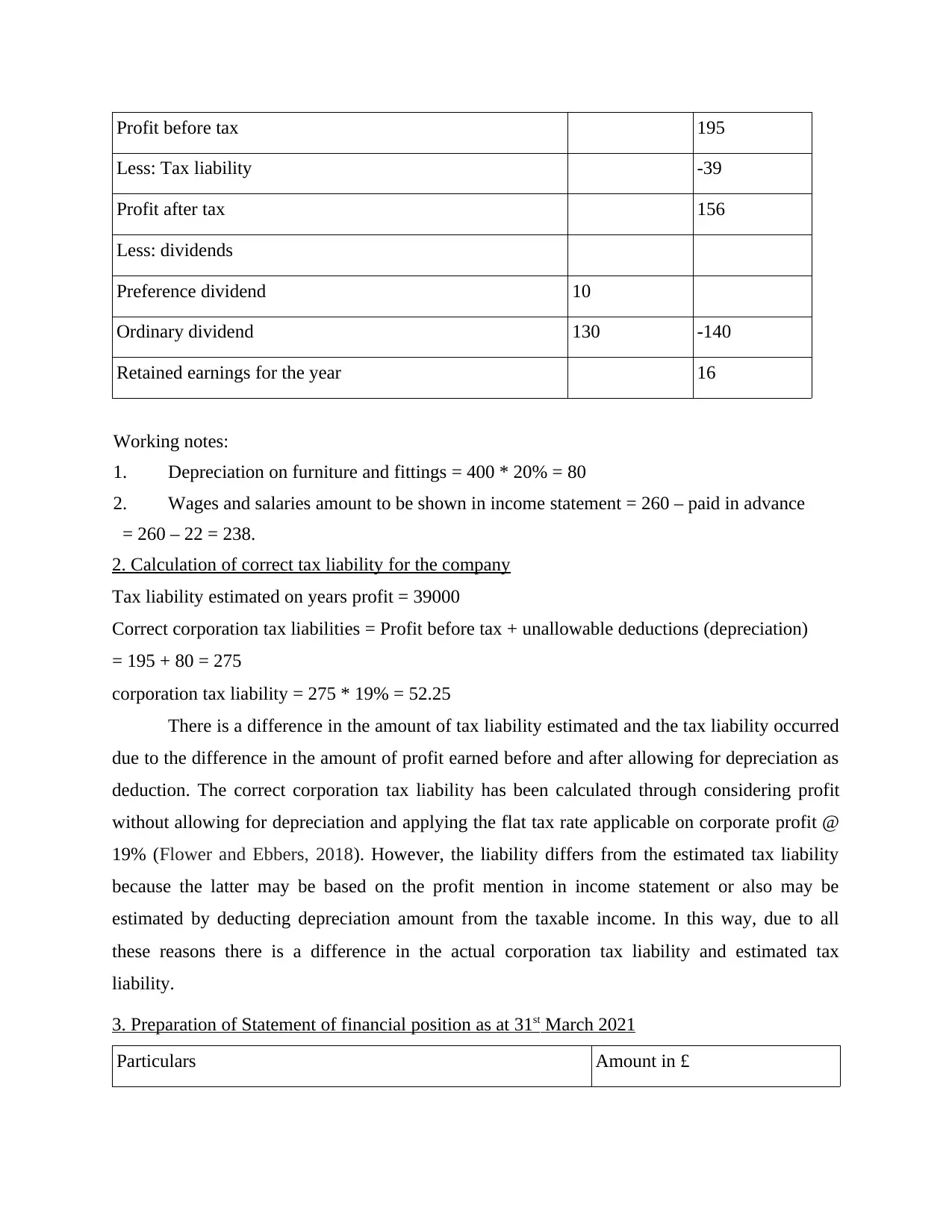

Financial Reporting Online Exam Solution: Ratio Analysis & NPV

VerifiedAdded on 2023/06/15

|18

|3980

|406

Homework Assignment

AI Summary

This document presents a comprehensive solution to an online exam focused on finance and financial reporting. It begins by analyzing the impact of COVID-19 on accounting functions, highlighting challenges such as revenue decline and compensation issues. The solution then addresses budgeting, goodwill, and ratio analysis, providing detailed explanations and examples. Furthermore, it explores methods of raising finance, including IPOs and offers through sale. The document includes an income statement, calculation of tax liability, and a statement of financial position, followed by the calculation and commentary on financial ratios. Finally, it covers NPV and payback period calculations for investment appraisal, concluding with a recommendation based on the analysis. This resource offers a detailed overview of key financial concepts and their practical application.

ONLINE EXAM FINANCE

AND FINANCIAL

REPORTING

AND FINANCIAL

REPORTING

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

TABLE OF CONTENTS

SECTION A.....................................................................................................................................3

Impact of covid- 19 on accounting functions............................................................................3

SECTION B.....................................................................................................................................4

Question B1.................................................................................................................................4

Question B2.................................................................................................................................4

Question B3.................................................................................................................................5

Question B4.................................................................................................................................6

SECTION C.....................................................................................................................................7

1. Income statement for the year ended 31st March 2021..........................................................7

2. Calculation of correct tax liability for the company...............................................................8

3. Preparation of Statement of financial position as at 31st March 2021...................................8

4. Calculation of financial ratios.................................................................................................9

5. Commenting on the ratios calculated....................................................................................10

SECTION D...................................................................................................................................11

1. Calculation of NPV and Pay Back Period............................................................................11

2. Recommendation..................................................................................................................13

3.................................................................................................................................................14

4.................................................................................................................................................14

REFERENCES..............................................................................................................................16

SECTION A.....................................................................................................................................3

Impact of covid- 19 on accounting functions............................................................................3

SECTION B.....................................................................................................................................4

Question B1.................................................................................................................................4

Question B2.................................................................................................................................4

Question B3.................................................................................................................................5

Question B4.................................................................................................................................6

SECTION C.....................................................................................................................................7

1. Income statement for the year ended 31st March 2021..........................................................7

2. Calculation of correct tax liability for the company...............................................................8

3. Preparation of Statement of financial position as at 31st March 2021...................................8

4. Calculation of financial ratios.................................................................................................9

5. Commenting on the ratios calculated....................................................................................10

SECTION D...................................................................................................................................11

1. Calculation of NPV and Pay Back Period............................................................................11

2. Recommendation..................................................................................................................13

3.................................................................................................................................................14

4.................................................................................................................................................14

REFERENCES..............................................................................................................................16

SECTION A

Impact of covid- 19 on accounting functions

Coronavirus has negatively affect the revenue of every organization and

most of the small companies were shut down and closed. On the other hand

accounting function include systematic tracking, storing, recording, analyzing and

summarizing and reporting of company financial transaction. All this functions is

necessary to be maintain properly in order to manage the accounts of

organization. Along with this, corona virus has impacted negatively on the finance

function as most of the organization has faced loss and the large companies

has reported considerable decline. In addition, to this, it has impacted on the

compensation in finance. Due to pandemic there was reduction in the

compensation such as in salary and bonus. Because of coronavirus there were

reduction in the fixed cost as organization has to pay the standard salary and

compensation to their employees (Roozen, Steens and Spoor, 2019). This has lead in the

loss to the company along with this there were deal in sending the income to

the subordinates because business was not able to generate revenue properly.

Along with this, there was negative impact on the account payable. It means the

amount that are due to the vendor or suppliers that has not been paid. The

organization was not able to pay the amount to their creditors as due to

pandemic there was not generation of profit and the company has to pay the

delayed expense to their employees. Along with this, due to lockdown in

many countries there was no export and import and because of that organization

has to face huge loss.

For example, in order to reduce the negative impact of Covid-19 over the individuals

and businesses, the Bank of England has reduced the interest rate up to 0.1% which has put

major impact over the function of accounting and finance. The finance team of the company are

responsible for selecting the best sources out of many from where they can acquire funds from

the market. The main goal of finance team is such that they have to select the sources whose cost

of acquisition must be low (Baum, Crosby and Devaney, 2021). So, as the interest rates are

decreases, the finance team can recommend the company to acquire the funds from the banks.

Impact of covid- 19 on accounting functions

Coronavirus has negatively affect the revenue of every organization and

most of the small companies were shut down and closed. On the other hand

accounting function include systematic tracking, storing, recording, analyzing and

summarizing and reporting of company financial transaction. All this functions is

necessary to be maintain properly in order to manage the accounts of

organization. Along with this, corona virus has impacted negatively on the finance

function as most of the organization has faced loss and the large companies

has reported considerable decline. In addition, to this, it has impacted on the

compensation in finance. Due to pandemic there was reduction in the

compensation such as in salary and bonus. Because of coronavirus there were

reduction in the fixed cost as organization has to pay the standard salary and

compensation to their employees (Roozen, Steens and Spoor, 2019). This has lead in the

loss to the company along with this there were deal in sending the income to

the subordinates because business was not able to generate revenue properly.

Along with this, there was negative impact on the account payable. It means the

amount that are due to the vendor or suppliers that has not been paid. The

organization was not able to pay the amount to their creditors as due to

pandemic there was not generation of profit and the company has to pay the

delayed expense to their employees. Along with this, due to lockdown in

many countries there was no export and import and because of that organization

has to face huge loss.

For example, in order to reduce the negative impact of Covid-19 over the individuals

and businesses, the Bank of England has reduced the interest rate up to 0.1% which has put

major impact over the function of accounting and finance. The finance team of the company are

responsible for selecting the best sources out of many from where they can acquire funds from

the market. The main goal of finance team is such that they have to select the sources whose cost

of acquisition must be low (Baum, Crosby and Devaney, 2021). So, as the interest rates are

decreases, the finance team can recommend the company to acquire the funds from the banks.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

But on the same side, as the interest rate decreases, the company unable to get higher returns

from the investment they invest in the banks and financial institutions of UK. Thus, in such way

the change of Covid-19 has affect the business in both positive and negative way.

SECTION B

Question B1

Budgeting in business involves preparation of financial plan on the basis current revenues and

expenses to forecast future events associated with such budgeted costs and revenues. With the

help of budgets, business can estimate its spending in advance, identify their resources and

allocate it efficiently along with facilitating prediction for future revenues (Flower and Ebbers,

2018). Thus, company performance can be determined and comparison can be done between the

budgeted and actual performance, so that deviations can be found out at the earliest and

subsequent corrective decisions can be make for correcting deviations. Accordingly, business's

strengths and weaknesses can be highlighted through budgeting. Concentration on cash flows,

cost reduction, profit improvements and increasing returns on investment could be possible

through budgeting.

Also, budgeting helps in demonstrating business priorities to all associated with the

business and thus organization's vision can be shared with both internal and external parties of

the organization (Iriyadi, Maulana and Nurjanah, 2018). Further, budgeting is helpful in meeting

business objectives by making financial decisions confidently.

Budgets are generally meant for those internal to the organisation, however in certain

case where external parties like auditors may demand for business budgets to ensure the business

objectives and goals are in alignment of the shareholder's goals and expectations. Managers uses

budgets for making arrangement for required financial resources on time and allocating it in

efficient and effective manner.

Question B2

The nature of goodwill is such where it is considered as an intangible fixed asset having no

physical existence and which cannot be seen or touched. The goodwill can be described and

identified in two ways that is, purchased and non – purchased goodwill (Barth, 2018). The

former arises when the consideration paid for business during acquisition and merger is higher

than the fair value of identifiable assets (Net). Alternatively, the valuation of non – purchased

from the investment they invest in the banks and financial institutions of UK. Thus, in such way

the change of Covid-19 has affect the business in both positive and negative way.

SECTION B

Question B1

Budgeting in business involves preparation of financial plan on the basis current revenues and

expenses to forecast future events associated with such budgeted costs and revenues. With the

help of budgets, business can estimate its spending in advance, identify their resources and

allocate it efficiently along with facilitating prediction for future revenues (Flower and Ebbers,

2018). Thus, company performance can be determined and comparison can be done between the

budgeted and actual performance, so that deviations can be found out at the earliest and

subsequent corrective decisions can be make for correcting deviations. Accordingly, business's

strengths and weaknesses can be highlighted through budgeting. Concentration on cash flows,

cost reduction, profit improvements and increasing returns on investment could be possible

through budgeting.

Also, budgeting helps in demonstrating business priorities to all associated with the

business and thus organization's vision can be shared with both internal and external parties of

the organization (Iriyadi, Maulana and Nurjanah, 2018). Further, budgeting is helpful in meeting

business objectives by making financial decisions confidently.

Budgets are generally meant for those internal to the organisation, however in certain

case where external parties like auditors may demand for business budgets to ensure the business

objectives and goals are in alignment of the shareholder's goals and expectations. Managers uses

budgets for making arrangement for required financial resources on time and allocating it in

efficient and effective manner.

Question B2

The nature of goodwill is such where it is considered as an intangible fixed asset having no

physical existence and which cannot be seen or touched. The goodwill can be described and

identified in two ways that is, purchased and non – purchased goodwill (Barth, 2018). The

former arises when the consideration paid for business during acquisition and merger is higher

than the fair value of identifiable assets (Net). Alternatively, the valuation of non – purchased

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

goodwill is done on the basis of customers of the trade where calculation is done as number of

year's purchase of super or average profits.

When a merger or acquisition took place in business, there is an amount shown in the balance

sheet of the company which indicates that the purchase consideration exceeds the net identifiable

fair value of the assets of the business (Breuer, 2021). It is shown under intangible assets section

of the balance sheet. When a company has large amount of goodwill in its balance sheet, it

results in attracting higher purchase prices.

For instance, company A acquires company B for $5 million. Assets are equal to $1.5 million

and liabilities are equal to $500000 million which results in fair value of the net identifiable

assets equivalent to $1million.

Goodwill = Purchase consideration – fair value of net identifiable assets = $5 million - $1million

= $4million.

This $4 million is the premium paid by company A which is over and above the company's net

identifiable assets and this amount will be shown in the balance sheet of the group as goodwill

under the intangible assets section.

Question B3

Basis of ratio analysis

Ratio analysis is a quantitative method to analyse the liquidity, efficiency and

performance of the company. The base of ratio analysis is as follows:

Income statement: This is a statement which covers the list of income and expenses

which is earned and incur by business. This income and expenses must be related to the

ongoing operation of business. The income statement is prepared by the company on the

basis of accrual concept and provides profit and loss.

Balance Sheet: The balance sheet of the business states the list of liabilities and assets

which must be balanced at the end date. This includes current and non-current assets,

liabilities, equities which is further used to analyse the liquidity and efficiency

performance of business (Harris, Hoang and Ngan, 2017).

Rationale of Ratio analysis

The importance and rationale of ratio analysis is as follows which provides various

benefits to the company:

year's purchase of super or average profits.

When a merger or acquisition took place in business, there is an amount shown in the balance

sheet of the company which indicates that the purchase consideration exceeds the net identifiable

fair value of the assets of the business (Breuer, 2021). It is shown under intangible assets section

of the balance sheet. When a company has large amount of goodwill in its balance sheet, it

results in attracting higher purchase prices.

For instance, company A acquires company B for $5 million. Assets are equal to $1.5 million

and liabilities are equal to $500000 million which results in fair value of the net identifiable

assets equivalent to $1million.

Goodwill = Purchase consideration – fair value of net identifiable assets = $5 million - $1million

= $4million.

This $4 million is the premium paid by company A which is over and above the company's net

identifiable assets and this amount will be shown in the balance sheet of the group as goodwill

under the intangible assets section.

Question B3

Basis of ratio analysis

Ratio analysis is a quantitative method to analyse the liquidity, efficiency and

performance of the company. The base of ratio analysis is as follows:

Income statement: This is a statement which covers the list of income and expenses

which is earned and incur by business. This income and expenses must be related to the

ongoing operation of business. The income statement is prepared by the company on the

basis of accrual concept and provides profit and loss.

Balance Sheet: The balance sheet of the business states the list of liabilities and assets

which must be balanced at the end date. This includes current and non-current assets,

liabilities, equities which is further used to analyse the liquidity and efficiency

performance of business (Harris, Hoang and Ngan, 2017).

Rationale of Ratio analysis

The importance and rationale of ratio analysis is as follows which provides various

benefits to the company:

It is important to analyse the financial statement of the company such as income

statement and balance sheet.

It is also important to analyse the operational efficiency of the firm using average

collection period and average payment period.

This is also helpful for identifying the profitability of company along with the business

risk to firms.

It also helps in determining the financial risk of firms including planning and forecasting

of futures.

Further, it is also helpful for the business to compare its performance with its own past

performance along with that of others competitors (Agbloyor and et.al., 2021).

For example, Gross profit margin of A company is 25% in the year 2020 while the gross

profit margin of B company is 20% in the same year. It means that company A is more profitable

than B and is earning high profit percentage than its competitors. This provides an opportunity to

company A that they can gain competitive advantage if they improve its profitability more. This

indicates that ratio analysis is most important part of every business (Lindvall and Larsson,

2017).

Question B4

There are many popular and potential methods of raising finance in the business which include

initial public offering or IPO and offer through sale (Choudhary, Merkley and Schipper, 2021).

Business must choose those method for raising finance which helps in making arrangement for

finance for the business operations. Floatation involves selling and issuing shares to the public

which facilitates raising finance from external sources. The two methods of floating to the stock

market are as follows:

Initial public offering (IPO): Here the shares or ownership stake of the private company are

issued to the public for the first time in the stock market. Often, investment bank gets involved in

the process and undertake the process of underwriting where they determined the share price,

develop prospectus, number of shares to be issued and promote the share issue among the

potential investors.

statement and balance sheet.

It is also important to analyse the operational efficiency of the firm using average

collection period and average payment period.

This is also helpful for identifying the profitability of company along with the business

risk to firms.

It also helps in determining the financial risk of firms including planning and forecasting

of futures.

Further, it is also helpful for the business to compare its performance with its own past

performance along with that of others competitors (Agbloyor and et.al., 2021).

For example, Gross profit margin of A company is 25% in the year 2020 while the gross

profit margin of B company is 20% in the same year. It means that company A is more profitable

than B and is earning high profit percentage than its competitors. This provides an opportunity to

company A that they can gain competitive advantage if they improve its profitability more. This

indicates that ratio analysis is most important part of every business (Lindvall and Larsson,

2017).

Question B4

There are many popular and potential methods of raising finance in the business which include

initial public offering or IPO and offer through sale (Choudhary, Merkley and Schipper, 2021).

Business must choose those method for raising finance which helps in making arrangement for

finance for the business operations. Floatation involves selling and issuing shares to the public

which facilitates raising finance from external sources. The two methods of floating to the stock

market are as follows:

Initial public offering (IPO): Here the shares or ownership stake of the private company are

issued to the public for the first time in the stock market. Often, investment bank gets involved in

the process and undertake the process of underwriting where they determined the share price,

develop prospectus, number of shares to be issued and promote the share issue among the

potential investors.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

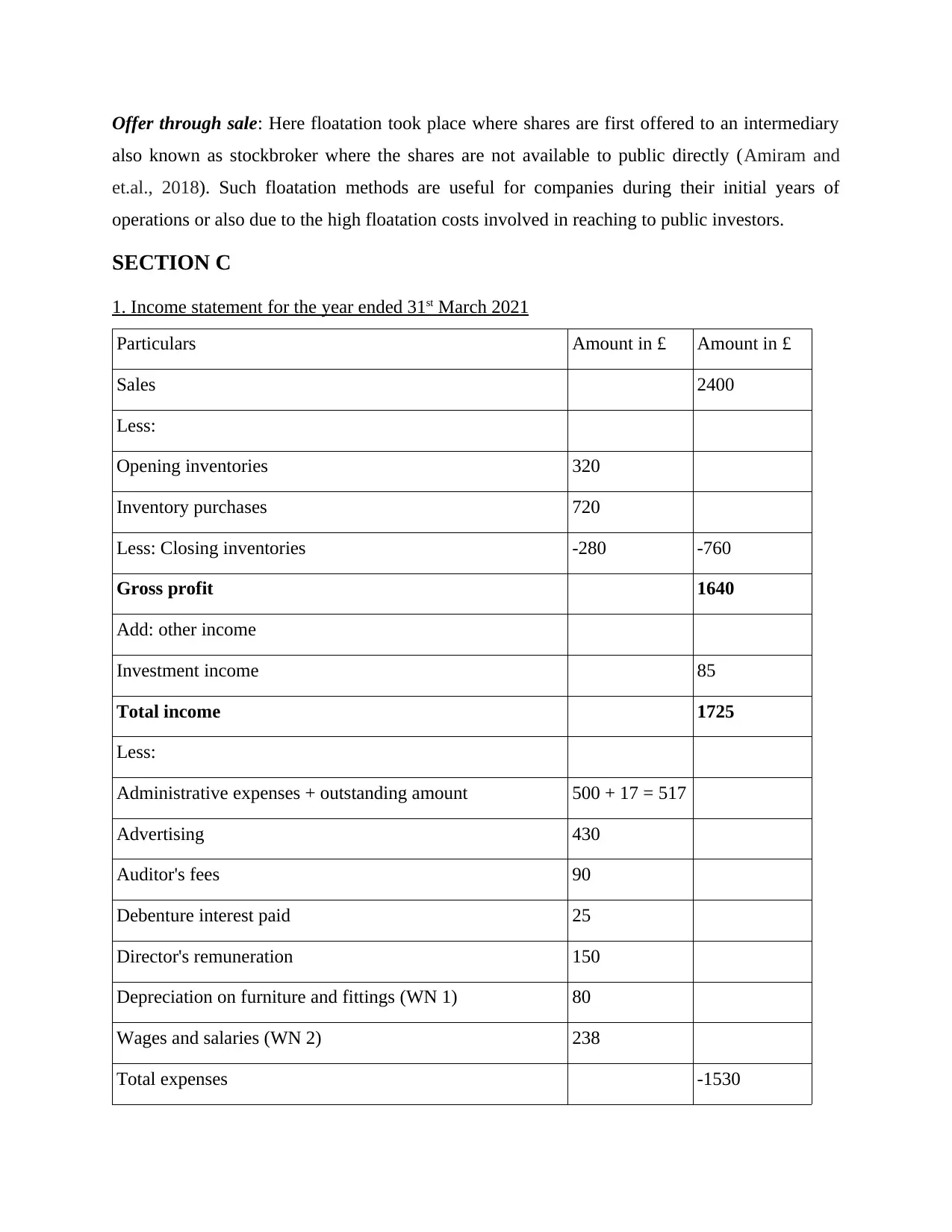

Offer through sale: Here floatation took place where shares are first offered to an intermediary

also known as stockbroker where the shares are not available to public directly (Amiram and

et.al., 2018). Such floatation methods are useful for companies during their initial years of

operations or also due to the high floatation costs involved in reaching to public investors.

SECTION C

1. Income statement for the year ended 31st March 2021

Particulars Amount in £ Amount in £

Sales 2400

Less:

Opening inventories 320

Inventory purchases 720

Less: Closing inventories -280 -760

Gross profit 1640

Add: other income

Investment income 85

Total income 1725

Less:

Administrative expenses + outstanding amount 500 + 17 = 517

Advertising 430

Auditor's fees 90

Debenture interest paid 25

Director's remuneration 150

Depreciation on furniture and fittings (WN 1) 80

Wages and salaries (WN 2) 238

Total expenses -1530

also known as stockbroker where the shares are not available to public directly (Amiram and

et.al., 2018). Such floatation methods are useful for companies during their initial years of

operations or also due to the high floatation costs involved in reaching to public investors.

SECTION C

1. Income statement for the year ended 31st March 2021

Particulars Amount in £ Amount in £

Sales 2400

Less:

Opening inventories 320

Inventory purchases 720

Less: Closing inventories -280 -760

Gross profit 1640

Add: other income

Investment income 85

Total income 1725

Less:

Administrative expenses + outstanding amount 500 + 17 = 517

Advertising 430

Auditor's fees 90

Debenture interest paid 25

Director's remuneration 150

Depreciation on furniture and fittings (WN 1) 80

Wages and salaries (WN 2) 238

Total expenses -1530

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Profit before tax 195

Less: Tax liability -39

Profit after tax 156

Less: dividends

Preference dividend 10

Ordinary dividend 130 -140

Retained earnings for the year 16

Working notes:

1. Depreciation on furniture and fittings = 400 * 20% = 80

2. Wages and salaries amount to be shown in income statement = 260 – paid in advance

= 260 – 22 = 238.

2. Calculation of correct tax liability for the company

Tax liability estimated on years profit = 39000

Correct corporation tax liabilities = Profit before tax + unallowable deductions (depreciation)

= 195 + 80 = 275

corporation tax liability = 275 * 19% = 52.25

There is a difference in the amount of tax liability estimated and the tax liability occurred

due to the difference in the amount of profit earned before and after allowing for depreciation as

deduction. The correct corporation tax liability has been calculated through considering profit

without allowing for depreciation and applying the flat tax rate applicable on corporate profit @

19% (Flower and Ebbers, 2018). However, the liability differs from the estimated tax liability

because the latter may be based on the profit mention in income statement or also may be

estimated by deducting depreciation amount from the taxable income. In this way, due to all

these reasons there is a difference in the actual corporation tax liability and estimated tax

liability.

3. Preparation of Statement of financial position as at 31st March 2021

Particulars Amount in £

Less: Tax liability -39

Profit after tax 156

Less: dividends

Preference dividend 10

Ordinary dividend 130 -140

Retained earnings for the year 16

Working notes:

1. Depreciation on furniture and fittings = 400 * 20% = 80

2. Wages and salaries amount to be shown in income statement = 260 – paid in advance

= 260 – 22 = 238.

2. Calculation of correct tax liability for the company

Tax liability estimated on years profit = 39000

Correct corporation tax liabilities = Profit before tax + unallowable deductions (depreciation)

= 195 + 80 = 275

corporation tax liability = 275 * 19% = 52.25

There is a difference in the amount of tax liability estimated and the tax liability occurred

due to the difference in the amount of profit earned before and after allowing for depreciation as

deduction. The correct corporation tax liability has been calculated through considering profit

without allowing for depreciation and applying the flat tax rate applicable on corporate profit @

19% (Flower and Ebbers, 2018). However, the liability differs from the estimated tax liability

because the latter may be based on the profit mention in income statement or also may be

estimated by deducting depreciation amount from the taxable income. In this way, due to all

these reasons there is a difference in the actual corporation tax liability and estimated tax

liability.

3. Preparation of Statement of financial position as at 31st March 2021

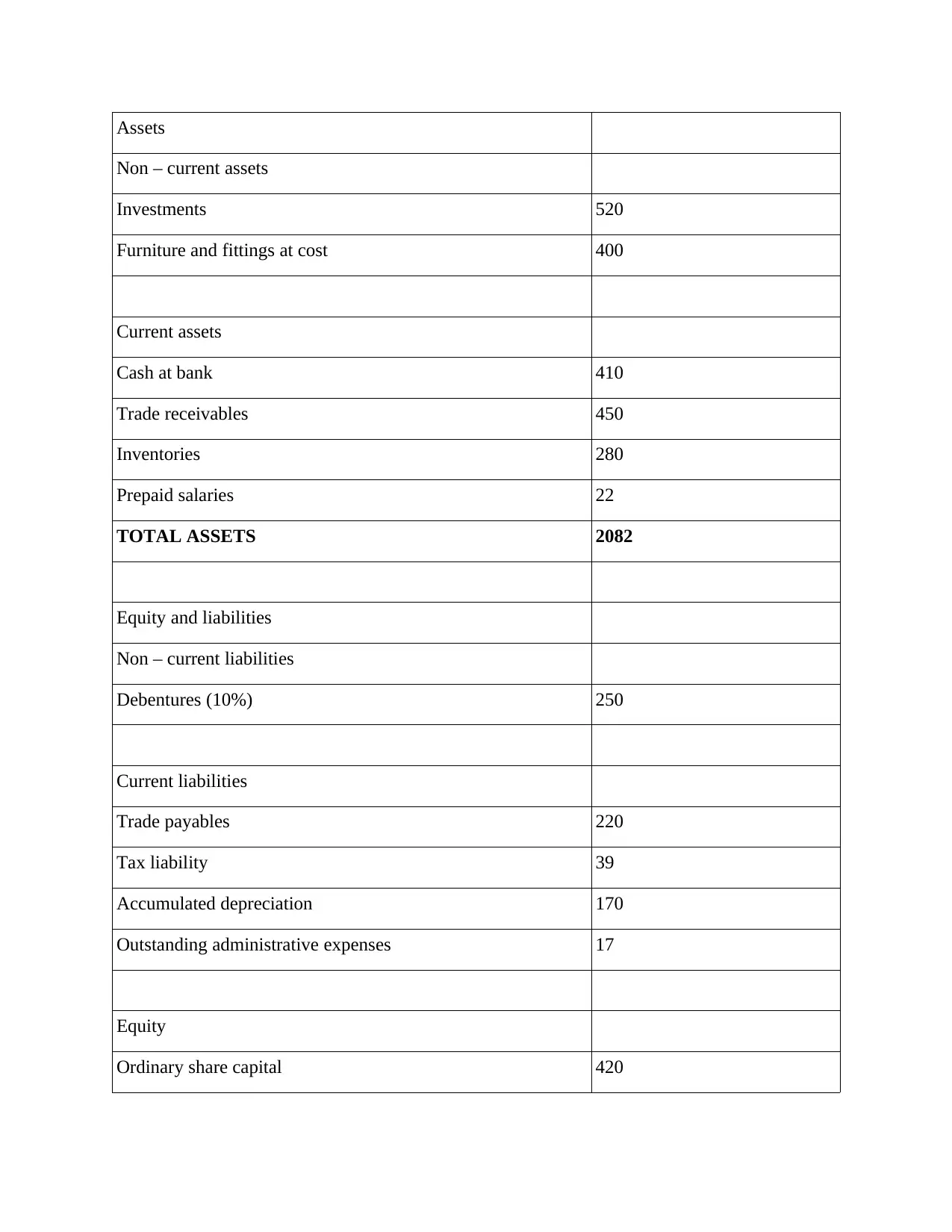

Particulars Amount in £

Assets

Non – current assets

Investments 520

Furniture and fittings at cost 400

Current assets

Cash at bank 410

Trade receivables 450

Inventories 280

Prepaid salaries 22

TOTAL ASSETS 2082

Equity and liabilities

Non – current liabilities

Debentures (10%) 250

Current liabilities

Trade payables 220

Tax liability 39

Accumulated depreciation 170

Outstanding administrative expenses 17

Equity

Ordinary share capital 420

Non – current assets

Investments 520

Furniture and fittings at cost 400

Current assets

Cash at bank 410

Trade receivables 450

Inventories 280

Prepaid salaries 22

TOTAL ASSETS 2082

Equity and liabilities

Non – current liabilities

Debentures (10%) 250

Current liabilities

Trade payables 220

Tax liability 39

Accumulated depreciation 170

Outstanding administrative expenses 17

Equity

Ordinary share capital 420

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

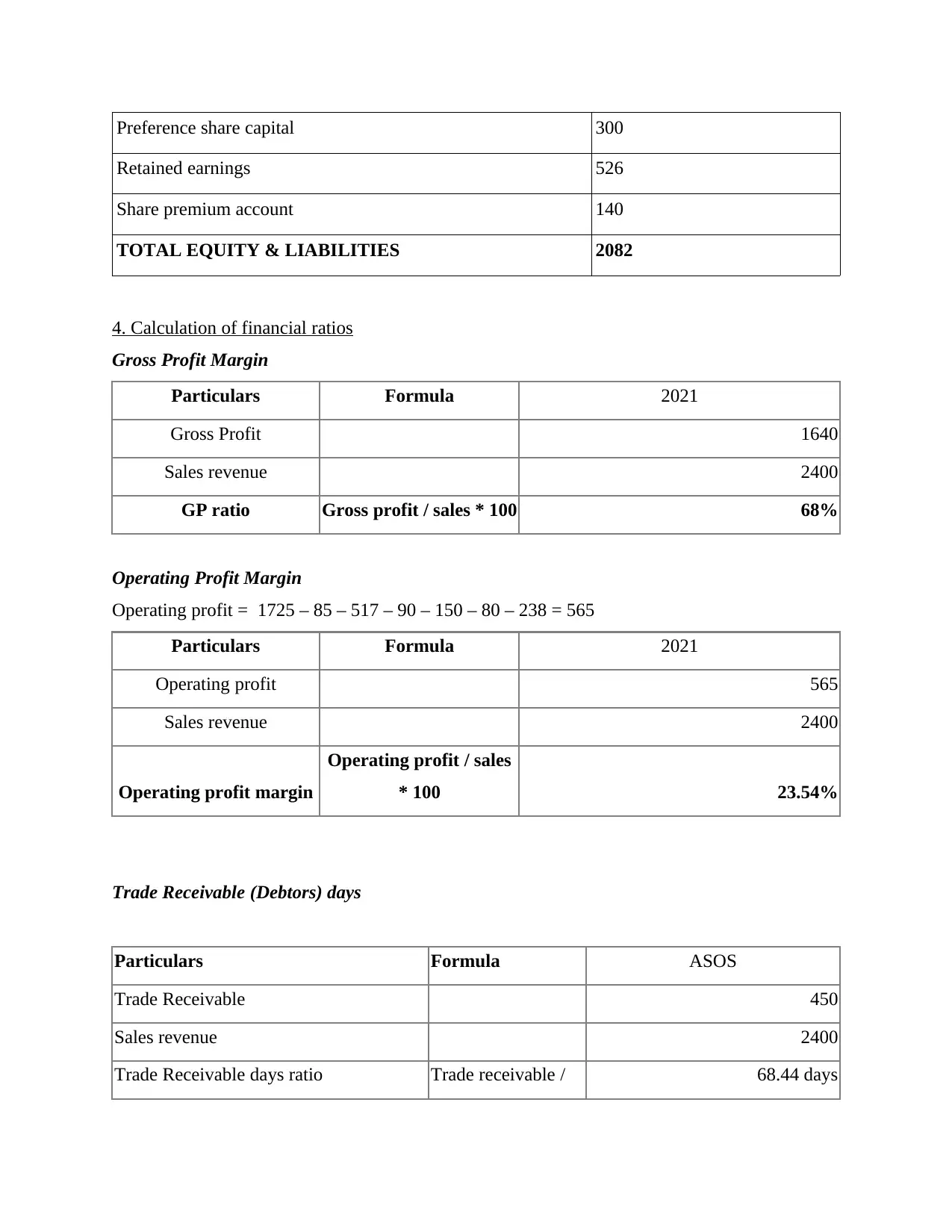

Preference share capital 300

Retained earnings 526

Share premium account 140

TOTAL EQUITY & LIABILITIES 2082

4. Calculation of financial ratios

Gross Profit Margin

Particulars Formula 2021

Gross Profit 1640

Sales revenue 2400

GP ratio Gross profit / sales * 100 68%

Operating Profit Margin

Operating profit = 1725 – 85 – 517 – 90 – 150 – 80 – 238 = 565

Particulars Formula 2021

Operating profit 565

Sales revenue 2400

Operating profit margin

Operating profit / sales

* 100 23.54%

Trade Receivable (Debtors) days

Particulars Formula ASOS

Trade Receivable 450

Sales revenue 2400

Trade Receivable days ratio Trade receivable / 68.44 days

Retained earnings 526

Share premium account 140

TOTAL EQUITY & LIABILITIES 2082

4. Calculation of financial ratios

Gross Profit Margin

Particulars Formula 2021

Gross Profit 1640

Sales revenue 2400

GP ratio Gross profit / sales * 100 68%

Operating Profit Margin

Operating profit = 1725 – 85 – 517 – 90 – 150 – 80 – 238 = 565

Particulars Formula 2021

Operating profit 565

Sales revenue 2400

Operating profit margin

Operating profit / sales

* 100 23.54%

Trade Receivable (Debtors) days

Particulars Formula ASOS

Trade Receivable 450

Sales revenue 2400

Trade Receivable days ratio Trade receivable / 68.44 days

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

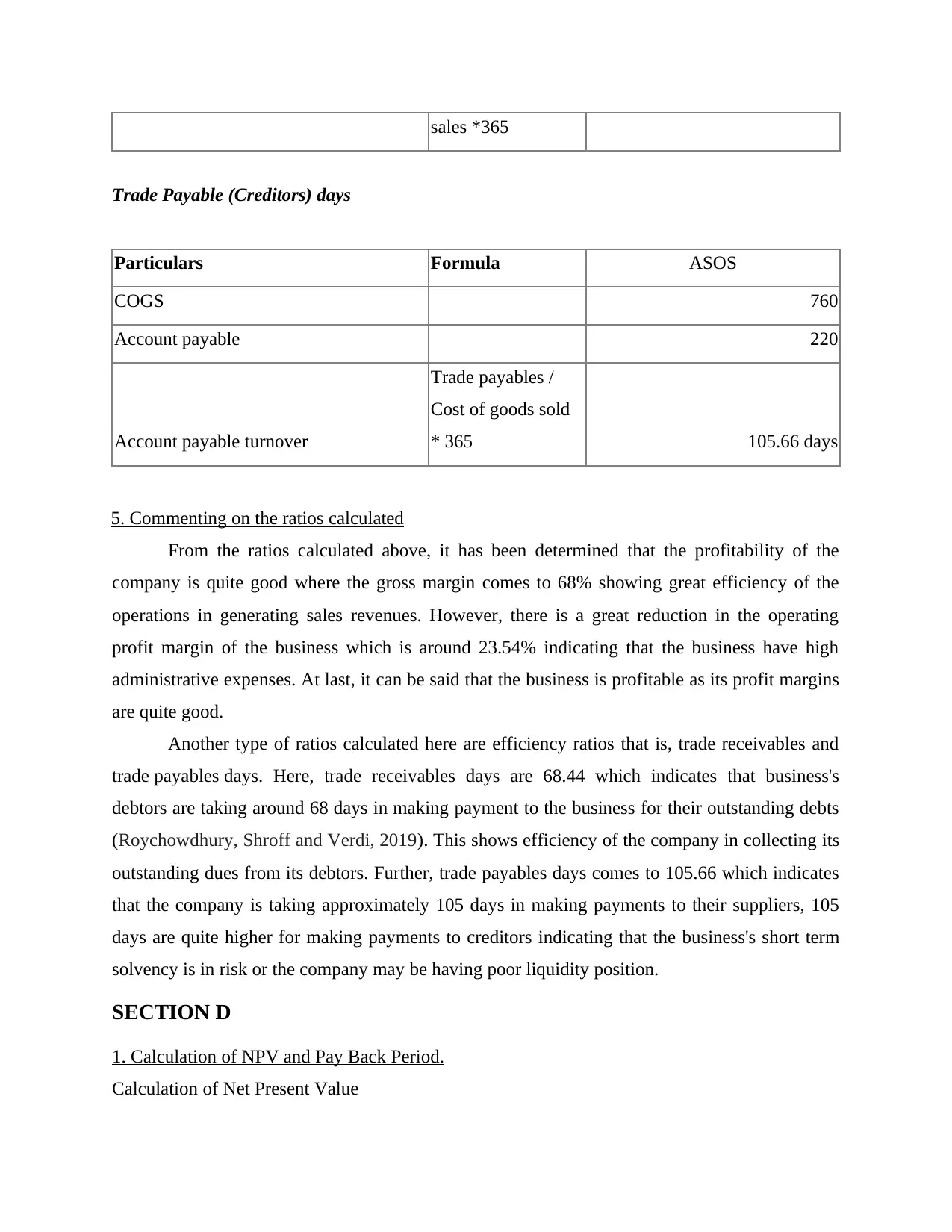

sales *365

Trade Payable (Creditors) days

Particulars Formula ASOS

COGS 760

Account payable 220

Account payable turnover

Trade payables /

Cost of goods sold

* 365 105.66 days

5. Commenting on the ratios calculated

From the ratios calculated above, it has been determined that the profitability of the

company is quite good where the gross margin comes to 68% showing great efficiency of the

operations in generating sales revenues. However, there is a great reduction in the operating

profit margin of the business which is around 23.54% indicating that the business have high

administrative expenses. At last, it can be said that the business is profitable as its profit margins

are quite good.

Another type of ratios calculated here are efficiency ratios that is, trade receivables and

trade payables days. Here, trade receivables days are 68.44 which indicates that business's

debtors are taking around 68 days in making payment to the business for their outstanding debts

(Roychowdhury, Shroff and Verdi, 2019). This shows efficiency of the company in collecting its

outstanding dues from its debtors. Further, trade payables days comes to 105.66 which indicates

that the company is taking approximately 105 days in making payments to their suppliers, 105

days are quite higher for making payments to creditors indicating that the business's short term

solvency is in risk or the company may be having poor liquidity position.

SECTION D

1. Calculation of NPV and Pay Back Period.

Calculation of Net Present Value

Trade Payable (Creditors) days

Particulars Formula ASOS

COGS 760

Account payable 220

Account payable turnover

Trade payables /

Cost of goods sold

* 365 105.66 days

5. Commenting on the ratios calculated

From the ratios calculated above, it has been determined that the profitability of the

company is quite good where the gross margin comes to 68% showing great efficiency of the

operations in generating sales revenues. However, there is a great reduction in the operating

profit margin of the business which is around 23.54% indicating that the business have high

administrative expenses. At last, it can be said that the business is profitable as its profit margins

are quite good.

Another type of ratios calculated here are efficiency ratios that is, trade receivables and

trade payables days. Here, trade receivables days are 68.44 which indicates that business's

debtors are taking around 68 days in making payment to the business for their outstanding debts

(Roychowdhury, Shroff and Verdi, 2019). This shows efficiency of the company in collecting its

outstanding dues from its debtors. Further, trade payables days comes to 105.66 which indicates

that the company is taking approximately 105 days in making payments to their suppliers, 105

days are quite higher for making payments to creditors indicating that the business's short term

solvency is in risk or the company may be having poor liquidity position.

SECTION D

1. Calculation of NPV and Pay Back Period.

Calculation of Net Present Value

Formula: Present value of cash inflow — Initial investment

Project A

Calculation of Present value of cash inflows

Years Cash inflow + Cash

saving — running

cost (£)

Discounting factor

@10%

Present value of cash

inflows (£)

1 68300

(93000 + 9500 –

34200)

0.91 62153

2 68300

(93000 + 9500 –

34200)

0.83 56689

3 68300

(93000 + 9500 –

34200)

0.75 51225

4 68300

(93000 + 9500 –

34200)

0.68 46444

5 68300

(93000 + 9500 –

34200)

0.62 42346

5 (working capital and

savage cash inflow)

30000

(22500 + 7500)

0.62 18600

Total Present value of Cash inflows = £62153 + £56689 + £51225 + £46444 + £42346 + £18600

= £277457

Present value of cash outflow or initial investment = £225000

NPV of Project A = 277457 – 225000 = £52475

Project B

Project A

Calculation of Present value of cash inflows

Years Cash inflow + Cash

saving — running

cost (£)

Discounting factor

@10%

Present value of cash

inflows (£)

1 68300

(93000 + 9500 –

34200)

0.91 62153

2 68300

(93000 + 9500 –

34200)

0.83 56689

3 68300

(93000 + 9500 –

34200)

0.75 51225

4 68300

(93000 + 9500 –

34200)

0.68 46444

5 68300

(93000 + 9500 –

34200)

0.62 42346

5 (working capital and

savage cash inflow)

30000

(22500 + 7500)

0.62 18600

Total Present value of Cash inflows = £62153 + £56689 + £51225 + £46444 + £42346 + £18600

= £277457

Present value of cash outflow or initial investment = £225000

NPV of Project A = 277457 – 225000 = £52475

Project B

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 18

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.