Finance Report: Analysis of the Hospitality Industry in the UK

VerifiedAdded on 2020/02/03

|23

|6180

|453

Report

AI Summary

This report provides a comprehensive financial analysis of the hospitality industry, focusing on key aspects such as sources of finance, revenue generation, cost components, and inventory and cash management. It delves into various methods for increasing revenue, including differentiated products and services, promotions, and commissions. The report examines different components of cost, gross profit, and selling prices, offering insights into how to control stock and cash within a business. Furthermore, it discusses budgeting processes, variance analysis, and the assessment of trial balances. It also covers the calculation and analysis of financial ratios, along with recommendations for future management strategies. The report explores the classification of costs as fixed, variable, and semi-variable, while calculating contribution per customer and explaining the cost-volume-profit relationship. Finally, it offers justification for short-term management decisions based on financial data and analysis. This report is a student contribution available on Desklib, a platform offering AI-based study tools.

FINANCE IN THE

HOSPITALITY

INDUSTRY

HOSPITALITY

INDUSTRY

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

TABLE OF CONTENTS

INTRODUCTION...........................................................................................................................1

TASK 1............................................................................................................................................1

1.1 Sources of finance to raise fund in business.....................................................................1

1.2 Various methods of generating income............................................................................2

TASK 2............................................................................................................................................3

2.1 Different components of cost, gross profit and selling prices..........................................3

2.2 Ways by which stock and cash can be control in business...............................................5

TASK 3............................................................................................................................................7

3.3 Discussing the purpose and process of budgeting control ...............................................7

3.4 Analysis of variances .......................................................................................................8

TASK 4 ...........................................................................................................................................9

3.1 Assessing the source and structure of trial balance .........................................................9

3.2 Evaluating business accounts, adjustments and notes ...................................................10

4.1 Calculating and analysing ratios ....................................................................................12

Recommending appropriate future management strategies ................................................15

TASK 5.........................................................................................................................................16

5.1 Distinguishing cost as fixed, variable and semi-variable ..............................................16

5.2 Calculating contribution per customer and Explaining CVP relationship.....................17

5.3 Justifying short-term management decisions................................................................19

CONCLUSION..............................................................................................................................19

REFERENCES..............................................................................................................................20

INTRODUCTION...........................................................................................................................1

TASK 1............................................................................................................................................1

1.1 Sources of finance to raise fund in business.....................................................................1

1.2 Various methods of generating income............................................................................2

TASK 2............................................................................................................................................3

2.1 Different components of cost, gross profit and selling prices..........................................3

2.2 Ways by which stock and cash can be control in business...............................................5

TASK 3............................................................................................................................................7

3.3 Discussing the purpose and process of budgeting control ...............................................7

3.4 Analysis of variances .......................................................................................................8

TASK 4 ...........................................................................................................................................9

3.1 Assessing the source and structure of trial balance .........................................................9

3.2 Evaluating business accounts, adjustments and notes ...................................................10

4.1 Calculating and analysing ratios ....................................................................................12

Recommending appropriate future management strategies ................................................15

TASK 5.........................................................................................................................................16

5.1 Distinguishing cost as fixed, variable and semi-variable ..............................................16

5.2 Calculating contribution per customer and Explaining CVP relationship.....................17

5.3 Justifying short-term management decisions................................................................19

CONCLUSION..............................................................................................................................19

REFERENCES..............................................................................................................................20

INTRODUCTION

In the present times, hospitality sector of UK is growing with the very high pace in line with the

travel and tourism sector. Now, customers prefer to stay in the hotel which offers high quality

and luxurious accommodation services to the customers. Further, in the competitive business

arena business unit can survive more effectually only when it offers high-quality services. Along

with this, effectual management of financial resources is also highly required in the hospitality

sector to build and sustain a competitive edge over others. Hence, the company is required to

undertake several tools and techniques which aid in the profit margin of the firm. The present

report is based on different case situations which will describe the sources that business units of

service sector can use to meet the financial requirements. Further, it will also shed light on the

methods which ensure effective management of cash and inventory within the firm. Besides this,

the report will also develop an understanding of the concepts of variance and ratio analysis as

well as break-even point which in turn helps in making suitable business decisions.

TASK 1

1.1 Sources of finance to raise fund in business

Each and every organisation whether it is operating in manufacture or services industry wants to

expand the business. For this, capital is required which will be generated by the business entity

from various sources. As per the present scenario to raise fund worth £50,000 foe sole trader

company, different sources are available (Jones and et.al., 2016). The sources are internal as well

as external which are stated below:

Internal sources of finance: The firm raise fund from the business inside which are known as

internal sources. Various sources for increase financed from internally are such as follows: Retained profits: As per the source profit which remains after paying dividend amount as

well as interest is identified as retained earnings. The remaining profit is to be reused in

the business for increase capital and expand the firm. Sale of assets: Another internal source is the sale of assets where the management sell

those assets which are not used and unable to generate revenue. After selling the asset

whichever fund comes from a market that will be used to increase finance in the business.

1

In the present times, hospitality sector of UK is growing with the very high pace in line with the

travel and tourism sector. Now, customers prefer to stay in the hotel which offers high quality

and luxurious accommodation services to the customers. Further, in the competitive business

arena business unit can survive more effectually only when it offers high-quality services. Along

with this, effectual management of financial resources is also highly required in the hospitality

sector to build and sustain a competitive edge over others. Hence, the company is required to

undertake several tools and techniques which aid in the profit margin of the firm. The present

report is based on different case situations which will describe the sources that business units of

service sector can use to meet the financial requirements. Further, it will also shed light on the

methods which ensure effective management of cash and inventory within the firm. Besides this,

the report will also develop an understanding of the concepts of variance and ratio analysis as

well as break-even point which in turn helps in making suitable business decisions.

TASK 1

1.1 Sources of finance to raise fund in business

Each and every organisation whether it is operating in manufacture or services industry wants to

expand the business. For this, capital is required which will be generated by the business entity

from various sources. As per the present scenario to raise fund worth £50,000 foe sole trader

company, different sources are available (Jones and et.al., 2016). The sources are internal as well

as external which are stated below:

Internal sources of finance: The firm raise fund from the business inside which are known as

internal sources. Various sources for increase financed from internally are such as follows: Retained profits: As per the source profit which remains after paying dividend amount as

well as interest is identified as retained earnings. The remaining profit is to be reused in

the business for increase capital and expand the firm. Sale of assets: Another internal source is the sale of assets where the management sell

those assets which are not used and unable to generate revenue. After selling the asset

whichever fund comes from a market that will be used to increase finance in the business.

1

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Personal savings: Here the owner uses its savings which are done in its personal life.

There is not any cost bear by the management to raise fund by this source (Liu and

Pennington-Gray, 2015).

External sources of finance: Further, there are various ways which are used to raise fund from

the external market are known as external sources which are given as below: Equity: Most widely used external source is equity financing in which the firm issue

equity shares in the market with the help of stock market. The shares are purchased by

shareholders and the amount used in the firm for business expansion, for that it has to

give dividend amount to shareholders. Bank loan: Further, as per the source the firm take a loan from various commercial banks

and use in the business. For this, it has to pay interest amount as a cost of finance. Venture capital: It is one type of external sources which allows manufacture and services

industry businesses to provide finance (Slåtten and Mehmetoglu, 2015). It imposes

charges on the firm regarding stake of the overall organisation. Leasing: As per the sources the business gives some part of the asset on lease to another

party and then raise the finance to expansion of the company.

Financial institutions: There are various institutions which provide finance to the firm

for business expansion. Several financial institutions are such as commercial banks, non-

commercial banks, traditional financial agencies, merchant banks, etc.

1.2 Various methods of generating income

There are various ways by which a restaurant can increase revenue and decrease costs,

which are stated below: Provide differentiate products and services: When the restaurant make and offer

products as well services different from the rivalry firms then number of customers will

be attracted (30 Ways Hotels Can Increase Revenues, Decrease Costs and Boost

Booking, 2013). This leads to generating and increase sales as well as the profitability of

the restaurant.

2

There is not any cost bear by the management to raise fund by this source (Liu and

Pennington-Gray, 2015).

External sources of finance: Further, there are various ways which are used to raise fund from

the external market are known as external sources which are given as below: Equity: Most widely used external source is equity financing in which the firm issue

equity shares in the market with the help of stock market. The shares are purchased by

shareholders and the amount used in the firm for business expansion, for that it has to

give dividend amount to shareholders. Bank loan: Further, as per the source the firm take a loan from various commercial banks

and use in the business. For this, it has to pay interest amount as a cost of finance. Venture capital: It is one type of external sources which allows manufacture and services

industry businesses to provide finance (Slåtten and Mehmetoglu, 2015). It imposes

charges on the firm regarding stake of the overall organisation. Leasing: As per the sources the business gives some part of the asset on lease to another

party and then raise the finance to expansion of the company.

Financial institutions: There are various institutions which provide finance to the firm

for business expansion. Several financial institutions are such as commercial banks, non-

commercial banks, traditional financial agencies, merchant banks, etc.

1.2 Various methods of generating income

There are various ways by which a restaurant can increase revenue and decrease costs,

which are stated below: Provide differentiate products and services: When the restaurant make and offer

products as well services different from the rivalry firms then number of customers will

be attracted (30 Ways Hotels Can Increase Revenues, Decrease Costs and Boost

Booking, 2013). This leads to generating and increase sales as well as the profitability of

the restaurant.

2

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Offer skims, and discounts: Apart from above ways the restaurant should allow to

consumers after providing various schemes as well as discounting offers. These types of

services will help to firm to attract a number of customers which lead to earn higher sales

and revenue (Torres, Singh and Robertson-Ring, 2015). Promotional activities: These types of activities and strategies increase awareness among

the people by which they attract to consumers its food items and services. It leads to

increase sales as well as profitability of the restaurant. Commissions: As per this source the restaurant can generate income by contracting with

travel and tourism companies. In this the restaurant provide consumers to the tour

company for staying and takes commission from respective tour firm. By this it is able to

generate income for the restaurant.

Sub letting: By providing very small part of the restaurant to stall such as cuisine,

Chinese etc. it can generate income. Provide small part is known as sub letting of the

company which helps to increase income as well as profitability of the restaurant.

TASK 2

2.1 Different components of cost, gross profit and selling prices

The cost of production, prices of products and services as well as profit, these all are very

sensitive and important factor of the organisation. Every firm has the aim to maximise profit and

financial health as well in the industry. In the present case, there is a firm Marks & Spencer is

offering its goods and services worldwide. There are several elements of cost, gross profit as

well prices are given as below:

Cost: It is a sensitive component of the business, and every company needs to manage

and reduce the cost of production which lead to enhance profitability. There are various

components of the cost are such as follows:

Direct costs: Those costs which are directly incurred in the production process are

known as direct costs. In the direct costs basically two categories included in the Marks and

Spencer while selling retail goods and services. Further, the two types are like as related to the

labour as well as material which are explained below:

3

consumers after providing various schemes as well as discounting offers. These types of

services will help to firm to attract a number of customers which lead to earn higher sales

and revenue (Torres, Singh and Robertson-Ring, 2015). Promotional activities: These types of activities and strategies increase awareness among

the people by which they attract to consumers its food items and services. It leads to

increase sales as well as profitability of the restaurant. Commissions: As per this source the restaurant can generate income by contracting with

travel and tourism companies. In this the restaurant provide consumers to the tour

company for staying and takes commission from respective tour firm. By this it is able to

generate income for the restaurant.

Sub letting: By providing very small part of the restaurant to stall such as cuisine,

Chinese etc. it can generate income. Provide small part is known as sub letting of the

company which helps to increase income as well as profitability of the restaurant.

TASK 2

2.1 Different components of cost, gross profit and selling prices

The cost of production, prices of products and services as well as profit, these all are very

sensitive and important factor of the organisation. Every firm has the aim to maximise profit and

financial health as well in the industry. In the present case, there is a firm Marks & Spencer is

offering its goods and services worldwide. There are several elements of cost, gross profit as

well prices are given as below:

Cost: It is a sensitive component of the business, and every company needs to manage

and reduce the cost of production which lead to enhance profitability. There are various

components of the cost are such as follows:

Direct costs: Those costs which are directly incurred in the production process are

known as direct costs. In the direct costs basically two categories included in the Marks and

Spencer while selling retail goods and services. Further, the two types are like as related to the

labour as well as material which are explained below:

3

Material costs: Material cost is an important component of the firm due to raw material

is very necessary for producing goods and services (Dogru and Sirakaya-Turk, 2016).

The cost is included in total cost of production which leads to decide the price of

products. With reference to the Marks and Spencer company: the material costs are such

as: purchasing goods and services for further selling, buying required materials, cost of

inventory, cost of products sold etc. Labour cost: To produce or to convert raw material into finished goods there is

manpower is required and a firm has to pay a cost to them. The cost is known as a labour

cost of products. For example: wages to staff of retail shop, online service provider

labours etc. Further, generally four categories of the labour costs are incurred in the

Marks and Spencer company which are: Variable labour, Fixed, Direct as well as the

Indirect labour expenses.

Indirect costs: In the production process expenses which are not directly consists,

identified as an indirect cost. Numerous indirect costs are given as below: Packaging expenses: The M&S sell goods after packing to them, without packing it not

sale into the market. Hence, another element is expenses which are incurred in the pack

the finished goods. For example: packing a particular food item such as to pack chocolate

wrapper is required which is a cost for the firm. Selling and distribution cost: Further, to advertise, promoting and selling the goods in

market cost is to be bear by the firm which is included in total cost. In order to sell the

products business gives advertisement using different sources for example newspapers,

social media, templates etc. In this firm has to give money to the social media, newspaper

agencies etc. which is expense of selling and distribution.

Overheads: As per the element there is various indirect cost are included in total cost.

The indirect costs are such as indirect labour and material, utility expenses, interest,

depreciation on assets, etc. (Mugassa, 2015). As per the overhead expenses, various costs

incurred in the Marks and Spencer entity are such as rental expenditures of plant and

property, electricity bills, accountants salary, human resource expenses, selling and

distribution, interest amount of debt, other administration costs etc.

4

is very necessary for producing goods and services (Dogru and Sirakaya-Turk, 2016).

The cost is included in total cost of production which leads to decide the price of

products. With reference to the Marks and Spencer company: the material costs are such

as: purchasing goods and services for further selling, buying required materials, cost of

inventory, cost of products sold etc. Labour cost: To produce or to convert raw material into finished goods there is

manpower is required and a firm has to pay a cost to them. The cost is known as a labour

cost of products. For example: wages to staff of retail shop, online service provider

labours etc. Further, generally four categories of the labour costs are incurred in the

Marks and Spencer company which are: Variable labour, Fixed, Direct as well as the

Indirect labour expenses.

Indirect costs: In the production process expenses which are not directly consists,

identified as an indirect cost. Numerous indirect costs are given as below: Packaging expenses: The M&S sell goods after packing to them, without packing it not

sale into the market. Hence, another element is expenses which are incurred in the pack

the finished goods. For example: packing a particular food item such as to pack chocolate

wrapper is required which is a cost for the firm. Selling and distribution cost: Further, to advertise, promoting and selling the goods in

market cost is to be bear by the firm which is included in total cost. In order to sell the

products business gives advertisement using different sources for example newspapers,

social media, templates etc. In this firm has to give money to the social media, newspaper

agencies etc. which is expense of selling and distribution.

Overheads: As per the element there is various indirect cost are included in total cost.

The indirect costs are such as indirect labour and material, utility expenses, interest,

depreciation on assets, etc. (Mugassa, 2015). As per the overhead expenses, various costs

incurred in the Marks and Spencer entity are such as rental expenditures of plant and

property, electricity bills, accountants salary, human resource expenses, selling and

distribution, interest amount of debt, other administration costs etc.

4

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Gross profit: It is a type of profit of the firm where the cost of goods sold is deducted

from total revenue of the organisation. Further, management keeps a record of the financial

transactions then, and only gross profit can be determined. Hence, main elements of gross profit

are such as below:

Cost of goods sold (COGS): It is the base of calculating the gross profit which is

deducted from the revenue generated by the company. Higher the COGS lead to reduce

gross profit at the end of year.

Sales or Revenue: Apart from this, the basic component which is taken into

consideration while assessing is gross profit is sales. When company generates more

amount of sales and revenue at the end of year, then gross profit will be also in the

increasing trend.

Management of the firm: Moreover, the last element which is taken into consideration

at the time of computing gross yield is the management of M&S business enterprise.

Selling price: Price of products and services is to be derive using total cost, market trend,

the financial position of the firm, etc. In the present case M&S can derive price after using its

important components which are as follows:

Market trend: In this element the company use trend and situation of the market and

industry. In the market if demand is higher, then firm will charge high selling price and in

case of lower demand, it will charge very low amount of price.

Total cost of production: Other aspect includes is cost which is incurred to produce and

manufacture the products and services. Price will be charge in the same direction of

costing like high cost of production leads to determine higher prices of the goods (Morris

and Goldsworthy, 2016).

Price of competitors: If the rivals take more price, then M&S will be derive lower price

for attracting more customers. Moreover, selling price determination is depends on the

competitors as well.

Goodwill or image of the firm: Further, brand image of the company is also considered

while determining the selling price of its products and services.

5

from total revenue of the organisation. Further, management keeps a record of the financial

transactions then, and only gross profit can be determined. Hence, main elements of gross profit

are such as below:

Cost of goods sold (COGS): It is the base of calculating the gross profit which is

deducted from the revenue generated by the company. Higher the COGS lead to reduce

gross profit at the end of year.

Sales or Revenue: Apart from this, the basic component which is taken into

consideration while assessing is gross profit is sales. When company generates more

amount of sales and revenue at the end of year, then gross profit will be also in the

increasing trend.

Management of the firm: Moreover, the last element which is taken into consideration

at the time of computing gross yield is the management of M&S business enterprise.

Selling price: Price of products and services is to be derive using total cost, market trend,

the financial position of the firm, etc. In the present case M&S can derive price after using its

important components which are as follows:

Market trend: In this element the company use trend and situation of the market and

industry. In the market if demand is higher, then firm will charge high selling price and in

case of lower demand, it will charge very low amount of price.

Total cost of production: Other aspect includes is cost which is incurred to produce and

manufacture the products and services. Price will be charge in the same direction of

costing like high cost of production leads to determine higher prices of the goods (Morris

and Goldsworthy, 2016).

Price of competitors: If the rivals take more price, then M&S will be derive lower price

for attracting more customers. Moreover, selling price determination is depends on the

competitors as well.

Goodwill or image of the firm: Further, brand image of the company is also considered

while determining the selling price of its products and services.

5

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

The quality of products: When quality of the services and goods are provided at the

higher level, then price will be determined in more amount.

2.2 Ways by which stock and cash can be control in business

To make the firm profitable, it is necessary to manage and control cost, stock as well as

cash balance of the firm (Li, Wang and 2015). It can be managed by various strategies or

methods which are shown below:

Methods of controlling stock in the business: Just-in-time method: It a technique where the company can reduce wastage or damage

products and enhance the efficiency of the company. Further, it allows selling the goods

at the right time with right quantity. Hence, it is an effective way to manage and control

over the stock of M&S organisation. On the other hand it affects smooth functioning of

the organisation. Fixed re-order stock level: As per the method, the stock is to order for purchasing after

selling out previous products. By this extra inventory will be not there and company able

to sell all the products in the proper manner which lead to control stock of the firm.

However, the management has to appoint person who pay attention on the specific

criteria which lead to increase cost of the production in company.

Economic Order Quantity: Another method of inventory control is EOQ where the

company is able to control over the stock. Further, it is beneficial in order to reduce

holding as well as ordering cost which lead to minimize overall cost of production.

However, it can be critically evaluated that it is based on formula which is complicated to

calculate and typical to control the inventory sometimes.

Methods of cash controlling in the business: Hire the right employee: When the firm recruit appropriate and skilled employee then

with the help of their efficiency stock as well as cash both are managed. Employees are

the key asset of the firm, so it is necessary to hire skilled employees in the firm. Further,

in this case the company has to pay hire wages or salary to the skilled employees which

lead to enhance cost and reduce profit as well.

6

higher level, then price will be determined in more amount.

2.2 Ways by which stock and cash can be control in business

To make the firm profitable, it is necessary to manage and control cost, stock as well as

cash balance of the firm (Li, Wang and 2015). It can be managed by various strategies or

methods which are shown below:

Methods of controlling stock in the business: Just-in-time method: It a technique where the company can reduce wastage or damage

products and enhance the efficiency of the company. Further, it allows selling the goods

at the right time with right quantity. Hence, it is an effective way to manage and control

over the stock of M&S organisation. On the other hand it affects smooth functioning of

the organisation. Fixed re-order stock level: As per the method, the stock is to order for purchasing after

selling out previous products. By this extra inventory will be not there and company able

to sell all the products in the proper manner which lead to control stock of the firm.

However, the management has to appoint person who pay attention on the specific

criteria which lead to increase cost of the production in company.

Economic Order Quantity: Another method of inventory control is EOQ where the

company is able to control over the stock. Further, it is beneficial in order to reduce

holding as well as ordering cost which lead to minimize overall cost of production.

However, it can be critically evaluated that it is based on formula which is complicated to

calculate and typical to control the inventory sometimes.

Methods of cash controlling in the business: Hire the right employee: When the firm recruit appropriate and skilled employee then

with the help of their efficiency stock as well as cash both are managed. Employees are

the key asset of the firm, so it is necessary to hire skilled employees in the firm. Further,

in this case the company has to pay hire wages or salary to the skilled employees which

lead to enhance cost and reduce profit as well.

6

Proper record of transactions: To record and analyse the financial transactions is very

necessary for the firm. It helps to know financial position, as well as management, is able

to know that where expenses are increases (Jackson and Singh, 2015). It is a widely used

method to control over the cash and increase the profitability of respective organisation in

the industry. Moreover, here the organisation has to appoint the specialist and use

softwares where it has to pay high amount which is a limitation of the method.

Monitoring and Audit system: By monitoring and checking the accounting transactions

the management able to determine that in which costs is increases. The point where firm

is having high cost then it will take corrective actions which lead to decrease cost and

increase cash balance. However, in auditing process the company has to hire auditor

which are taking higher fees.

TASK 3

3.3 Discussing the purpose and process of budgeting control

Budgetary control may be defined as a process where actual financial results are

compared with the standard measures. Hence, by employing such process business unit can find

out the deviations which take place in financial aspects. In this way, by taking corrective

measure within the suitable time frame company can attain success.

Purpose of budgeting control

Elimination of waste and the heavy increase in the profitability aspect is one of the main

objectives of the business organisation. Moreover, with the motive to create an effectual image in

the mind of higher management personnel make an effort to utilise financial resources according

to the predetermined plan (Assaf and Josiassen, 2016). In addition to this, by practising

budgetary control system company can make the proper anticipation of capital expenses for the

near future.

Process of budgeting control Budget framing: In the very first step manager frames budget by assessing the financial

needs and requirements of each department. Circulation of the budget: At this stage, manager circulates budget at each level of the

department to provide deeper insight to personnel about spending level.

7

necessary for the firm. It helps to know financial position, as well as management, is able

to know that where expenses are increases (Jackson and Singh, 2015). It is a widely used

method to control over the cash and increase the profitability of respective organisation in

the industry. Moreover, here the organisation has to appoint the specialist and use

softwares where it has to pay high amount which is a limitation of the method.

Monitoring and Audit system: By monitoring and checking the accounting transactions

the management able to determine that in which costs is increases. The point where firm

is having high cost then it will take corrective actions which lead to decrease cost and

increase cash balance. However, in auditing process the company has to hire auditor

which are taking higher fees.

TASK 3

3.3 Discussing the purpose and process of budgeting control

Budgetary control may be defined as a process where actual financial results are

compared with the standard measures. Hence, by employing such process business unit can find

out the deviations which take place in financial aspects. In this way, by taking corrective

measure within the suitable time frame company can attain success.

Purpose of budgeting control

Elimination of waste and the heavy increase in the profitability aspect is one of the main

objectives of the business organisation. Moreover, with the motive to create an effectual image in

the mind of higher management personnel make an effort to utilise financial resources according

to the predetermined plan (Assaf and Josiassen, 2016). In addition to this, by practising

budgetary control system company can make the proper anticipation of capital expenses for the

near future.

Process of budgeting control Budget framing: In the very first step manager frames budget by assessing the financial

needs and requirements of each department. Circulation of the budget: At this stage, manager circulates budget at each level of the

department to provide deeper insight to personnel about spending level.

7

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Making comparisons: Once, circulation of the budget has been made after that company

makes a comparison of the actual performance with standard amount. Through this,

deviations can be assessed by the firm in an effectual way which takes place in the

respective department such as finance, marketing, etc. (Fong and et.al., 2016).

Monitoring and control: In the last stage, the manager makes an assessment of the

causes of deviations and thereby takes corrective action business unit can take corrective

measure or action within the suitable time frame.

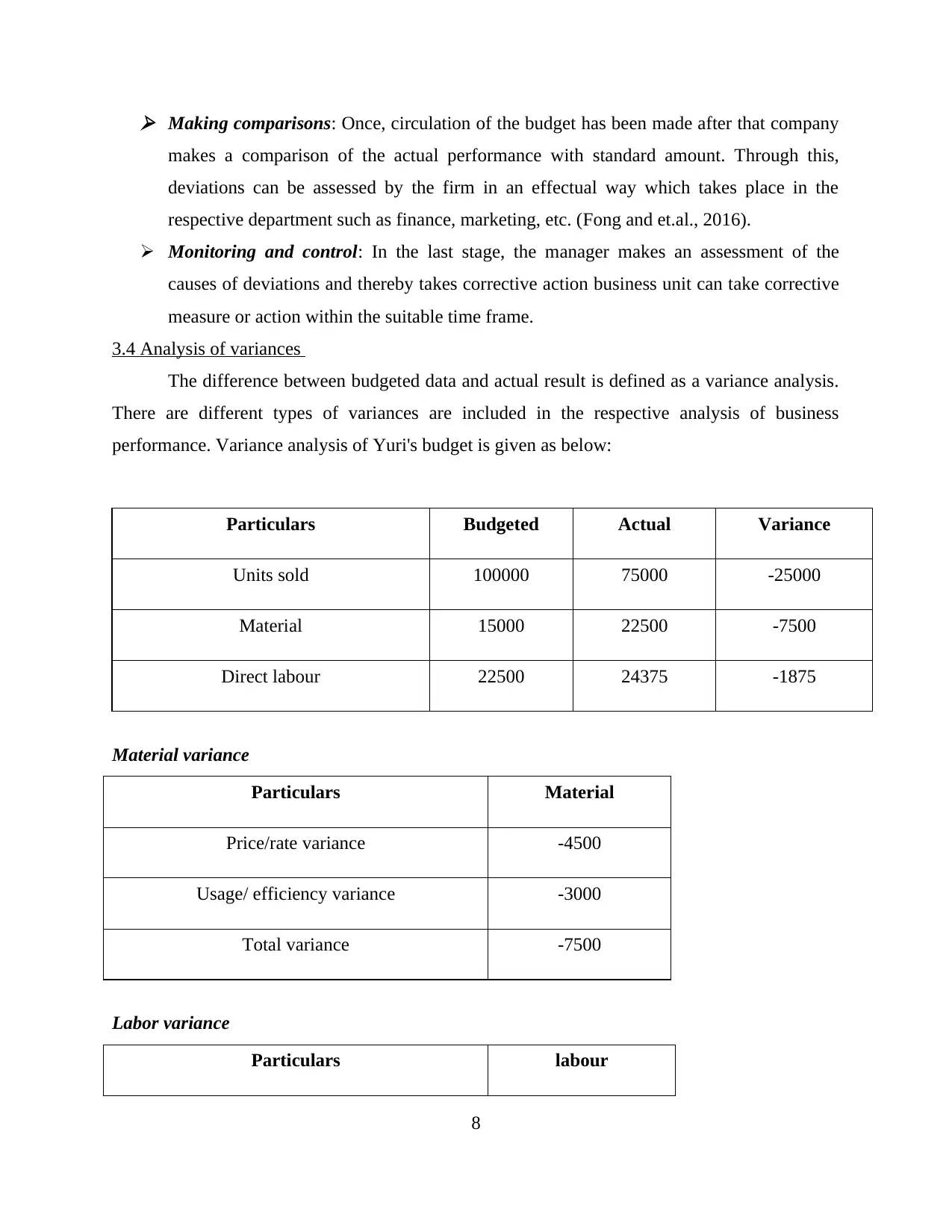

3.4 Analysis of variances

The difference between budgeted data and actual result is defined as a variance analysis.

There are different types of variances are included in the respective analysis of business

performance. Variance analysis of Yuri's budget is given as below:

Particulars Budgeted Actual Variance

Units sold 100000 75000 -25000

Material 15000 22500 -7500

Direct labour 22500 24375 -1875

Material variance

Particulars Material

Price/rate variance -4500

Usage/ efficiency variance -3000

Total variance -7500

Labor variance

Particulars labour

8

makes a comparison of the actual performance with standard amount. Through this,

deviations can be assessed by the firm in an effectual way which takes place in the

respective department such as finance, marketing, etc. (Fong and et.al., 2016).

Monitoring and control: In the last stage, the manager makes an assessment of the

causes of deviations and thereby takes corrective action business unit can take corrective

measure or action within the suitable time frame.

3.4 Analysis of variances

The difference between budgeted data and actual result is defined as a variance analysis.

There are different types of variances are included in the respective analysis of business

performance. Variance analysis of Yuri's budget is given as below:

Particulars Budgeted Actual Variance

Units sold 100000 75000 -25000

Material 15000 22500 -7500

Direct labour 22500 24375 -1875

Material variance

Particulars Material

Price/rate variance -4500

Usage/ efficiency variance -3000

Total variance -7500

Labor variance

Particulars labour

8

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Price/rate variance 3750

Usage/ efficiency variance -5625

Total variance -1875

From the above-mentioned table of variance analysis, it can be interpreted that the Yuri is

producing less number of units as per the expected units. Further, material variances as such as

prices and usage are decreasing due to increase prices as well as efficiency to produce goods and

services. Material variance, as well as labour variance both, is unfavourable for the firm that is -

7500 and -1875 respectively. It can be said that the firm has not an appropriate strategy to meet

its goals and objectives.

From the above table it can be assessed that company it is not able to sell the units as per

the budgeted data as well as material and direct labour is also unfavourable for the firm. Here the

management is not utilizes its raw material in effective manner and labours are not more efficient

in order to meet with expected units. Here direct labour and material variances are -1875 and -

7500 respectively. To overcome the situation it can be suggested that the management should use

effective marketing strategies to attract more number of customers which lead to increase sales

as well as units sold in the company. Further, it has to use the potential raw materials in proper

manner by which wastage will reduce and material used in appropriate way.

Moreover, as per the material variance of Yuri's budget, due to increasing prices of

services the price/rate variance is unfavourable for the company. Due to increasing wastage and

damage products or services material efficiency variance is adverse for the firm. In order to

eliminate the adverse situation the company needs to use total quality management and six sigma

approaches by which damage products will decrease and usage variance get increase. Further,

according to labour variance its efficiency variance is not achieved due to labour are not

productive and efficient for generating sales. It can be recommended that the company should

provide better training to employees which lead to increase skills and efficiencies of them.

9

Usage/ efficiency variance -5625

Total variance -1875

From the above-mentioned table of variance analysis, it can be interpreted that the Yuri is

producing less number of units as per the expected units. Further, material variances as such as

prices and usage are decreasing due to increase prices as well as efficiency to produce goods and

services. Material variance, as well as labour variance both, is unfavourable for the firm that is -

7500 and -1875 respectively. It can be said that the firm has not an appropriate strategy to meet

its goals and objectives.

From the above table it can be assessed that company it is not able to sell the units as per

the budgeted data as well as material and direct labour is also unfavourable for the firm. Here the

management is not utilizes its raw material in effective manner and labours are not more efficient

in order to meet with expected units. Here direct labour and material variances are -1875 and -

7500 respectively. To overcome the situation it can be suggested that the management should use

effective marketing strategies to attract more number of customers which lead to increase sales

as well as units sold in the company. Further, it has to use the potential raw materials in proper

manner by which wastage will reduce and material used in appropriate way.

Moreover, as per the material variance of Yuri's budget, due to increasing prices of

services the price/rate variance is unfavourable for the company. Due to increasing wastage and

damage products or services material efficiency variance is adverse for the firm. In order to

eliminate the adverse situation the company needs to use total quality management and six sigma

approaches by which damage products will decrease and usage variance get increase. Further,

according to labour variance its efficiency variance is not achieved due to labour are not

productive and efficient for generating sales. It can be recommended that the company should

provide better training to employees which lead to increase skills and efficiencies of them.

9

TASK 4

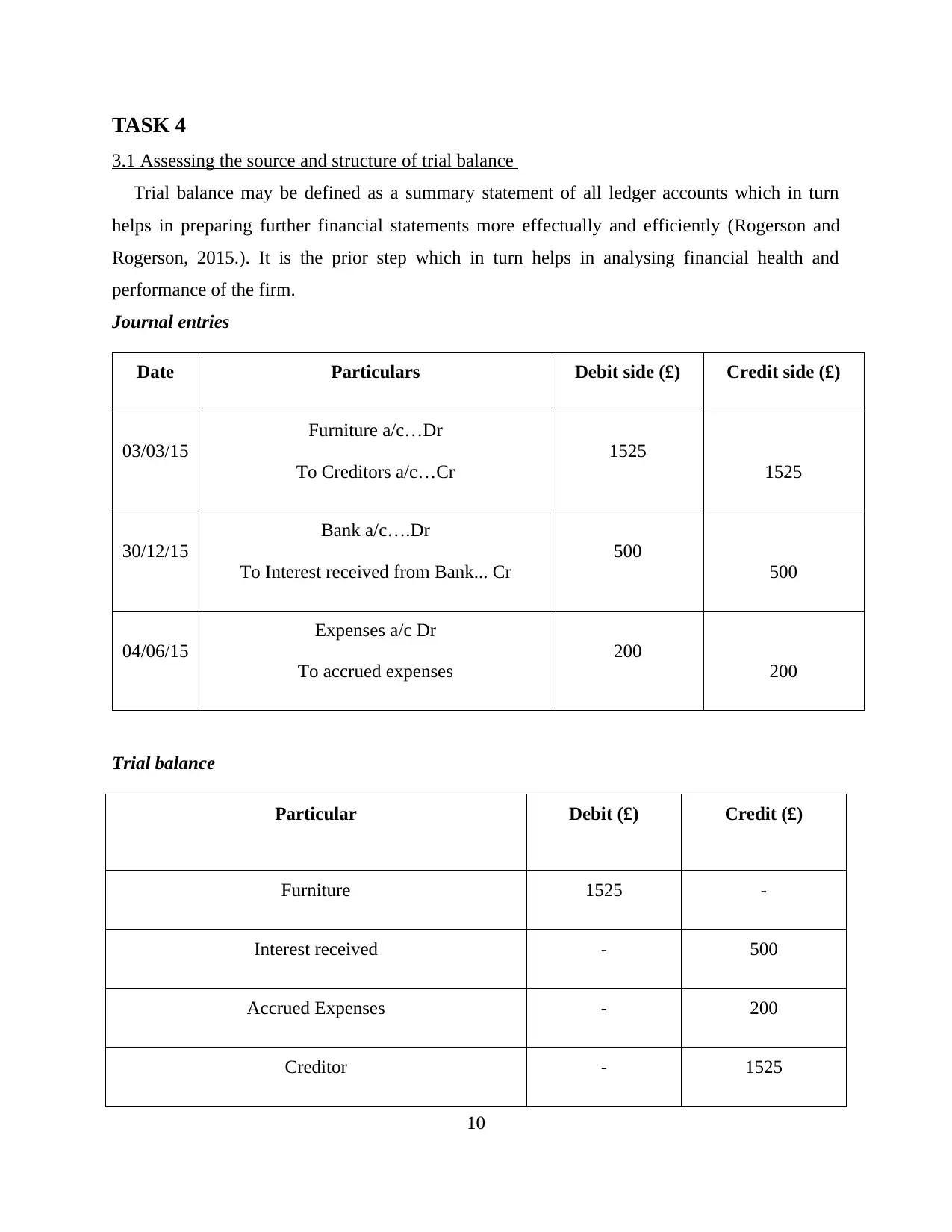

3.1 Assessing the source and structure of trial balance

Trial balance may be defined as a summary statement of all ledger accounts which in turn

helps in preparing further financial statements more effectually and efficiently (Rogerson and

Rogerson, 2015.). It is the prior step which in turn helps in analysing financial health and

performance of the firm.

Journal entries

Date Particulars Debit side (£) Credit side (£)

03/03/15

Furniture a/c…Dr

To Creditors a/c…Cr

1525

1525

30/12/15

Bank a/c….Dr

To Interest received from Bank... Cr

500

500

04/06/15

Expenses a/c Dr

To accrued expenses

200

200

Trial balance

Particular Debit (£) Credit (£)

Furniture 1525 -

Interest received - 500

Accrued Expenses - 200

Creditor - 1525

10

3.1 Assessing the source and structure of trial balance

Trial balance may be defined as a summary statement of all ledger accounts which in turn

helps in preparing further financial statements more effectually and efficiently (Rogerson and

Rogerson, 2015.). It is the prior step which in turn helps in analysing financial health and

performance of the firm.

Journal entries

Date Particulars Debit side (£) Credit side (£)

03/03/15

Furniture a/c…Dr

To Creditors a/c…Cr

1525

1525

30/12/15

Bank a/c….Dr

To Interest received from Bank... Cr

500

500

04/06/15

Expenses a/c Dr

To accrued expenses

200

200

Trial balance

Particular Debit (£) Credit (£)

Furniture 1525 -

Interest received - 500

Accrued Expenses - 200

Creditor - 1525

10

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 23

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.