M522 Finance & Risk Management: Stock Analysis of LG & Samsung

VerifiedAdded on 2023/06/04

|19

|4671

|283

Report

AI Summary

This report provides a detailed financial and risk management analysis of LG and Samsung stocks, covering key financial ratios such as current ratio, quick ratio, return on assets, return on equity, debt-equity ratio, and price-to-equity ratio. It includes calculations of log returns, arithmetic average returns, standard deviations (risk), correlations, systematic risk (beta), cost of equity, portfolio return, and portfolio beta. The analysis assesses capital structure choices, firm valuation, the impact of future dividends, and potential undervaluation or overvaluation. The report also examines the relationship between company announcements and share price behavior, culminating in investment recommendations based on the comprehensive financial analysis of both companies. This document is available on Desklib, a platform offering a wide array of study tools and solved assignments for students.

Finance and risk management

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Table of Contents

INTRODUCTION...........................................................................................................................3

MAIN BODY..................................................................................................................................3

1. Ratios.......................................................................................................................................3

2 Log Returns..............................................................................................................................6

3 Arithmetic Average Returns.....................................................................................................9

4 Risk (Std. Deviations) of the Individual Stocks.....................................................................10

5 Correlation between the two Stocks.......................................................................................10

6 Systematic Risk (betas- the slope of the regression)..............................................................10

7 Cost of Equity (required rate of return)..................................................................................12

8 Portfolio Return......................................................................................................................12

9 Portfolio Beta..........................................................................................................................12

10 Portfolio Risk........................................................................................................................13

11. Capital Structure Choices and Firm Valuation....................................................................13

12 Stock Prices depend on Future Dividends and Dividend Growth........................................15

13 Undervaluation or Overvaluation.........................................................................................16

14 Relationship between Company Announcements and Share Price Behaviour....................16

15 Recommendations.................................................................................................................17

CONCLUSION..............................................................................................................................17

REFERENCES................................................................................................................................1

INTRODUCTION...........................................................................................................................3

MAIN BODY..................................................................................................................................3

1. Ratios.......................................................................................................................................3

2 Log Returns..............................................................................................................................6

3 Arithmetic Average Returns.....................................................................................................9

4 Risk (Std. Deviations) of the Individual Stocks.....................................................................10

5 Correlation between the two Stocks.......................................................................................10

6 Systematic Risk (betas- the slope of the regression)..............................................................10

7 Cost of Equity (required rate of return)..................................................................................12

8 Portfolio Return......................................................................................................................12

9 Portfolio Beta..........................................................................................................................12

10 Portfolio Risk........................................................................................................................13

11. Capital Structure Choices and Firm Valuation....................................................................13

12 Stock Prices depend on Future Dividends and Dividend Growth........................................15

13 Undervaluation or Overvaluation.........................................................................................16

14 Relationship between Company Announcements and Share Price Behaviour....................16

15 Recommendations.................................................................................................................17

CONCLUSION..............................................................................................................................17

REFERENCES................................................................................................................................1

INTRODUCTION

Management of finances and risk involved in the process of investing in certain

stocks is referred to as financial and risk management. It involves monitoring returns, risks, beta

values and other financial factors to base the investing decision. Therefore, the following report

which involves analysis of two stocks i.e., LG and Samsung includes such process of financial

and risk management. For the analysis of the finance and risk management the organizations

selected by Samsung Electronics and LG Electronics.

MAIN BODY

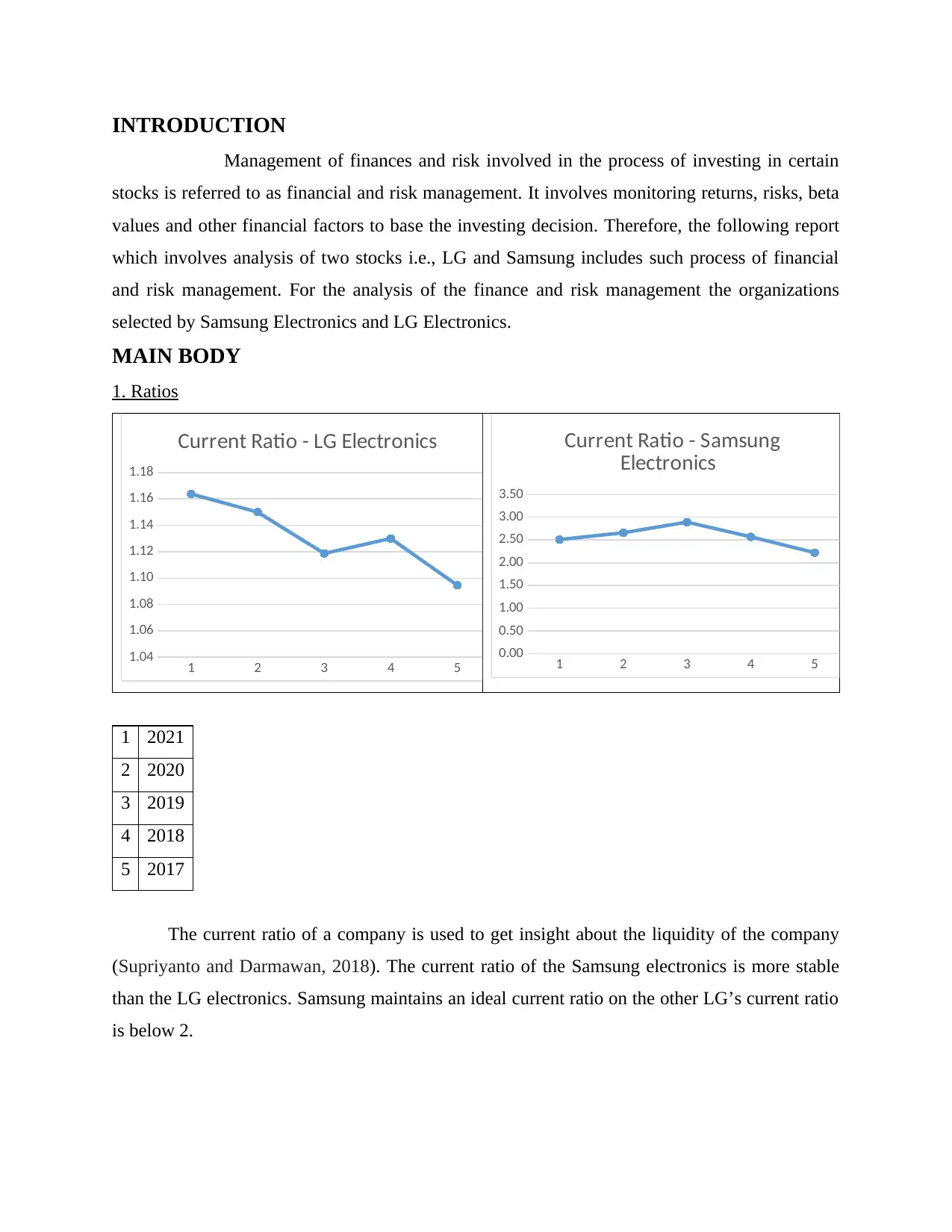

1. Ratios

1 2 3 4 5

1.04

1.06

1.08

1.10

1.12

1.14

1.16

1.18

Current Ratio - LG Electronics

1 2 3 4 5

0.00

0.50

1.00

1.50

2.00

2.50

3.00

3.50

Current Ratio - Samsung

Electronics

1 2021

2 2020

3 2019

4 2018

5 2017

The current ratio of a company is used to get insight about the liquidity of the company

(Supriyanto and Darmawan, 2018). The current ratio of the Samsung electronics is more stable

than the LG electronics. Samsung maintains an ideal current ratio on the other LG’s current ratio

is below 2.

Management of finances and risk involved in the process of investing in certain

stocks is referred to as financial and risk management. It involves monitoring returns, risks, beta

values and other financial factors to base the investing decision. Therefore, the following report

which involves analysis of two stocks i.e., LG and Samsung includes such process of financial

and risk management. For the analysis of the finance and risk management the organizations

selected by Samsung Electronics and LG Electronics.

MAIN BODY

1. Ratios

1 2 3 4 5

1.04

1.06

1.08

1.10

1.12

1.14

1.16

1.18

Current Ratio - LG Electronics

1 2 3 4 5

0.00

0.50

1.00

1.50

2.00

2.50

3.00

3.50

Current Ratio - Samsung

Electronics

1 2021

2 2020

3 2019

4 2018

5 2017

The current ratio of a company is used to get insight about the liquidity of the company

(Supriyanto and Darmawan, 2018). The current ratio of the Samsung electronics is more stable

than the LG electronics. Samsung maintains an ideal current ratio on the other LG’s current ratio

is below 2.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 2 3 4 5

0.73

0.74

0.75

0.76

0.77

0.78

0.79

Quick Ratio - LG Electronics

1 2 3 4 5

0.00

0.50

1.00

1.50

2.00

2.50

3.00

Quick Ratio - Samsung

Electronics

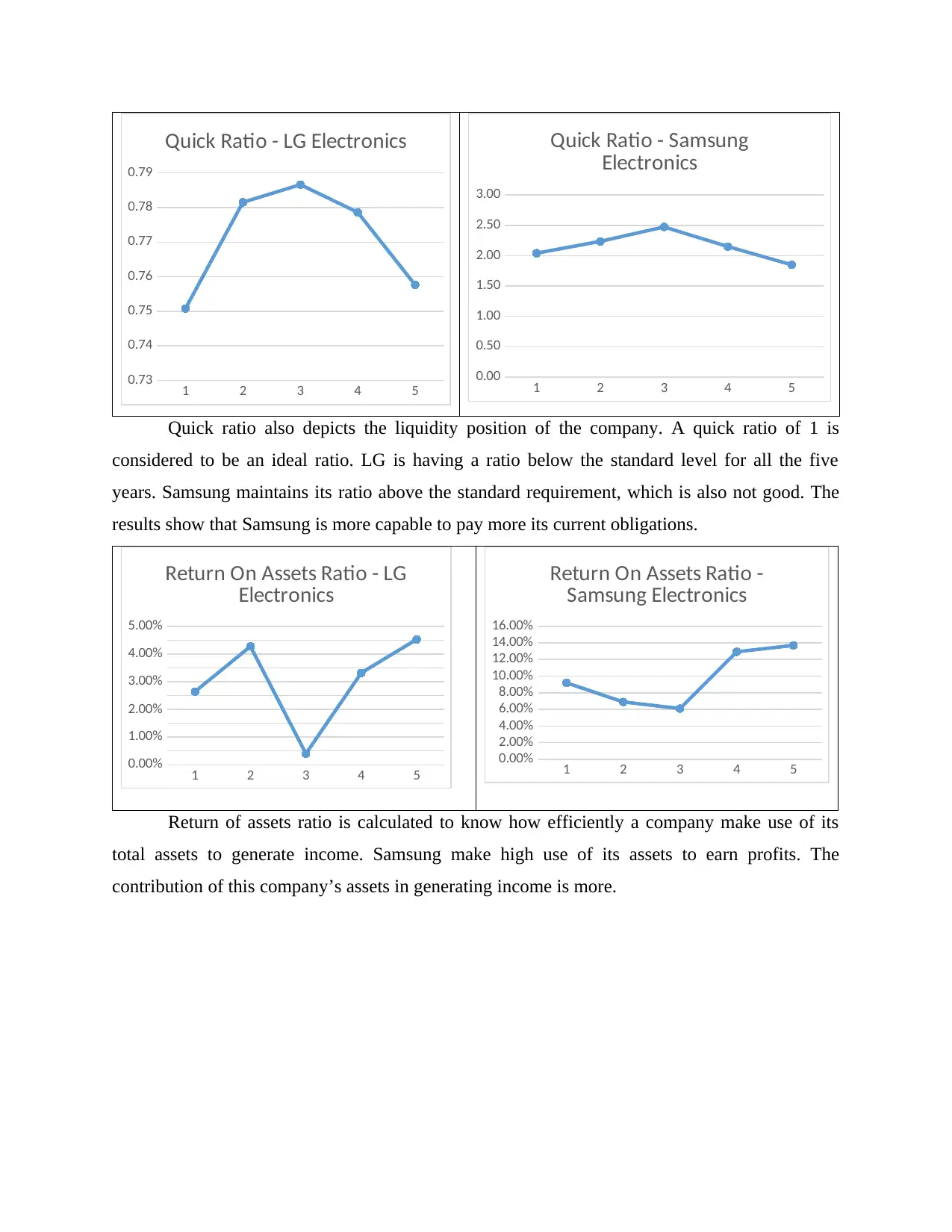

Quick ratio also depicts the liquidity position of the company. A quick ratio of 1 is

considered to be an ideal ratio. LG is having a ratio below the standard level for all the five

years. Samsung maintains its ratio above the standard requirement, which is also not good. The

results show that Samsung is more capable to pay more its current obligations.

1 2 3 4 5

0.00%

1.00%

2.00%

3.00%

4.00%

5.00%

Return On Assets Ratio - LG

Electronics

1 2 3 4 5

0.00%

2.00%

4.00%

6.00%

8.00%

10.00%

12.00%

14.00%

16.00%

Return On Assets Ratio -

Samsung Electronics

Return of assets ratio is calculated to know how efficiently a company make use of its

total assets to generate income. Samsung make high use of its assets to earn profits. The

contribution of this company’s assets in generating income is more.

0.73

0.74

0.75

0.76

0.77

0.78

0.79

Quick Ratio - LG Electronics

1 2 3 4 5

0.00

0.50

1.00

1.50

2.00

2.50

3.00

Quick Ratio - Samsung

Electronics

Quick ratio also depicts the liquidity position of the company. A quick ratio of 1 is

considered to be an ideal ratio. LG is having a ratio below the standard level for all the five

years. Samsung maintains its ratio above the standard requirement, which is also not good. The

results show that Samsung is more capable to pay more its current obligations.

1 2 3 4 5

0.00%

1.00%

2.00%

3.00%

4.00%

5.00%

Return On Assets Ratio - LG

Electronics

1 2 3 4 5

0.00%

2.00%

4.00%

6.00%

8.00%

10.00%

12.00%

14.00%

16.00%

Return On Assets Ratio -

Samsung Electronics

Return of assets ratio is calculated to know how efficiently a company make use of its

total assets to generate income. Samsung make high use of its assets to earn profits. The

contribution of this company’s assets in generating income is more.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

1 2 3 4 5

0.00%

2.00%

4.00%

6.00%

8.00%

10.00%

12.00%

14.00%

Return On Equity Ratio - LG

Electronics

1 2 3 4 5

0.00%

5.00%

10.00%

15.00%

20.00%

25.00%

Return On Equity Ratio -

Samsung Electronics

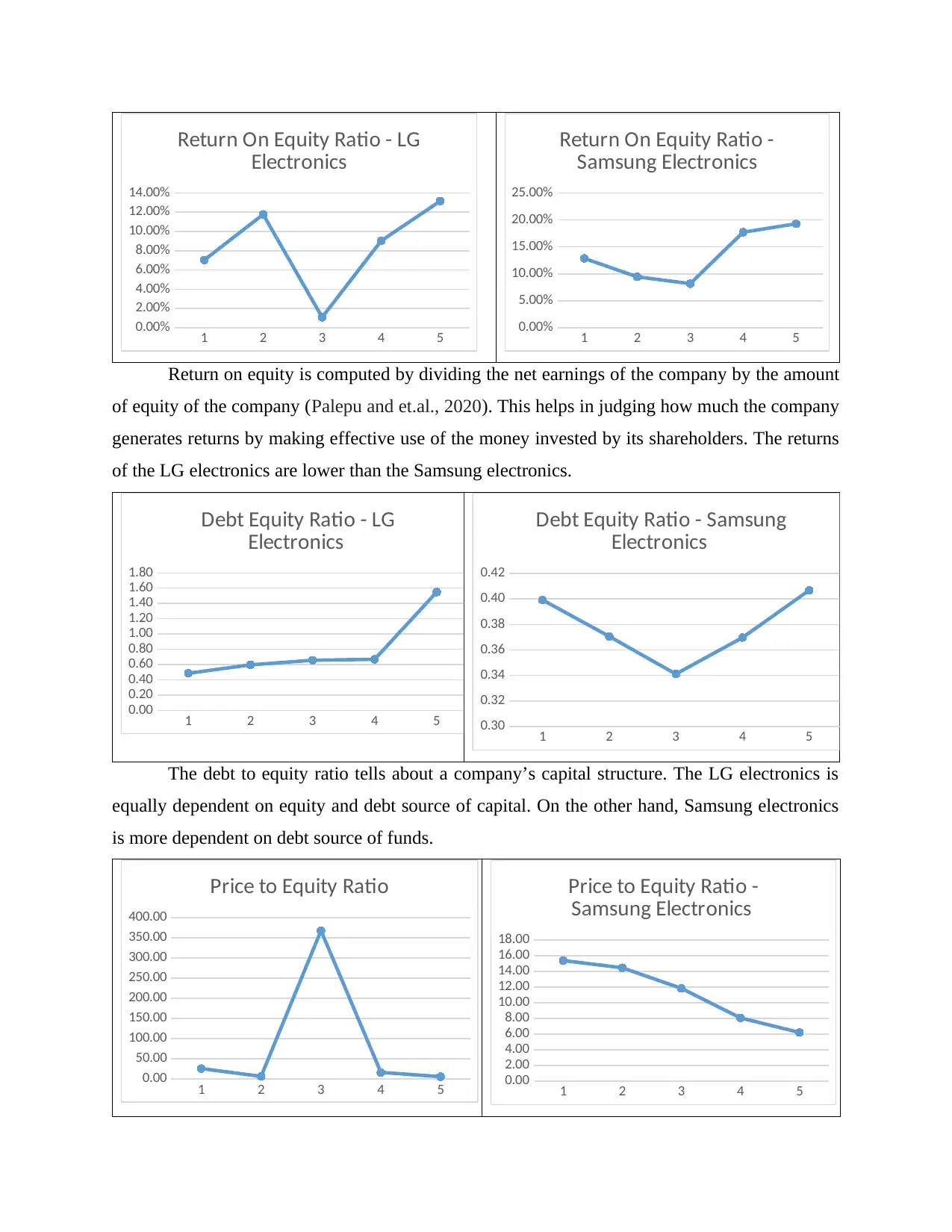

Return on equity is computed by dividing the net earnings of the company by the amount

of equity of the company (Palepu and et.al., 2020). This helps in judging how much the company

generates returns by making effective use of the money invested by its shareholders. The returns

of the LG electronics are lower than the Samsung electronics.

1 2 3 4 5

0.00

0.20

0.40

0.60

0.80

1.00

1.20

1.40

1.60

1.80

Debt Equity Ratio - LG

Electronics

1 2 3 4 5

0.30

0.32

0.34

0.36

0.38

0.40

0.42

Debt Equity Ratio - Samsung

Electronics

The debt to equity ratio tells about a company’s capital structure. The LG electronics is

equally dependent on equity and debt source of capital. On the other hand, Samsung electronics

is more dependent on debt source of funds.

1 2 3 4 5

0.00

50.00

100.00

150.00

200.00

250.00

300.00

350.00

400.00

Price to Equity Ratio

1 2 3 4 5

0.00

2.00

4.00

6.00

8.00

10.00

12.00

14.00

16.00

18.00

Price to Equity Ratio -

Samsung Electronics

0.00%

2.00%

4.00%

6.00%

8.00%

10.00%

12.00%

14.00%

Return On Equity Ratio - LG

Electronics

1 2 3 4 5

0.00%

5.00%

10.00%

15.00%

20.00%

25.00%

Return On Equity Ratio -

Samsung Electronics

Return on equity is computed by dividing the net earnings of the company by the amount

of equity of the company (Palepu and et.al., 2020). This helps in judging how much the company

generates returns by making effective use of the money invested by its shareholders. The returns

of the LG electronics are lower than the Samsung electronics.

1 2 3 4 5

0.00

0.20

0.40

0.60

0.80

1.00

1.20

1.40

1.60

1.80

Debt Equity Ratio - LG

Electronics

1 2 3 4 5

0.30

0.32

0.34

0.36

0.38

0.40

0.42

Debt Equity Ratio - Samsung

Electronics

The debt to equity ratio tells about a company’s capital structure. The LG electronics is

equally dependent on equity and debt source of capital. On the other hand, Samsung electronics

is more dependent on debt source of funds.

1 2 3 4 5

0.00

50.00

100.00

150.00

200.00

250.00

300.00

350.00

400.00

Price to Equity Ratio

1 2 3 4 5

0.00

2.00

4.00

6.00

8.00

10.00

12.00

14.00

16.00

18.00

Price to Equity Ratio -

Samsung Electronics

The price to equity ratio of LG electronics shows that the company is returns are more

fluctuation whereas Samsung Electronics price to equity ratio is gradually rising.

2 Log Returns

LG:

Date Adj Close Log Returns (%)

10/1/2017 15.882865

11/1/2017 15.882865 0.0000

12/1/2017 15.882865 0.0000

1/1/2018 16.071074 -1.1780

2/1/2018 16.071074 0.0000

3/1/2018 16.071074 0.0000

4/1/2018 16.071074 0.0000

5/1/2018 16.071074 0.0000

6/1/2018 16.071074 0.0000

7/1/2018 16.071074 0.0000

8/1/2018 16.071074 0.0000

9/1/2018 16.071074 0.0000

10/1/2018 16.071074 0.0000

11/1/2018 16.071074 0.0000

12/1/2018 16.071074 0.0000

1/1/2019 16.393099 -1.9839

2/1/2019 16.393099 0.0000

3/1/2019 16.393099 0.0000

4/1/2019 16.393099 0.0000

5/1/2019 16.393099 0.0000

6/1/2019 16.393099 0.0000

7/1/2019 11.197355 38.1183

8/1/2019 9.158154 20.1033

9/1/2019 9.158154 0.0000

10/1/2019 9.158154 0.0000

11/1/2019 9.158154 0.0000

12/1/2019 11.172949 -19.8851

1/1/2020 11.288638 -1.0301

2/1/2020 11.288638 0.0000

3/1/2020 11.288638 0.0000

4/1/2020 11.288638 0.0000

5/1/2020 11.288638 0.0000

6/1/2020 11.288638 0.0000

7/1/2020 11.288638 0.0000

8/1/2020 11.288638 0.0000

9/1/2020 11.288638 0.0000

fluctuation whereas Samsung Electronics price to equity ratio is gradually rising.

2 Log Returns

LG:

Date Adj Close Log Returns (%)

10/1/2017 15.882865

11/1/2017 15.882865 0.0000

12/1/2017 15.882865 0.0000

1/1/2018 16.071074 -1.1780

2/1/2018 16.071074 0.0000

3/1/2018 16.071074 0.0000

4/1/2018 16.071074 0.0000

5/1/2018 16.071074 0.0000

6/1/2018 16.071074 0.0000

7/1/2018 16.071074 0.0000

8/1/2018 16.071074 0.0000

9/1/2018 16.071074 0.0000

10/1/2018 16.071074 0.0000

11/1/2018 16.071074 0.0000

12/1/2018 16.071074 0.0000

1/1/2019 16.393099 -1.9839

2/1/2019 16.393099 0.0000

3/1/2019 16.393099 0.0000

4/1/2019 16.393099 0.0000

5/1/2019 16.393099 0.0000

6/1/2019 16.393099 0.0000

7/1/2019 11.197355 38.1183

8/1/2019 9.158154 20.1033

9/1/2019 9.158154 0.0000

10/1/2019 9.158154 0.0000

11/1/2019 9.158154 0.0000

12/1/2019 11.172949 -19.8851

1/1/2020 11.288638 -1.0301

2/1/2020 11.288638 0.0000

3/1/2020 11.288638 0.0000

4/1/2020 11.288638 0.0000

5/1/2020 11.288638 0.0000

6/1/2020 11.288638 0.0000

7/1/2020 11.288638 0.0000

8/1/2020 11.288638 0.0000

9/1/2020 11.288638 0.0000

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

10/1/2020 11.288638 0.0000

11/1/2020 11.288638 0.0000

12/1/2020 11.288638 0.0000

1/1/2021 33.267841 -108.0794

2/1/2021 33.267841 0.0000

3/1/2021 33.267841 0.0000

4/1/2021 33.267841 0.0000

5/1/2021 33.267841 0.0000

6/1/2021 33.267841 0.0000

7/1/2021 33.267841 0.0000

8/1/2021 33.267841 0.0000

9/1/2021 33.267841 0.0000

10/1/2021 33.267841 0.0000

11/1/2021 25.060307 28.3306

12/1/2021 26.638908 -6.1088

1/1/2022 28.200001 -5.6949

2/1/2022 24.799999 12.8478

3/1/2022 24 3.2790

4/1/2022 22.4 6.8993

5/1/2022 21.200001 5.5060

6/1/2022 17 22.0788

7/1/2022 17 0.0000

8/1/2022 17.1 -0.5865

9/1/2022 15.3 11.1226

9/15/2022 15.3 0.0000

Samsung:

Date Adj Close Log Returns (%)

10/1/2017 47691.1563

11/1/2017 43985.3125 8.0890

12/1/2017 44123.8477 -0.3145

1/1/2018 43594.9531 1.2059

2/1/2018 41113.8047 5.8597

3/1/2018 43000.8828 -4.4877

4/1/2018 46642.3047 -8.1287

5/1/2018 44618.207 4.4366

6/1/2018 41054.0234 8.3253

7/1/2018 41004.7305 0.1201

8/1/2018 42955.2305 -4.6471

9/1/2018 41182.0586 4.2156

10/1/2018 37874.2266 8.3732

11/1/2018 37382.9375 1.3056

12/1/2018 34569.168 7.8252

11/1/2020 11.288638 0.0000

12/1/2020 11.288638 0.0000

1/1/2021 33.267841 -108.0794

2/1/2021 33.267841 0.0000

3/1/2021 33.267841 0.0000

4/1/2021 33.267841 0.0000

5/1/2021 33.267841 0.0000

6/1/2021 33.267841 0.0000

7/1/2021 33.267841 0.0000

8/1/2021 33.267841 0.0000

9/1/2021 33.267841 0.0000

10/1/2021 33.267841 0.0000

11/1/2021 25.060307 28.3306

12/1/2021 26.638908 -6.1088

1/1/2022 28.200001 -5.6949

2/1/2022 24.799999 12.8478

3/1/2022 24 3.2790

4/1/2022 22.4 6.8993

5/1/2022 21.200001 5.5060

6/1/2022 17 22.0788

7/1/2022 17 0.0000

8/1/2022 17.1 -0.5865

9/1/2022 15.3 11.1226

9/15/2022 15.3 0.0000

Samsung:

Date Adj Close Log Returns (%)

10/1/2017 47691.1563

11/1/2017 43985.3125 8.0890

12/1/2017 44123.8477 -0.3145

1/1/2018 43594.9531 1.2059

2/1/2018 41113.8047 5.8597

3/1/2018 43000.8828 -4.4877

4/1/2018 46642.3047 -8.1287

5/1/2018 44618.207 4.4366

6/1/2018 41054.0234 8.3253

7/1/2018 41004.7305 0.1201

8/1/2018 42955.2305 -4.6471

9/1/2018 41182.0586 4.2156

10/1/2018 37874.2266 8.3732

11/1/2018 37382.9375 1.3056

12/1/2018 34569.168 7.8252

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

1/1/2019 41608.0234 -18.5331

2/1/2019 40661.3555 2.3015

3/1/2019 40255.6484 1.0028

4/1/2019 41662.7656 -3.4357

5/1/2019 38618.6992 7.5871

6/1/2019 42707.7422 -10.0644

7/1/2019 41530.1289 2.7961

8/1/2019 40293.8438 3.0220

9/1/2019 44918.4727 -10.8650

10/1/2019 46489.2617 -3.4372

11/1/2019 46397.0117 0.1986

12/1/2019 51470.2539 -10.3769

1/1/2020 52358.2656 -1.7106

2/1/2020 50315.9141 3.9788

3/1/2020 44328.1406 12.6702

4/1/2020 46759.6055 -5.3400

5/1/2020 47414.2461 -1.3903

6/1/2020 49378.1367 -4.0585

7/1/2020 54509.6563 -9.8870

8/1/2020 50838.0156 6.9733

9/1/2020 54792.0938 -7.4901

10/1/2020 53613.5703 2.1744

11/1/2020 63180.6602 -16.4196

12/1/2020 76726.1406 -19.4244

1/1/2021 79628.1563 -3.7125

2/1/2021 80113.6953 -0.6079

3/1/2021 79045.5234 1.3423

4/1/2021 79494.3125 -0.5662

5/1/2021 78518.9219 1.2346

6/1/2021 78714 -0.2481

7/1/2021 76907.1328 2.3222

8/1/2021 75143.6563 2.3197

9/1/2021 72596.4141 3.4486

10/1/2021 68708.75 5.5039

11/1/2021 70185.2969 -2.1262

12/1/2021 77075.8594 -9.3651

1/1/2022 72479.875 6.1481

2/1/2022 71095.5391 1.9284

3/1/2022 68821.2656 3.2512

4/1/2022 66990.375 2.6964

5/1/2022 66990.375 0.0000

6/1/2022 56653.5859 16.7594

7/1/2022 61400 -8.0455

2/1/2019 40661.3555 2.3015

3/1/2019 40255.6484 1.0028

4/1/2019 41662.7656 -3.4357

5/1/2019 38618.6992 7.5871

6/1/2019 42707.7422 -10.0644

7/1/2019 41530.1289 2.7961

8/1/2019 40293.8438 3.0220

9/1/2019 44918.4727 -10.8650

10/1/2019 46489.2617 -3.4372

11/1/2019 46397.0117 0.1986

12/1/2019 51470.2539 -10.3769

1/1/2020 52358.2656 -1.7106

2/1/2020 50315.9141 3.9788

3/1/2020 44328.1406 12.6702

4/1/2020 46759.6055 -5.3400

5/1/2020 47414.2461 -1.3903

6/1/2020 49378.1367 -4.0585

7/1/2020 54509.6563 -9.8870

8/1/2020 50838.0156 6.9733

9/1/2020 54792.0938 -7.4901

10/1/2020 53613.5703 2.1744

11/1/2020 63180.6602 -16.4196

12/1/2020 76726.1406 -19.4244

1/1/2021 79628.1563 -3.7125

2/1/2021 80113.6953 -0.6079

3/1/2021 79045.5234 1.3423

4/1/2021 79494.3125 -0.5662

5/1/2021 78518.9219 1.2346

6/1/2021 78714 -0.2481

7/1/2021 76907.1328 2.3222

8/1/2021 75143.6563 2.3197

9/1/2021 72596.4141 3.4486

10/1/2021 68708.75 5.5039

11/1/2021 70185.2969 -2.1262

12/1/2021 77075.8594 -9.3651

1/1/2022 72479.875 6.1481

2/1/2022 71095.5391 1.9284

3/1/2022 68821.2656 3.2512

4/1/2022 66990.375 2.6964

5/1/2022 66990.375 0.0000

6/1/2022 56653.5859 16.7594

7/1/2022 61400 -8.0455

8/1/2022 59700 2.8078

9/1/2022 55300 7.6559

9/22/2022 54400 1.6409

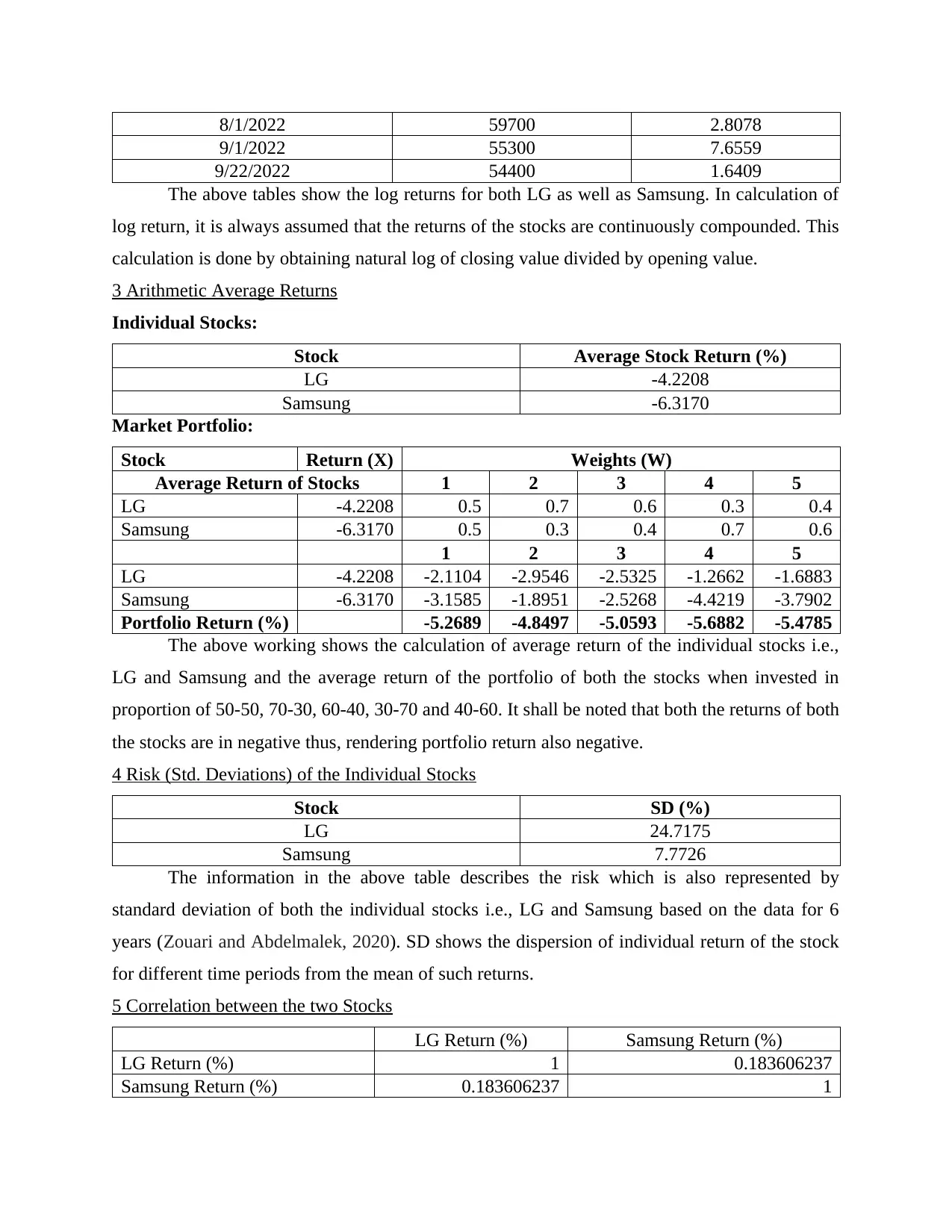

The above tables show the log returns for both LG as well as Samsung. In calculation of

log return, it is always assumed that the returns of the stocks are continuously compounded. This

calculation is done by obtaining natural log of closing value divided by opening value.

3 Arithmetic Average Returns

Individual Stocks:

Stock Average Stock Return (%)

LG -4.2208

Samsung -6.3170

Market Portfolio:

Stock Return (X) Weights (W)

Average Return of Stocks 1 2 3 4 5

LG -4.2208 0.5 0.7 0.6 0.3 0.4

Samsung -6.3170 0.5 0.3 0.4 0.7 0.6

1 2 3 4 5

LG -4.2208 -2.1104 -2.9546 -2.5325 -1.2662 -1.6883

Samsung -6.3170 -3.1585 -1.8951 -2.5268 -4.4219 -3.7902

Portfolio Return (%) -5.2689 -4.8497 -5.0593 -5.6882 -5.4785

The above working shows the calculation of average return of the individual stocks i.e.,

LG and Samsung and the average return of the portfolio of both the stocks when invested in

proportion of 50-50, 70-30, 60-40, 30-70 and 40-60. It shall be noted that both the returns of both

the stocks are in negative thus, rendering portfolio return also negative.

4 Risk (Std. Deviations) of the Individual Stocks

Stock SD (%)

LG 24.7175

Samsung 7.7726

The information in the above table describes the risk which is also represented by

standard deviation of both the individual stocks i.e., LG and Samsung based on the data for 6

years (Zouari and Abdelmalek, 2020). SD shows the dispersion of individual return of the stock

for different time periods from the mean of such returns.

5 Correlation between the two Stocks

LG Return (%) Samsung Return (%)

LG Return (%) 1 0.183606237

Samsung Return (%) 0.183606237 1

9/1/2022 55300 7.6559

9/22/2022 54400 1.6409

The above tables show the log returns for both LG as well as Samsung. In calculation of

log return, it is always assumed that the returns of the stocks are continuously compounded. This

calculation is done by obtaining natural log of closing value divided by opening value.

3 Arithmetic Average Returns

Individual Stocks:

Stock Average Stock Return (%)

LG -4.2208

Samsung -6.3170

Market Portfolio:

Stock Return (X) Weights (W)

Average Return of Stocks 1 2 3 4 5

LG -4.2208 0.5 0.7 0.6 0.3 0.4

Samsung -6.3170 0.5 0.3 0.4 0.7 0.6

1 2 3 4 5

LG -4.2208 -2.1104 -2.9546 -2.5325 -1.2662 -1.6883

Samsung -6.3170 -3.1585 -1.8951 -2.5268 -4.4219 -3.7902

Portfolio Return (%) -5.2689 -4.8497 -5.0593 -5.6882 -5.4785

The above working shows the calculation of average return of the individual stocks i.e.,

LG and Samsung and the average return of the portfolio of both the stocks when invested in

proportion of 50-50, 70-30, 60-40, 30-70 and 40-60. It shall be noted that both the returns of both

the stocks are in negative thus, rendering portfolio return also negative.

4 Risk (Std. Deviations) of the Individual Stocks

Stock SD (%)

LG 24.7175

Samsung 7.7726

The information in the above table describes the risk which is also represented by

standard deviation of both the individual stocks i.e., LG and Samsung based on the data for 6

years (Zouari and Abdelmalek, 2020). SD shows the dispersion of individual return of the stock

for different time periods from the mean of such returns.

5 Correlation between the two Stocks

LG Return (%) Samsung Return (%)

LG Return (%) 1 0.183606237

Samsung Return (%) 0.183606237 1

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

The above data represent the correlation between the two stocks namely LG and

Samsung. The value of correlation i.e., 0.1836 shows the presence of positive weak correlation

i.e., both the stocks are very slightly correlated and that too positively (Breitenstein, Nguyen and

Walther, 2021). This means that the stock prices of both the stock will move in the same

direction.

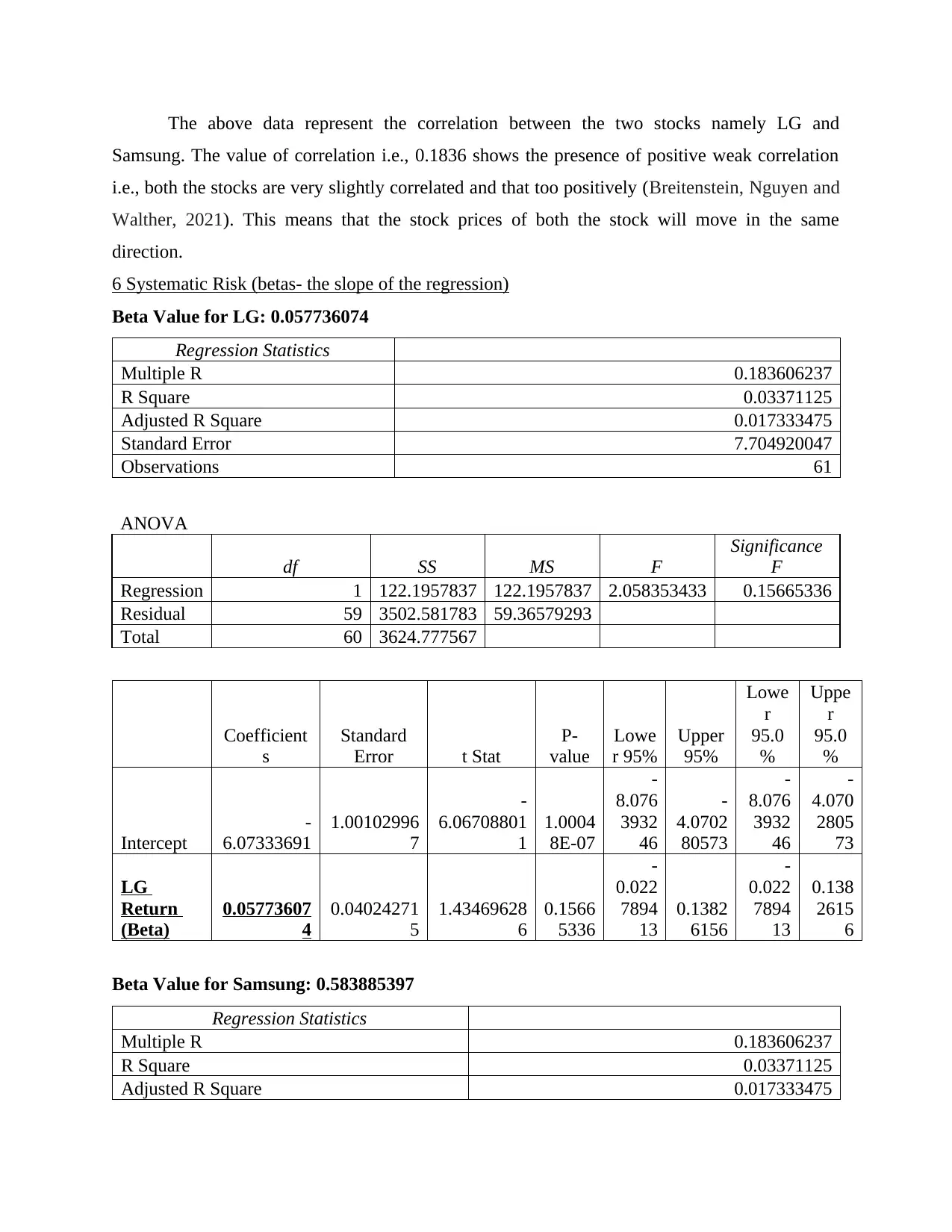

6 Systematic Risk (betas- the slope of the regression)

Beta Value for LG: 0.057736074

Regression Statistics

Multiple R 0.183606237

R Square 0.03371125

Adjusted R Square 0.017333475

Standard Error 7.704920047

Observations 61

ANOVA

df SS MS F

Significance

F

Regression 1 122.1957837 122.1957837 2.058353433 0.15665336

Residual 59 3502.581783 59.36579293

Total 60 3624.777567

Coefficient

s

Standard

Error t Stat

P-

value

Lowe

r 95%

Upper

95%

Lowe

r

95.0

%

Uppe

r

95.0

%

Intercept

-

6.07333691

1.00102996

7

-

6.06708801

1

1.0004

8E-07

-

8.076

3932

46

-

4.0702

80573

-

8.076

3932

46

-

4.070

2805

73

LG

Return

(Beta)

0.05773607

4

0.04024271

5

1.43469628

6

0.1566

5336

-

0.022

7894

13

0.1382

6156

-

0.022

7894

13

0.138

2615

6

Beta Value for Samsung: 0.583885397

Regression Statistics

Multiple R 0.183606237

R Square 0.03371125

Adjusted R Square 0.017333475

Samsung. The value of correlation i.e., 0.1836 shows the presence of positive weak correlation

i.e., both the stocks are very slightly correlated and that too positively (Breitenstein, Nguyen and

Walther, 2021). This means that the stock prices of both the stock will move in the same

direction.

6 Systematic Risk (betas- the slope of the regression)

Beta Value for LG: 0.057736074

Regression Statistics

Multiple R 0.183606237

R Square 0.03371125

Adjusted R Square 0.017333475

Standard Error 7.704920047

Observations 61

ANOVA

df SS MS F

Significance

F

Regression 1 122.1957837 122.1957837 2.058353433 0.15665336

Residual 59 3502.581783 59.36579293

Total 60 3624.777567

Coefficient

s

Standard

Error t Stat

P-

value

Lowe

r 95%

Upper

95%

Lowe

r

95.0

%

Uppe

r

95.0

%

Intercept

-

6.07333691

1.00102996

7

-

6.06708801

1

1.0004

8E-07

-

8.076

3932

46

-

4.0702

80573

-

8.076

3932

46

-

4.070

2805

73

LG

Return

(Beta)

0.05773607

4

0.04024271

5

1.43469628

6

0.1566

5336

-

0.022

7894

13

0.1382

6156

-

0.022

7894

13

0.138

2615

6

Beta Value for Samsung: 0.583885397

Regression Statistics

Multiple R 0.183606237

R Square 0.03371125

Adjusted R Square 0.017333475

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Standard Error 24.50238279

Observations 61

ANOVA

df SS MS F

Significance

F

Regression 1 1235.766986 1235.766986 2.058353433 0.15665336

Residual 59 35421.63899 600.3667625

Total 60 36657.40598

Coefficients

Standard

Error

t

Stat P-value

Lower

95%

Upper

95%

Lower

95.0%

Upper

95.0%

Intercept -0.532383075

4.056040

414

-

0.13

1256

847

0.89601

8684

-

8.6485

01197

7.5837

35047

-

8.64850

1197

7.5837

35047

Samsung

Return

(Beta) 0.583885397

0.406974

914

1.43

4696

286

0.15665

336

-

0.2304

69524

1.3982

40318

-

0.23046

9524

1.3982

40318

The above tabular representation shows the values of systematic risk of both the stocks of

LG and Samsung which is 0.0577 and 0.5839 respectively. The intercept of regression of LG and

Samsung is -6.0733 and -0.5323 respectively (Mishchenko and et.al., 2021). The value of R

Square of both the stocks is 0.0337 which shows that change in one stock will lead to same

directional chance in the other stock by 3.37%.

7 Cost of Equity (required rate of return)

LG Samsung

Particulars Figures Figures

Rf (Risk free rate) 1.86% 1.86%

Beta 0.0577 0.5839

Rm (market return) -0.0422 -0.0632

CAPM = Rf + Beta (Rm - Rf) 1.5% -2.9%

The cost of capital is impacted by the market risk via the equity funding costs. Cost of

equity is most often calculated by the formula of Capital Asset Pricing Model (Mashrur and

et.al., 2020). Accurate estimation of cost of equity will assist entities in minimization of such

cost of equity and keep the investors satisfied regarding handling the risks involved in such

returns.

Observations 61

ANOVA

df SS MS F

Significance

F

Regression 1 1235.766986 1235.766986 2.058353433 0.15665336

Residual 59 35421.63899 600.3667625

Total 60 36657.40598

Coefficients

Standard

Error

t

Stat P-value

Lower

95%

Upper

95%

Lower

95.0%

Upper

95.0%

Intercept -0.532383075

4.056040

414

-

0.13

1256

847

0.89601

8684

-

8.6485

01197

7.5837

35047

-

8.64850

1197

7.5837

35047

Samsung

Return

(Beta) 0.583885397

0.406974

914

1.43

4696

286

0.15665

336

-

0.2304

69524

1.3982

40318

-

0.23046

9524

1.3982

40318

The above tabular representation shows the values of systematic risk of both the stocks of

LG and Samsung which is 0.0577 and 0.5839 respectively. The intercept of regression of LG and

Samsung is -6.0733 and -0.5323 respectively (Mishchenko and et.al., 2021). The value of R

Square of both the stocks is 0.0337 which shows that change in one stock will lead to same

directional chance in the other stock by 3.37%.

7 Cost of Equity (required rate of return)

LG Samsung

Particulars Figures Figures

Rf (Risk free rate) 1.86% 1.86%

Beta 0.0577 0.5839

Rm (market return) -0.0422 -0.0632

CAPM = Rf + Beta (Rm - Rf) 1.5% -2.9%

The cost of capital is impacted by the market risk via the equity funding costs. Cost of

equity is most often calculated by the formula of Capital Asset Pricing Model (Mashrur and

et.al., 2020). Accurate estimation of cost of equity will assist entities in minimization of such

cost of equity and keep the investors satisfied regarding handling the risks involved in such

returns.

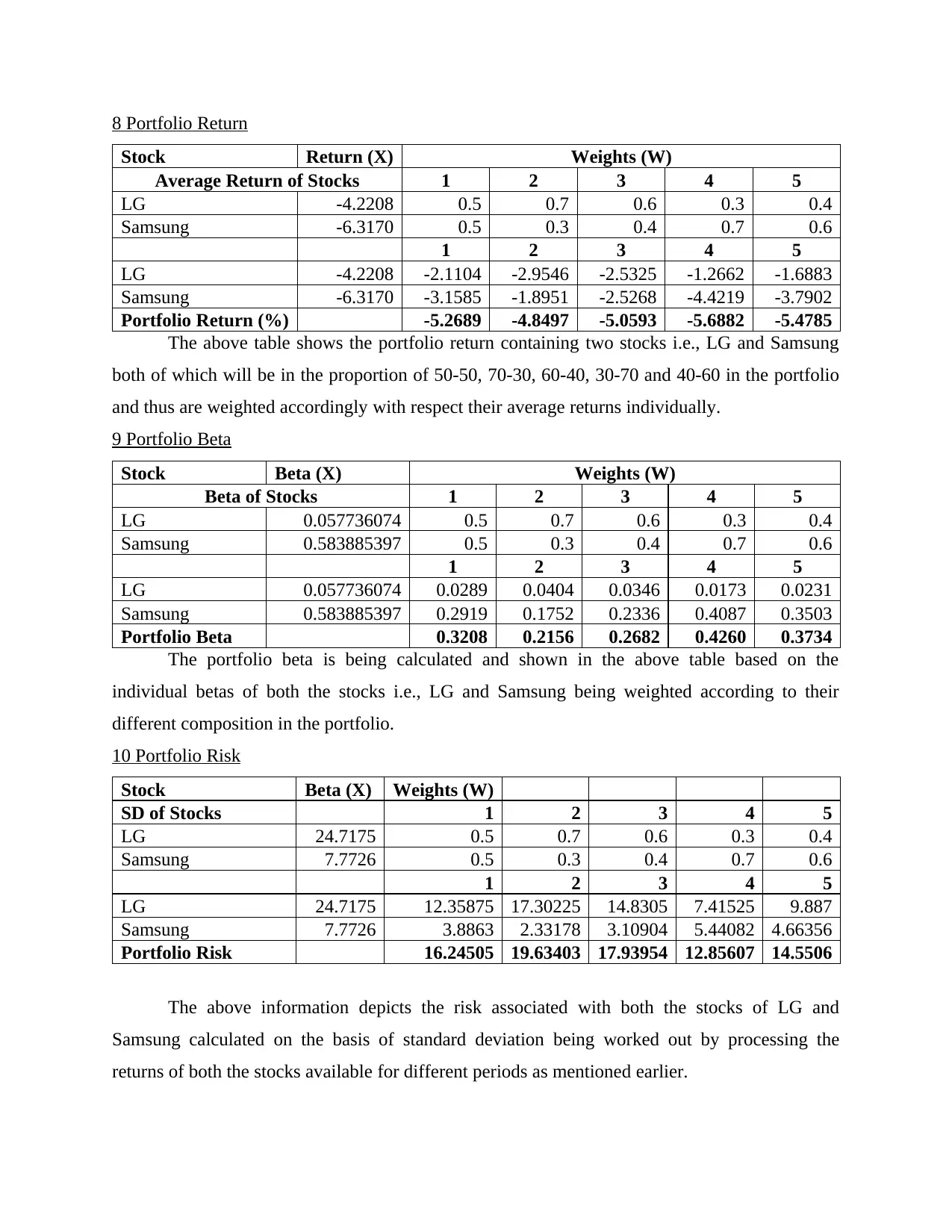

8 Portfolio Return

Stock Return (X) Weights (W)

Average Return of Stocks 1 2 3 4 5

LG -4.2208 0.5 0.7 0.6 0.3 0.4

Samsung -6.3170 0.5 0.3 0.4 0.7 0.6

1 2 3 4 5

LG -4.2208 -2.1104 -2.9546 -2.5325 -1.2662 -1.6883

Samsung -6.3170 -3.1585 -1.8951 -2.5268 -4.4219 -3.7902

Portfolio Return (%) -5.2689 -4.8497 -5.0593 -5.6882 -5.4785

The above table shows the portfolio return containing two stocks i.e., LG and Samsung

both of which will be in the proportion of 50-50, 70-30, 60-40, 30-70 and 40-60 in the portfolio

and thus are weighted accordingly with respect their average returns individually.

9 Portfolio Beta

Stock Beta (X) Weights (W)

Beta of Stocks 1 2 3 4 5

LG 0.057736074 0.5 0.7 0.6 0.3 0.4

Samsung 0.583885397 0.5 0.3 0.4 0.7 0.6

1 2 3 4 5

LG 0.057736074 0.0289 0.0404 0.0346 0.0173 0.0231

Samsung 0.583885397 0.2919 0.1752 0.2336 0.4087 0.3503

Portfolio Beta 0.3208 0.2156 0.2682 0.4260 0.3734

The portfolio beta is being calculated and shown in the above table based on the

individual betas of both the stocks i.e., LG and Samsung being weighted according to their

different composition in the portfolio.

10 Portfolio Risk

Stock Beta (X) Weights (W)

SD of Stocks 1 2 3 4 5

LG 24.7175 0.5 0.7 0.6 0.3 0.4

Samsung 7.7726 0.5 0.3 0.4 0.7 0.6

1 2 3 4 5

LG 24.7175 12.35875 17.30225 14.8305 7.41525 9.887

Samsung 7.7726 3.8863 2.33178 3.10904 5.44082 4.66356

Portfolio Risk 16.24505 19.63403 17.93954 12.85607 14.5506

The above information depicts the risk associated with both the stocks of LG and

Samsung calculated on the basis of standard deviation being worked out by processing the

returns of both the stocks available for different periods as mentioned earlier.

Stock Return (X) Weights (W)

Average Return of Stocks 1 2 3 4 5

LG -4.2208 0.5 0.7 0.6 0.3 0.4

Samsung -6.3170 0.5 0.3 0.4 0.7 0.6

1 2 3 4 5

LG -4.2208 -2.1104 -2.9546 -2.5325 -1.2662 -1.6883

Samsung -6.3170 -3.1585 -1.8951 -2.5268 -4.4219 -3.7902

Portfolio Return (%) -5.2689 -4.8497 -5.0593 -5.6882 -5.4785

The above table shows the portfolio return containing two stocks i.e., LG and Samsung

both of which will be in the proportion of 50-50, 70-30, 60-40, 30-70 and 40-60 in the portfolio

and thus are weighted accordingly with respect their average returns individually.

9 Portfolio Beta

Stock Beta (X) Weights (W)

Beta of Stocks 1 2 3 4 5

LG 0.057736074 0.5 0.7 0.6 0.3 0.4

Samsung 0.583885397 0.5 0.3 0.4 0.7 0.6

1 2 3 4 5

LG 0.057736074 0.0289 0.0404 0.0346 0.0173 0.0231

Samsung 0.583885397 0.2919 0.1752 0.2336 0.4087 0.3503

Portfolio Beta 0.3208 0.2156 0.2682 0.4260 0.3734

The portfolio beta is being calculated and shown in the above table based on the

individual betas of both the stocks i.e., LG and Samsung being weighted according to their

different composition in the portfolio.

10 Portfolio Risk

Stock Beta (X) Weights (W)

SD of Stocks 1 2 3 4 5

LG 24.7175 0.5 0.7 0.6 0.3 0.4

Samsung 7.7726 0.5 0.3 0.4 0.7 0.6

1 2 3 4 5

LG 24.7175 12.35875 17.30225 14.8305 7.41525 9.887

Samsung 7.7726 3.8863 2.33178 3.10904 5.44082 4.66356

Portfolio Risk 16.24505 19.63403 17.93954 12.85607 14.5506

The above information depicts the risk associated with both the stocks of LG and

Samsung calculated on the basis of standard deviation being worked out by processing the

returns of both the stocks available for different periods as mentioned earlier.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 19

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.