Finance Memorandum: Proposed Project Evaluation for Pinto Limited

VerifiedAdded on 2021/05/30

|7

|1108

|86

Report

AI Summary

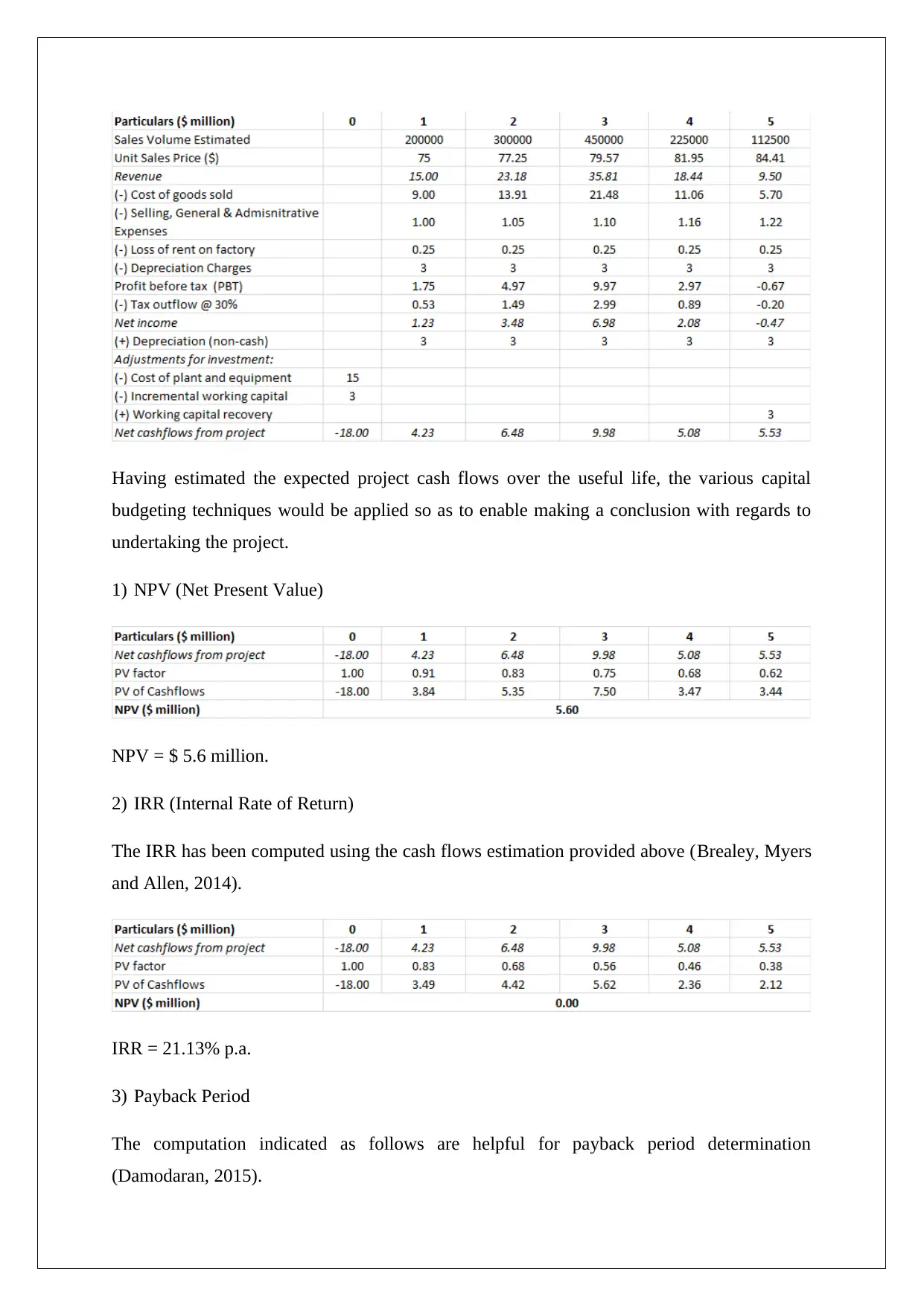

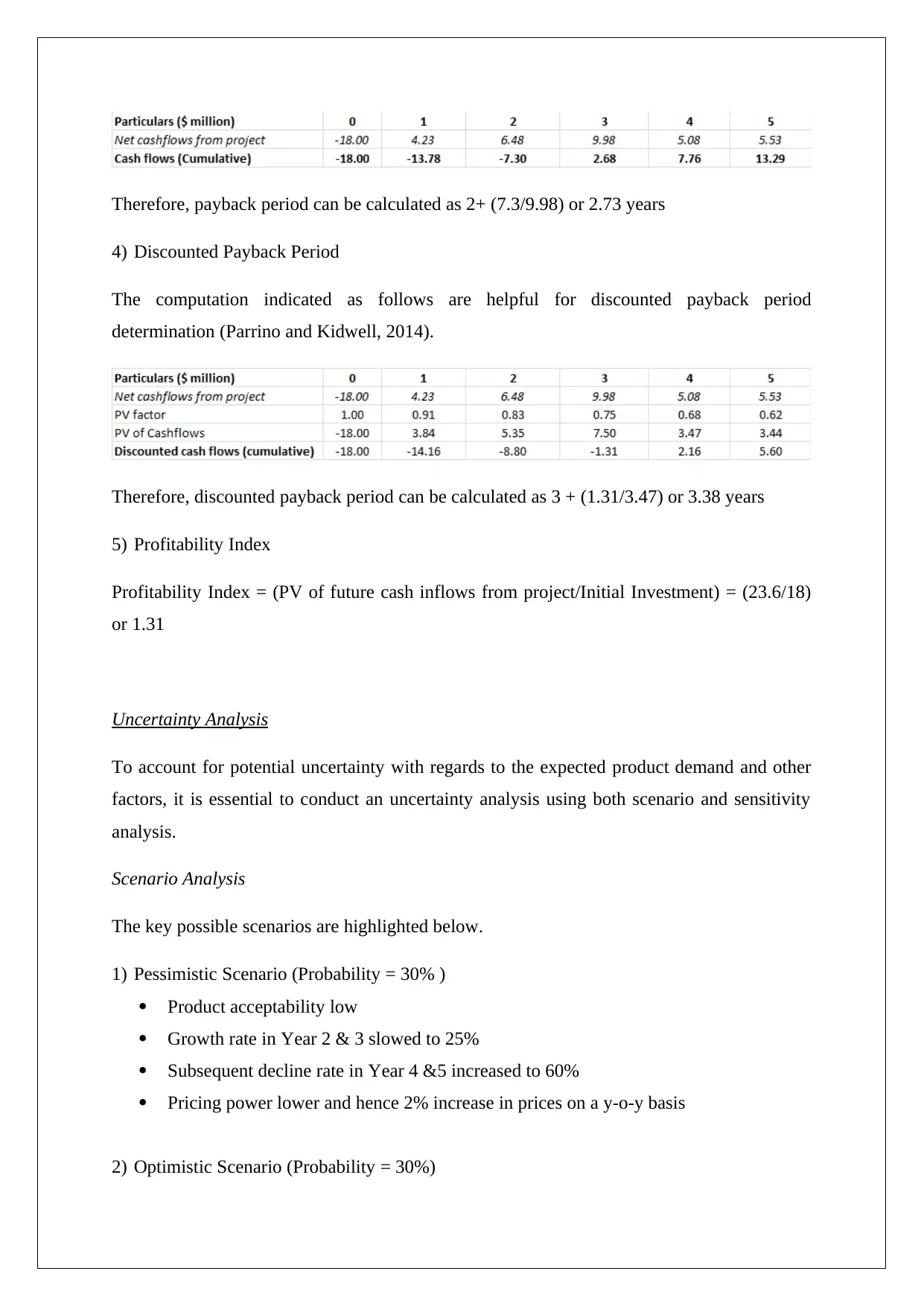

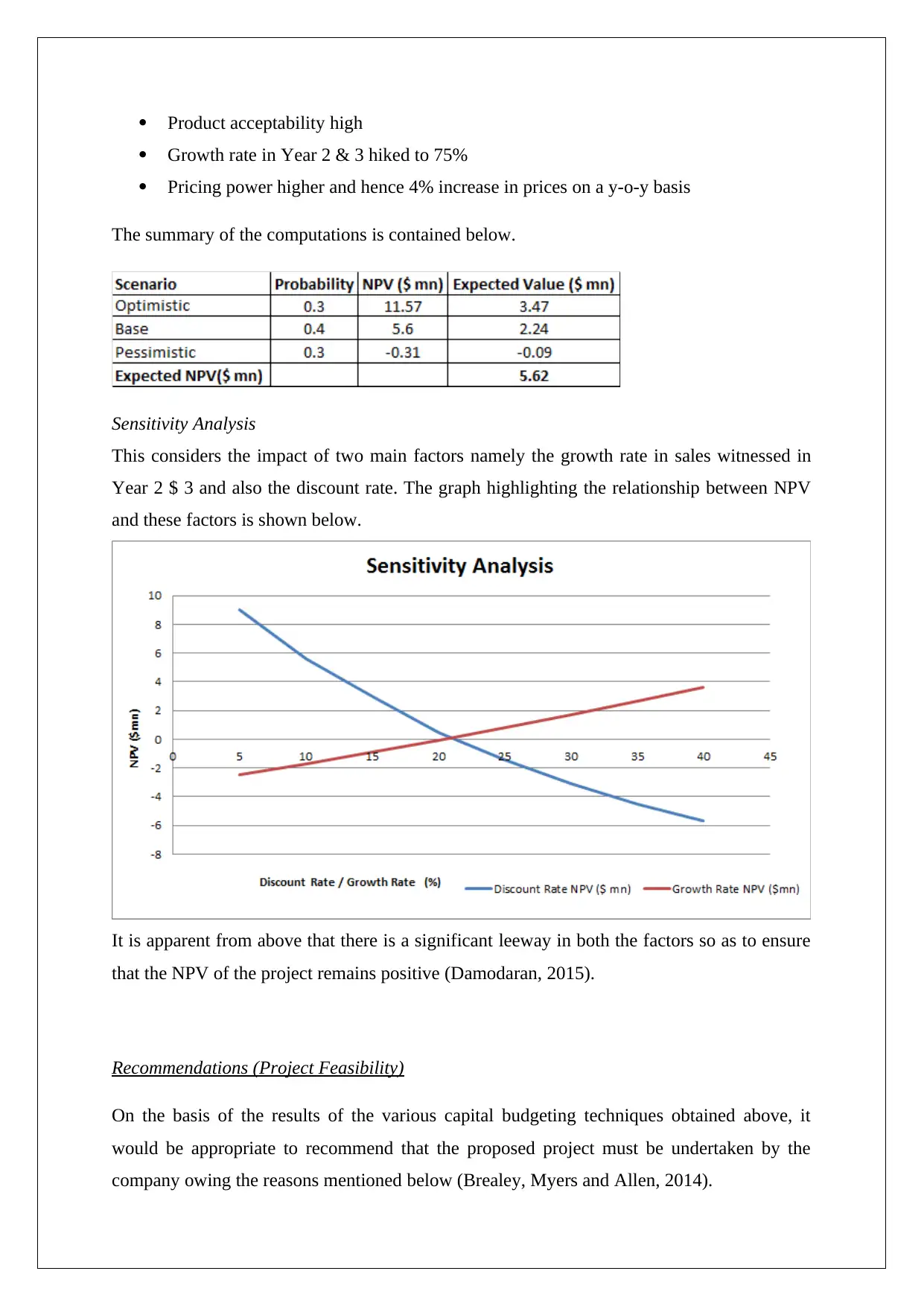

This finance memorandum, addressed to the CEO of Pinto Limited, presents an analysis of a proposed project in the face of increasing competition. The analysis incorporates key assumptions and considers sunk costs, opportunity costs, and depreciation. It calculates Net Present Value (NPV), Internal Rate of Return (IRR), payback period, discounted payback period, and Profitability Index (PI) to assess the project's financial viability. The report also includes scenario and sensitivity analyses to account for uncertainty, examining optimistic and pessimistic scenarios, and the impact of growth and discount rates on NPV. Based on the results, the memorandum recommends undertaking the project, highlighting its positive NPV, favorable IRR, and other positive indicators, concluding the project is financially feasible and creates value for shareholders.

1 out of 7

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.