Business Finance Report: UTL, Madagascar Industries Financial Analysis

VerifiedAdded on 2023/01/16

|19

|3917

|63

Report

AI Summary

This report delves into the intricacies of business finance, focusing on working capital management and cash flow analysis within the context of UberTools Ltd (UTL) and Madagascar Industries. The report examines the relationship between cash flow and profit, emphasizing the importance of effective working capital management, including receivables, payables, and inventory. It analyzes how changes in working capital impact cash flows and provides recommendations for UTL to improve its cash flow issues. Furthermore, the report explores various financial ratios, such as sales growth, gross profit margin, operating profit margin, and gearing, to assess the financial performance of businesses. The analysis includes the calculation and interpretation of these ratios for Madagascar Industries, offering insights into its financial health and performance trends. The report concludes by suggesting strategies for Boards to evaluate the financial performance of a business, providing a comprehensive overview of financial management principles and their practical application.

Running head: BUSINESS FINANCE

Business Finance

Name of the Student

Name of the University

Author’s Note

Business Finance

Name of the Student

Name of the University

Author’s Note

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

1BUSINESS FINANCE

Table of Contents

Part 1..........................................................................................................................................2

Requirement [i]......................................................................................................................3

Requirement [ii].....................................................................................................................5

Requirement [iii]....................................................................................................................6

Part 2..........................................................................................................................................8

Requirement [i]......................................................................................................................9

Requirement [ii]...................................................................................................................14

References................................................................................................................................16

Table of Contents

Part 1..........................................................................................................................................2

Requirement [i]......................................................................................................................3

Requirement [ii].....................................................................................................................5

Requirement [iii]....................................................................................................................6

Part 2..........................................................................................................................................8

Requirement [i]......................................................................................................................9

Requirement [ii]...................................................................................................................14

References................................................................................................................................16

2BUSINESS FINANCE

Part 1

Executive Summary

This report aim at discussing different aspects of working capital management and cash flows

management in order to resolve the working capital and cash flow related issues in UberTools

Ltd (UTL). This report also sheds light on the crucial aspects like receivable, payables,

inventories and the effects on working capital due to the changes in working capital.

Part 1

Executive Summary

This report aim at discussing different aspects of working capital management and cash flows

management in order to resolve the working capital and cash flow related issues in UberTools

Ltd (UTL). This report also sheds light on the crucial aspects like receivable, payables,

inventories and the effects on working capital due to the changes in working capital.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

3BUSINESS FINANCE

Requirement [i]

Answer to [a]

In businesses, Cash Flow and Profit are considered as two different parameters, it is

needed to keep track of both of these aspects when running the business.

Cash Flow – Cash flow can be considered as the money that flows in and out of the business

from different business operations, financial and investing activities. It is the money that the

businesses need for meeting the present and long-term financial obligations (Ball et al. 2016).

Profit – Profit can be considered as net income of the companies and it is what leftovers from

sales after the payments of all the expenses. A business cannot ensure their long-term

sustainability unless there is profit (Nikolov and Whited 2014).

Difference – It needs to be mentioned that there are certain differences between cash flow

and profit as each of them produces different results. Profit is a narrow concept in accounting

since it only considers the income and expenses at a certain period; but the concept of cash

flow is dynamic since its concern is the movement of money in and out of a business and it

considers the time when the movement of money occurs. For this reason, the cash flow

concept is more in line with accounting reality as a business can be profitable, but still not

having adequate cash flow can harm its operations (Ball et al. 2016).

Answer to [b]

Working Capital – Working Capital can be considered as the money available to a company

for ensuring smooth day-to-day business operations. There are two very clear objectives of

working capital; first, to ensure increase in the profitability of the firms and two, to ensure the

presence of adequate liquidity for meeting the short-term business obligation when they fall

due for ensuring continuous business operations (Tsai 2016).

Requirement [i]

Answer to [a]

In businesses, Cash Flow and Profit are considered as two different parameters, it is

needed to keep track of both of these aspects when running the business.

Cash Flow – Cash flow can be considered as the money that flows in and out of the business

from different business operations, financial and investing activities. It is the money that the

businesses need for meeting the present and long-term financial obligations (Ball et al. 2016).

Profit – Profit can be considered as net income of the companies and it is what leftovers from

sales after the payments of all the expenses. A business cannot ensure their long-term

sustainability unless there is profit (Nikolov and Whited 2014).

Difference – It needs to be mentioned that there are certain differences between cash flow

and profit as each of them produces different results. Profit is a narrow concept in accounting

since it only considers the income and expenses at a certain period; but the concept of cash

flow is dynamic since its concern is the movement of money in and out of a business and it

considers the time when the movement of money occurs. For this reason, the cash flow

concept is more in line with accounting reality as a business can be profitable, but still not

having adequate cash flow can harm its operations (Ball et al. 2016).

Answer to [b]

Working Capital – Working Capital can be considered as the money available to a company

for ensuring smooth day-to-day business operations. There are two very clear objectives of

working capital; first, to ensure increase in the profitability of the firms and two, to ensure the

presence of adequate liquidity for meeting the short-term business obligation when they fall

due for ensuring continuous business operations (Tsai 2016).

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

4BUSINESS FINANCE

Receivables – Receivable can be considered as the amount due from a customer, supplier,

employee or any other party for business purposes. The classification of receivables can be

done as accounts receivable, notes receivable and it can also be represented as an asset from a

firm (Harris and Mooney Jr 2013).

Inventory – Inventory is referred to an accounting term that is considered as goods that are in

different stages of work-in-progress for the purpose of sales. Inventories include finished

goods available for selling, work-in-progress that is the process of being made and raw

materials that need to be used for producing finished goods (Wild 2017).

Payables – Payables can be considered as the money outstanding to lenders, creditors,

employees, government or other parties for business purposes and these are presented in the

company’s balance sheet as liabilities. They are considered as short-term liabilities in case

they are due within 12 months, otherwise they are considered as long-term liabilities

(Muscettola 2014).

Answer to [c]

It needs to be mentioned that the changes in working capital affects cash flows in

many ways. An aggressive approach related to the investment level in working capital

indicates the intention of a firm to operate with less inventory, cash and trade receivable. It

increases profit since less cash is involved with the current asset but will increase risk due to

the increase in the possibility of shortage in cash or inventory (Baños-Caballero, García-

Teruel and Martínez-Solano 2014). On the other hand, the companies become able in

maintaining large cash balance with the help of a conservative and more flexible policy for

maintaining working capital policy. In addition, this change in working capital position will

reduce the financial risk since it assists in reducing the inventory related risks. Lastly, in the

presence of a moderate working capital policy, the companies will be able in marinating a

Receivables – Receivable can be considered as the amount due from a customer, supplier,

employee or any other party for business purposes. The classification of receivables can be

done as accounts receivable, notes receivable and it can also be represented as an asset from a

firm (Harris and Mooney Jr 2013).

Inventory – Inventory is referred to an accounting term that is considered as goods that are in

different stages of work-in-progress for the purpose of sales. Inventories include finished

goods available for selling, work-in-progress that is the process of being made and raw

materials that need to be used for producing finished goods (Wild 2017).

Payables – Payables can be considered as the money outstanding to lenders, creditors,

employees, government or other parties for business purposes and these are presented in the

company’s balance sheet as liabilities. They are considered as short-term liabilities in case

they are due within 12 months, otherwise they are considered as long-term liabilities

(Muscettola 2014).

Answer to [c]

It needs to be mentioned that the changes in working capital affects cash flows in

many ways. An aggressive approach related to the investment level in working capital

indicates the intention of a firm to operate with less inventory, cash and trade receivable. It

increases profit since less cash is involved with the current asset but will increase risk due to

the increase in the possibility of shortage in cash or inventory (Baños-Caballero, García-

Teruel and Martínez-Solano 2014). On the other hand, the companies become able in

maintaining large cash balance with the help of a conservative and more flexible policy for

maintaining working capital policy. In addition, this change in working capital position will

reduce the financial risk since it assists in reducing the inventory related risks. Lastly, in the

presence of a moderate working capital policy, the companies will be able in marinating a

5BUSINESS FINANCE

moderate level of cash flows in their businesses in the presence of moderate level of risk.

Hence, it can be seen from the above discussion that the changes in working capital affects

the ability of the companies in maintaining adequate level of cash flows for their business

operations. Every business needs to consider this aspect foe efficient working capital

management (Tsai 2016).

Requirement [ii]

It can be seen from the provided scenario of UTL that the company has registered

impressive amounts of turnovers as well as operating profit before tax in the last year that are

£400 million and £35 million respectively. There is not any problem with UTL in this aspect

as the company has ensured impressive profitability. However, the earlier discussion

indicates towards the fact in spite of the presence of profitability, companies can suffer in

case they do not have sufficient cash flows and this is the issue with UTL. It can be seen from

the given situation that Omar who is responsible for managing UTI is not able in ensuring

adequate cash flows in the business that is affecting the company from different aspects

(Akoto, Awunyo-Vitor and Angmor 2013).

In the absence of sufficient cash flows, Omar is not able in paying the debts of UTI

and thus, it increases from £250 million to £350 million. For this reason, Omar is requesting

other shareholders to increase the amount of investment for infusing cash in the business. In

addition, Omar is not considering the effective management of working capital as he is

continuously investing money in the business when there is only few ways left of inflow of

cash in the business. This ineffective management of working capital by Omar has increased

the amount of stock of materials and supplies at UTL’s production site. This huge stock of

inventory is blocking the ways of cash inflows in the business which is increasing the

business risks. Lastly, the increased amount of due receivables is hindering the ways of cash

moderate level of cash flows in their businesses in the presence of moderate level of risk.

Hence, it can be seen from the above discussion that the changes in working capital affects

the ability of the companies in maintaining adequate level of cash flows for their business

operations. Every business needs to consider this aspect foe efficient working capital

management (Tsai 2016).

Requirement [ii]

It can be seen from the provided scenario of UTL that the company has registered

impressive amounts of turnovers as well as operating profit before tax in the last year that are

£400 million and £35 million respectively. There is not any problem with UTL in this aspect

as the company has ensured impressive profitability. However, the earlier discussion

indicates towards the fact in spite of the presence of profitability, companies can suffer in

case they do not have sufficient cash flows and this is the issue with UTL. It can be seen from

the given situation that Omar who is responsible for managing UTI is not able in ensuring

adequate cash flows in the business that is affecting the company from different aspects

(Akoto, Awunyo-Vitor and Angmor 2013).

In the absence of sufficient cash flows, Omar is not able in paying the debts of UTI

and thus, it increases from £250 million to £350 million. For this reason, Omar is requesting

other shareholders to increase the amount of investment for infusing cash in the business. In

addition, Omar is not considering the effective management of working capital as he is

continuously investing money in the business when there is only few ways left of inflow of

cash in the business. This ineffective management of working capital by Omar has increased

the amount of stock of materials and supplies at UTL’s production site. This huge stock of

inventory is blocking the ways of cash inflows in the business which is increasing the

business risks. Lastly, the increased amount of due receivables is hindering the ways of cash

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

6BUSINESS FINANCE

inflows in the business of UTL leaving ineffective working capital management in the

company (Akoto, Awunyo-Vitor and Angmor 2013).

Requirement [iii]

Working capital can be considered as the balance between current liabilities and

current assets. At the same time, working capital can be considered as equilibrium between

the resource-purchasing and income-generating business activities of a firm in which it has

major linkage with the effective cash flow management (Aktas, Croci and Petmezas 2015).

The above discussion shows many issues in UTL that can be resolved with the help of the

following steps.

As per the earlier discussion, UTL has certain major issue related to cash flows as the

company lacks adequate cash inflows for their business. Thus, it is recommended to Omar to

use the Cash Conversion Cycle for determining the amount of cash required for any level of

sales. In order to afford a longer cash conversion cycle, UTL needs greater investments in

working capital. This particular will ensure the presence of sufficient cash inflows in the

business of UTL so that they can conduct their daily business operations in smooth manner

(Abbadi and Abbadi 2013).

The earlier discussion also shows the UTL has major issues with inventory

management as a large stock of materials and supplies has developed in the company’s

production site. For this reason, the company is needed to reduce the inventory conversion

period to get rid of this issue and this can be ensured by shortening the production cycle

length. For this, UTL can use Just-in-Time production system as this will be more responsive

to the change in sales level. Frequent clearing of stock will increases sales in ensuring cash

inflow and the issue of working capital will be reduced (Aktas, Croci and Petmezas 2015).

inflows in the business of UTL leaving ineffective working capital management in the

company (Akoto, Awunyo-Vitor and Angmor 2013).

Requirement [iii]

Working capital can be considered as the balance between current liabilities and

current assets. At the same time, working capital can be considered as equilibrium between

the resource-purchasing and income-generating business activities of a firm in which it has

major linkage with the effective cash flow management (Aktas, Croci and Petmezas 2015).

The above discussion shows many issues in UTL that can be resolved with the help of the

following steps.

As per the earlier discussion, UTL has certain major issue related to cash flows as the

company lacks adequate cash inflows for their business. Thus, it is recommended to Omar to

use the Cash Conversion Cycle for determining the amount of cash required for any level of

sales. In order to afford a longer cash conversion cycle, UTL needs greater investments in

working capital. This particular will ensure the presence of sufficient cash inflows in the

business of UTL so that they can conduct their daily business operations in smooth manner

(Abbadi and Abbadi 2013).

The earlier discussion also shows the UTL has major issues with inventory

management as a large stock of materials and supplies has developed in the company’s

production site. For this reason, the company is needed to reduce the inventory conversion

period to get rid of this issue and this can be ensured by shortening the production cycle

length. For this, UTL can use Just-in-Time production system as this will be more responsive

to the change in sales level. Frequent clearing of stock will increases sales in ensuring cash

inflow and the issue of working capital will be reduced (Aktas, Croci and Petmezas 2015).

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

7BUSINESS FINANCE

It can also be seen from the earlier discussion that UTL has major amount outstanding

from its two big customers which is affecting working capital and cash-flows of the

company. In order to resolve this issue, the company is needed to shorten the trade receivable

conversion period while offering their major customers incentive for early payments through

the reduction of credit period. In addition, the company needs to ensure more effective

examination of credit worthiness (Abbadi and Abbadi 2013). These steps will ensure the

effective management of working capital and cash flows in the company.

It can also be seen from the earlier discussion that UTL has major amount outstanding

from its two big customers which is affecting working capital and cash-flows of the

company. In order to resolve this issue, the company is needed to shorten the trade receivable

conversion period while offering their major customers incentive for early payments through

the reduction of credit period. In addition, the company needs to ensure more effective

examination of credit worthiness (Abbadi and Abbadi 2013). These steps will ensure the

effective management of working capital and cash flows in the company.

8BUSINESS FINANCE

Part 2

Executive Summary

This part of the report intents to discuss about different financial ratios in order to measure

different elements of the financial performance of the companies. In addition, this report also

sheds on the ways of Boards for assessing the financial performance of a business.

Part 2

Executive Summary

This part of the report intents to discuss about different financial ratios in order to measure

different elements of the financial performance of the companies. In addition, this report also

sheds on the ways of Boards for assessing the financial performance of a business.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

9BUSINESS FINANCE

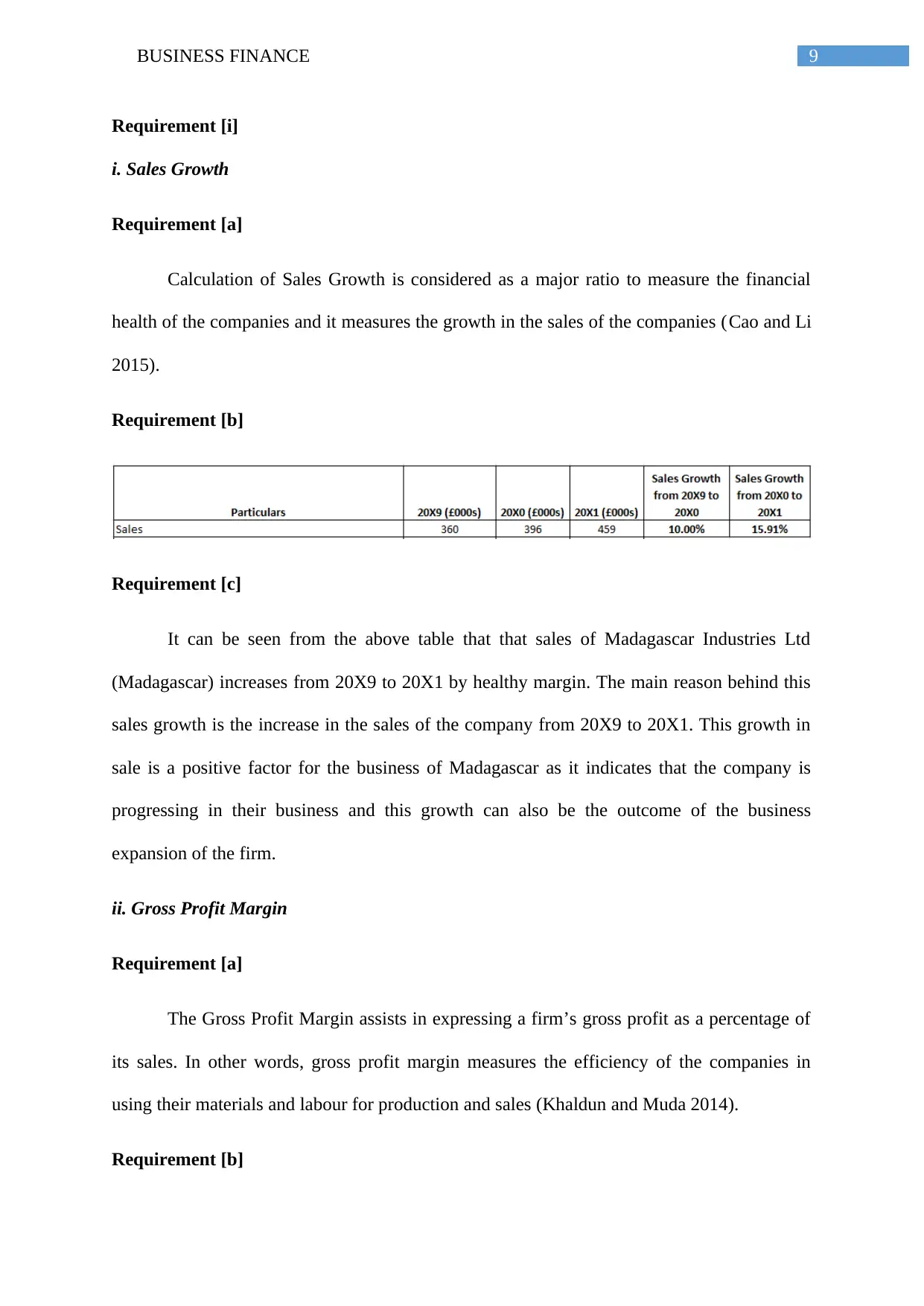

Requirement [i]

i. Sales Growth

Requirement [a]

Calculation of Sales Growth is considered as a major ratio to measure the financial

health of the companies and it measures the growth in the sales of the companies (Cao and Li

2015).

Requirement [b]

Requirement [c]

It can be seen from the above table that that sales of Madagascar Industries Ltd

(Madagascar) increases from 20X9 to 20X1 by healthy margin. The main reason behind this

sales growth is the increase in the sales of the company from 20X9 to 20X1. This growth in

sale is a positive factor for the business of Madagascar as it indicates that the company is

progressing in their business and this growth can also be the outcome of the business

expansion of the firm.

ii. Gross Profit Margin

Requirement [a]

The Gross Profit Margin assists in expressing a firm’s gross profit as a percentage of

its sales. In other words, gross profit margin measures the efficiency of the companies in

using their materials and labour for production and sales (Khaldun and Muda 2014).

Requirement [b]

Requirement [i]

i. Sales Growth

Requirement [a]

Calculation of Sales Growth is considered as a major ratio to measure the financial

health of the companies and it measures the growth in the sales of the companies (Cao and Li

2015).

Requirement [b]

Requirement [c]

It can be seen from the above table that that sales of Madagascar Industries Ltd

(Madagascar) increases from 20X9 to 20X1 by healthy margin. The main reason behind this

sales growth is the increase in the sales of the company from 20X9 to 20X1. This growth in

sale is a positive factor for the business of Madagascar as it indicates that the company is

progressing in their business and this growth can also be the outcome of the business

expansion of the firm.

ii. Gross Profit Margin

Requirement [a]

The Gross Profit Margin assists in expressing a firm’s gross profit as a percentage of

its sales. In other words, gross profit margin measures the efficiency of the companies in

using their materials and labour for production and sales (Khaldun and Muda 2014).

Requirement [b]

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

10BUSINESS FINANCE

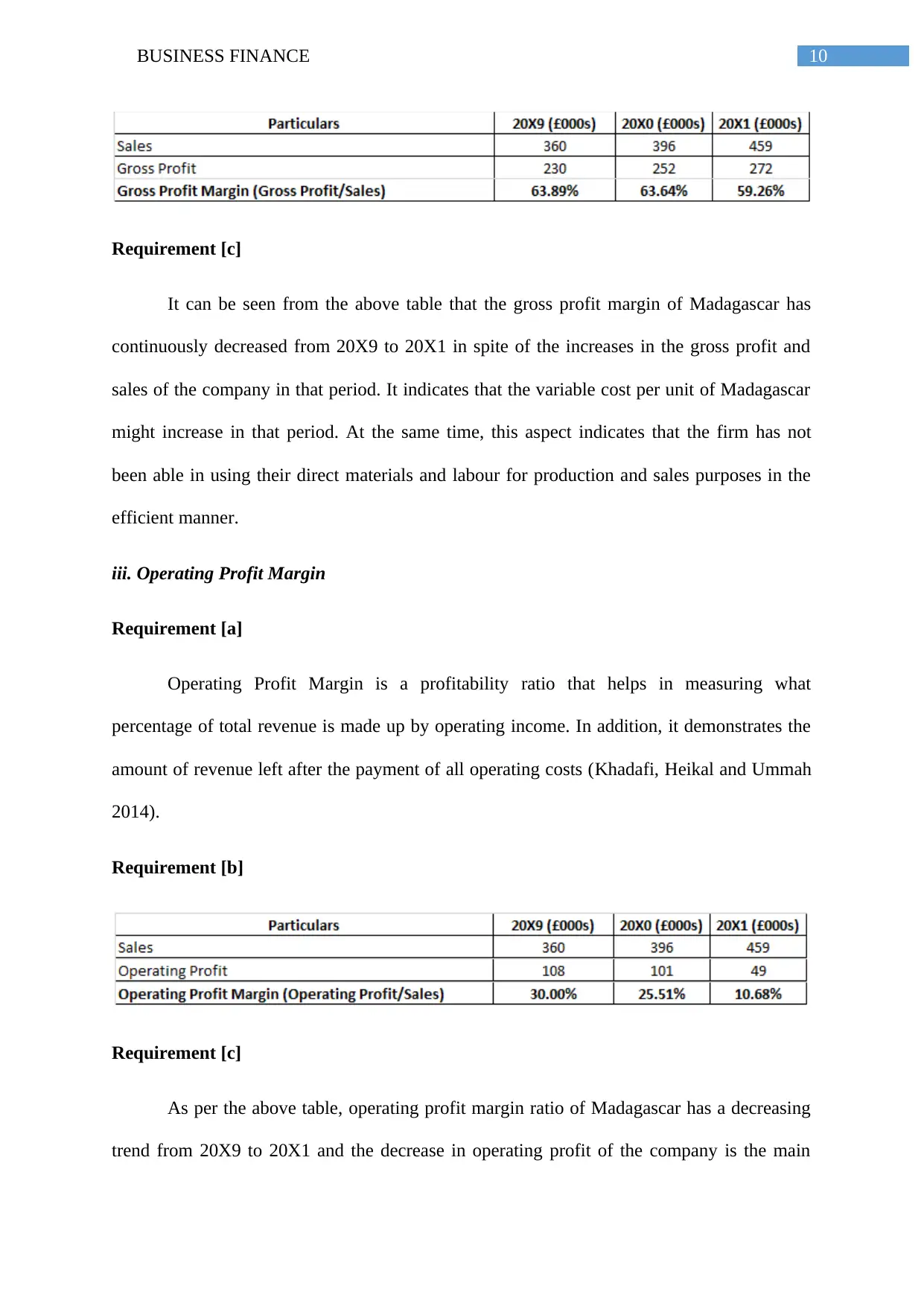

Requirement [c]

It can be seen from the above table that the gross profit margin of Madagascar has

continuously decreased from 20X9 to 20X1 in spite of the increases in the gross profit and

sales of the company in that period. It indicates that the variable cost per unit of Madagascar

might increase in that period. At the same time, this aspect indicates that the firm has not

been able in using their direct materials and labour for production and sales purposes in the

efficient manner.

iii. Operating Profit Margin

Requirement [a]

Operating Profit Margin is a profitability ratio that helps in measuring what

percentage of total revenue is made up by operating income. In addition, it demonstrates the

amount of revenue left after the payment of all operating costs (Khadafi, Heikal and Ummah

2014).

Requirement [b]

Requirement [c]

As per the above table, operating profit margin ratio of Madagascar has a decreasing

trend from 20X9 to 20X1 and the decrease in operating profit of the company is the main

Requirement [c]

It can be seen from the above table that the gross profit margin of Madagascar has

continuously decreased from 20X9 to 20X1 in spite of the increases in the gross profit and

sales of the company in that period. It indicates that the variable cost per unit of Madagascar

might increase in that period. At the same time, this aspect indicates that the firm has not

been able in using their direct materials and labour for production and sales purposes in the

efficient manner.

iii. Operating Profit Margin

Requirement [a]

Operating Profit Margin is a profitability ratio that helps in measuring what

percentage of total revenue is made up by operating income. In addition, it demonstrates the

amount of revenue left after the payment of all operating costs (Khadafi, Heikal and Ummah

2014).

Requirement [b]

Requirement [c]

As per the above table, operating profit margin ratio of Madagascar has a decreasing

trend from 20X9 to 20X1 and the decrease in operating profit of the company is the main

11BUSINESS FINANCE

reason for this decrease. As per the provided information, other key reasons for the decrease

in this ratio are the increase in both the operating expenses and depreciation expenses in that

time span. All these aspects have together affected this ration of Madagascar.

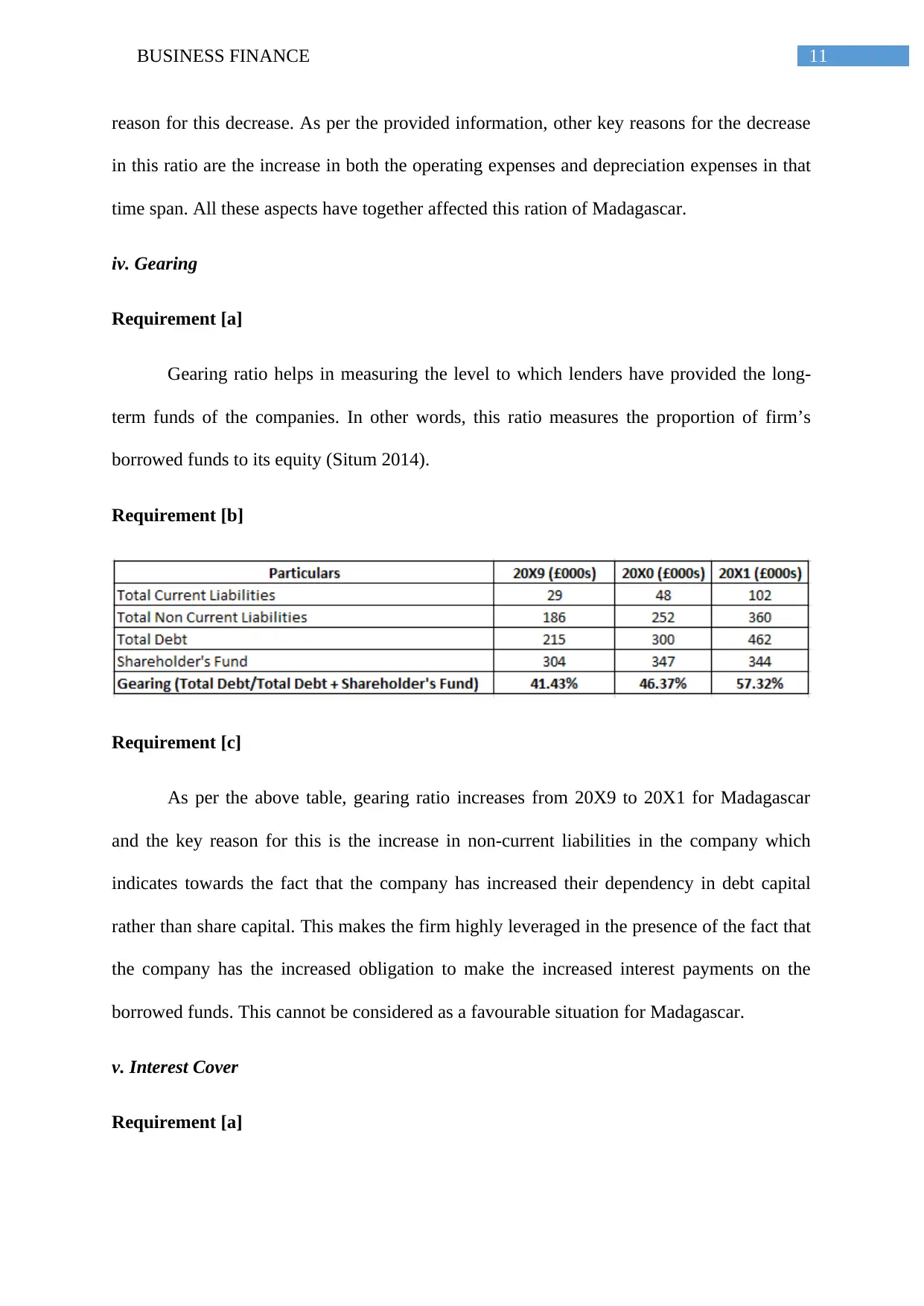

iv. Gearing

Requirement [a]

Gearing ratio helps in measuring the level to which lenders have provided the long-

term funds of the companies. In other words, this ratio measures the proportion of firm’s

borrowed funds to its equity (Situm 2014).

Requirement [b]

Requirement [c]

As per the above table, gearing ratio increases from 20X9 to 20X1 for Madagascar

and the key reason for this is the increase in non-current liabilities in the company which

indicates towards the fact that the company has increased their dependency in debt capital

rather than share capital. This makes the firm highly leveraged in the presence of the fact that

the company has the increased obligation to make the increased interest payments on the

borrowed funds. This cannot be considered as a favourable situation for Madagascar.

v. Interest Cover

Requirement [a]

reason for this decrease. As per the provided information, other key reasons for the decrease

in this ratio are the increase in both the operating expenses and depreciation expenses in that

time span. All these aspects have together affected this ration of Madagascar.

iv. Gearing

Requirement [a]

Gearing ratio helps in measuring the level to which lenders have provided the long-

term funds of the companies. In other words, this ratio measures the proportion of firm’s

borrowed funds to its equity (Situm 2014).

Requirement [b]

Requirement [c]

As per the above table, gearing ratio increases from 20X9 to 20X1 for Madagascar

and the key reason for this is the increase in non-current liabilities in the company which

indicates towards the fact that the company has increased their dependency in debt capital

rather than share capital. This makes the firm highly leveraged in the presence of the fact that

the company has the increased obligation to make the increased interest payments on the

borrowed funds. This cannot be considered as a favourable situation for Madagascar.

v. Interest Cover

Requirement [a]

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 19

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.