Finance Problem Set

VerifiedAdded on 2019/09/20

|6

|677

|330

Homework Assignment

AI Summary

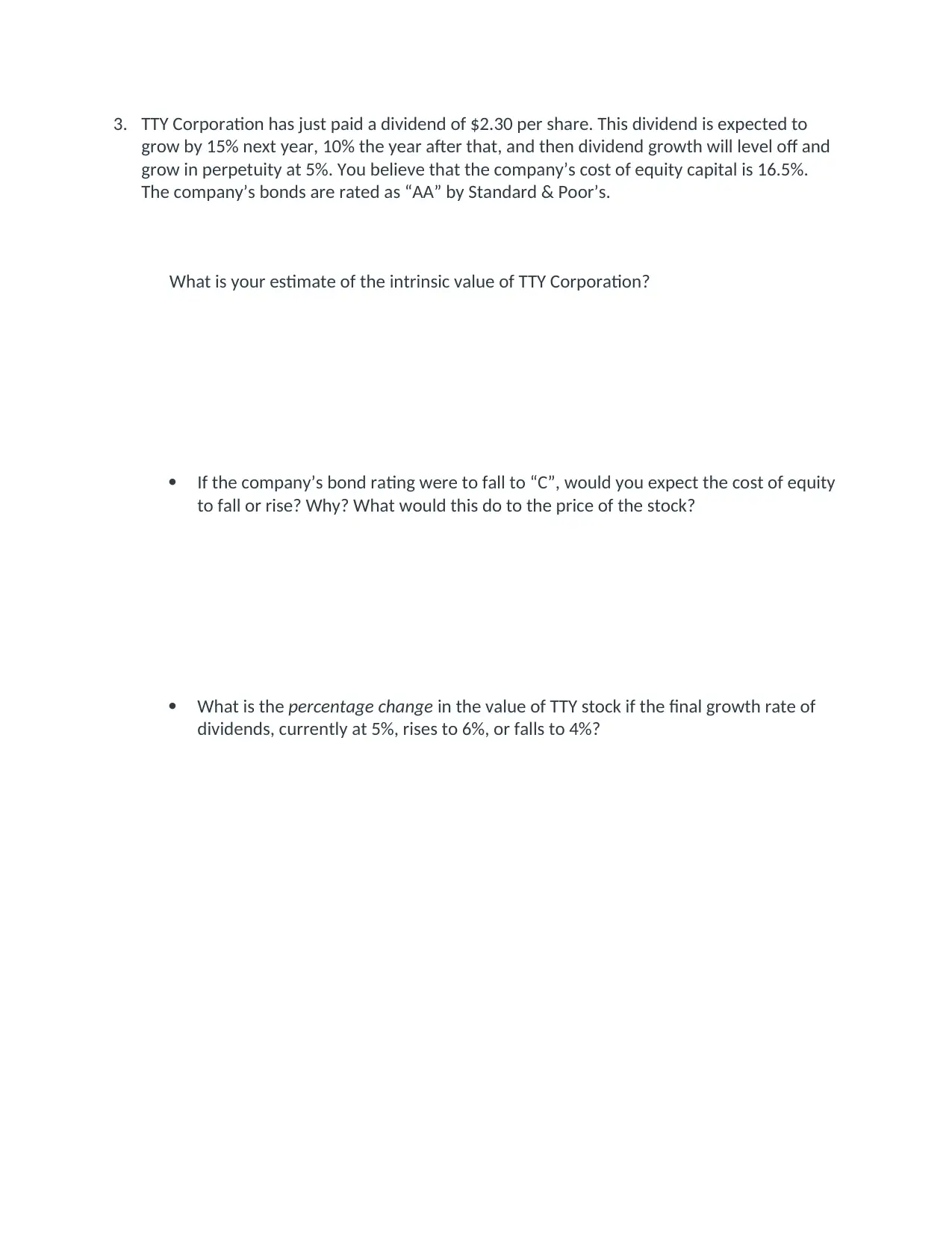

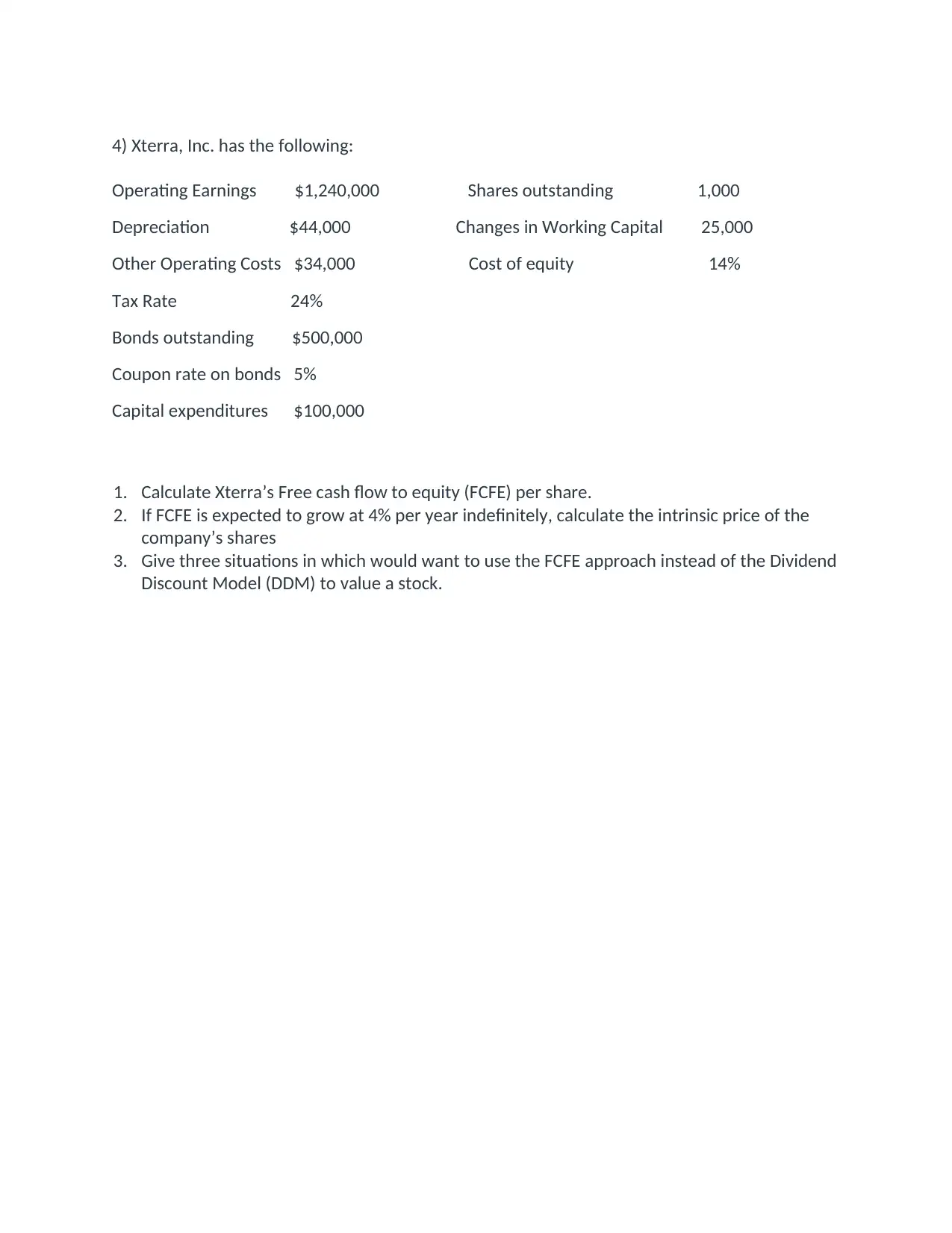

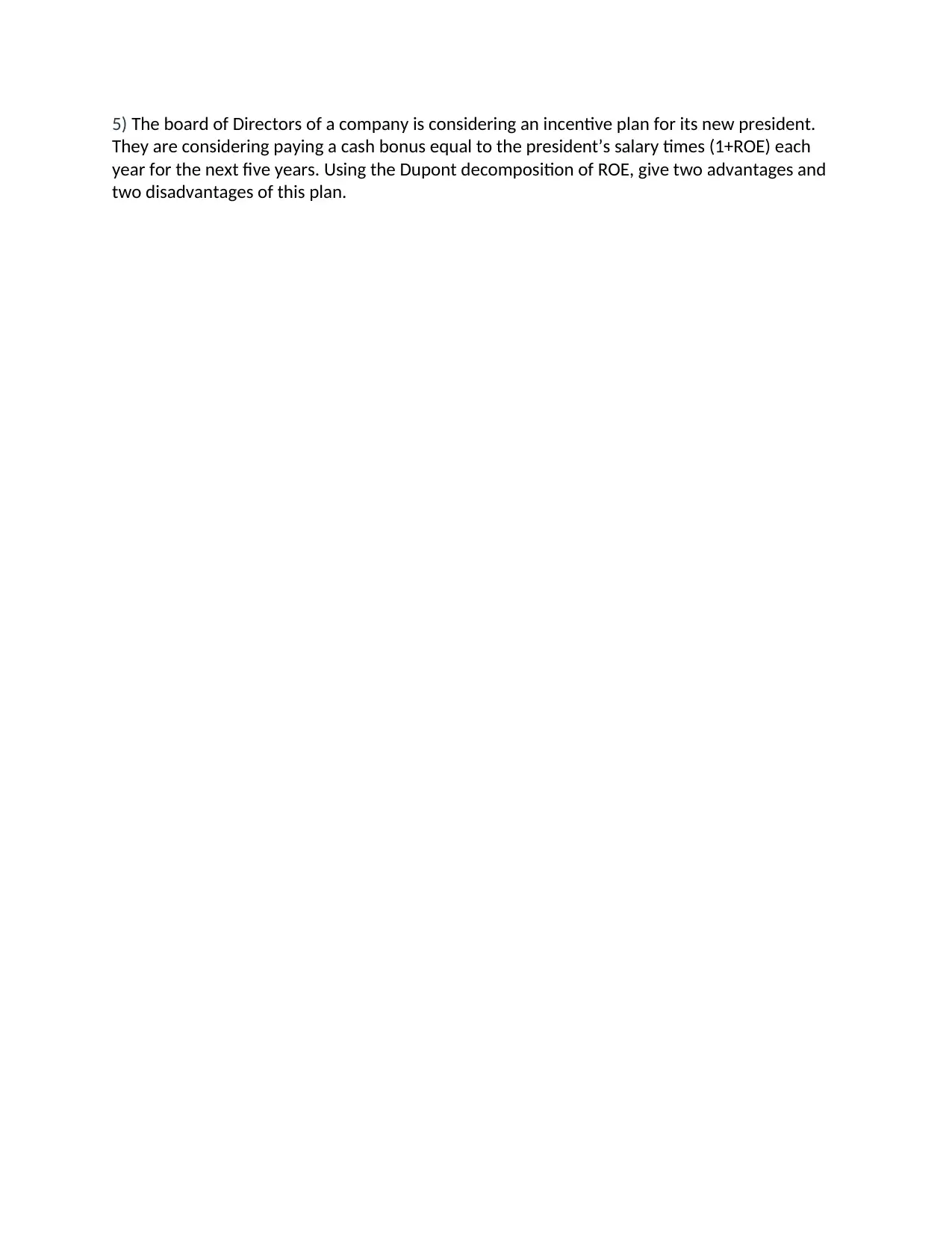

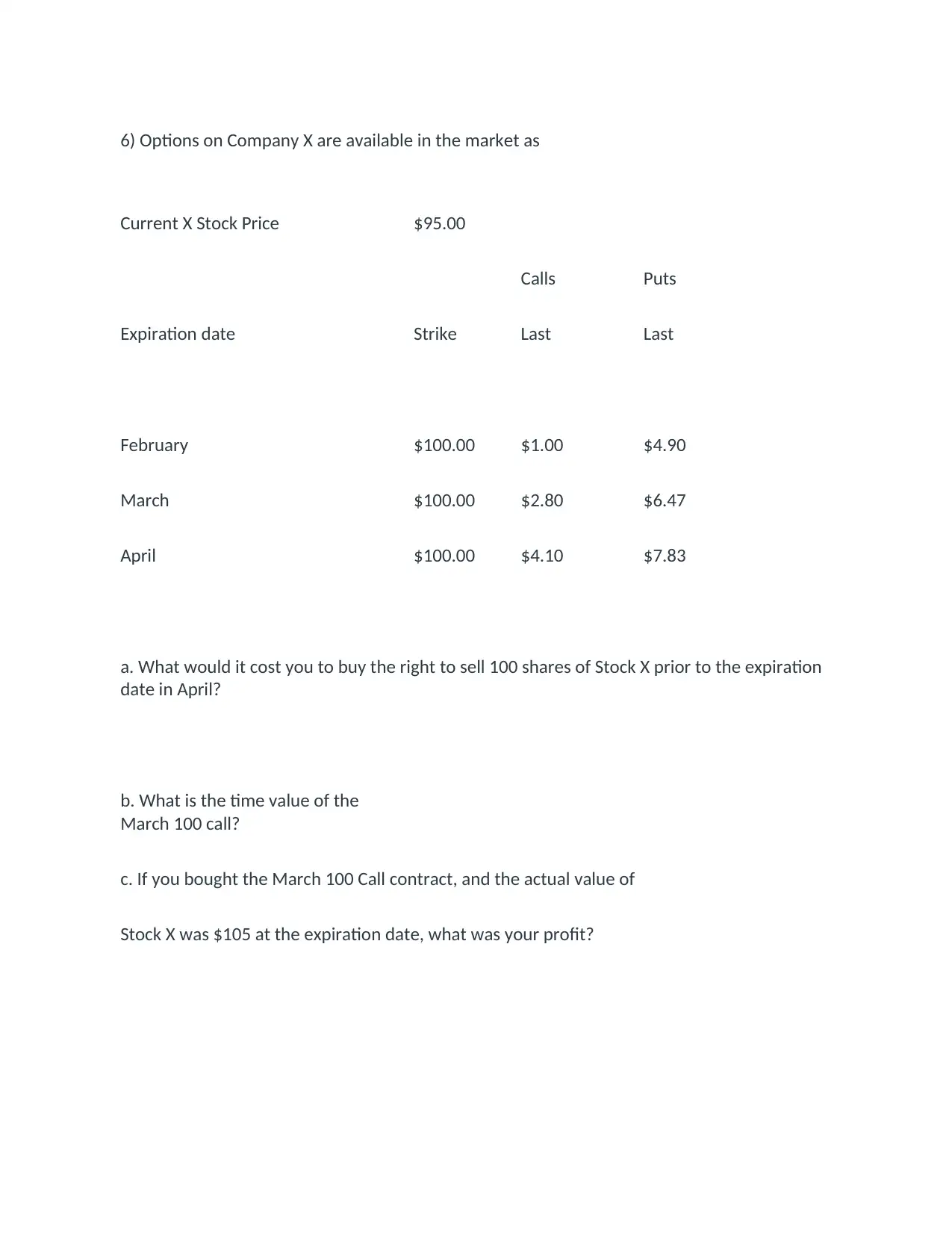

This assignment presents a series of problems related to financial valuation and risk management. The first problem involves calculating the intrinsic value of a corporation's stock using a dividend discount model, considering varying dividend growth rates and the impact of credit rating changes on the cost of equity. The second problem focuses on calculating free cash flow to equity (FCFE) per share and using it to determine the intrinsic price of a company's shares, comparing it to the dividend discount model. The third problem explores the advantages and disadvantages of an incentive plan based on return on equity (ROE). The fourth problem involves analyzing options pricing using market data, calculating the cost of options, time value, and profit/loss scenarios. The fifth problem delves into the Black-Scholes model for option valuation and put-call parity. Finally, the assignment concludes with a hedging problem using S&P 500 index futures, requiring the calculation of cash flow and an explanation of basis risk.

1 out of 6

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.