BFA728 Finance for Managers Assignment: Capital Budgeting and Equity

VerifiedAdded on 2022/10/17

|12

|2136

|63

Homework Assignment

AI Summary

This assignment analyzes capital budgeting techniques, including payback period, net present value (NPV), and internal rate of return (IRR), to evaluate the suitability of printer investments. The analysis compares two printers, identifying conflicting rankings based on different methods and exploring the theoretical and practical bases for decision-making. Furthermore, the assignment delves into private equity investments, discussing their global resurgence, various types (leveraged buyout, growth equity, and venture capital funds), and associated opportunities and risks such as operational, funding, and liquidity risks. The report concludes with a summary of the findings, emphasizing the role of private equity as a funding instrument and the importance of understanding both the advantages and potential risks for business managers.

Running head: FINANCE FOR MANAGER

Finance for manager

Name of the Student

Name of the University

Author’s note

Finance for manager

Name of the Student

Name of the University

Author’s note

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

1FINANCE FOR MANAGER

Executive Summary

The purpose of this paper is to discuss about the various capital budgeting techniques for

judging the suitability of a project. In this case three of the key capital techniques have been

used, that is, net present value, internal rate of return and payback period. Through these

techniques, the acceptability of the printer is judged and suitable explanations are provided in

each section. In the second part of the report, a thorough and detailed explanation is provided

regarding the different types of private equity investments which are available to the

businesses. In this context, the global resurgence of these investments are explained followed

by the risks and opportunities of these investments.

Executive Summary

The purpose of this paper is to discuss about the various capital budgeting techniques for

judging the suitability of a project. In this case three of the key capital techniques have been

used, that is, net present value, internal rate of return and payback period. Through these

techniques, the acceptability of the printer is judged and suitable explanations are provided in

each section. In the second part of the report, a thorough and detailed explanation is provided

regarding the different types of private equity investments which are available to the

businesses. In this context, the global resurgence of these investments are explained followed

by the risks and opportunities of these investments.

2FINANCE FOR MANAGER

Table of Contents

Part 1..........................................................................................................................................3

Payback period...........................................................................................................................3

Net present value........................................................................................................................3

Internal rate of return.................................................................................................................4

Brief note for management for indicating theoretical and practical basis about which printer

should be preferred.....................................................................................................................6

Part -2.........................................................................................................................................6

Introduction................................................................................................................................6

Discussion..................................................................................................................................7

Global resurgence of the private equity asset class....................................................................7

Different types of private equity investments............................................................................7

Opportunities and risks of investing in private equity...............................................................8

Conclusion................................................................................................................................10

References................................................................................................................................11

Table of Contents

Part 1..........................................................................................................................................3

Payback period...........................................................................................................................3

Net present value........................................................................................................................3

Internal rate of return.................................................................................................................4

Brief note for management for indicating theoretical and practical basis about which printer

should be preferred.....................................................................................................................6

Part -2.........................................................................................................................................6

Introduction................................................................................................................................6

Discussion..................................................................................................................................7

Global resurgence of the private equity asset class....................................................................7

Different types of private equity investments............................................................................7

Opportunities and risks of investing in private equity...............................................................8

Conclusion................................................................................................................................10

References................................................................................................................................11

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

3FINANCE FOR MANAGER

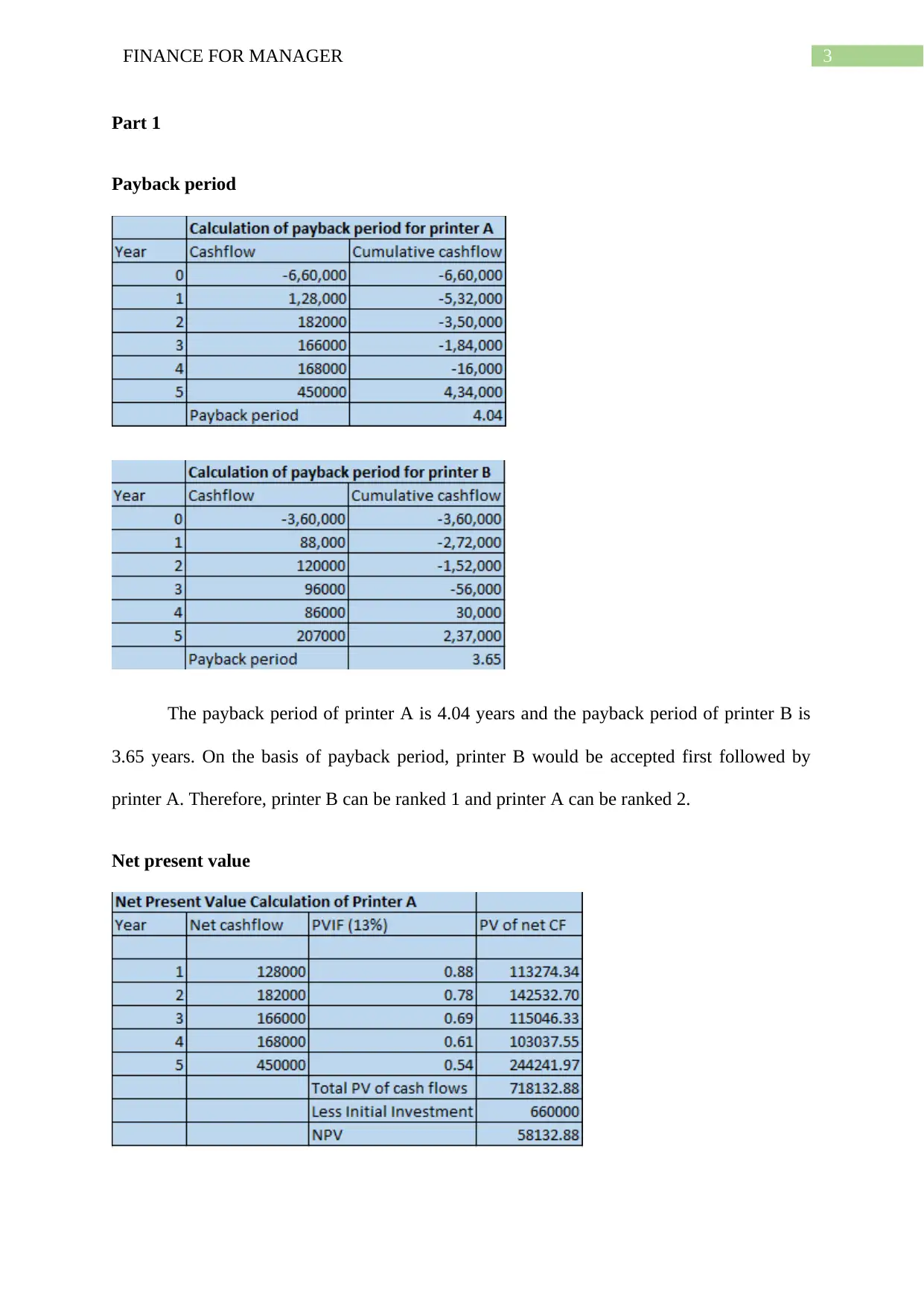

Part 1

Payback period

The payback period of printer A is 4.04 years and the payback period of printer B is

3.65 years. On the basis of payback period, printer B would be accepted first followed by

printer A. Therefore, printer B can be ranked 1 and printer A can be ranked 2.

Net present value

Part 1

Payback period

The payback period of printer A is 4.04 years and the payback period of printer B is

3.65 years. On the basis of payback period, printer B would be accepted first followed by

printer A. Therefore, printer B can be ranked 1 and printer A can be ranked 2.

Net present value

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

4FINANCE FOR MANAGER

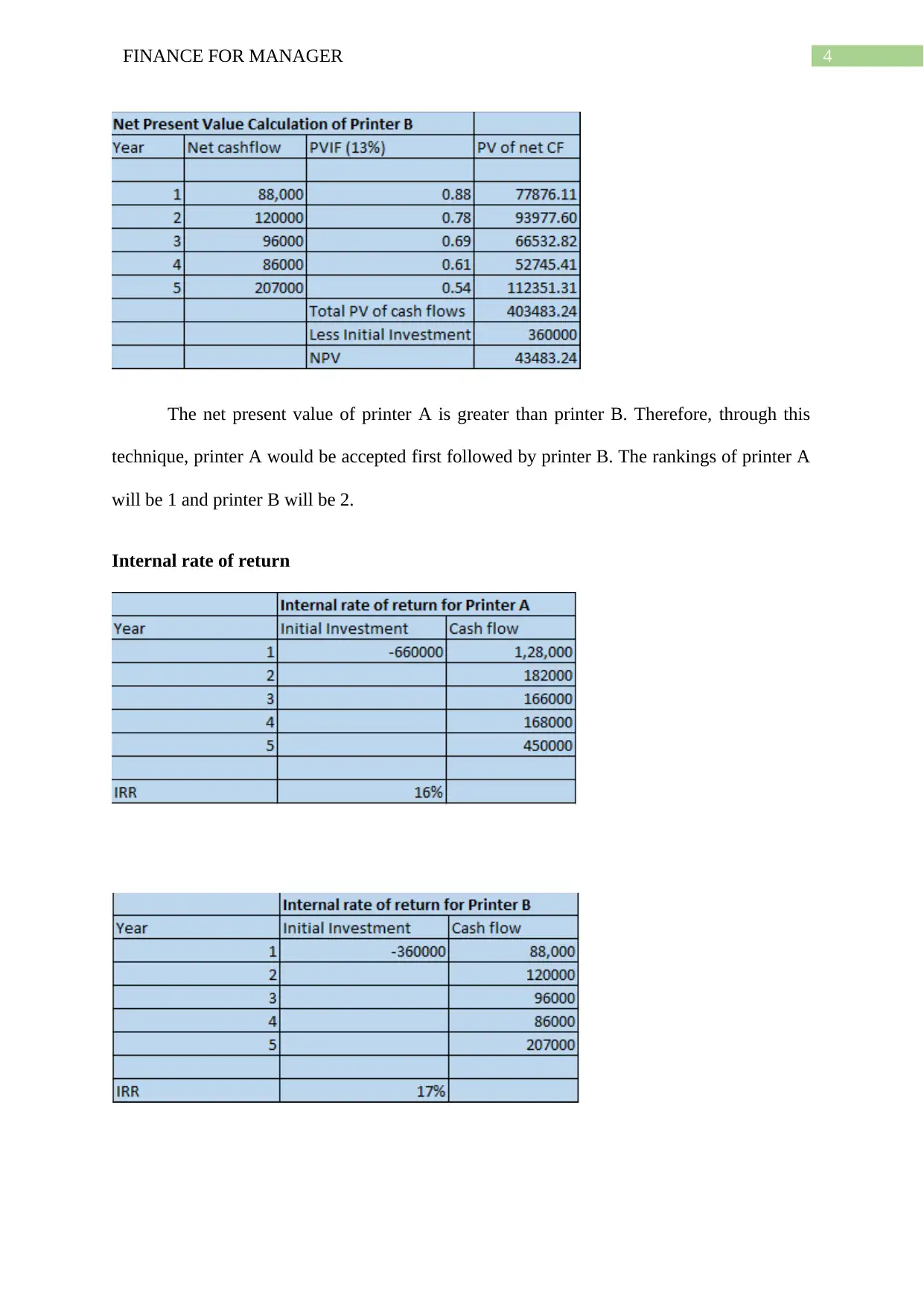

The net present value of printer A is greater than printer B. Therefore, through this

technique, printer A would be accepted first followed by printer B. The rankings of printer A

will be 1 and printer B will be 2.

Internal rate of return

The net present value of printer A is greater than printer B. Therefore, through this

technique, printer A would be accepted first followed by printer B. The rankings of printer A

will be 1 and printer B will be 2.

Internal rate of return

5FINANCE FOR MANAGER

The internal rate of return for printer B is greater than that of printer A. Therefore,

printer B would be accepted first followed by printer A. Consequently, printer B would be

ranked 1 and printer A would be ranked 2. Summarise the findings of these two techniques

and find out whether the two projects have conflicted rankings. The above analysis provided

that following results.

Using the payback period technique, printer B is more profitable than printer A. On

the basis of net present value technique, printer A is more profitable than printer B. On the

basis of internal rate of return method, printer B is again more profitable than printer A. From

this it can be stated that the printers have conflicted rankings on the basis of these three

different methods.

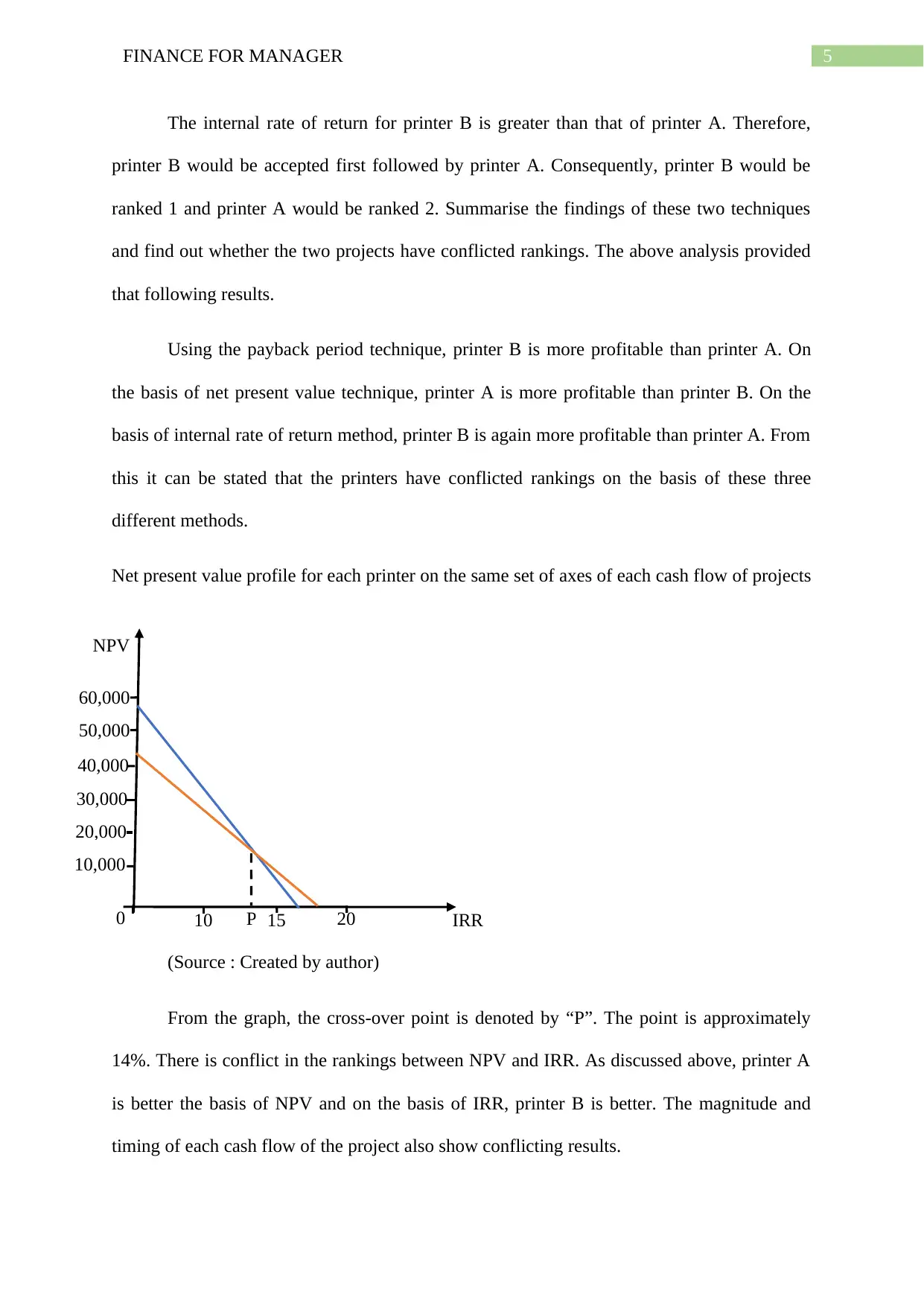

Net present value profile for each printer on the same set of axes of each cash flow of projects

(Source : Created by author)

From the graph, the cross-over point is denoted by “P”. The point is approximately

14%. There is conflict in the rankings between NPV and IRR. As discussed above, printer A

is better the basis of NPV and on the basis of IRR, printer B is better. The magnitude and

timing of each cash flow of the project also show conflicting results.

NPV

IRR0 P 202020

20

1510

10,000

0

20,000

30,000

40,000

50,000

60,000

The internal rate of return for printer B is greater than that of printer A. Therefore,

printer B would be accepted first followed by printer A. Consequently, printer B would be

ranked 1 and printer A would be ranked 2. Summarise the findings of these two techniques

and find out whether the two projects have conflicted rankings. The above analysis provided

that following results.

Using the payback period technique, printer B is more profitable than printer A. On

the basis of net present value technique, printer A is more profitable than printer B. On the

basis of internal rate of return method, printer B is again more profitable than printer A. From

this it can be stated that the printers have conflicted rankings on the basis of these three

different methods.

Net present value profile for each printer on the same set of axes of each cash flow of projects

(Source : Created by author)

From the graph, the cross-over point is denoted by “P”. The point is approximately

14%. There is conflict in the rankings between NPV and IRR. As discussed above, printer A

is better the basis of NPV and on the basis of IRR, printer B is better. The magnitude and

timing of each cash flow of the project also show conflicting results.

NPV

IRR0 P 202020

20

1510

10,000

0

20,000

30,000

40,000

50,000

60,000

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

6FINANCE FOR MANAGER

Brief note for management for indicating theoretical and practical basis about which

printer should be preferred.

Theoretically, the printer having maximum net present value should be chosen as the

cash inflow is exceeding the initial investment. Theoretically, net present value method is

considered to be superior than payback period method and internal rate of return method.

Practically, the printer having less payback period should be chosen as it is always

recommended for the managers to recover their entire investment within the shortest possible

time. Therefore, from this analysis, printer A should be chosen.

There is a difference in the recommendation provided because the theoretical and

practical aspects and conditions are always different. Theoretical perspective is based on

many assumptions which are not applicable in practical situations. Due to all these factors,

the recommendation is different in the two situations.

Part -2

Introduction

The ultimate purpose of this report is to bring about a short description regarding the

background of the private equity asset class. It has been seen that private equity can be

considered to be a good source of funding as through this method the investors provide

capital to businesses even if they are not listed in stock exchanges. In this regard, the global

resurgence of the private equity asset class is defined followed by the different types of

investments available for the businesses. Finally, the opportunities and risks that arise due to

private equity investments are also analysed and explained.

Brief note for management for indicating theoretical and practical basis about which

printer should be preferred.

Theoretically, the printer having maximum net present value should be chosen as the

cash inflow is exceeding the initial investment. Theoretically, net present value method is

considered to be superior than payback period method and internal rate of return method.

Practically, the printer having less payback period should be chosen as it is always

recommended for the managers to recover their entire investment within the shortest possible

time. Therefore, from this analysis, printer A should be chosen.

There is a difference in the recommendation provided because the theoretical and

practical aspects and conditions are always different. Theoretical perspective is based on

many assumptions which are not applicable in practical situations. Due to all these factors,

the recommendation is different in the two situations.

Part -2

Introduction

The ultimate purpose of this report is to bring about a short description regarding the

background of the private equity asset class. It has been seen that private equity can be

considered to be a good source of funding as through this method the investors provide

capital to businesses even if they are not listed in stock exchanges. In this regard, the global

resurgence of the private equity asset class is defined followed by the different types of

investments available for the businesses. Finally, the opportunities and risks that arise due to

private equity investments are also analysed and explained.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

7FINANCE FOR MANAGER

Discussion

Global resurgence of the private equity asset class

The private equity industry has dealt with heavy pressures in past days. Despite of the

hard situations, the private equity industry saw an impressive surge in the value of its

investment in the year 2018 (Gilligan and Wright 2014).The total buyout value of these

investments jumped up to 10% growing up to approximately $582 billion. The industry has

capped the strongest five-year run and has made history.

The funds raised from private equity attracted an impressive amount of capital in the

year 2018. Due to this situation, the gross profit of the businesses got raised up to $714

billion from investors during the same year. This is considered to be the third largest amount

in the history of private equity industries. The total record rose up to $3.7 trillion.

The regions that contributed to such an enormous amount of fund raising were

primarily the emerging market and the Asia-pacific regions. The investor who were

continuing with their diversification strategies, saw a massive growth in these sectors

(Merme, Ahlers and Gupta 2014). In the global phenomenon, China has strengthened its

regulations regarding private equity investments. Therefore, there has been a massive decline

in private equity funds in China (Merme, Ahlers and Gupta 2014). This has been mainly done

for reducing debt and financial risk of the country. Therefore, China saw only 14% fund

raising through this process. However, in the other parts of the world, the private equity

investment saw a global upsurge in its functioning.

Different types of private equity investments

There can be many kinds of private equity investments available for funding the

businesses. Out of them, three kinds of investments are common and popular.

1) Leveraged buyout funds

Discussion

Global resurgence of the private equity asset class

The private equity industry has dealt with heavy pressures in past days. Despite of the

hard situations, the private equity industry saw an impressive surge in the value of its

investment in the year 2018 (Gilligan and Wright 2014).The total buyout value of these

investments jumped up to 10% growing up to approximately $582 billion. The industry has

capped the strongest five-year run and has made history.

The funds raised from private equity attracted an impressive amount of capital in the

year 2018. Due to this situation, the gross profit of the businesses got raised up to $714

billion from investors during the same year. This is considered to be the third largest amount

in the history of private equity industries. The total record rose up to $3.7 trillion.

The regions that contributed to such an enormous amount of fund raising were

primarily the emerging market and the Asia-pacific regions. The investor who were

continuing with their diversification strategies, saw a massive growth in these sectors

(Merme, Ahlers and Gupta 2014). In the global phenomenon, China has strengthened its

regulations regarding private equity investments. Therefore, there has been a massive decline

in private equity funds in China (Merme, Ahlers and Gupta 2014). This has been mainly done

for reducing debt and financial risk of the country. Therefore, China saw only 14% fund

raising through this process. However, in the other parts of the world, the private equity

investment saw a global upsurge in its functioning.

Different types of private equity investments

There can be many kinds of private equity investments available for funding the

businesses. Out of them, three kinds of investments are common and popular.

1) Leveraged buyout funds

8FINANCE FOR MANAGER

These funds are required for controlling the stakes or risks of the firms. The companies

engaging in these investments mainly have stable cash flows. The transactions occurring

in these types of funds mainly use a combination of debt and equity capital (Jenkinson

and Sousa 2015). The private equity companies buy the businesses with the mixture of

their own funds as well as the borrowed funds. In return the Private equity firm provides a

collateral to the firm from which it is borrowing its money (Jenkinson and Sousa 2015).

The collaterals mainly consist of hard assets or working capital pledges of the private

equity firm.

2) Growth equity funds

Growth equity funds can be defined as those funds which are invested in the growing

businesses. These businesses are generally keened to scale their operations and enter new

markets accordingly (Mietzner and Schweizer 2014). These funds are more widely used

as compared to venture capital funds. The targeted industry has comparatively higher

growth than that of venture capital industries.

3) Venture capital funds

The venture capital funds are mostly used for used for investing in minority stakes mostly

for the start-up companies (Harris et al. 2014). The funds are classified into early stage

and later stage funds. Early stage funds are generally used for investing in the companies

which are amateurs of technology and have the desire to invent and commercialise new

technologies (Harris et al. 2014). Later stage funds are mostly used for the companies

which have already shown their skills in these segments and are looking to scale

operations. These strategies help the businesses to maximise their growth potential.

Opportunities and risks of investing in private equity

The different advantages and opportunities of private equity can be listed as follows

These funds are required for controlling the stakes or risks of the firms. The companies

engaging in these investments mainly have stable cash flows. The transactions occurring

in these types of funds mainly use a combination of debt and equity capital (Jenkinson

and Sousa 2015). The private equity companies buy the businesses with the mixture of

their own funds as well as the borrowed funds. In return the Private equity firm provides a

collateral to the firm from which it is borrowing its money (Jenkinson and Sousa 2015).

The collaterals mainly consist of hard assets or working capital pledges of the private

equity firm.

2) Growth equity funds

Growth equity funds can be defined as those funds which are invested in the growing

businesses. These businesses are generally keened to scale their operations and enter new

markets accordingly (Mietzner and Schweizer 2014). These funds are more widely used

as compared to venture capital funds. The targeted industry has comparatively higher

growth than that of venture capital industries.

3) Venture capital funds

The venture capital funds are mostly used for used for investing in minority stakes mostly

for the start-up companies (Harris et al. 2014). The funds are classified into early stage

and later stage funds. Early stage funds are generally used for investing in the companies

which are amateurs of technology and have the desire to invent and commercialise new

technologies (Harris et al. 2014). Later stage funds are mostly used for the companies

which have already shown their skills in these segments and are looking to scale

operations. These strategies help the businesses to maximise their growth potential.

Opportunities and risks of investing in private equity

The different advantages and opportunities of private equity can be listed as follows

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

9FINANCE FOR MANAGER

1) Infusion of cash in the business due to increase of financial resources through

these investments which automatically fuels growth.

2) Private equity also comes with providing suitable talents to the business which

were not present before (Appelbaum and Batt 2014).

3) The management gets good incentives through private equity investments

4) The returns of investing in private equity have proven to quite high (Appelbaum

and Batt 2014).

5) The private equity investments are committed to provide the businesses with

short-term as well as long-term successes.

The different kinds of risks which are associated with private equity investments can be

classified as follows.

1) Operational risk – This is the risk of loss due to inadequate and improper

processes and systems that are prevalent in the organisations. This is a key

consideration for the investors which is irrespective of the asset classes (Sorensen

and Jagannathan 2015).

2) Funding risk – This is the default risk of the investors while they cannot provide

capital commitments to the businesses (Caselli and Negri 2018). This risk is

closely related to the liquidity risk and is seen mostly in situations when there is a

shortfall of fund.

3) Liquidity risk – This risk occurs due to the inability of the investors to redeem

their investments at any given point of time (Sorensen and Jagannathan 2015).

4) Market risk – Private equity investments are subjected to valuations which are not

done very frequently. The investments are generally valued on a quarterly basis

and consist of subjectivity in their assessments.

1) Infusion of cash in the business due to increase of financial resources through

these investments which automatically fuels growth.

2) Private equity also comes with providing suitable talents to the business which

were not present before (Appelbaum and Batt 2014).

3) The management gets good incentives through private equity investments

4) The returns of investing in private equity have proven to quite high (Appelbaum

and Batt 2014).

5) The private equity investments are committed to provide the businesses with

short-term as well as long-term successes.

The different kinds of risks which are associated with private equity investments can be

classified as follows.

1) Operational risk – This is the risk of loss due to inadequate and improper

processes and systems that are prevalent in the organisations. This is a key

consideration for the investors which is irrespective of the asset classes (Sorensen

and Jagannathan 2015).

2) Funding risk – This is the default risk of the investors while they cannot provide

capital commitments to the businesses (Caselli and Negri 2018). This risk is

closely related to the liquidity risk and is seen mostly in situations when there is a

shortfall of fund.

3) Liquidity risk – This risk occurs due to the inability of the investors to redeem

their investments at any given point of time (Sorensen and Jagannathan 2015).

4) Market risk – Private equity investments are subjected to valuations which are not

done very frequently. The investments are generally valued on a quarterly basis

and consist of subjectivity in their assessments.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

10FINANCE FOR MANAGER

Conclusion

From the above report, it can be concluded that the private equity investments can be

good sources through which businesses can get the seed capital required for their growth and

development. Even for the start-up businesses, private equity can serve as a major funding

instrument. In this respect, the increasing upsurge of private equity investments is highlighted

followed by their different available types. The last section discusses about the opportunities,

advantages and the probable risks of the private equity investments. Through the analysis of

the above statements, a business manager can find out the suitability of private equity

investments for the upheaval of their businesses.

Conclusion

From the above report, it can be concluded that the private equity investments can be

good sources through which businesses can get the seed capital required for their growth and

development. Even for the start-up businesses, private equity can serve as a major funding

instrument. In this respect, the increasing upsurge of private equity investments is highlighted

followed by their different available types. The last section discusses about the opportunities,

advantages and the probable risks of the private equity investments. Through the analysis of

the above statements, a business manager can find out the suitability of private equity

investments for the upheaval of their businesses.

11FINANCE FOR MANAGER

References

Appelbaum, E. and Batt, R., 2014. Private equity at work: When wall street manages main

street. Russell Sage Foundation.

Caselli, S. and Negri, G., 2018. Private equity and venture capital in Europe: markets,

techniques, and deals. Academic Press.

Gilligan, J. and Wright, M., 2014. Private equity demystified: An explanatory guide.

Harris, R.S., Jenkinson, T., Kaplan, S.N. and Stucke, R., 2014. Has persistence persisted in

private equity? Evidence from buyout and venture capital funds.

Jenkinson, T. and Sousa, M., 2015. What determines the exit decision for leveraged

buyouts?. Journal of Banking & Finance, 59, pp.399-408.

Merme, V., Ahlers, R. and Gupta, J., 2014. Private equity, public affair: Hydropower

financing in the Mekong Basin. Global Environmental Change, 24, pp.20-29.

Mietzner, M. and Schweizer, D., 2014. Hedge funds versus private equity funds as

shareholder activists in Germany—differences in value creation. Journal of Economics and

Finance, 38(2), pp.181-208.

Sorensen, M. and Jagannathan, R., 2015. The public market equivalent and private equity

performance. Financial Analysts Journal, 71(4), pp.43-50.

References

Appelbaum, E. and Batt, R., 2014. Private equity at work: When wall street manages main

street. Russell Sage Foundation.

Caselli, S. and Negri, G., 2018. Private equity and venture capital in Europe: markets,

techniques, and deals. Academic Press.

Gilligan, J. and Wright, M., 2014. Private equity demystified: An explanatory guide.

Harris, R.S., Jenkinson, T., Kaplan, S.N. and Stucke, R., 2014. Has persistence persisted in

private equity? Evidence from buyout and venture capital funds.

Jenkinson, T. and Sousa, M., 2015. What determines the exit decision for leveraged

buyouts?. Journal of Banking & Finance, 59, pp.399-408.

Merme, V., Ahlers, R. and Gupta, J., 2014. Private equity, public affair: Hydropower

financing in the Mekong Basin. Global Environmental Change, 24, pp.20-29.

Mietzner, M. and Schweizer, D., 2014. Hedge funds versus private equity funds as

shareholder activists in Germany—differences in value creation. Journal of Economics and

Finance, 38(2), pp.181-208.

Sorensen, M. and Jagannathan, R., 2015. The public market equivalent and private equity

performance. Financial Analysts Journal, 71(4), pp.43-50.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 12

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.