Managing Operations and Finance: A Comprehensive Report

VerifiedAdded on 2023/01/19

|15

|3561

|76

Report

AI Summary

This report delves into the critical aspects of managing operations and finance, starting with an introduction to management accounting and its role in business decision-making, contrasting it with financial accounting. It explores investment appraisal techniques, including Net Present Value (NPV), Payback Period, and Internal Rate of Return (IRR), to evaluate project viability, using Cucumber Limited as a case study. The report then emphasizes the significance of business plans and budgeting in guiding operations and controlling costs. Furthermore, it discusses the balanced scorecard method for performance evaluation. The report provides insights into strategic decision-making, cost control, and financial planning, offering a comprehensive overview of key concepts in operations and finance management.

Managing Operations and Finance

1

1

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Contents

Introduction...........................................................................................................................................3

Role of Management Accounting and difference with financial accounting..........................................4

Investment appraisal..............................................................................................................................7

Importance of business plan and budgeting.........................................................................................10

Balanced scorecard method.................................................................................................................12

Conclusion...........................................................................................................................................14

References...........................................................................................................................................15

2

Introduction...........................................................................................................................................3

Role of Management Accounting and difference with financial accounting..........................................4

Investment appraisal..............................................................................................................................7

Importance of business plan and budgeting.........................................................................................10

Balanced scorecard method.................................................................................................................12

Conclusion...........................................................................................................................................14

References...........................................................................................................................................15

2

Introduction

Management Accounting has become a very essential part of business management and

business organizations are giving Management Accounting equal importance as financial

accounting. Management Accounting helps in improving the internet performance of the

company by evaluating the data collected with the help of financial accounting. Therefore it

can be said that the success of a business organization is dependent on effective and efficient

financial as well as management accounting (Otley, 2016). This report will identify some of

the basic differences between financial accounting and Management Accounting along with

the importance of Management Accounting in a business organization. This report will also

use project appraisal techniques for selection of a particular project on the basis of its

financial viability. At last usefulness of the balanced scorecard, the method will be discussed.

3

Management Accounting has become a very essential part of business management and

business organizations are giving Management Accounting equal importance as financial

accounting. Management Accounting helps in improving the internet performance of the

company by evaluating the data collected with the help of financial accounting. Therefore it

can be said that the success of a business organization is dependent on effective and efficient

financial as well as management accounting (Otley, 2016). This report will identify some of

the basic differences between financial accounting and Management Accounting along with

the importance of Management Accounting in a business organization. This report will also

use project appraisal techniques for selection of a particular project on the basis of its

financial viability. At last usefulness of the balanced scorecard, the method will be discussed.

3

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Role of Management Accounting and difference with financial accounting

Management Accounting has become a very essential part of business management as it

helps business managers to take important business decisions. Data collected by business

managers through financial accounting is taken as primary data in Management Accounting.

Information provided by managerial Accountants helps in the development of long term as

well as short term business strategies (Weygandt, Kimmel and Kieso, 2015). Importance of

Managerial Accounting in business can be explained with the help of the following factors-

Productivity and profitability of a product- management of the company can easily

identify the profitability and productivity of a product with the help of financial statement

analysis which is a part of managerial accounting. Management uses trend analysis of

historical data for evaluating whether a particular product is profitable or not. Decisions in

relation to expansion or shutdown can be taken with the help of managerial accounting.

Purchase for manufacturing decision- Decisions in relation to production or purchase of

raw material is also important to maintain effective balance in the cost structure (Appelbaum

et.al, 2017). With the help of managerial accounting, the various factors can be considered by

business managers before taking such decisions in the interest of the company.

Managerial decision making- Managerial accounting please very important role in the

decision-making process of managers. Different Tools and techniques of managerial

accounting such as budgeting, cost analysis, break-even analysis, etc. are used by managers

or before evaluating any business decision.

On the basis of these factors, it can be said that the importance of managerial accounting is

equal to financial accounting if not more.

Difference between financial accounting and managerial accounting

Managerial accounting Financial accounting

Reports generated with the help of

managerial accounting are used for internal

purpose only.

Managers are required to prepare reports in

financial accounting that will be shown to

every stakeholder in the organization

(Narayanaswamy, 2017).

There are no specific rules and regulations

governing Management Accounting in

Specific rules and regulations such as

financial accounting standards and financial

4

Management Accounting has become a very essential part of business management as it

helps business managers to take important business decisions. Data collected by business

managers through financial accounting is taken as primary data in Management Accounting.

Information provided by managerial Accountants helps in the development of long term as

well as short term business strategies (Weygandt, Kimmel and Kieso, 2015). Importance of

Managerial Accounting in business can be explained with the help of the following factors-

Productivity and profitability of a product- management of the company can easily

identify the profitability and productivity of a product with the help of financial statement

analysis which is a part of managerial accounting. Management uses trend analysis of

historical data for evaluating whether a particular product is profitable or not. Decisions in

relation to expansion or shutdown can be taken with the help of managerial accounting.

Purchase for manufacturing decision- Decisions in relation to production or purchase of

raw material is also important to maintain effective balance in the cost structure (Appelbaum

et.al, 2017). With the help of managerial accounting, the various factors can be considered by

business managers before taking such decisions in the interest of the company.

Managerial decision making- Managerial accounting please very important role in the

decision-making process of managers. Different Tools and techniques of managerial

accounting such as budgeting, cost analysis, break-even analysis, etc. are used by managers

or before evaluating any business decision.

On the basis of these factors, it can be said that the importance of managerial accounting is

equal to financial accounting if not more.

Difference between financial accounting and managerial accounting

Managerial accounting Financial accounting

Reports generated with the help of

managerial accounting are used for internal

purpose only.

Managers are required to prepare reports in

financial accounting that will be shown to

every stakeholder in the organization

(Narayanaswamy, 2017).

There are no specific rules and regulations

governing Management Accounting in

Specific rules and regulations such as

financial accounting standards and financial

4

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

business operations. reporting framework are developed by

different account inequalities for the

regulation of financial accounting.

Different measurement units are used in

Management Accounting surcharge time

and units (Khalil and Simon, 2015).

Financial accounting uses only one

measurement unit i.e. amount.

Reports in managerial accounting are

developed for a specific purpose.

These are also called as general purpose

reports.

Different models of costing

Absorption costing- In this type of Costing allocation in cost is done on the basis of variable

cost and fixed cost. Therefore it can be said that in absorption costing both fixed cost and

variable cost to production are absorbed.

Marginal costing- major focus in this type of costing is on different elements of variable cost

such as direct material, direct labour, direct overhead cost, etc. print cost is not included in

this costing as such cost will incur irrespective of the business operations (Warren Jr, Moffitt

and Byrnes, 2015).

Activity-based costing- This type of cost method is used in a business organization that

undertaking a different kind of activities for the production of product and services. Division

of production cost is undertaken on the basis of different activities.

Job costing- This type of costing method is used when the characteristics of each job are

dependent on the requirement of customers. For example, production cost allocation in

customizable product and services will be done with the help of job costing.

Process costing- This type of post method is used in a business organization that is

conducting to manufacturing process on the basis of the process. Each and every process is

classified in different departments (Cooper, 2017). Direct never material and overhead cost is

allocated on a particular product on the basis of activity undertaken by a particular

department.

5

different account inequalities for the

regulation of financial accounting.

Different measurement units are used in

Management Accounting surcharge time

and units (Khalil and Simon, 2015).

Financial accounting uses only one

measurement unit i.e. amount.

Reports in managerial accounting are

developed for a specific purpose.

These are also called as general purpose

reports.

Different models of costing

Absorption costing- In this type of Costing allocation in cost is done on the basis of variable

cost and fixed cost. Therefore it can be said that in absorption costing both fixed cost and

variable cost to production are absorbed.

Marginal costing- major focus in this type of costing is on different elements of variable cost

such as direct material, direct labour, direct overhead cost, etc. print cost is not included in

this costing as such cost will incur irrespective of the business operations (Warren Jr, Moffitt

and Byrnes, 2015).

Activity-based costing- This type of cost method is used in a business organization that

undertaking a different kind of activities for the production of product and services. Division

of production cost is undertaken on the basis of different activities.

Job costing- This type of costing method is used when the characteristics of each job are

dependent on the requirement of customers. For example, production cost allocation in

customizable product and services will be done with the help of job costing.

Process costing- This type of post method is used in a business organization that is

conducting to manufacturing process on the basis of the process. Each and every process is

classified in different departments (Cooper, 2017). Direct never material and overhead cost is

allocated on a particular product on the basis of activity undertaken by a particular

department.

5

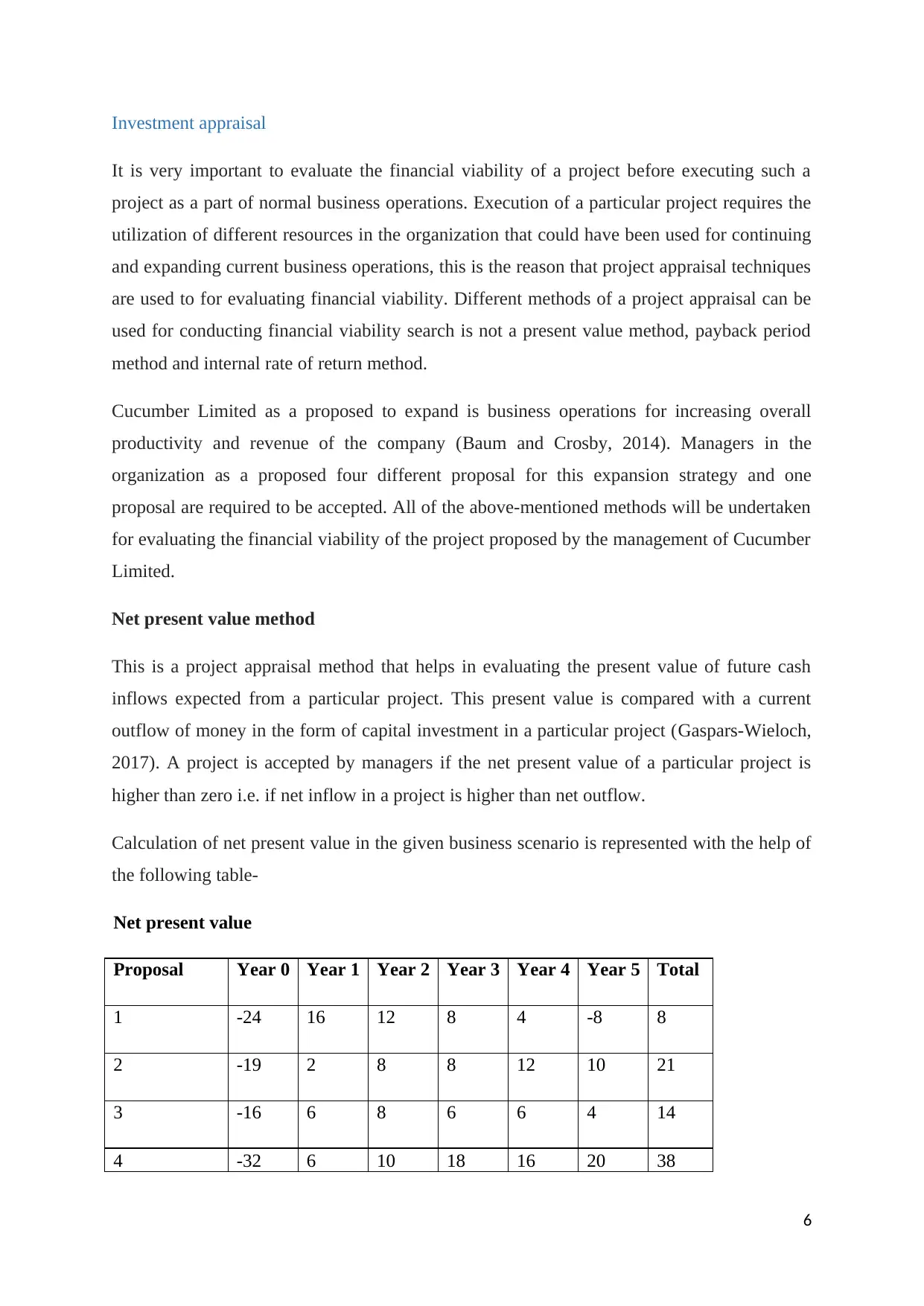

Investment appraisal

It is very important to evaluate the financial viability of a project before executing such a

project as a part of normal business operations. Execution of a particular project requires the

utilization of different resources in the organization that could have been used for continuing

and expanding current business operations, this is the reason that project appraisal techniques

are used to for evaluating financial viability. Different methods of a project appraisal can be

used for conducting financial viability search is not a present value method, payback period

method and internal rate of return method.

Cucumber Limited as a proposed to expand is business operations for increasing overall

productivity and revenue of the company (Baum and Crosby, 2014). Managers in the

organization as a proposed four different proposal for this expansion strategy and one

proposal are required to be accepted. All of the above-mentioned methods will be undertaken

for evaluating the financial viability of the project proposed by the management of Cucumber

Limited.

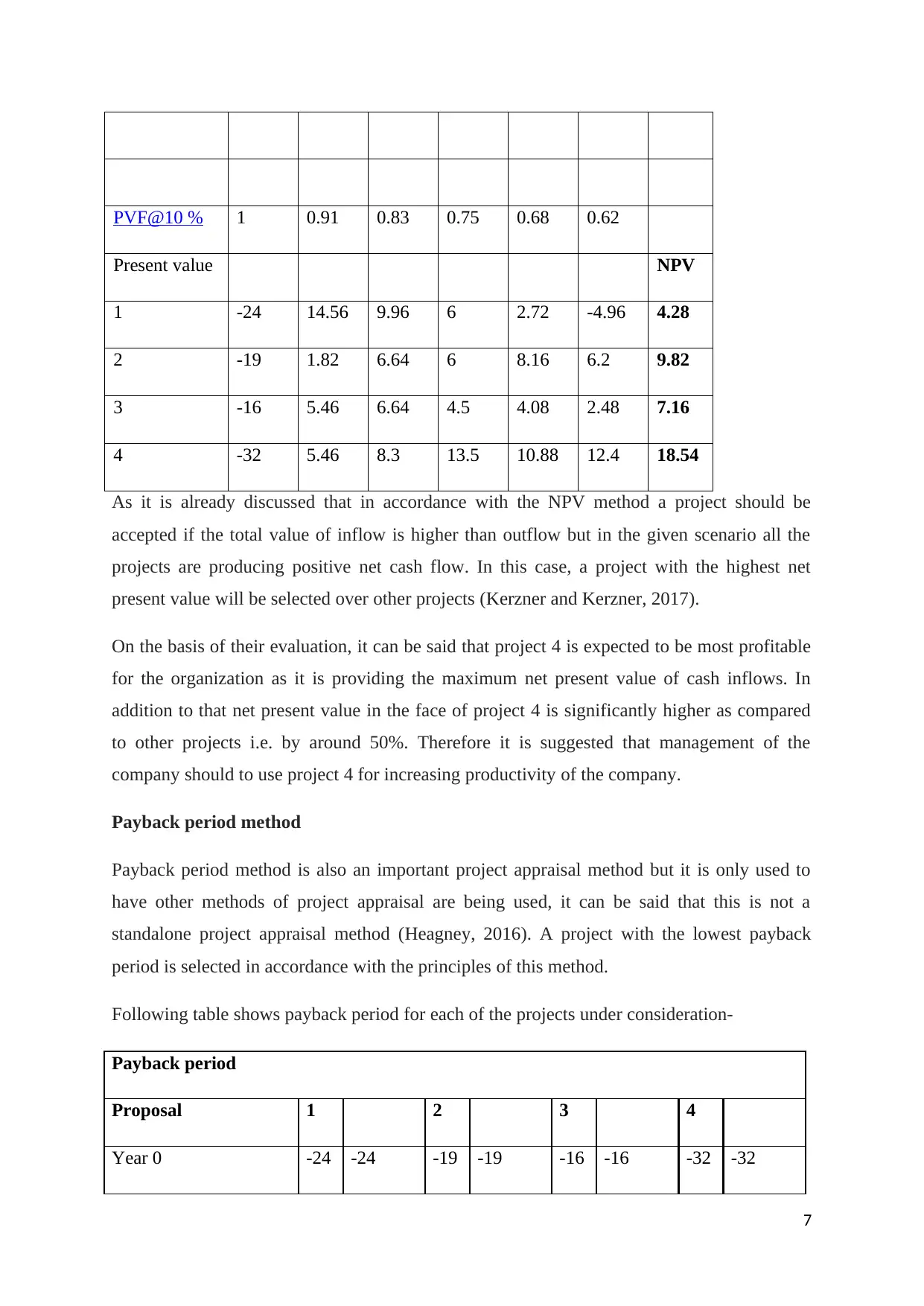

Net present value method

This is a project appraisal method that helps in evaluating the present value of future cash

inflows expected from a particular project. This present value is compared with a current

outflow of money in the form of capital investment in a particular project (Gaspars-Wieloch,

2017). A project is accepted by managers if the net present value of a particular project is

higher than zero i.e. if net inflow in a project is higher than net outflow.

Calculation of net present value in the given business scenario is represented with the help of

the following table-

Net present value

Proposal Year 0 Year 1 Year 2 Year 3 Year 4 Year 5 Total

1 -24 16 12 8 4 -8 8

2 -19 2 8 8 12 10 21

3 -16 6 8 6 6 4 14

4 -32 6 10 18 16 20 38

6

It is very important to evaluate the financial viability of a project before executing such a

project as a part of normal business operations. Execution of a particular project requires the

utilization of different resources in the organization that could have been used for continuing

and expanding current business operations, this is the reason that project appraisal techniques

are used to for evaluating financial viability. Different methods of a project appraisal can be

used for conducting financial viability search is not a present value method, payback period

method and internal rate of return method.

Cucumber Limited as a proposed to expand is business operations for increasing overall

productivity and revenue of the company (Baum and Crosby, 2014). Managers in the

organization as a proposed four different proposal for this expansion strategy and one

proposal are required to be accepted. All of the above-mentioned methods will be undertaken

for evaluating the financial viability of the project proposed by the management of Cucumber

Limited.

Net present value method

This is a project appraisal method that helps in evaluating the present value of future cash

inflows expected from a particular project. This present value is compared with a current

outflow of money in the form of capital investment in a particular project (Gaspars-Wieloch,

2017). A project is accepted by managers if the net present value of a particular project is

higher than zero i.e. if net inflow in a project is higher than net outflow.

Calculation of net present value in the given business scenario is represented with the help of

the following table-

Net present value

Proposal Year 0 Year 1 Year 2 Year 3 Year 4 Year 5 Total

1 -24 16 12 8 4 -8 8

2 -19 2 8 8 12 10 21

3 -16 6 8 6 6 4 14

4 -32 6 10 18 16 20 38

6

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

PVF@10 % 1 0.91 0.83 0.75 0.68 0.62

Present value NPV

1 -24 14.56 9.96 6 2.72 -4.96 4.28

2 -19 1.82 6.64 6 8.16 6.2 9.82

3 -16 5.46 6.64 4.5 4.08 2.48 7.16

4 -32 5.46 8.3 13.5 10.88 12.4 18.54

As it is already discussed that in accordance with the NPV method a project should be

accepted if the total value of inflow is higher than outflow but in the given scenario all the

projects are producing positive net cash flow. In this case, a project with the highest net

present value will be selected over other projects (Kerzner and Kerzner, 2017).

On the basis of their evaluation, it can be said that project 4 is expected to be most profitable

for the organization as it is providing the maximum net present value of cash inflows. In

addition to that net present value in the face of project 4 is significantly higher as compared

to other projects i.e. by around 50%. Therefore it is suggested that management of the

company should to use project 4 for increasing productivity of the company.

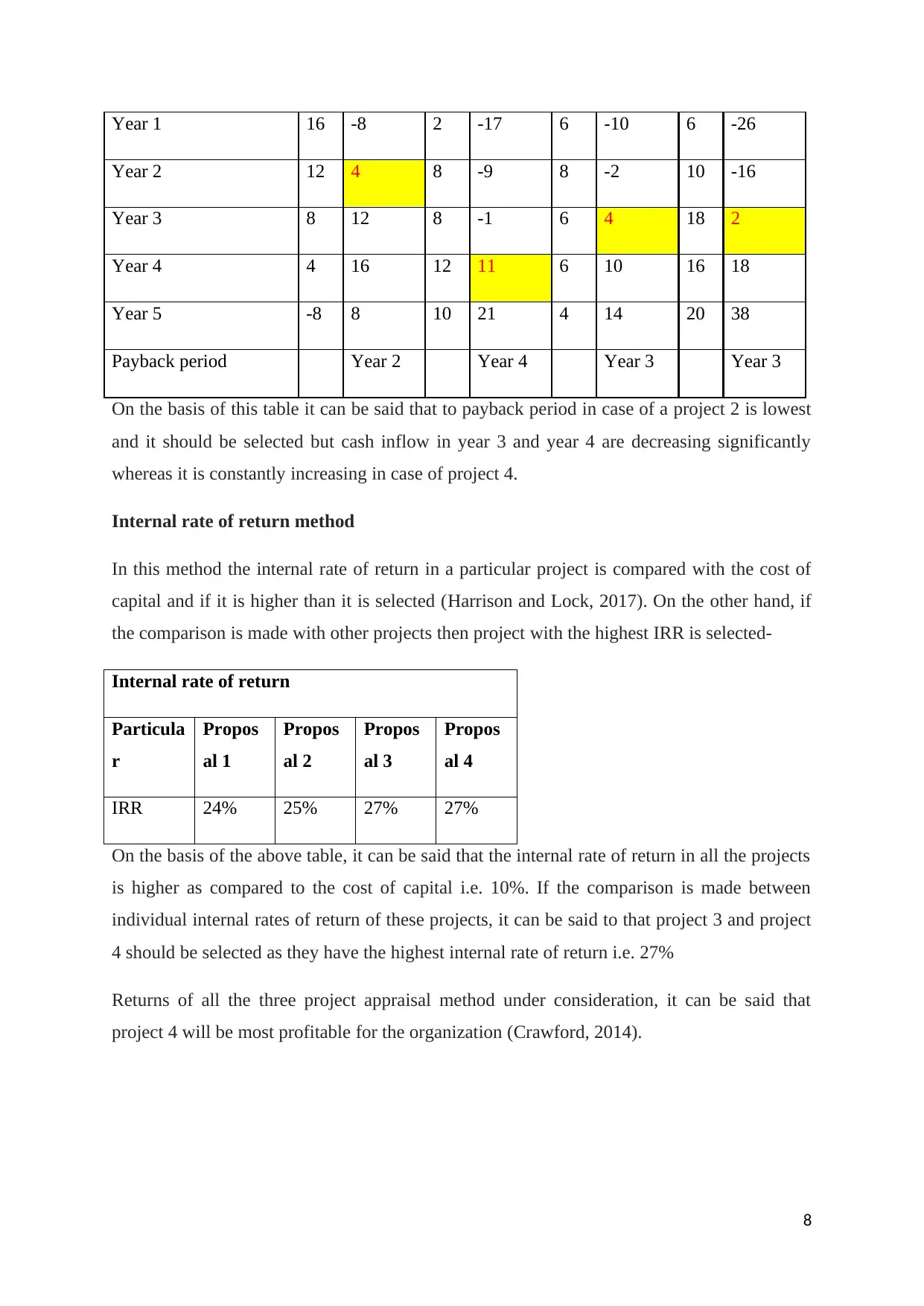

Payback period method

Payback period method is also an important project appraisal method but it is only used to

have other methods of project appraisal are being used, it can be said that this is not a

standalone project appraisal method (Heagney, 2016). A project with the lowest payback

period is selected in accordance with the principles of this method.

Following table shows payback period for each of the projects under consideration-

Payback period

Proposal 1 2 3 4

Year 0 -24 -24 -19 -19 -16 -16 -32 -32

7

Present value NPV

1 -24 14.56 9.96 6 2.72 -4.96 4.28

2 -19 1.82 6.64 6 8.16 6.2 9.82

3 -16 5.46 6.64 4.5 4.08 2.48 7.16

4 -32 5.46 8.3 13.5 10.88 12.4 18.54

As it is already discussed that in accordance with the NPV method a project should be

accepted if the total value of inflow is higher than outflow but in the given scenario all the

projects are producing positive net cash flow. In this case, a project with the highest net

present value will be selected over other projects (Kerzner and Kerzner, 2017).

On the basis of their evaluation, it can be said that project 4 is expected to be most profitable

for the organization as it is providing the maximum net present value of cash inflows. In

addition to that net present value in the face of project 4 is significantly higher as compared

to other projects i.e. by around 50%. Therefore it is suggested that management of the

company should to use project 4 for increasing productivity of the company.

Payback period method

Payback period method is also an important project appraisal method but it is only used to

have other methods of project appraisal are being used, it can be said that this is not a

standalone project appraisal method (Heagney, 2016). A project with the lowest payback

period is selected in accordance with the principles of this method.

Following table shows payback period for each of the projects under consideration-

Payback period

Proposal 1 2 3 4

Year 0 -24 -24 -19 -19 -16 -16 -32 -32

7

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Year 1 16 -8 2 -17 6 -10 6 -26

Year 2 12 4 8 -9 8 -2 10 -16

Year 3 8 12 8 -1 6 4 18 2

Year 4 4 16 12 11 6 10 16 18

Year 5 -8 8 10 21 4 14 20 38

Payback period Year 2 Year 4 Year 3 Year 3

On the basis of this table it can be said that to payback period in case of a project 2 is lowest

and it should be selected but cash inflow in year 3 and year 4 are decreasing significantly

whereas it is constantly increasing in case of project 4.

Internal rate of return method

In this method the internal rate of return in a particular project is compared with the cost of

capital and if it is higher than it is selected (Harrison and Lock, 2017). On the other hand, if

the comparison is made with other projects then project with the highest IRR is selected-

Internal rate of return

Particula

r

Propos

al 1

Propos

al 2

Propos

al 3

Propos

al 4

IRR 24% 25% 27% 27%

On the basis of the above table, it can be said that the internal rate of return in all the projects

is higher as compared to the cost of capital i.e. 10%. If the comparison is made between

individual internal rates of return of these projects, it can be said to that project 3 and project

4 should be selected as they have the highest internal rate of return i.e. 27%

Returns of all the three project appraisal method under consideration, it can be said that

project 4 will be most profitable for the organization (Crawford, 2014).

8

Year 2 12 4 8 -9 8 -2 10 -16

Year 3 8 12 8 -1 6 4 18 2

Year 4 4 16 12 11 6 10 16 18

Year 5 -8 8 10 21 4 14 20 38

Payback period Year 2 Year 4 Year 3 Year 3

On the basis of this table it can be said that to payback period in case of a project 2 is lowest

and it should be selected but cash inflow in year 3 and year 4 are decreasing significantly

whereas it is constantly increasing in case of project 4.

Internal rate of return method

In this method the internal rate of return in a particular project is compared with the cost of

capital and if it is higher than it is selected (Harrison and Lock, 2017). On the other hand, if

the comparison is made with other projects then project with the highest IRR is selected-

Internal rate of return

Particula

r

Propos

al 1

Propos

al 2

Propos

al 3

Propos

al 4

IRR 24% 25% 27% 27%

On the basis of the above table, it can be said that the internal rate of return in all the projects

is higher as compared to the cost of capital i.e. 10%. If the comparison is made between

individual internal rates of return of these projects, it can be said to that project 3 and project

4 should be selected as they have the highest internal rate of return i.e. 27%

Returns of all the three project appraisal method under consideration, it can be said that

project 4 will be most profitable for the organization (Crawford, 2014).

8

Importance of business plan and budgeting

Business plan- Businessman can be defined as the summary of different business activities

and related aspect of business operations that are required to be completed in a particular

business organization. Preparation of a business plan is very important as it helps in

providing a certain direction to business operations. Management of the company would be

able to achieve its goals and objective with the help of business planning (DaSilva and

Trkman, 2014). Roles and responsibility to different experts available in the organization can

also be assigned so that effective and full potential of resources can be achieved. Cost

estimation can also be made by Business managers with the help of the business plan so that

cost-efficient sources of finance can be arranged for daily as well as long term operations.

Budgeting- Use of budgeting in business operations has increased over the period of time due

to its various advantages. Budgetary control is a very critical cost controlling strategy used by

Business organizations to manage their cost in accordance with their cost structure. Overall

profitability margins can be increased by reducing the cost with the help of budgeting. The

target can be provided to separate departments with the help of the budgeting process so that

an appropriate direction can be provided to departmental operations (Cardoş, 2014). With the

help of budgeting, management can allocate higher resources to critical business operation to

achieve maximum profitability and resource utilization.

Report to management

To General Manager,

Cucumber Limited

Following are some of the strategic decisions that are required to be taken in Cucumber

Limited for improving productivity and profitability-

Budgetary control- It is important for every business manager to understand the concept and

advantages of budgetary control in order to control the overall cost of production as well as

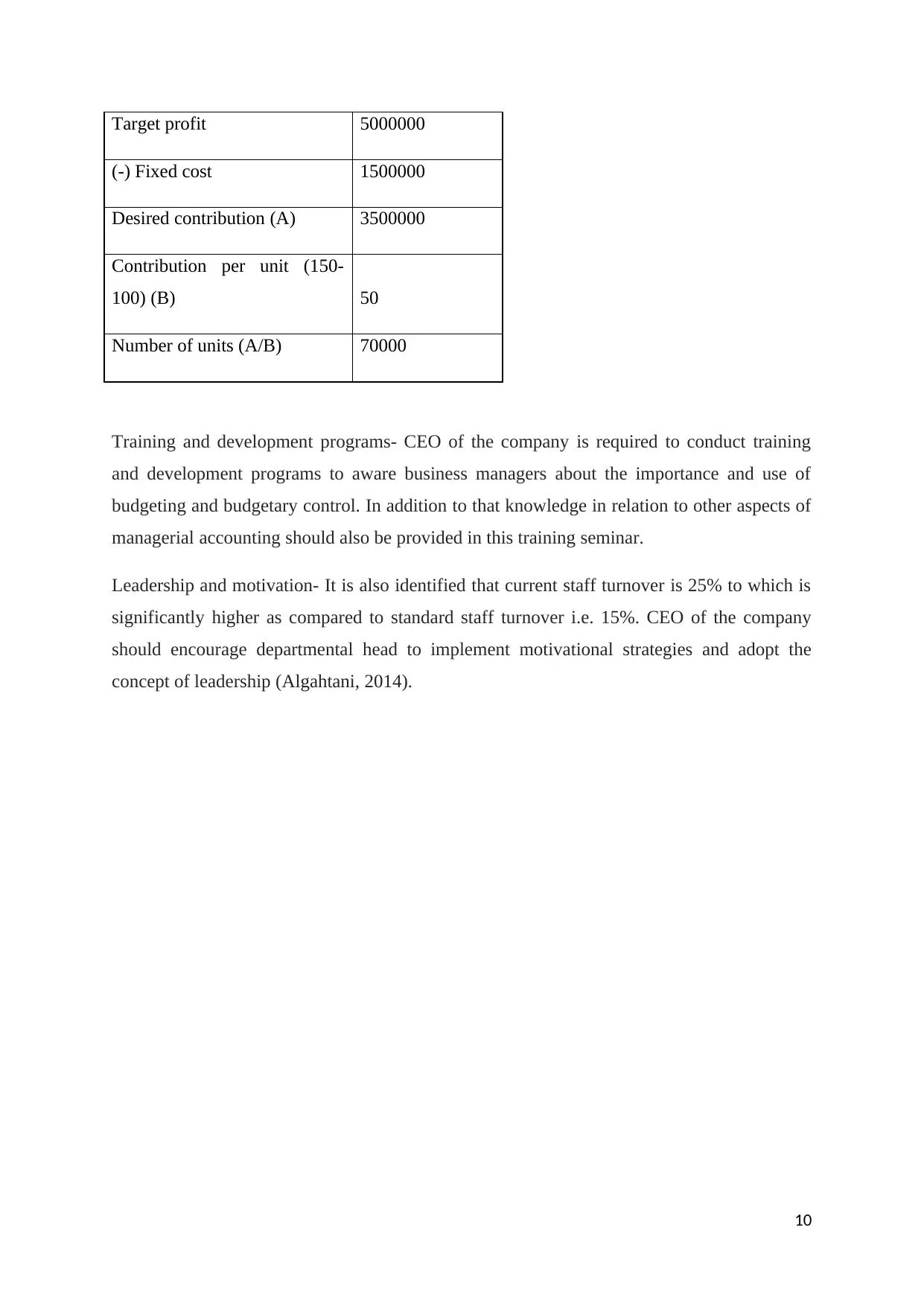

an indirect cost (Gitman, Juchau and Flanagan, 2015). Number of units that will be required

to achieve a target profit of 5 million per annum will be as follows-

Particular

Amount($)/

Units

9

Business plan- Businessman can be defined as the summary of different business activities

and related aspect of business operations that are required to be completed in a particular

business organization. Preparation of a business plan is very important as it helps in

providing a certain direction to business operations. Management of the company would be

able to achieve its goals and objective with the help of business planning (DaSilva and

Trkman, 2014). Roles and responsibility to different experts available in the organization can

also be assigned so that effective and full potential of resources can be achieved. Cost

estimation can also be made by Business managers with the help of the business plan so that

cost-efficient sources of finance can be arranged for daily as well as long term operations.

Budgeting- Use of budgeting in business operations has increased over the period of time due

to its various advantages. Budgetary control is a very critical cost controlling strategy used by

Business organizations to manage their cost in accordance with their cost structure. Overall

profitability margins can be increased by reducing the cost with the help of budgeting. The

target can be provided to separate departments with the help of the budgeting process so that

an appropriate direction can be provided to departmental operations (Cardoş, 2014). With the

help of budgeting, management can allocate higher resources to critical business operation to

achieve maximum profitability and resource utilization.

Report to management

To General Manager,

Cucumber Limited

Following are some of the strategic decisions that are required to be taken in Cucumber

Limited for improving productivity and profitability-

Budgetary control- It is important for every business manager to understand the concept and

advantages of budgetary control in order to control the overall cost of production as well as

an indirect cost (Gitman, Juchau and Flanagan, 2015). Number of units that will be required

to achieve a target profit of 5 million per annum will be as follows-

Particular

Amount($)/

Units

9

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Target profit 5000000

(-) Fixed cost 1500000

Desired contribution (A) 3500000

Contribution per unit (150-

100) (B) 50

Number of units (A/B) 70000

Training and development programs- CEO of the company is required to conduct training

and development programs to aware business managers about the importance and use of

budgeting and budgetary control. In addition to that knowledge in relation to other aspects of

managerial accounting should also be provided in this training seminar.

Leadership and motivation- It is also identified that current staff turnover is 25% to which is

significantly higher as compared to standard staff turnover i.e. 15%. CEO of the company

should encourage departmental head to implement motivational strategies and adopt the

concept of leadership (Algahtani, 2014).

10

(-) Fixed cost 1500000

Desired contribution (A) 3500000

Contribution per unit (150-

100) (B) 50

Number of units (A/B) 70000

Training and development programs- CEO of the company is required to conduct training

and development programs to aware business managers about the importance and use of

budgeting and budgetary control. In addition to that knowledge in relation to other aspects of

managerial accounting should also be provided in this training seminar.

Leadership and motivation- It is also identified that current staff turnover is 25% to which is

significantly higher as compared to standard staff turnover i.e. 15%. CEO of the company

should encourage departmental head to implement motivational strategies and adopt the

concept of leadership (Algahtani, 2014).

10

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Balanced scorecard method

Balanced scorecard methodology can be described as a performance metric that is used for

evaluating different aspects of the business. Various internal functioning in a business

organization can be improved with the help of the balanced scorecard method. Primary

advantages of using balanced scorecard method as follows-

Balanced scorecard method helps in the overall analysis of the internal performance of

the company which is very essential for making strategic decisions and improving the

current situation of the company. Currently, there are various internal issues in the

management of Cucumber Limited, balanced scorecard method can be very useful in this

scenario (Niven, 2014).

Balanced scorecard method is primarily useful in strategic management of the company

and one of the primary issues identified in case of cucumber Limited is strategic

management as business managers do not have sufficient knowledge about budgetary

control and other managerial accounting tools and techniques.

Balanced scorecard method helps in integration of long term goals and objectives into

daily operations of the company.

This methodology helps in providing a performance evaluation Framework who business

operations that can be helpful in aligning business operations in accordance with vision

and mission.

The financial health of an organization can be identified with the help of key performance

indicators provided in the balanced scorecard methodology framework (Mehralian et.al,

2017). Performance evaluation of different resources can be conducted with the help of a

balanced scorecard method which will be helpful in the identification of operational and

management issues.

Balanced scorecard for Cucumber Limited

Following are the factors that should be considered for performance evaluation in accordance

with balance for card developed for cucumber Limited. These factors can also be considered

as key performance indicators-

Financial

11

Balanced scorecard methodology can be described as a performance metric that is used for

evaluating different aspects of the business. Various internal functioning in a business

organization can be improved with the help of the balanced scorecard method. Primary

advantages of using balanced scorecard method as follows-

Balanced scorecard method helps in the overall analysis of the internal performance of

the company which is very essential for making strategic decisions and improving the

current situation of the company. Currently, there are various internal issues in the

management of Cucumber Limited, balanced scorecard method can be very useful in this

scenario (Niven, 2014).

Balanced scorecard method is primarily useful in strategic management of the company

and one of the primary issues identified in case of cucumber Limited is strategic

management as business managers do not have sufficient knowledge about budgetary

control and other managerial accounting tools and techniques.

Balanced scorecard method helps in integration of long term goals and objectives into

daily operations of the company.

This methodology helps in providing a performance evaluation Framework who business

operations that can be helpful in aligning business operations in accordance with vision

and mission.

The financial health of an organization can be identified with the help of key performance

indicators provided in the balanced scorecard methodology framework (Mehralian et.al,

2017). Performance evaluation of different resources can be conducted with the help of a

balanced scorecard method which will be helpful in the identification of operational and

management issues.

Balanced scorecard for Cucumber Limited

Following are the factors that should be considered for performance evaluation in accordance

with balance for card developed for cucumber Limited. These factors can also be considered

as key performance indicators-

Financial

11

Increased revenue - overall revenue of the company should be analysed over the period of

time in order to identify whether resources employed by the organization are adding value to

the company or not.

Increased profitability and decreased operating cost- This performance indicator will help in

evaluating the efficiency of Management to control cost with the help of effective budgeting

and budgetary control (Valmohammadi and Ahmadi, 2015). Overall profitability margin such

as gross profit and net profit should be analysed over the period of time.

Customer

Key performance indicator in relation to Customer Management has already prepared by the

organization i.e. "Excellent" customer rating should be at least 80%.

Internal processes

Current management of the company has been identified as a different kind of internal

problems. First key performance indicator should be variance identified in variance analysis

after comparing actual results with budgeted results (Mehralian et.al, 2017). Staff turnover

ratio should be another key performance indicator and it should be reduced from 25 % to

15%.

Organizational capacity

Increase of productivity- Management has proposed to implement a new project for

increasing capacity of the organization. The comparison should be made with actually

increased productivity with target productivity projected by the management.

12

time in order to identify whether resources employed by the organization are adding value to

the company or not.

Increased profitability and decreased operating cost- This performance indicator will help in

evaluating the efficiency of Management to control cost with the help of effective budgeting

and budgetary control (Valmohammadi and Ahmadi, 2015). Overall profitability margin such

as gross profit and net profit should be analysed over the period of time.

Customer

Key performance indicator in relation to Customer Management has already prepared by the

organization i.e. "Excellent" customer rating should be at least 80%.

Internal processes

Current management of the company has been identified as a different kind of internal

problems. First key performance indicator should be variance identified in variance analysis

after comparing actual results with budgeted results (Mehralian et.al, 2017). Staff turnover

ratio should be another key performance indicator and it should be reduced from 25 % to

15%.

Organizational capacity

Increase of productivity- Management has proposed to implement a new project for

increasing capacity of the organization. The comparison should be made with actually

increased productivity with target productivity projected by the management.

12

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 15

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.