrong anticipation of the oil price movement and hedge strategy.

Thus, it can be estimated that the lack of appropriate knowledge and research can lead to

major loss for the airline company, while increasing the risk involved in operations.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

FINANCE PORTFOLIO MANAGEMENT

9

References and Bibliography:

Bayram, M., Orucova Buyukoz, G. and Partal, T., 2018. Parameter Estimation in a Black-

Scholes Model. Thermal Science, 22(1), pp.S117-S122.

Corley, M. and Advisors, M.E., 2016. Airline fuel hedging in 2016 & beyond. Airline

Economics Growth Frontiers, Dubai.

Dafir, S.M. and Gajjala, V.N., 2016. Fuel Hedging and Risk Management: Strategies for

Airlines, Shippers and Other Consumers. John Wiley & Sons.

Forbes.com. 2019. Forbes. [online] Available at: https://www.forbes.com/ [Accessed 26 Mar.

2019].

Fukui, H. and Miyoshi, C., 2017. The impact of aviation fuel tax on fuel consumption and

carbon emissions: The case of the US airline industry. Transportation Research Part D:

Transport and Environment, 50, pp.234-253.

Hu, R., Xiao, Y.B. and Jiang, C., 2018. Jet fuel hedging, operational fuel efficiency

improvement and carbon tax. Transportation Research Part B: Methodological, 116, pp.103-

123.

Korkeamäki, T., Liljeblom, E. and Pfister, M., 2016. Airline fuel hedging and management

ownership. The Journal of Risk Finance, 17(5), pp.492-509.

Lim, S.H. and Turner, P.A., 2016. Airline Fuel Hedging: Do Hedge Horizon and Contract

Maturity Matter?. In Journal of the Transportation Research Forum (Vol. 55, No. 1424-

2017-1739).

9

References and Bibliography:

Bayram, M., Orucova Buyukoz, G. and Partal, T., 2018. Parameter Estimation in a Black-

Scholes Model. Thermal Science, 22(1), pp.S117-S122.

Corley, M. and Advisors, M.E., 2016. Airline fuel hedging in 2016 & beyond. Airline

Economics Growth Frontiers, Dubai.

Dafir, S.M. and Gajjala, V.N., 2016. Fuel Hedging and Risk Management: Strategies for

Airlines, Shippers and Other Consumers. John Wiley & Sons.

Forbes.com. 2019. Forbes. [online] Available at: https://www.forbes.com/ [Accessed 26 Mar.

2019].

Fukui, H. and Miyoshi, C., 2017. The impact of aviation fuel tax on fuel consumption and

carbon emissions: The case of the US airline industry. Transportation Research Part D:

Transport and Environment, 50, pp.234-253.

Hu, R., Xiao, Y.B. and Jiang, C., 2018. Jet fuel hedging, operational fuel efficiency

improvement and carbon tax. Transportation Research Part B: Methodological, 116, pp.103-

123.

Korkeamäki, T., Liljeblom, E. and Pfister, M., 2016. Airline fuel hedging and management

ownership. The Journal of Risk Finance, 17(5), pp.492-509.

Lim, S.H. and Turner, P.A., 2016. Airline Fuel Hedging: Do Hedge Horizon and Contract

Maturity Matter?. In Journal of the Transportation Research Forum (Vol. 55, No. 1424-

2017-1739).

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

FINANCE PORTFOLIO MANAGEMENT

10

Miyoshi, C. and Fukui, H., 2018. Measuring the rebound effects in air transport: The impact

of jet fuel prices and air carriers’ fuel efficiency improvement of the European

airlines. Transportation Research Part A: Policy and Practice, 112, pp.71-84.

Shokrollahi, F. and Sottinen, T., 2017. Hedging in fractional Black–Scholes model with

transaction costs. Statistics & Probability Letters, 130, pp.85-91.

Sibdari, S., Mohammadian, I. and Pyke, D.F., 2018. On the impact of jet fuel cost on airlines’

capacity choice: Evidence from the US domestic markets. Transportation Research Part E:

Logistics and Transportation Review, 111, pp.1-17.

Sturm, M., Goldstein, M.A., Huntington, H. and Douglas, T.A., 2017. Using an option

pricing approach to evaluate strategic decisions in a rapidly changing climate: Black–Scholes

and climate change. Climatic Change, 140(3-4), pp.437-449.

Turner, P.A. and Lim, S.H., 2015. Hedging jet fuel price risk: The case of US passenger

airlines. Journal of Air Transport Management, 44, pp.54-64.

Zhang, H., Liu, F., Turner, I. and Yang, Q., 2016. Numerical solution of the time fractional

Black–Scholes model governing European options. Computers & Mathematics with

Applications, 71(9), pp.1772-1783.

10

Miyoshi, C. and Fukui, H., 2018. Measuring the rebound effects in air transport: The impact

of jet fuel prices and air carriers’ fuel efficiency improvement of the European

airlines. Transportation Research Part A: Policy and Practice, 112, pp.71-84.

Shokrollahi, F. and Sottinen, T., 2017. Hedging in fractional Black–Scholes model with

transaction costs. Statistics & Probability Letters, 130, pp.85-91.

Sibdari, S., Mohammadian, I. and Pyke, D.F., 2018. On the impact of jet fuel cost on airlines’

capacity choice: Evidence from the US domestic markets. Transportation Research Part E:

Logistics and Transportation Review, 111, pp.1-17.

Sturm, M., Goldstein, M.A., Huntington, H. and Douglas, T.A., 2017. Using an option

pricing approach to evaluate strategic decisions in a rapidly changing climate: Black–Scholes

and climate change. Climatic Change, 140(3-4), pp.437-449.

Turner, P.A. and Lim, S.H., 2015. Hedging jet fuel price risk: The case of US passenger

airlines. Journal of Air Transport Management, 44, pp.54-64.

Zhang, H., Liu, F., Turner, I. and Yang, Q., 2016. Numerical solution of the time fractional

Black–Scholes model governing European options. Computers & Mathematics with

Applications, 71(9), pp.1772-1783.

1 out of 11

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.