Finance & Reporting Online Exam Solution: Budgeting, Goodwill, Ratios

VerifiedAdded on 2023/06/15

|16

|3196

|235

Homework Assignment

AI Summary

This document provides a detailed solution to an online exam in Finance and Financial Reporting. It addresses the impact of COVID-19 on organizational finance, covering topics such as budgeting, goodwill calculation (including a numerical example), ratio analysis with interpretations, and methods of raising finance. The solution includes an income statement, corporation tax calculation, and a statement of financial position. Furthermore, it calculates and interprets key financial ratios like gross profit margin, operating profit margin, trade receivable days, and trade payable days. Finally, the document includes a Net Present Value (NPV) calculation for project evaluation. Desklib offers similar solved assignments and study resources for students.

ONLINE EXAM FINANCE

AND FINANCIAL

REPORTING

AND FINANCIAL

REPORTING

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

TABLE OF CONTENTS

SECTION A.....................................................................................................................................1

SECTION B.....................................................................................................................................1

Question B1.................................................................................................................................1

Question B2.................................................................................................................................2

Question B3.................................................................................................................................3

Question B4 ................................................................................................................................3

SECTION C.....................................................................................................................................4

1. .................................................................................................................................................4

2...................................................................................................................................................5

3...................................................................................................................................................5

4...................................................................................................................................................6

5...................................................................................................................................................7

SECTION D.....................................................................................................................................8

1...................................................................................................................................................8

2.................................................................................................................................................10

3.................................................................................................................................................11

4................................................................................................................................................11

REFERENCES..............................................................................................................................12

SECTION A.....................................................................................................................................1

SECTION B.....................................................................................................................................1

Question B1.................................................................................................................................1

Question B2.................................................................................................................................2

Question B3.................................................................................................................................3

Question B4 ................................................................................................................................3

SECTION C.....................................................................................................................................4

1. .................................................................................................................................................4

2...................................................................................................................................................5

3...................................................................................................................................................5

4...................................................................................................................................................6

5...................................................................................................................................................7

SECTION D.....................................................................................................................................8

1...................................................................................................................................................8

2.................................................................................................................................................10

3.................................................................................................................................................11

4................................................................................................................................................11

REFERENCES..............................................................................................................................12

SECTION A

The COVID-19 is the most challenging pandemic for every organization, which makes

them to rethink about their business and for survival. This pandemic has the great impact on the

organizations. This leads to many circumstances which are temporary closure, diversification,

personnel changes and changes in the working practices and many other changes in operating

functions. The pandemic has not only affected the employment but also affected the salaries of

those personnels who are still employed in the organization (Jinjarak and et.al., 2020). Due to

impact of covid the employees are getting reduction in their salaries, bonus, commission, etc.

This has the impact on the finance function of the company by not earning the adequate profit

due to happening of the pandemic.

The pandemic has makes the organization to have the unforeseen challenges that is

temporary closure of the company which reduces the profitability of the business and has impact

on the accounting of the company. This makes the organization to work with the different

strategies and practices which makes difficult for the company to operate with the new strategies

and practices. The changes in personnel or the employees that are working from home makes the

work difficult for the organization. It is hard for the company to manage their work as the

employees are working from there home. It may have a bad impact on the finance function and

organizational accounting. In order to mange these circumstances the organization should hire or

provide training to their employees in order to retain and enhance the skills during the

challenging business environment. The COVID-19 had a impact on firms in the year 2020 and

which is moving to the 2021. There are different measures taken by the company in order cope

up with these circumstances and makes the company to have good accounting and finance

function.

SECTION B

Question B1

Budgeting is the process of making and doing the planning in order to spend the money

by the organization. By making this plan this makes the company know in advance that they will

have the adequate amount in the future in order to buy things. The proper budgeting helps the

business to have the proper cash flow, reduces costs, makes to improve the profit and makes the

company to have high returns on their investments. It is the base of the organization in order to

get success in the future. It is used to estimate the plan of the expenditure in order to restrict the

1

The COVID-19 is the most challenging pandemic for every organization, which makes

them to rethink about their business and for survival. This pandemic has the great impact on the

organizations. This leads to many circumstances which are temporary closure, diversification,

personnel changes and changes in the working practices and many other changes in operating

functions. The pandemic has not only affected the employment but also affected the salaries of

those personnels who are still employed in the organization (Jinjarak and et.al., 2020). Due to

impact of covid the employees are getting reduction in their salaries, bonus, commission, etc.

This has the impact on the finance function of the company by not earning the adequate profit

due to happening of the pandemic.

The pandemic has makes the organization to have the unforeseen challenges that is

temporary closure of the company which reduces the profitability of the business and has impact

on the accounting of the company. This makes the organization to work with the different

strategies and practices which makes difficult for the company to operate with the new strategies

and practices. The changes in personnel or the employees that are working from home makes the

work difficult for the organization. It is hard for the company to manage their work as the

employees are working from there home. It may have a bad impact on the finance function and

organizational accounting. In order to mange these circumstances the organization should hire or

provide training to their employees in order to retain and enhance the skills during the

challenging business environment. The COVID-19 had a impact on firms in the year 2020 and

which is moving to the 2021. There are different measures taken by the company in order cope

up with these circumstances and makes the company to have good accounting and finance

function.

SECTION B

Question B1

Budgeting is the process of making and doing the planning in order to spend the money

by the organization. By making this plan this makes the company know in advance that they will

have the adequate amount in the future in order to buy things. The proper budgeting helps the

business to have the proper cash flow, reduces costs, makes to improve the profit and makes the

company to have high returns on their investments. It is the base of the organization in order to

get success in the future. It is used to estimate the plan of the expenditure in order to restrict the

1

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

company to do other expenditure. Proper budgeting ensures the organizations to ensure that the

money allocated must be sued in the best way.

The internal persons of the organization that can be mangers or employees must know

about the proper planning of the amount estimated to be spent. This makes them to have the

efficient use of the resources (Butcher, 2020). The external person may use this information in

the negative and in the positive way too. By knowing about the information they can suggest

them some better approaches to the company in order to have the good estimation of the

expenditure of the money by the organization.

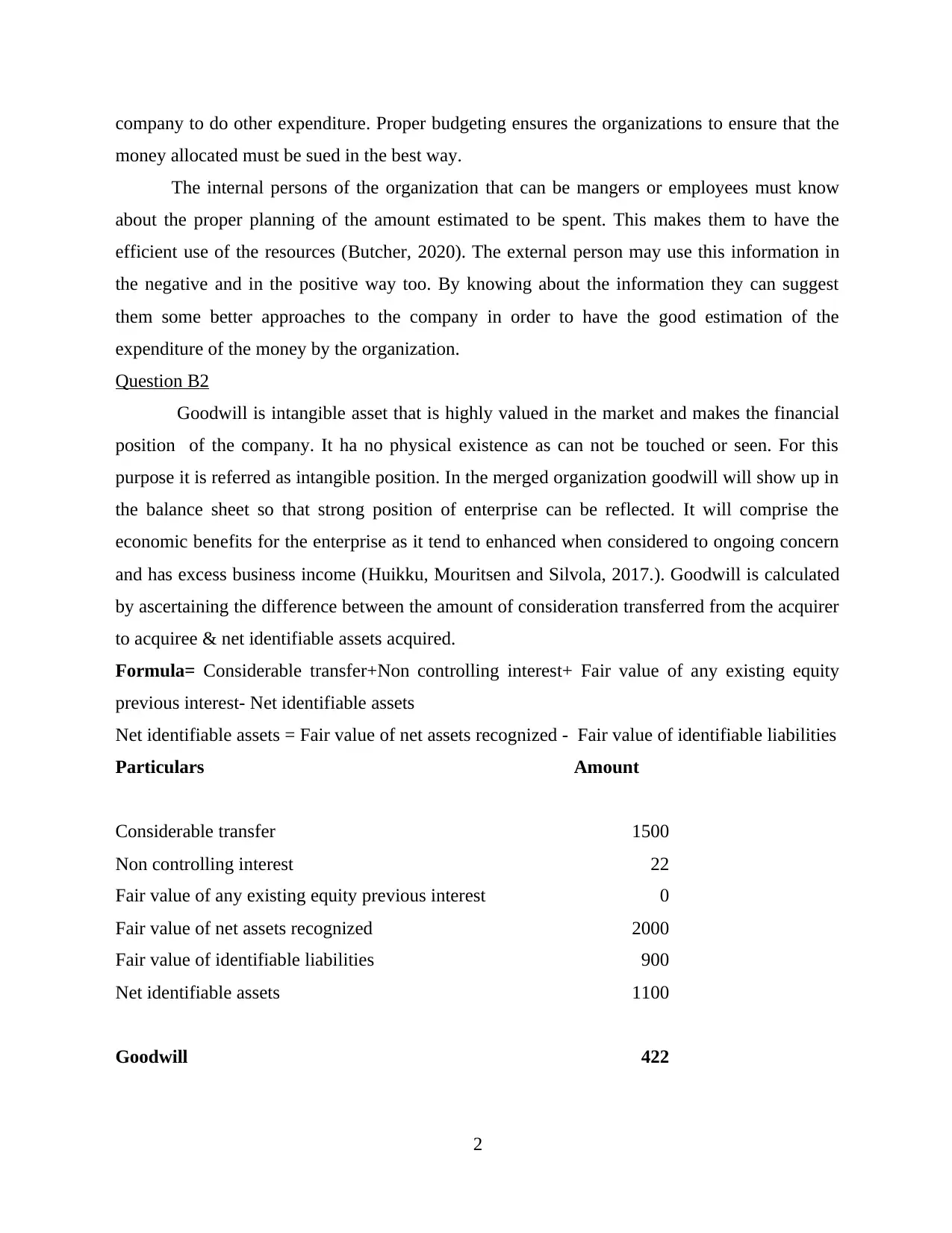

Question B2

Goodwill is intangible asset that is highly valued in the market and makes the financial

position of the company. It ha no physical existence as can not be touched or seen. For this

purpose it is referred as intangible position. In the merged organization goodwill will show up in

the balance sheet so that strong position of enterprise can be reflected. It will comprise the

economic benefits for the enterprise as it tend to enhanced when considered to ongoing concern

and has excess business income (Huikku, Mouritsen and Silvola, 2017.). Goodwill is calculated

by ascertaining the difference between the amount of consideration transferred from the acquirer

to acquiree & net identifiable assets acquired.

Formula= Considerable transfer+Non controlling interest+ Fair value of any existing equity

previous interest- Net identifiable assets

Net identifiable assets = Fair value of net assets recognized - Fair value of identifiable liabilities

Particulars Amount

Considerable transfer 1500

Non controlling interest 22

Fair value of any existing equity previous interest 0

Fair value of net assets recognized 2000

Fair value of identifiable liabilities 900

Net identifiable assets 1100

Goodwill 422

2

money allocated must be sued in the best way.

The internal persons of the organization that can be mangers or employees must know

about the proper planning of the amount estimated to be spent. This makes them to have the

efficient use of the resources (Butcher, 2020). The external person may use this information in

the negative and in the positive way too. By knowing about the information they can suggest

them some better approaches to the company in order to have the good estimation of the

expenditure of the money by the organization.

Question B2

Goodwill is intangible asset that is highly valued in the market and makes the financial

position of the company. It ha no physical existence as can not be touched or seen. For this

purpose it is referred as intangible position. In the merged organization goodwill will show up in

the balance sheet so that strong position of enterprise can be reflected. It will comprise the

economic benefits for the enterprise as it tend to enhanced when considered to ongoing concern

and has excess business income (Huikku, Mouritsen and Silvola, 2017.). Goodwill is calculated

by ascertaining the difference between the amount of consideration transferred from the acquirer

to acquiree & net identifiable assets acquired.

Formula= Considerable transfer+Non controlling interest+ Fair value of any existing equity

previous interest- Net identifiable assets

Net identifiable assets = Fair value of net assets recognized - Fair value of identifiable liabilities

Particulars Amount

Considerable transfer 1500

Non controlling interest 22

Fair value of any existing equity previous interest 0

Fair value of net assets recognized 2000

Fair value of identifiable liabilities 900

Net identifiable assets 1100

Goodwill 422

2

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

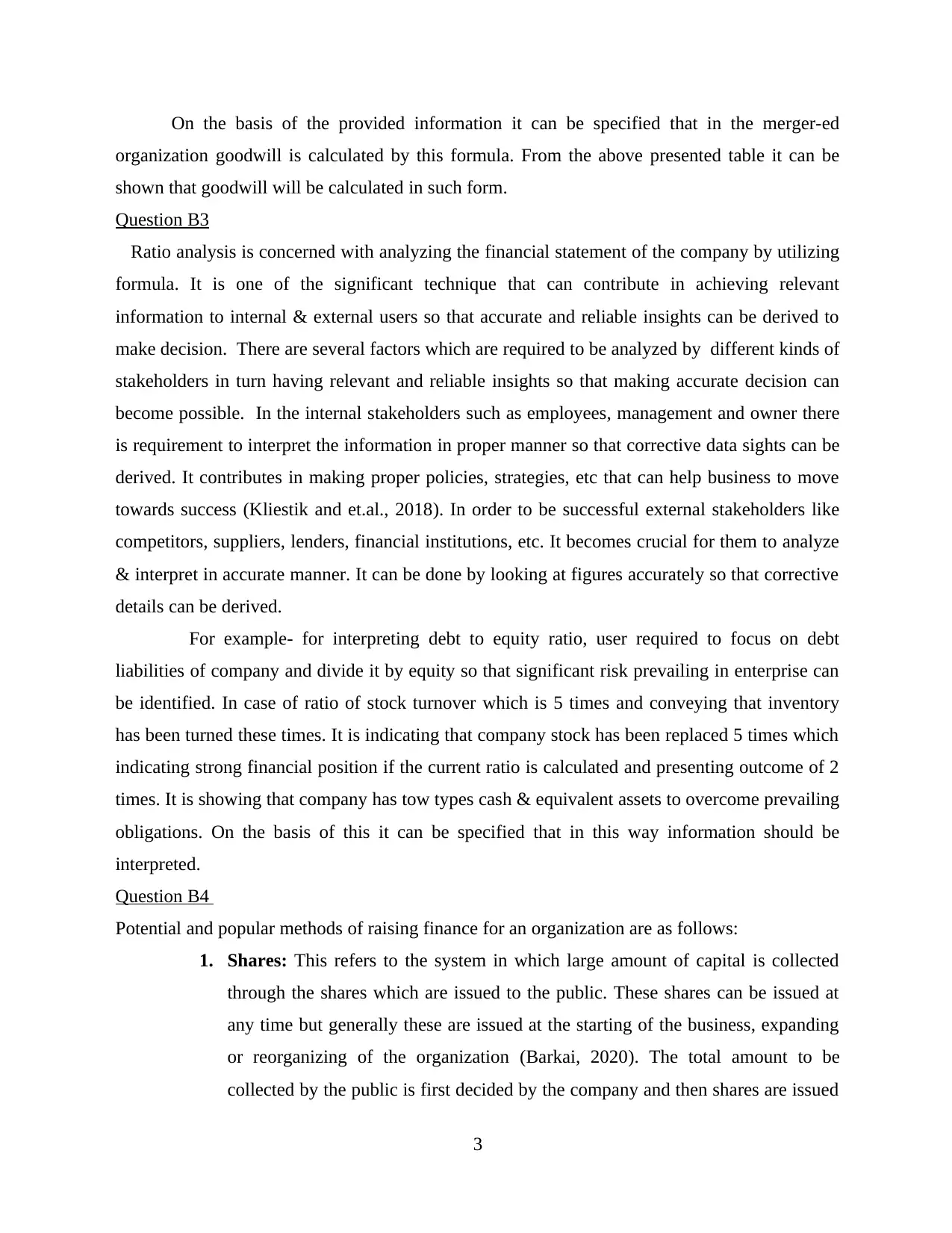

On the basis of the provided information it can be specified that in the merger-ed

organization goodwill is calculated by this formula. From the above presented table it can be

shown that goodwill will be calculated in such form.

Question B3

Ratio analysis is concerned with analyzing the financial statement of the company by utilizing

formula. It is one of the significant technique that can contribute in achieving relevant

information to internal & external users so that accurate and reliable insights can be derived to

make decision. There are several factors which are required to be analyzed by different kinds of

stakeholders in turn having relevant and reliable insights so that making accurate decision can

become possible. In the internal stakeholders such as employees, management and owner there

is requirement to interpret the information in proper manner so that corrective data sights can be

derived. It contributes in making proper policies, strategies, etc that can help business to move

towards success (Kliestik and et.al., 2018). In order to be successful external stakeholders like

competitors, suppliers, lenders, financial institutions, etc. It becomes crucial for them to analyze

& interpret in accurate manner. It can be done by looking at figures accurately so that corrective

details can be derived.

For example- for interpreting debt to equity ratio, user required to focus on debt

liabilities of company and divide it by equity so that significant risk prevailing in enterprise can

be identified. In case of ratio of stock turnover which is 5 times and conveying that inventory

has been turned these times. It is indicating that company stock has been replaced 5 times which

indicating strong financial position if the current ratio is calculated and presenting outcome of 2

times. It is showing that company has tow types cash & equivalent assets to overcome prevailing

obligations. On the basis of this it can be specified that in this way information should be

interpreted.

Question B4

Potential and popular methods of raising finance for an organization are as follows:

1. Shares: This refers to the system in which large amount of capital is collected

through the shares which are issued to the public. These shares can be issued at

any time but generally these are issued at the starting of the business, expanding

or reorganizing of the organization (Barkai, 2020). The total amount to be

collected by the public is first decided by the company and then shares are issued

3

organization goodwill is calculated by this formula. From the above presented table it can be

shown that goodwill will be calculated in such form.

Question B3

Ratio analysis is concerned with analyzing the financial statement of the company by utilizing

formula. It is one of the significant technique that can contribute in achieving relevant

information to internal & external users so that accurate and reliable insights can be derived to

make decision. There are several factors which are required to be analyzed by different kinds of

stakeholders in turn having relevant and reliable insights so that making accurate decision can

become possible. In the internal stakeholders such as employees, management and owner there

is requirement to interpret the information in proper manner so that corrective data sights can be

derived. It contributes in making proper policies, strategies, etc that can help business to move

towards success (Kliestik and et.al., 2018). In order to be successful external stakeholders like

competitors, suppliers, lenders, financial institutions, etc. It becomes crucial for them to analyze

& interpret in accurate manner. It can be done by looking at figures accurately so that corrective

details can be derived.

For example- for interpreting debt to equity ratio, user required to focus on debt

liabilities of company and divide it by equity so that significant risk prevailing in enterprise can

be identified. In case of ratio of stock turnover which is 5 times and conveying that inventory

has been turned these times. It is indicating that company stock has been replaced 5 times which

indicating strong financial position if the current ratio is calculated and presenting outcome of 2

times. It is showing that company has tow types cash & equivalent assets to overcome prevailing

obligations. On the basis of this it can be specified that in this way information should be

interpreted.

Question B4

Potential and popular methods of raising finance for an organization are as follows:

1. Shares: This refers to the system in which large amount of capital is collected

through the shares which are issued to the public. These shares can be issued at

any time but generally these are issued at the starting of the business, expanding

or reorganizing of the organization (Barkai, 2020). The total amount to be

collected by the public is first decided by the company and then shares are issued

3

to the public. This makes the organization to raise their finance in the market. The

shareholders of the company are given dividends at the time of profit in the

company. There are two types of shares by which the company raises the funds

that are preference shares and equity shares.

2. Debentures: When the organization thinks to have finance from taking loans

rather than selling the shares, they the debentures are issued. When the borrowed

capital of the firm is divided than each part of that capital is called the debentures.

These are generally the debts for the company for which company has to pay the

interest at the regular intervals. By taking the debentures the company can raise

the finance and makes the organization to increase their profits. There are many

types of debentures that the company can take includes redeemable and

irredeemable; secured and unsecured; convertible and non-convertible

debentures. It is the type of bond or the debt instrument which not secured by

collateral security. These are the loan which means these are the liabilities for the

company because this has to be paid in future.

SECTION C

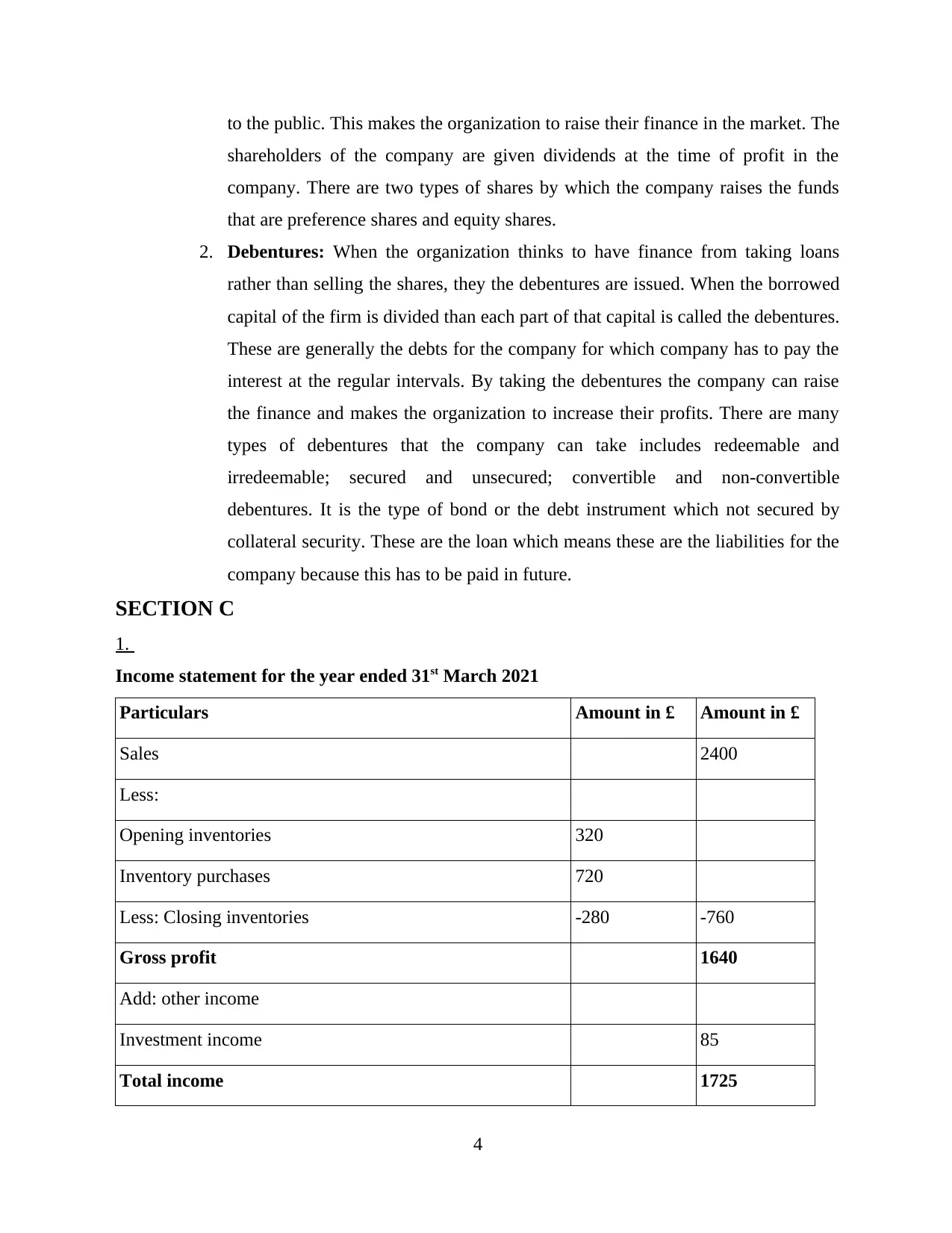

1.

Income statement for the year ended 31st March 2021

Particulars Amount in £ Amount in £

Sales 2400

Less:

Opening inventories 320

Inventory purchases 720

Less: Closing inventories -280 -760

Gross profit 1640

Add: other income

Investment income 85

Total income 1725

4

shareholders of the company are given dividends at the time of profit in the

company. There are two types of shares by which the company raises the funds

that are preference shares and equity shares.

2. Debentures: When the organization thinks to have finance from taking loans

rather than selling the shares, they the debentures are issued. When the borrowed

capital of the firm is divided than each part of that capital is called the debentures.

These are generally the debts for the company for which company has to pay the

interest at the regular intervals. By taking the debentures the company can raise

the finance and makes the organization to increase their profits. There are many

types of debentures that the company can take includes redeemable and

irredeemable; secured and unsecured; convertible and non-convertible

debentures. It is the type of bond or the debt instrument which not secured by

collateral security. These are the loan which means these are the liabilities for the

company because this has to be paid in future.

SECTION C

1.

Income statement for the year ended 31st March 2021

Particulars Amount in £ Amount in £

Sales 2400

Less:

Opening inventories 320

Inventory purchases 720

Less: Closing inventories -280 -760

Gross profit 1640

Add: other income

Investment income 85

Total income 1725

4

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

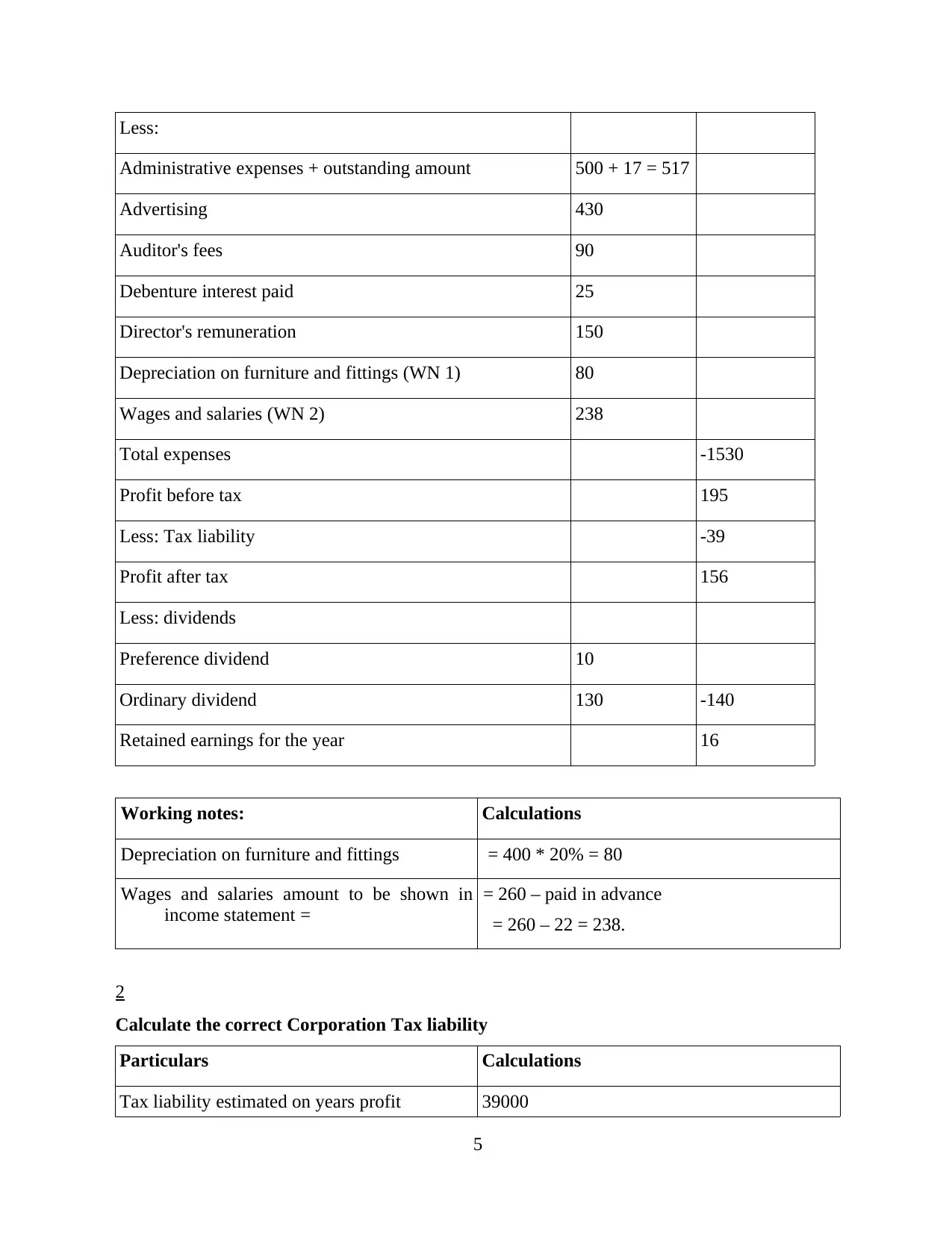

Less:

Administrative expenses + outstanding amount 500 + 17 = 517

Advertising 430

Auditor's fees 90

Debenture interest paid 25

Director's remuneration 150

Depreciation on furniture and fittings (WN 1) 80

Wages and salaries (WN 2) 238

Total expenses -1530

Profit before tax 195

Less: Tax liability -39

Profit after tax 156

Less: dividends

Preference dividend 10

Ordinary dividend 130 -140

Retained earnings for the year 16

Working notes: Calculations

Depreciation on furniture and fittings = 400 * 20% = 80

Wages and salaries amount to be shown in

income statement =

= 260 – paid in advance

= 260 – 22 = 238.

2

Calculate the correct Corporation Tax liability

Particulars Calculations

Tax liability estimated on years profit 39000

5

Administrative expenses + outstanding amount 500 + 17 = 517

Advertising 430

Auditor's fees 90

Debenture interest paid 25

Director's remuneration 150

Depreciation on furniture and fittings (WN 1) 80

Wages and salaries (WN 2) 238

Total expenses -1530

Profit before tax 195

Less: Tax liability -39

Profit after tax 156

Less: dividends

Preference dividend 10

Ordinary dividend 130 -140

Retained earnings for the year 16

Working notes: Calculations

Depreciation on furniture and fittings = 400 * 20% = 80

Wages and salaries amount to be shown in

income statement =

= 260 – paid in advance

= 260 – 22 = 238.

2

Calculate the correct Corporation Tax liability

Particulars Calculations

Tax liability estimated on years profit 39000

5

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Correct corporation tax liabilities = Profit

before tax + unallowable deductions

(depreciation)

= 195 + 80 = 275

corporation tax liability = 275 * 19% = 52.25

From the evaluation of the provided information it can be specified that the difference

has been derived due to the difference in profit obtained before and after deducting the

depreciation. It can be interpreted that difference has been achieved as tax has been calculated

tax rate of 19%.

3

Statement of financial position as at 31st March 2021

Particulars Amount in £

Assets

Non – current assets

Investments 520

Furniture and fittings at cost 400

Current assets

Cash at bank 410

Trade receivables 450

Inventories 280

Prepaid salaries 22

TOTAL ASSETS 2082

6

before tax + unallowable deductions

(depreciation)

= 195 + 80 = 275

corporation tax liability = 275 * 19% = 52.25

From the evaluation of the provided information it can be specified that the difference

has been derived due to the difference in profit obtained before and after deducting the

depreciation. It can be interpreted that difference has been achieved as tax has been calculated

tax rate of 19%.

3

Statement of financial position as at 31st March 2021

Particulars Amount in £

Assets

Non – current assets

Investments 520

Furniture and fittings at cost 400

Current assets

Cash at bank 410

Trade receivables 450

Inventories 280

Prepaid salaries 22

TOTAL ASSETS 2082

6

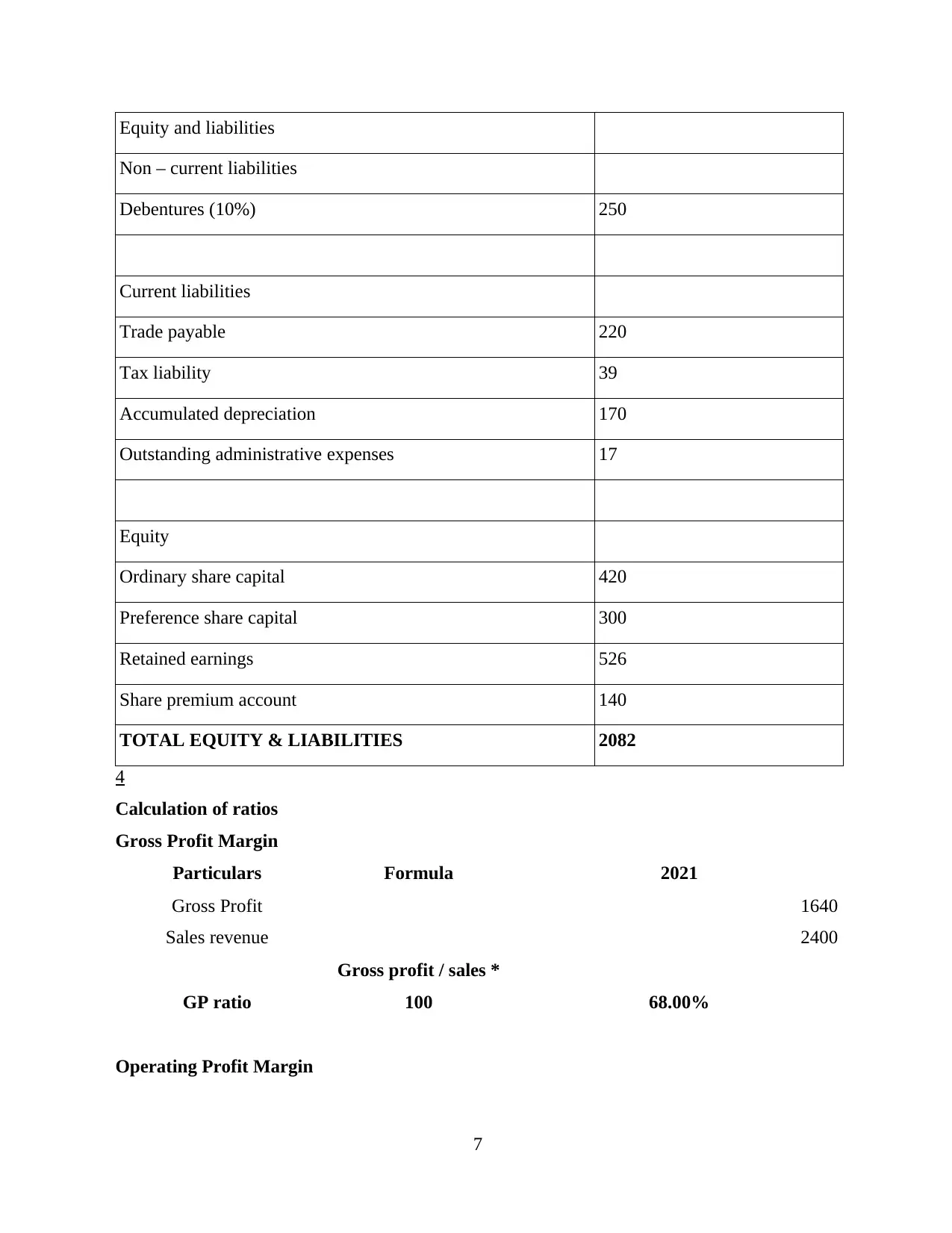

Equity and liabilities

Non – current liabilities

Debentures (10%) 250

Current liabilities

Trade payable 220

Tax liability 39

Accumulated depreciation 170

Outstanding administrative expenses 17

Equity

Ordinary share capital 420

Preference share capital 300

Retained earnings 526

Share premium account 140

TOTAL EQUITY & LIABILITIES 2082

4

Calculation of ratios

Gross Profit Margin

Particulars Formula 2021

Gross Profit 1640

Sales revenue 2400

GP ratio

Gross profit / sales *

100 68.00%

Operating Profit Margin

7

Non – current liabilities

Debentures (10%) 250

Current liabilities

Trade payable 220

Tax liability 39

Accumulated depreciation 170

Outstanding administrative expenses 17

Equity

Ordinary share capital 420

Preference share capital 300

Retained earnings 526

Share premium account 140

TOTAL EQUITY & LIABILITIES 2082

4

Calculation of ratios

Gross Profit Margin

Particulars Formula 2021

Gross Profit 1640

Sales revenue 2400

GP ratio

Gross profit / sales *

100 68.00%

Operating Profit Margin

7

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

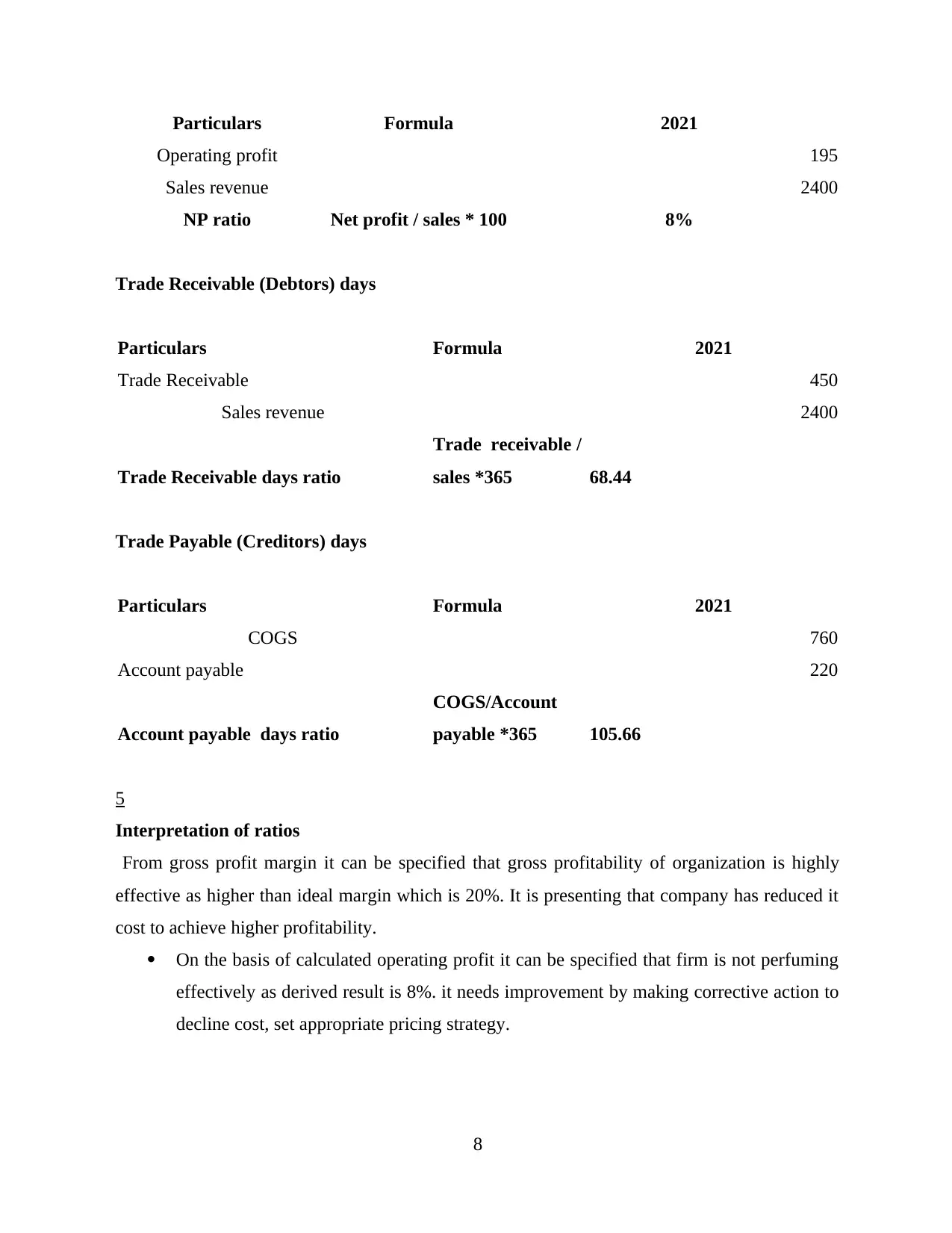

Particulars Formula 2021

Operating profit 195

Sales revenue 2400

NP ratio Net profit / sales * 100 8%

Trade Receivable (Debtors) days

Particulars Formula 2021

Trade Receivable 450

Sales revenue 2400

Trade Receivable days ratio

Trade receivable /

sales *365 68.44

Trade Payable (Creditors) days

Particulars Formula 2021

COGS 760

Account payable 220

Account payable days ratio

COGS/Account

payable *365 105.66

5

Interpretation of ratios

From gross profit margin it can be specified that gross profitability of organization is highly

effective as higher than ideal margin which is 20%. It is presenting that company has reduced it

cost to achieve higher profitability.

On the basis of calculated operating profit it can be specified that firm is not perfuming

effectively as derived result is 8%. it needs improvement by making corrective action to

decline cost, set appropriate pricing strategy.

8

Operating profit 195

Sales revenue 2400

NP ratio Net profit / sales * 100 8%

Trade Receivable (Debtors) days

Particulars Formula 2021

Trade Receivable 450

Sales revenue 2400

Trade Receivable days ratio

Trade receivable /

sales *365 68.44

Trade Payable (Creditors) days

Particulars Formula 2021

COGS 760

Account payable 220

Account payable days ratio

COGS/Account

payable *365 105.66

5

Interpretation of ratios

From gross profit margin it can be specified that gross profitability of organization is highly

effective as higher than ideal margin which is 20%. It is presenting that company has reduced it

cost to achieve higher profitability.

On the basis of calculated operating profit it can be specified that firm is not perfuming

effectively as derived result is 8%. it needs improvement by making corrective action to

decline cost, set appropriate pricing strategy.

8

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Trade receivable in days indicating low effectiveness in collecting funds from traders

(Stewart, 2017.). It is reflecting low liquidity position which need to be improved by

declining days of collecting funds.

Trade payable ratio provides assistance indicating credibility to pay off payments o

suppliers. It is found be less effective as in 105.66 days company pay to supplier which

can affect credibility & trustworthiness.

SECTION D

1

Calculation of Net Present Value

Formula: Present value of cash inflow — Initial investment

Project A

Calculation of Present value of cash inflows

Years Cash inflow + Cash

saving — running

cost (£)

Discounting factor

@10%

Present value of cash

inflows (£)

1 68300

(93000 + 9500 –

34200)

0.91 62153

2 68300

(93000 + 9500 –

34200)

0.83 56689

3 68300

(93000 + 9500 –

34200)

0.75 51225

4 68300

(93000 + 9500 –

34200)

0.68 46444

5 68300

(93000 + 9500 –

0.62 42346

9

(Stewart, 2017.). It is reflecting low liquidity position which need to be improved by

declining days of collecting funds.

Trade payable ratio provides assistance indicating credibility to pay off payments o

suppliers. It is found be less effective as in 105.66 days company pay to supplier which

can affect credibility & trustworthiness.

SECTION D

1

Calculation of Net Present Value

Formula: Present value of cash inflow — Initial investment

Project A

Calculation of Present value of cash inflows

Years Cash inflow + Cash

saving — running

cost (£)

Discounting factor

@10%

Present value of cash

inflows (£)

1 68300

(93000 + 9500 –

34200)

0.91 62153

2 68300

(93000 + 9500 –

34200)

0.83 56689

3 68300

(93000 + 9500 –

34200)

0.75 51225

4 68300

(93000 + 9500 –

34200)

0.68 46444

5 68300

(93000 + 9500 –

0.62 42346

9

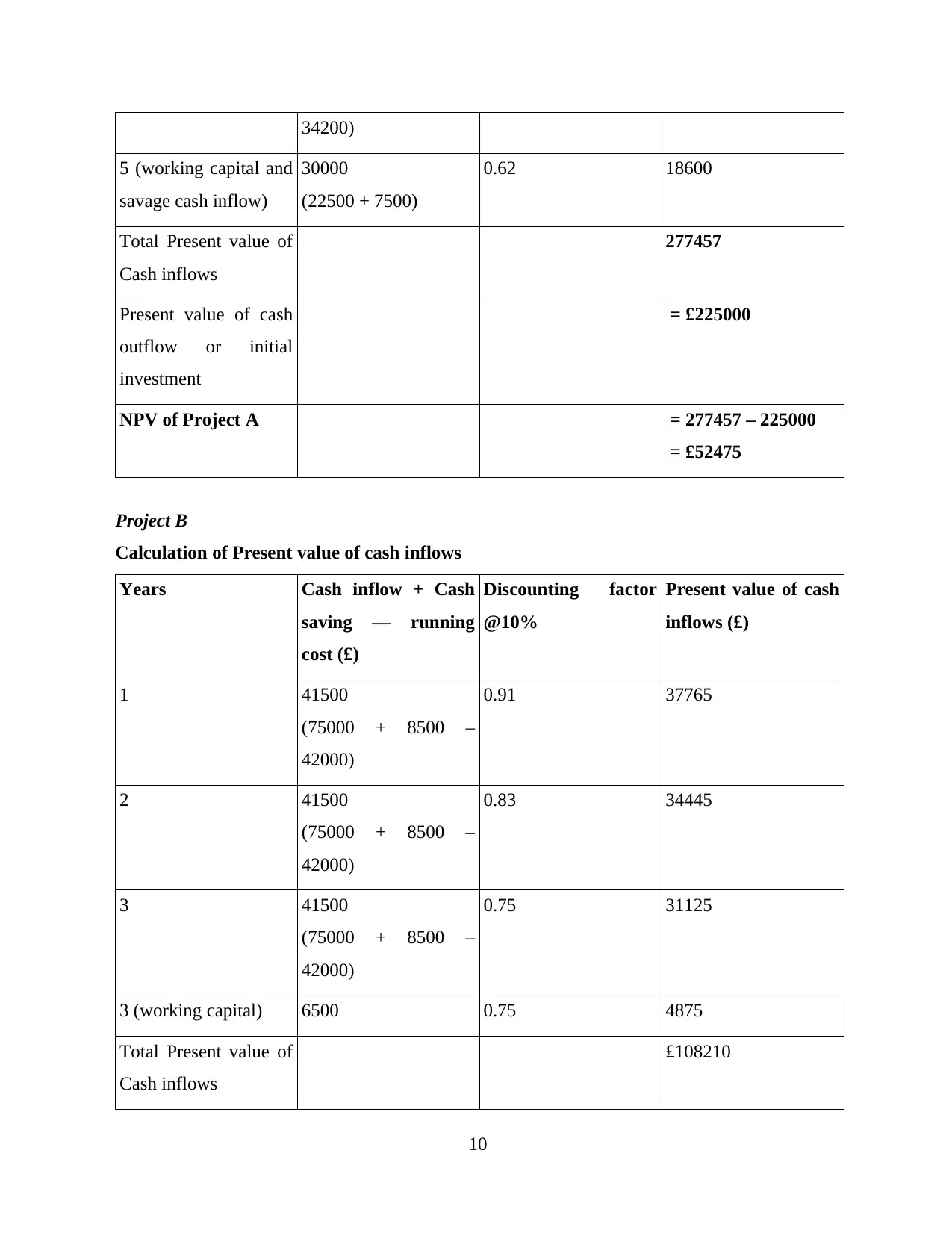

34200)

5 (working capital and

savage cash inflow)

30000

(22500 + 7500)

0.62 18600

Total Present value of

Cash inflows

277457

Present value of cash

outflow or initial

investment

= £225000

NPV of Project A = 277457 – 225000

= £52475

Project B

Calculation of Present value of cash inflows

Years Cash inflow + Cash

saving — running

cost (£)

Discounting factor

@10%

Present value of cash

inflows (£)

1 41500

(75000 + 8500 –

42000)

0.91 37765

2 41500

(75000 + 8500 –

42000)

0.83 34445

3 41500

(75000 + 8500 –

42000)

0.75 31125

3 (working capital) 6500 0.75 4875

Total Present value of

Cash inflows

£108210

10

5 (working capital and

savage cash inflow)

30000

(22500 + 7500)

0.62 18600

Total Present value of

Cash inflows

277457

Present value of cash

outflow or initial

investment

= £225000

NPV of Project A = 277457 – 225000

= £52475

Project B

Calculation of Present value of cash inflows

Years Cash inflow + Cash

saving — running

cost (£)

Discounting factor

@10%

Present value of cash

inflows (£)

1 41500

(75000 + 8500 –

42000)

0.91 37765

2 41500

(75000 + 8500 –

42000)

0.83 34445

3 41500

(75000 + 8500 –

42000)

0.75 31125

3 (working capital) 6500 0.75 4875

Total Present value of

Cash inflows

£108210

10

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 16

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.