University Finance Report: a2 Milk Company Financial Analysis

VerifiedAdded on 2023/04/23

|8

|1323

|327

Report

AI Summary

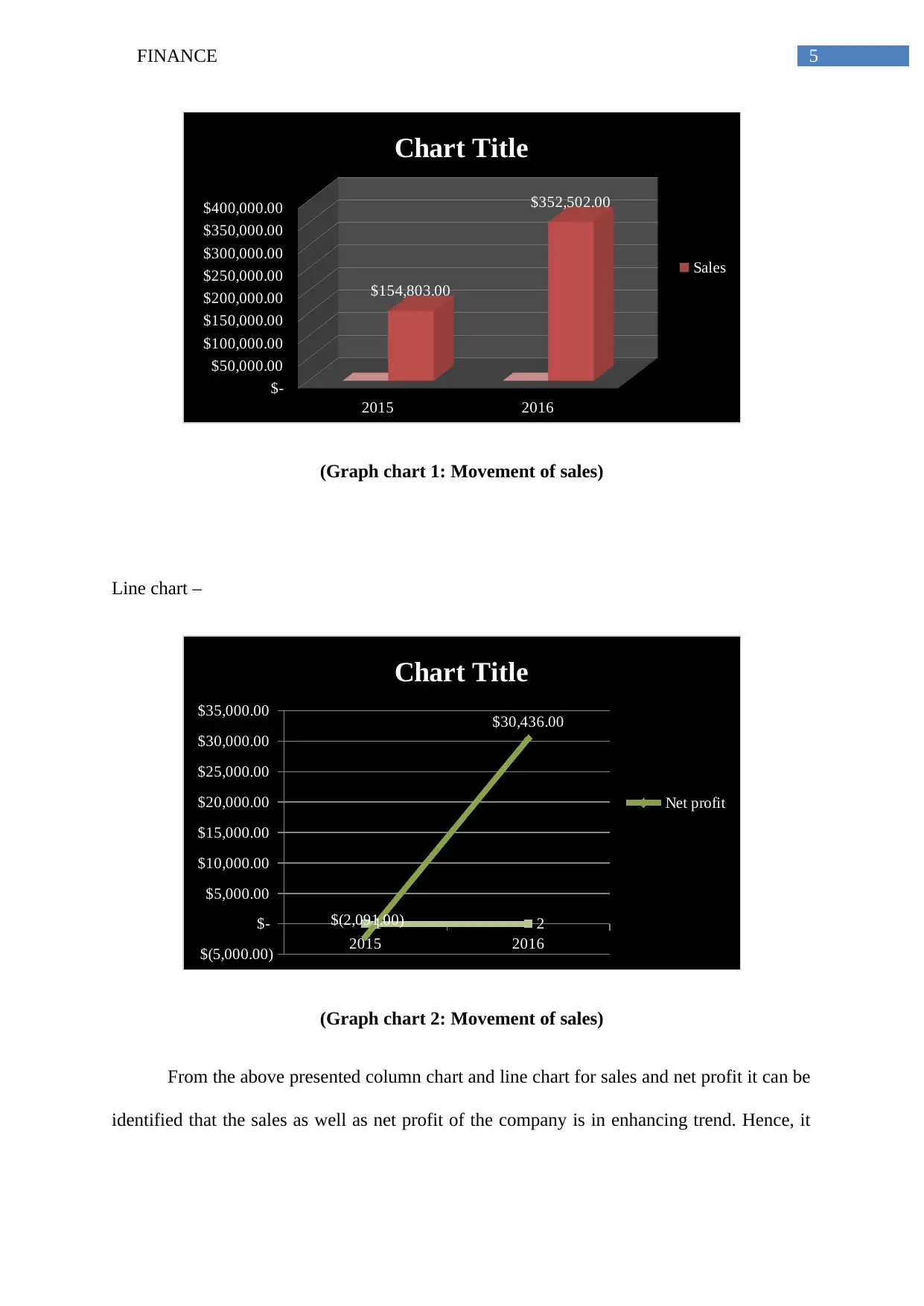

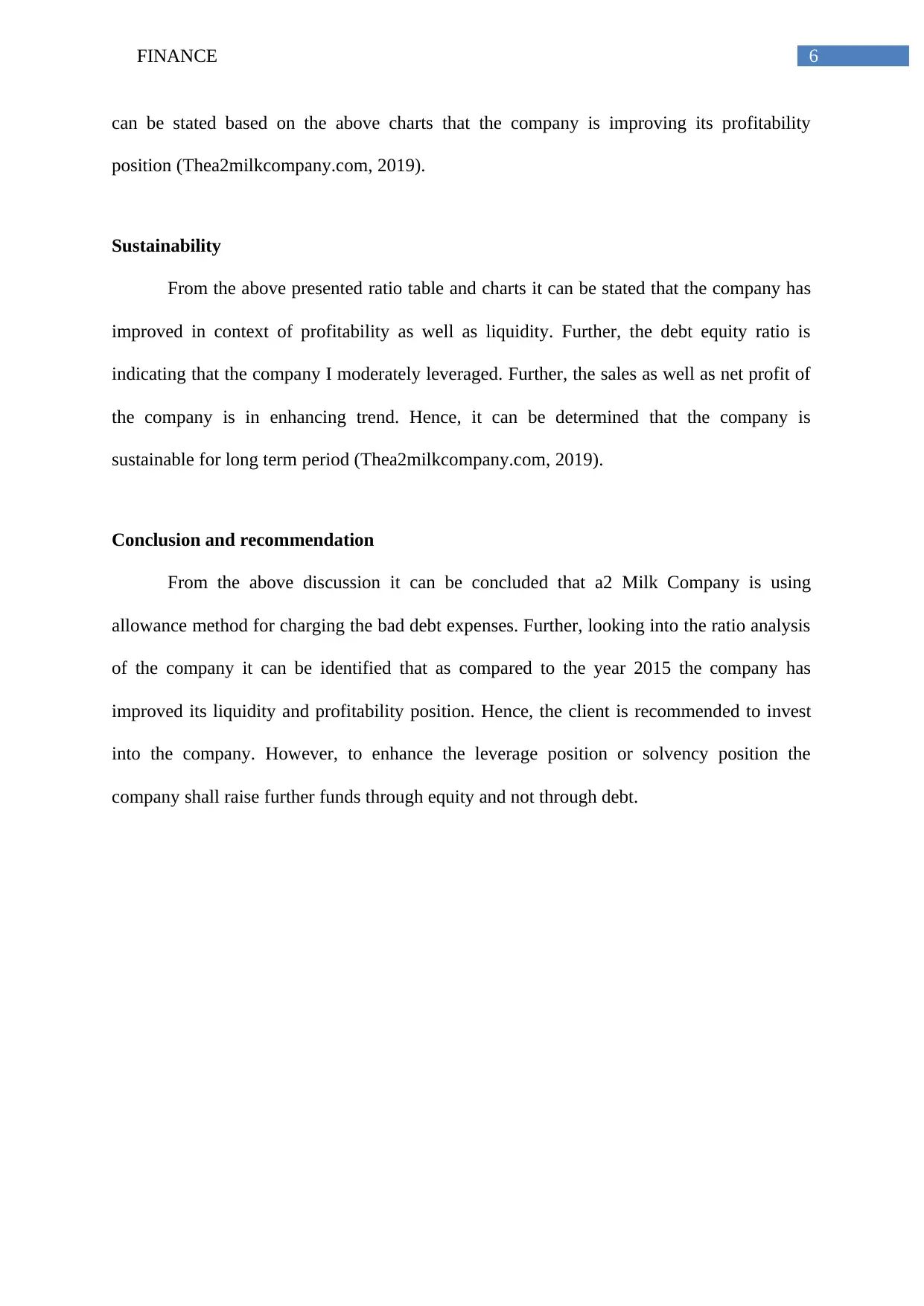

This finance report analyzes the financial position of the a2 Milk Company, focusing on the year ended 2016. It examines the company's bad debt expenses, specifically the $69,000 recorded, and the allowance method used. The report calculates and interprets key financial ratios such as net profit margin, current ratio, and debt-equity ratio to assess the company's liquidity, profitability, and solvency. The analysis includes charts illustrating sales and net profit trends, leading to an evaluation of the company's sustainability. The report concludes with recommendations for investment, suggesting the company should prioritize equity financing over debt to enhance its leverage position. The report uses information from the company's annual report and relevant financial literature to support its findings.

1 out of 8

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.