Financial Analysis Report: EOQ, Payback, Ratios, and IFRS Framework

VerifiedAdded on 2023/01/03

|15

|3595

|28

Report

AI Summary

This finance report delves into core financial concepts and calculations. It begins with an introduction to finance, followed by the calculation of the Economic Order Quantity (EOQ) and the Total Annual Cost. It then analyzes two investment options using the payback period and accounting rate of return, including a discussion of capital investment decision characteristics. The report also includes a detailed calculation and interpretation of various financial ratios for the year ended March 31, 2019, focusing on profitability, asset usage, and liquidity. Furthermore, it demonstrates the roles of the IFRS foundation, IFRS interpretation committee, and IFRS advisory council within the international regulatory framework for accounting, as well as the role of the audit committee within corporate governance. The report concludes with a summary of key findings and a list of references.

INTRODUCTION TO

FINANCE

FINANCE

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Table of Contents

INTRODUCTION...........................................................................................................................3

MAIN BODY...................................................................................................................................3

Question 1........................................................................................................................................3

a) Calculation of EOQ:-..............................................................................................................3

b) Calculation of Total Annual Cost:-.........................................................................................3

Question 2........................................................................................................................................5

a) Payback Period:-.....................................................................................................................5

b) Accounting rate of return:-.....................................................................................................5

Accounting Rate of Return Technique:-.....................................................................................6

d) Characteristics of capital investment decisions:-....................................................................7

Question .3 ......................................................................................................................................8

Calculation of Ratios for the year ended 31st March, 2019:-.....................................................8

QUESTION 4.................................................................................................................................10

Demonstrates the role of IFRS foundation, IFRS interpretation committee and IFRS advisory

council with international regulatory framework for accounting.............................................10

Demonstrating upon role of the audit committee within the corporate governance. ...............11

CONCLUSION..............................................................................................................................12

REFERENCES..............................................................................................................................13

INTRODUCTION...........................................................................................................................3

MAIN BODY...................................................................................................................................3

Question 1........................................................................................................................................3

a) Calculation of EOQ:-..............................................................................................................3

b) Calculation of Total Annual Cost:-.........................................................................................3

Question 2........................................................................................................................................5

a) Payback Period:-.....................................................................................................................5

b) Accounting rate of return:-.....................................................................................................5

Accounting Rate of Return Technique:-.....................................................................................6

d) Characteristics of capital investment decisions:-....................................................................7

Question .3 ......................................................................................................................................8

Calculation of Ratios for the year ended 31st March, 2019:-.....................................................8

QUESTION 4.................................................................................................................................10

Demonstrates the role of IFRS foundation, IFRS interpretation committee and IFRS advisory

council with international regulatory framework for accounting.............................................10

Demonstrating upon role of the audit committee within the corporate governance. ...............11

CONCLUSION..............................................................................................................................12

REFERENCES..............................................................................................................................13

INTRODUCTION

Finance is considered to be as the term which is is significant to describe the key financial

activities of the business. This study tends to mainly focus on contrasting the key varied set of

different sources of finance within the business. Furthermore, this study also calculates the

economic order quantity and payback period for option A and option B. Furthermore, this study

also critically demonstrate the importance or relevance of the considering audience linked with

the financial statement analysis. The present study demonstrates the role of IFRS foundation,

IFRS interpretation committee and IFRS advisory council with international regulatory

framework for accounting . This study tends to mainly demonstrate upon role of the audit

committee within the corporate governance.

MAIN BODY

Question 1

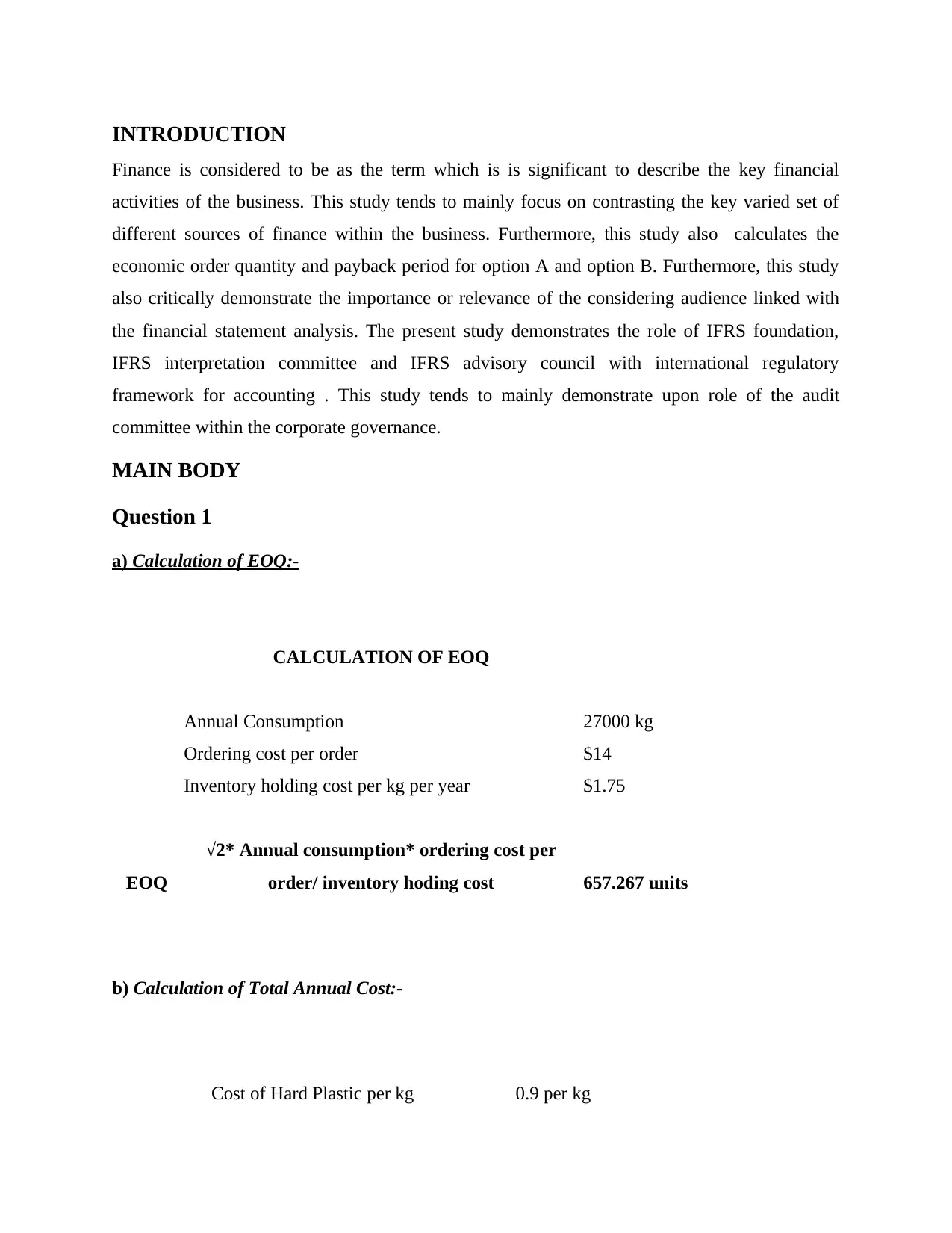

a) Calculation of EOQ:-

CALCULATION OF EOQ

Annual Consumption 27000 kg

Ordering cost per order $14

Inventory holding cost per kg per year $1.75

EOQ

√2* Annual consumption* ordering cost per

order/ inventory hoding cost 657.267 units

b) Calculation of Total Annual Cost:-

Cost of Hard Plastic per kg 0.9 per kg

Finance is considered to be as the term which is is significant to describe the key financial

activities of the business. This study tends to mainly focus on contrasting the key varied set of

different sources of finance within the business. Furthermore, this study also calculates the

economic order quantity and payback period for option A and option B. Furthermore, this study

also critically demonstrate the importance or relevance of the considering audience linked with

the financial statement analysis. The present study demonstrates the role of IFRS foundation,

IFRS interpretation committee and IFRS advisory council with international regulatory

framework for accounting . This study tends to mainly demonstrate upon role of the audit

committee within the corporate governance.

MAIN BODY

Question 1

a) Calculation of EOQ:-

CALCULATION OF EOQ

Annual Consumption 27000 kg

Ordering cost per order $14

Inventory holding cost per kg per year $1.75

EOQ

√2* Annual consumption* ordering cost per

order/ inventory hoding cost 657.267 units

b) Calculation of Total Annual Cost:-

Cost of Hard Plastic per kg 0.9 per kg

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

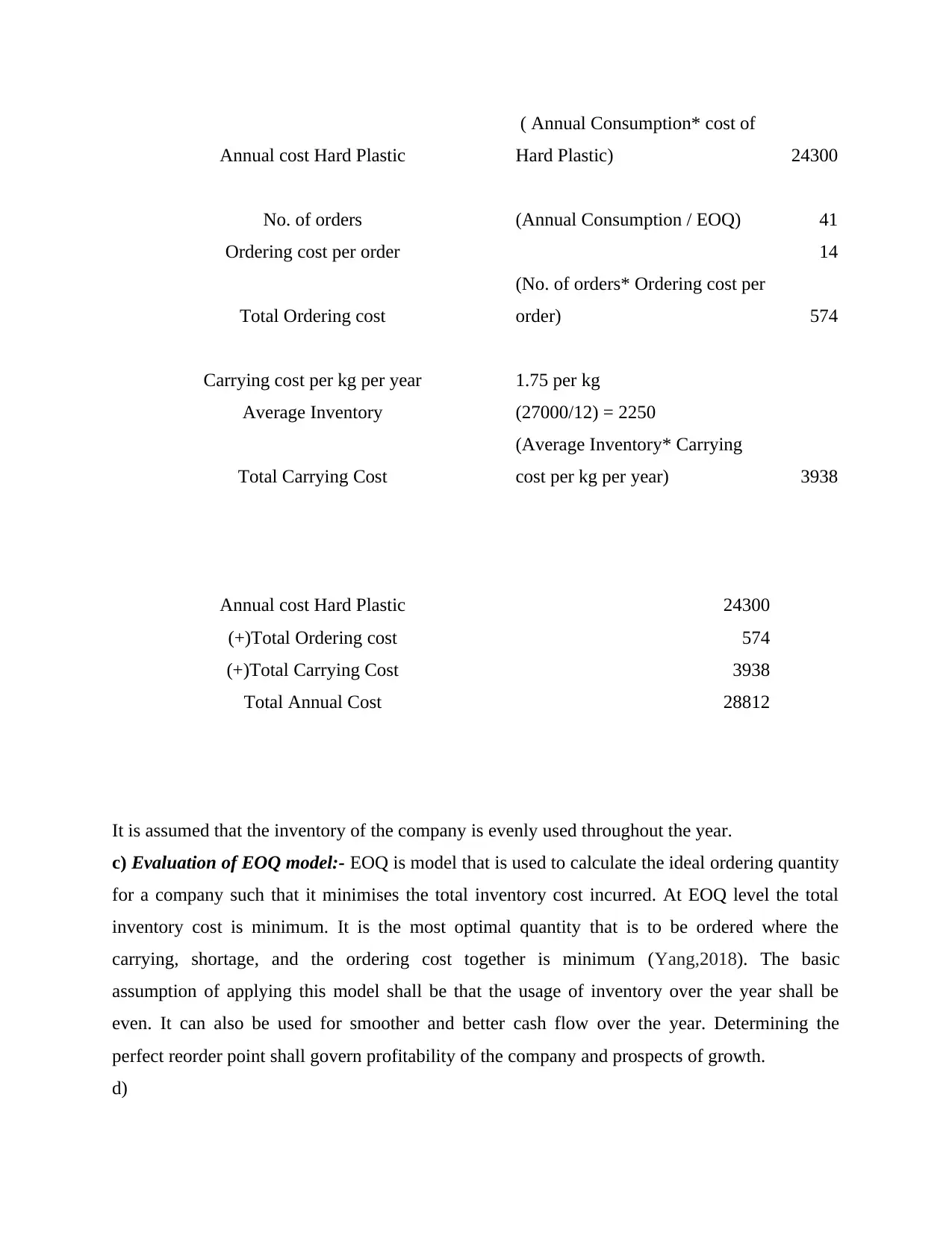

Annual cost Hard Plastic

( Annual Consumption* cost of

Hard Plastic) 24300

No. of orders (Annual Consumption / EOQ) 41

Ordering cost per order 14

Total Ordering cost

(No. of orders* Ordering cost per

order) 574

Carrying cost per kg per year 1.75 per kg

Average Inventory (27000/12) = 2250

Total Carrying Cost

(Average Inventory* Carrying

cost per kg per year) 3938

Annual cost Hard Plastic 24300

(+)Total Ordering cost 574

(+)Total Carrying Cost 3938

Total Annual Cost 28812

It is assumed that the inventory of the company is evenly used throughout the year.

c) Evaluation of EOQ model:- EOQ is model that is used to calculate the ideal ordering quantity

for a company such that it minimises the total inventory cost incurred. At EOQ level the total

inventory cost is minimum. It is the most optimal quantity that is to be ordered where the

carrying, shortage, and the ordering cost together is minimum (Yang,2018). The basic

assumption of applying this model shall be that the usage of inventory over the year shall be

even. It can also be used for smoother and better cash flow over the year. Determining the

perfect reorder point shall govern profitability of the company and prospects of growth.

d)

( Annual Consumption* cost of

Hard Plastic) 24300

No. of orders (Annual Consumption / EOQ) 41

Ordering cost per order 14

Total Ordering cost

(No. of orders* Ordering cost per

order) 574

Carrying cost per kg per year 1.75 per kg

Average Inventory (27000/12) = 2250

Total Carrying Cost

(Average Inventory* Carrying

cost per kg per year) 3938

Annual cost Hard Plastic 24300

(+)Total Ordering cost 574

(+)Total Carrying Cost 3938

Total Annual Cost 28812

It is assumed that the inventory of the company is evenly used throughout the year.

c) Evaluation of EOQ model:- EOQ is model that is used to calculate the ideal ordering quantity

for a company such that it minimises the total inventory cost incurred. At EOQ level the total

inventory cost is minimum. It is the most optimal quantity that is to be ordered where the

carrying, shortage, and the ordering cost together is minimum (Yang,2018). The basic

assumption of applying this model shall be that the usage of inventory over the year shall be

even. It can also be used for smoother and better cash flow over the year. Determining the

perfect reorder point shall govern profitability of the company and prospects of growth.

d)

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Costs of holding Inventories:- Costs of holding inventories is an essential part of the total

inventory cost. It includes the carrying cost of the damaged goods, storage cost, warehouse rent,

insurance cost, watchmen cost etc. All these cost combined together gives the holding cost per

kg per annum charged on the inventory. It increases with the increase in quantity to be ordered as

higher quantity ordered has to be stored. Also there can be damages in the warehouse of the

company which increases its cost (Gorshkov, Murgul, and Oliynyk, 2016).

Costs of failing to manage inventories:- There are certain costs that are incurred when the

management is inefficient in managing the inventory like the damaged goods cost, transportation

cost and the cost of short supply of goods.

Practical implications of managing inventory:-

a good inventory management system shall help in saving cost and time

it shall also reduce amount of damages

it will allow the company to know when order is to be placed

shall avoid overstocking and under stocking it shall help in timely meeting the demands of the customers

Question 2

a) Payback Period:-

Option A Option B

Gulf stream G650ER

Boeing

BBJ Max

7

Year Cash Inflows

Cash

Inflows

1 3200 3900

2 3300 3600

3 3100 3300

4 3000 3100

5 2900 2600

inventory cost. It includes the carrying cost of the damaged goods, storage cost, warehouse rent,

insurance cost, watchmen cost etc. All these cost combined together gives the holding cost per

kg per annum charged on the inventory. It increases with the increase in quantity to be ordered as

higher quantity ordered has to be stored. Also there can be damages in the warehouse of the

company which increases its cost (Gorshkov, Murgul, and Oliynyk, 2016).

Costs of failing to manage inventories:- There are certain costs that are incurred when the

management is inefficient in managing the inventory like the damaged goods cost, transportation

cost and the cost of short supply of goods.

Practical implications of managing inventory:-

a good inventory management system shall help in saving cost and time

it shall also reduce amount of damages

it will allow the company to know when order is to be placed

shall avoid overstocking and under stocking it shall help in timely meeting the demands of the customers

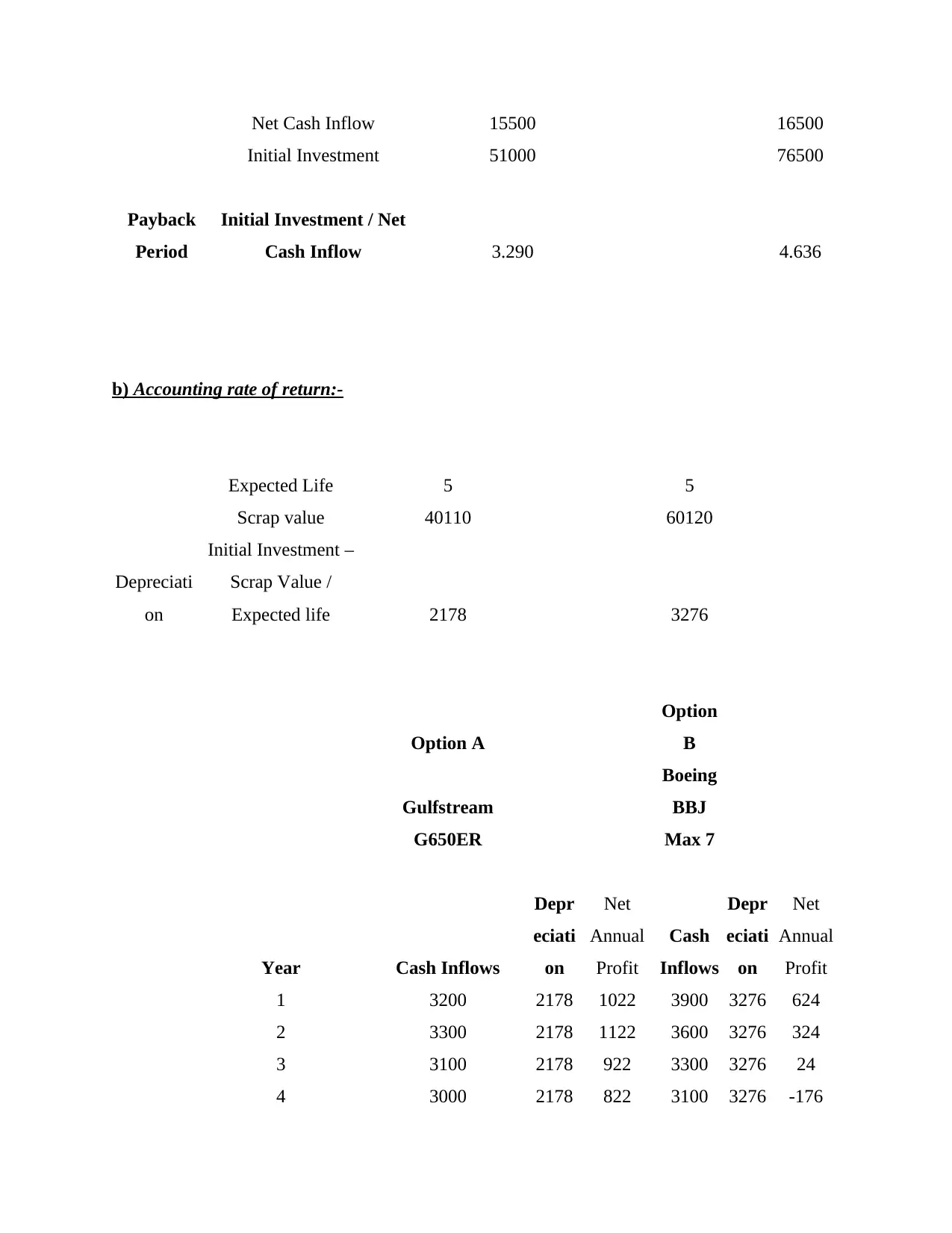

Question 2

a) Payback Period:-

Option A Option B

Gulf stream G650ER

Boeing

BBJ Max

7

Year Cash Inflows

Cash

Inflows

1 3200 3900

2 3300 3600

3 3100 3300

4 3000 3100

5 2900 2600

Net Cash Inflow 15500 16500

Initial Investment 51000 76500

Payback

Period

Initial Investment / Net

Cash Inflow 3.290 4.636

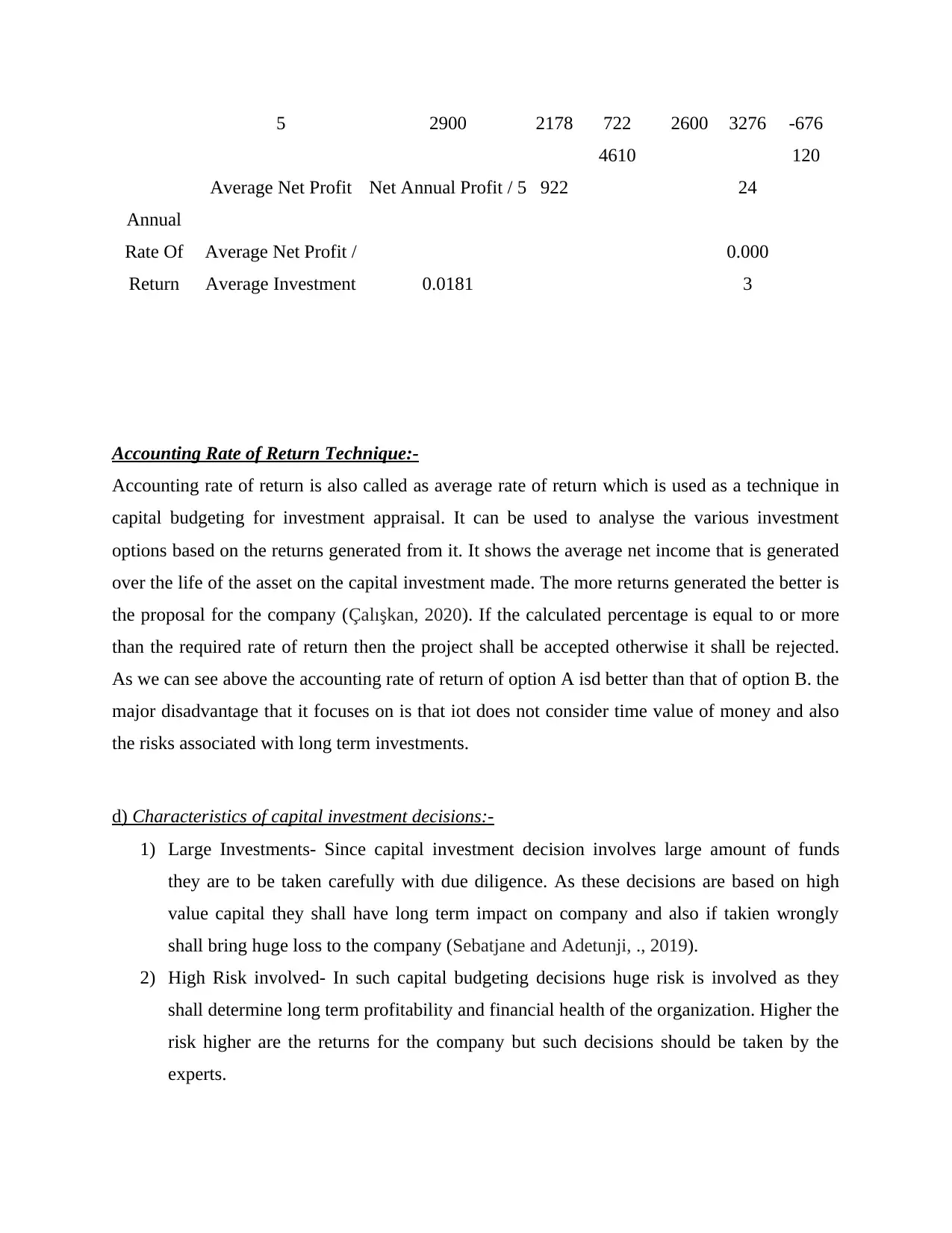

b) Accounting rate of return:-

Expected Life 5 5

Scrap value 40110 60120

Depreciati

on

Initial Investment –

Scrap Value /

Expected life 2178 3276

Option A

Option

B

Gulfstream

G650ER

Boeing

BBJ

Max 7

Year Cash Inflows

Depr

eciati

on

Net

Annual

Profit

Cash

Inflows

Depr

eciati

on

Net

Annual

Profit

1 3200 2178 1022 3900 3276 624

2 3300 2178 1122 3600 3276 324

3 3100 2178 922 3300 3276 24

4 3000 2178 822 3100 3276 -176

Initial Investment 51000 76500

Payback

Period

Initial Investment / Net

Cash Inflow 3.290 4.636

b) Accounting rate of return:-

Expected Life 5 5

Scrap value 40110 60120

Depreciati

on

Initial Investment –

Scrap Value /

Expected life 2178 3276

Option A

Option

B

Gulfstream

G650ER

Boeing

BBJ

Max 7

Year Cash Inflows

Depr

eciati

on

Net

Annual

Profit

Cash

Inflows

Depr

eciati

on

Net

Annual

Profit

1 3200 2178 1022 3900 3276 624

2 3300 2178 1122 3600 3276 324

3 3100 2178 922 3300 3276 24

4 3000 2178 822 3100 3276 -176

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

5 2900 2178 722 2600 3276 -676

4610 120

Average Net Profit Net Annual Profit / 5 922 24

Annual

Rate Of

Return

Average Net Profit /

Average Investment 0.0181

0.000

3

Accounting Rate of Return Technique:-

Accounting rate of return is also called as average rate of return which is used as a technique in

capital budgeting for investment appraisal. It can be used to analyse the various investment

options based on the returns generated from it. It shows the average net income that is generated

over the life of the asset on the capital investment made. The more returns generated the better is

the proposal for the company (Çalışkan, 2020). If the calculated percentage is equal to or more

than the required rate of return then the project shall be accepted otherwise it shall be rejected.

As we can see above the accounting rate of return of option A isd better than that of option B. the

major disadvantage that it focuses on is that iot does not consider time value of money and also

the risks associated with long term investments.

d) Characteristics of capital investment decisions:-

1) Large Investments- Since capital investment decision involves large amount of funds

they are to be taken carefully with due diligence. As these decisions are based on high

value capital they shall have long term impact on company and also if takien wrongly

shall bring huge loss to the company (Sebatjane and Adetunji, ., 2019).

2) High Risk involved- In such capital budgeting decisions huge risk is involved as they

shall determine long term profitability and financial health of the organization. Higher the

risk higher are the returns for the company but such decisions should be taken by the

experts.

4610 120

Average Net Profit Net Annual Profit / 5 922 24

Annual

Rate Of

Return

Average Net Profit /

Average Investment 0.0181

0.000

3

Accounting Rate of Return Technique:-

Accounting rate of return is also called as average rate of return which is used as a technique in

capital budgeting for investment appraisal. It can be used to analyse the various investment

options based on the returns generated from it. It shows the average net income that is generated

over the life of the asset on the capital investment made. The more returns generated the better is

the proposal for the company (Çalışkan, 2020). If the calculated percentage is equal to or more

than the required rate of return then the project shall be accepted otherwise it shall be rejected.

As we can see above the accounting rate of return of option A isd better than that of option B. the

major disadvantage that it focuses on is that iot does not consider time value of money and also

the risks associated with long term investments.

d) Characteristics of capital investment decisions:-

1) Large Investments- Since capital investment decision involves large amount of funds

they are to be taken carefully with due diligence. As these decisions are based on high

value capital they shall have long term impact on company and also if takien wrongly

shall bring huge loss to the company (Sebatjane and Adetunji, ., 2019).

2) High Risk involved- In such capital budgeting decisions huge risk is involved as they

shall determine long term profitability and financial health of the organization. Higher the

risk higher are the returns for the company but such decisions should be taken by the

experts.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

3) Irreversible Decisions- Such decisions as taken by the management of the company are

irreversible in nature which means once taken cannot be reversed. The management has

to take these decisions with utmost care as there are higher risk associated and also last

longer (Kadim, Sunardi and Husain, T2020).

4) Cost Structure- Obviously these decisions shall impact the cost structure of the company

and shall minimise profits of the company. If a huge cost decision is not able to generate

the simultaneous incomes then it shall lead to losses.

5) Affects Competitive Strengths- A profitable decision taken shall contribute to the

strengths of the company vis a vis decision taken wrong shall lead to company bearing

consequences.

Advantages and disadvantages of IRR:-

Advantages:-

The major advantage of IRR as a capital budgeting technique is that it considers the time

value of money to calculate whether a investment proposal shall be accepted or rejected.

It is a simple technique and does not require experts for its calculation. Its easily

calculated as well as analysed. If its greater than the cost of capital the decision is to

accepted, otherwise rejected.

It does not need required rate of return for its calculation which simplifies the process in

itself. Required rate of return is just a rough estimate and so its better that IRR does not

require it.

Disadvantages:-

The main disadvantage that such projects carry is that it does not focus on economies of

scale in the operations of a business. Economies of scale is always beneficial for the

company as it decreases the cost per unit. But this concept is completely ignored by IRR.

Certain projects like the Dependent and mutually exclusive ones are ignored in this

technique of capital budgeting (Hosaka, 2019).

If there is a mix of positive as well as negative cash flows in that case multiple IRR's are

generated.

irreversible in nature which means once taken cannot be reversed. The management has

to take these decisions with utmost care as there are higher risk associated and also last

longer (Kadim, Sunardi and Husain, T2020).

4) Cost Structure- Obviously these decisions shall impact the cost structure of the company

and shall minimise profits of the company. If a huge cost decision is not able to generate

the simultaneous incomes then it shall lead to losses.

5) Affects Competitive Strengths- A profitable decision taken shall contribute to the

strengths of the company vis a vis decision taken wrong shall lead to company bearing

consequences.

Advantages and disadvantages of IRR:-

Advantages:-

The major advantage of IRR as a capital budgeting technique is that it considers the time

value of money to calculate whether a investment proposal shall be accepted or rejected.

It is a simple technique and does not require experts for its calculation. Its easily

calculated as well as analysed. If its greater than the cost of capital the decision is to

accepted, otherwise rejected.

It does not need required rate of return for its calculation which simplifies the process in

itself. Required rate of return is just a rough estimate and so its better that IRR does not

require it.

Disadvantages:-

The main disadvantage that such projects carry is that it does not focus on economies of

scale in the operations of a business. Economies of scale is always beneficial for the

company as it decreases the cost per unit. But this concept is completely ignored by IRR.

Certain projects like the Dependent and mutually exclusive ones are ignored in this

technique of capital budgeting (Hosaka, 2019).

If there is a mix of positive as well as negative cash flows in that case multiple IRR's are

generated.

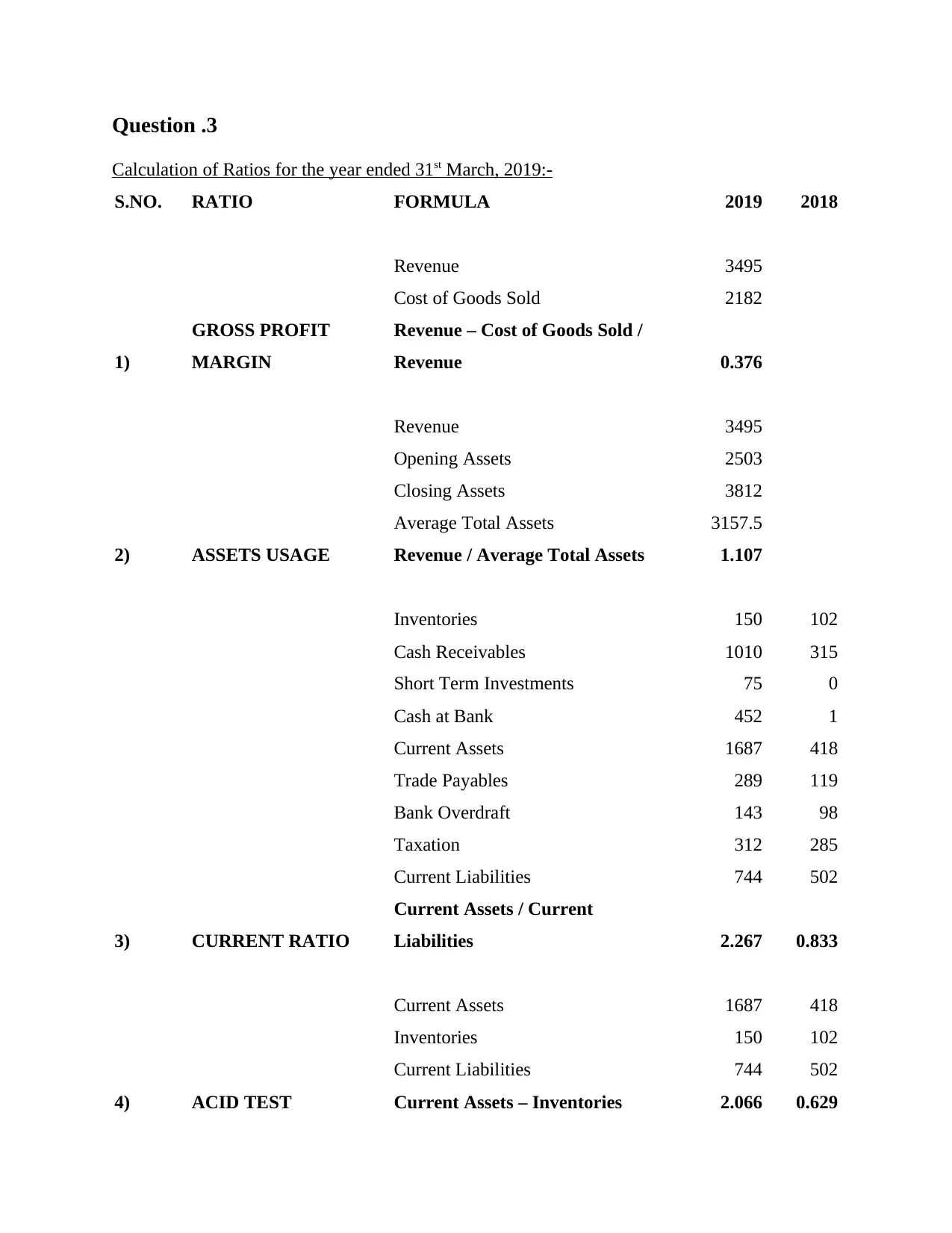

Question .3

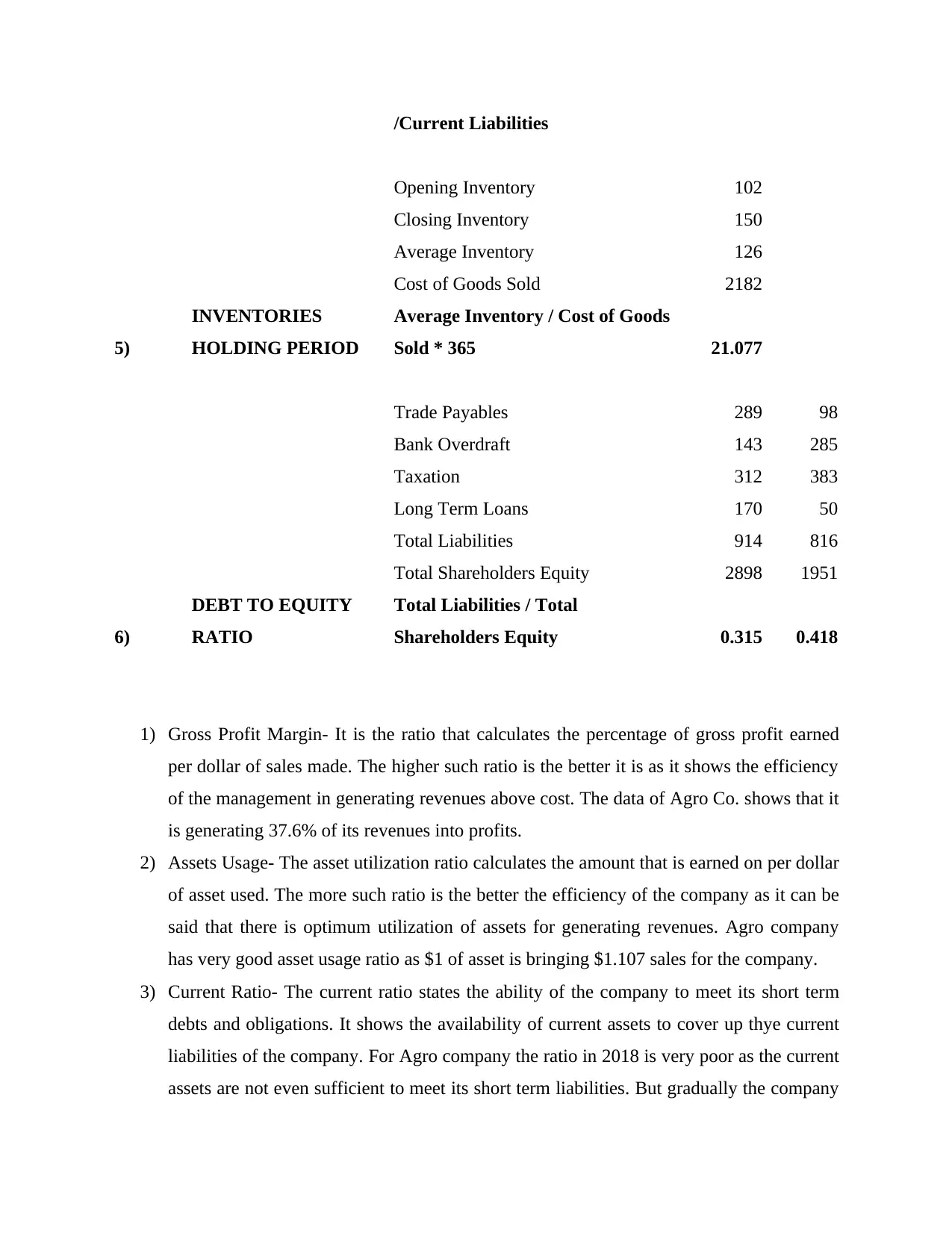

Calculation of Ratios for the year ended 31st March, 2019:-

S.NO. RATIO FORMULA 2019 2018

Revenue 3495

Cost of Goods Sold 2182

1)

GROSS PROFIT

MARGIN

Revenue – Cost of Goods Sold /

Revenue 0.376

Revenue 3495

Opening Assets 2503

Closing Assets 3812

Average Total Assets 3157.5

2) ASSETS USAGE Revenue / Average Total Assets 1.107

Inventories 150 102

Cash Receivables 1010 315

Short Term Investments 75 0

Cash at Bank 452 1

Current Assets 1687 418

Trade Payables 289 119

Bank Overdraft 143 98

Taxation 312 285

Current Liabilities 744 502

3) CURRENT RATIO

Current Assets / Current

Liabilities 2.267 0.833

Current Assets 1687 418

Inventories 150 102

Current Liabilities 744 502

4) ACID TEST Current Assets – Inventories 2.066 0.629

Calculation of Ratios for the year ended 31st March, 2019:-

S.NO. RATIO FORMULA 2019 2018

Revenue 3495

Cost of Goods Sold 2182

1)

GROSS PROFIT

MARGIN

Revenue – Cost of Goods Sold /

Revenue 0.376

Revenue 3495

Opening Assets 2503

Closing Assets 3812

Average Total Assets 3157.5

2) ASSETS USAGE Revenue / Average Total Assets 1.107

Inventories 150 102

Cash Receivables 1010 315

Short Term Investments 75 0

Cash at Bank 452 1

Current Assets 1687 418

Trade Payables 289 119

Bank Overdraft 143 98

Taxation 312 285

Current Liabilities 744 502

3) CURRENT RATIO

Current Assets / Current

Liabilities 2.267 0.833

Current Assets 1687 418

Inventories 150 102

Current Liabilities 744 502

4) ACID TEST Current Assets – Inventories 2.066 0.629

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

/Current Liabilities

Opening Inventory 102

Closing Inventory 150

Average Inventory 126

Cost of Goods Sold 2182

5)

INVENTORIES

HOLDING PERIOD

Average Inventory / Cost of Goods

Sold * 365 21.077

Trade Payables 289 98

Bank Overdraft 143 285

Taxation 312 383

Long Term Loans 170 50

Total Liabilities 914 816

Total Shareholders Equity 2898 1951

6)

DEBT TO EQUITY

RATIO

Total Liabilities / Total

Shareholders Equity 0.315 0.418

1) Gross Profit Margin- It is the ratio that calculates the percentage of gross profit earned

per dollar of sales made. The higher such ratio is the better it is as it shows the efficiency

of the management in generating revenues above cost. The data of Agro Co. shows that it

is generating 37.6% of its revenues into profits.

2) Assets Usage- The asset utilization ratio calculates the amount that is earned on per dollar

of asset used. The more such ratio is the better the efficiency of the company as it can be

said that there is optimum utilization of assets for generating revenues. Agro company

has very good asset usage ratio as $1 of asset is bringing $1.107 sales for the company.

3) Current Ratio- The current ratio states the ability of the company to meet its short term

debts and obligations. It shows the availability of current assets to cover up thye current

liabilities of the company. For Agro company the ratio in 2018 is very poor as the current

assets are not even sufficient to meet its short term liabilities. But gradually the company

Opening Inventory 102

Closing Inventory 150

Average Inventory 126

Cost of Goods Sold 2182

5)

INVENTORIES

HOLDING PERIOD

Average Inventory / Cost of Goods

Sold * 365 21.077

Trade Payables 289 98

Bank Overdraft 143 285

Taxation 312 383

Long Term Loans 170 50

Total Liabilities 914 816

Total Shareholders Equity 2898 1951

6)

DEBT TO EQUITY

RATIO

Total Liabilities / Total

Shareholders Equity 0.315 0.418

1) Gross Profit Margin- It is the ratio that calculates the percentage of gross profit earned

per dollar of sales made. The higher such ratio is the better it is as it shows the efficiency

of the management in generating revenues above cost. The data of Agro Co. shows that it

is generating 37.6% of its revenues into profits.

2) Assets Usage- The asset utilization ratio calculates the amount that is earned on per dollar

of asset used. The more such ratio is the better the efficiency of the company as it can be

said that there is optimum utilization of assets for generating revenues. Agro company

has very good asset usage ratio as $1 of asset is bringing $1.107 sales for the company.

3) Current Ratio- The current ratio states the ability of the company to meet its short term

debts and obligations. It shows the availability of current assets to cover up thye current

liabilities of the company. For Agro company the ratio in 2018 is very poor as the current

assets are not even sufficient to meet its short term liabilities. But gradually the company

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

is performing better as in the year 2019 its current assets are more than double its current

liabilities.

4) Acid Test- This is a more specific version of current ratio where it is found out how much

short term assets are there to cover short term liabilities. In 2018 it is an alarming

situation as there are less assets to meet up the obligations but in 2019 they are double the

amount of liabilities (Arkan, 2016).

5) Inventories holding period- It shows the average number of days a firm holds the

inventory. The Agro company averagely holds the inventory for 21 days.

6) Debt to Equity Ratio- The percentage of company's operations being financed by its debt

funds. It shows the financial leverage of the company. In the year 2018 it is 41.8% and in

the year 2019 it is 31.5%.

b) It is very important to consider the audience in the financial statement analysis as there are

various users of such information. The external and internal users of the financial data of an

organization are crucial for the growth of the company.

1) Debt management- In order to manage the debts of the company and its timely

recoveries, the debtors have to be considered while doing the financial analysis. In how

much time are the debts to be recovered and what amount can get converted into bad

debts and what impact shall it have on the operating cycle.

2) Avoiding fraudulent activities- To avoid frauds and manipulations in an organization it is

important to analyse the financial data through auditors. It is also mandatory to supervise

the operations of employees and the management in an organisation.

3) Investments- For carrying out smooth and efficient operations in a company it is very

essential that there are sufficient funds available. These funds are provided by the

existing shareholders or can be provided by the potential ones. So it is important to

consider such audience in the financial analysis and to generate better results for them,

which shall ultimately lead to growth of the company.

4) Trend analysis- For the growth and development of Agro company it is important to

analyse the current trend in the market. For such analysis it is very important to consider

the tastes and preferences of customers and also the competitors.

liabilities.

4) Acid Test- This is a more specific version of current ratio where it is found out how much

short term assets are there to cover short term liabilities. In 2018 it is an alarming

situation as there are less assets to meet up the obligations but in 2019 they are double the

amount of liabilities (Arkan, 2016).

5) Inventories holding period- It shows the average number of days a firm holds the

inventory. The Agro company averagely holds the inventory for 21 days.

6) Debt to Equity Ratio- The percentage of company's operations being financed by its debt

funds. It shows the financial leverage of the company. In the year 2018 it is 41.8% and in

the year 2019 it is 31.5%.

b) It is very important to consider the audience in the financial statement analysis as there are

various users of such information. The external and internal users of the financial data of an

organization are crucial for the growth of the company.

1) Debt management- In order to manage the debts of the company and its timely

recoveries, the debtors have to be considered while doing the financial analysis. In how

much time are the debts to be recovered and what amount can get converted into bad

debts and what impact shall it have on the operating cycle.

2) Avoiding fraudulent activities- To avoid frauds and manipulations in an organization it is

important to analyse the financial data through auditors. It is also mandatory to supervise

the operations of employees and the management in an organisation.

3) Investments- For carrying out smooth and efficient operations in a company it is very

essential that there are sufficient funds available. These funds are provided by the

existing shareholders or can be provided by the potential ones. So it is important to

consider such audience in the financial analysis and to generate better results for them,

which shall ultimately lead to growth of the company.

4) Trend analysis- For the growth and development of Agro company it is important to

analyse the current trend in the market. For such analysis it is very important to consider

the tastes and preferences of customers and also the competitors.

QUESTION 4

Demonstrates the role of IFRS foundation, IFRS interpretation committee and IFRS advisory

council with international regulatory framework for accounting.

IFRS foundation: It is considered to be as a non- profit organization. The primary role of

the company is to develop the IFRS standards and also bring out accountability, efficiency and

transparency (Williams, 2014). It is useful in fostering long term financial stability associated

with the global economy. It is considered to be highly significant in setting the high quality

standards and also tends to comply with the accepted degree of financial reporting.

IFRS advisory council: It is considered to be as a formal advisory body to the trustee

associated with the IFRS foundation as well as international accounting standard board. It is

significant in effectively providing strategic set of support as well as the advice. It is significant

in advising the board upon the priorities and agenda for the decision making. It is prominent in

significant standard setting projects. International regulatory framework for accounting is the

prominent framework for preparation of the key financial statements in order to examine the

position of the organization.

IFRS interpretation committee: It is referred to as an interpretative body associated with

the international accounting standard board (Mexmonov, 2020). This is useful for the members

in providing best possible technical set of expertise and also improve the market experience

associated with the application of the IFRS standards. International regulatory framework for

accounting is prominent to provide the specific set of rules as well as the key regulations

associated with the accounting.

Demonstrating upon role of the audit committee within the corporate governance.

Corporate governance in turn is referred to as the prominent system through which the

company has been controlled as well as directed. However, the corporate governance is crucial

because it usually influence how the decision markers tend to act and they can be effectively held

highly accountable for the actions and decisions (Suryanto, Thalassinos and Thalassinos, 2017).

The audit committee must in turn also have at least one individual within the committee who is

referred to as a financial expert. They must have complete degree of knowledge associated with

the key financial issues. The key primary role of the audit committee is to effectively form the

significant set of the cornerstone related with the effective corporate governance. However, the

Demonstrates the role of IFRS foundation, IFRS interpretation committee and IFRS advisory

council with international regulatory framework for accounting.

IFRS foundation: It is considered to be as a non- profit organization. The primary role of

the company is to develop the IFRS standards and also bring out accountability, efficiency and

transparency (Williams, 2014). It is useful in fostering long term financial stability associated

with the global economy. It is considered to be highly significant in setting the high quality

standards and also tends to comply with the accepted degree of financial reporting.

IFRS advisory council: It is considered to be as a formal advisory body to the trustee

associated with the IFRS foundation as well as international accounting standard board. It is

significant in effectively providing strategic set of support as well as the advice. It is significant

in advising the board upon the priorities and agenda for the decision making. It is prominent in

significant standard setting projects. International regulatory framework for accounting is the

prominent framework for preparation of the key financial statements in order to examine the

position of the organization.

IFRS interpretation committee: It is referred to as an interpretative body associated with

the international accounting standard board (Mexmonov, 2020). This is useful for the members

in providing best possible technical set of expertise and also improve the market experience

associated with the application of the IFRS standards. International regulatory framework for

accounting is prominent to provide the specific set of rules as well as the key regulations

associated with the accounting.

Demonstrating upon role of the audit committee within the corporate governance.

Corporate governance in turn is referred to as the prominent system through which the

company has been controlled as well as directed. However, the corporate governance is crucial

because it usually influence how the decision markers tend to act and they can be effectively held

highly accountable for the actions and decisions (Suryanto, Thalassinos and Thalassinos, 2017).

The audit committee must in turn also have at least one individual within the committee who is

referred to as a financial expert. They must have complete degree of knowledge associated with

the key financial issues. The key primary role of the audit committee is to effectively form the

significant set of the cornerstone related with the effective corporate governance. However, the

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 15

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.