Finance Module: Quantitative Calculations Assignment - University

VerifiedAdded on 2022/09/17

|16

|1299

|25

Homework Assignment

AI Summary

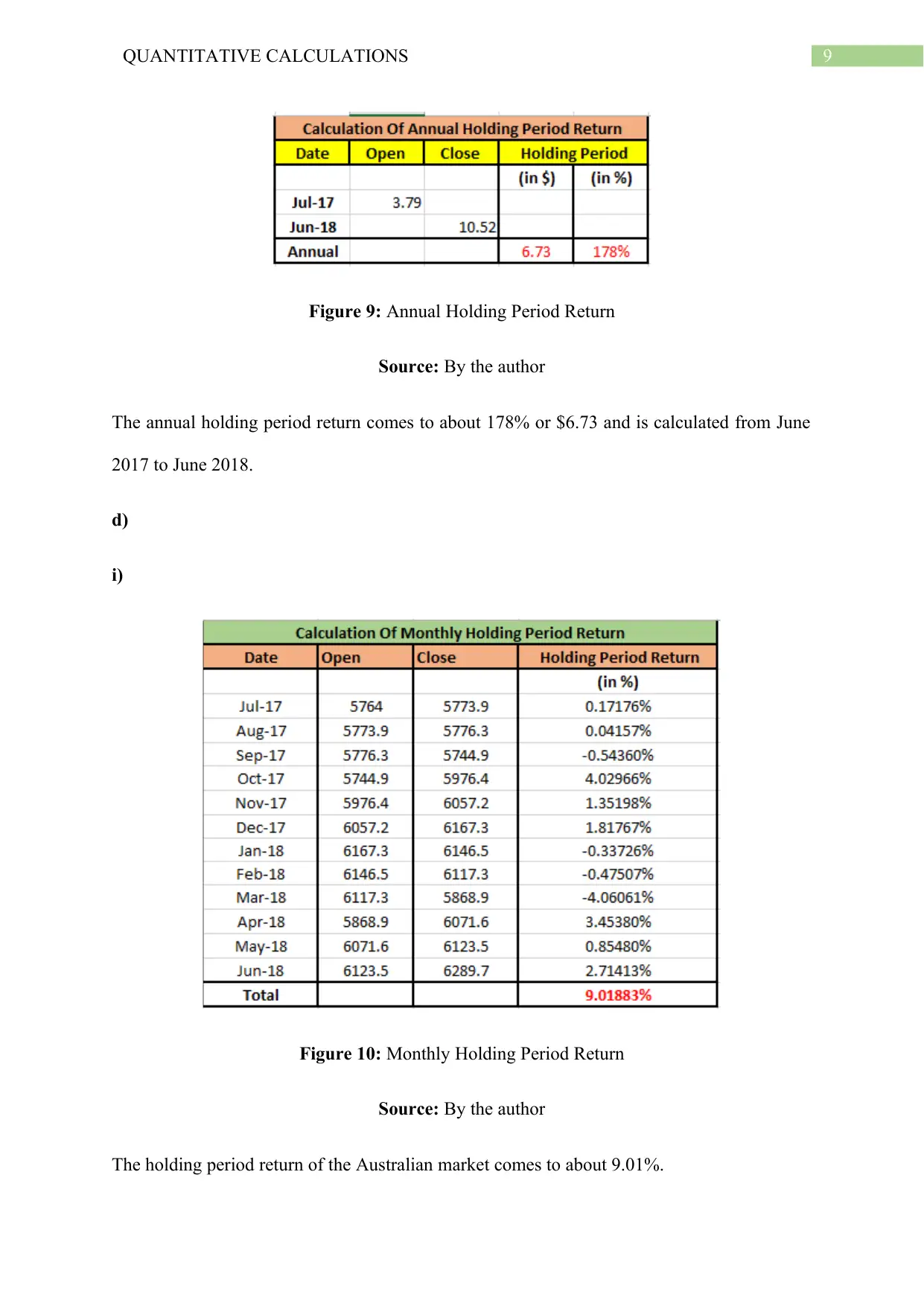

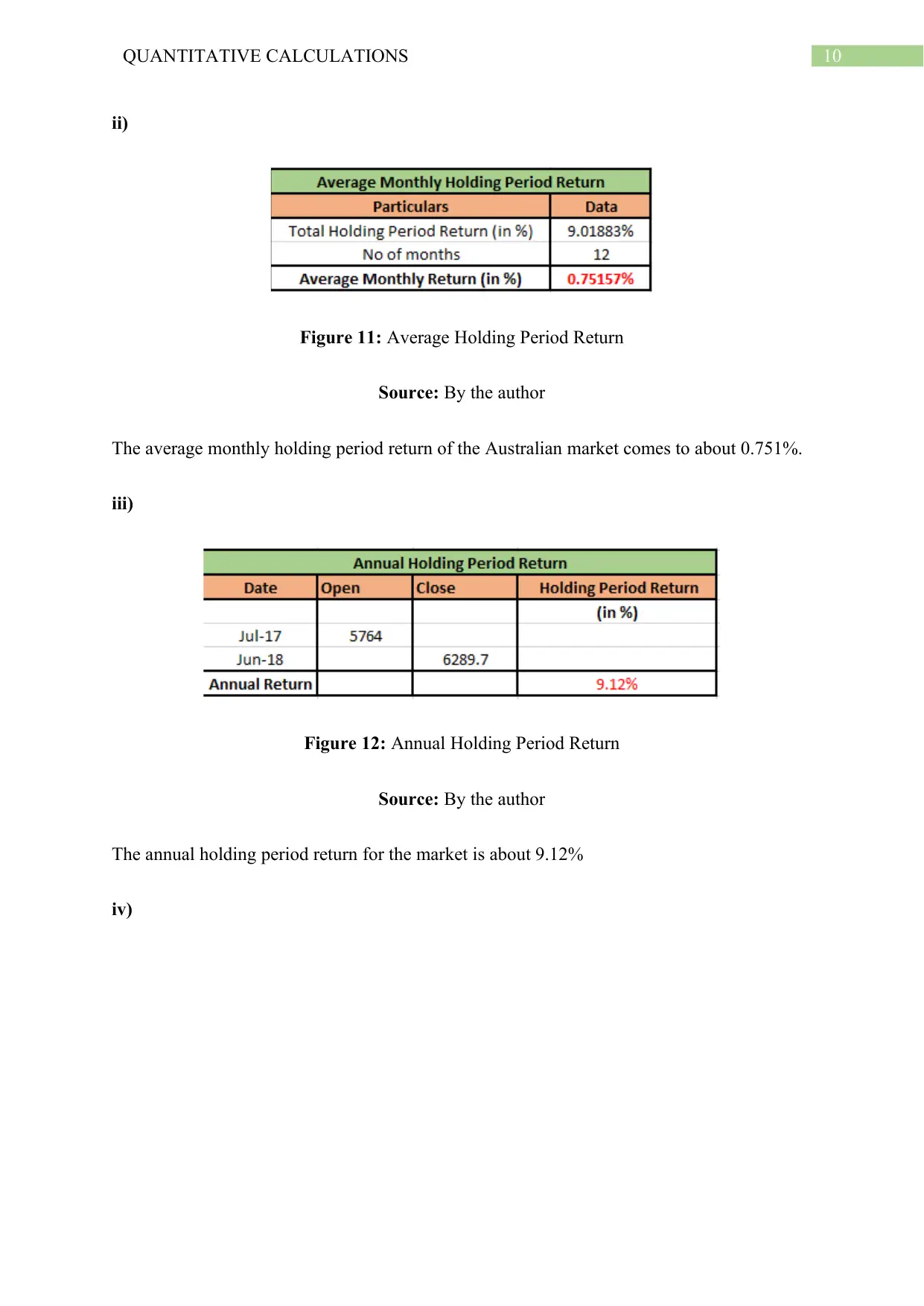

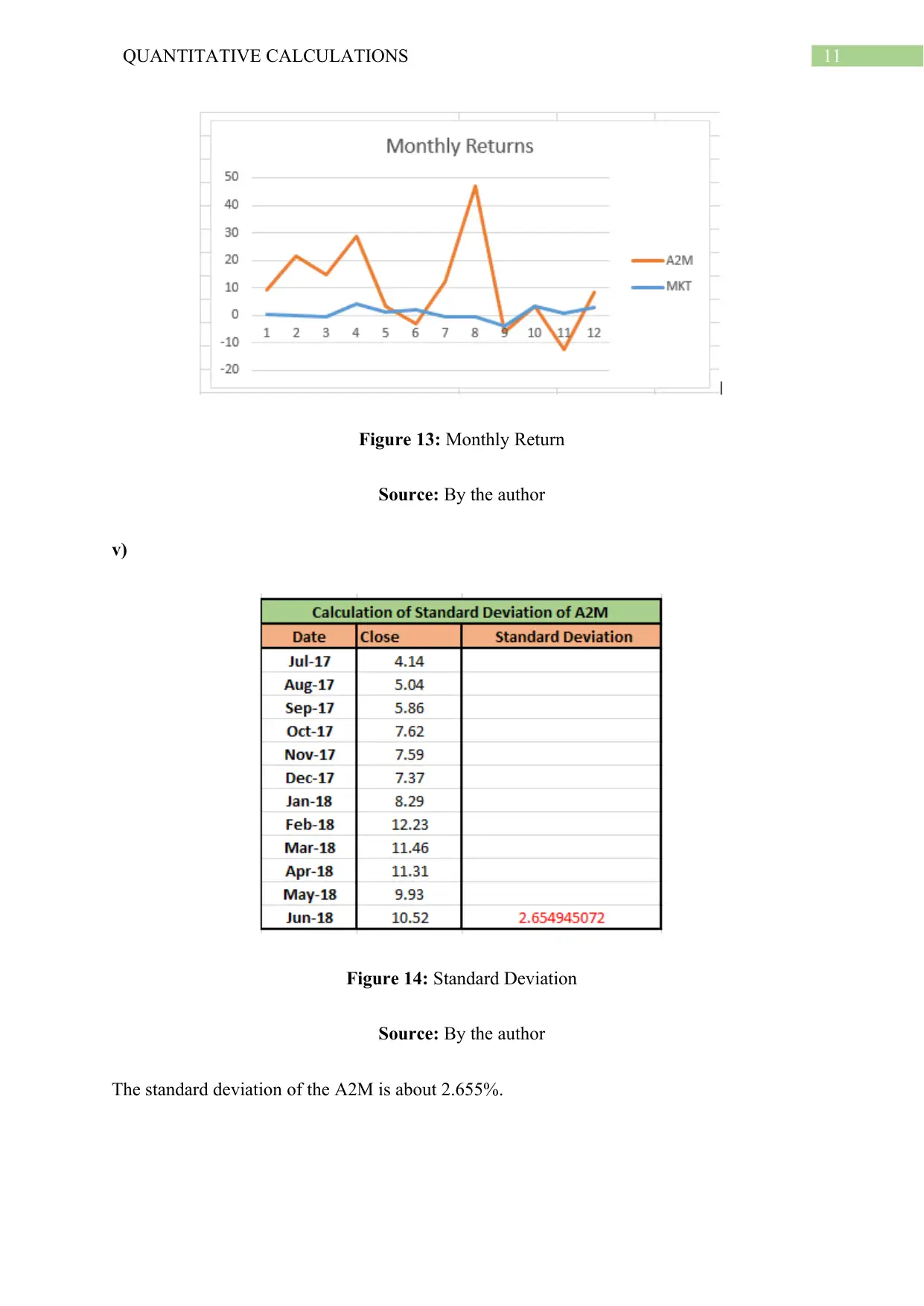

This assignment solution covers various quantitative calculations in finance. It includes calculations for determining the monthly payments needed to accumulate a specific future value, net present value (NPV) analysis to assess investment viability, and future value calculations for diversified portfolios and superannuation accounts. The solution also explores the differences between nominal, real, and notional interest rates and analyzes the impact of changes in the cash rate by the Reserve Bank of Australia. Furthermore, the assignment delves into dividend imputation, holding period returns, and market analysis, including standard deviation, beta, and the application of the Capital Asset Pricing Model (CAPM) to determine expected returns. The solution provides detailed formulas, workings, and interpretations of the results, along with relevant references.

1 out of 16

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.