Business Finance Report: GRL Company Analysis and Recommendations

VerifiedAdded on 2020/06/04

|13

|2932

|68

Report

AI Summary

This report provides a comprehensive analysis of business finance principles, focusing on cash flow, working capital management, and capital budgeting techniques. Part 1 defines and differentiates profit, cash flow, and working capital, including its components (receivables, inventory, payables) and how fluctuations impact cash flow. Hypothetical figures are used to illustrate these concepts, followed by an analysis of the GRL company's cash flow management and recommendations for improvement. Part 2 delves into capital budgeting, explaining its purpose, key stages, and evaluating techniques such as payback period, net present value (NPV), and internal rate of return (IRR). The report applies these techniques using hypothetical data for two projects, Leeds Ventures and Bristol Ventures, calculating payback periods and NPVs. Finally, it analyzes the results and suggests a project for the GRL company.

BUSINESS FINANCE

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

TABLE OF CONTENTS

PART 1............................................................................................................................................1

I. a. Meaning of profit and cash-flow along with difference..................................................1

I. b. Meaning of working capital and its components............................................................1

I. c. Ways by which fluctuations in working capital influence cash-flow.............................2

II. Application of the above terms using hypothetical figures...............................................2

III. Analysing as well as recommending steps which should be taken GRL company for

managing cash flow................................................................................................................3

PART 2............................................................................................................................................4

I. a. Meaning of capital budgeting, its purpose and key stages of procedure.........................4

I. b. Evaluating three capital budgeting techniques................................................................5

II. Applying the above concepts using hypothetical data.......................................................6

III. Analysing and suggesting one project..............................................................................9

REFERENCES..............................................................................................................................10

PART 1............................................................................................................................................1

I. a. Meaning of profit and cash-flow along with difference..................................................1

I. b. Meaning of working capital and its components............................................................1

I. c. Ways by which fluctuations in working capital influence cash-flow.............................2

II. Application of the above terms using hypothetical figures...............................................2

III. Analysing as well as recommending steps which should be taken GRL company for

managing cash flow................................................................................................................3

PART 2............................................................................................................................................4

I. a. Meaning of capital budgeting, its purpose and key stages of procedure.........................4

I. b. Evaluating three capital budgeting techniques................................................................5

II. Applying the above concepts using hypothetical data.......................................................6

III. Analysing and suggesting one project..............................................................................9

REFERENCES..............................................................................................................................10

PART 1

I. a. Meaning of profit and cash-flow along with difference

A financial earning which generated by the firm or difference among amount earned as

well as spent on several business activities is considered as profit. Higher the amount of profit at

the workplace is highly beneficial for every firm including GardenRite Limited enterprise.

Amount which reflects difference between specifically two values which are like cash

incomes and cash payments is known as cash-flow in financials (Fazzari and Papadimitrio,

2015). Lower the amount of this aspect shows that firm has low liquidity position in the industry.

Amount of profit is computed on the yearly or half yearly basis at the workplace of every

entity whereas calculation of cash flow is performed on monthly or half yearly basis. Profit is

used by both internal and external stakeholders of the GRL while cash flows taken into account

by only internal stakeholders. Using profit, the management of cited organisation can make

decisions for providing dividend to shareholders whereas cash flow helps to make investment

and funding judgements. In addition to this, profit reflects outline of financial performance of an

enterprise in the industry while cash flow shows only liquidity or cash condition.

I. b. Meaning of working capital and its components Working capital: An amount which is used in the firm for day-to-day activities and

trading is known as working capital. It is calculated using particular formula which is

WC = current assets – current liabilities. Those contents which are relied under current

assets like cash, stock, accounts receivables, debtors etc. are included in this aspect

(Johnson, McLaughlin and Haueter, 2015). On the another side, each and every

component of current liabilities which involve short-term loans, accrued liabilities,

accounts payables etc. taken into account. Further, it has major three elements which are

described below: Receivables: Sum of money which will be received by the firm in next years or after

some months is considered as receivables. This amount will be paid by those customers

who purchased products and services from GRL on credit rather than cash.

1

I. a. Meaning of profit and cash-flow along with difference

A financial earning which generated by the firm or difference among amount earned as

well as spent on several business activities is considered as profit. Higher the amount of profit at

the workplace is highly beneficial for every firm including GardenRite Limited enterprise.

Amount which reflects difference between specifically two values which are like cash

incomes and cash payments is known as cash-flow in financials (Fazzari and Papadimitrio,

2015). Lower the amount of this aspect shows that firm has low liquidity position in the industry.

Amount of profit is computed on the yearly or half yearly basis at the workplace of every

entity whereas calculation of cash flow is performed on monthly or half yearly basis. Profit is

used by both internal and external stakeholders of the GRL while cash flows taken into account

by only internal stakeholders. Using profit, the management of cited organisation can make

decisions for providing dividend to shareholders whereas cash flow helps to make investment

and funding judgements. In addition to this, profit reflects outline of financial performance of an

enterprise in the industry while cash flow shows only liquidity or cash condition.

I. b. Meaning of working capital and its components Working capital: An amount which is used in the firm for day-to-day activities and

trading is known as working capital. It is calculated using particular formula which is

WC = current assets – current liabilities. Those contents which are relied under current

assets like cash, stock, accounts receivables, debtors etc. are included in this aspect

(Johnson, McLaughlin and Haueter, 2015). On the another side, each and every

component of current liabilities which involve short-term loans, accrued liabilities,

accounts payables etc. taken into account. Further, it has major three elements which are

described below: Receivables: Sum of money which will be received by the firm in next years or after

some months is considered as receivables. This amount will be paid by those customers

who purchased products and services from GRL on credit rather than cash.

1

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Inventory: Goods and services or any other assets which are not sold in current year and

remained at the workplace is known as inventory. In each enterprise there are two kinds

of stock available which are like closing and opening.

Payables: Sum of money which is owed by an organisation and will be paid to its

suppliers or creditors after some times is known as payables (Wilson, 2016). It can be in

form of short-term debts, purchase of raw materials etc.

I. c. Ways by which fluctuations in working capital influence cash-flow

Working capital is difference of two values i.e. current assets and current liabilities which

create positive and negative impact on the GRL's cash flows. There is highly direct relationship

between both the terms of finance which are like cash flows and working capital. Due to

increasing in working capital of the entity, cash flows will also enhance. The reason is that, when

cash assets enhance and cash liabilities will reduce then amount of working capital will be

affected in positive direction. This specific term clearly reflects that cash inflows will enhance as

compared to the cash outflows. Ultimately, amount of cash flows will improve which is positive

indication to boost up overall financial performance.

On the other side, due to increase in current liabilities and decline in current assets

working capital will be affected negatively. As per the direct or positive relations among these

both the aspects it can be said that, cash flows will reduce in the company (Keasey, Pindado and

Rodrigues, 2015). Higher the value of working capital and cash flows is beneficial for every

enterprise.

II. Application of the above terms using hypothetical figures

In order to perform computation of working capital there are some components of current

assets and current liabilities are taken into account. Further, it majorly relies on three aspects

which are like receivables, payables as well as inventories. Figures used to make calculation of

WC are hypothetical (Macve, 2015). Moreover, application of the above stated elements and

working capital is stated below:

Particulars Amount

Current assets

Cash 80000

2

remained at the workplace is known as inventory. In each enterprise there are two kinds

of stock available which are like closing and opening.

Payables: Sum of money which is owed by an organisation and will be paid to its

suppliers or creditors after some times is known as payables (Wilson, 2016). It can be in

form of short-term debts, purchase of raw materials etc.

I. c. Ways by which fluctuations in working capital influence cash-flow

Working capital is difference of two values i.e. current assets and current liabilities which

create positive and negative impact on the GRL's cash flows. There is highly direct relationship

between both the terms of finance which are like cash flows and working capital. Due to

increasing in working capital of the entity, cash flows will also enhance. The reason is that, when

cash assets enhance and cash liabilities will reduce then amount of working capital will be

affected in positive direction. This specific term clearly reflects that cash inflows will enhance as

compared to the cash outflows. Ultimately, amount of cash flows will improve which is positive

indication to boost up overall financial performance.

On the other side, due to increase in current liabilities and decline in current assets

working capital will be affected negatively. As per the direct or positive relations among these

both the aspects it can be said that, cash flows will reduce in the company (Keasey, Pindado and

Rodrigues, 2015). Higher the value of working capital and cash flows is beneficial for every

enterprise.

II. Application of the above terms using hypothetical figures

In order to perform computation of working capital there are some components of current

assets and current liabilities are taken into account. Further, it majorly relies on three aspects

which are like receivables, payables as well as inventories. Figures used to make calculation of

WC are hypothetical (Macve, 2015). Moreover, application of the above stated elements and

working capital is stated below:

Particulars Amount

Current assets

Cash 80000

2

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

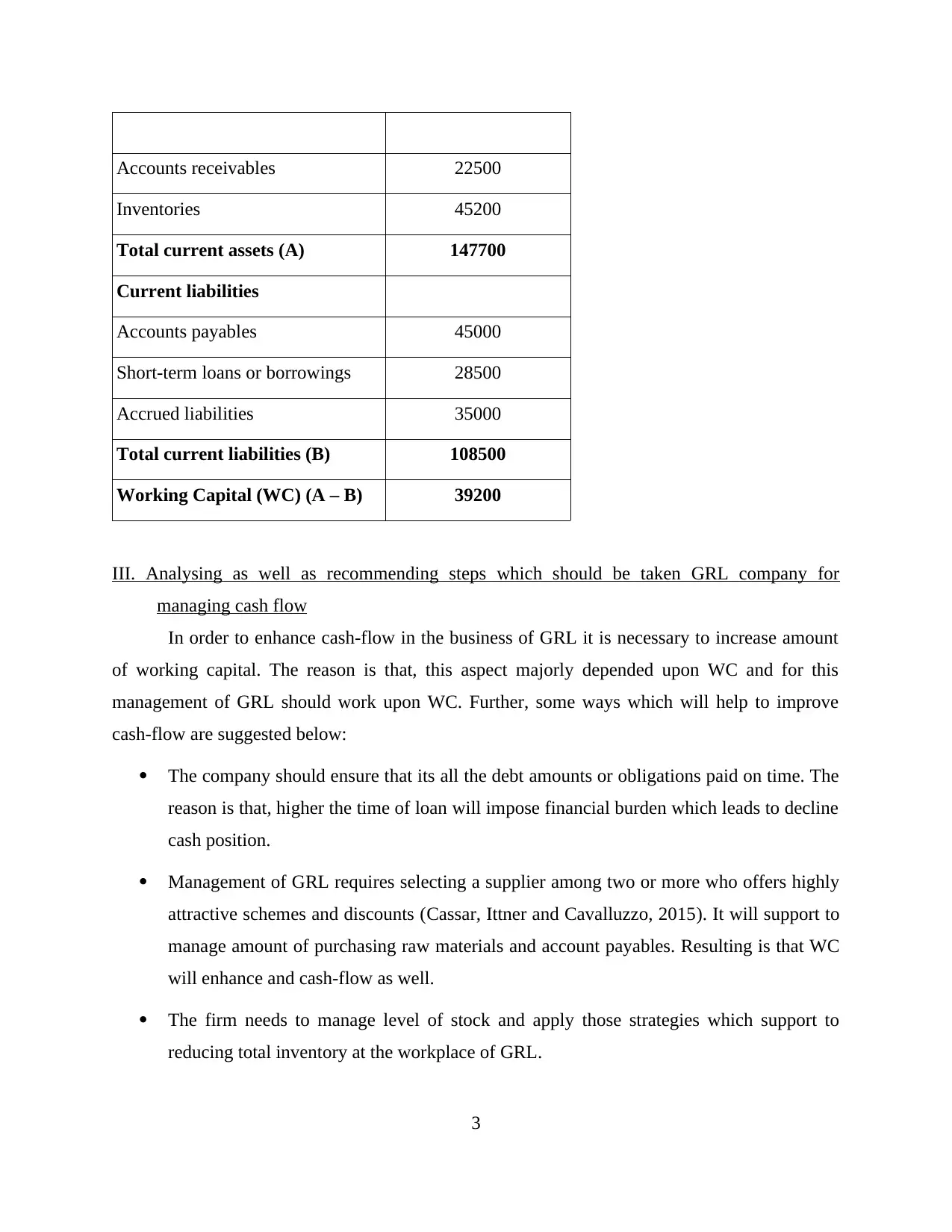

Accounts receivables 22500

Inventories 45200

Total current assets (A) 147700

Current liabilities

Accounts payables 45000

Short-term loans or borrowings 28500

Accrued liabilities 35000

Total current liabilities (B) 108500

Working Capital (WC) (A – B) 39200

III. Analysing as well as recommending steps which should be taken GRL company for

managing cash flow

In order to enhance cash-flow in the business of GRL it is necessary to increase amount

of working capital. The reason is that, this aspect majorly depended upon WC and for this

management of GRL should work upon WC. Further, some ways which will help to improve

cash-flow are suggested below:

The company should ensure that its all the debt amounts or obligations paid on time. The

reason is that, higher the time of loan will impose financial burden which leads to decline

cash position.

Management of GRL requires selecting a supplier among two or more who offers highly

attractive schemes and discounts (Cassar, Ittner and Cavalluzzo, 2015). It will support to

manage amount of purchasing raw materials and account payables. Resulting is that WC

will enhance and cash-flow as well.

The firm needs to manage level of stock and apply those strategies which support to

reducing total inventory at the workplace of GRL.

3

Inventories 45200

Total current assets (A) 147700

Current liabilities

Accounts payables 45000

Short-term loans or borrowings 28500

Accrued liabilities 35000

Total current liabilities (B) 108500

Working Capital (WC) (A – B) 39200

III. Analysing as well as recommending steps which should be taken GRL company for

managing cash flow

In order to enhance cash-flow in the business of GRL it is necessary to increase amount

of working capital. The reason is that, this aspect majorly depended upon WC and for this

management of GRL should work upon WC. Further, some ways which will help to improve

cash-flow are suggested below:

The company should ensure that its all the debt amounts or obligations paid on time. The

reason is that, higher the time of loan will impose financial burden which leads to decline

cash position.

Management of GRL requires selecting a supplier among two or more who offers highly

attractive schemes and discounts (Cassar, Ittner and Cavalluzzo, 2015). It will support to

manage amount of purchasing raw materials and account payables. Resulting is that WC

will enhance and cash-flow as well.

The firm needs to manage level of stock and apply those strategies which support to

reducing total inventory at the workplace of GRL.

3

At the time of making expenses it should analyse fixed and variable costs. If any of the

expenditure seems high and unproductive then can be reduced which is indication of

enhancing cash position in GRL.

Management should analyse financial information or transactions within very short

period of time. It will help to decline unnecessary costs and enhance working capital

(Kumaran, 2015).

At the end, GRL needs to apply attractive marketing strategies which will support to raise

sales revenue and cash position.

PART 2

I. a. Meaning of capital budgeting, its purpose and key stages of procedure

A planning procedure which is considered by an enterprise in order to analyse and

evaluate long term investments at the workplace which are like machinery, purchase of property

or plant, etc. is known as capital budgeting. Due to helping in investment decisions at the

working environment, it considers as investment appraisal techniques as well (Capital

Budgeting, 2015). It consists of various tools like NPV, IRR, payback period, ARR, profitability

index, etc.

Purposes or objectives of capital budgeting are stated below:

In order to assess profitable capital expenses of the project, this is an essential aspect.

To determine that whether replacement of existing machinery will give higher profit as

compared to previous or not.

For selecting and implementing one project among two or more simultaneous in GRL

firm, it is one of the best approaches.

To identify financial resources, needed in capital expenditure. For evaluating one of the best projects and decide to implement at the workplace.

Process of capital budgeting:

Identifying one of more projects as well as generation.

Screening and then evaluation of projects after applying tools and methods of capital

budgeting (Johnstone, 2015).

Selection of one project which has the highest NPV, IRR, ARR and lowest payback

period.

4

expenditure seems high and unproductive then can be reduced which is indication of

enhancing cash position in GRL.

Management should analyse financial information or transactions within very short

period of time. It will help to decline unnecessary costs and enhance working capital

(Kumaran, 2015).

At the end, GRL needs to apply attractive marketing strategies which will support to raise

sales revenue and cash position.

PART 2

I. a. Meaning of capital budgeting, its purpose and key stages of procedure

A planning procedure which is considered by an enterprise in order to analyse and

evaluate long term investments at the workplace which are like machinery, purchase of property

or plant, etc. is known as capital budgeting. Due to helping in investment decisions at the

working environment, it considers as investment appraisal techniques as well (Capital

Budgeting, 2015). It consists of various tools like NPV, IRR, payback period, ARR, profitability

index, etc.

Purposes or objectives of capital budgeting are stated below:

In order to assess profitable capital expenses of the project, this is an essential aspect.

To determine that whether replacement of existing machinery will give higher profit as

compared to previous or not.

For selecting and implementing one project among two or more simultaneous in GRL

firm, it is one of the best approaches.

To identify financial resources, needed in capital expenditure. For evaluating one of the best projects and decide to implement at the workplace.

Process of capital budgeting:

Identifying one of more projects as well as generation.

Screening and then evaluation of projects after applying tools and methods of capital

budgeting (Johnstone, 2015).

Selection of one project which has the highest NPV, IRR, ARR and lowest payback

period.

4

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Implementation at the workplace of GRL Company.

Reviewing performance of the project after completing investment years.

I. b. Evaluating three capital budgeting techniques

Payback Period

A method which helps an entity for determining years or period in which total amount of

initial investment will be recovered is known as payback period. For performing computation of

this, firstly, cumulative cash flows are calculated and then formula is applied i.e.

Payback period = Investment required / Net annual cash flow

Advantages:

It is a very simple method to make calculations.

Easy to make analysis and interpretation of computations.

One of the important indicators of cash position of liquidity of specific project

(Advantages And Disadvantages Of Pay Back Period (PBP), 2012). It is highly cost effective or cheap method.

Drawbacks:

It does not consider the time value of money.

It ignores cash inflows which are occurred after the payback period.

Net Present Value

NPV represents current value of the present investment which will be incurred after

completing project. On the basis of this, decision for investing money is taken in a proper way.

Formula to compute NPV of project is stated as below:

Benefits:

It considers time value of money and gives higher importance to this.

It uses both cash inflows i.e. before and after the project's life.

Risks and return or profitability; both these aspects are to be given with higher priority

while computing NPV of project (Keythman, 2016). It helps to enhance or maximise value of firm i.e. GRL.

5

Reviewing performance of the project after completing investment years.

I. b. Evaluating three capital budgeting techniques

Payback Period

A method which helps an entity for determining years or period in which total amount of

initial investment will be recovered is known as payback period. For performing computation of

this, firstly, cumulative cash flows are calculated and then formula is applied i.e.

Payback period = Investment required / Net annual cash flow

Advantages:

It is a very simple method to make calculations.

Easy to make analysis and interpretation of computations.

One of the important indicators of cash position of liquidity of specific project

(Advantages And Disadvantages Of Pay Back Period (PBP), 2012). It is highly cost effective or cheap method.

Drawbacks:

It does not consider the time value of money.

It ignores cash inflows which are occurred after the payback period.

Net Present Value

NPV represents current value of the present investment which will be incurred after

completing project. On the basis of this, decision for investing money is taken in a proper way.

Formula to compute NPV of project is stated as below:

Benefits:

It considers time value of money and gives higher importance to this.

It uses both cash inflows i.e. before and after the project's life.

Risks and return or profitability; both these aspects are to be given with higher priority

while computing NPV of project (Keythman, 2016). It helps to enhance or maximise value of firm i.e. GRL.

5

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Drawbacks:

To use and implement, NPV is difficult.

If the projects have not same life and initial investment then not they are useful to make

comparison.

Therefore, beneficial and profitable decisions cannot to be made.

Internal rate of return

The tool through which returns which will be generated at the end of project completion

and assess profitability of an investment is considered as internal rate of return (IRR). Formula

for performing calculation of IRR is stated as below:

Benefits:

It is very simple to interpret and make analysis.

It uses time value of money through which effective decisions can be made.

In this, cost of capital or discounting factor is not needed. If needs to address discounting factor then analysts can take as per his or her convenience

(Akers, 2016).

Limitations:

It includes little complex and tedious calculation.

It does not consider the economies of scale while performing calculation.

Not supportive to compare in between two or mutually exclusive projects.

II. Applying the above concepts using hypothetical data

Payback Period

Project 1: Leeds Ventures

Year Cash flow of project Cumulative cash flow

Initial investment £10000000

1 580000 9420000

2 900000 8520000

6

To use and implement, NPV is difficult.

If the projects have not same life and initial investment then not they are useful to make

comparison.

Therefore, beneficial and profitable decisions cannot to be made.

Internal rate of return

The tool through which returns which will be generated at the end of project completion

and assess profitability of an investment is considered as internal rate of return (IRR). Formula

for performing calculation of IRR is stated as below:

Benefits:

It is very simple to interpret and make analysis.

It uses time value of money through which effective decisions can be made.

In this, cost of capital or discounting factor is not needed. If needs to address discounting factor then analysts can take as per his or her convenience

(Akers, 2016).

Limitations:

It includes little complex and tedious calculation.

It does not consider the economies of scale while performing calculation.

Not supportive to compare in between two or mutually exclusive projects.

II. Applying the above concepts using hypothetical data

Payback Period

Project 1: Leeds Ventures

Year Cash flow of project Cumulative cash flow

Initial investment £10000000

1 580000 9420000

2 900000 8520000

6

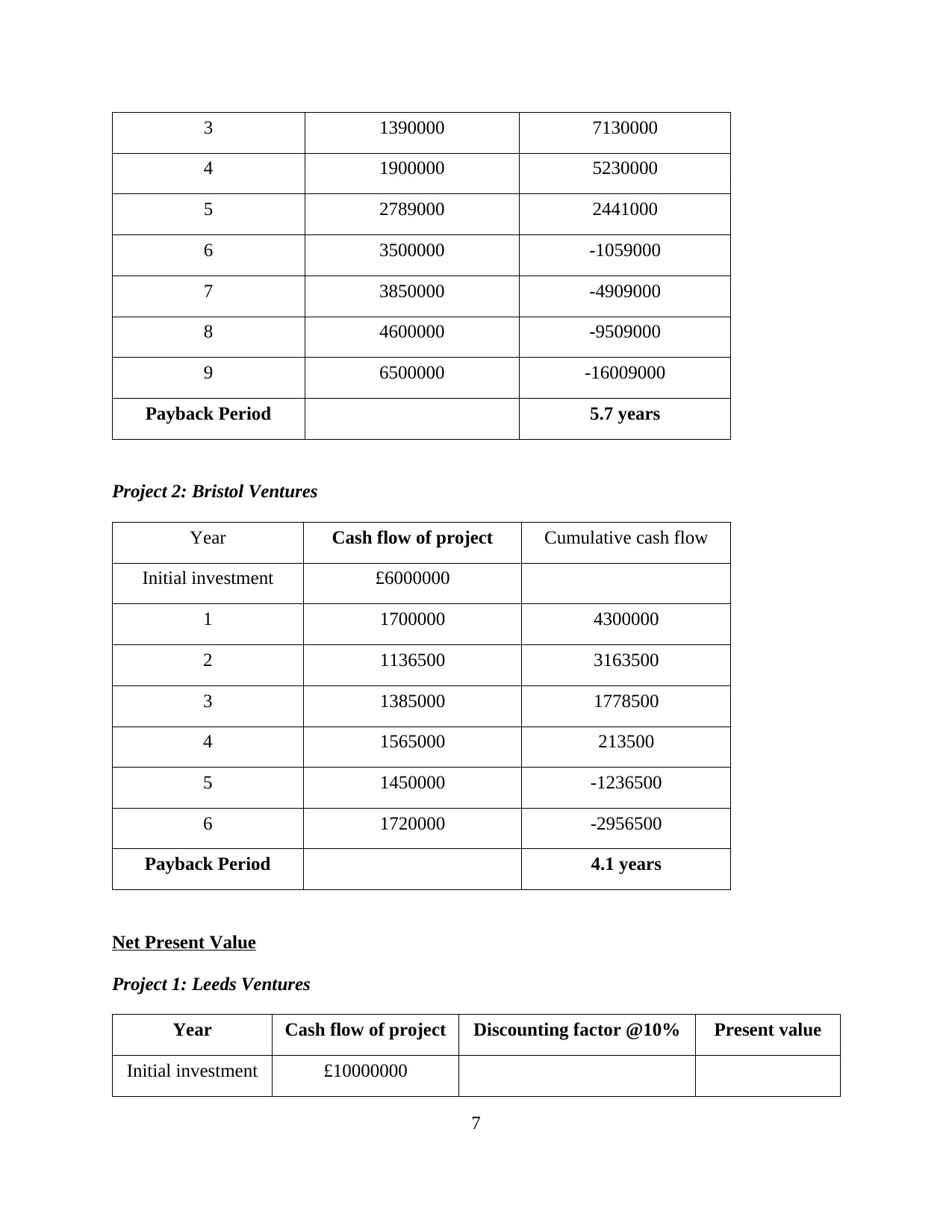

3 1390000 7130000

4 1900000 5230000

5 2789000 2441000

6 3500000 -1059000

7 3850000 -4909000

8 4600000 -9509000

9 6500000 -16009000

Payback Period 5.7 years

Project 2: Bristol Ventures

Year Cash flow of project Cumulative cash flow

Initial investment £6000000

1 1700000 4300000

2 1136500 3163500

3 1385000 1778500

4 1565000 213500

5 1450000 -1236500

6 1720000 -2956500

Payback Period 4.1 years

Net Present Value

Project 1: Leeds Ventures

Year Cash flow of project Discounting factor @10% Present value

Initial investment £10000000

7

4 1900000 5230000

5 2789000 2441000

6 3500000 -1059000

7 3850000 -4909000

8 4600000 -9509000

9 6500000 -16009000

Payback Period 5.7 years

Project 2: Bristol Ventures

Year Cash flow of project Cumulative cash flow

Initial investment £6000000

1 1700000 4300000

2 1136500 3163500

3 1385000 1778500

4 1565000 213500

5 1450000 -1236500

6 1720000 -2956500

Payback Period 4.1 years

Net Present Value

Project 1: Leeds Ventures

Year Cash flow of project Discounting factor @10% Present value

Initial investment £10000000

7

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

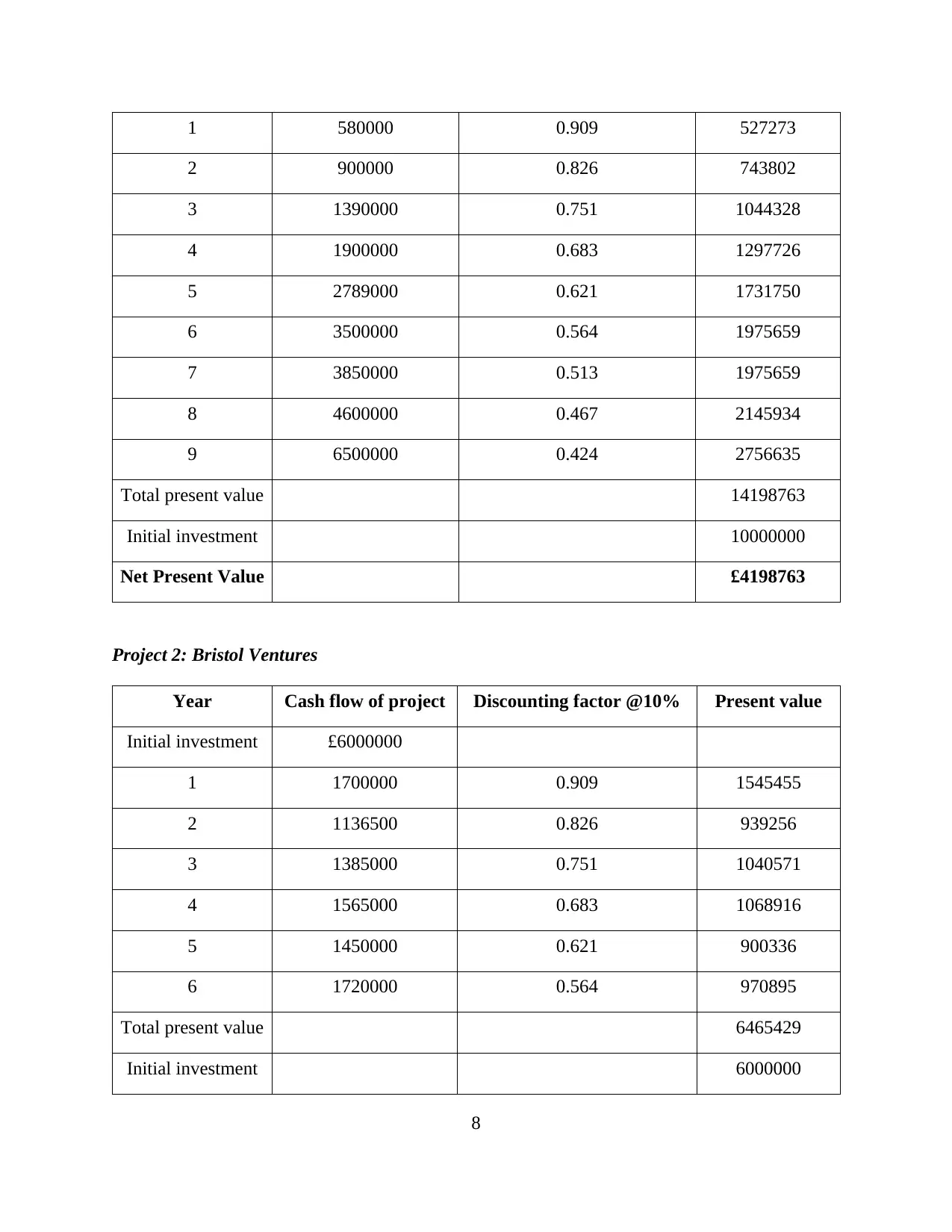

1 580000 0.909 527273

2 900000 0.826 743802

3 1390000 0.751 1044328

4 1900000 0.683 1297726

5 2789000 0.621 1731750

6 3500000 0.564 1975659

7 3850000 0.513 1975659

8 4600000 0.467 2145934

9 6500000 0.424 2756635

Total present value 14198763

Initial investment 10000000

Net Present Value £4198763

Project 2: Bristol Ventures

Year Cash flow of project Discounting factor @10% Present value

Initial investment £6000000

1 1700000 0.909 1545455

2 1136500 0.826 939256

3 1385000 0.751 1040571

4 1565000 0.683 1068916

5 1450000 0.621 900336

6 1720000 0.564 970895

Total present value 6465429

Initial investment 6000000

8

2 900000 0.826 743802

3 1390000 0.751 1044328

4 1900000 0.683 1297726

5 2789000 0.621 1731750

6 3500000 0.564 1975659

7 3850000 0.513 1975659

8 4600000 0.467 2145934

9 6500000 0.424 2756635

Total present value 14198763

Initial investment 10000000

Net Present Value £4198763

Project 2: Bristol Ventures

Year Cash flow of project Discounting factor @10% Present value

Initial investment £6000000

1 1700000 0.909 1545455

2 1136500 0.826 939256

3 1385000 0.751 1040571

4 1565000 0.683 1068916

5 1450000 0.621 900336

6 1720000 0.564 970895

Total present value 6465429

Initial investment 6000000

8

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

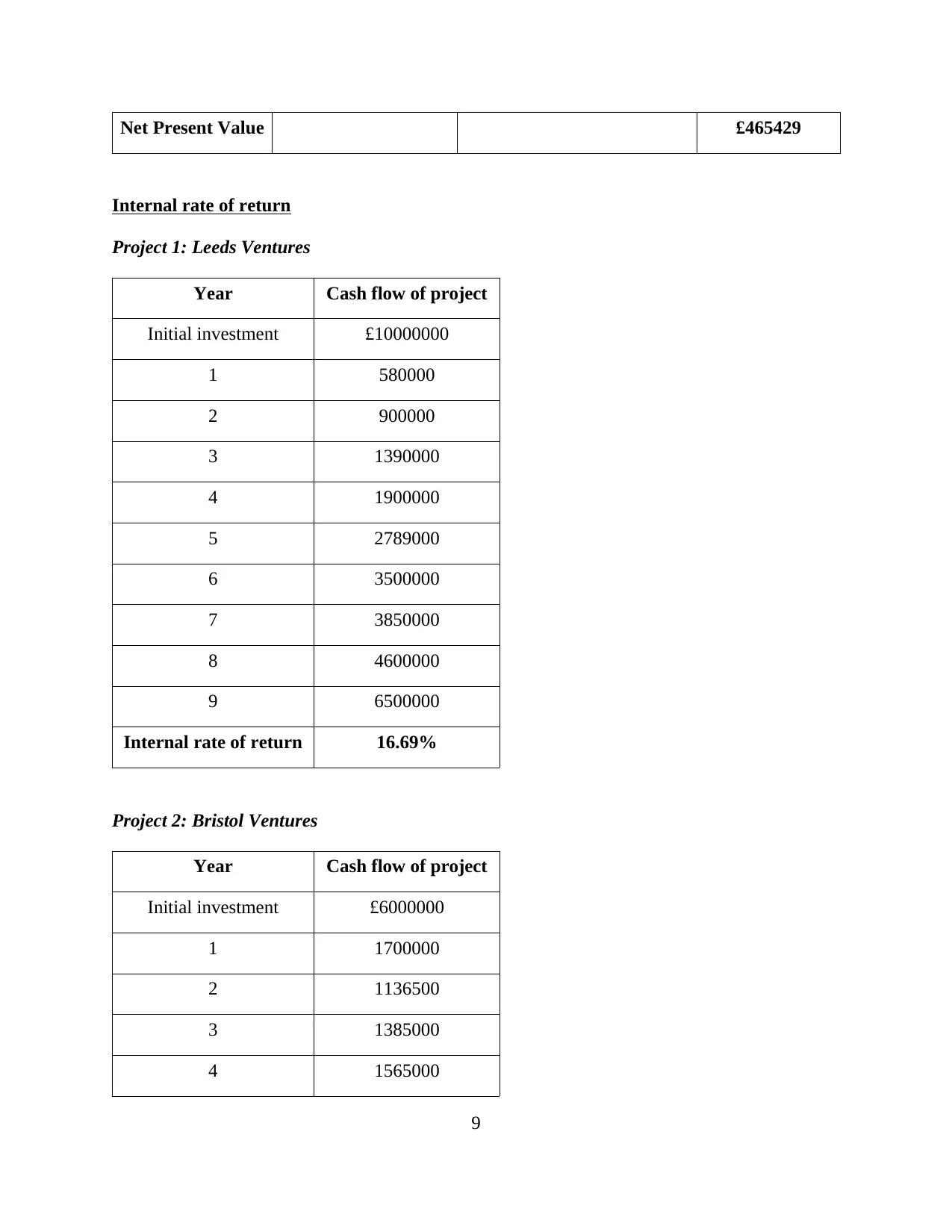

Net Present Value £465429

Internal rate of return

Project 1: Leeds Ventures

Year Cash flow of project

Initial investment £10000000

1 580000

2 900000

3 1390000

4 1900000

5 2789000

6 3500000

7 3850000

8 4600000

9 6500000

Internal rate of return 16.69%

Project 2: Bristol Ventures

Year Cash flow of project

Initial investment £6000000

1 1700000

2 1136500

3 1385000

4 1565000

9

Internal rate of return

Project 1: Leeds Ventures

Year Cash flow of project

Initial investment £10000000

1 580000

2 900000

3 1390000

4 1900000

5 2789000

6 3500000

7 3850000

8 4600000

9 6500000

Internal rate of return 16.69%

Project 2: Bristol Ventures

Year Cash flow of project

Initial investment £6000000

1 1700000

2 1136500

3 1385000

4 1565000

9

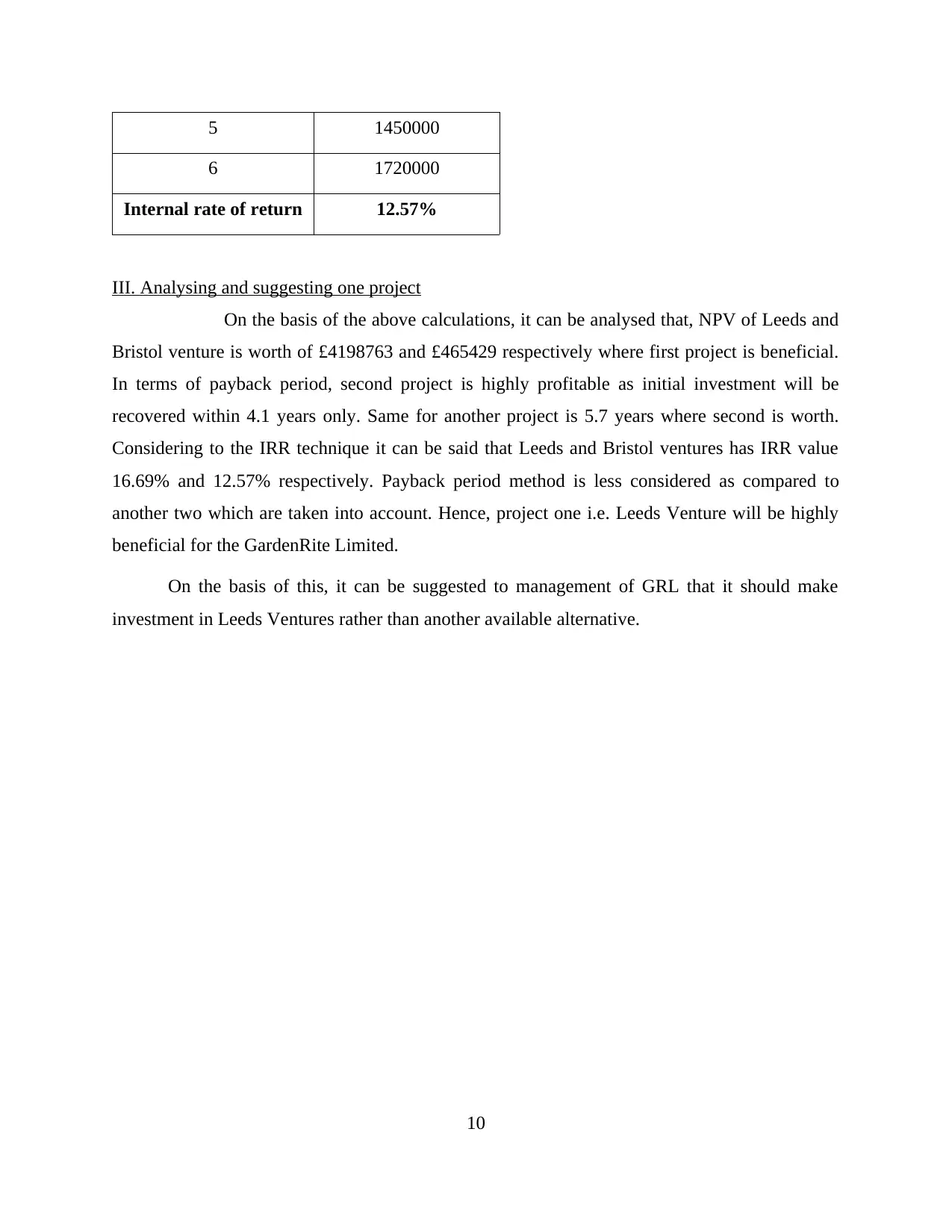

5 1450000

6 1720000

Internal rate of return 12.57%

III. Analysing and suggesting one project

On the basis of the above calculations, it can be analysed that, NPV of Leeds and

Bristol venture is worth of £4198763 and £465429 respectively where first project is beneficial.

In terms of payback period, second project is highly profitable as initial investment will be

recovered within 4.1 years only. Same for another project is 5.7 years where second is worth.

Considering to the IRR technique it can be said that Leeds and Bristol ventures has IRR value

16.69% and 12.57% respectively. Payback period method is less considered as compared to

another two which are taken into account. Hence, project one i.e. Leeds Venture will be highly

beneficial for the GardenRite Limited.

On the basis of this, it can be suggested to management of GRL that it should make

investment in Leeds Ventures rather than another available alternative.

10

6 1720000

Internal rate of return 12.57%

III. Analysing and suggesting one project

On the basis of the above calculations, it can be analysed that, NPV of Leeds and

Bristol venture is worth of £4198763 and £465429 respectively where first project is beneficial.

In terms of payback period, second project is highly profitable as initial investment will be

recovered within 4.1 years only. Same for another project is 5.7 years where second is worth.

Considering to the IRR technique it can be said that Leeds and Bristol ventures has IRR value

16.69% and 12.57% respectively. Payback period method is less considered as compared to

another two which are taken into account. Hence, project one i.e. Leeds Venture will be highly

beneficial for the GardenRite Limited.

On the basis of this, it can be suggested to management of GRL that it should make

investment in Leeds Ventures rather than another available alternative.

10

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 13

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.