Financial Management Report: Brand PLC and Lovewell Ltd Analysis

VerifiedAdded on 2021/02/21

|16

|3670

|24

Report

AI Summary

This financial management report delves into key concepts and practical applications. It begins with an introduction to financial management, emphasizing its role in controlling, managing, and directing business operations. The main body analyzes a right issue scenario for Brand PLC, calculating the number of shares to be issued, determining theoretical ex-rights prices, and evaluating expected earnings per share under different right issue prices. It then explores scrip dividends, outlining their benefits and drawbacks for both shareholders and the company. The report further examines investment appraisal techniques, specifically payback period and accounting rate of return, to assess the economic feasibility of a project for Lovewell Ltd. The payback period analysis determines the time required to recover the initial investment, while the accounting rate of return assesses the profitability of the investment. The report concludes with recommendations based on the financial analysis, providing insights for effective financial decision-making. The report aims to provide a comprehensive understanding of financial management principles and their application in real-world business scenarios, including decision-making related to right issues and investment projects.

Financial Management

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Table of Contents

INTRODUCTION...........................................................................................................................1

MAIN BODY ..................................................................................................................................1

Question 2 Right issue.................................................................................................................1

Question 3 Investment appraisal techniques................................................................................6

CONCLUSION..............................................................................................................................13

REFERENCES..............................................................................................................................14

INTRODUCTION...........................................................................................................................1

MAIN BODY ..................................................................................................................................1

Question 2 Right issue.................................................................................................................1

Question 3 Investment appraisal techniques................................................................................6

CONCLUSION..............................................................................................................................13

REFERENCES..............................................................................................................................14

INTRODUCTION

Financial management refers to controlling, managing, directing, evaluating the business

operational activities of the business organisation. It obtain the required fund and utilized in the

business to effective operation of the business function (Castrogiovanni and et. al 2016). It also

apply the basic accounting concepts, general principle in the financial activities of the entity.

Financial management is generally concerned with regular and adequate supply of fund in the

enterprises. It may cover the

financial aspects such as capital requirement, source of fund, investment fund, management of

cash and financial control over the enterprises. In the subject of financial management some of

the basic concepts includes that is defined in this report. For the better understanding of the

financial function in the business, report includes earning per share and right issue concept foer

brand plc and investment appraisal techniques of a food manufacturing company lovewell Ltd.

This report of the financial management is beneficial for the management of the particular

companies in the decision making process regarding company's earning or net profit and how

much amount cost to the company for issue price. And business can make decision regarding the

investment proposal that will be benefited for the organisation lovewell Ltd. So they can make

decision which option is best for organisation as well as increase the profitability in present

situation.

MAIN BODY

Question 2 Right issue

Right issue:

Right issue is basically share that are provided by the company to existing shareholder to

the company. It is also called as right offer. In the basic terms, it is defined as when a enterprises

require some additional capital in the business than it goes to present shareholder for the purpose

to issue the share at discount price for these existing shareholders. It is invitation to stakeholders

to purchase the share in the company at certain discount on market price (Cummins and Derrig,

2012). These are some benefit of the right issue that are discussed as below:

The main benefit to the shareholder is shares are issued at less price so they can purchsed

it on discount or minimum price from market rate.

All the benefit are the same that is given on ordinary share such as dividend, bonus share.

1

Financial management refers to controlling, managing, directing, evaluating the business

operational activities of the business organisation. It obtain the required fund and utilized in the

business to effective operation of the business function (Castrogiovanni and et. al 2016). It also

apply the basic accounting concepts, general principle in the financial activities of the entity.

Financial management is generally concerned with regular and adequate supply of fund in the

enterprises. It may cover the

financial aspects such as capital requirement, source of fund, investment fund, management of

cash and financial control over the enterprises. In the subject of financial management some of

the basic concepts includes that is defined in this report. For the better understanding of the

financial function in the business, report includes earning per share and right issue concept foer

brand plc and investment appraisal techniques of a food manufacturing company lovewell Ltd.

This report of the financial management is beneficial for the management of the particular

companies in the decision making process regarding company's earning or net profit and how

much amount cost to the company for issue price. And business can make decision regarding the

investment proposal that will be benefited for the organisation lovewell Ltd. So they can make

decision which option is best for organisation as well as increase the profitability in present

situation.

MAIN BODY

Question 2 Right issue

Right issue:

Right issue is basically share that are provided by the company to existing shareholder to

the company. It is also called as right offer. In the basic terms, it is defined as when a enterprises

require some additional capital in the business than it goes to present shareholder for the purpose

to issue the share at discount price for these existing shareholders. It is invitation to stakeholders

to purchase the share in the company at certain discount on market price (Cummins and Derrig,

2012). These are some benefit of the right issue that are discussed as below:

The main benefit to the shareholder is shares are issued at less price so they can purchsed

it on discount or minimum price from market rate.

All the benefit are the same that is given on ordinary share such as dividend, bonus share.

1

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Particular company can save the fund regarding the extra cost on issuing the share like

underwriters commission, promotional cost and other issue cost.

Share are issued to those stakeholder who are the holder of the share in prior allotment of

share so control of the company are in the hands of shareholder.

There are some types of Right issue that are discussed as under:

Renounce able right issue: The existing shareholder have right to transfer the particular

right share to anyone who may or may not a shareholder of the company.

Non- Renounce able right issue: For the existing shareholder, they does not have the right

to transfer the opted shares to anyone. But they have two option, either they skip this

right option or they purchase it for value maximization or divided purpose.

Limitation of the right issue:

Right issue is offer to existing shareholder in specific condition of the company like if

company may not have sufficient fund or resources in the business or they fails to find it

objectives in the particular year (Feng and et. al, 2016).

The value of shares may get cut so it wants to enlarge number of share that issued prior.

For the reputed company, it is going to create negative impact in market that company

has not adequate fund and it is troubled to operate the business function smoothly.

This concept of right issue will defiantly help in understanding the solution of particle problem

that is discussed in the report as follows:

Basic information that are provided by brand plc regarding this question:

Profit after tax (PAT) = 15 percent of share holders funds

ordinary shares of 50p each = 200000 £(i.e. 4000 shares of 50 pound each)

Reserves = 400000£

600000£

Amount that is required to raise the increase the fund thorough right share = £160000

Current ex-dividend market price of brand plc = £ 1.90

Rights issues prices recommended by the finance director = £1.80, £1.60 and £1.40

2

underwriters commission, promotional cost and other issue cost.

Share are issued to those stakeholder who are the holder of the share in prior allotment of

share so control of the company are in the hands of shareholder.

There are some types of Right issue that are discussed as under:

Renounce able right issue: The existing shareholder have right to transfer the particular

right share to anyone who may or may not a shareholder of the company.

Non- Renounce able right issue: For the existing shareholder, they does not have the right

to transfer the opted shares to anyone. But they have two option, either they skip this

right option or they purchase it for value maximization or divided purpose.

Limitation of the right issue:

Right issue is offer to existing shareholder in specific condition of the company like if

company may not have sufficient fund or resources in the business or they fails to find it

objectives in the particular year (Feng and et. al, 2016).

The value of shares may get cut so it wants to enlarge number of share that issued prior.

For the reputed company, it is going to create negative impact in market that company

has not adequate fund and it is troubled to operate the business function smoothly.

This concept of right issue will defiantly help in understanding the solution of particle problem

that is discussed in the report as follows:

Basic information that are provided by brand plc regarding this question:

Profit after tax (PAT) = 15 percent of share holders funds

ordinary shares of 50p each = 200000 £(i.e. 4000 shares of 50 pound each)

Reserves = 400000£

600000£

Amount that is required to raise the increase the fund thorough right share = £160000

Current ex-dividend market price of brand plc = £ 1.90

Rights issues prices recommended by the finance director = £1.80, £1.60 and £1.40

2

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

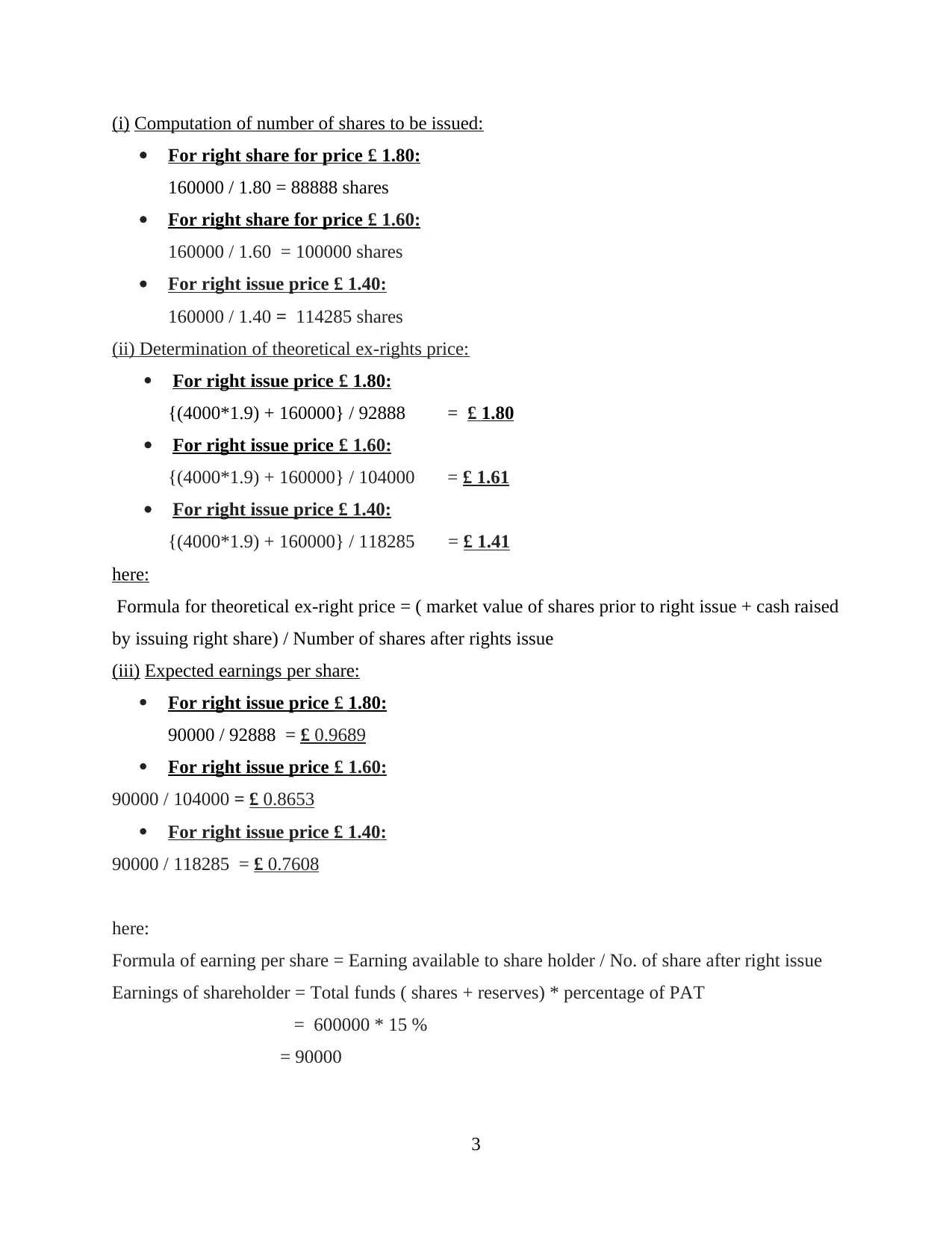

(i) Computation of number of shares to be issued:

For right share for price £ 1.80:

160000 / 1.80 = 88888 shares

For right share for price £ 1.60:

160000 / 1.60 = 100000 shares

For right issue price £ 1.40:

160000 / 1.40 = 114285 shares

(ii) Determination of theoretical ex-rights price:

For right issue price £ 1.80:

{(4000*1.9) + 160000} / 92888 = £ 1.80

For right issue price £ 1.60:

{(4000*1.9) + 160000} / 104000 = £ 1.61

For right issue price £ 1.40:

{(4000*1.9) + 160000} / 118285 = £ 1.41

here:

Formula for theoretical ex-right price = ( market value of shares prior to right issue + cash raised

by issuing right share) / Number of shares after rights issue

(iii) Expected earnings per share:

For right issue price £ 1.80:

90000 / 92888 = £ 0.9689

For right issue price £ 1.60:

90000 / 104000 = £ 0.8653

For right issue price £ 1.40:

90000 / 118285 = £ 0.7608

here:

Formula of earning per share = Earning available to share holder / No. of share after right issue

Earnings of shareholder = Total funds ( shares + reserves) * percentage of PAT

= 600000 * 15 %

= 90000

3

For right share for price £ 1.80:

160000 / 1.80 = 88888 shares

For right share for price £ 1.60:

160000 / 1.60 = 100000 shares

For right issue price £ 1.40:

160000 / 1.40 = 114285 shares

(ii) Determination of theoretical ex-rights price:

For right issue price £ 1.80:

{(4000*1.9) + 160000} / 92888 = £ 1.80

For right issue price £ 1.60:

{(4000*1.9) + 160000} / 104000 = £ 1.61

For right issue price £ 1.40:

{(4000*1.9) + 160000} / 118285 = £ 1.41

here:

Formula for theoretical ex-right price = ( market value of shares prior to right issue + cash raised

by issuing right share) / Number of shares after rights issue

(iii) Expected earnings per share:

For right issue price £ 1.80:

90000 / 92888 = £ 0.9689

For right issue price £ 1.60:

90000 / 104000 = £ 0.8653

For right issue price £ 1.40:

90000 / 118285 = £ 0.7608

here:

Formula of earning per share = Earning available to share holder / No. of share after right issue

Earnings of shareholder = Total funds ( shares + reserves) * percentage of PAT

= 600000 * 15 %

= 90000

3

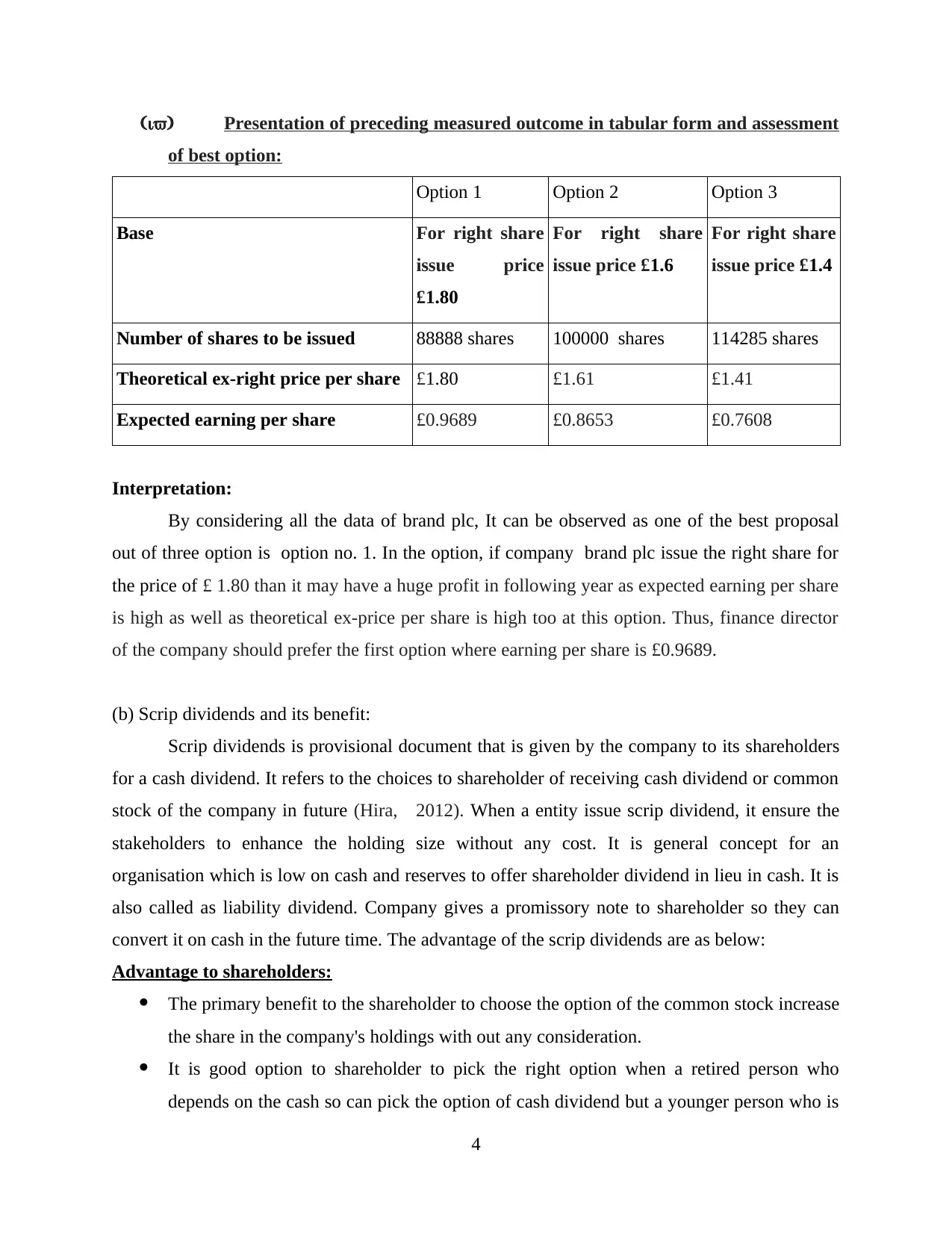

(iv) Presentation of preceding measured outcome in tabular form and assessment

of best option:

Option 1 Option 2 Option 3

Base For right share

issue price

£1.80

For right share

issue price £1.6

For right share

issue price £1.4

Number of shares to be issued 88888 shares 100000 shares 114285 shares

Theoretical ex-right price per share £1.80 £1.61 £1.41

Expected earning per share £0.9689 £0.8653 £0.7608

Interpretation:

By considering all the data of brand plc, It can be observed as one of the best proposal

out of three option is option no. 1. In the option, if company brand plc issue the right share for

the price of £ 1.80 than it may have a huge profit in following year as expected earning per share

is high as well as theoretical ex-price per share is high too at this option. Thus, finance director

of the company should prefer the first option where earning per share is £0.9689.

(b) Scrip dividends and its benefit:

Scrip dividends is provisional document that is given by the company to its shareholders

for a cash dividend. It refers to the choices to shareholder of receiving cash dividend or common

stock of the company in future (Hira, 2012). When a entity issue scrip dividend, it ensure the

stakeholders to enhance the holding size without any cost. It is general concept for an

organisation which is low on cash and reserves to offer shareholder dividend in lieu in cash. It is

also called as liability dividend. Company gives a promissory note to shareholder so they can

convert it on cash in the future time. The advantage of the scrip dividends are as below:

Advantage to shareholders:

The primary benefit to the shareholder to choose the option of the common stock increase

the share in the company's holdings with out any consideration.

It is good option to shareholder to pick the right option when a retired person who

depends on the cash so can pick the option of cash dividend but a younger person who is

4

of best option:

Option 1 Option 2 Option 3

Base For right share

issue price

£1.80

For right share

issue price £1.6

For right share

issue price £1.4

Number of shares to be issued 88888 shares 100000 shares 114285 shares

Theoretical ex-right price per share £1.80 £1.61 £1.41

Expected earning per share £0.9689 £0.8653 £0.7608

Interpretation:

By considering all the data of brand plc, It can be observed as one of the best proposal

out of three option is option no. 1. In the option, if company brand plc issue the right share for

the price of £ 1.80 than it may have a huge profit in following year as expected earning per share

is high as well as theoretical ex-price per share is high too at this option. Thus, finance director

of the company should prefer the first option where earning per share is £0.9689.

(b) Scrip dividends and its benefit:

Scrip dividends is provisional document that is given by the company to its shareholders

for a cash dividend. It refers to the choices to shareholder of receiving cash dividend or common

stock of the company in future (Hira, 2012). When a entity issue scrip dividend, it ensure the

stakeholders to enhance the holding size without any cost. It is general concept for an

organisation which is low on cash and reserves to offer shareholder dividend in lieu in cash. It is

also called as liability dividend. Company gives a promissory note to shareholder so they can

convert it on cash in the future time. The advantage of the scrip dividends are as below:

Advantage to shareholders:

The primary benefit to the shareholder to choose the option of the common stock increase

the share in the company's holdings with out any consideration.

It is good option to shareholder to pick the right option when a retired person who

depends on the cash so can pick the option of cash dividend but a younger person who is

4

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

in job services , can pick the common stock option to increase the wealth in holding

company.

It is beneficial to shareholder to earn dividend income which is provide tax benefit in

total in come.

Shareholder would like to accept the option of scrip dividend when company's share price

is under rated.

Investor can elected this option of dividend as they won't have to pay the any transaction

cost to receive it.

Benefit to company:

The basic benefit to company is do not spend the money on cash when people the

common stock option in the company.

It will help in smooth flow of operational function of the company as this method is

diversify the monetary fund in the company as opting the stock option by the

shareholders (Iatridis and Dimitras, 2013).

It may increase the long term financing abilities in the business by reducing the owners

capital.

Following are the disadvantage of scrip dividends:

It increases the cash payment system of the company due to increment in the dividend per

share.

It is negative impact on the company earning by opting the cash dividend by the

shareholders.

Scrip dividend is become pessimistic theory in corporate that company is suffering from

the problem of out of cash.

This dividend option is not for the organisation which does not wants to issue further

share capital in the market and not to raise the share capital but due to cash payment issue

it need to pay the scrip dividend.

5

company.

It is beneficial to shareholder to earn dividend income which is provide tax benefit in

total in come.

Shareholder would like to accept the option of scrip dividend when company's share price

is under rated.

Investor can elected this option of dividend as they won't have to pay the any transaction

cost to receive it.

Benefit to company:

The basic benefit to company is do not spend the money on cash when people the

common stock option in the company.

It will help in smooth flow of operational function of the company as this method is

diversify the monetary fund in the company as opting the stock option by the

shareholders (Iatridis and Dimitras, 2013).

It may increase the long term financing abilities in the business by reducing the owners

capital.

Following are the disadvantage of scrip dividends:

It increases the cash payment system of the company due to increment in the dividend per

share.

It is negative impact on the company earning by opting the cash dividend by the

shareholders.

Scrip dividend is become pessimistic theory in corporate that company is suffering from

the problem of out of cash.

This dividend option is not for the organisation which does not wants to issue further

share capital in the market and not to raise the share capital but due to cash payment issue

it need to pay the scrip dividend.

5

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Question 3 Investment appraisal techniques.

(1) Finding of economic feasible project by applying different kind of investment appraisal

techniques:

For the enterprises, there are different kind of investment project available, out of those

company needs to select the best one which is beneficial in future for revenue generation

(Karampinis and Hevas, 2013). The management of the business organisation needs to analyse

the business condition and choose the best possible option that will enhance the capacity and

productivity of the organisation. The detailed discussion of the investment project which help in

solving the practical question mention in this report:

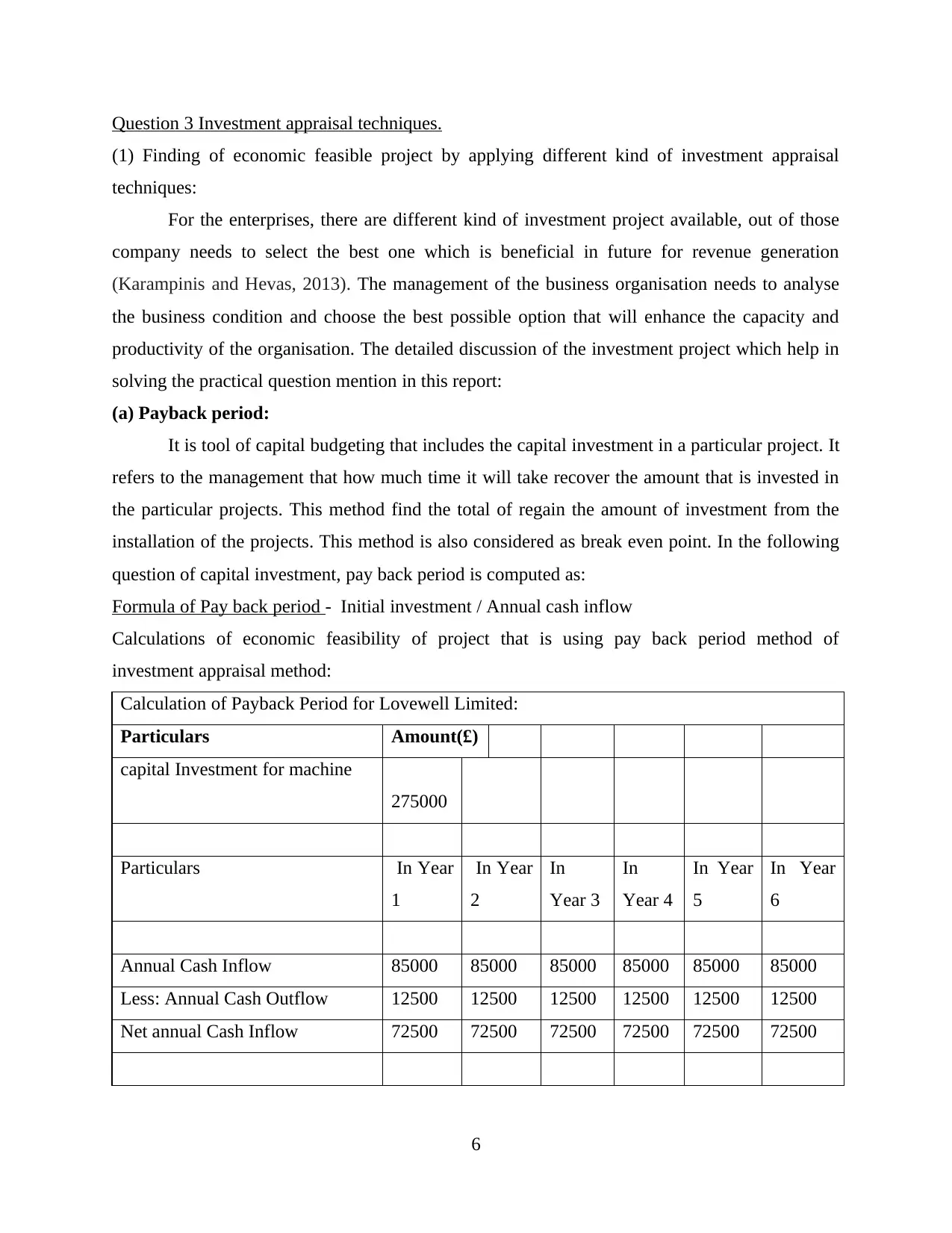

(a) Payback period:

It is tool of capital budgeting that includes the capital investment in a particular project. It

refers to the management that how much time it will take recover the amount that is invested in

the particular projects. This method find the total of regain the amount of investment from the

installation of the projects. This method is also considered as break even point. In the following

question of capital investment, pay back period is computed as:

Formula of Pay back period - Initial investment / Annual cash inflow

Calculations of economic feasibility of project that is using pay back period method of

investment appraisal method:

Calculation of Payback Period for Lovewell Limited:

Particulars Amount(£)

capital Investment for machine

275000

Particulars In Year

1

In Year

2

In

Year 3

In

Year 4

In Year

5

In Year

6

Annual Cash Inflow 85000 85000 85000 85000 85000 85000

Less: Annual Cash Outflow 12500 12500 12500 12500 12500 12500

Net annual Cash Inflow 72500 72500 72500 72500 72500 72500

6

(1) Finding of economic feasible project by applying different kind of investment appraisal

techniques:

For the enterprises, there are different kind of investment project available, out of those

company needs to select the best one which is beneficial in future for revenue generation

(Karampinis and Hevas, 2013). The management of the business organisation needs to analyse

the business condition and choose the best possible option that will enhance the capacity and

productivity of the organisation. The detailed discussion of the investment project which help in

solving the practical question mention in this report:

(a) Payback period:

It is tool of capital budgeting that includes the capital investment in a particular project. It

refers to the management that how much time it will take recover the amount that is invested in

the particular projects. This method find the total of regain the amount of investment from the

installation of the projects. This method is also considered as break even point. In the following

question of capital investment, pay back period is computed as:

Formula of Pay back period - Initial investment / Annual cash inflow

Calculations of economic feasibility of project that is using pay back period method of

investment appraisal method:

Calculation of Payback Period for Lovewell Limited:

Particulars Amount(£)

capital Investment for machine

275000

Particulars In Year

1

In Year

2

In

Year 3

In

Year 4

In Year

5

In Year

6

Annual Cash Inflow 85000 85000 85000 85000 85000 85000

Less: Annual Cash Outflow 12500 12500 12500 12500 12500 12500

Net annual Cash Inflow 72500 72500 72500 72500 72500 72500

6

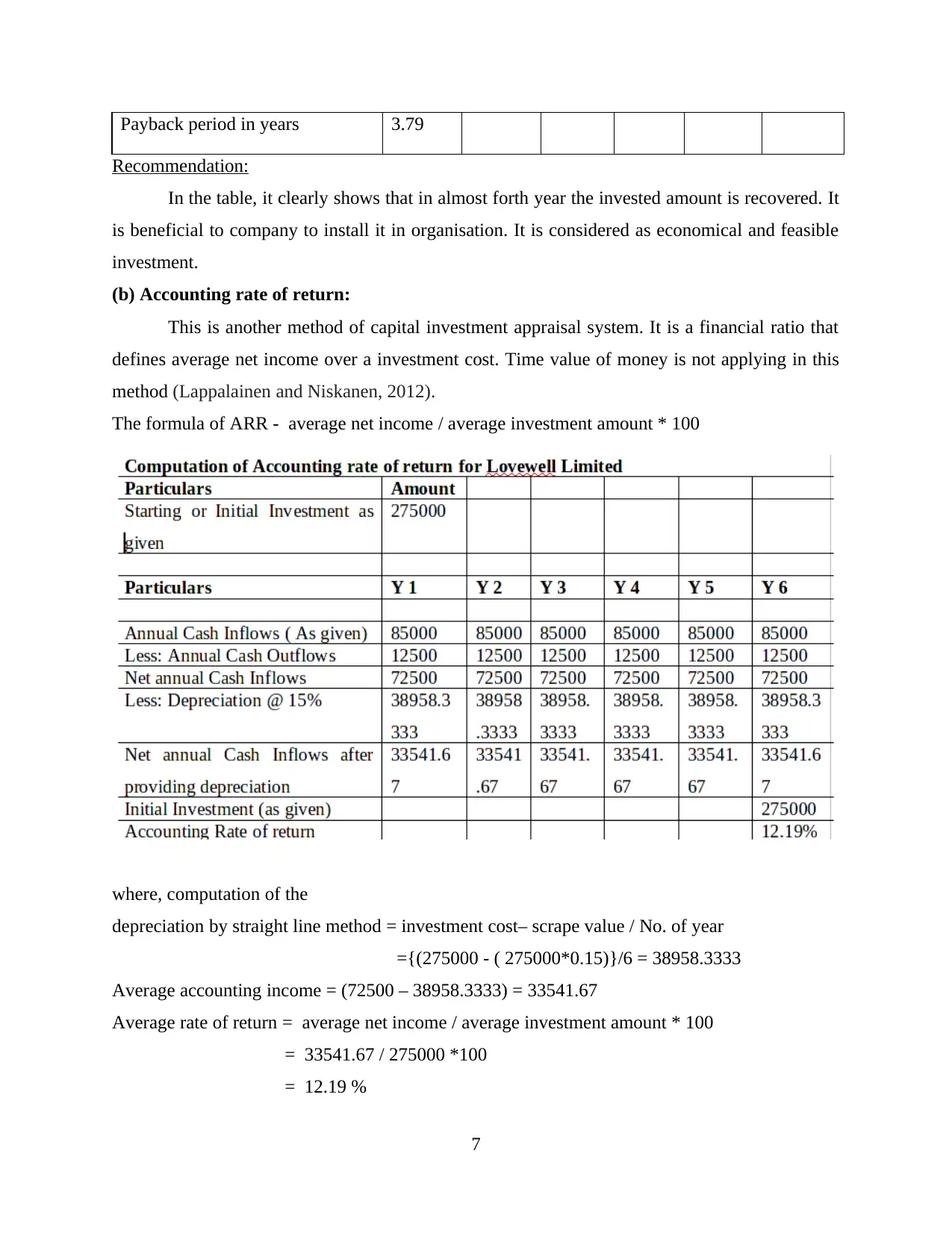

Payback period in years 3.79

Recommendation:

In the table, it clearly shows that in almost forth year the invested amount is recovered. It

is beneficial to company to install it in organisation. It is considered as economical and feasible

investment.

(b) Accounting rate of return:

This is another method of capital investment appraisal system. It is a financial ratio that

defines average net income over a investment cost. Time value of money is not applying in this

method (Lappalainen and Niskanen, 2012).

The formula of ARR - average net income / average investment amount * 100

where, computation of the

depreciation by straight line method = investment cost– scrape value / No. of year

={(275000 - ( 275000*0.15)}/6 = 38958.3333

Average accounting income = (72500 – 38958.3333) = 33541.67

Average rate of return = average net income / average investment amount * 100

= 33541.67 / 275000 *100

= 12.19 %

7

Recommendation:

In the table, it clearly shows that in almost forth year the invested amount is recovered. It

is beneficial to company to install it in organisation. It is considered as economical and feasible

investment.

(b) Accounting rate of return:

This is another method of capital investment appraisal system. It is a financial ratio that

defines average net income over a investment cost. Time value of money is not applying in this

method (Lappalainen and Niskanen, 2012).

The formula of ARR - average net income / average investment amount * 100

where, computation of the

depreciation by straight line method = investment cost– scrape value / No. of year

={(275000 - ( 275000*0.15)}/6 = 38958.3333

Average accounting income = (72500 – 38958.3333) = 33541.67

Average rate of return = average net income / average investment amount * 100

= 33541.67 / 275000 *100

= 12.19 %

7

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Recommendation:

After calculating the ARR it is determined that it is feasible and beneficial for company

to spend in it. Machine should be acquired by the lovewell limited.

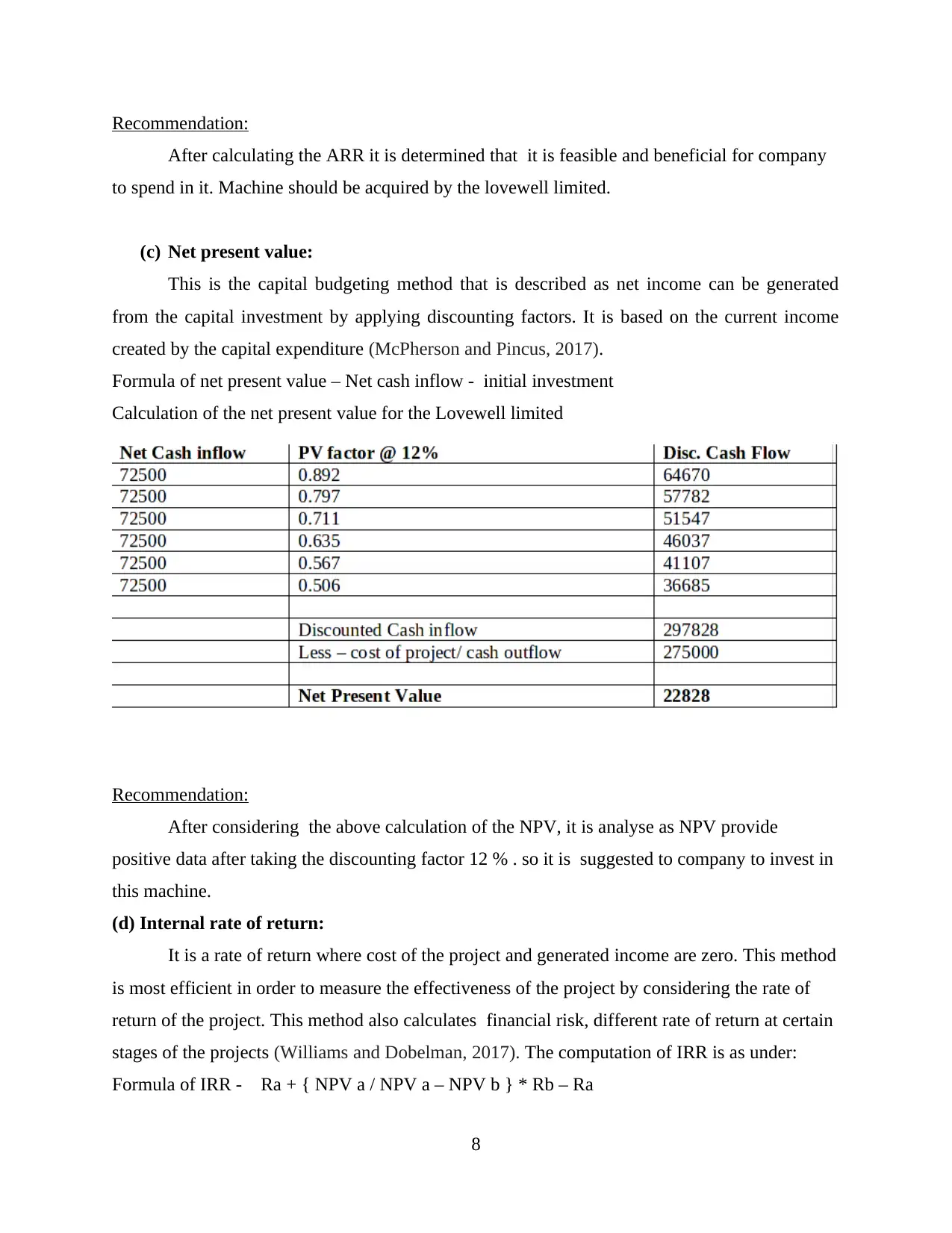

(c) Net present value:

This is the capital budgeting method that is described as net income can be generated

from the capital investment by applying discounting factors. It is based on the current income

created by the capital expenditure (McPherson and Pincus, 2017).

Formula of net present value – Net cash inflow - initial investment

Calculation of the net present value for the Lovewell limited

Recommendation:

After considering the above calculation of the NPV, it is analyse as NPV provide

positive data after taking the discounting factor 12 % . so it is suggested to company to invest in

this machine.

(d) Internal rate of return:

It is a rate of return where cost of the project and generated income are zero. This method

is most efficient in order to measure the effectiveness of the project by considering the rate of

return of the project. This method also calculates financial risk, different rate of return at certain

stages of the projects (Williams and Dobelman, 2017). The computation of IRR is as under:

Formula of IRR - Ra + { NPV a / NPV a – NPV b } * Rb – Ra

8

After calculating the ARR it is determined that it is feasible and beneficial for company

to spend in it. Machine should be acquired by the lovewell limited.

(c) Net present value:

This is the capital budgeting method that is described as net income can be generated

from the capital investment by applying discounting factors. It is based on the current income

created by the capital expenditure (McPherson and Pincus, 2017).

Formula of net present value – Net cash inflow - initial investment

Calculation of the net present value for the Lovewell limited

Recommendation:

After considering the above calculation of the NPV, it is analyse as NPV provide

positive data after taking the discounting factor 12 % . so it is suggested to company to invest in

this machine.

(d) Internal rate of return:

It is a rate of return where cost of the project and generated income are zero. This method

is most efficient in order to measure the effectiveness of the project by considering the rate of

return of the project. This method also calculates financial risk, different rate of return at certain

stages of the projects (Williams and Dobelman, 2017). The computation of IRR is as under:

Formula of IRR - Ra + { NPV a / NPV a – NPV b } * Rb – Ra

8

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

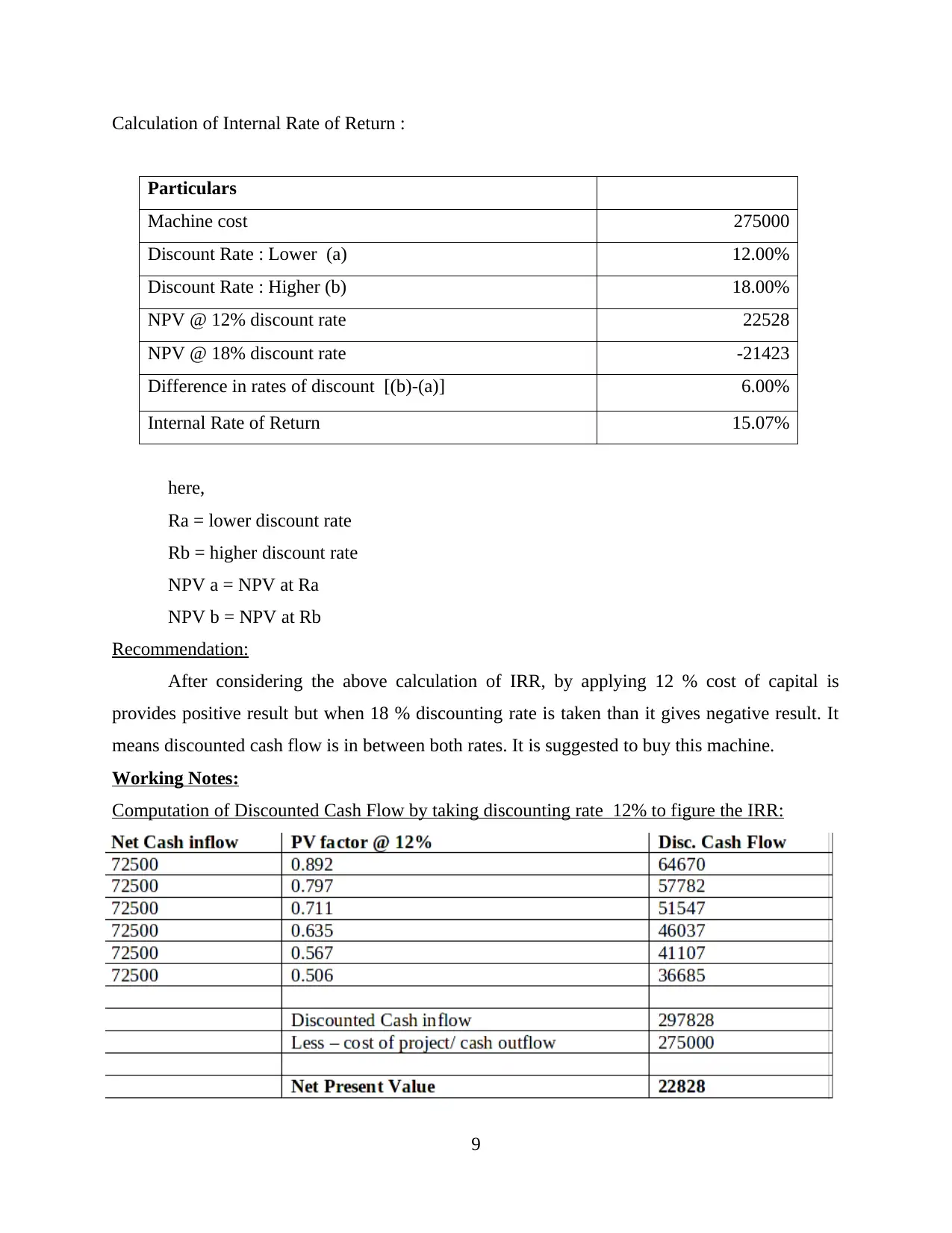

Calculation of Internal Rate of Return :

Particulars

Machine cost 275000

Discount Rate : Lower (a) 12.00%

Discount Rate : Higher (b) 18.00%

NPV @ 12% discount rate 22528

NPV @ 18% discount rate -21423

Difference in rates of discount [(b)-(a)] 6.00%

Internal Rate of Return 15.07%

here,

Ra = lower discount rate

Rb = higher discount rate

NPV a = NPV at Ra

NPV b = NPV at Rb

Recommendation:

After considering the above calculation of IRR, by applying 12 % cost of capital is

provides positive result but when 18 % discounting rate is taken than it gives negative result. It

means discounted cash flow is in between both rates. It is suggested to buy this machine.

Working Notes:

Computation of Discounted Cash Flow by taking discounting rate 12% to figure the IRR:

9

Particulars

Machine cost 275000

Discount Rate : Lower (a) 12.00%

Discount Rate : Higher (b) 18.00%

NPV @ 12% discount rate 22528

NPV @ 18% discount rate -21423

Difference in rates of discount [(b)-(a)] 6.00%

Internal Rate of Return 15.07%

here,

Ra = lower discount rate

Rb = higher discount rate

NPV a = NPV at Ra

NPV b = NPV at Rb

Recommendation:

After considering the above calculation of IRR, by applying 12 % cost of capital is

provides positive result but when 18 % discounting rate is taken than it gives negative result. It

means discounted cash flow is in between both rates. It is suggested to buy this machine.

Working Notes:

Computation of Discounted Cash Flow by taking discounting rate 12% to figure the IRR:

9

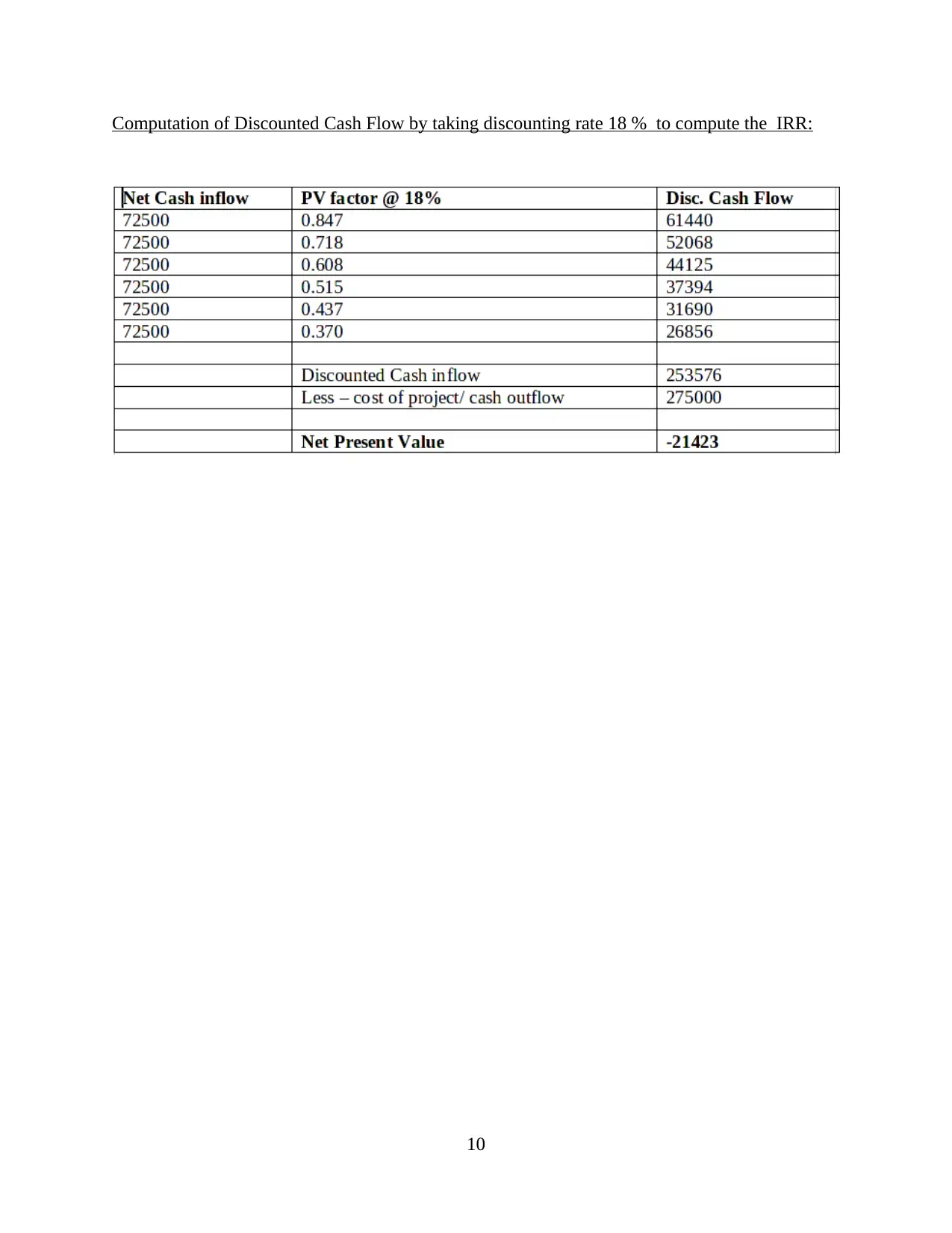

Computation of Discounted Cash Flow by taking discounting rate 18 % to compute the IRR:

10

10

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 16

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.