Finance Project: Evaluating Capital Budgeting for Watley Ltd

VerifiedAdded on 2021/12/14

|8

|2178

|43

Project

AI Summary

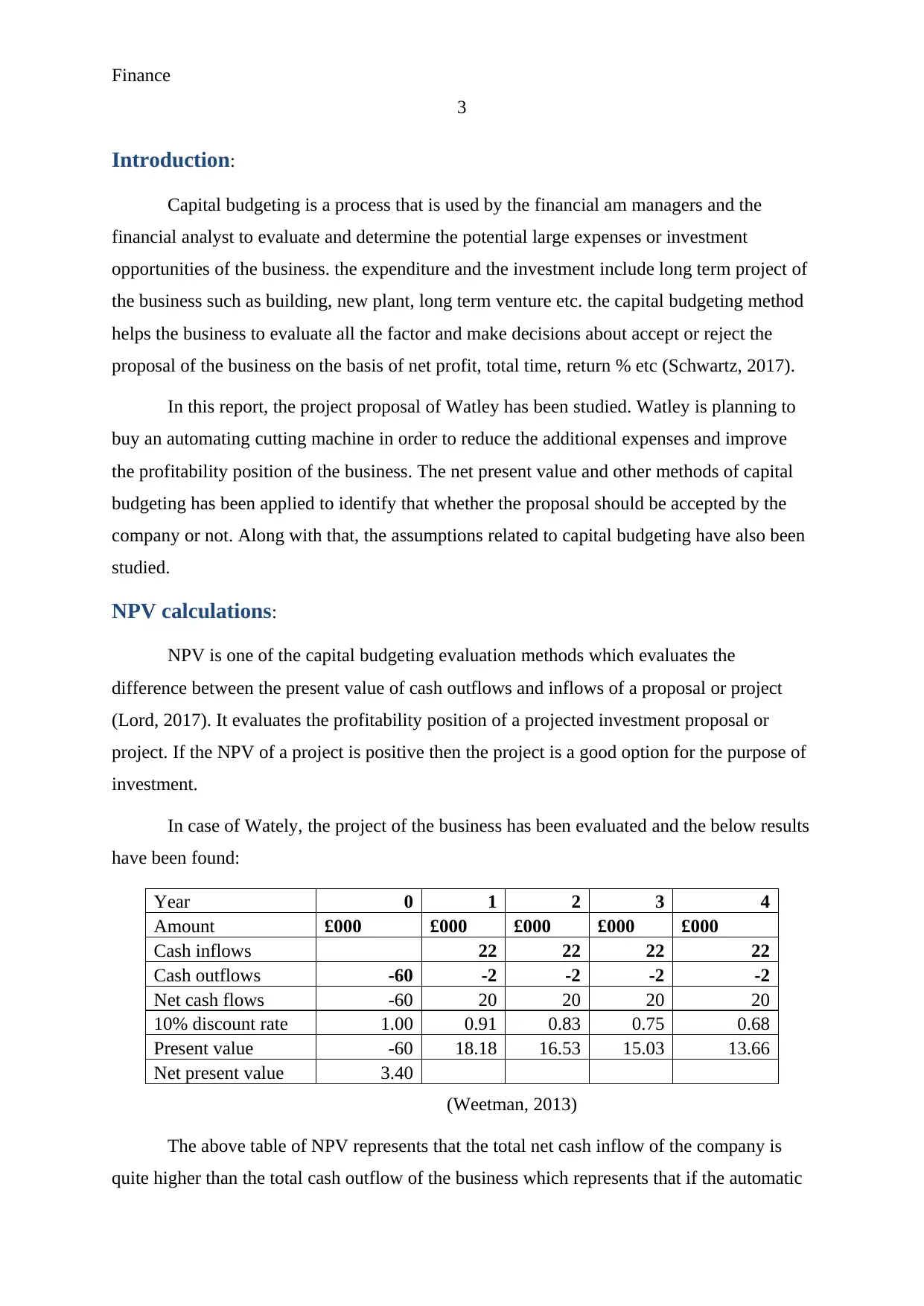

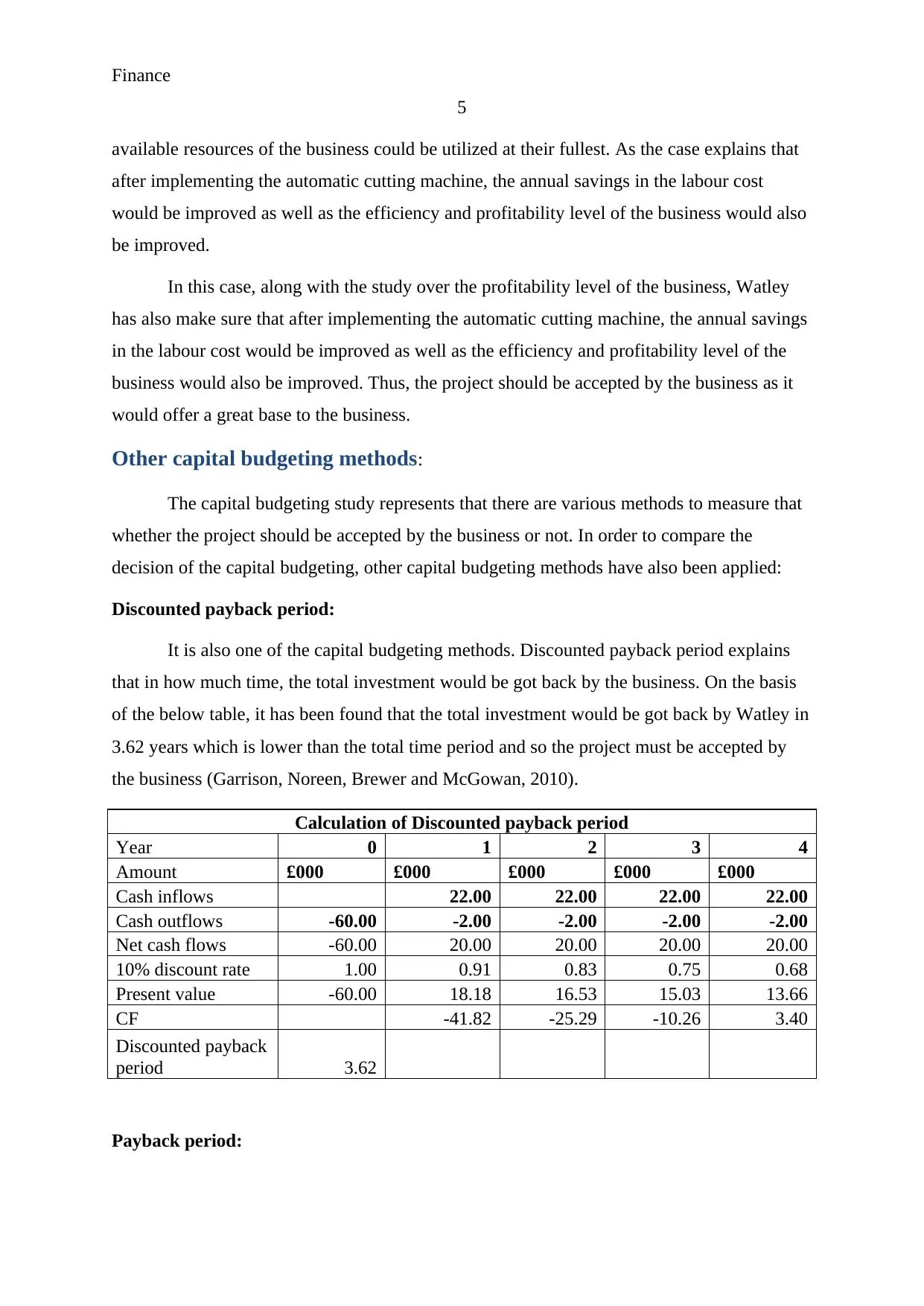

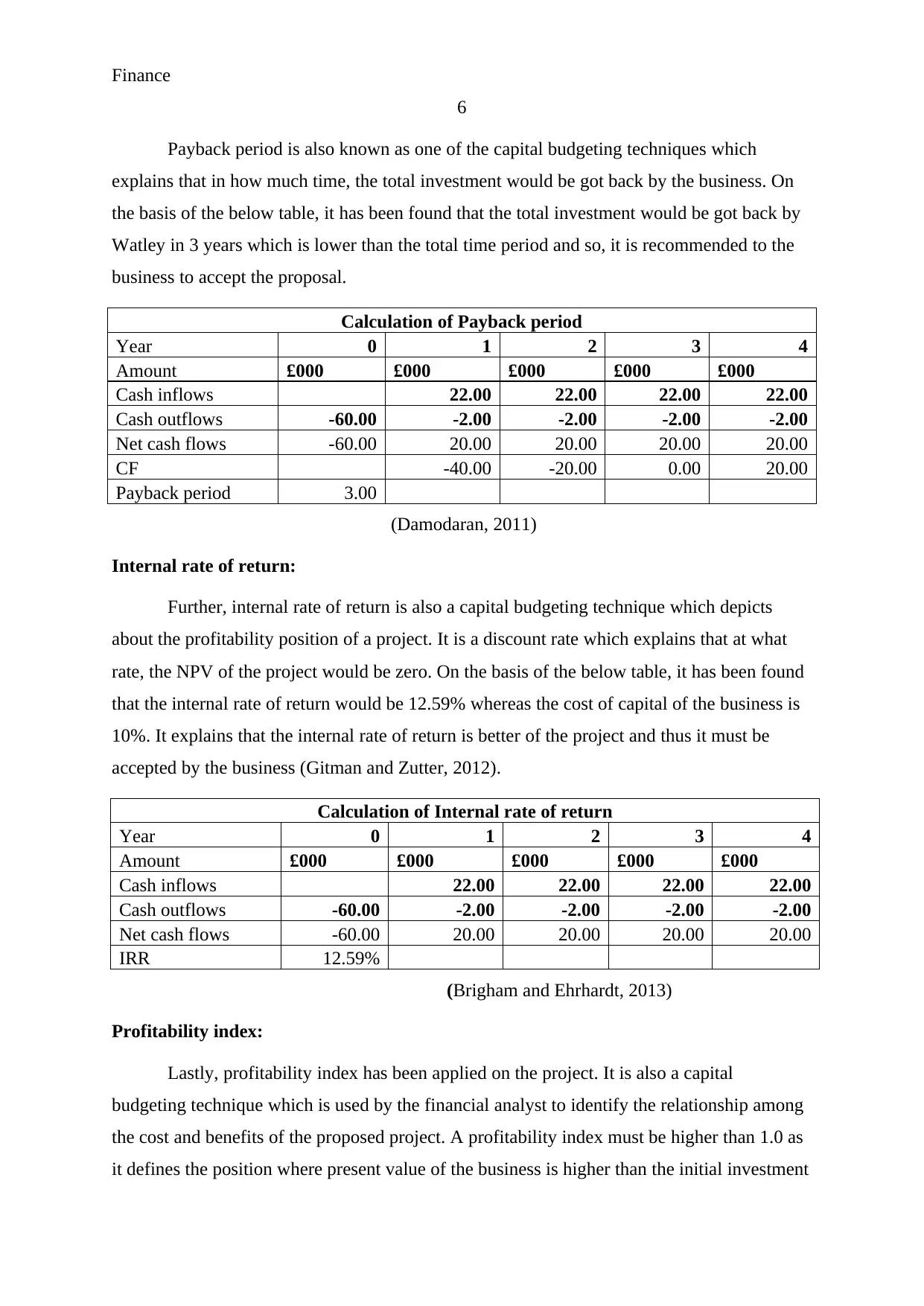

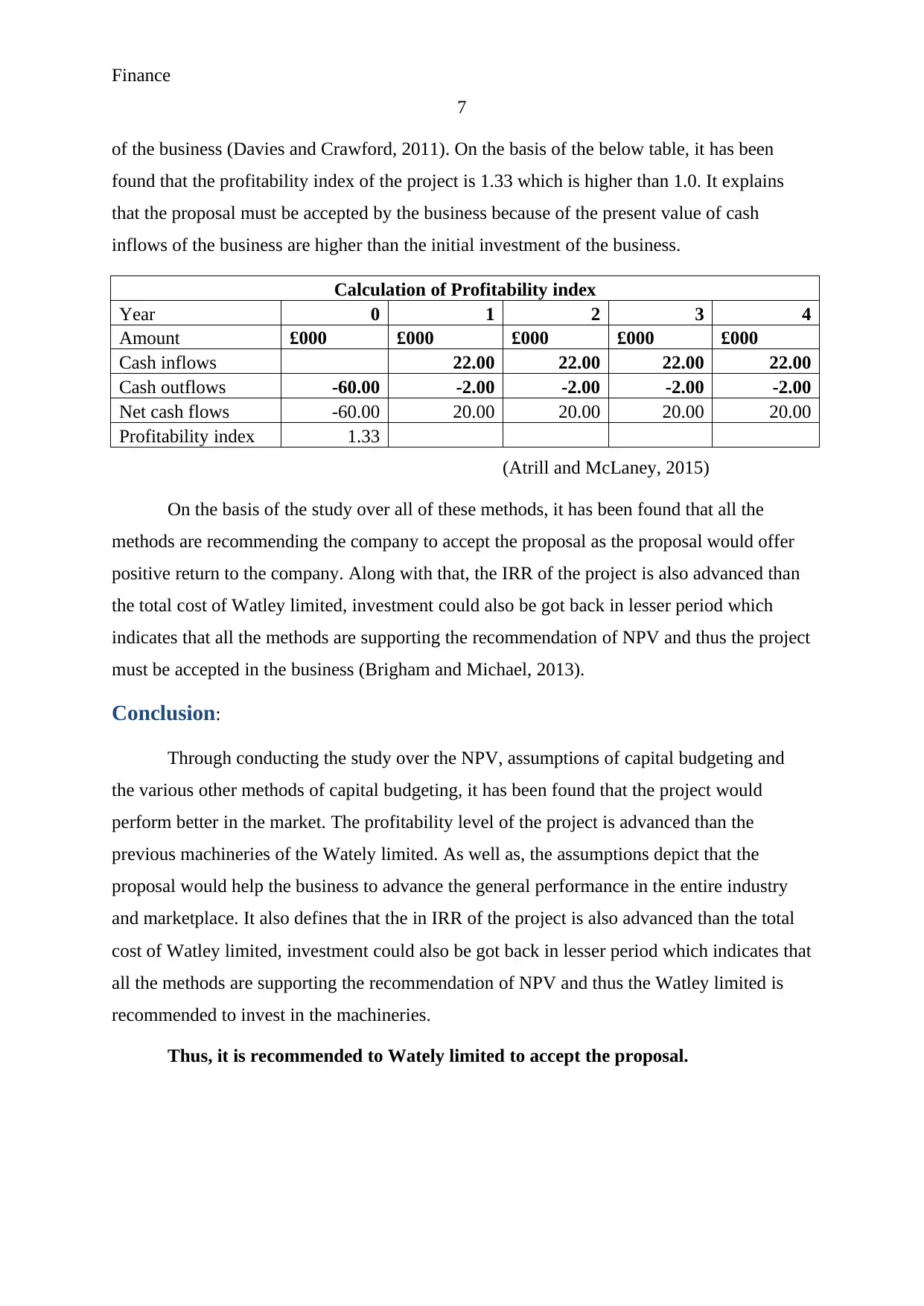

This project report analyzes a capital budgeting proposal for Watley Ltd, focusing on the potential purchase of an automated cutting machine. The report utilizes Net Present Value (NPV) calculations, considering cash inflows and outflows over a four-year period, and concludes that the project has a positive NPV, suggesting it is a good investment. It also addresses key assumptions of capital budgeting, such as maximizing shareholder worth and efficient resource management. Furthermore, the report employs other capital budgeting methods like discounted payback period, payback period, internal rate of return (IRR), and profitability index to support the NPV's recommendation. All methods consistently suggest the project's viability, recommending Watley Ltd to accept the proposal. The report references several financial management and accounting sources to support its analysis and conclusions.

1 out of 8

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.