University Finance Report: Project Investment and Analysis

VerifiedAdded on 2020/03/16

|15

|2602

|33

Report

AI Summary

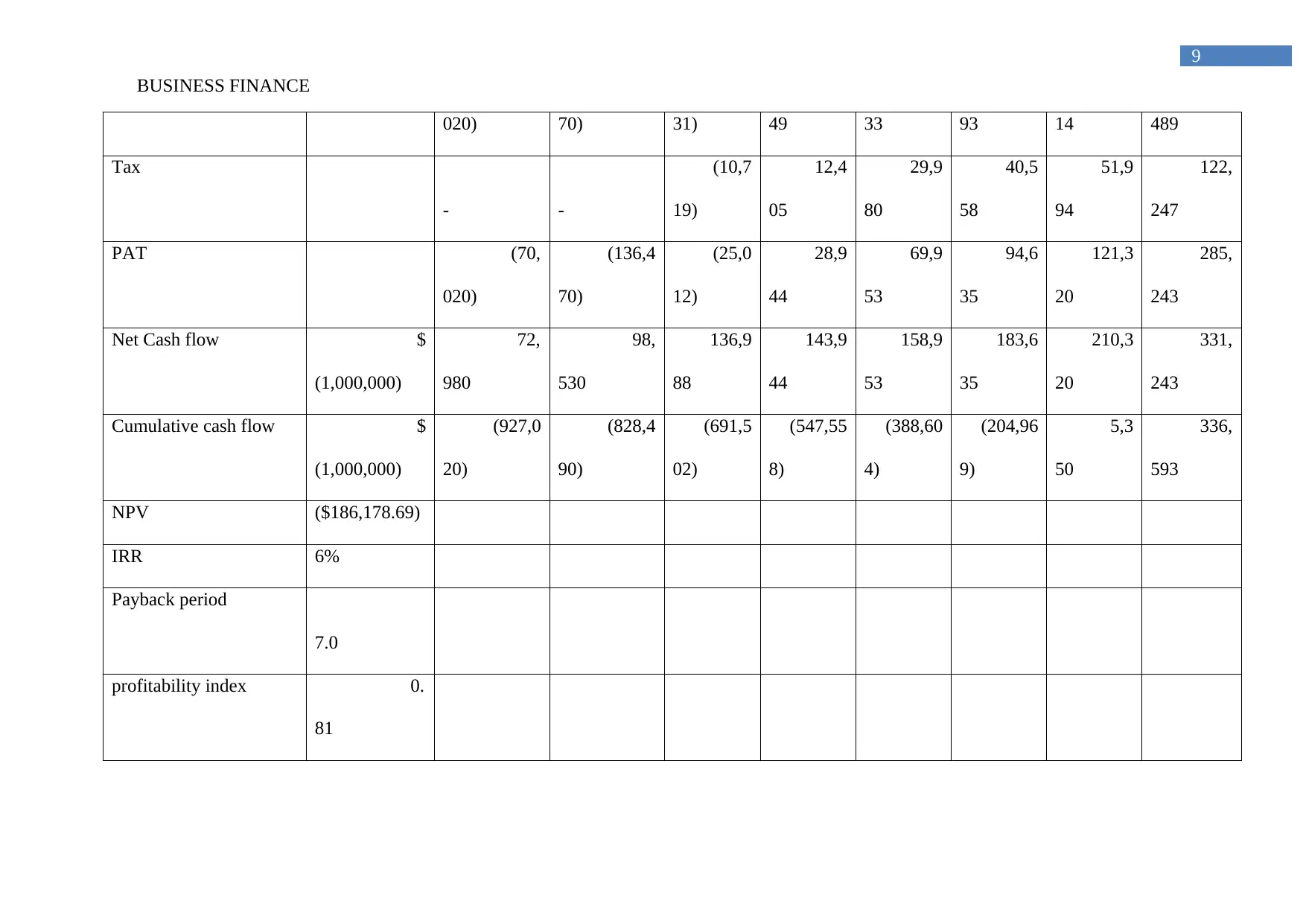

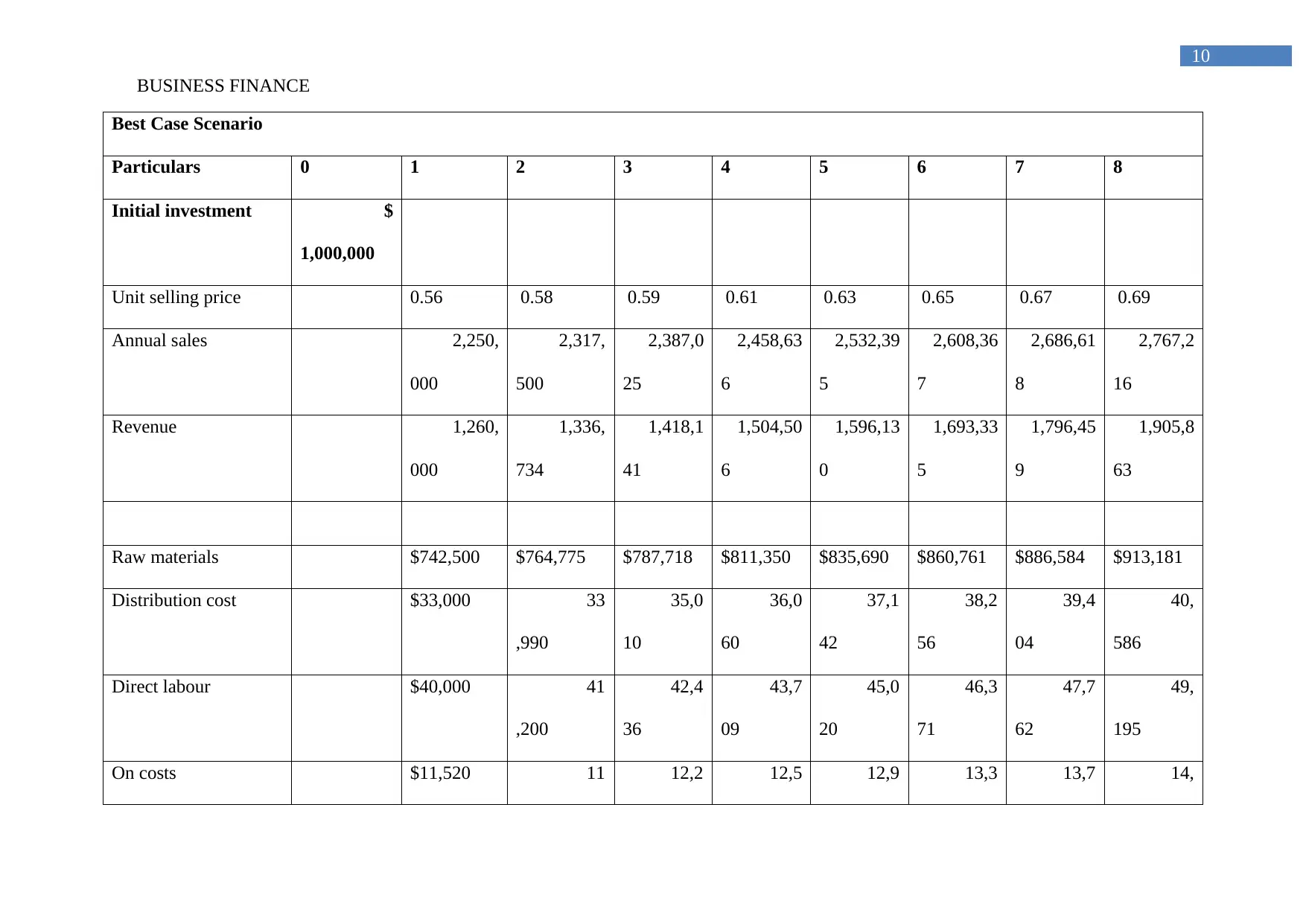

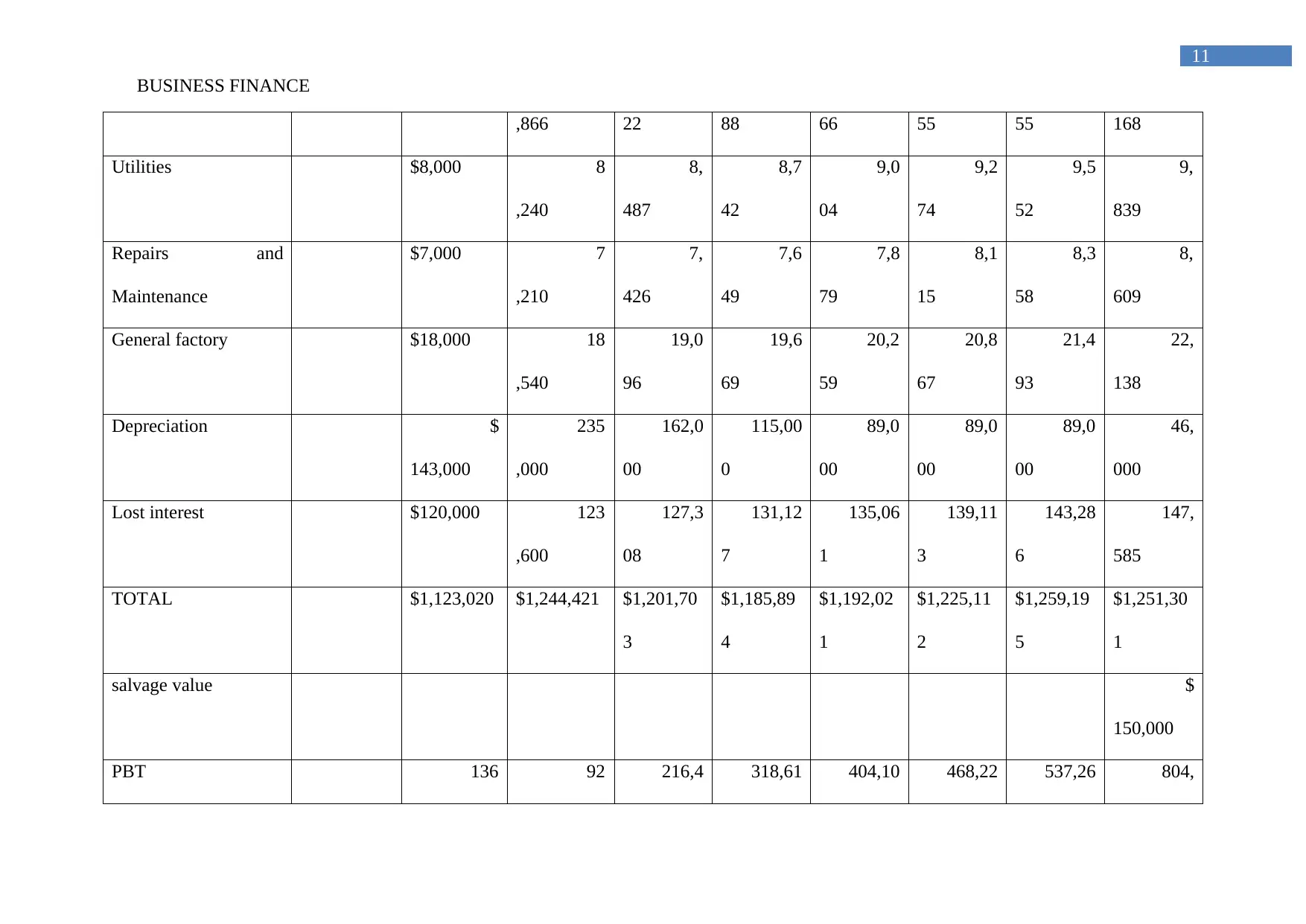

This report presents a comprehensive financial analysis of a new business project, evaluating its viability and potential returns. The analysis begins by identifying and omitting irrelevant expenses from an exhibit, followed by the calculation of incremental cash flows over an eight-year period. Key financial metrics such as Net Present Value (NPV), Internal Rate of Return (IRR), and Profitability Index (PI) are computed to assess the project's profitability. A sensitivity analysis is conducted to evaluate the project's performance under best-case and worst-case scenarios, alongside the derivation of expected sales, standard deviation, and coefficient of variance. The report also explores the impact of sales changes on project worthiness and discusses the rationale for using a high discount rate. Finally, it provides recommendations for the project, suggesting strategies to improve investment returns, and concludes that, despite potential risks, the project is viable and can generate positive returns, especially with increased sales as predicted by the sales team.

1 out of 15

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.