Organisational Finance: Reporting, Auditing & Financial Management

VerifiedAdded on 2023/06/12

|9

|2169

|97

Report

AI Summary

This report provides an overview of key aspects of organisational finance, including practices for recognizing and reviewing profit and losses, the concept of financial probity, examples of fraudulent behavior, and the purposes of accounting software for managing finances. It also covers budgeting factors, taxation and superannuation obligations, and the Acts governing financial reporting and auditing. The report outlines GST reporting requirements, defines PAYG withholding and installments, and offers recommendations for organizational improvement based on financial analysis. Additionally, it discusses the preparation of financial management reports, emphasizing monitoring financial positions, ensuring timely customer payments, meeting tax deadlines, maintaining updated accounting records, and controlling overhead costs. The report concludes by highlighting the importance of budgeting and financial reporting for successful operation in a competitive market.

MANAGE

ORGANISATIONAL

FINANCE

ORGANISATIONAL

FINANCE

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Table of Contents

INTRODUCTION.................................................................................................................................................. 3

MAIN BODY........................................................................................................................................................ 3

LIST THREE PRACTISES WHICH CAN BE USED TO RECOGNISE AND REVIEW PROFITS AND LOSSES FROM A PROFIT AND LOSS STATEMENT.3

DEFINE THE CONCEPT OF FINANCIAL PROBITY AND ITS IMPORTANCE TO A BUSINESS...................................................................3

LIST FOUR EXAMPLES OF WHAT WOULD BE CONSIDERED FRAUDULENT BEHAVIOUR IN REGARD TO COMPANY FUNDS I.E., NOT MEETING

FINANCIAL PROBITY REQUIREMENTS.................................................................................................................................3

LIST FIVE PURPOSES OF ACCOUNTING SOFTWARE THAT CAN BE USED FOR MANAGING FINANCE....................................................4

LIST THREE FACTORS OF A BUDGET..................................................................................................................................4

STATE FOUR MAIN TAXATION AND SUPERANNUATION OBLIGATIONS FOR A INDUSTRY. CONCISELY DISCUSS EACH OBLIGATION............4

ASCERTAIN THE ACT THAT FEATURES REQUIREMENTS FOR FINANCE BASED REPORTING, AUDITING AND EXPLAIN THE RELATED NEEDS

FOR BUSINESSES FOR PREPARING AND LODGING FINANCIAL REPORTS UNDER SUCH ACTS............................................................4

OUTLINE THE REPORTING REQUIREMENTS THAT ARE HELPFUL IN CASE OF GOODS AND SERVICES TAX (GST)...................................5

DEFINE PAYG WITHHOLDING AND PAYG INSTALMENTS......................................................................................................5

REVIEW THE REPORT AND STATE ANY 5 RECOMMENDATIONS THAT CAN BE ADAPTED BY ANY ORGANISATION IN RESPONSE TO YOUR

ANALYSIS.................................................................................................................................................................... 5

ASSESMENT TASK 2:............................................................................................................................................ 7

PREPARATION OF FINANCIAL MANAGEMENT......................................................................................................................7

THERE ARE MANY STEPS REQUIRED IN PREPARING A FINANCIAL MANAGEMENT RELATED REPORT SUCH AS:....................................7

ESTABLISH BUDGETS AND ALLOCATE FUNDS ACCORDINGLY...................................................................................................7

CONCLUSION...................................................................................................................................................... 8

REFERENCES....................................................................................................................................................................9

INTRODUCTION.................................................................................................................................................. 3

MAIN BODY........................................................................................................................................................ 3

LIST THREE PRACTISES WHICH CAN BE USED TO RECOGNISE AND REVIEW PROFITS AND LOSSES FROM A PROFIT AND LOSS STATEMENT.3

DEFINE THE CONCEPT OF FINANCIAL PROBITY AND ITS IMPORTANCE TO A BUSINESS...................................................................3

LIST FOUR EXAMPLES OF WHAT WOULD BE CONSIDERED FRAUDULENT BEHAVIOUR IN REGARD TO COMPANY FUNDS I.E., NOT MEETING

FINANCIAL PROBITY REQUIREMENTS.................................................................................................................................3

LIST FIVE PURPOSES OF ACCOUNTING SOFTWARE THAT CAN BE USED FOR MANAGING FINANCE....................................................4

LIST THREE FACTORS OF A BUDGET..................................................................................................................................4

STATE FOUR MAIN TAXATION AND SUPERANNUATION OBLIGATIONS FOR A INDUSTRY. CONCISELY DISCUSS EACH OBLIGATION............4

ASCERTAIN THE ACT THAT FEATURES REQUIREMENTS FOR FINANCE BASED REPORTING, AUDITING AND EXPLAIN THE RELATED NEEDS

FOR BUSINESSES FOR PREPARING AND LODGING FINANCIAL REPORTS UNDER SUCH ACTS............................................................4

OUTLINE THE REPORTING REQUIREMENTS THAT ARE HELPFUL IN CASE OF GOODS AND SERVICES TAX (GST)...................................5

DEFINE PAYG WITHHOLDING AND PAYG INSTALMENTS......................................................................................................5

REVIEW THE REPORT AND STATE ANY 5 RECOMMENDATIONS THAT CAN BE ADAPTED BY ANY ORGANISATION IN RESPONSE TO YOUR

ANALYSIS.................................................................................................................................................................... 5

ASSESMENT TASK 2:............................................................................................................................................ 7

PREPARATION OF FINANCIAL MANAGEMENT......................................................................................................................7

THERE ARE MANY STEPS REQUIRED IN PREPARING A FINANCIAL MANAGEMENT RELATED REPORT SUCH AS:....................................7

ESTABLISH BUDGETS AND ALLOCATE FUNDS ACCORDINGLY...................................................................................................7

CONCLUSION...................................................................................................................................................... 8

REFERENCES....................................................................................................................................................................9

INTRODUCTION

The report prepared below explains practices that can be put in use for recognising and

reviewing profit and losses (Guthrie AM and et.al., 2021). It also explains uses of acts such as GST

and PAYG. It also takes in account components of a budget as well. It helps to find out related

issues in a running business and what can be frauds that counter the working and running of a

company. It is useful in finding out concept of financial probity. It states purposes of accounting

software that would help to manage finance and fund related operations.

MAIN BODY

List three practises which can be used to recognise and review profits and losses from a profit

and loss statement.

Cost of goods sold

Net income

Source of income

Define the concept of financial probity and its importance to a business.

Probity is the proof of ethical behaviour in a specific practice. Financial probity states,

strict following of code of ethics that are based on absolute honesty, especially in monetary areas

or commercial matters and which are beyond legal requirements (Chen, Yao and Zhou, 2021).

Probity requirements:

Handle tender members equally and fairly.

Implement public sector moral and values.

Sustain confidentiality information and important data of tender participants.

List four examples of what would be considered fraudulent behaviour in regard to company

funds i.e., not meeting financial probity requirements.

1. Timecard fraud and Ghost employee schemes.

2. Frauds related to commission.

3. Credit card and expenditure reporting scam.

4. Fake vendor frauds.

The report prepared below explains practices that can be put in use for recognising and

reviewing profit and losses (Guthrie AM and et.al., 2021). It also explains uses of acts such as GST

and PAYG. It also takes in account components of a budget as well. It helps to find out related

issues in a running business and what can be frauds that counter the working and running of a

company. It is useful in finding out concept of financial probity. It states purposes of accounting

software that would help to manage finance and fund related operations.

MAIN BODY

List three practises which can be used to recognise and review profits and losses from a profit

and loss statement.

Cost of goods sold

Net income

Source of income

Define the concept of financial probity and its importance to a business.

Probity is the proof of ethical behaviour in a specific practice. Financial probity states,

strict following of code of ethics that are based on absolute honesty, especially in monetary areas

or commercial matters and which are beyond legal requirements (Chen, Yao and Zhou, 2021).

Probity requirements:

Handle tender members equally and fairly.

Implement public sector moral and values.

Sustain confidentiality information and important data of tender participants.

List four examples of what would be considered fraudulent behaviour in regard to company

funds i.e., not meeting financial probity requirements.

1. Timecard fraud and Ghost employee schemes.

2. Frauds related to commission.

3. Credit card and expenditure reporting scam.

4. Fake vendor frauds.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

List five purposes of accounting software that can be used for managing finance.

1. Book keeping

2. Budgeting and forecasting

3. Inventory management

4. Expense management

5. Payroll

List three factors of a budget.

Variable costs

Fixed costs

Cash flow

State four main taxation and superannuation obligations for a industry. Concisely discuss each

obligation.

Superannuation Guarantee: It is said to be the foundation of mandatory superannuation system. It

helps to lift living standards of people after retirement and reflect a positive effect on

related economy (Mahesh, Vijayapala and Dasanayaka, 2018).

Fringe Benefits Tax (FBT): It is a type of tax that is being paid by employers on benefits

to an employee over their paid salaries or wages.

Goods and Services Tax (GST): It is sort of tax at a rate of 10% applicable in most goods,

services and other things that are being consumed or sold. If the related business is

registered for GST it is necessary for a company to collect extra amount from customers.

Pay As You Go (PAYG): When employee of a company is paid, it is necessary to hold a

certain quantity of tax from their payslip. It is a process of holding tax on behalf of staff

persons.

Ascertain the Act that features requirements for finance based reporting, auditing and explain

the related needs for businesses for preparing and lodging financial reports under such

Acts.

Section 292 of corporation Act 2021 demands the following entities to develop finance

related statements and reports:

Public firms

Small proprietary organisations that are controlled by foreign entities.

1. Book keeping

2. Budgeting and forecasting

3. Inventory management

4. Expense management

5. Payroll

List three factors of a budget.

Variable costs

Fixed costs

Cash flow

State four main taxation and superannuation obligations for a industry. Concisely discuss each

obligation.

Superannuation Guarantee: It is said to be the foundation of mandatory superannuation system. It

helps to lift living standards of people after retirement and reflect a positive effect on

related economy (Mahesh, Vijayapala and Dasanayaka, 2018).

Fringe Benefits Tax (FBT): It is a type of tax that is being paid by employers on benefits

to an employee over their paid salaries or wages.

Goods and Services Tax (GST): It is sort of tax at a rate of 10% applicable in most goods,

services and other things that are being consumed or sold. If the related business is

registered for GST it is necessary for a company to collect extra amount from customers.

Pay As You Go (PAYG): When employee of a company is paid, it is necessary to hold a

certain quantity of tax from their payslip. It is a process of holding tax on behalf of staff

persons.

Ascertain the Act that features requirements for finance based reporting, auditing and explain

the related needs for businesses for preparing and lodging financial reports under such

Acts.

Section 292 of corporation Act 2021 demands the following entities to develop finance

related statements and reports:

Public firms

Small proprietary organisations that are controlled by foreign entities.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

All enumerated and managed investment schemes.

Small firms that shareowners direct to facilitate a financial statement.

Outline the reporting requirements that are helpful in case of goods and services tax (GST).

It can be explained as a multi- stage, designed oriented tax that is implemented on every

value addition, replacing multiple indirect nature taxes that involves excise duty, service-related

taxes, VAT etc. Goods and services are involved under a single domestic indirect taxable law

(Mittal, 2020). There are many records that must be kept and recorded under such report that is

inclusion of bills of supply, credit and debit reports etc.

Define PAYG withholding and PAYG instalments.

Pay as you go withholding obligations for non-profitable companies are similar as in case

of businesses. Enterprises that are exempted from income taxes are not exempted from PAYG

withholding obligations (Migdadi, Zaid, Yousif and Almestarihi, 2018). If any company has

employees, it Is necessary to withhold quantity from their pay and send the withheld amount

with the help of PAYG withholding system.

Under PAYG instalment it can be explained as a system that is helpful for making payment in

instalments during the income year towards a organisation or a respectives person’s expected

liability on invested income.

Review the report and state any 5 recommendations that can be adapted by any organisation in

response to your analysis.

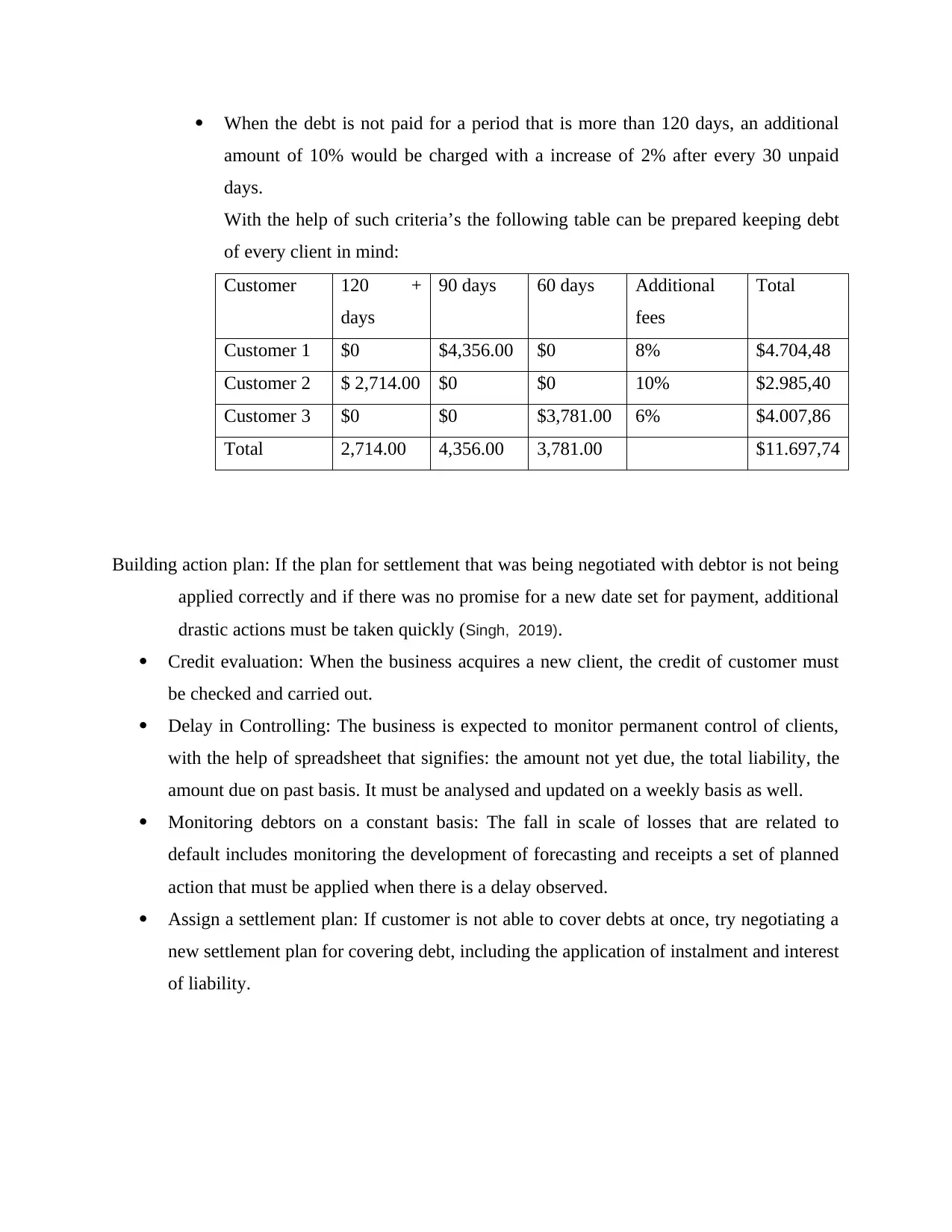

According to table it can be recorded that there are 3 customers in business, it is

necessary to make best use of company’s protocol for carrying out debt collection using

a percentage that is proportional to the period of original debt (Provan and Pryor, 2019).

In relation with organisation debt collection protocol, the following criteria would be

helpful:

If the debt is not paid for a time period of 60 to 90 days, an excess of 6% interest

would be applied.

With debt amounting for the period between 90 to 120 days additional interest

rate of 8% would be implemented.

Small firms that shareowners direct to facilitate a financial statement.

Outline the reporting requirements that are helpful in case of goods and services tax (GST).

It can be explained as a multi- stage, designed oriented tax that is implemented on every

value addition, replacing multiple indirect nature taxes that involves excise duty, service-related

taxes, VAT etc. Goods and services are involved under a single domestic indirect taxable law

(Mittal, 2020). There are many records that must be kept and recorded under such report that is

inclusion of bills of supply, credit and debit reports etc.

Define PAYG withholding and PAYG instalments.

Pay as you go withholding obligations for non-profitable companies are similar as in case

of businesses. Enterprises that are exempted from income taxes are not exempted from PAYG

withholding obligations (Migdadi, Zaid, Yousif and Almestarihi, 2018). If any company has

employees, it Is necessary to withhold quantity from their pay and send the withheld amount

with the help of PAYG withholding system.

Under PAYG instalment it can be explained as a system that is helpful for making payment in

instalments during the income year towards a organisation or a respectives person’s expected

liability on invested income.

Review the report and state any 5 recommendations that can be adapted by any organisation in

response to your analysis.

According to table it can be recorded that there are 3 customers in business, it is

necessary to make best use of company’s protocol for carrying out debt collection using

a percentage that is proportional to the period of original debt (Provan and Pryor, 2019).

In relation with organisation debt collection protocol, the following criteria would be

helpful:

If the debt is not paid for a time period of 60 to 90 days, an excess of 6% interest

would be applied.

With debt amounting for the period between 90 to 120 days additional interest

rate of 8% would be implemented.

When the debt is not paid for a period that is more than 120 days, an additional

amount of 10% would be charged with a increase of 2% after every 30 unpaid

days.

With the help of such criteria’s the following table can be prepared keeping debt

of every client in mind:

Customer 120 +

days

90 days 60 days Additional

fees

Total

Customer 1 $0 $4,356.00 $0 8% $4.704,48

Customer 2 $ 2,714.00 $0 $0 10% $2.985,40

Customer 3 $0 $0 $3,781.00 6% $4.007,86

Total 2,714.00 4,356.00 3,781.00 $11.697,74

Building action plan: If the plan for settlement that was being negotiated with debtor is not being

applied correctly and if there was no promise for a new date set for payment, additional

drastic actions must be taken quickly (Singh, 2019).

Credit evaluation: When the business acquires a new client, the credit of customer must

be checked and carried out.

Delay in Controlling: The business is expected to monitor permanent control of clients,

with the help of spreadsheet that signifies: the amount not yet due, the total liability, the

amount due on past basis. It must be analysed and updated on a weekly basis as well.

Monitoring debtors on a constant basis: The fall in scale of losses that are related to

default includes monitoring the development of forecasting and receipts a set of planned

action that must be applied when there is a delay observed.

Assign a settlement plan: If customer is not able to cover debts at once, try negotiating a

new settlement plan for covering debt, including the application of instalment and interest

of liability.

amount of 10% would be charged with a increase of 2% after every 30 unpaid

days.

With the help of such criteria’s the following table can be prepared keeping debt

of every client in mind:

Customer 120 +

days

90 days 60 days Additional

fees

Total

Customer 1 $0 $4,356.00 $0 8% $4.704,48

Customer 2 $ 2,714.00 $0 $0 10% $2.985,40

Customer 3 $0 $0 $3,781.00 6% $4.007,86

Total 2,714.00 4,356.00 3,781.00 $11.697,74

Building action plan: If the plan for settlement that was being negotiated with debtor is not being

applied correctly and if there was no promise for a new date set for payment, additional

drastic actions must be taken quickly (Singh, 2019).

Credit evaluation: When the business acquires a new client, the credit of customer must

be checked and carried out.

Delay in Controlling: The business is expected to monitor permanent control of clients,

with the help of spreadsheet that signifies: the amount not yet due, the total liability, the

amount due on past basis. It must be analysed and updated on a weekly basis as well.

Monitoring debtors on a constant basis: The fall in scale of losses that are related to

default includes monitoring the development of forecasting and receipts a set of planned

action that must be applied when there is a delay observed.

Assign a settlement plan: If customer is not able to cover debts at once, try negotiating a

new settlement plan for covering debt, including the application of instalment and interest

of liability.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

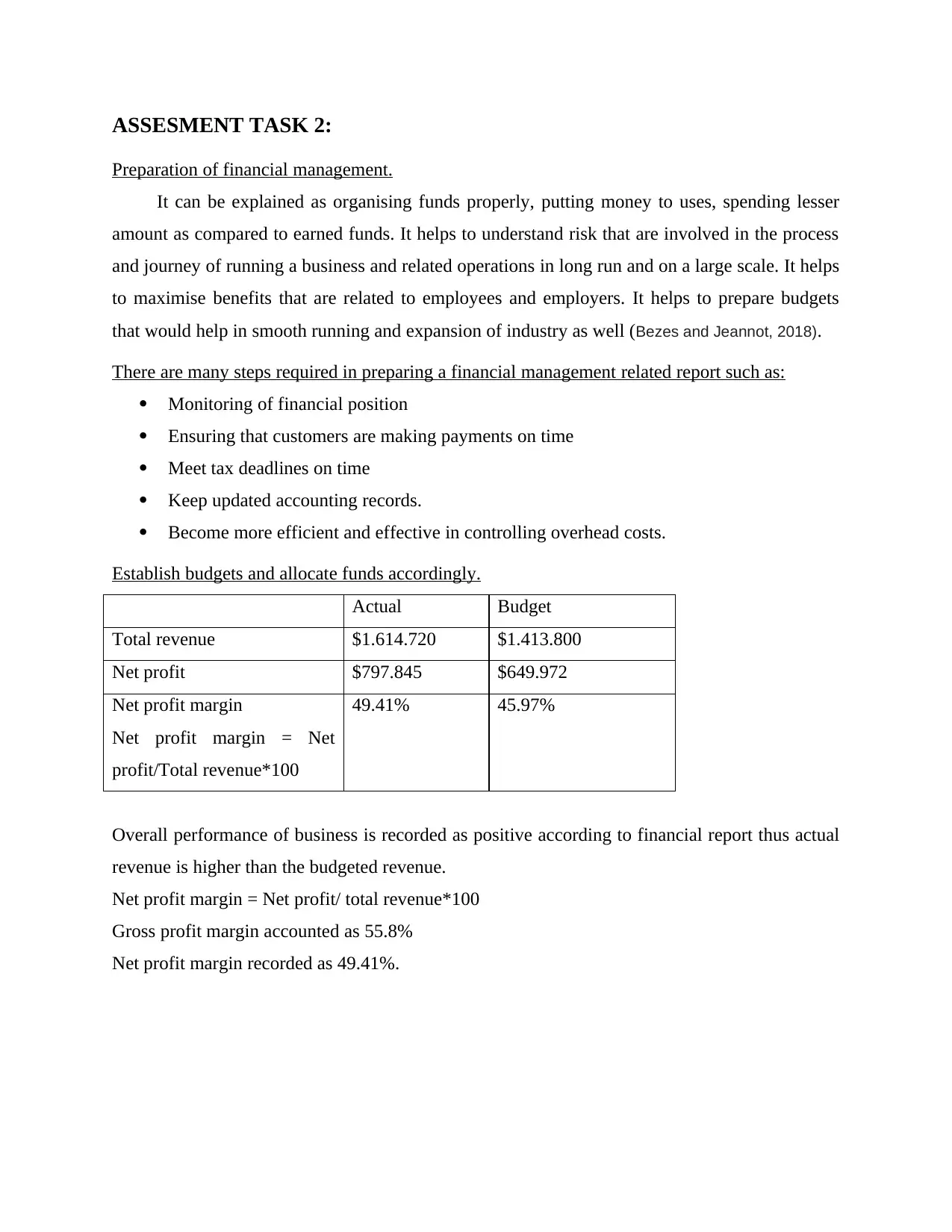

ASSESMENT TASK 2:

Preparation of financial management.

It can be explained as organising funds properly, putting money to uses, spending lesser

amount as compared to earned funds. It helps to understand risk that are involved in the process

and journey of running a business and related operations in long run and on a large scale. It helps

to maximise benefits that are related to employees and employers. It helps to prepare budgets

that would help in smooth running and expansion of industry as well (Bezes and Jeannot, 2018).

There are many steps required in preparing a financial management related report such as:

Monitoring of financial position

Ensuring that customers are making payments on time

Meet tax deadlines on time

Keep updated accounting records.

Become more efficient and effective in controlling overhead costs.

Establish budgets and allocate funds accordingly.

Actual Budget

Total revenue $1.614.720 $1.413.800

Net profit $797.845 $649.972

Net profit margin

Net profit margin = Net

profit/Total revenue*100

49.41% 45.97%

Overall performance of business is recorded as positive according to financial report thus actual

revenue is higher than the budgeted revenue.

Net profit margin = Net profit/ total revenue*100

Gross profit margin accounted as 55.8%

Net profit margin recorded as 49.41%.

Preparation of financial management.

It can be explained as organising funds properly, putting money to uses, spending lesser

amount as compared to earned funds. It helps to understand risk that are involved in the process

and journey of running a business and related operations in long run and on a large scale. It helps

to maximise benefits that are related to employees and employers. It helps to prepare budgets

that would help in smooth running and expansion of industry as well (Bezes and Jeannot, 2018).

There are many steps required in preparing a financial management related report such as:

Monitoring of financial position

Ensuring that customers are making payments on time

Meet tax deadlines on time

Keep updated accounting records.

Become more efficient and effective in controlling overhead costs.

Establish budgets and allocate funds accordingly.

Actual Budget

Total revenue $1.614.720 $1.413.800

Net profit $797.845 $649.972

Net profit margin

Net profit margin = Net

profit/Total revenue*100

49.41% 45.97%

Overall performance of business is recorded as positive according to financial report thus actual

revenue is higher than the budgeted revenue.

Net profit margin = Net profit/ total revenue*100

Gross profit margin accounted as 55.8%

Net profit margin recorded as 49.41%.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

CONCLUSION

From the above prepared report, it can be concluded that preparation of budgets and

finance related reports are necessary to carry out activities in a market. it thus also gives

ideas as how to help in functioning of a company in competitive market. It provides a idea

of acts such as GST and PAYG. It also helps to understand planning of budgets and what are

its related factors.

From the above prepared report, it can be concluded that preparation of budgets and

finance related reports are necessary to carry out activities in a market. it thus also gives

ideas as how to help in functioning of a company in competitive market. It provides a idea

of acts such as GST and PAYG. It also helps to understand planning of budgets and what are

its related factors.

REFERENCES

Books and Journals

Bezes, P. and Jeannot, G., 2018. Autonomy and managerial reforms in Europe: Let or make

public managers manage?. Public administration. 96(1). pp.3-22.

Chen, H., Yao, Y. and Zhou, H., 2021. How does knowledge coupling affect exploratory and

exploitative innovation? The chained mediation role of organisational memory and

knowledge creation. Technology Analysis & Strategic Management 33(6). pp.713-727.

Guthrie AM, J., Linnenluecke, M.K., Martin‐Sardesai, A., Shen, Y. and Smith, T., 2021. On the

resilience of Australian public universities: why our institutions may fail unless vice‐

chancellors rethink broken commercial business models. Accounting & Finance.

Mahesh, D.D., Vijayapala, S. and Dasanayaka, S.W.S.B., 2018, May. Factors affecting the

intention to adopt big data technology: A study based on financial services industry of

Sri Lanka. In 2018 Moratuwa Engineering Research Conference (MERCon) (pp. 420-

425). IEEE.

Migdadi, M.M., Zaid, M.K.S.A., Yousif, M. and Almestarihi, R.D., 2018. An empirical

examination of collaborative knowledge management practices and organisational

performance: the mediating roles of supply chain integration and knowledge

quality. International Journal of Business Excellence. 14(2). pp.180-211.

Mittal, P., 2020. Big data and analytics: a data management perspective in public

administration. International Journal of Big Data Management. 1(2). pp.152-165.

Provan, D.J. and Pryor, P., 2019. The emergence of the occupational health and safety profession

in Australia. Safety science. 117. pp.428-436.

Singh, R., 2019, November. Organisational embeddedness as a moderator on the organisational

support, trust and workplace deviance relationships. In Evidence-based HRM: a Global

Forum for Empirical Scholarship. Emerald Publishing Limited.

Books and Journals

Bezes, P. and Jeannot, G., 2018. Autonomy and managerial reforms in Europe: Let or make

public managers manage?. Public administration. 96(1). pp.3-22.

Chen, H., Yao, Y. and Zhou, H., 2021. How does knowledge coupling affect exploratory and

exploitative innovation? The chained mediation role of organisational memory and

knowledge creation. Technology Analysis & Strategic Management 33(6). pp.713-727.

Guthrie AM, J., Linnenluecke, M.K., Martin‐Sardesai, A., Shen, Y. and Smith, T., 2021. On the

resilience of Australian public universities: why our institutions may fail unless vice‐

chancellors rethink broken commercial business models. Accounting & Finance.

Mahesh, D.D., Vijayapala, S. and Dasanayaka, S.W.S.B., 2018, May. Factors affecting the

intention to adopt big data technology: A study based on financial services industry of

Sri Lanka. In 2018 Moratuwa Engineering Research Conference (MERCon) (pp. 420-

425). IEEE.

Migdadi, M.M., Zaid, M.K.S.A., Yousif, M. and Almestarihi, R.D., 2018. An empirical

examination of collaborative knowledge management practices and organisational

performance: the mediating roles of supply chain integration and knowledge

quality. International Journal of Business Excellence. 14(2). pp.180-211.

Mittal, P., 2020. Big data and analytics: a data management perspective in public

administration. International Journal of Big Data Management. 1(2). pp.152-165.

Provan, D.J. and Pryor, P., 2019. The emergence of the occupational health and safety profession

in Australia. Safety science. 117. pp.428-436.

Singh, R., 2019, November. Organisational embeddedness as a moderator on the organisational

support, trust and workplace deviance relationships. In Evidence-based HRM: a Global

Forum for Empirical Scholarship. Emerald Publishing Limited.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 9

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.