Finance Presentation: COVID-19 Impact on Australian Stocks

VerifiedAdded on 2022/09/13

|12

|525

|17

Presentation

AI Summary

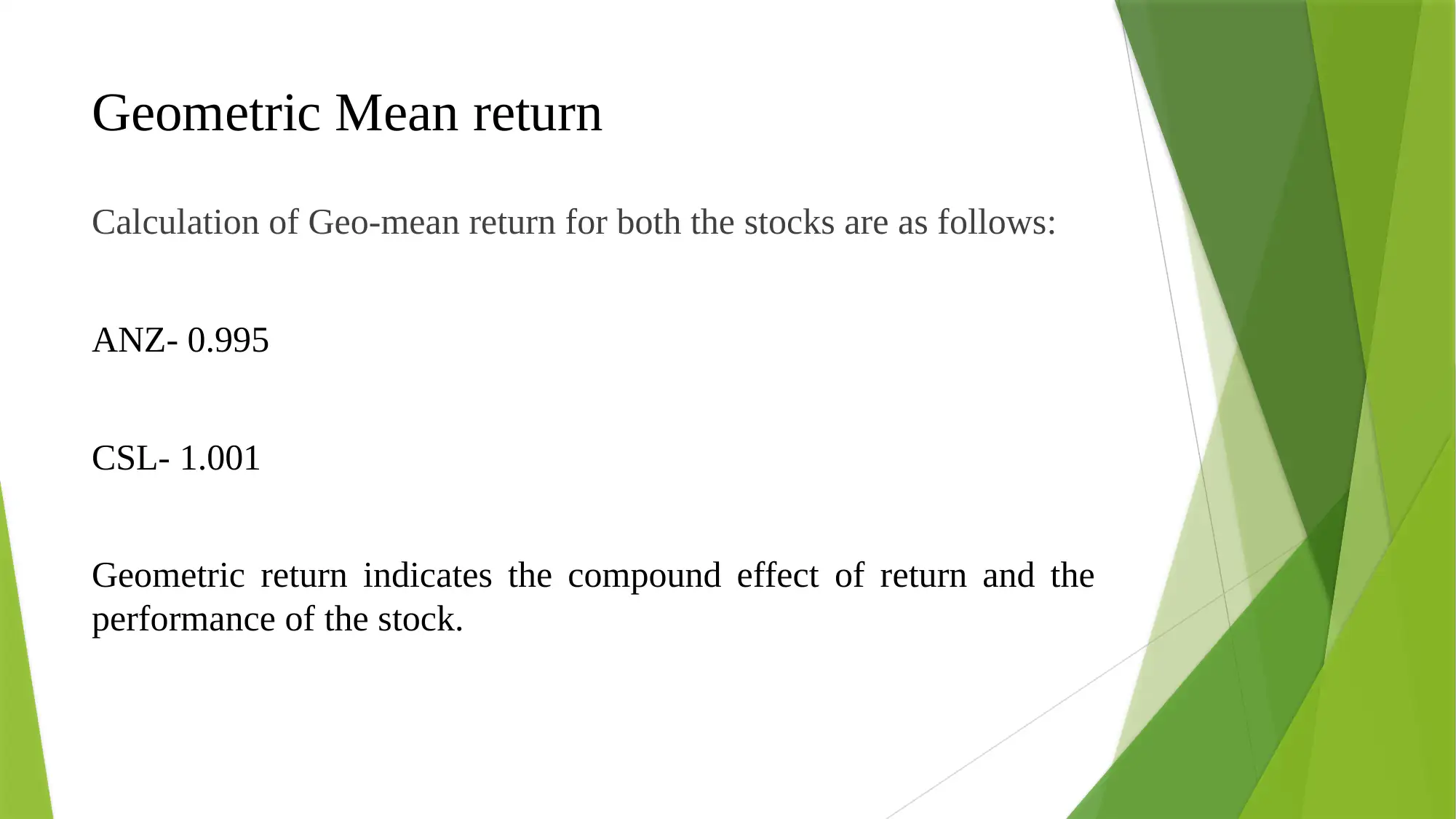

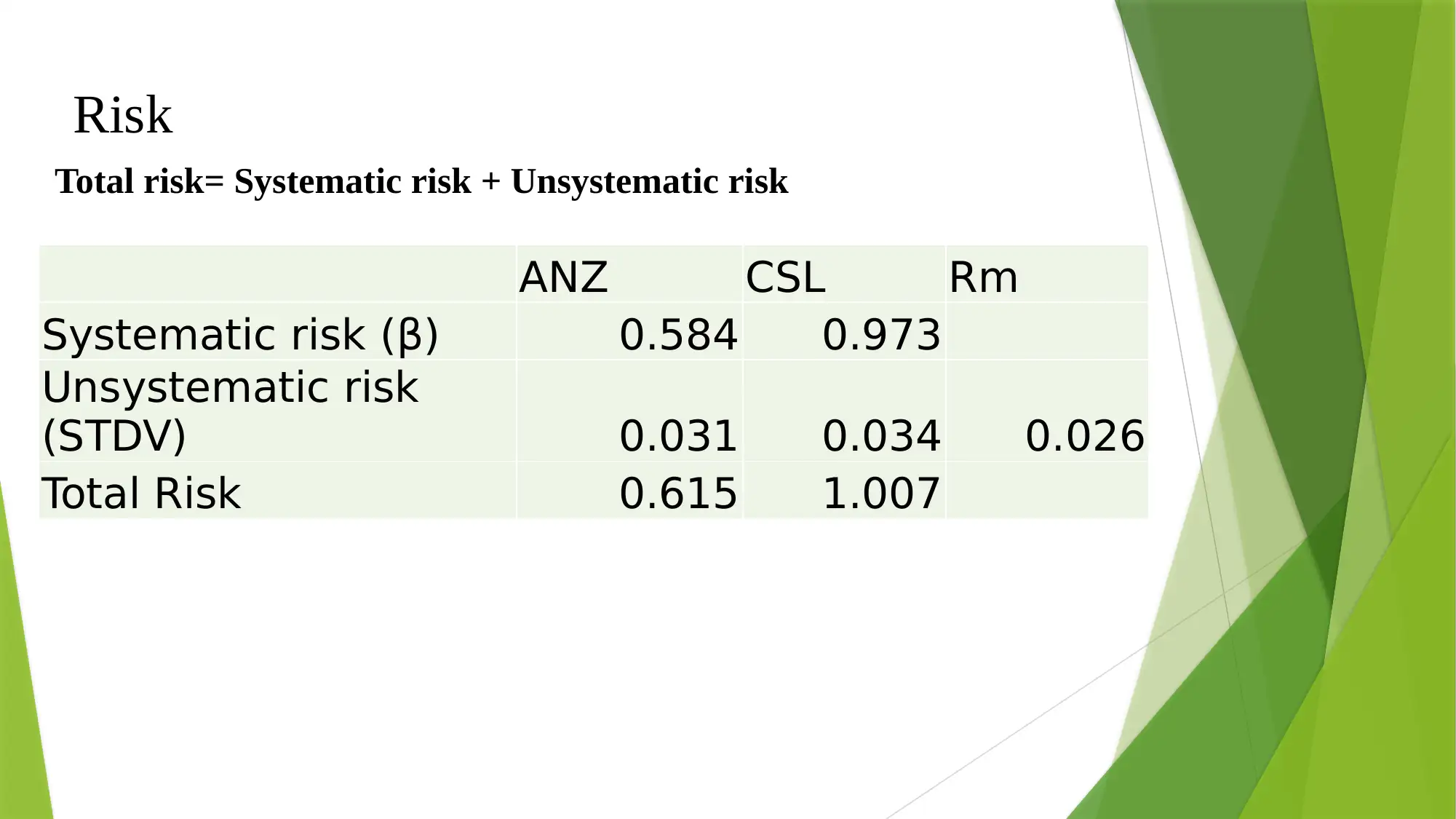

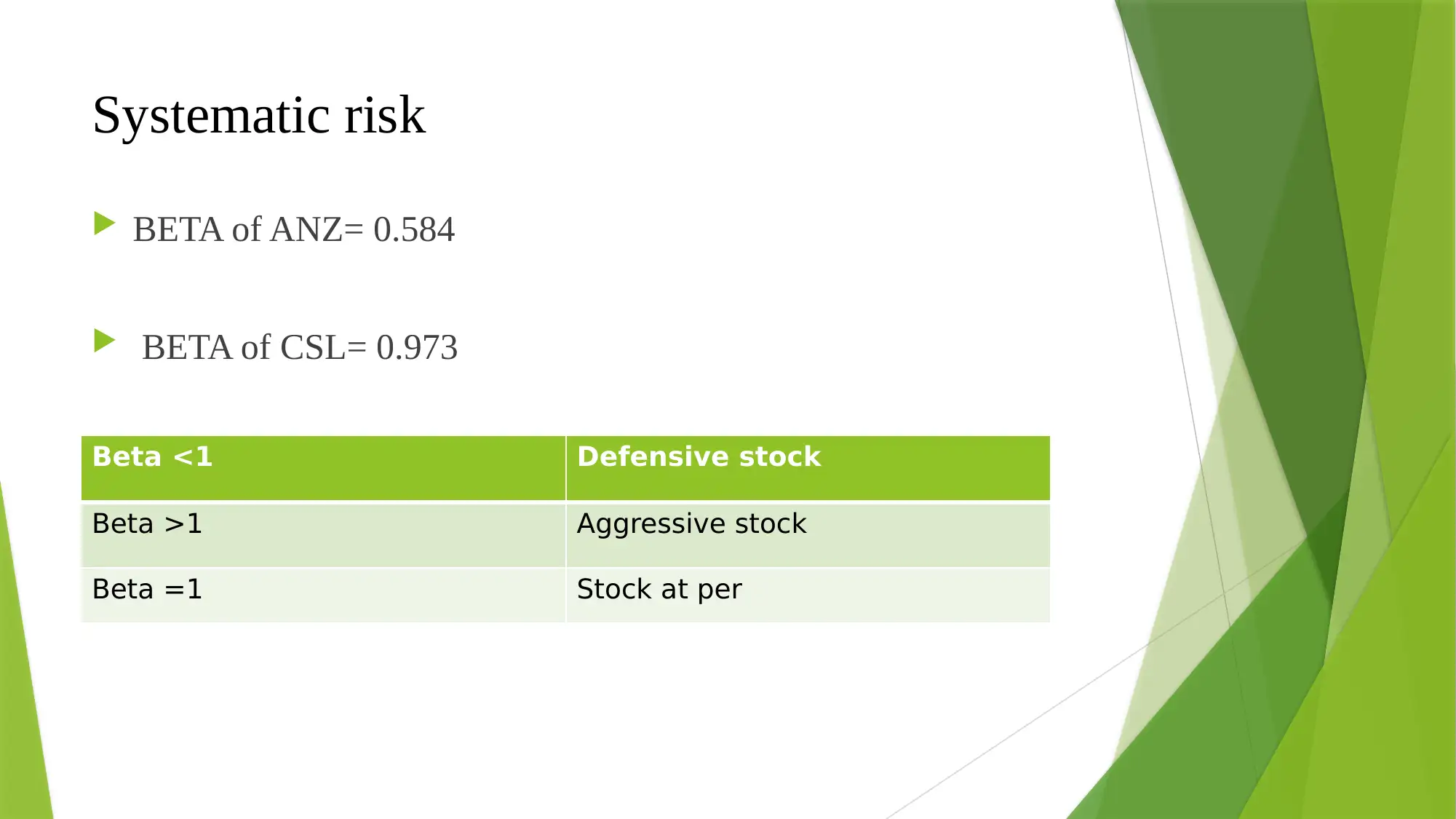

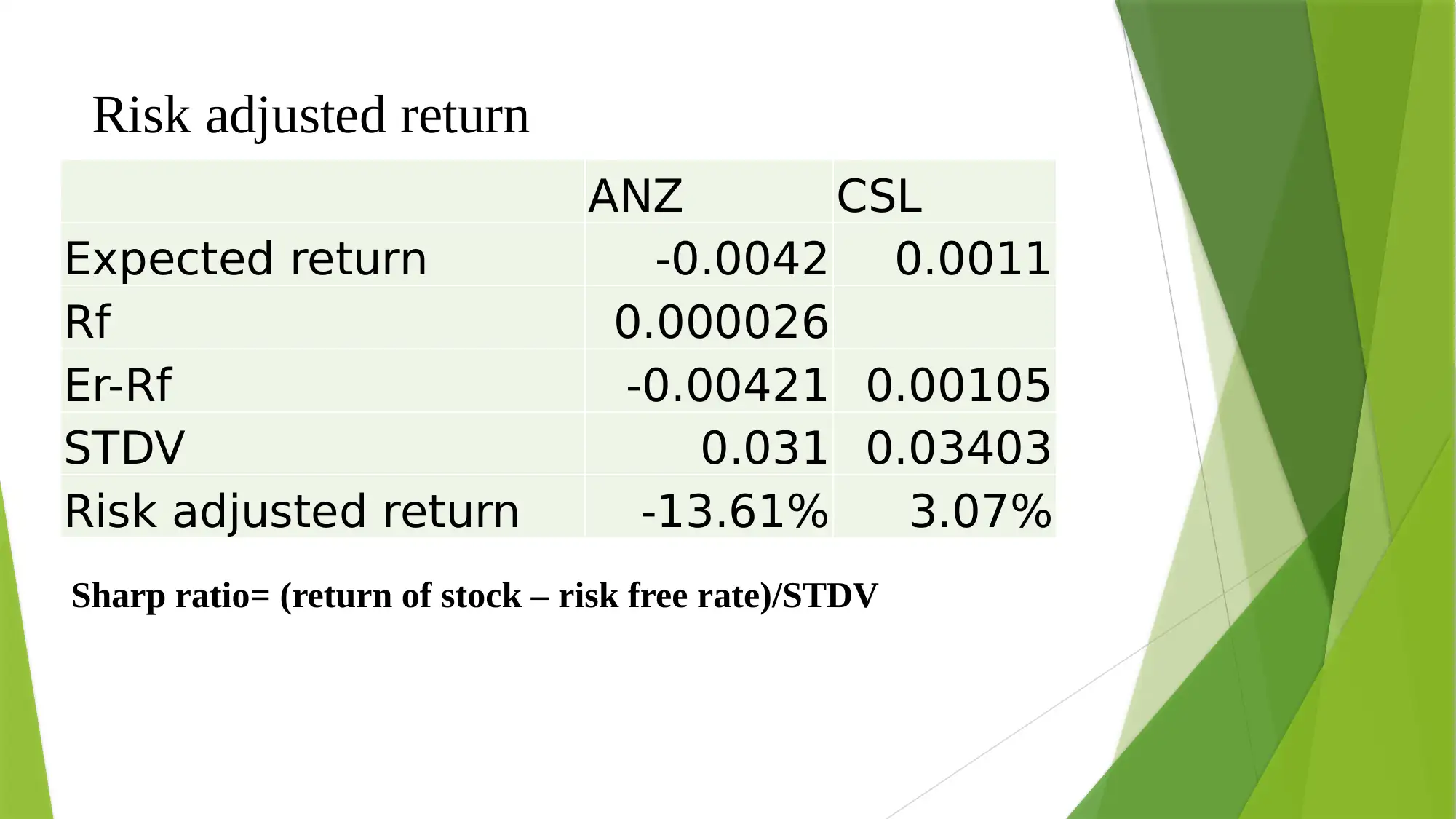

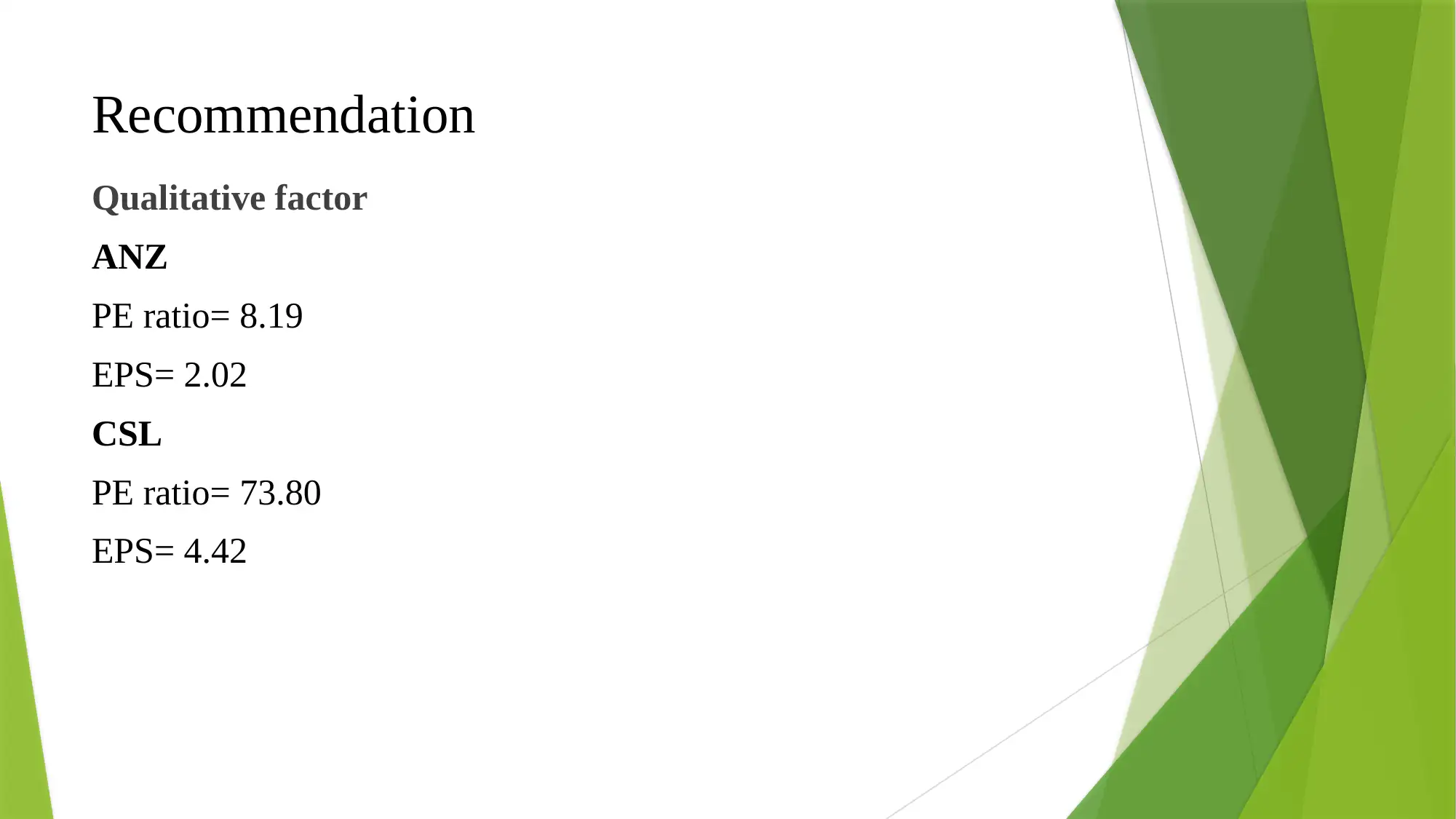

This presentation analyzes the financial impact of the COVID-19 pandemic on the Australian stock market, focusing on two specific stocks: Australia and New Zealand Banking Group (ANZ) and CSL Limited. The analysis includes an introduction to the pandemic's global economic effects, particularly the contraction of the global economy, and an overview of the selected stocks' performance. The presentation uses data collected from Yahoo Finance from November 2019 to March 2020 to calculate geometric mean returns, assess risk using Beta values and Sharpe ratios, and evaluate qualitative factors like PE ratios and EPS. It highlights the impact of the pandemic on stock prices, including market volatility and rating downgrades. The findings suggest that while all stocks experienced a downturn, CSL showed positive growth potential, making it a favorable long-term investment option. The presentation concludes with recommendations and a bibliography of referenced sources.

1 out of 12

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.