Finance Exam Solution - Investment Decisions and Cost Analysis

VerifiedAdded on 2023/01/07

|7

|1001

|76

Homework Assignment

AI Summary

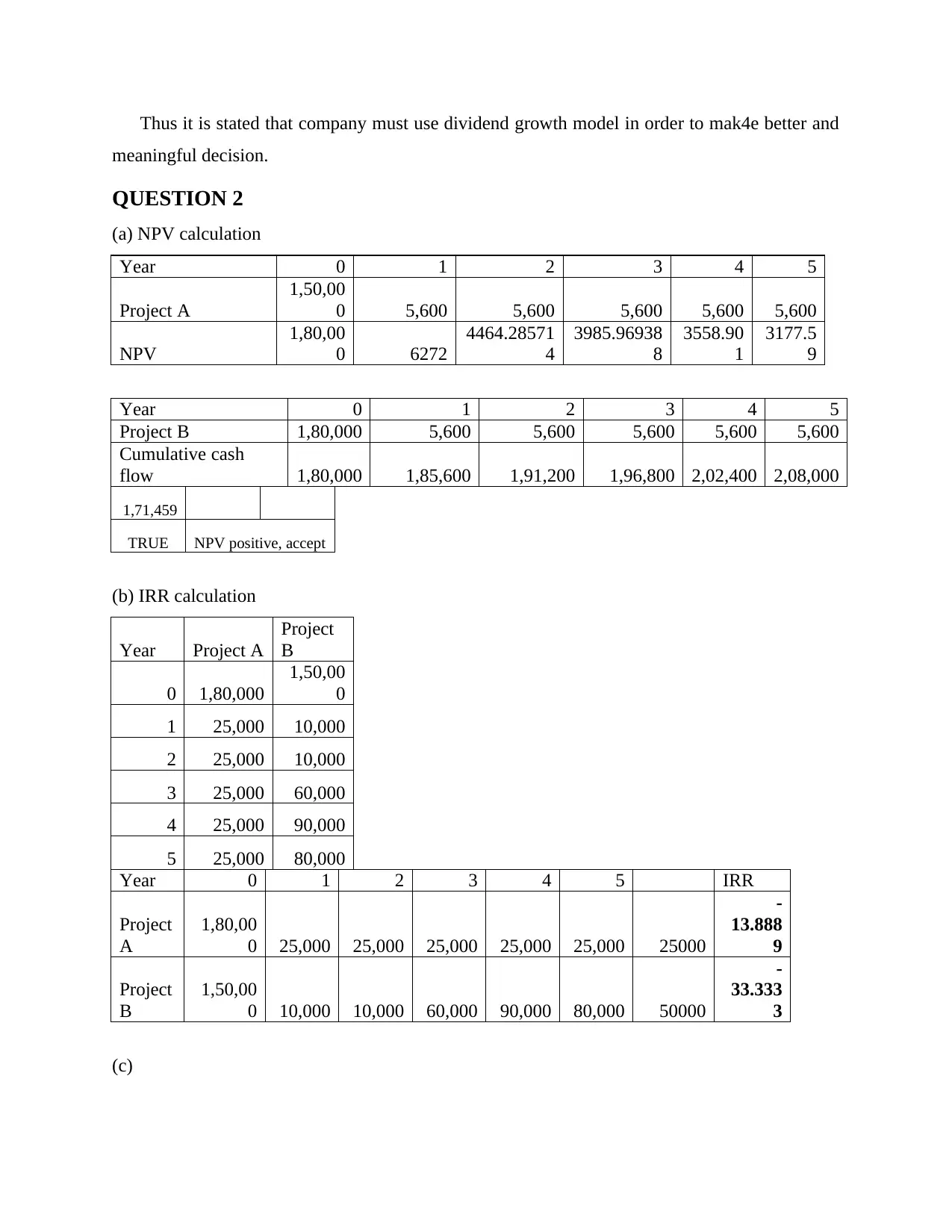

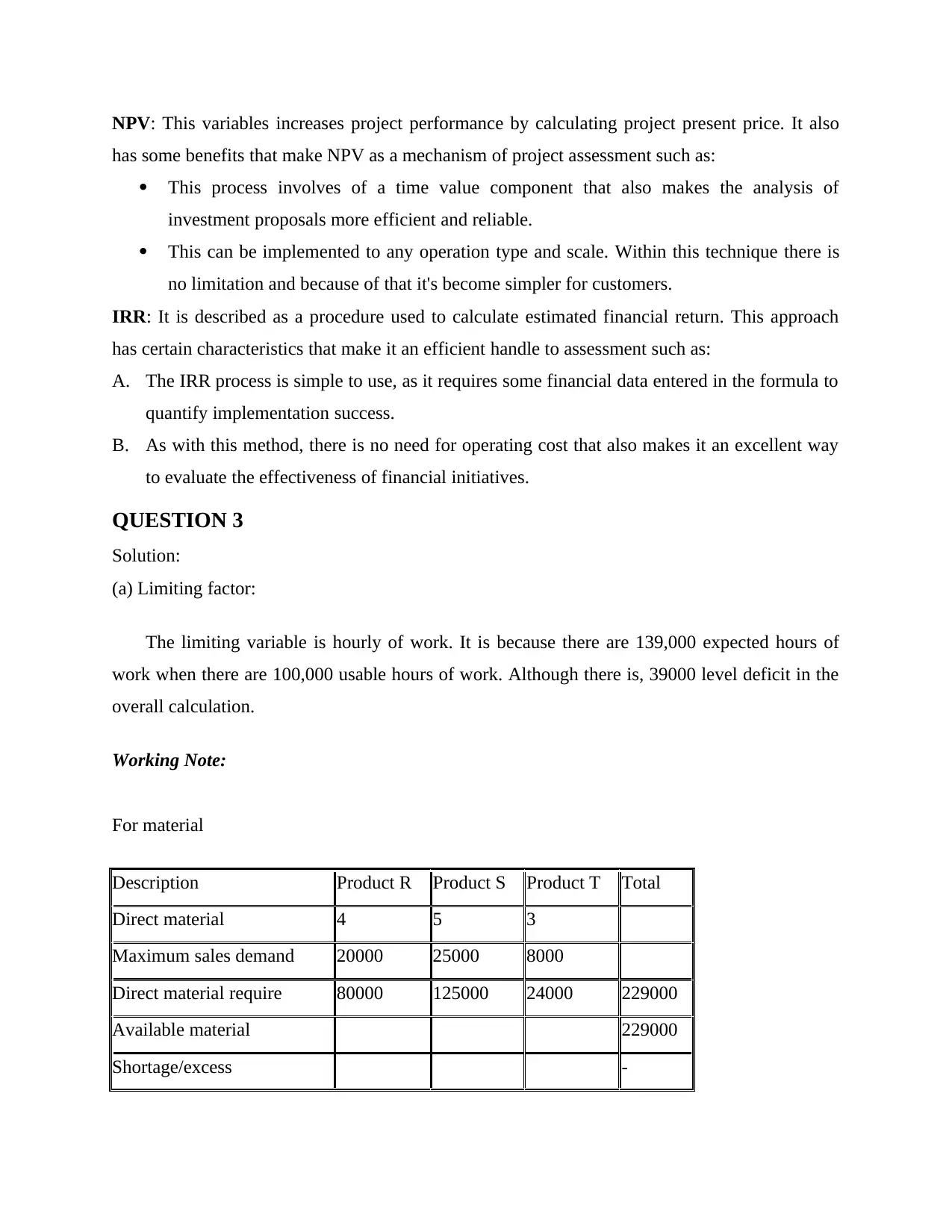

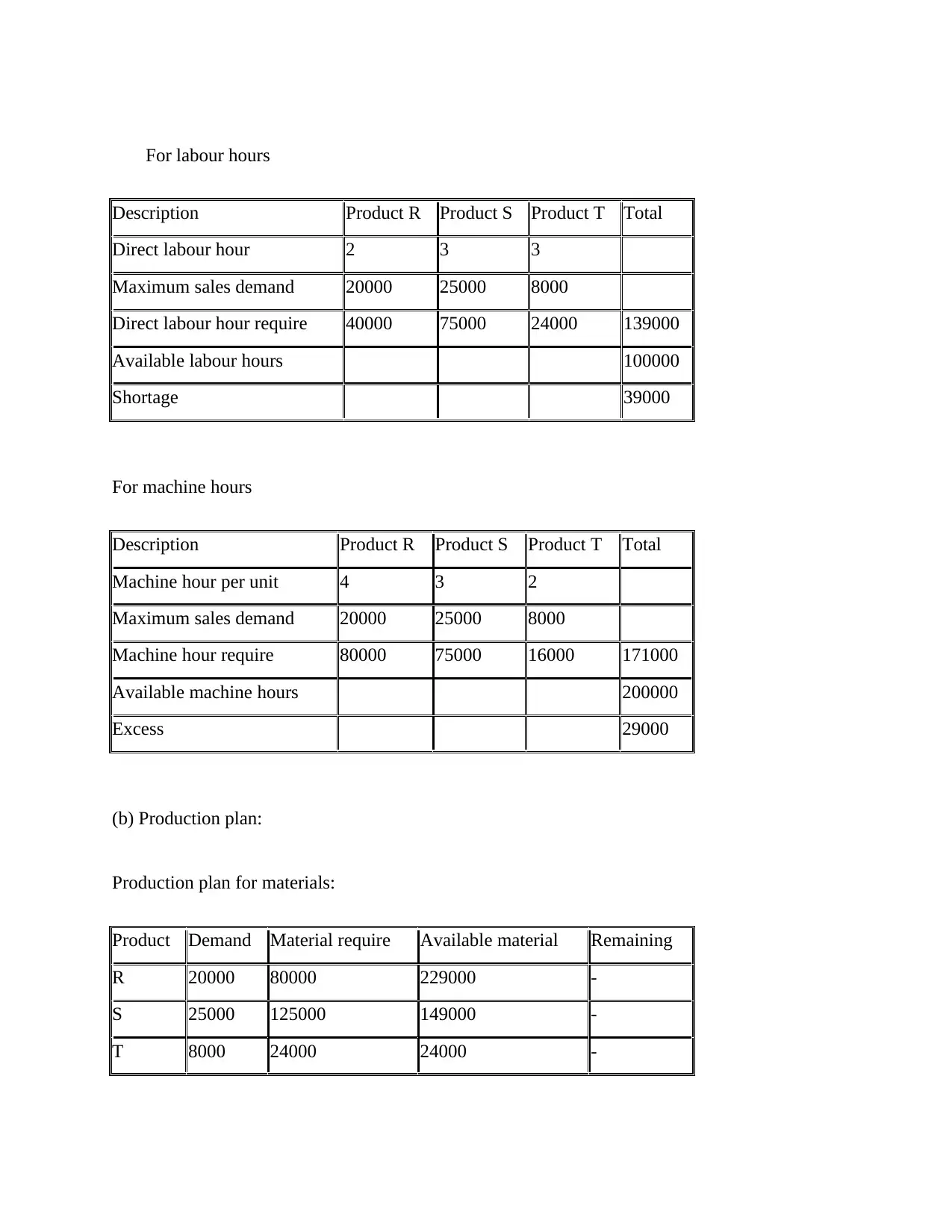

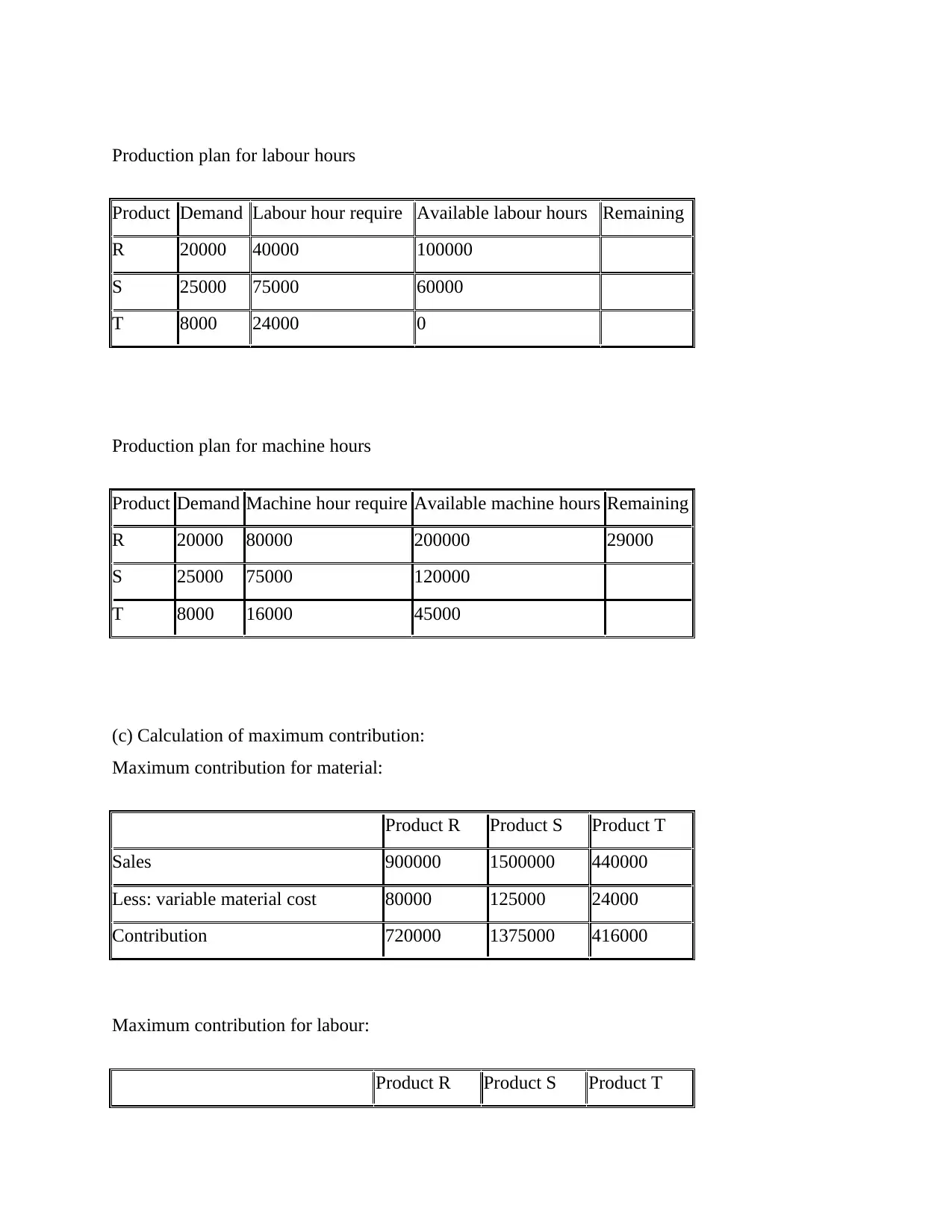

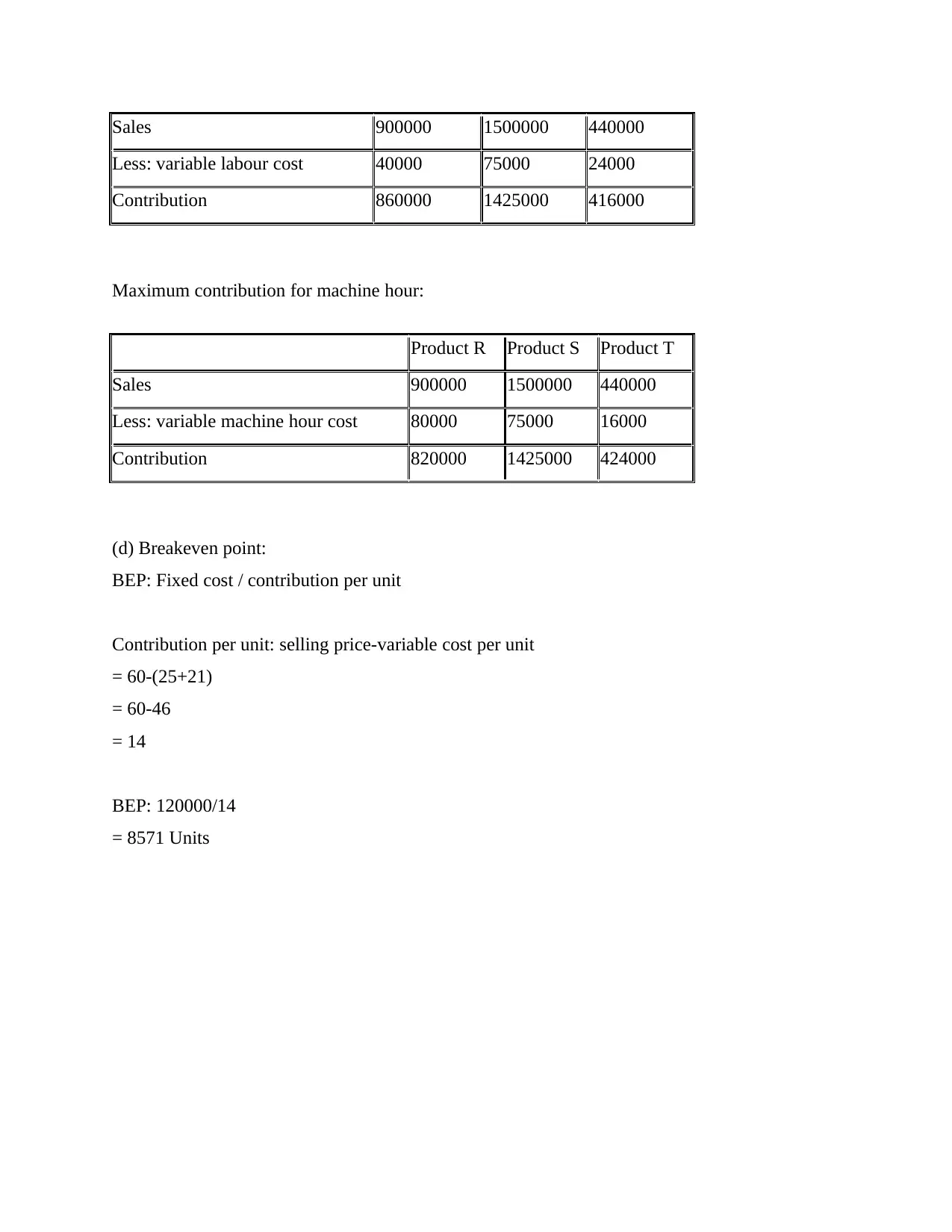

This document provides a detailed solution to a finance exam, addressing key concepts in investment analysis and production planning. The solution begins with calculations for the P/E ratio and intrinsic value using the dividend growth model, followed by a discussion of their limitations. The second part of the solution involves calculating the Net Present Value (NPV) and Internal Rate of Return (IRR) for two projects, along with an explanation of their benefits. The third section focuses on production planning, identifying the limiting factor, creating production plans for materials, labor, and machine hours, calculating maximum contribution, and determining the breakeven point. The solution includes working notes and comprehensive calculations to support the answers.

1 out of 7

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.