Financial Analysis and Recommendations for Vector Limited

VerifiedAdded on 2020/04/01

|10

|1690

|53

Report

AI Summary

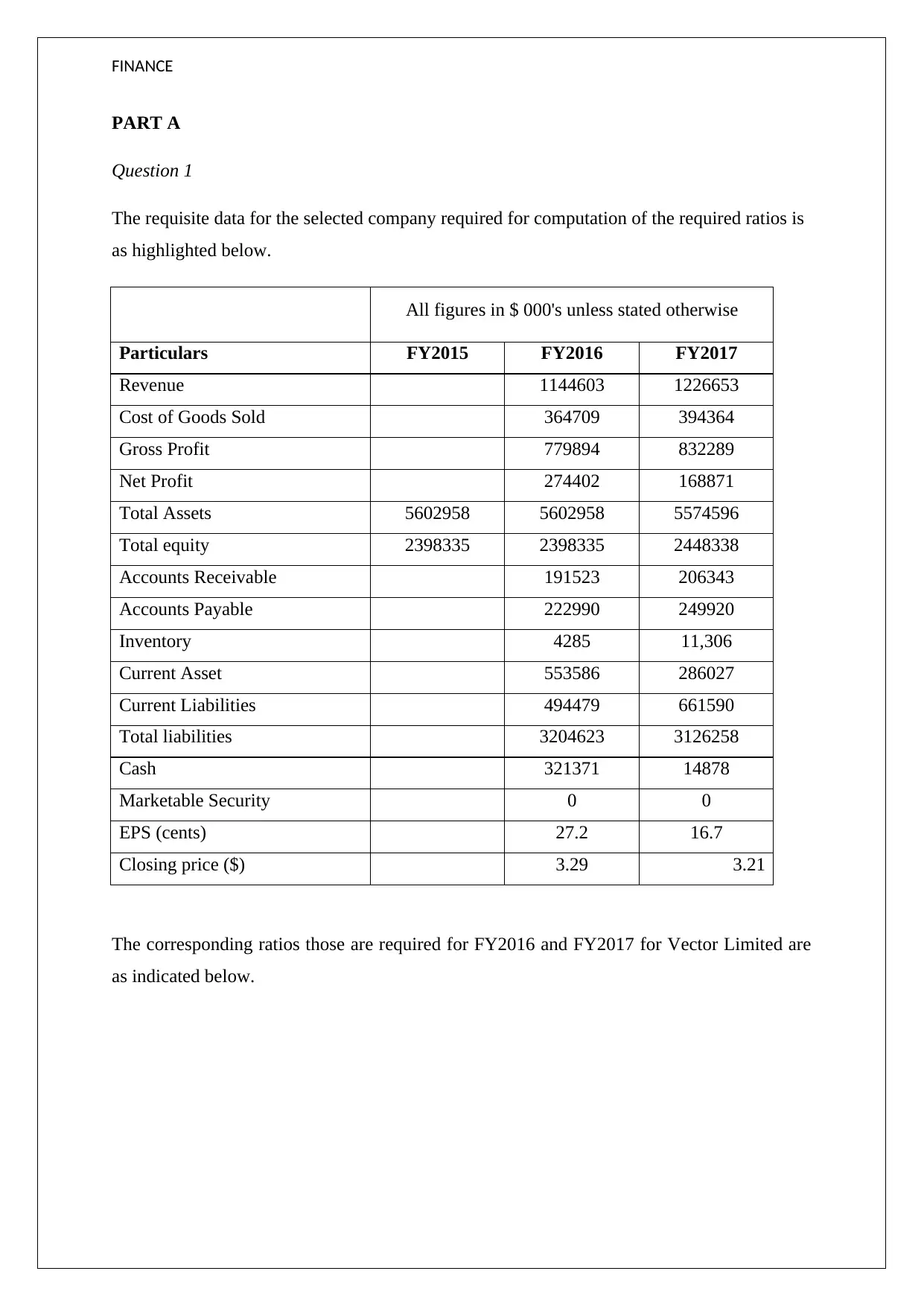

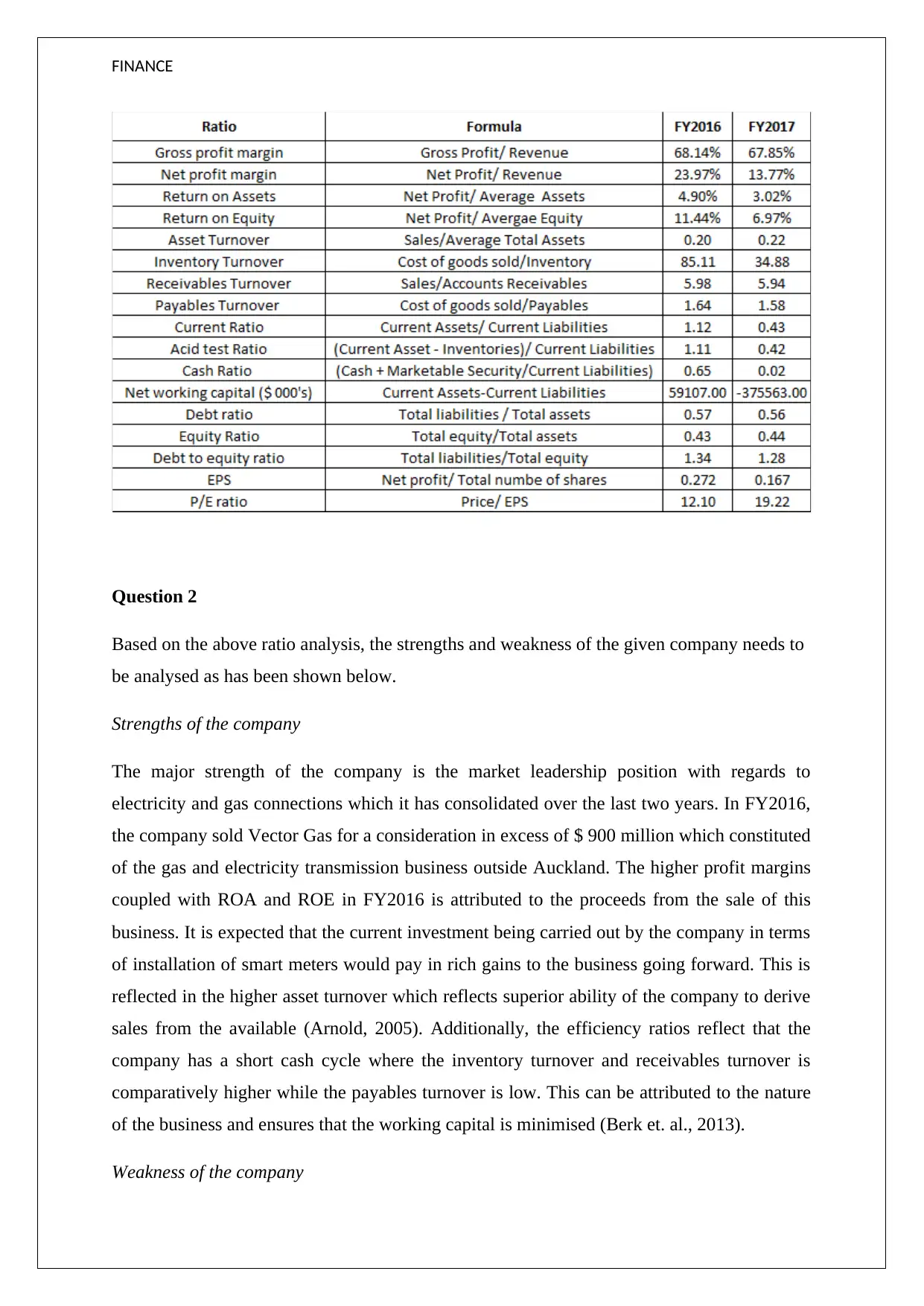

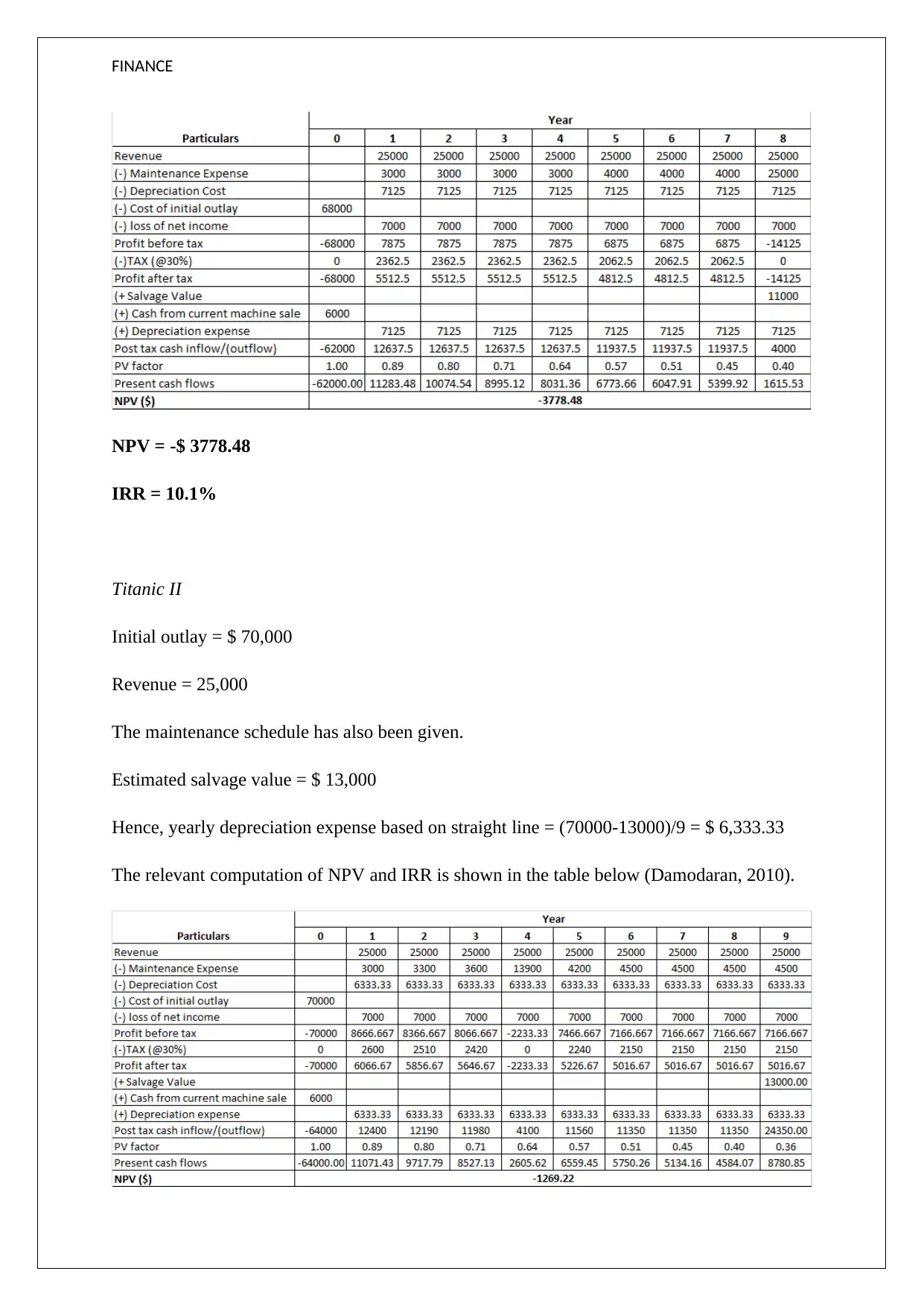

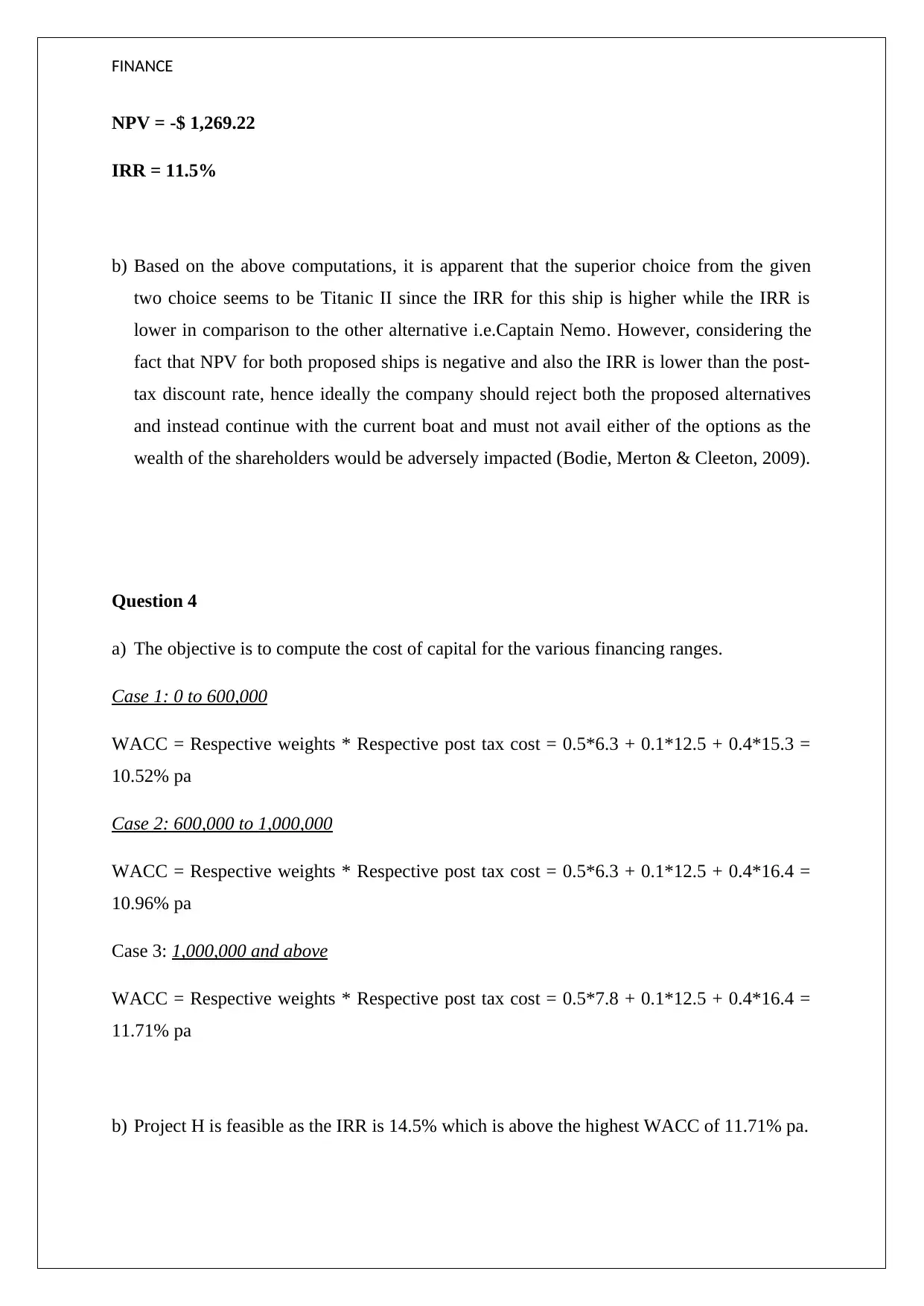

This finance report presents a comprehensive analysis of Vector Limited's financial performance, covering key financial ratios, including profitability, liquidity, and solvency. It evaluates the company's strengths and weaknesses, focusing on its market position, efficiency, and liquidity challenges. The report also assesses investment proposals using Internal Rate of Return (IRR) and Net Present Value (NPV) calculations for two boat projects, recommending rejection of both. Furthermore, it determines the Weighted Average Cost of Capital (WACC) for different financing ranges and evaluates the feasibility of various projects based on their IRRs. The report concludes with strategic recommendations for Vector Limited, emphasizing the need to improve short-term liquidity, manage balance sheet leverage, and be conservative with infrastructure investments, supported by references to financial management literature.

1 out of 10

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.