Comprehensive Finance Case Study: Risk, Return, and Financing

VerifiedAdded on 2020/04/01

|8

|1161

|279

Case Study

AI Summary

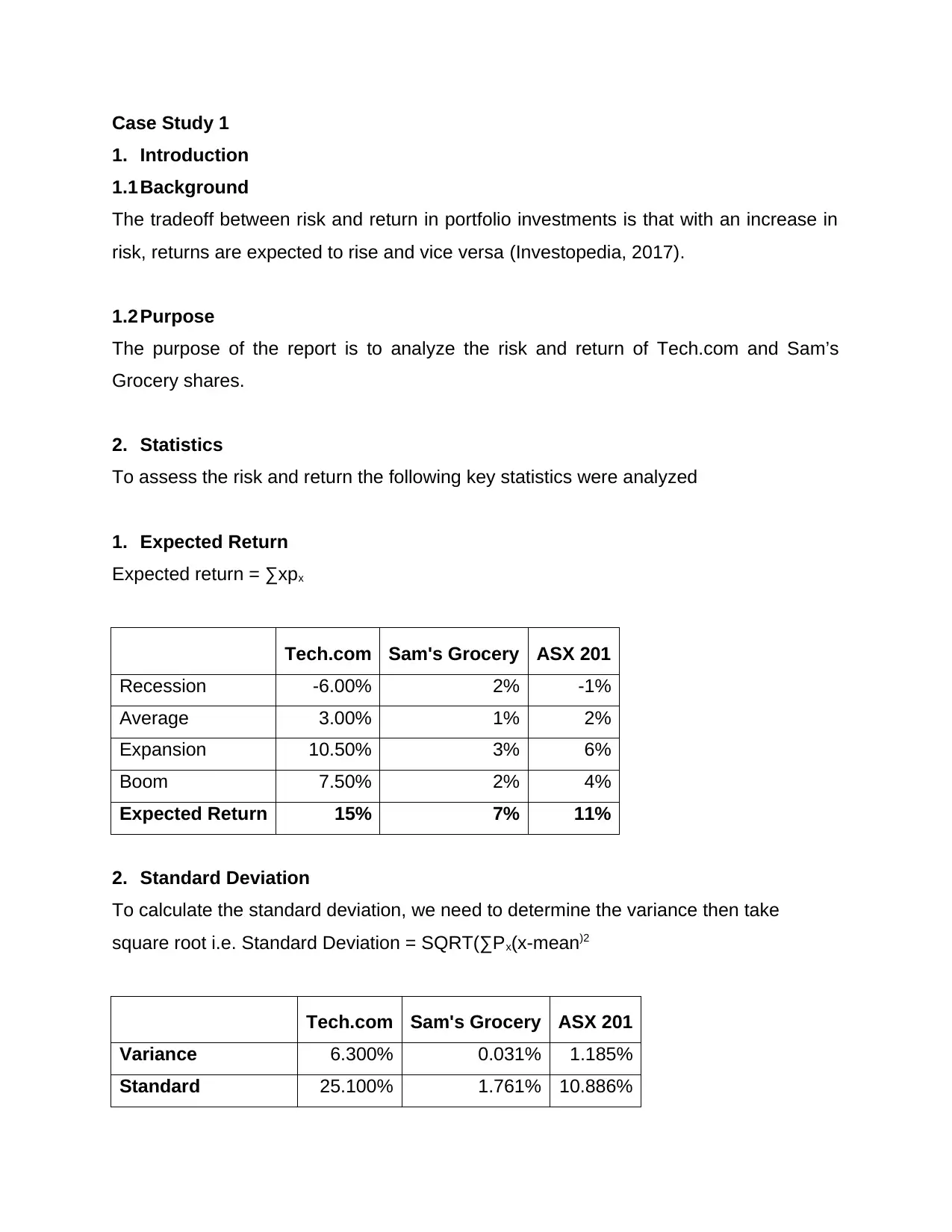

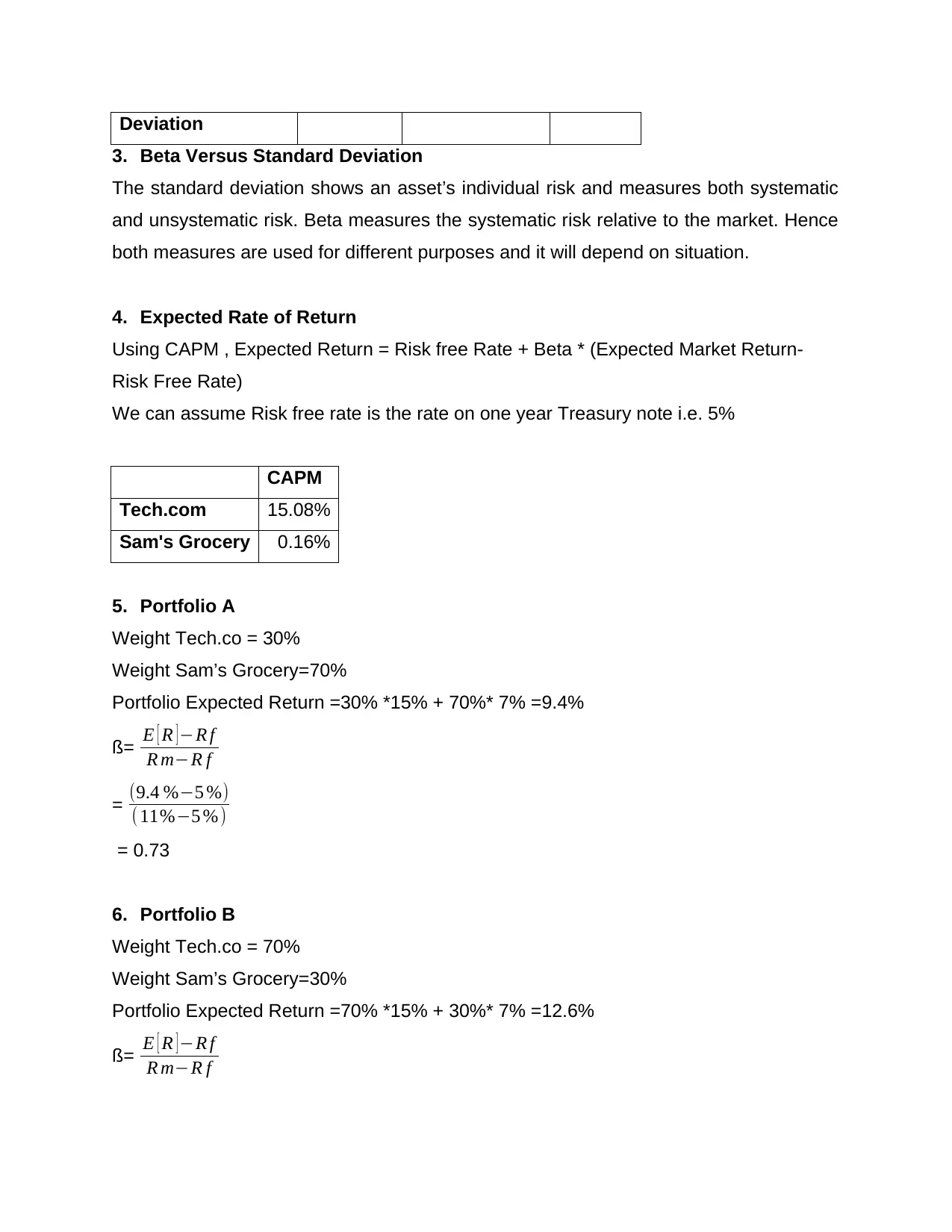

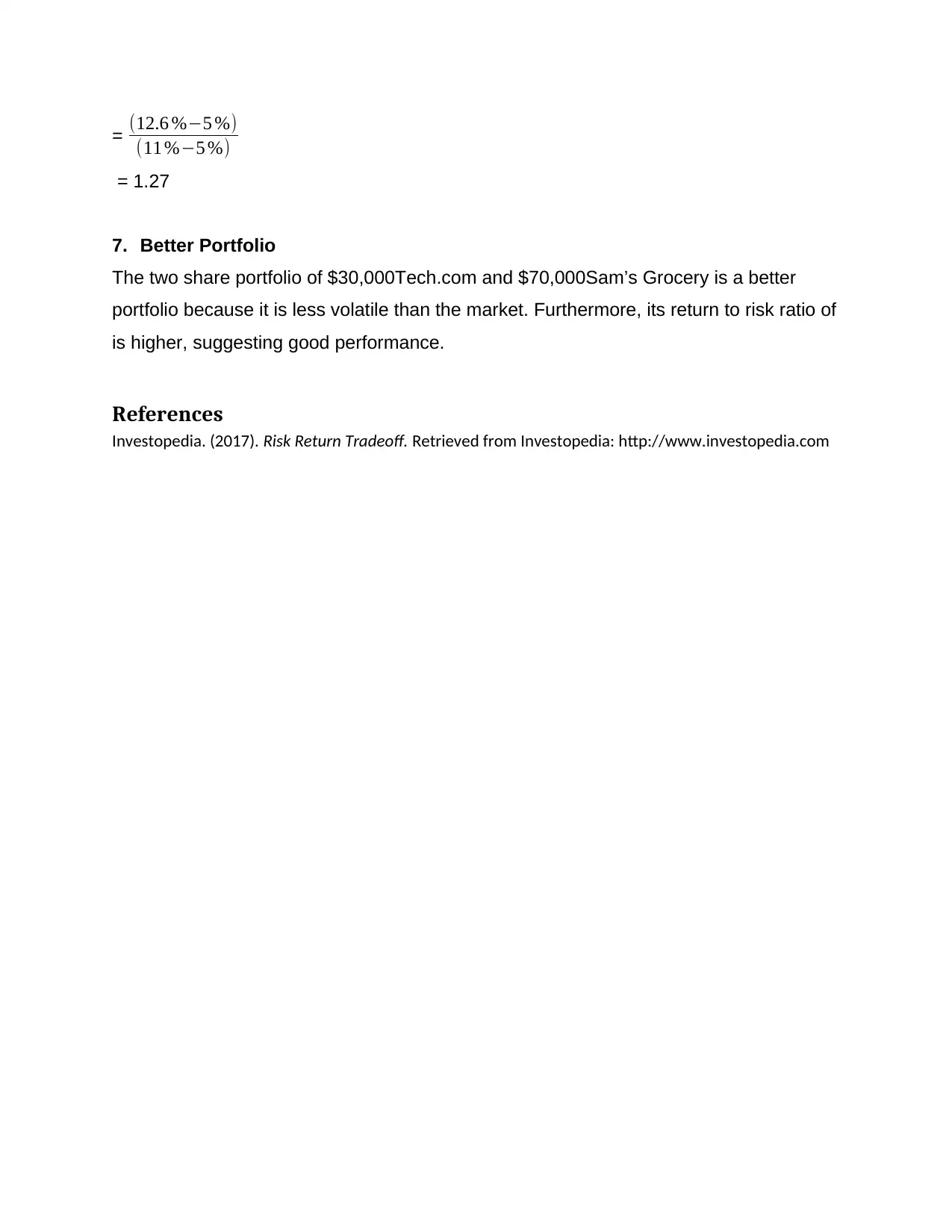

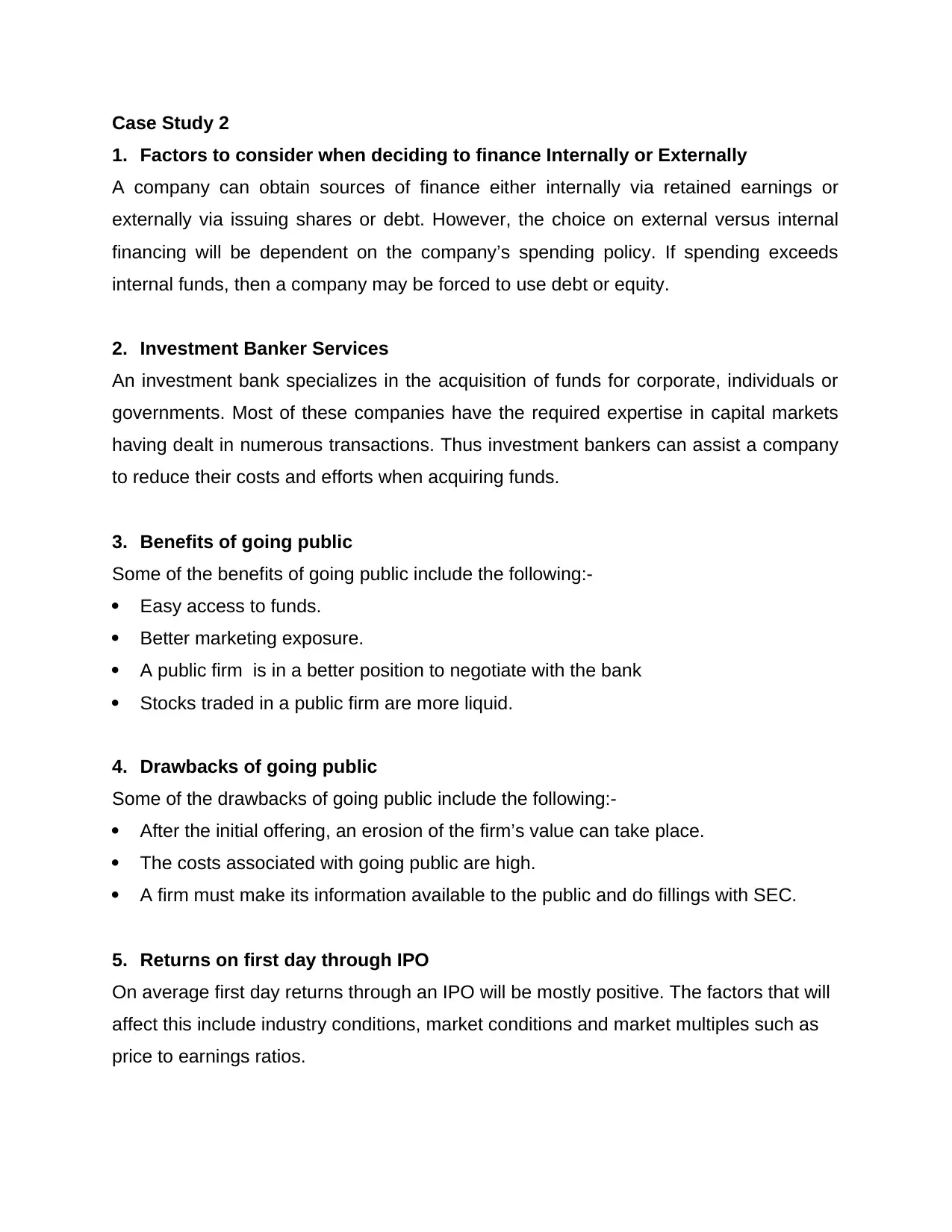

This finance case study examines three distinct scenarios. The first case study analyzes the risk and return of Tech.com and Sam's Grocery shares, calculating expected return, standard deviation, and beta to assess portfolio performance. The second case study explores factors influencing financing decisions, differentiating between internal and external financing, and outlining the benefits and drawbacks of going public, along with an overview of investment banking services. The third case study focuses on loan calculations, determining monthly and quarterly payments, outstanding loan balances, and evaluating the potential benefits of loan refinancing, including a comparison of effective annual rates and the impact of different payment frequencies.

1 out of 8

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.